Examining the 2007-09 Subprime Crisis: Causes & UK Regulatory Changes

VerifiedAdded on 2023/04/21

|15

|7862

|140

Essay

AI Summary

This essay examines the subprime crisis of 2007-2009, focusing on its micro and macro causes as well as the UK's subsequent financial regulation reforms. It begins by outlining the sequence of events in financial crises, highlighting the role of asymmetric information and the impact on financial markets. The analysis covers the global financial imbalances, low real interest rates, consumer inertia, corporate leverage, compensation schemes, and the role of rating agencies. It further details the stages of the crisis, from excessive lending in the US subprime market to the contagion throughout the global economy. The essay also addresses the UK governmental responses, including monetary, fiscal, and stabilization policies, and assesses their effectiveness in ameliorating the impact of the banking crisis. The assignment concludes by emphasizing the importance of understanding the factors that led to the crisis and the measures implemented by the Bank of England.

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/289750481

Crisis periods and contagion effects in the CEE stock markets: the influence of

the 2007 US subprime crisis

Article · January 2016

DOI: 10.1504/IJCEE.2016.075612

CITATIONS

0

READS

53

2 authors:

Some of the authors of this publication are also working on these related projects:

Comparative research on commonality in liquidity on the Central and Eastern European stock markets (NCN, OPUS 11, 2016/21/B/HS4/02004)View project

BST/2017/2018View project

Joanna Olbrys

Bialystok University of Technology

86PUBLICATIONS307CITATIONS

SEE PROFILE

Elzbieta Majewska

University of Bialystok

24PUBLICATIONS96CITATIONS

SEE PROFILE

All content following this page was uploaded by Joanna Olbrys on 13 July 2016.

The user has requested enhancement of the downloaded file.

Crisis periods and contagion effects in the CEE stock markets: the influence of

the 2007 US subprime crisis

Article · January 2016

DOI: 10.1504/IJCEE.2016.075612

CITATIONS

0

READS

53

2 authors:

Some of the authors of this publication are also working on these related projects:

Comparative research on commonality in liquidity on the Central and Eastern European stock markets (NCN, OPUS 11, 2016/21/B/HS4/02004)View project

BST/2017/2018View project

Joanna Olbrys

Bialystok University of Technology

86PUBLICATIONS307CITATIONS

SEE PROFILE

Elzbieta Majewska

University of Bialystok

24PUBLICATIONS96CITATIONS

SEE PROFILE

All content following this page was uploaded by Joanna Olbrys on 13 July 2016.

The user has requested enhancement of the downloaded file.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

124 Int. J. Computational Economics and Econometrics, Vol. 6, No. 2, 2016

Copyright © 2016 Inderscience Enterprises Ltd.

Crisis periods and contagion effects in the CEE stock

markets: the influence of the 2007 US subprime crisis

Joanna Olbrys*

Faculty of Computer Science,

Bialystok University of Technology,

Wiejska 45A, 15–351 Bialystok, Poland

Email: j.olbrys@pb.edu.pl

*Corresponding author

Elzbieta Majewska

Faculty of Mathematics and Informatics,

University of Bialystok,

K. Ciolkowskiego 1M, 15-245 Bialystok, Poland

Email: elam@math.uwb.edu.pl

Abstract: The main goal of this paper is a direct identification of crisis periods

in the eight Central and Eastern European (CEE) equity markets, and, for

comparison, in the US market. A statistical procedure of dividing market

states into up and down markets is employed. The results confirm

October 2007–February 2009 as the common period of the recent global

financial crisis in the CEE markets, except for Slovakia. Moreover, the effect of

increasing cross-market correlations in the crisis period in the context of

contagion is investigated, applying both standard contemporaneous correlations

and volatility-adjusted correlation coefficients. A research hypothesis that there

was no contagion effect among the US and the CEE stock markets during the

2007–2009 crisis is explicitly tested. The robustness analysis of contagion tests

based on monthly, weekly and daily data is provided. The results reveal that the

utilised tests are rather less sensitive with respect to the choice of data

frequency.

Keywords: CEE stock markets; crisis period; market states; cross-market

correlations; contagion.

Reference to this paper should be made as follows: Olbrys, J. and

Majewska, E. (2016) ‘Crisis periods and contagion effects in the CEE stock

markets: the influence of the 2007 US subprime crisis’, Int. J. Computational

Economics and Econometrics, Vol. 6, No. 2, pp.124–137.

Biographical notes: Joanna Olbrys is an Assistant Professor at the Faculty of

Computer Science, Bialystok University of Technology. She holds her PhD in

Technical Sciences on Control Engineering and Robotics from the Systems

Research Institute of Polish Academy of Sciences in Warsaw. She was the

Head and the Principal Investigator of a research project financially supported

by the Polish Ministry of Science and Higher Education. She has a large

number of publications in various scientific journals such as Emerging Markets

Finance and Trade, Argumenta Oeconomica, Operations Research and

Decisions, La Pensée, Chinese Business Review, Folia Oeconomica Stetinensia

Copyright © 2016 Inderscience Enterprises Ltd.

Crisis periods and contagion effects in the CEE stock

markets: the influence of the 2007 US subprime crisis

Joanna Olbrys*

Faculty of Computer Science,

Bialystok University of Technology,

Wiejska 45A, 15–351 Bialystok, Poland

Email: j.olbrys@pb.edu.pl

*Corresponding author

Elzbieta Majewska

Faculty of Mathematics and Informatics,

University of Bialystok,

K. Ciolkowskiego 1M, 15-245 Bialystok, Poland

Email: elam@math.uwb.edu.pl

Abstract: The main goal of this paper is a direct identification of crisis periods

in the eight Central and Eastern European (CEE) equity markets, and, for

comparison, in the US market. A statistical procedure of dividing market

states into up and down markets is employed. The results confirm

October 2007–February 2009 as the common period of the recent global

financial crisis in the CEE markets, except for Slovakia. Moreover, the effect of

increasing cross-market correlations in the crisis period in the context of

contagion is investigated, applying both standard contemporaneous correlations

and volatility-adjusted correlation coefficients. A research hypothesis that there

was no contagion effect among the US and the CEE stock markets during the

2007–2009 crisis is explicitly tested. The robustness analysis of contagion tests

based on monthly, weekly and daily data is provided. The results reveal that the

utilised tests are rather less sensitive with respect to the choice of data

frequency.

Keywords: CEE stock markets; crisis period; market states; cross-market

correlations; contagion.

Reference to this paper should be made as follows: Olbrys, J. and

Majewska, E. (2016) ‘Crisis periods and contagion effects in the CEE stock

markets: the influence of the 2007 US subprime crisis’, Int. J. Computational

Economics and Econometrics, Vol. 6, No. 2, pp.124–137.

Biographical notes: Joanna Olbrys is an Assistant Professor at the Faculty of

Computer Science, Bialystok University of Technology. She holds her PhD in

Technical Sciences on Control Engineering and Robotics from the Systems

Research Institute of Polish Academy of Sciences in Warsaw. She was the

Head and the Principal Investigator of a research project financially supported

by the Polish Ministry of Science and Higher Education. She has a large

number of publications in various scientific journals such as Emerging Markets

Finance and Trade, Argumenta Oeconomica, Operations Research and

Decisions, La Pensée, Chinese Business Review, Folia Oeconomica Stetinensia

Crisis periods and contagion effects in the CEE stock markets 125

and Dynamic Econometric Models, Control and Cybernetics. She acts as a

Referee to Tourism Management, International Review of Economics and

Finance, Economic Modelling and Acta Oeconomica.

Elzbieta Majewska is an Assistant Professor at the Faculty of Mathematics

and Informatics, University of Bialystok. She holds her PhD in Economics

from the Warsaw University of Life Science. She has a number of publications

in various scientific journals such as Argumenta Oeconomica, Operations

Research and Decisions, La Pensée and Chinese Business Review.

This paper is a revised and expanded version of a paper entitled ‘Direct

identification of crisis periods on the CEE stock markets: the influence of the

2007 US subprime crisis’ presented at the ICOAE, Chania, Island of Crete,

Greece, 3–5 July, 2014.

1 Introduction

An event that had significant impact on a group of eight Central and Eastern European

(CEE) emerging markets was the accession to the European Union (EU) on the 1st of

May 2004. These eight countries, in the order of decreasing population size, are: Poland,

the Czech Republic, Hungary, Slovakia, Lithuania, Latvia, Slovenia and Estonia. The

CEE economies are interesting in many respects, especially in the context of the

influence of the 2007 US subprime crisis.

There have been numerous studies of the influence and consequences of the 2007 US

subprime crisis for developed and emerging stock markets in the world. As the aim of

this paper is a direct statistical identification of crisis periods in the CEE equity markets,

we focus our analysis of the previous literature on the studies related mostly to the

European economies. According to the literature (Calomiris, 2009; Brunnermeier, 2009;

Claessens et al., 2010), the financial crisis timeline, from the US perspective, was

marketed by the following events:

• the increase in subprime delinquency rates in the spring of 2007

• the ensuing liquidity crunch in late 2007

• the liquidation of Bear Stearns in March 2008

• the failure of Lehman Brothers in September 2008.

The US economy officially slipped into recession following the peak in December 2007.

The crisis began in the USA, but initially it did not affect the CEE markets to the same

extent. Claessens et al. (2010) identified five groups of countries based on the date they

were affected by the crisis. They advocated that Latvia and Estonia entered recession at

2008Q1, Hungary at 2008Q2, together with the major Western European countries, i.e.,

the UK, France and Germany, Lithuania and Slovenia at 2008Q3, while Poland and the

Czech Republic slipped into recession in 2008Q4. Slovakia entered recession with a

delay, to wit in 2009Q1. As a matter of fact, the Baltic region stock markets were among

the most affected by the crisis. Lane and Milesi-Ferretti (2011, p.19) showed that

and Dynamic Econometric Models, Control and Cybernetics. She acts as a

Referee to Tourism Management, International Review of Economics and

Finance, Economic Modelling and Acta Oeconomica.

Elzbieta Majewska is an Assistant Professor at the Faculty of Mathematics

and Informatics, University of Bialystok. She holds her PhD in Economics

from the Warsaw University of Life Science. She has a number of publications

in various scientific journals such as Argumenta Oeconomica, Operations

Research and Decisions, La Pensée and Chinese Business Review.

This paper is a revised and expanded version of a paper entitled ‘Direct

identification of crisis periods on the CEE stock markets: the influence of the

2007 US subprime crisis’ presented at the ICOAE, Chania, Island of Crete,

Greece, 3–5 July, 2014.

1 Introduction

An event that had significant impact on a group of eight Central and Eastern European

(CEE) emerging markets was the accession to the European Union (EU) on the 1st of

May 2004. These eight countries, in the order of decreasing population size, are: Poland,

the Czech Republic, Hungary, Slovakia, Lithuania, Latvia, Slovenia and Estonia. The

CEE economies are interesting in many respects, especially in the context of the

influence of the 2007 US subprime crisis.

There have been numerous studies of the influence and consequences of the 2007 US

subprime crisis for developed and emerging stock markets in the world. As the aim of

this paper is a direct statistical identification of crisis periods in the CEE equity markets,

we focus our analysis of the previous literature on the studies related mostly to the

European economies. According to the literature (Calomiris, 2009; Brunnermeier, 2009;

Claessens et al., 2010), the financial crisis timeline, from the US perspective, was

marketed by the following events:

• the increase in subprime delinquency rates in the spring of 2007

• the ensuing liquidity crunch in late 2007

• the liquidation of Bear Stearns in March 2008

• the failure of Lehman Brothers in September 2008.

The US economy officially slipped into recession following the peak in December 2007.

The crisis began in the USA, but initially it did not affect the CEE markets to the same

extent. Claessens et al. (2010) identified five groups of countries based on the date they

were affected by the crisis. They advocated that Latvia and Estonia entered recession at

2008Q1, Hungary at 2008Q2, together with the major Western European countries, i.e.,

the UK, France and Germany, Lithuania and Slovenia at 2008Q3, while Poland and the

Czech Republic slipped into recession in 2008Q4. Slovakia entered recession with a

delay, to wit in 2009Q1. As a matter of fact, the Baltic region stock markets were among

the most affected by the crisis. Lane and Milesi-Ferretti (2011, p.19) showed that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

126 J. Olbrys and E. Majewska

Lithuania, Latvia and Estonia entered the group of the ‘Top 5’ crisis countries. Marer

(2010) analysed the CEE economies among other Eastern European countries in the

context of commonalities and differences during recent financial crisis. He stressed that

the global liquidity crisis hit the most vulnerable economies (i.e., Hungary and the Baltic

States) immediately and hard, while the region’s less vulnerable countries (i.e., Poland,

the Czech Republic, Slovenia and Slovakia) were less affected.

It is pertinent to note that there is no unanimity in determining the global crisis period

among the researchers. In particular, there is no agreement about the pre-, post- and crisis

periods. For example, Pisani-Ferry and Sapir (2010) proposed two phases of crisis in the

EU. They advocated that the first phase started in August 2007 with a general liquidity

strain. The second phase started in September 2008 with the bankruptcy of Lehman

Brothers. Similarly, Mishkin (2011) divided the financial crisis into two distinct phases:

the first from August 2007 to August 2008, called the US subprime mortgage crisis, and

the second, which started in mid-September 2008, known as the global financial crisis.

Dooley and Hutchison (2009) investigated the links between the US and a broad range of

emerging markets over a subprime crisis period from February 2007 to March 2009.

They analysed three phases of the subprime crisis and they argued that the first phase of

the crisis ran from 27 February, 2007. The authors stressed that the emerging markets

were somewhat insulated and decoupled from the US market from early 2007 to summer

2008. Calomiris et al. (2012) considered three ‘crisis shocks’ related to key features of

the 2007–2008 crisis for the emerging and developed economies: the collapse of global

trade, the contraction of credit supply and selling pressure on firm’s equity. They

advocated August 2007–December 2008 as the crisis period. Bartram and Bodnar (2009)

proposed a detailed investigation of the global financial crisis 2008–2009 and provided a

timeline of events and policy actions for the crisis in equity markets. They advocated

1 January, 2007–12 September, 2008 as the pre-crisis period, and 28 October,

2008–27 February, 2009 as the post-crisis period. As a matter of fact, their choice of the

post-crisis period seems to be rather controversial in the light of the stock market indexes

continuing their decline during this period. Olbrys and Majewska (2013) proposed

27 February, 2007–9 March, 2009 as a crisis period, based on the S&P500 index decline.

The overall S&P500 index fell from 1399.04 (27 February, 2007) to 676.53 (9 March,

2009) and it lost 51.64% of its previous value during the crisis period.

The main goal of this paper is a direct identification of crisis periods on the eight CEE

stock markets, and, for comparison, on the US market. The sample period begins with the

CEE accession to the EU on the 1st of May, 2004, and ends on 30 April, 2013, and it

includes the 2007 US subprime crisis period. We employ a statistical procedure of

dividing market states into bullish and bearish markets (Pagan and Sossounov, 2003).

The study whether states are common during the crisis period is a crucial topic because of

many practical implications in light of market globalisation, as well as international

portfolio choice and diversification. Our results confirm October 2007–February 2009 as

the common period of the recent global financial crisis, except for Slovakia.

Furthermore, we investigate the effect of increasing cross-market correlations in the

crisis period in the context of contagion, applying both standard contemporaneous

correlations and volatility-adjusted correlation coefficients proposed by Forbes and

Rigobon (2002), who stressed that market return volatility can bias standard cross-

correlations. We explicitly test a research hypothesis that there was no contagion effect

Lithuania, Latvia and Estonia entered the group of the ‘Top 5’ crisis countries. Marer

(2010) analysed the CEE economies among other Eastern European countries in the

context of commonalities and differences during recent financial crisis. He stressed that

the global liquidity crisis hit the most vulnerable economies (i.e., Hungary and the Baltic

States) immediately and hard, while the region’s less vulnerable countries (i.e., Poland,

the Czech Republic, Slovenia and Slovakia) were less affected.

It is pertinent to note that there is no unanimity in determining the global crisis period

among the researchers. In particular, there is no agreement about the pre-, post- and crisis

periods. For example, Pisani-Ferry and Sapir (2010) proposed two phases of crisis in the

EU. They advocated that the first phase started in August 2007 with a general liquidity

strain. The second phase started in September 2008 with the bankruptcy of Lehman

Brothers. Similarly, Mishkin (2011) divided the financial crisis into two distinct phases:

the first from August 2007 to August 2008, called the US subprime mortgage crisis, and

the second, which started in mid-September 2008, known as the global financial crisis.

Dooley and Hutchison (2009) investigated the links between the US and a broad range of

emerging markets over a subprime crisis period from February 2007 to March 2009.

They analysed three phases of the subprime crisis and they argued that the first phase of

the crisis ran from 27 February, 2007. The authors stressed that the emerging markets

were somewhat insulated and decoupled from the US market from early 2007 to summer

2008. Calomiris et al. (2012) considered three ‘crisis shocks’ related to key features of

the 2007–2008 crisis for the emerging and developed economies: the collapse of global

trade, the contraction of credit supply and selling pressure on firm’s equity. They

advocated August 2007–December 2008 as the crisis period. Bartram and Bodnar (2009)

proposed a detailed investigation of the global financial crisis 2008–2009 and provided a

timeline of events and policy actions for the crisis in equity markets. They advocated

1 January, 2007–12 September, 2008 as the pre-crisis period, and 28 October,

2008–27 February, 2009 as the post-crisis period. As a matter of fact, their choice of the

post-crisis period seems to be rather controversial in the light of the stock market indexes

continuing their decline during this period. Olbrys and Majewska (2013) proposed

27 February, 2007–9 March, 2009 as a crisis period, based on the S&P500 index decline.

The overall S&P500 index fell from 1399.04 (27 February, 2007) to 676.53 (9 March,

2009) and it lost 51.64% of its previous value during the crisis period.

The main goal of this paper is a direct identification of crisis periods on the eight CEE

stock markets, and, for comparison, on the US market. The sample period begins with the

CEE accession to the EU on the 1st of May, 2004, and ends on 30 April, 2013, and it

includes the 2007 US subprime crisis period. We employ a statistical procedure of

dividing market states into bullish and bearish markets (Pagan and Sossounov, 2003).

The study whether states are common during the crisis period is a crucial topic because of

many practical implications in light of market globalisation, as well as international

portfolio choice and diversification. Our results confirm October 2007–February 2009 as

the common period of the recent global financial crisis, except for Slovakia.

Furthermore, we investigate the effect of increasing cross-market correlations in the

crisis period in the context of contagion, applying both standard contemporaneous

correlations and volatility-adjusted correlation coefficients proposed by Forbes and

Rigobon (2002), who stressed that market return volatility can bias standard cross-

correlations. We explicitly test a research hypothesis that there was no contagion effect

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Crisis periods and contagion effects in the CEE stock markets 127

among the US and the CEE equity markets during the 2007–2009 global financial crisis.

The robustness analysis of contagion tests based on monthly, weekly and daily

logarithmic returns of major stock market indexes is provided. The empirical results

reveal that the utilised tests are rather less sensitive with respect to the choice of data

frequency.

To the best of the authors’ knowledge, no such research has been undertaken jointly

for the CEE and the US stock markets.

The remainder of this paper is organised as follows. Section 2 specifies the

methodological background of the statistical method of dividing market states into up and

down markets. In Section 3, we propose a brief analysis of the effect of increasing cross-

market correlations in down markets, especially in crisis periods. In Section 4, we present

data description and empirical results on the main indexes of the CEE and US stock

markets. Section 5 recalls the main findings and presents the conclusions.

2 Procedure for identification of bullish and bearish markets

Lunde and Timmermann (2000) stressed that there is no generally accepted formal

definition of up and down markets in finance literature. They created an algorithm for

detecting bull and bear states. Cooper et al. (2004) identified an up or a down market

when the past 12-, 24- or 36-month market return is non-negative (negative),

respectively. Pagan and Sossounov (2003) developed an algorithm that seemed to be

successful in locating periods in time that were considered bull and bear markets in US

equity prices. They tested monthly data of the S&P500 index, in the period from

January 1835 to May 1997. Lee et al. (2011) proposed a modified version of the

Pagan-Sossounov method of dividing market states into bullish, bearish and range-bound

markets. We employ a three-stage procedure of dividing market states into up and down

markets (Olbrys and Majewska, 2014a). Our methodology builds on Pagan and

Sossounov (2003). In the first step, we conduct a preliminary identification of turning

points, i.e., peaks and troughs, based on conditions (1) and (2), respectively:

8 1 1 8ln , , ln ln ln , , ln ,t t t t tP P P P P− − + +< >… … (1)

8 1 1 8ln , , ln ln ln , , ln ,t t t t tP P P P P− − + +> <… … (2)

where Pt represents the market index of month t, and from successive peaks/troughs we

choose the highest/deepest one, respectively. Pagan and Sossounov (2003) stressed that

in the business cycle literature an algorithm for describing turning points in time series

was developed by Bry and Boschan (1971), but they modified this algorithm by taking

the eight-month window (instead of six) in marking the initial location of turning points.

The main goal was not to smooth any of the monthly, already smoothed, data.

In the second step, we rule out the phases (peak-trough or trough-peak) that last for

less than 4 months and cycles (peak-trough-peak or trough-peak-trough) that last for less

than 16 months. Pagan and Sossounov (2003) pointed out that in business cycle dating

the minimal cycle length is 15 months; hence, 16 months were chosen to create a

symmetric window of eight periods. Furthermore, they advocated four months as the

minimal length of a phase.

In the last step, we calculate the amplitudes A for each phase (amplitude is the

difference in the natural logs of the index value in subsequent turning points). During the

among the US and the CEE equity markets during the 2007–2009 global financial crisis.

The robustness analysis of contagion tests based on monthly, weekly and daily

logarithmic returns of major stock market indexes is provided. The empirical results

reveal that the utilised tests are rather less sensitive with respect to the choice of data

frequency.

To the best of the authors’ knowledge, no such research has been undertaken jointly

for the CEE and the US stock markets.

The remainder of this paper is organised as follows. Section 2 specifies the

methodological background of the statistical method of dividing market states into up and

down markets. In Section 3, we propose a brief analysis of the effect of increasing cross-

market correlations in down markets, especially in crisis periods. In Section 4, we present

data description and empirical results on the main indexes of the CEE and US stock

markets. Section 5 recalls the main findings and presents the conclusions.

2 Procedure for identification of bullish and bearish markets

Lunde and Timmermann (2000) stressed that there is no generally accepted formal

definition of up and down markets in finance literature. They created an algorithm for

detecting bull and bear states. Cooper et al. (2004) identified an up or a down market

when the past 12-, 24- or 36-month market return is non-negative (negative),

respectively. Pagan and Sossounov (2003) developed an algorithm that seemed to be

successful in locating periods in time that were considered bull and bear markets in US

equity prices. They tested monthly data of the S&P500 index, in the period from

January 1835 to May 1997. Lee et al. (2011) proposed a modified version of the

Pagan-Sossounov method of dividing market states into bullish, bearish and range-bound

markets. We employ a three-stage procedure of dividing market states into up and down

markets (Olbrys and Majewska, 2014a). Our methodology builds on Pagan and

Sossounov (2003). In the first step, we conduct a preliminary identification of turning

points, i.e., peaks and troughs, based on conditions (1) and (2), respectively:

8 1 1 8ln , , ln ln ln , , ln ,t t t t tP P P P P− − + +< >… … (1)

8 1 1 8ln , , ln ln ln , , ln ,t t t t tP P P P P− − + +> <… … (2)

where Pt represents the market index of month t, and from successive peaks/troughs we

choose the highest/deepest one, respectively. Pagan and Sossounov (2003) stressed that

in the business cycle literature an algorithm for describing turning points in time series

was developed by Bry and Boschan (1971), but they modified this algorithm by taking

the eight-month window (instead of six) in marking the initial location of turning points.

The main goal was not to smooth any of the monthly, already smoothed, data.

In the second step, we rule out the phases (peak-trough or trough-peak) that last for

less than 4 months and cycles (peak-trough-peak or trough-peak-trough) that last for less

than 16 months. Pagan and Sossounov (2003) pointed out that in business cycle dating

the minimal cycle length is 15 months; hence, 16 months were chosen to create a

symmetric window of eight periods. Furthermore, they advocated four months as the

minimal length of a phase.

In the last step, we calculate the amplitudes A for each phase (amplitude is the

difference in the natural logs of the index value in subsequent turning points). During the

128 J. Olbrys and E. Majewska

bull/bear market period, there must be a large enough (of at least 20%) rise/fall in the

index value. This means that the amplitude of a given phase must fulfil the condition

A ≥ 0.18 or A ≤ −0.22 for the bull or bear market period, respectively (Olbrys and

Majewska, 2014a, p.255). The identification of market states is a problem of considerable

importance, as Cooper et al. (2004) among others obtained that profits to investment

strategies depend critically on the state of the market.

3 Effect of increasing cross-market correlations in the crisis period

International equity market correlation is a very important topic because of many

practical implications, especially in the context of international portfolio choice and

diversification. For example, Longin and Solnik (2001) studied the conditional

correlation structure of international equity returns and derived a formal statistical

method, based on the extreme value theory. They found that conditional correlation

increases in bear markets, but not in bull markets. Goetzmann et al. (2005) examined the

correlation structure of the major world markets over 150 years. They found that

international equity correlations change dramatically through time, thus the

diversification benefits to global investing are not constant. Hong et al. (2007) provided a

model-free test for asymmetric correlations in bear vs. bull markets. They evaluated the

economic significance of incorporating asymmetries into investment decisions.

Although there is no unanimity in research regarding the reasons of increasing

cross-market correlations in crisis periods, the majority of researchers agree that during

crucial market events correlations change dramatically. This evidence is often justified by

the authors as the consequence of contagion. As a matter of fact, contagion is not simply

revealed by increased correlation of market returns during a crisis period (e.g., Edwards,

2000; Bekaert et al., 2005 and the references therein). Among others, Rigobon (2002,

p.4) stressed that there is no accordance on what contagion means. Furthermore, Forbes

and Rigobon (2002) defined contagion as a significant increase in cross-market linkages

after a shock to one country (or group of countries), but they stated that this definition is

not universally accepted. They stressed that heteroscedasticity in market returns biases

tests for contagion based on correlation and correlation coefficients are conditional on

market volatility. The authors proposed the following correction for the volatility bias:

( )2

ˆ

ˆ ,

ˆ1 1

C

VA

C

ρ

ρ

δ ρ

=

+ −

(3)

where ˆVAρ is the unconditional volatility-adjusted cross-correlation coefficient between

markets, ˆCρ is the estimated conditional cross-correlation coefficient in the crisis period

and δ is the relative increase in the variance of market returns in the crisis period

compared with the pre-crisis period:

2

2

ˆ 1,

ˆ

C

PC

σ

δ σ

= − (4)

where 2

ˆCσ and 2

ˆPCσ are the variances in the high-volatility (crisis) and low-volatility

(pre-crisis) periods, respectively. By construction, it is obvious that 2 2

ˆ ˆC PCσ σ≥ ,

bull/bear market period, there must be a large enough (of at least 20%) rise/fall in the

index value. This means that the amplitude of a given phase must fulfil the condition

A ≥ 0.18 or A ≤ −0.22 for the bull or bear market period, respectively (Olbrys and

Majewska, 2014a, p.255). The identification of market states is a problem of considerable

importance, as Cooper et al. (2004) among others obtained that profits to investment

strategies depend critically on the state of the market.

3 Effect of increasing cross-market correlations in the crisis period

International equity market correlation is a very important topic because of many

practical implications, especially in the context of international portfolio choice and

diversification. For example, Longin and Solnik (2001) studied the conditional

correlation structure of international equity returns and derived a formal statistical

method, based on the extreme value theory. They found that conditional correlation

increases in bear markets, but not in bull markets. Goetzmann et al. (2005) examined the

correlation structure of the major world markets over 150 years. They found that

international equity correlations change dramatically through time, thus the

diversification benefits to global investing are not constant. Hong et al. (2007) provided a

model-free test for asymmetric correlations in bear vs. bull markets. They evaluated the

economic significance of incorporating asymmetries into investment decisions.

Although there is no unanimity in research regarding the reasons of increasing

cross-market correlations in crisis periods, the majority of researchers agree that during

crucial market events correlations change dramatically. This evidence is often justified by

the authors as the consequence of contagion. As a matter of fact, contagion is not simply

revealed by increased correlation of market returns during a crisis period (e.g., Edwards,

2000; Bekaert et al., 2005 and the references therein). Among others, Rigobon (2002,

p.4) stressed that there is no accordance on what contagion means. Furthermore, Forbes

and Rigobon (2002) defined contagion as a significant increase in cross-market linkages

after a shock to one country (or group of countries), but they stated that this definition is

not universally accepted. They stressed that heteroscedasticity in market returns biases

tests for contagion based on correlation and correlation coefficients are conditional on

market volatility. The authors proposed the following correction for the volatility bias:

( )2

ˆ

ˆ ,

ˆ1 1

C

VA

C

ρ

ρ

δ ρ

=

+ −

(3)

where ˆVAρ is the unconditional volatility-adjusted cross-correlation coefficient between

markets, ˆCρ is the estimated conditional cross-correlation coefficient in the crisis period

and δ is the relative increase in the variance of market returns in the crisis period

compared with the pre-crisis period:

2

2

ˆ 1,

ˆ

C

PC

σ

δ σ

= − (4)

where 2

ˆCσ and 2

ˆPCσ are the variances in the high-volatility (crisis) and low-volatility

(pre-crisis) periods, respectively. By construction, it is obvious that 2 2

ˆ ˆC PCσ σ≥ ,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Crisis periods and contagion effects in the CEE stock markets 129

hence δ ≥ 0 and ˆ ˆ ,VA Cρ ρ≤ i.e., during the periods of high volatility the unconditional

volatility-adjusted cross-correlation ˆVAρ will be smaller than the estimated conditional

cross-correlation ˆCρ between markets. The evaluation of contagion is carried out by

testing the hypotheses:

0

1

:

: ,

VA PC

VA PC

H

H

ρ ρ

ρ ρ

=

≠ (5)

where PCρ is the cross-correlation coefficient in the pre-crisis period, and the null

hypothesis states that there is no contagion. The Z-statistic, which is asymptotically a

standard normal random variable, tests the null of no contagion, i.e., the equality of the

crisis with pre-crisis cross-market correlation coefficients. The test is performed with the

Fisher (1921) z-transformation of sample correlation coefficients. If the absolute value of

the Z-statistic is greater than the critical value, the null hypothesis of identical correlation

coefficients can be rejected (Olbrys and Majewska, 2014c).

4 Data description and empirical results on the main indexes of the CEE

and US stock markets

In this study, we use our own database, not a commercial one. The raw data consists of

daily closing prices of the stock market indexes. We calculate daily, weekly and monthly

logarithmic returns of the major CEE stock market indexes (i.e., WIG, PX, BUX, SBI

TOP, SAX, OMXV, OMXT and OMXR) and the New York market index – S&P500.

There are 1969 daily, 469 weekly and 108 monthly observations for each series for the

period beginning May 2004 and ending April 2013 (9 years). To employ the procedure

described in Section 2, the data was extended to the period from September 2003 to

December 2013 (eight months back and forward).

We use weekly Wednesday-to-Wednesday logarithmic returns, which are thought to

iron out any possible impact of the day-of-the-week effects of daily data. As for daily

returns, one potentially serious problem, which may substantially disrupt various analyses

employing multivariate time series, is the non-synchronous trading effect II between

international stock markets (Olbrys and Majewska, 2014d). Therefore, in this research,

we employ a ‘common trading window’ procedure as a daily data-matching method. We

perform the robustness analysis with respect to various data frequencies, using daily,

weekly and monthly logarithmic returns of the stock market indexes. All analyses are

conducted using the open-source computer software Gretl 1.9.14 (Adkins, 2014).

4.1 Preliminary statistics

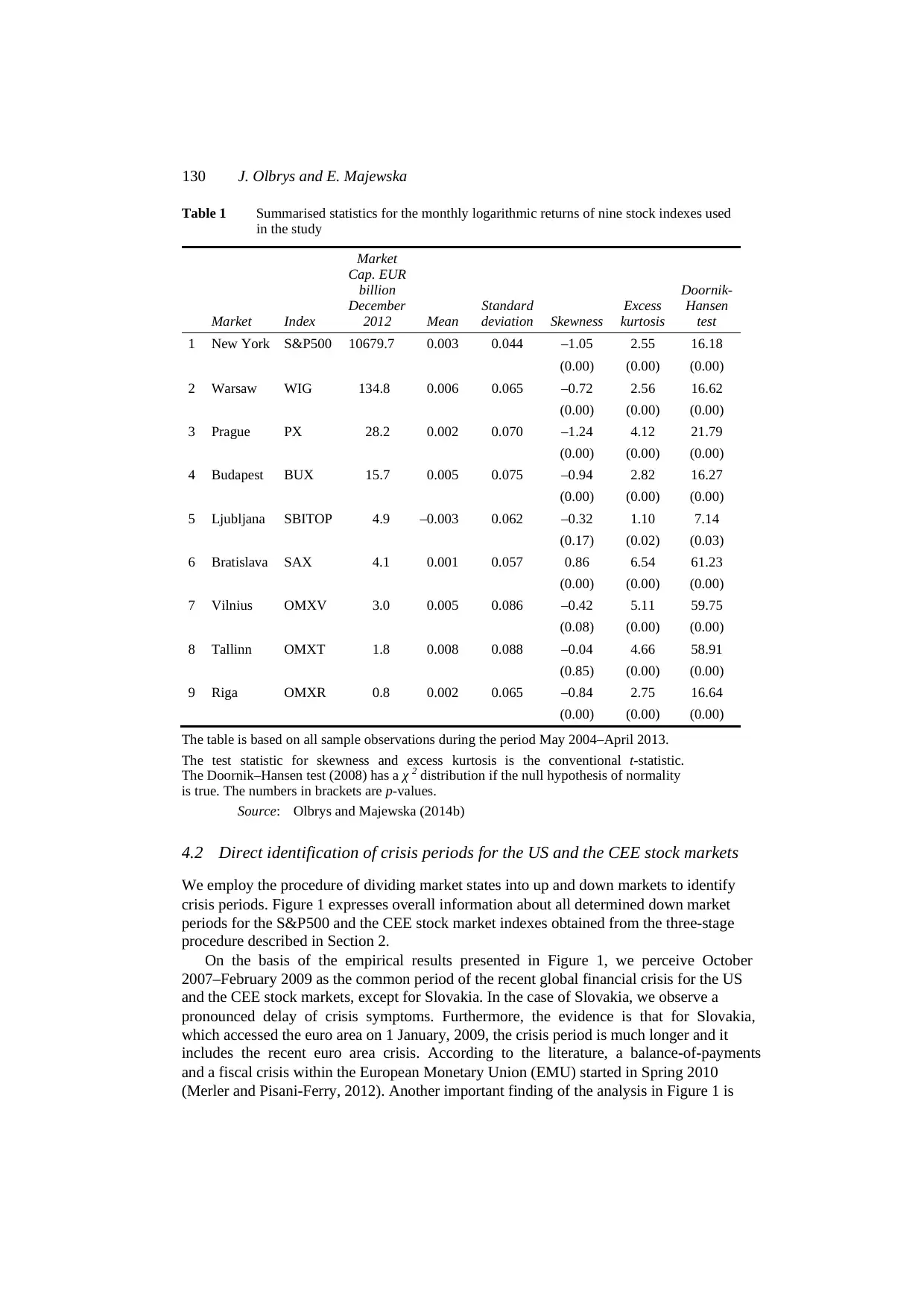

Table 1 reports summarised statistics for the monthly logarithmic returns for nine stock

indexes (in order of decreasing value of market capitalisation at the end of 2012), as well

as statistics testing for normality.

Several results in Table 1 are worth a comment. The measure for skewness shows that

the return series are skewed, except for the SBI TOP, OMXV and OMXT series.

The measure for excess kurtosis shows that all series are highly leptokurtic with respect

to the normal distribution. The Doornik-Hansen (Doornik and Hansen, 2008) test rejects

normality for each of the return series at the 5% level of significance.

hence δ ≥ 0 and ˆ ˆ ,VA Cρ ρ≤ i.e., during the periods of high volatility the unconditional

volatility-adjusted cross-correlation ˆVAρ will be smaller than the estimated conditional

cross-correlation ˆCρ between markets. The evaluation of contagion is carried out by

testing the hypotheses:

0

1

:

: ,

VA PC

VA PC

H

H

ρ ρ

ρ ρ

=

≠ (5)

where PCρ is the cross-correlation coefficient in the pre-crisis period, and the null

hypothesis states that there is no contagion. The Z-statistic, which is asymptotically a

standard normal random variable, tests the null of no contagion, i.e., the equality of the

crisis with pre-crisis cross-market correlation coefficients. The test is performed with the

Fisher (1921) z-transformation of sample correlation coefficients. If the absolute value of

the Z-statistic is greater than the critical value, the null hypothesis of identical correlation

coefficients can be rejected (Olbrys and Majewska, 2014c).

4 Data description and empirical results on the main indexes of the CEE

and US stock markets

In this study, we use our own database, not a commercial one. The raw data consists of

daily closing prices of the stock market indexes. We calculate daily, weekly and monthly

logarithmic returns of the major CEE stock market indexes (i.e., WIG, PX, BUX, SBI

TOP, SAX, OMXV, OMXT and OMXR) and the New York market index – S&P500.

There are 1969 daily, 469 weekly and 108 monthly observations for each series for the

period beginning May 2004 and ending April 2013 (9 years). To employ the procedure

described in Section 2, the data was extended to the period from September 2003 to

December 2013 (eight months back and forward).

We use weekly Wednesday-to-Wednesday logarithmic returns, which are thought to

iron out any possible impact of the day-of-the-week effects of daily data. As for daily

returns, one potentially serious problem, which may substantially disrupt various analyses

employing multivariate time series, is the non-synchronous trading effect II between

international stock markets (Olbrys and Majewska, 2014d). Therefore, in this research,

we employ a ‘common trading window’ procedure as a daily data-matching method. We

perform the robustness analysis with respect to various data frequencies, using daily,

weekly and monthly logarithmic returns of the stock market indexes. All analyses are

conducted using the open-source computer software Gretl 1.9.14 (Adkins, 2014).

4.1 Preliminary statistics

Table 1 reports summarised statistics for the monthly logarithmic returns for nine stock

indexes (in order of decreasing value of market capitalisation at the end of 2012), as well

as statistics testing for normality.

Several results in Table 1 are worth a comment. The measure for skewness shows that

the return series are skewed, except for the SBI TOP, OMXV and OMXT series.

The measure for excess kurtosis shows that all series are highly leptokurtic with respect

to the normal distribution. The Doornik-Hansen (Doornik and Hansen, 2008) test rejects

normality for each of the return series at the 5% level of significance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

130 J. Olbrys and E. Majewska

Table 1 Summarised statistics for the monthly logarithmic returns of nine stock indexes used

in the study

Market Index

Market

Cap. EUR

billion

December

2012 Mean

Standard

deviation Skewness

Excess

kurtosis

Doornik-

Hansen

test

1 New York S&P500 10679.7 0.003 0.044 –1.05 2.55 16.18

(0.00) (0.00) (0.00)

2 Warsaw WIG 134.8 0.006 0.065 –0.72 2.56 16.62

(0.00) (0.00) (0.00)

3 Prague PX 28.2 0.002 0.070 –1.24 4.12 21.79

(0.00) (0.00) (0.00)

4 Budapest BUX 15.7 0.005 0.075 –0.94 2.82 16.27

(0.00) (0.00) (0.00)

5 Ljubljana SBITOP 4.9 –0.003 0.062 –0.32 1.10 7.14

(0.17) (0.02) (0.03)

6 Bratislava SAX 4.1 0.001 0.057 0.86 6.54 61.23

(0.00) (0.00) (0.00)

7 Vilnius OMXV 3.0 0.005 0.086 –0.42 5.11 59.75

(0.08) (0.00) (0.00)

8 Tallinn OMXT 1.8 0.008 0.088 –0.04 4.66 58.91

(0.85) (0.00) (0.00)

9 Riga OMXR 0.8 0.002 0.065 –0.84 2.75 16.64

(0.00) (0.00) (0.00)

The table is based on all sample observations during the period May 2004–April 2013.

The test statistic for skewness and excess kurtosis is the conventional t-statistic.

The Doornik–Hansen test (2008) has a χ 2 distribution if the null hypothesis of normality

is true. The numbers in brackets are p-values.

Source: Olbrys and Majewska (2014b)

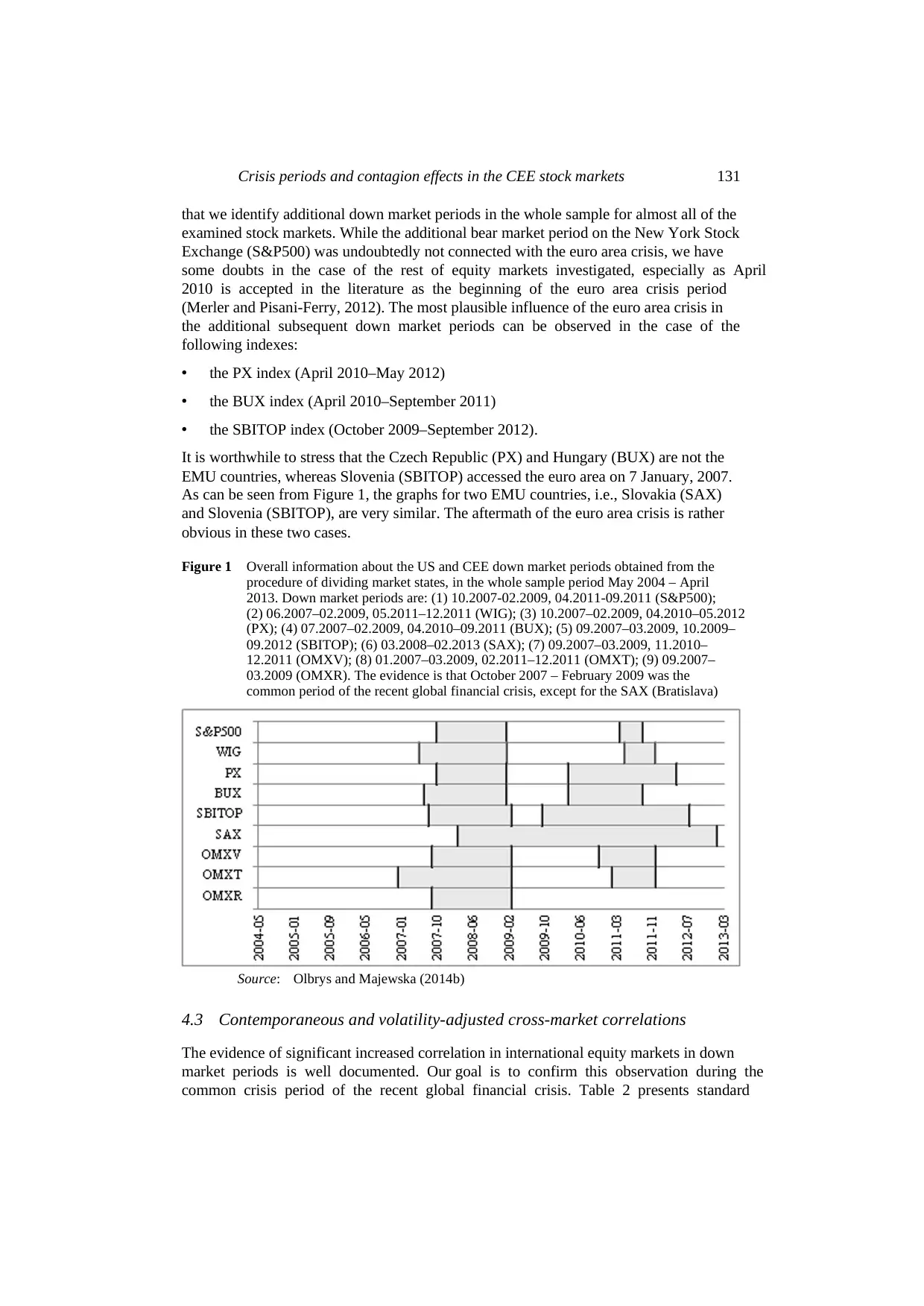

4.2 Direct identification of crisis periods for the US and the CEE stock markets

We employ the procedure of dividing market states into up and down markets to identify

crisis periods. Figure 1 expresses overall information about all determined down market

periods for the S&P500 and the CEE stock market indexes obtained from the three-stage

procedure described in Section 2.

On the basis of the empirical results presented in Figure 1, we perceive October

2007–February 2009 as the common period of the recent global financial crisis for the US

and the CEE stock markets, except for Slovakia. In the case of Slovakia, we observe a

pronounced delay of crisis symptoms. Furthermore, the evidence is that for Slovakia,

which accessed the euro area on 1 January, 2009, the crisis period is much longer and it

includes the recent euro area crisis. According to the literature, a balance-of-payments

and a fiscal crisis within the European Monetary Union (EMU) started in Spring 2010

(Merler and Pisani-Ferry, 2012). Another important finding of the analysis in Figure 1 is

Table 1 Summarised statistics for the monthly logarithmic returns of nine stock indexes used

in the study

Market Index

Market

Cap. EUR

billion

December

2012 Mean

Standard

deviation Skewness

Excess

kurtosis

Doornik-

Hansen

test

1 New York S&P500 10679.7 0.003 0.044 –1.05 2.55 16.18

(0.00) (0.00) (0.00)

2 Warsaw WIG 134.8 0.006 0.065 –0.72 2.56 16.62

(0.00) (0.00) (0.00)

3 Prague PX 28.2 0.002 0.070 –1.24 4.12 21.79

(0.00) (0.00) (0.00)

4 Budapest BUX 15.7 0.005 0.075 –0.94 2.82 16.27

(0.00) (0.00) (0.00)

5 Ljubljana SBITOP 4.9 –0.003 0.062 –0.32 1.10 7.14

(0.17) (0.02) (0.03)

6 Bratislava SAX 4.1 0.001 0.057 0.86 6.54 61.23

(0.00) (0.00) (0.00)

7 Vilnius OMXV 3.0 0.005 0.086 –0.42 5.11 59.75

(0.08) (0.00) (0.00)

8 Tallinn OMXT 1.8 0.008 0.088 –0.04 4.66 58.91

(0.85) (0.00) (0.00)

9 Riga OMXR 0.8 0.002 0.065 –0.84 2.75 16.64

(0.00) (0.00) (0.00)

The table is based on all sample observations during the period May 2004–April 2013.

The test statistic for skewness and excess kurtosis is the conventional t-statistic.

The Doornik–Hansen test (2008) has a χ 2 distribution if the null hypothesis of normality

is true. The numbers in brackets are p-values.

Source: Olbrys and Majewska (2014b)

4.2 Direct identification of crisis periods for the US and the CEE stock markets

We employ the procedure of dividing market states into up and down markets to identify

crisis periods. Figure 1 expresses overall information about all determined down market

periods for the S&P500 and the CEE stock market indexes obtained from the three-stage

procedure described in Section 2.

On the basis of the empirical results presented in Figure 1, we perceive October

2007–February 2009 as the common period of the recent global financial crisis for the US

and the CEE stock markets, except for Slovakia. In the case of Slovakia, we observe a

pronounced delay of crisis symptoms. Furthermore, the evidence is that for Slovakia,

which accessed the euro area on 1 January, 2009, the crisis period is much longer and it

includes the recent euro area crisis. According to the literature, a balance-of-payments

and a fiscal crisis within the European Monetary Union (EMU) started in Spring 2010

(Merler and Pisani-Ferry, 2012). Another important finding of the analysis in Figure 1 is

Crisis periods and contagion effects in the CEE stock markets 131

that we identify additional down market periods in the whole sample for almost all of the

examined stock markets. While the additional bear market period on the New York Stock

Exchange (S&P500) was undoubtedly not connected with the euro area crisis, we have

some doubts in the case of the rest of equity markets investigated, especially as April

2010 is accepted in the literature as the beginning of the euro area crisis period

(Merler and Pisani-Ferry, 2012). The most plausible influence of the euro area crisis in

the additional subsequent down market periods can be observed in the case of the

following indexes:

• the PX index (April 2010–May 2012)

• the BUX index (April 2010–September 2011)

• the SBITOP index (October 2009–September 2012).

It is worthwhile to stress that the Czech Republic (PX) and Hungary (BUX) are not the

EMU countries, whereas Slovenia (SBITOP) accessed the euro area on 7 January, 2007.

As can be seen from Figure 1, the graphs for two EMU countries, i.e., Slovakia (SAX)

and Slovenia (SBITOP), are very similar. The aftermath of the euro area crisis is rather

obvious in these two cases.

Figure 1 Overall information about the US and CEE down market periods obtained from the

procedure of dividing market states, in the whole sample period May 2004 – April

2013. Down market periods are: (1) 10.2007-02.2009, 04.2011-09.2011 (S&P500);

(2) 06.2007–02.2009, 05.2011–12.2011 (WIG); (3) 10.2007–02.2009, 04.2010–05.2012

(PX); (4) 07.2007–02.2009, 04.2010–09.2011 (BUX); (5) 09.2007–03.2009, 10.2009–

09.2012 (SBITOP); (6) 03.2008–02.2013 (SAX); (7) 09.2007–03.2009, 11.2010–

12.2011 (OMXV); (8) 01.2007–03.2009, 02.2011–12.2011 (OMXT); (9) 09.2007–

03.2009 (OMXR). The evidence is that October 2007 – February 2009 was the

common period of the recent global financial crisis, except for the SAX (Bratislava)

Source: Olbrys and Majewska (2014b)

4.3 Contemporaneous and volatility-adjusted cross-market correlations

The evidence of significant increased correlation in international equity markets in down

market periods is well documented. Our goal is to confirm this observation during the

common crisis period of the recent global financial crisis. Table 2 presents standard

that we identify additional down market periods in the whole sample for almost all of the

examined stock markets. While the additional bear market period on the New York Stock

Exchange (S&P500) was undoubtedly not connected with the euro area crisis, we have

some doubts in the case of the rest of equity markets investigated, especially as April

2010 is accepted in the literature as the beginning of the euro area crisis period

(Merler and Pisani-Ferry, 2012). The most plausible influence of the euro area crisis in

the additional subsequent down market periods can be observed in the case of the

following indexes:

• the PX index (April 2010–May 2012)

• the BUX index (April 2010–September 2011)

• the SBITOP index (October 2009–September 2012).

It is worthwhile to stress that the Czech Republic (PX) and Hungary (BUX) are not the

EMU countries, whereas Slovenia (SBITOP) accessed the euro area on 7 January, 2007.

As can be seen from Figure 1, the graphs for two EMU countries, i.e., Slovakia (SAX)

and Slovenia (SBITOP), are very similar. The aftermath of the euro area crisis is rather

obvious in these two cases.

Figure 1 Overall information about the US and CEE down market periods obtained from the

procedure of dividing market states, in the whole sample period May 2004 – April

2013. Down market periods are: (1) 10.2007-02.2009, 04.2011-09.2011 (S&P500);

(2) 06.2007–02.2009, 05.2011–12.2011 (WIG); (3) 10.2007–02.2009, 04.2010–05.2012

(PX); (4) 07.2007–02.2009, 04.2010–09.2011 (BUX); (5) 09.2007–03.2009, 10.2009–

09.2012 (SBITOP); (6) 03.2008–02.2013 (SAX); (7) 09.2007–03.2009, 11.2010–

12.2011 (OMXV); (8) 01.2007–03.2009, 02.2011–12.2011 (OMXT); (9) 09.2007–

03.2009 (OMXR). The evidence is that October 2007 – February 2009 was the

common period of the recent global financial crisis, except for the SAX (Bratislava)

Source: Olbrys and Majewska (2014b)

4.3 Contemporaneous and volatility-adjusted cross-market correlations

The evidence of significant increased correlation in international equity markets in down

market periods is well documented. Our goal is to confirm this observation during the

common crisis period of the recent global financial crisis. Table 2 presents standard

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

132 J. Olbrys and E. Majewska

contemporaneous correlations and volatility-adjusted correlation coefficients, given by

equation (3), of monthly logarithmic returns on the pairs of indexes S&P500/CEE stock

market index (excluding SAX). For comparison, we calculate the dependencies both in

the whole sample (May 2004–April 2013) and in two subsamples of equal size:

• the pre-crisis period May 2006–September 2007 (17 months)

• the common crisis period October 2007–February 2009 (17 months).

We investigate the cross-market linkages after a shock to the US financial market.

Supporting values are equal to: 2

ˆCσ = 0.00362 (the variance in the high-volatility period

in the US stock market) and 2

ˆPCσ = 0.00053 (the variance in the low-volatility period in

the US stock market), while the relative increase in the variance of S&P500, given by

equation (4), is equal to δ = 5.8663. Our results confirm that during the period of high

volatility in the US stock market (the common crisis period October 2007–February

2009), the estimated conditional cross-correlations between the US and CEE markets

were greater than the corresponding unconditional volatility-adjusted correlations;

however, the p-values in brackets inform that contemporaneous correlations are not

statistically significant in some cases.

Several results in Table 2 are especially important. On the basis of the monthly

data, there is no reason to reject the null hypothesis of no contagion based on

volatility-adjusted cross-market correlations for each of the return series. The Student’s t

critical value is 1.701 (at the 10% level of significance). On the other hand, in the case

of contemporaneous cross-market correlations, the conclusions concerning contagion

are not such homogeneous. As we can observe, the Forbes-Rigobon correction for

heteroscedastic bias in index returns leads to a substantial reduction in differences among

cross-market correlation coefficients in the pre-crisis and crisis periods. Our results are

consistent with the literature and confirm that accommodating heteroscedasticity is valid

for detecting contagion across international stock markets (e.g., Forbes and Rigobon,

2002; Serwa and Bohl, 2005).

4.4 Robustness analysis of contagion tests

In this section, we present the robustness analysis of the empirical results concerning the

research hypothesis of no contagion effects among the US and the CEE equity markets

during the recent 2007–2009 global financial crisis. We perform contagion tests using

weekly and daily logarithmic returns and we compare the results obtained with those

presented in Table 2 for monthly returns.

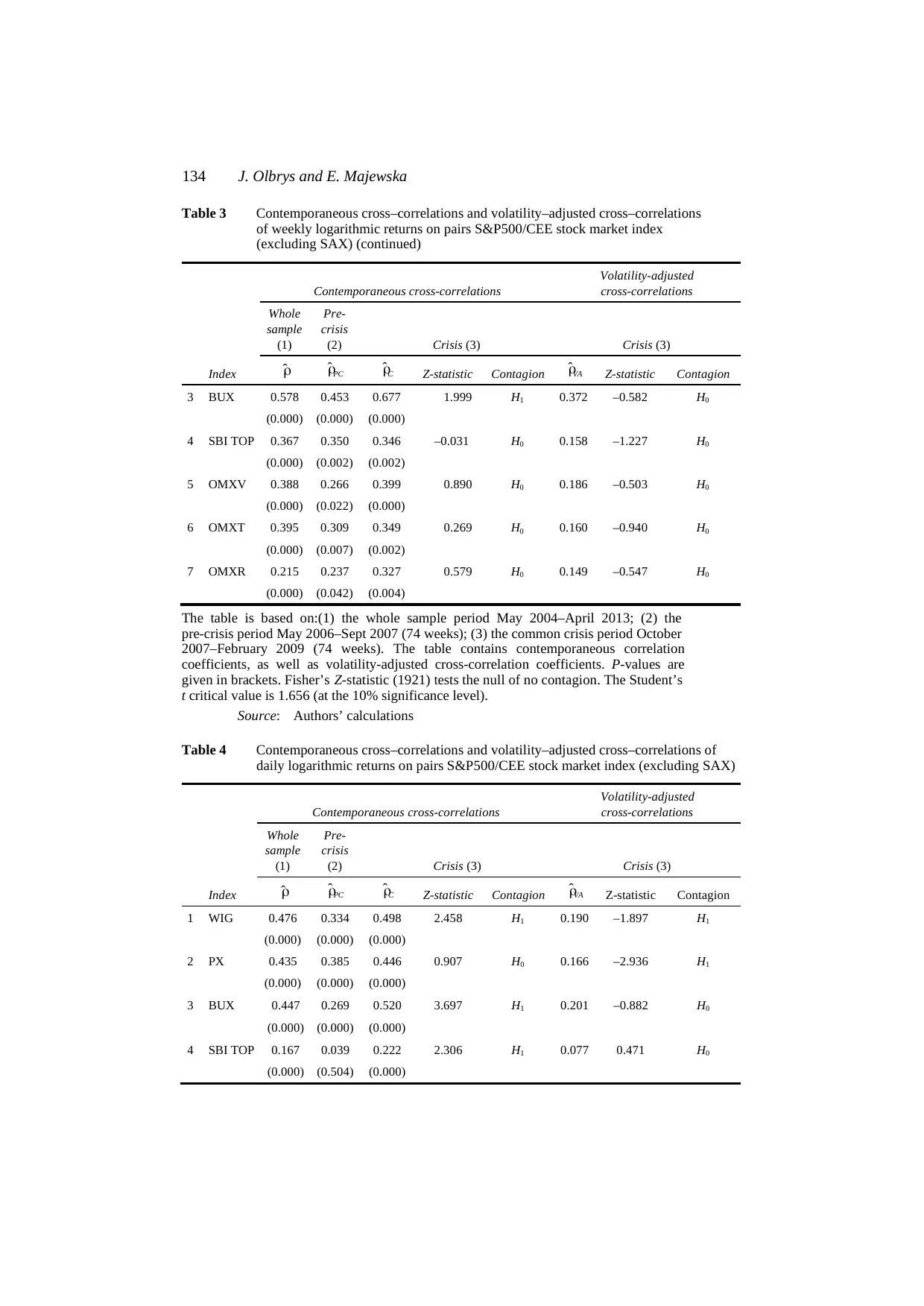

The empirical results reported in Tables 2–4 are not homogeneous, albeit only in a

few cases. On the one hand, the results of the testing of the null hypothesis of no

contagion effects based on both the monthly and the weekly data are qualitatively the

same (see Tables 2 and 3). On the other hand, when daily logarithmic returns are used

(Table 4), we observe that changes in the data frequency had some impact on the results

obtained. Unlike those shown in Tables 2–3, the results based on the Forbes-Rigobon

volatility-adjusted cross-market correlations allow to reject the null of no contagion for

daily logarithmic returns of the WIG (Warsaw) and PX (Prague) indexes. To sum up, the

results reveal that the contagion tests are rather less sensitive with respect to the choice of

data frequency.

contemporaneous correlations and volatility-adjusted correlation coefficients, given by

equation (3), of monthly logarithmic returns on the pairs of indexes S&P500/CEE stock

market index (excluding SAX). For comparison, we calculate the dependencies both in

the whole sample (May 2004–April 2013) and in two subsamples of equal size:

• the pre-crisis period May 2006–September 2007 (17 months)

• the common crisis period October 2007–February 2009 (17 months).

We investigate the cross-market linkages after a shock to the US financial market.

Supporting values are equal to: 2

ˆCσ = 0.00362 (the variance in the high-volatility period

in the US stock market) and 2

ˆPCσ = 0.00053 (the variance in the low-volatility period in

the US stock market), while the relative increase in the variance of S&P500, given by

equation (4), is equal to δ = 5.8663. Our results confirm that during the period of high

volatility in the US stock market (the common crisis period October 2007–February

2009), the estimated conditional cross-correlations between the US and CEE markets

were greater than the corresponding unconditional volatility-adjusted correlations;

however, the p-values in brackets inform that contemporaneous correlations are not

statistically significant in some cases.

Several results in Table 2 are especially important. On the basis of the monthly

data, there is no reason to reject the null hypothesis of no contagion based on

volatility-adjusted cross-market correlations for each of the return series. The Student’s t

critical value is 1.701 (at the 10% level of significance). On the other hand, in the case

of contemporaneous cross-market correlations, the conclusions concerning contagion

are not such homogeneous. As we can observe, the Forbes-Rigobon correction for

heteroscedastic bias in index returns leads to a substantial reduction in differences among

cross-market correlation coefficients in the pre-crisis and crisis periods. Our results are

consistent with the literature and confirm that accommodating heteroscedasticity is valid

for detecting contagion across international stock markets (e.g., Forbes and Rigobon,

2002; Serwa and Bohl, 2005).

4.4 Robustness analysis of contagion tests

In this section, we present the robustness analysis of the empirical results concerning the

research hypothesis of no contagion effects among the US and the CEE equity markets

during the recent 2007–2009 global financial crisis. We perform contagion tests using

weekly and daily logarithmic returns and we compare the results obtained with those

presented in Table 2 for monthly returns.

The empirical results reported in Tables 2–4 are not homogeneous, albeit only in a

few cases. On the one hand, the results of the testing of the null hypothesis of no

contagion effects based on both the monthly and the weekly data are qualitatively the

same (see Tables 2 and 3). On the other hand, when daily logarithmic returns are used

(Table 4), we observe that changes in the data frequency had some impact on the results

obtained. Unlike those shown in Tables 2–3, the results based on the Forbes-Rigobon

volatility-adjusted cross-market correlations allow to reject the null of no contagion for

daily logarithmic returns of the WIG (Warsaw) and PX (Prague) indexes. To sum up, the

results reveal that the contagion tests are rather less sensitive with respect to the choice of

data frequency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Crisis periods and contagion effects in the CEE stock markets 133

Table 2 Contemporaneous cross–correlations and volatility–adjusted cross–correlations

of monthly logarithmic returns on pairs S&P500/CEE stock market index

(excluding SAX)

Index

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

1 WIG 0.767 0.438 0.850 2.081 H1 0.524 0.298 H0

(0.000) (0.079) (0.000)

2 PX 0.750 0.672 0.894 1.659 H0 0.606 –0.297 H0

(0.000) (0.003) (0.000)

3 BUX 0.744 0.405 0.817 1.900 H1 0.476 0.232 H0

(0.000) (0.107) (0.000)

4 SBI 0.414 0.114 0.408 0.843 H0 0.168 0.146 H0

TOP (0.000) (0.664) (0.104)

5 OMXV 0.465 0.145 0.653 1.679 H0 0.313 0.469 H0

(0.000) (0.580) (0.005)

6 OMXT 0.480 0.374 0.574 0.689 H0 0.258 –0.340 H0

(0.000) (0.140) (0.016)

7 OMXR 0.386 0.239 0.284 0.128 H0 0.112 –0.346 H0

(0.000) (0.356) (0.269)

The table is based on: (1) the whole sample period May 2004–April 2013; (2) the

pre-crisis period May 2006–Sept 2007 (17 months); (3) the common crisis period

October 2007–February 2009 (17 months). The table contains contemporaneous

correlation coefficients, as well as volatility-adjusted cross-correlation coefficients ˆ .VAρ

P-values are given in brackets. Fisher’s Z-statistic (1921) tests the null of no contagion.

The Student’s t critical value is 1.701 (at the 10% significance level).

Source: Olbrys and Majewska (2014b)

Table 3 Contemporaneous cross–correlations and volatility–adjusted cross–correlations

of weekly logarithmic returns on pairs S&P500/CEE stock market index

(excluding SAX)

Index

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

1 WIG 0.608 0.403 0.678 2.368 H1 0.372 –0.215 H0

(0.000) (0.000) (0.000)

2 PX 0.616 0.527 0.634 0.961 H0 0.336 –1.410 H0

(0.000) (0.000) (0.000)

Table 2 Contemporaneous cross–correlations and volatility–adjusted cross–correlations

of monthly logarithmic returns on pairs S&P500/CEE stock market index

(excluding SAX)

Index

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

1 WIG 0.767 0.438 0.850 2.081 H1 0.524 0.298 H0

(0.000) (0.079) (0.000)

2 PX 0.750 0.672 0.894 1.659 H0 0.606 –0.297 H0

(0.000) (0.003) (0.000)

3 BUX 0.744 0.405 0.817 1.900 H1 0.476 0.232 H0

(0.000) (0.107) (0.000)

4 SBI 0.414 0.114 0.408 0.843 H0 0.168 0.146 H0

TOP (0.000) (0.664) (0.104)

5 OMXV 0.465 0.145 0.653 1.679 H0 0.313 0.469 H0

(0.000) (0.580) (0.005)

6 OMXT 0.480 0.374 0.574 0.689 H0 0.258 –0.340 H0

(0.000) (0.140) (0.016)

7 OMXR 0.386 0.239 0.284 0.128 H0 0.112 –0.346 H0

(0.000) (0.356) (0.269)

The table is based on: (1) the whole sample period May 2004–April 2013; (2) the

pre-crisis period May 2006–Sept 2007 (17 months); (3) the common crisis period

October 2007–February 2009 (17 months). The table contains contemporaneous

correlation coefficients, as well as volatility-adjusted cross-correlation coefficients ˆ .VAρ

P-values are given in brackets. Fisher’s Z-statistic (1921) tests the null of no contagion.

The Student’s t critical value is 1.701 (at the 10% significance level).

Source: Olbrys and Majewska (2014b)

Table 3 Contemporaneous cross–correlations and volatility–adjusted cross–correlations

of weekly logarithmic returns on pairs S&P500/CEE stock market index

(excluding SAX)

Index

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

1 WIG 0.608 0.403 0.678 2.368 H1 0.372 –0.215 H0

(0.000) (0.000) (0.000)

2 PX 0.616 0.527 0.634 0.961 H0 0.336 –1.410 H0

(0.000) (0.000) (0.000)

134 J. Olbrys and E. Majewska

Table 3 Contemporaneous cross–correlations and volatility–adjusted cross–correlations

of weekly logarithmic returns on pairs S&P500/CEE stock market index

(excluding SAX) (continued)

Index

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

3 BUX 0.578 0.453 0.677 1.999 H1 0.372 –0.582 H0

(0.000) (0.000) (0.000)

4 SBI TOP 0.367 0.350 0.346 –0.031 H0 0.158 –1.227 H0

(0.000) (0.002) (0.002)

5 OMXV 0.388 0.266 0.399 0.890 H0 0.186 –0.503 H0

(0.000) (0.022) (0.000)

6 OMXT 0.395 0.309 0.349 0.269 H0 0.160 –0.940 H0

(0.000) (0.007) (0.002)

7 OMXR 0.215 0.237 0.327 0.579 H0 0.149 –0.547 H0

(0.000) (0.042) (0.004)

The table is based on:(1) the whole sample period May 2004–April 2013; (2) the

pre-crisis period May 2006–Sept 2007 (74 weeks); (3) the common crisis period October

2007–February 2009 (74 weeks). The table contains contemporaneous correlation

coefficients, as well as volatility-adjusted cross-correlation coefficients. P-values are

given in brackets. Fisher’s Z-statistic (1921) tests the null of no contagion. The Student’s

t critical value is 1.656 (at the 10% significance level).

Source: Authors’ calculations

Table 4 Contemporaneous cross–correlations and volatility–adjusted cross–correlations of

daily logarithmic returns on pairs S&P500/CEE stock market index (excluding SAX)

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

Index ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

1 WIG 0.476 0.334 0.498 2.458 H1 0.190 –1.897 H1

(0.000) (0.000) (0.000)

2 PX 0.435 0.385 0.446 0.907 H0 0.166 –2.936 H1

(0.000) (0.000) (0.000)

3 BUX 0.447 0.269 0.520 3.697 H1 0.201 –0.882 H0

(0.000) (0.000) (0.000)

4 SBI TOP 0.167 0.039 0.222 2.306 H1 0.077 0.471 H0

(0.000) (0.504) (0.000)

Table 3 Contemporaneous cross–correlations and volatility–adjusted cross–correlations

of weekly logarithmic returns on pairs S&P500/CEE stock market index

(excluding SAX) (continued)

Index

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

3 BUX 0.578 0.453 0.677 1.999 H1 0.372 –0.582 H0

(0.000) (0.000) (0.000)

4 SBI TOP 0.367 0.350 0.346 –0.031 H0 0.158 –1.227 H0

(0.000) (0.002) (0.002)

5 OMXV 0.388 0.266 0.399 0.890 H0 0.186 –0.503 H0

(0.000) (0.022) (0.000)

6 OMXT 0.395 0.309 0.349 0.269 H0 0.160 –0.940 H0

(0.000) (0.007) (0.002)

7 OMXR 0.215 0.237 0.327 0.579 H0 0.149 –0.547 H0

(0.000) (0.042) (0.004)

The table is based on:(1) the whole sample period May 2004–April 2013; (2) the

pre-crisis period May 2006–Sept 2007 (74 weeks); (3) the common crisis period October

2007–February 2009 (74 weeks). The table contains contemporaneous correlation

coefficients, as well as volatility-adjusted cross-correlation coefficients. P-values are

given in brackets. Fisher’s Z-statistic (1921) tests the null of no contagion. The Student’s

t critical value is 1.656 (at the 10% significance level).

Source: Authors’ calculations

Table 4 Contemporaneous cross–correlations and volatility–adjusted cross–correlations of

daily logarithmic returns on pairs S&P500/CEE stock market index (excluding SAX)

Contemporaneous cross-correlations

Volatility-adjusted

cross-correlations

Whole

sample

(1)

Pre-

crisis

(2) Crisis (3) Crisis (3)

Index ˆρ ˆPCρ ˆCρ Z-statistic Contagion ˆVAρ Z-statistic Contagion

1 WIG 0.476 0.334 0.498 2.458 H1 0.190 –1.897 H1

(0.000) (0.000) (0.000)

2 PX 0.435 0.385 0.446 0.907 H0 0.166 –2.936 H1

(0.000) (0.000) (0.000)

3 BUX 0.447 0.269 0.520 3.697 H1 0.201 –0.882 H0

(0.000) (0.000) (0.000)

4 SBI TOP 0.167 0.039 0.222 2.306 H1 0.077 0.471 H0

(0.000) (0.504) (0.000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.