Critical Analysis: Market Failure & Bias in the 2008 Crisis

VerifiedAdded on 2023/06/15

|14

|3445

|125

Essay

AI Summary

This essay critically assesses the extent to which market failure and behavioral biases explain the 2008 financial crisis in the United States. It begins by providing a background of the crisis, highlighting the role of mortgage-backed securities and collateralized debt obligations. The analysis then focuses on market failures such as monopolies in credit rating agencies and asymmetric information regarding the quality of sub-prime mortgages. It further explores behavioral biases, including confirmation bias and overconfidence, that contributed to the crisis. The essay also touches upon the efficient market hypothesis and moral hazard, concluding that a combination of market imperfections and behavioral factors played a significant role in the crisis.

Running head: INVESTING AND FINANCIAL MARKETS

Investing and Financial Markets

University Name

Student Name

Authors’ Note

Investing and Financial Markets

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INVESTING AND FINANCIAL MARKETS

Table of Contents

1. Objective................................................................................................................................2

2. Introduction............................................................................................................................2

3. Background of the global financial crisis of 2008.................................................................3

4. Market Failure and Financial Crisis of the year 2008............................................................5

4.1 Monopoly.............................................................................................................................5

4.2 Asymmetric Information......................................................................................................7

5. Behavioural Bias Theory and Financial Crisis of the year 2008...........................................8

5.1 Confirmation Bias................................................................................................................8

5.2 Overconfidence....................................................................................................................9

6. Conclusion..............................................................................................................................9

References................................................................................................................................11

INVESTING AND FINANCIAL MARKETS

Table of Contents

1. Objective................................................................................................................................2

2. Introduction............................................................................................................................2

3. Background of the global financial crisis of 2008.................................................................3

4. Market Failure and Financial Crisis of the year 2008............................................................5

4.1 Monopoly.............................................................................................................................5

4.2 Asymmetric Information......................................................................................................7

5. Behavioural Bias Theory and Financial Crisis of the year 2008...........................................8

5.1 Confirmation Bias................................................................................................................8

5.2 Overconfidence....................................................................................................................9

6. Conclusion..............................................................................................................................9

References................................................................................................................................11

3

INVESTING AND FINANCIAL MARKETS

Topic: Critical assessment of the extent to which market failure and behavioural bias

can explicate current financial crisis, referring to substantiation from at least one

current financial crisis

1. Objective

The purpose of the current study at hand is to elucidate in detail the financial crisis of the year

2008 in the USA by utilizing market failure as well as behavioural bias to illustrate the said

crisis. By comprehending the causes behind the financial crisis can help in prevention of

occurrence of financial crisis in the upcoming period (Goh et al. 2015).

2. Introduction

The current study elucidates in detail about the financial crisis of the year 2007 and 2008 is

also referred to as worldwide financial crisis. The financial crisis of the year 2008 can be

regarded by many economists to have worst financial crisis since the period of Great

Depression of the year 1930s. The study throws light on the risk taking behaviour, excessive

leverage of different US banks, excessive bail outs of various financial institutions, effects of

quantitative easing strategies in addition to different asset relief programme that augmented

the financial crisis of 2008.

3. Background of the global financial crisis of 2008

Subsequent to the Second World War, government of United States became interested in re-

establishing the domestic economy as well as generating new housing grounds. Thus,

America introduced a mechanism of lending, also referred to as mortgage. This mechanism

refers to a legal contract between two different parties that transfers property ownership to a

particular lender as a specific security for acquirement of loans (Armantier et al. 2015). In

essence, a mortgage permits one to loan money from a particular bank otherwise other

INVESTING AND FINANCIAL MARKETS

Topic: Critical assessment of the extent to which market failure and behavioural bias

can explicate current financial crisis, referring to substantiation from at least one

current financial crisis

1. Objective

The purpose of the current study at hand is to elucidate in detail the financial crisis of the year

2008 in the USA by utilizing market failure as well as behavioural bias to illustrate the said

crisis. By comprehending the causes behind the financial crisis can help in prevention of

occurrence of financial crisis in the upcoming period (Goh et al. 2015).

2. Introduction

The current study elucidates in detail about the financial crisis of the year 2007 and 2008 is

also referred to as worldwide financial crisis. The financial crisis of the year 2008 can be

regarded by many economists to have worst financial crisis since the period of Great

Depression of the year 1930s. The study throws light on the risk taking behaviour, excessive

leverage of different US banks, excessive bail outs of various financial institutions, effects of

quantitative easing strategies in addition to different asset relief programme that augmented

the financial crisis of 2008.

3. Background of the global financial crisis of 2008

Subsequent to the Second World War, government of United States became interested in re-

establishing the domestic economy as well as generating new housing grounds. Thus,

America introduced a mechanism of lending, also referred to as mortgage. This mechanism

refers to a legal contract between two different parties that transfers property ownership to a

particular lender as a specific security for acquirement of loans (Armantier et al. 2015). In

essence, a mortgage permits one to loan money from a particular bank otherwise other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

INVESTING AND FINANCIAL MARKETS

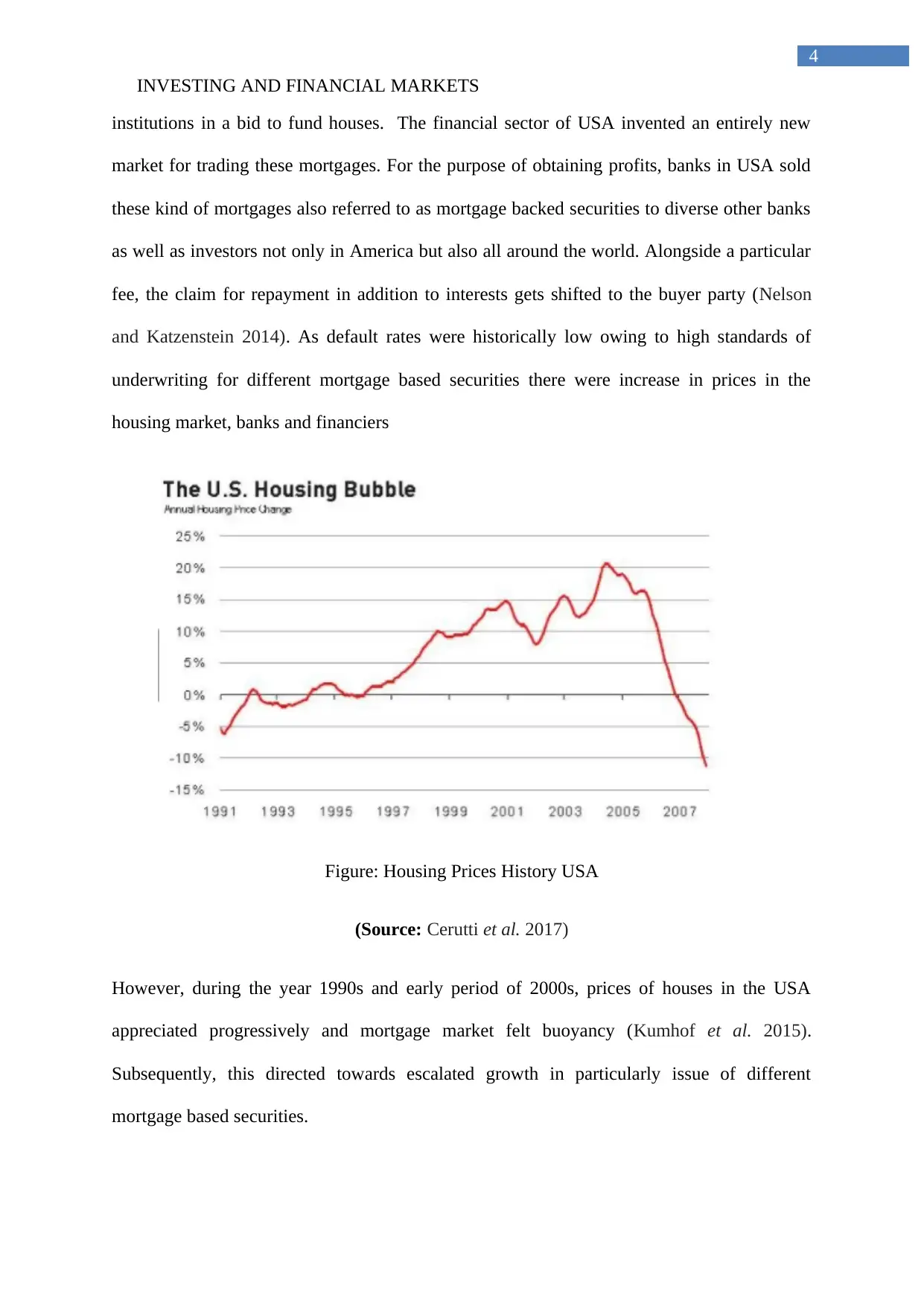

institutions in a bid to fund houses. The financial sector of USA invented an entirely new

market for trading these mortgages. For the purpose of obtaining profits, banks in USA sold

these kind of mortgages also referred to as mortgage backed securities to diverse other banks

as well as investors not only in America but also all around the world. Alongside a particular

fee, the claim for repayment in addition to interests gets shifted to the buyer party (Nelson

and Katzenstein 2014). As default rates were historically low owing to high standards of

underwriting for different mortgage based securities there were increase in prices in the

housing market, banks and financiers

Figure: Housing Prices History USA

(Source: Cerutti et al. 2017)

However, during the year 1990s and early period of 2000s, prices of houses in the USA

appreciated progressively and mortgage market felt buoyancy (Kumhof et al. 2015).

Subsequently, this directed towards escalated growth in particularly issue of different

mortgage based securities.

INVESTING AND FINANCIAL MARKETS

institutions in a bid to fund houses. The financial sector of USA invented an entirely new

market for trading these mortgages. For the purpose of obtaining profits, banks in USA sold

these kind of mortgages also referred to as mortgage backed securities to diverse other banks

as well as investors not only in America but also all around the world. Alongside a particular

fee, the claim for repayment in addition to interests gets shifted to the buyer party (Nelson

and Katzenstein 2014). As default rates were historically low owing to high standards of

underwriting for different mortgage based securities there were increase in prices in the

housing market, banks and financiers

Figure: Housing Prices History USA

(Source: Cerutti et al. 2017)

However, during the year 1990s and early period of 2000s, prices of houses in the USA

appreciated progressively and mortgage market felt buoyancy (Kumhof et al. 2015).

Subsequently, this directed towards escalated growth in particularly issue of different

mortgage based securities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

INVESTING AND FINANCIAL MARKETS

As rightly indicated by Leamer (2015), investment banks purchased mortgages from various

issuers of mortgage particularly in the growth phase of house prices. In actual fact, there was

comparatively lesser number of new mortgages to securitize. Thereafter, traders began

explore repackaging the MBSs along with other forms of debt. Nevertheless, the latter

category of repackaging is a specific form of financial instrument that is also referred to as

CDOs (collaterised debt obligations). As suggested by Rey (2015), CDOs are essentially

securities that comprise of diverse kinds of debt, namely MBSs as well as corporate bonds

that gets repackaged into a specific product and marketed to financiers in the secondary

market. As per suppositions, the notion of pooling together varied categories of debt can

lessen overall risk. These kind of repackaged assets have the need to be comparatively safe,

although in actual fact, most of repackaged debt comprised of mortgages of inferior quality.

In essence, these mortgaged were specifically loans that were sanctioned to different

borrowers with low rating of credit and poor history of credit (that is to say sub-prime

mortgages) (Balakrishnan et al. 2016). Regardless of these identified issues, majority of the

rating agencies, counting Standard & Poor’s, Fitch Rating as well as Moody’s Investor

Service were providing top rating of AAA to MBSs as well as CDOs.

4. Market Failure and Financial Crisis of the year 2008

Market failure primarily takes place at the time when freely functioning markets fail to

deliver an effectual else wise socially optimal allotment of scarce resources. As rightly

indicated by Bech et al. (2014), four different states of affairs that can signify market failures

include asymmetric information, public goods, situation of monopoly in addition to different

external effects. However, the current segment under consideration takes account of influence

of monopoly along with asymmetric information on particularly financial crisis of United

States.

INVESTING AND FINANCIAL MARKETS

As rightly indicated by Leamer (2015), investment banks purchased mortgages from various

issuers of mortgage particularly in the growth phase of house prices. In actual fact, there was

comparatively lesser number of new mortgages to securitize. Thereafter, traders began

explore repackaging the MBSs along with other forms of debt. Nevertheless, the latter

category of repackaging is a specific form of financial instrument that is also referred to as

CDOs (collaterised debt obligations). As suggested by Rey (2015), CDOs are essentially

securities that comprise of diverse kinds of debt, namely MBSs as well as corporate bonds

that gets repackaged into a specific product and marketed to financiers in the secondary

market. As per suppositions, the notion of pooling together varied categories of debt can

lessen overall risk. These kind of repackaged assets have the need to be comparatively safe,

although in actual fact, most of repackaged debt comprised of mortgages of inferior quality.

In essence, these mortgaged were specifically loans that were sanctioned to different

borrowers with low rating of credit and poor history of credit (that is to say sub-prime

mortgages) (Balakrishnan et al. 2016). Regardless of these identified issues, majority of the

rating agencies, counting Standard & Poor’s, Fitch Rating as well as Moody’s Investor

Service were providing top rating of AAA to MBSs as well as CDOs.

4. Market Failure and Financial Crisis of the year 2008

Market failure primarily takes place at the time when freely functioning markets fail to

deliver an effectual else wise socially optimal allotment of scarce resources. As rightly

indicated by Bech et al. (2014), four different states of affairs that can signify market failures

include asymmetric information, public goods, situation of monopoly in addition to different

external effects. However, the current segment under consideration takes account of influence

of monopoly along with asymmetric information on particularly financial crisis of United

States.

6

INVESTING AND FINANCIAL MARKETS

4.1 Monopoly

Treeck (2014) says this kind of market failure is effectually collusion otherwise abuse of

power ensuing from concentrated market. At a time when there is small number of

corporations in a specific market, they might perhaps select to operate together to enhance

their joint powers and exploit consumers in the market. As suggested by Goh et al. (2015),

market failure originating from insufficient competition is mainly owing to supremacy of

monopolies in the market economy. An important nature as well as characteristic of

monopoly is essentially the presence high barriers to enter a specific industry/segment.

Fundamentally, subsistence of monopoly in specific markets of US also contributed to certain

extent to the financial crisis of the year 2008. As mentioned above in the study, major credit

rating agencies were endowing asset based securities with AAA rating. In essence, the big

credit rating agencies operated in an oligopoly market for rating agencies and had an

advantaged position given by the regulators of the financial market. Also they acquired

immunity from different legal prosecution over their presented ratings. In the period of 2008

crisis, business of repackaging as well as selling debts comprising of sub-prime mortgages

were operating effectually (Armantier et al. 2015). In addition to this, the big credit rating

agencies also became financially enthused to issue high ratings to these sorts of assets since

they generated earnings by means of such kinds of securities. In addition to this, banks also

started channelizing more money to fund home buyers belonging to low income categories

(with low credit rating). However, this led to a vicious cycle and led to the burst of the

housing bubble. With the burst of the housing bubble and defaults of mortgage loans, huge

losses were encountered and institutional financiers holding these kinds of assets suffered

huge amounts of losses (Nelson and Katzenstein 2014).

As mentioned by Leamer (2015), the mortgage market in US consisted of both primary as

well as secondary market. Essentially, loans derived from different financial institutions

INVESTING AND FINANCIAL MARKETS

4.1 Monopoly

Treeck (2014) says this kind of market failure is effectually collusion otherwise abuse of

power ensuing from concentrated market. At a time when there is small number of

corporations in a specific market, they might perhaps select to operate together to enhance

their joint powers and exploit consumers in the market. As suggested by Goh et al. (2015),

market failure originating from insufficient competition is mainly owing to supremacy of

monopolies in the market economy. An important nature as well as characteristic of

monopoly is essentially the presence high barriers to enter a specific industry/segment.

Fundamentally, subsistence of monopoly in specific markets of US also contributed to certain

extent to the financial crisis of the year 2008. As mentioned above in the study, major credit

rating agencies were endowing asset based securities with AAA rating. In essence, the big

credit rating agencies operated in an oligopoly market for rating agencies and had an

advantaged position given by the regulators of the financial market. Also they acquired

immunity from different legal prosecution over their presented ratings. In the period of 2008

crisis, business of repackaging as well as selling debts comprising of sub-prime mortgages

were operating effectually (Armantier et al. 2015). In addition to this, the big credit rating

agencies also became financially enthused to issue high ratings to these sorts of assets since

they generated earnings by means of such kinds of securities. In addition to this, banks also

started channelizing more money to fund home buyers belonging to low income categories

(with low credit rating). However, this led to a vicious cycle and led to the burst of the

housing bubble. With the burst of the housing bubble and defaults of mortgage loans, huge

losses were encountered and institutional financiers holding these kinds of assets suffered

huge amounts of losses (Nelson and Katzenstein 2014).

As mentioned by Leamer (2015), the mortgage market in US consisted of both primary as

well as secondary market. Essentially, loans derived from different financial institutions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

INVESTING AND FINANCIAL MARKETS

namely banks were part of the primary market. However, these financial institutions were

capable of obtaining finances they loan particularly from secondary markets. In addition to

this, there were two different government backed units that in fact monopolised the entire

secondary mortgage market, (that is to say, The Federal Mortgage Association along with

The Federal Home Loan Mortgage Corporation). With the support of the government of the

United States, these two institutions started to acquire finances at lower rates in comparison

to other financial institutions (Balakrishnan et al. 2016). In actual fact, this benefit of

acquiring funds helped them to dominate the entire secondary market by buying huge

amounts of mortgage backed securities comprising of mainly the sub-prime mortgage.

Nonetheless, at the time when prices of housing dropped and purchasers defaulted, both the

said institutions encountered huge amount of losses in particularly mortgage security (Bech et

al. 2014). This directed the government to bail them out for preventing worsening of the

crisis situation and cease bleeding of the housing market, financial system and the entire

economy.

4.2 Asymmetric Information

As suggested by Leamer (2015), this type of failure of the market persists at the time when a

specific individual or else a party has supplementary information than other individuals or

else party and utilizes that benefit for exploitation of the other party. In essence, finance is a

market in specifically information time and again on the probability that they will be able to

repay loan than the lender.

With regard to financial crisis of 2008, the investment banks were marketing sub-prime

mortgages based securities were aware of subsistence of inferior quality in the assets.

Nevertheless, in a bid to boost profits, they were ahead to market the securities to financiers

that did not have inside information regarding problematic assets (Cerutti et al. 2017). In

INVESTING AND FINANCIAL MARKETS

namely banks were part of the primary market. However, these financial institutions were

capable of obtaining finances they loan particularly from secondary markets. In addition to

this, there were two different government backed units that in fact monopolised the entire

secondary mortgage market, (that is to say, The Federal Mortgage Association along with

The Federal Home Loan Mortgage Corporation). With the support of the government of the

United States, these two institutions started to acquire finances at lower rates in comparison

to other financial institutions (Balakrishnan et al. 2016). In actual fact, this benefit of

acquiring funds helped them to dominate the entire secondary market by buying huge

amounts of mortgage backed securities comprising of mainly the sub-prime mortgage.

Nonetheless, at the time when prices of housing dropped and purchasers defaulted, both the

said institutions encountered huge amount of losses in particularly mortgage security (Bech et

al. 2014). This directed the government to bail them out for preventing worsening of the

crisis situation and cease bleeding of the housing market, financial system and the entire

economy.

4.2 Asymmetric Information

As suggested by Leamer (2015), this type of failure of the market persists at the time when a

specific individual or else a party has supplementary information than other individuals or

else party and utilizes that benefit for exploitation of the other party. In essence, finance is a

market in specifically information time and again on the probability that they will be able to

repay loan than the lender.

With regard to financial crisis of 2008, the investment banks were marketing sub-prime

mortgages based securities were aware of subsistence of inferior quality in the assets.

Nevertheless, in a bid to boost profits, they were ahead to market the securities to financiers

that did not have inside information regarding problematic assets (Cerutti et al. 2017). In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

INVESTING AND FINANCIAL MARKETS

essence, they bought the said assets endowed with high rating assurance by major credit

rating agencies, thinking they were protected investments.

However, in this context it can be hereby stated that availability of more accurate information

particularly financial markets could have assisted financiers to know more in detail about

lethal nature of investment assets. They could have known in detail about sub-prime

mortgages and would be less keen to invest in the same. In case if the banks were unable to

market investment products, they would have lesser funds at their disposal (Nelson and

Katzenstein 2014). Subsequently less credit would be available to different purchasers with

low income as well as poor profiles of credit. Essentially, this could have prevented

plummeting of sub-prime mortgages and housing bubble burst.

4.3 Market Efficiency

The economic downturn as well as disorder in particularly financial markets that is indicated

as the global financial crisis (GFC) has spawned a striking expression of blame. Goh et al.

(2015), suggests that the efficient market hypothesis (EMH) is the notion that financial

markets ruthlessly make use of all obtainable information at the time of establishing prices of

security. As per Goh et al. (2015), an efficient market is necessarily the one in which prices

complete replicate all the available important information. At the micro-level , this notion of

market efficiency can be considered to be the extent to which financial security prices

replicate information that is necessarily relative to different other securities specifically

within the same class of asset. Again, at the macro level, the concern is regarding whether the

entire market on the whole replicates all available information. This is to say, whether share

market is necessarily fairly priced in comparison to relatively less risky asset, for example,

government debt.

INVESTING AND FINANCIAL MARKETS

essence, they bought the said assets endowed with high rating assurance by major credit

rating agencies, thinking they were protected investments.

However, in this context it can be hereby stated that availability of more accurate information

particularly financial markets could have assisted financiers to know more in detail about

lethal nature of investment assets. They could have known in detail about sub-prime

mortgages and would be less keen to invest in the same. In case if the banks were unable to

market investment products, they would have lesser funds at their disposal (Nelson and

Katzenstein 2014). Subsequently less credit would be available to different purchasers with

low income as well as poor profiles of credit. Essentially, this could have prevented

plummeting of sub-prime mortgages and housing bubble burst.

4.3 Market Efficiency

The economic downturn as well as disorder in particularly financial markets that is indicated

as the global financial crisis (GFC) has spawned a striking expression of blame. Goh et al.

(2015), suggests that the efficient market hypothesis (EMH) is the notion that financial

markets ruthlessly make use of all obtainable information at the time of establishing prices of

security. As per Goh et al. (2015), an efficient market is necessarily the one in which prices

complete replicate all the available important information. At the micro-level , this notion of

market efficiency can be considered to be the extent to which financial security prices

replicate information that is necessarily relative to different other securities specifically

within the same class of asset. Again, at the macro level, the concern is regarding whether the

entire market on the whole replicates all available information. This is to say, whether share

market is necessarily fairly priced in comparison to relatively less risky asset, for example,

government debt.

9

INVESTING AND FINANCIAL MARKETS

In spite of several limitations of the theory of market efficiency, there is specific claim that it

is accountable for the present global crisis. There is a belief in the fact that market efficiency

was accountable for asset bubble, for different investment analysts miscalculated risks. There

are many who believed in accountability of market efficiency for the collapse of the firm

Lehman Bros (Kumhof et al. 2015). Scholars were of the view that efficient market might

have forecasted the crash.

4.4. Moral Hazard

Goh et al. (2015) suggests that moral hazard subsists in a specific market in which a specific

individual or corporation undertakes more risks that they ought to be. This is because they

know that they are either covered by insurance or else they believe that the government shall

shield them from any kind of damage occurring as an outcome of the risks.

5. Behavioural Bias Theory and Financial Crisis of the year 2008

As correctly mentioned by Treeck (2014), behavioural bias also known as human factor

influences perception regarding information and process of arriving at decisions. The current

study at hand focuses on two pertinent facets namely the confirmation bias as well as

confidence bearing in mind behavioural facets that influence the financial crisis of the year

2008. The current section hereby highlights the psychological pitfalls that led to the financial

crisis

5.1 Confirmation Bias

As rightly put forward by Armantier et al. (2015), confirmation bias directs people to

essentially overweight specific information that actually confirms their beliefs and prior

information. On the other hand, confirmation bias also underweight information that

necessarily disconfirms and disregards their own views. Risk managers also were susceptible

INVESTING AND FINANCIAL MARKETS

In spite of several limitations of the theory of market efficiency, there is specific claim that it

is accountable for the present global crisis. There is a belief in the fact that market efficiency

was accountable for asset bubble, for different investment analysts miscalculated risks. There

are many who believed in accountability of market efficiency for the collapse of the firm

Lehman Bros (Kumhof et al. 2015). Scholars were of the view that efficient market might

have forecasted the crash.

4.4. Moral Hazard

Goh et al. (2015) suggests that moral hazard subsists in a specific market in which a specific

individual or corporation undertakes more risks that they ought to be. This is because they

know that they are either covered by insurance or else they believe that the government shall

shield them from any kind of damage occurring as an outcome of the risks.

5. Behavioural Bias Theory and Financial Crisis of the year 2008

As correctly mentioned by Treeck (2014), behavioural bias also known as human factor

influences perception regarding information and process of arriving at decisions. The current

study at hand focuses on two pertinent facets namely the confirmation bias as well as

confidence bearing in mind behavioural facets that influence the financial crisis of the year

2008. The current section hereby highlights the psychological pitfalls that led to the financial

crisis

5.1 Confirmation Bias

As rightly put forward by Armantier et al. (2015), confirmation bias directs people to

essentially overweight specific information that actually confirms their beliefs and prior

information. On the other hand, confirmation bias also underweight information that

necessarily disconfirms and disregards their own views. Risk managers also were susceptible

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

INVESTING AND FINANCIAL MARKETS

to this confirmation bias. Essentially at the time when business concerns started experiencing

losses during the first quarters of the year 2007, the team responsible for management of risk

failed to implement supplementary methodologies for averting the identified risks.

Thereafter, matters got worse and led to financial crisis. Financiers purchased high rated

securities mainly with the sub prime mortgages elements. Essentially, the sophisticated

investors should have acquired more information regarding the structure of the securities

along with the risk associated to the same (Nelson and Katzenstein 2014). Instead, the

investors went into investments in these securities as these products were extremely

profitable and therefore they depended on information that was in line and in conformation

with their own beliefs and views. For instance, they depended on the information on high

ratings (AAA) conferred by the rating agencies, various news stressing on the positive trends

on housing prices and mortgage supported securities and many others (Leamer 2015). As

such, they ignored all the available conflicting information that presented bubble forming in

the prices of housing, and risk associated to the complicated nature of the securities and many

others.

5.2 Overconfidence

An important feature of the behavioural finance is that financiers are inclined to express

excessive optimism that necessarily stems from overconfidence. A detrimental effect of the

same is that it shows the way to excessive trading by financiers as substantiated by escalating

popularity of ground-breaking mortgage securities observed in the milieu of lively housing

market. Overconfidence was also exhibited by another set of people namely the home

purchasers of the US (Cerutti et al. 2017). They in actual fact overrated their potential to

acquire mortgage loans that in turn led to higher degrees of leverage along with abundance of

INVESTING AND FINANCIAL MARKETS

to this confirmation bias. Essentially at the time when business concerns started experiencing

losses during the first quarters of the year 2007, the team responsible for management of risk

failed to implement supplementary methodologies for averting the identified risks.

Thereafter, matters got worse and led to financial crisis. Financiers purchased high rated

securities mainly with the sub prime mortgages elements. Essentially, the sophisticated

investors should have acquired more information regarding the structure of the securities

along with the risk associated to the same (Nelson and Katzenstein 2014). Instead, the

investors went into investments in these securities as these products were extremely

profitable and therefore they depended on information that was in line and in conformation

with their own beliefs and views. For instance, they depended on the information on high

ratings (AAA) conferred by the rating agencies, various news stressing on the positive trends

on housing prices and mortgage supported securities and many others (Leamer 2015). As

such, they ignored all the available conflicting information that presented bubble forming in

the prices of housing, and risk associated to the complicated nature of the securities and many

others.

5.2 Overconfidence

An important feature of the behavioural finance is that financiers are inclined to express

excessive optimism that necessarily stems from overconfidence. A detrimental effect of the

same is that it shows the way to excessive trading by financiers as substantiated by escalating

popularity of ground-breaking mortgage securities observed in the milieu of lively housing

market. Overconfidence was also exhibited by another set of people namely the home

purchasers of the US (Cerutti et al. 2017). They in actual fact overrated their potential to

acquire mortgage loans that in turn led to higher degrees of leverage along with abundance of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

INVESTING AND FINANCIAL MARKETS

sub prime mortgage that again banks utilized to package into complicated security assets.

Altogether these factors directed the way towards financial crisis of the year 2008.

5.3 Heading Bias

As rightly put forward by Bech et al. (2014), focus of expansion (abbreviated as FOE)

indicates the heading direction of a particular observer during the period of self motion. Prior

experiments reflect that humans have the potential to appropriately perceive their own

heading from a particular optic flow. Nevertheless, at the time when the setting basically

contains an independently moving item, then the judgements on heading might perhaps get

biased. Thus, it can be said that when a specific item approaches a particular observer, this

heading bias might be owing to discrepant optic flow specifically within object contours that

emanates from a secondary form of FOE. In itself, sub-prime mortgage currently indicate

towards present bias. As per present bias, individuals have the tendency to concentrate on the

present and move as per present conditions and tend to undervalue future period. During the

pre-crisis period, individuals were heading in a direction with a focus on the present situation

and arrived at decisions that they later regretted (Cerutti et al. 2017). This is because the

factor “now” moved with time. Individuals might have put off an undesirable decision,

planned to do something in the future period, however, when the future period arrived, they

changed their mind and shelved their prior decision. This can be referred to as a heading bias

as their judgement on sub prime mortgage changed. Investors headed towards taking up the

mortgage with focus on present and ignored the threats that the risky assets might pose.

6. Conclusion

The financial crisis of the year 2008 emanated from housing bubble in the United States that

in turn stretched and widened to the entire financial system as well as economy. The above

study helps in gaining comprehensive understanding regarding diverse features of market

INVESTING AND FINANCIAL MARKETS

sub prime mortgage that again banks utilized to package into complicated security assets.

Altogether these factors directed the way towards financial crisis of the year 2008.

5.3 Heading Bias

As rightly put forward by Bech et al. (2014), focus of expansion (abbreviated as FOE)

indicates the heading direction of a particular observer during the period of self motion. Prior

experiments reflect that humans have the potential to appropriately perceive their own

heading from a particular optic flow. Nevertheless, at the time when the setting basically

contains an independently moving item, then the judgements on heading might perhaps get

biased. Thus, it can be said that when a specific item approaches a particular observer, this

heading bias might be owing to discrepant optic flow specifically within object contours that

emanates from a secondary form of FOE. In itself, sub-prime mortgage currently indicate

towards present bias. As per present bias, individuals have the tendency to concentrate on the

present and move as per present conditions and tend to undervalue future period. During the

pre-crisis period, individuals were heading in a direction with a focus on the present situation

and arrived at decisions that they later regretted (Cerutti et al. 2017). This is because the

factor “now” moved with time. Individuals might have put off an undesirable decision,

planned to do something in the future period, however, when the future period arrived, they

changed their mind and shelved their prior decision. This can be referred to as a heading bias

as their judgement on sub prime mortgage changed. Investors headed towards taking up the

mortgage with focus on present and ignored the threats that the risky assets might pose.

6. Conclusion

The financial crisis of the year 2008 emanated from housing bubble in the United States that

in turn stretched and widened to the entire financial system as well as economy. The above

study helps in gaining comprehensive understanding regarding diverse features of market

12

INVESTING AND FINANCIAL MARKETS

failure along with behavioural bias that led to financial crisis. Essentially, this insight into the

financial crisis is expected to generate more awareness among different entities namely

regulators, different financial institutions, financiers, as well as credit rating agencies among

many others that in turn can avoid financial crises of similar nature in the future.

INVESTING AND FINANCIAL MARKETS

failure along with behavioural bias that led to financial crisis. Essentially, this insight into the

financial crisis is expected to generate more awareness among different entities namely

regulators, different financial institutions, financiers, as well as credit rating agencies among

many others that in turn can avoid financial crises of similar nature in the future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.