Financial Crisis: Insurance Sector Perspective

VerifiedAdded on 2019/09/26

|11

|2363

|202

Essay

AI Summary

This essay examines the impact of the 2008 financial crisis on the insurance sector, focusing on the role of credit default swaps (CDS). It details how the crisis affected various segments, including US mortgage insurance companies, life insurance companies, financial guarantee insurance companies, and insurance-dominated financial groups like AIG. The essay highlights the significant losses incurred by these entities, particularly AIG's USD 60 billion loss in Q1 2009, leading to government intervention. Furthermore, it discusses lessons learned from the crisis, such as the importance of robust risk management, transparent valuations, and a more effective regulatory framework. The essay concludes by emphasizing the insurance sector's role as a shock absorber during the crisis, despite the challenges faced by specific segments, and the need for simpler structures and financial instruments to enhance transparency and reduce systemic risk.

Financial Crisis

- An Insurance Sector Perspective

1 | P a g e

- An Insurance Sector Perspective

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Page no.

I Introduction .. 3

II Credit Default Swaps – A build up to the crisis .. 3

III Impact on specific insurance sector segments and companies .. 4

IV Learnings from the after-effects .. 8

V Conclusion .. 9

2 | P a g e

Page no.

I Introduction .. 3

II Credit Default Swaps – A build up to the crisis .. 3

III Impact on specific insurance sector segments and companies .. 4

IV Learnings from the after-effects .. 8

V Conclusion .. 9

2 | P a g e

I. Introduction

The financial crisis seems to have had a minimal impact on the insurance sector vis-s-vis the

banking sector whose solvency was endangered. However, insurance sector has been affected in

adverse ways. This essay discusses the build-up of the financial crisis with a specific financial

instrument at the core of it in Section II, its impact on the specific insurance segments and

companies in the US in section III, some lessons learnt from this crisis in section IV. Section V

concludes.

II. Credit Default Swaps (CDS) – A build up to the crisis

Experts have presented a diverse view on the role of the insurance sector in the financial crisis

with some backing the insurance sector to cushion the volatility as against few experts blaming

the insurance product (CDS) as the root cause for the crisis. This is per views expressed by Chief

Executive of Allstate (an US insurance company) as below:

“It was, after all, an insurance product that contributed to the risk that almost brought down the global

economy. It should be no surprise that a big insurer like AIG would be a major issuer of credit default swap.

What is surprising is the claim that insurance did not contribute to the recent market failures, and therefore

insurers don’t need to consider how to prevent them from happening again.1”

At the epicenter of the crisis is the fundamental shift in the bank’s business model from their

core of tendering loans and holding them until maturity to distributing credit risks. These were

conceptualized through innovative financial instruments viz. Credit default Swaps (CDS). A

CDS is a bilateral agreement designed explicitly to shift credit risk between two parties. In a

CDS, one party (protection buyer) pays a periodic fee to another party (protection seller) in

return for compensation for default or similar credit event by a reference entity2. It is a particular

1 The New York Times, 2009

2 Panagiotis Papadopoulus

3 | P a g e

The financial crisis seems to have had a minimal impact on the insurance sector vis-s-vis the

banking sector whose solvency was endangered. However, insurance sector has been affected in

adverse ways. This essay discusses the build-up of the financial crisis with a specific financial

instrument at the core of it in Section II, its impact on the specific insurance segments and

companies in the US in section III, some lessons learnt from this crisis in section IV. Section V

concludes.

II. Credit Default Swaps (CDS) – A build up to the crisis

Experts have presented a diverse view on the role of the insurance sector in the financial crisis

with some backing the insurance sector to cushion the volatility as against few experts blaming

the insurance product (CDS) as the root cause for the crisis. This is per views expressed by Chief

Executive of Allstate (an US insurance company) as below:

“It was, after all, an insurance product that contributed to the risk that almost brought down the global

economy. It should be no surprise that a big insurer like AIG would be a major issuer of credit default swap.

What is surprising is the claim that insurance did not contribute to the recent market failures, and therefore

insurers don’t need to consider how to prevent them from happening again.1”

At the epicenter of the crisis is the fundamental shift in the bank’s business model from their

core of tendering loans and holding them until maturity to distributing credit risks. These were

conceptualized through innovative financial instruments viz. Credit default Swaps (CDS). A

CDS is a bilateral agreement designed explicitly to shift credit risk between two parties. In a

CDS, one party (protection buyer) pays a periodic fee to another party (protection seller) in

return for compensation for default or similar credit event by a reference entity2. It is a particular

1 The New York Times, 2009

2 Panagiotis Papadopoulus

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

type of swap designed to transfer the credit exposure of fixed income products between two or

more parties. The buyer of the swap makes payments to the swap’s seller up until the maturity

date of a contract. In return, the seller agrees that, in the event that the debt issuer defaults or

experiences another credit event, the seller will pay the buyer the security’s premium as well

all interest payments that would have been paid between that time and the security’s maturity

date3.

A covered CDS is wherein the protection buyer owns instruments issued by the reference entity.

Thus it helps the owner of the asset / instrument to manage the risk associated with the

investment which is similar to the insurance contract. In case the protection buyer does not own

particular reference obligation, the covered CDS engulfs the shape and form of a ‘naked’ CDS

thus divulging from the motive of insurance onto speculation4. If an insurer acts as a protection

seller, then it is exposed to a negative impact due to an increase in credit risk. Huge CDS losses

are inevitable against a fall in the value of a portfolio of mortgage-backed securities. Following

the subprime crisis, AIG’s credit portfolio depreciated by USD 11 billion in Q4 2008 with a loss

of USD 5.3 billion5. Numerous U.S. insurers have already begun to set up reserves for potential

claims following the financial crisis.

III. Impact on specific insurance sector segments and companies

a. US mortgage insurance companies:

The crisis began with the US residential mortgage market and these entities survival

hinged on mortgages retaining or increasing in value. Thus the US mortgage insurance

companies witnessed the brunt of the financial crisis, 2007. These insurance companies

3 Investopedia, 2015

4 New York State Insurance Department Circular Letter , 2008

5 Sjostrom, 2009

4 | P a g e

more parties. The buyer of the swap makes payments to the swap’s seller up until the maturity

date of a contract. In return, the seller agrees that, in the event that the debt issuer defaults or

experiences another credit event, the seller will pay the buyer the security’s premium as well

all interest payments that would have been paid between that time and the security’s maturity

date3.

A covered CDS is wherein the protection buyer owns instruments issued by the reference entity.

Thus it helps the owner of the asset / instrument to manage the risk associated with the

investment which is similar to the insurance contract. In case the protection buyer does not own

particular reference obligation, the covered CDS engulfs the shape and form of a ‘naked’ CDS

thus divulging from the motive of insurance onto speculation4. If an insurer acts as a protection

seller, then it is exposed to a negative impact due to an increase in credit risk. Huge CDS losses

are inevitable against a fall in the value of a portfolio of mortgage-backed securities. Following

the subprime crisis, AIG’s credit portfolio depreciated by USD 11 billion in Q4 2008 with a loss

of USD 5.3 billion5. Numerous U.S. insurers have already begun to set up reserves for potential

claims following the financial crisis.

III. Impact on specific insurance sector segments and companies

a. US mortgage insurance companies:

The crisis began with the US residential mortgage market and these entities survival

hinged on mortgages retaining or increasing in value. Thus the US mortgage insurance

companies witnessed the brunt of the financial crisis, 2007. These insurance companies

3 Investopedia, 2015

4 New York State Insurance Department Circular Letter , 2008

5 Sjostrom, 2009

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

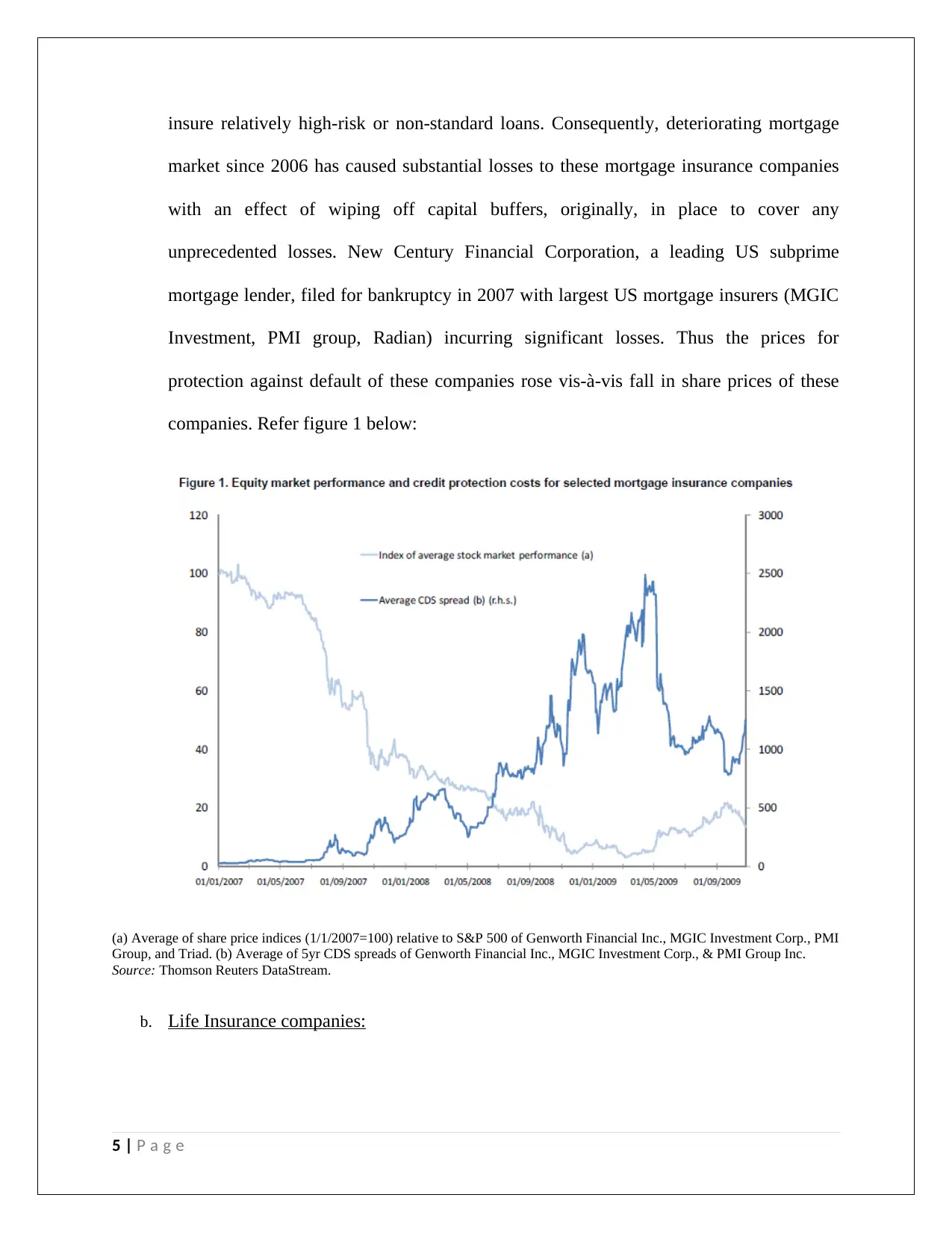

insure relatively high-risk or non-standard loans. Consequently, deteriorating mortgage

market since 2006 has caused substantial losses to these mortgage insurance companies

with an effect of wiping off capital buffers, originally, in place to cover any

unprecedented losses. New Century Financial Corporation, a leading US subprime

mortgage lender, filed for bankruptcy in 2007 with largest US mortgage insurers (MGIC

Investment, PMI group, Radian) incurring significant losses. Thus the prices for

protection against default of these companies rose vis-à-vis fall in share prices of these

companies. Refer figure 1 below:

(a) Average of share price indices (1/1/2007=100) relative to S&P 500 of Genworth Financial Inc., MGIC Investment Corp., PMI

Group, and Triad. (b) Average of 5yr CDS spreads of Genworth Financial Inc., MGIC Investment Corp., & PMI Group Inc.

Source: Thomson Reuters DataStream.

b. Life Insurance companies:

5 | P a g e

market since 2006 has caused substantial losses to these mortgage insurance companies

with an effect of wiping off capital buffers, originally, in place to cover any

unprecedented losses. New Century Financial Corporation, a leading US subprime

mortgage lender, filed for bankruptcy in 2007 with largest US mortgage insurers (MGIC

Investment, PMI group, Radian) incurring significant losses. Thus the prices for

protection against default of these companies rose vis-à-vis fall in share prices of these

companies. Refer figure 1 below:

(a) Average of share price indices (1/1/2007=100) relative to S&P 500 of Genworth Financial Inc., MGIC Investment Corp., PMI

Group, and Triad. (b) Average of 5yr CDS spreads of Genworth Financial Inc., MGIC Investment Corp., & PMI Group Inc.

Source: Thomson Reuters DataStream.

b. Life Insurance companies:

5 | P a g e

Life insurance companies have lower exposure to lesser rated mortgage backed securities.

They generally invest in equity and corporate bond markets. The financial crisis led to

lower valuations of these equities and corporate bonds. Thus a lower bond interests

implies a significant increase in actuarial liability levels.

Life insurance companies have annuities contracts and guarantees to fulfill couples with

deteriorating bond interest rates stretched the credit risk exposure of these companies

along with asset-liability management challenges. Further, hedging positions turned

costly owing to heightened market volatility. However, the only continuing boon for life

insurance companies is that they continue to face lower liquidity risk as compared with

banks and financial institutions. They would be prone to ratings downgrades thus

increasing their appetite for higher liquidity. The financial stress at these life insurance

companies would reflect in lower confidence of policy-holders’ in these companies

resulting in annulment of contract from their end even though such action will entail

termination fees and investment losses.

c. Financial guarantee insurance companies:

Financial guarantee insurance companies lost their AAA ratings status, which was their

core of business model. These companies tend to be highly leveraged institutions and

their business model revolves around lending their high rating to lower rated debt issuers

and guaranteeing interest and principal repayment obligations. With their own ratings

downgraded, their share prices plummeted with a rise in premium to cover credit default

of such financial guarantee insurance companies. The difficulties experienced by these

entities would adversely affect the financial markets through different channels. The

6 | P a g e

They generally invest in equity and corporate bond markets. The financial crisis led to

lower valuations of these equities and corporate bonds. Thus a lower bond interests

implies a significant increase in actuarial liability levels.

Life insurance companies have annuities contracts and guarantees to fulfill couples with

deteriorating bond interest rates stretched the credit risk exposure of these companies

along with asset-liability management challenges. Further, hedging positions turned

costly owing to heightened market volatility. However, the only continuing boon for life

insurance companies is that they continue to face lower liquidity risk as compared with

banks and financial institutions. They would be prone to ratings downgrades thus

increasing their appetite for higher liquidity. The financial stress at these life insurance

companies would reflect in lower confidence of policy-holders’ in these companies

resulting in annulment of contract from their end even though such action will entail

termination fees and investment losses.

c. Financial guarantee insurance companies:

Financial guarantee insurance companies lost their AAA ratings status, which was their

core of business model. These companies tend to be highly leveraged institutions and

their business model revolves around lending their high rating to lower rated debt issuers

and guaranteeing interest and principal repayment obligations. With their own ratings

downgraded, their share prices plummeted with a rise in premium to cover credit default

of such financial guarantee insurance companies. The difficulties experienced by these

entities would adversely affect the financial markets through different channels. The

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

insurance regulation in the US resides with the respective states. The New York State

insurance regulator has been closing the written contract with the counterparts of the

financial guarantors with an aim to provide financial restructure assistance to these

guarantors’ insurance companies.

d. Insurance-Dominated financial groups

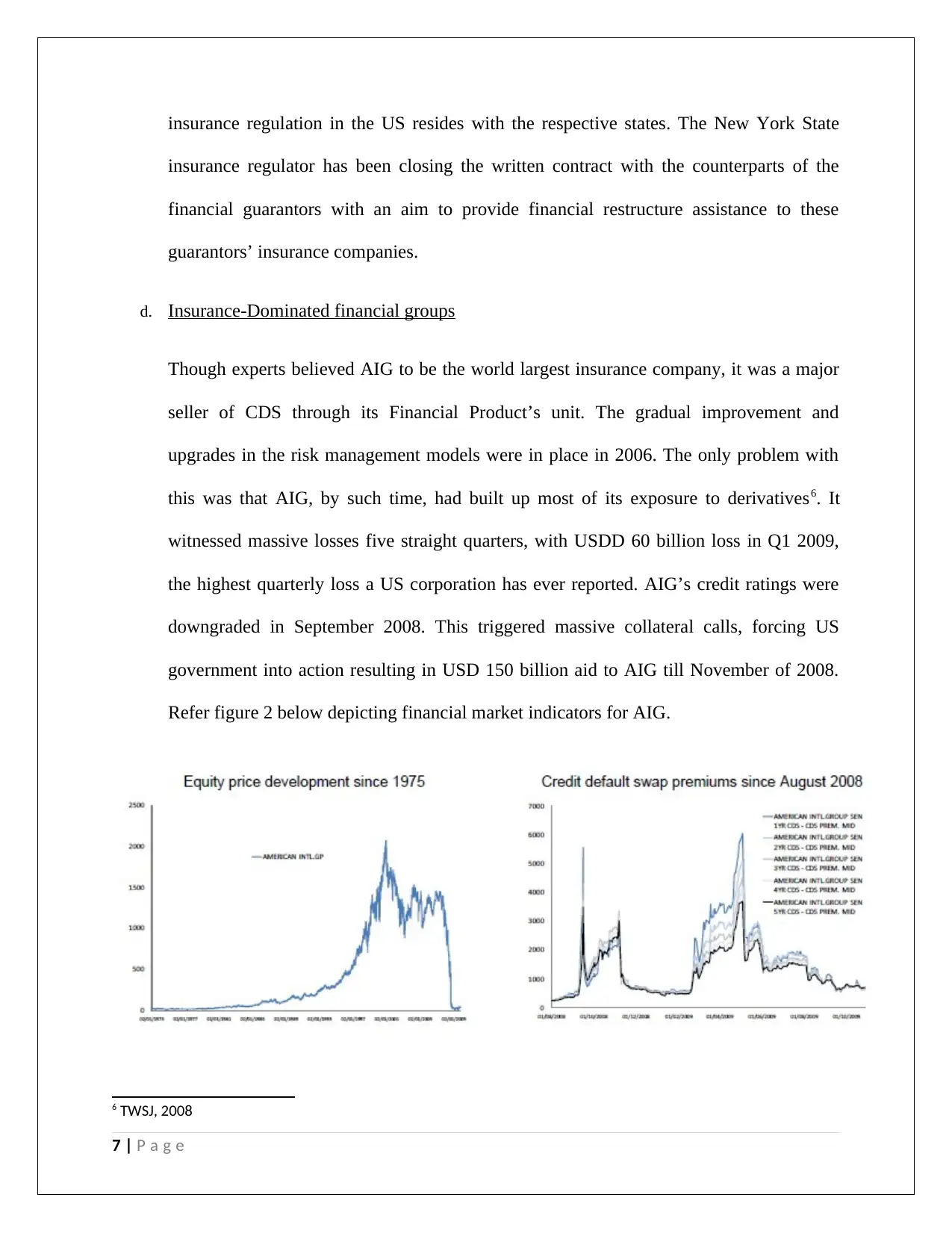

Though experts believed AIG to be the world largest insurance company, it was a major

seller of CDS through its Financial Product’s unit. The gradual improvement and

upgrades in the risk management models were in place in 2006. The only problem with

this was that AIG, by such time, had built up most of its exposure to derivatives6. It

witnessed massive losses five straight quarters, with USDD 60 billion loss in Q1 2009,

the highest quarterly loss a US corporation has ever reported. AIG’s credit ratings were

downgraded in September 2008. This triggered massive collateral calls, forcing US

government into action resulting in USD 150 billion aid to AIG till November of 2008.

Refer figure 2 below depicting financial market indicators for AIG.

6 TWSJ, 2008

7 | P a g e

insurance regulator has been closing the written contract with the counterparts of the

financial guarantors with an aim to provide financial restructure assistance to these

guarantors’ insurance companies.

d. Insurance-Dominated financial groups

Though experts believed AIG to be the world largest insurance company, it was a major

seller of CDS through its Financial Product’s unit. The gradual improvement and

upgrades in the risk management models were in place in 2006. The only problem with

this was that AIG, by such time, had built up most of its exposure to derivatives6. It

witnessed massive losses five straight quarters, with USDD 60 billion loss in Q1 2009,

the highest quarterly loss a US corporation has ever reported. AIG’s credit ratings were

downgraded in September 2008. This triggered massive collateral calls, forcing US

government into action resulting in USD 150 billion aid to AIG till November of 2008.

Refer figure 2 below depicting financial market indicators for AIG.

6 TWSJ, 2008

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Source: Thomson Reuters DataStream

AIG was a significant counter party to systemically important banks. (The likes of Goldman

Sachs, Societe Generale, Deutsche Bank, BoA, Barclays and so on). Thus AIG itself was

being considered systemically important. Thus there was a focus-shift of government aid in

terms of liquidity infusion measures from banking companies and financial institutions to

insurance companies.

IV. Learnings from the after-effects

Insurance companies are financial institutions which operate with a longer term liabilities than

commercial and investment banks. Hence, they have the capacity to adopt investment strategies

with longer-term horizons. This in effect is a stabilizing catalyst in the financial system.

Moreover, since they cover a variety of hazards, they have the ability to reinvest the proceeds in

financial assets.

The crisis has highlighted issues related to valuation of securities in a low liquid market scenario.

With liquidity evaporating from the markets, valuations methodologies observes a shift from

observable inputs to unobservable inputs. Thus market participants failed to correctly value the

financial health of institutions. Questions are being raised on the efficacy of the accounting rules

in ensuring transparent valuation of assets of all types of financial institutions.

Despite insurance companies have relatively stable flow of income through premium collection;

they are not completely immune to liquidity risks. During crisis, insurance companies face rating

downgrades leading to collateral calls and subsequently demand for liquid money. With credit

lines drying up from the already stressed banking sector, owing to crisis, central banks would

have to intervene to provide liquidity support. This was witnessed with AIG which was the first

financial conglomerate to received US government aid.

8 | P a g e

AIG was a significant counter party to systemically important banks. (The likes of Goldman

Sachs, Societe Generale, Deutsche Bank, BoA, Barclays and so on). Thus AIG itself was

being considered systemically important. Thus there was a focus-shift of government aid in

terms of liquidity infusion measures from banking companies and financial institutions to

insurance companies.

IV. Learnings from the after-effects

Insurance companies are financial institutions which operate with a longer term liabilities than

commercial and investment banks. Hence, they have the capacity to adopt investment strategies

with longer-term horizons. This in effect is a stabilizing catalyst in the financial system.

Moreover, since they cover a variety of hazards, they have the ability to reinvest the proceeds in

financial assets.

The crisis has highlighted issues related to valuation of securities in a low liquid market scenario.

With liquidity evaporating from the markets, valuations methodologies observes a shift from

observable inputs to unobservable inputs. Thus market participants failed to correctly value the

financial health of institutions. Questions are being raised on the efficacy of the accounting rules

in ensuring transparent valuation of assets of all types of financial institutions.

Despite insurance companies have relatively stable flow of income through premium collection;

they are not completely immune to liquidity risks. During crisis, insurance companies face rating

downgrades leading to collateral calls and subsequently demand for liquid money. With credit

lines drying up from the already stressed banking sector, owing to crisis, central banks would

have to intervene to provide liquidity support. This was witnessed with AIG which was the first

financial conglomerate to received US government aid.

8 | P a g e

Problems for large conglomerate arise from the financial product’s unit that operates in capital

markets providing credit protection. Losses for AIG mounted at its financial product’s unit were

so massive that it camouflaged its diversified revenue sources. Thus there is a need for a well-

functioning internal controls system, corporate governance and risk management in these

companies and regulatory and supervisory framework at a macro level.

A way ahead for large conglomerates would be to re-analyze the benefits of insurance companies

expanding their business into banking or commercial or investment activities. AIG’s federal

support involved a planned break-up into separate divisions.

The crisis has called for a lesser complex financial instruments and institutional structures. A

large conglomerate, with various divisions, operates out of one common capital base. This

capital base is raised by all the various divisions combined, but a particular division may have

access to capital raised by a less risky division leading to cross-subsidization of risk exposure at

the divisional level. Thus a regulatory framework needs to be in place to segregate capital for

different type of uses. A simple financial instrument would be easily valued leading to

transparent valuations of financial institutions. This will assist in reducing uncertainties in the

valuation of banks themselves.

The crisis calls for an intra organizational supervision, governance and information sharing

leading to close scrutiny of the activities. This needs to be gradually expanded at inter

organizational, national and international level as well.

V. Conclusion

The financial crisis was seen more as the one impacting the banking and financial sectors.

However, it has reflected a more visible effect on the insurance sector. Even though the trigger of

the crisis lay at US mortgage market and subsequent failure of CDS arrangements, the far

9 | P a g e

markets providing credit protection. Losses for AIG mounted at its financial product’s unit were

so massive that it camouflaged its diversified revenue sources. Thus there is a need for a well-

functioning internal controls system, corporate governance and risk management in these

companies and regulatory and supervisory framework at a macro level.

A way ahead for large conglomerates would be to re-analyze the benefits of insurance companies

expanding their business into banking or commercial or investment activities. AIG’s federal

support involved a planned break-up into separate divisions.

The crisis has called for a lesser complex financial instruments and institutional structures. A

large conglomerate, with various divisions, operates out of one common capital base. This

capital base is raised by all the various divisions combined, but a particular division may have

access to capital raised by a less risky division leading to cross-subsidization of risk exposure at

the divisional level. Thus a regulatory framework needs to be in place to segregate capital for

different type of uses. A simple financial instrument would be easily valued leading to

transparent valuations of financial institutions. This will assist in reducing uncertainties in the

valuation of banks themselves.

The crisis calls for an intra organizational supervision, governance and information sharing

leading to close scrutiny of the activities. This needs to be gradually expanded at inter

organizational, national and international level as well.

V. Conclusion

The financial crisis was seen more as the one impacting the banking and financial sectors.

However, it has reflected a more visible effect on the insurance sector. Even though the trigger of

the crisis lay at US mortgage market and subsequent failure of CDS arrangements, the far

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reaching effects on the market volatility and investment portfolios have rendered adverse effect

on insurance companies.

The position for underwriting is uncertain, but not all negative as the crisis have changed the

behaviors and demand for specific types of financial products. This is a positive for life

insurance companies.

The crisis has shown that insurance companies, which were once expected to be immune to

liquidity risks, may have to witness liquidity crisis more than what their risk management models

have factored. Thus liquidity risk is becoming more of an issue for some insurance companies.

Further, it has surfaces the ideology that one unit may endanger the survival of the entire

organization. Hence there is a need for a simpler structure which enables insurance companies to

focus on their core business models and enabling investors to judge the risk exposure for an

insurer.

It is imperative to note that the insurance, excluding certain insurance segments, overall the

insurance sector have played a role of a shock-absorber during financial crisis. With lower

liquidity and lower leveraged positions, insurance companies didn’t require to force-sell their

investments. Moreover, steady flow of premium from the market participants to the insurance

companies implied that these were re-invested in financial assets helping them to support their

prices.

10 | P a g e

on insurance companies.

The position for underwriting is uncertain, but not all negative as the crisis have changed the

behaviors and demand for specific types of financial products. This is a positive for life

insurance companies.

The crisis has shown that insurance companies, which were once expected to be immune to

liquidity risks, may have to witness liquidity crisis more than what their risk management models

have factored. Thus liquidity risk is becoming more of an issue for some insurance companies.

Further, it has surfaces the ideology that one unit may endanger the survival of the entire

organization. Hence there is a need for a simpler structure which enables insurance companies to

focus on their core business models and enabling investors to judge the risk exposure for an

insurer.

It is imperative to note that the insurance, excluding certain insurance segments, overall the

insurance sector have played a role of a shock-absorber during financial crisis. With lower

liquidity and lower leveraged positions, insurance companies didn’t require to force-sell their

investments. Moreover, steady flow of premium from the market participants to the insurance

companies implied that these were re-invested in financial assets helping them to support their

prices.

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Anon, 2008, Faulty computer models helped sink giant AIG, [Online], Available at

http://www.jstic.com/Newsgroup/WSJE/2008/WSJEWJ_November_3nd.pdf, [Accessed date

10th December 2015]

Anon, N.D., Credit Default Swap – CDS, [Online], Available at

http://www.investopedia.com/terms/c/creditdefaultswap.asp, [Accessed date 10th December

2015]

Eric Dinallo, New York State Insurance Department Circular Letter No. 19, [Online], Available

at http://www.dfs.ny.gov/insurance/circltr/2008/cl08_19.htm, [Accessed date 10th December

2015]

Papadopoulus , PP, 2010. Credit Default Swaps - Pricing, Valuation and Investment

Applications, 1.

Tom Wilson, 2009, Regulate Me, Please, [Online}, Available at

http://www.nytimes.com/2009/04/16/opinion/16wilson.html?_r=0, [Access date 10th Dec 2015]

William K. Sjostrum, Jr.,2009, The AIG Bailout, 66 Wash. & Lee L. Rev. 943, Available at

http://scholarlycommons.law.wlu.edu/wlulr/vol66/iss3/2., [Accessed date 10th December 2015]

11 | P a g e

Anon, 2008, Faulty computer models helped sink giant AIG, [Online], Available at

http://www.jstic.com/Newsgroup/WSJE/2008/WSJEWJ_November_3nd.pdf, [Accessed date

10th December 2015]

Anon, N.D., Credit Default Swap – CDS, [Online], Available at

http://www.investopedia.com/terms/c/creditdefaultswap.asp, [Accessed date 10th December

2015]

Eric Dinallo, New York State Insurance Department Circular Letter No. 19, [Online], Available

at http://www.dfs.ny.gov/insurance/circltr/2008/cl08_19.htm, [Accessed date 10th December

2015]

Papadopoulus , PP, 2010. Credit Default Swaps - Pricing, Valuation and Investment

Applications, 1.

Tom Wilson, 2009, Regulate Me, Please, [Online}, Available at

http://www.nytimes.com/2009/04/16/opinion/16wilson.html?_r=0, [Access date 10th Dec 2015]

William K. Sjostrum, Jr.,2009, The AIG Bailout, 66 Wash. & Lee L. Rev. 943, Available at

http://scholarlycommons.law.wlu.edu/wlulr/vol66/iss3/2., [Accessed date 10th December 2015]

11 | P a g e

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.