Financial System Data Analysis and Report and Forecasting: Webflims

VerifiedAdded on 2023/01/07

|25

|7567

|89

Report

AI Summary

This report provides a detailed financial analysis of Webflims, a company based in Melbourne, Australia, focusing on its financial systems, data, and forecasting. It begins with an introduction to financial analysis and planning, emphasizing the importance of forecasting sales and other revenues. Part A examines the current financial systems, including budgets and balance sheets, and analyzes the company's financial data from 2019-20, highlighting variances and requirements. A forecasted budget and balance sheet are also included. Part B discusses management responsibilities and legal requirements for financial reporting, referencing Australian Accounting Standards and the Corporations Act 2001. The report includes an analysis of financial statements and supporting notes. The assignment also outlines financial plans, delegated authorities, internal control procedures, and reporting periods, along with recommendations on budgeted expenses. The conclusion summarizes the key findings and recommendations.

Financial System Data

Analysis and Report and

Forecasting

Analysis and Report and

Forecasting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B..........................................................................................................................................10

PART C..........................................................................................................................................12

PART D.........................................................................................................................................16

PART E..........................................................................................................................................18

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B..........................................................................................................................................10

PART C..........................................................................................................................................12

PART D.........................................................................................................................................16

PART E..........................................................................................................................................18

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION

Financial analysis is the method of reviewing companies, programs, expenditures and other

activities relevant to finance to assess their efficiency and appropriateness. Financial process is

usually further used evaluate how an entity is extremely strong, liquid phase, liquid or financially

viable to justify a financial return (Andreescu and et. al., 2013). Financial planning is the

method of collection, estimate, or prediction of future performance of a business. Manager seeks

to foresee how the company will look economically throughout the future using financial reports.

Predicting a company's sales is a typical way of creating monetary prognoses. At the end,

revenue figures decide where the (commercial) company. Thus, they are essential measures for

smart decision taking and help organizational goals. Other important components of capital

budgeting include forecasting other revenues, long term operating expenses, as well as

investment. In this report, Webflims have been selected which is located in Melbourne,

Australia. The company use to provide different online solution to various other firms that seeks

to increase their brand popularity.

In this report, forecast about future financial resources, asset performance and capacity by

performing, steps to set the business targets and compliance mechanisms is discussed. In

addition, Management of the financial risk and steps to monitor compliance with the financial

projections are also elaborated.

PART A

1. Current financial systems and documents

Financial system used

Budget: A budget is a financial plan of income and expenses for a determined period of time,

which is generally, compiled which regularly re-evaluated. Manager can create budgets for a

individual, a group of individuals, a company, a country, or anything else which earns millions

and uses in different operations.

Balance sheet: A balance sheet is consider to be a most important financial statement which

records at a particular moment in time the assets , liabilities as well as equity of a business and

forms a framework for estimating investment returns and determining the cash position. It

also offers a summary of what an enterprise owns and owes, and the sums that investors

contribute.

Financial analysis is the method of reviewing companies, programs, expenditures and other

activities relevant to finance to assess their efficiency and appropriateness. Financial process is

usually further used evaluate how an entity is extremely strong, liquid phase, liquid or financially

viable to justify a financial return (Andreescu and et. al., 2013). Financial planning is the

method of collection, estimate, or prediction of future performance of a business. Manager seeks

to foresee how the company will look economically throughout the future using financial reports.

Predicting a company's sales is a typical way of creating monetary prognoses. At the end,

revenue figures decide where the (commercial) company. Thus, they are essential measures for

smart decision taking and help organizational goals. Other important components of capital

budgeting include forecasting other revenues, long term operating expenses, as well as

investment. In this report, Webflims have been selected which is located in Melbourne,

Australia. The company use to provide different online solution to various other firms that seeks

to increase their brand popularity.

In this report, forecast about future financial resources, asset performance and capacity by

performing, steps to set the business targets and compliance mechanisms is discussed. In

addition, Management of the financial risk and steps to monitor compliance with the financial

projections are also elaborated.

PART A

1. Current financial systems and documents

Financial system used

Budget: A budget is a financial plan of income and expenses for a determined period of time,

which is generally, compiled which regularly re-evaluated. Manager can create budgets for a

individual, a group of individuals, a company, a country, or anything else which earns millions

and uses in different operations.

Balance sheet: A balance sheet is consider to be a most important financial statement which

records at a particular moment in time the assets , liabilities as well as equity of a business and

forms a framework for estimating investment returns and determining the cash position. It

also offers a summary of what an enterprise owns and owes, and the sums that investors

contribute.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Covering

These two documents cover the useful information related to the different financial

transaction of company for a specific period of time. Such as balance sheet covers, the entire

information about the assets and liabilities of company and equity balance within an accounting

year. On the other side, budget includes within Webflims a detailed estimation about expenses on

different operations and total income to be generated through these activities in upcoming time.

It mainly relies over the past information so future results may vary (Bedi, Alpaslan and Green,

2016).

Strategic and tactical management

Strategic information management outcomes are a strategic benefit, input on issues to the

management, input on issues to clients, maintaining due diligence, reducing prices, fostering

trust with suppliers and through revenue as consumers know their data is secure. Trust and

transparency are guaranteed, enforcement is given with the legislative and legal specifications.

Risks are reduced, and regulate rises are made accessible and accessible data is given. The

tactical advantages have a beneficial influence mostly on interaction between the company and

its stakeholders. Operation administration includes managing the users' routine commands,

modes of entry, and procedures. The management and modification of access controls, such as

network controls as well as access rights, are instances. Keywords and rights to enter or leave an

entity must be generated or revoked.

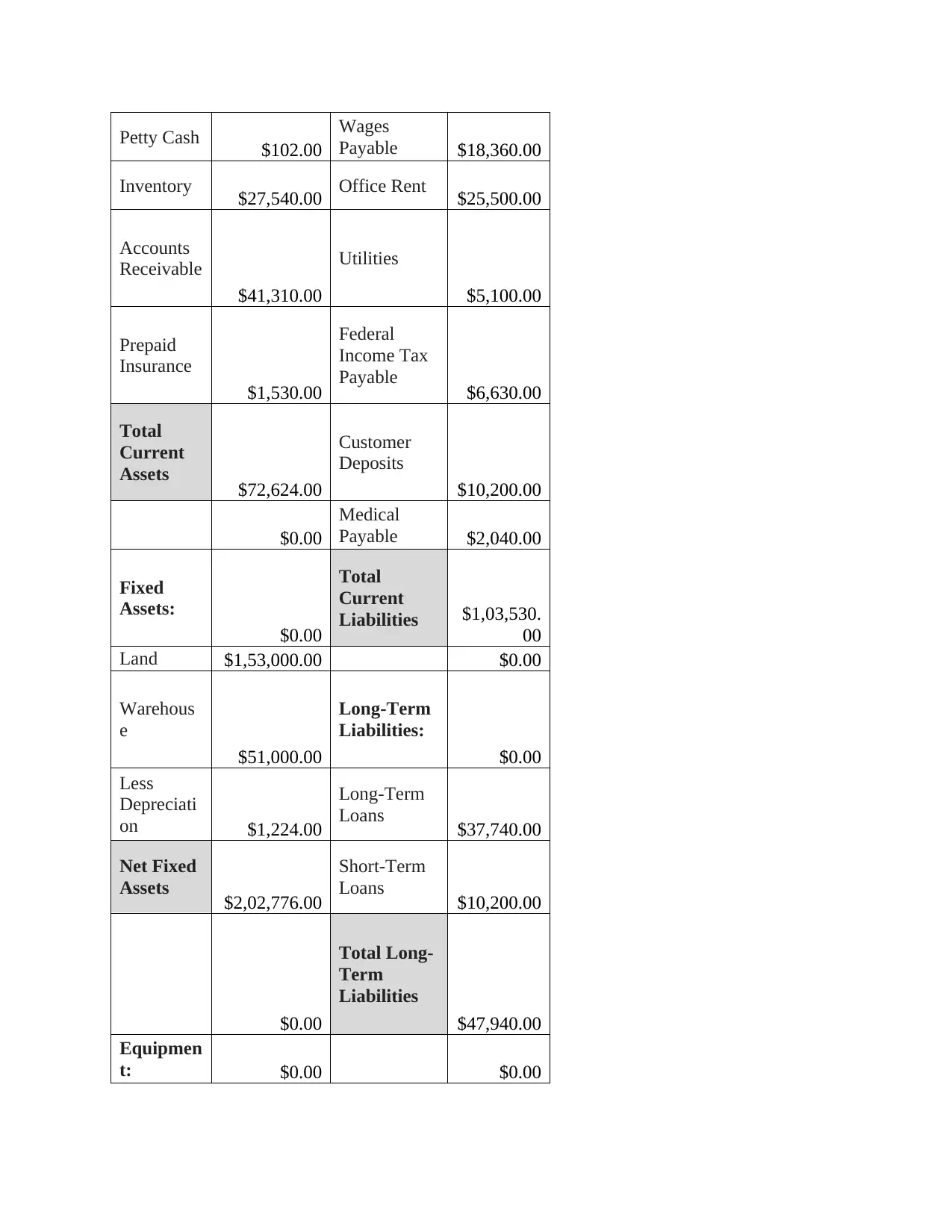

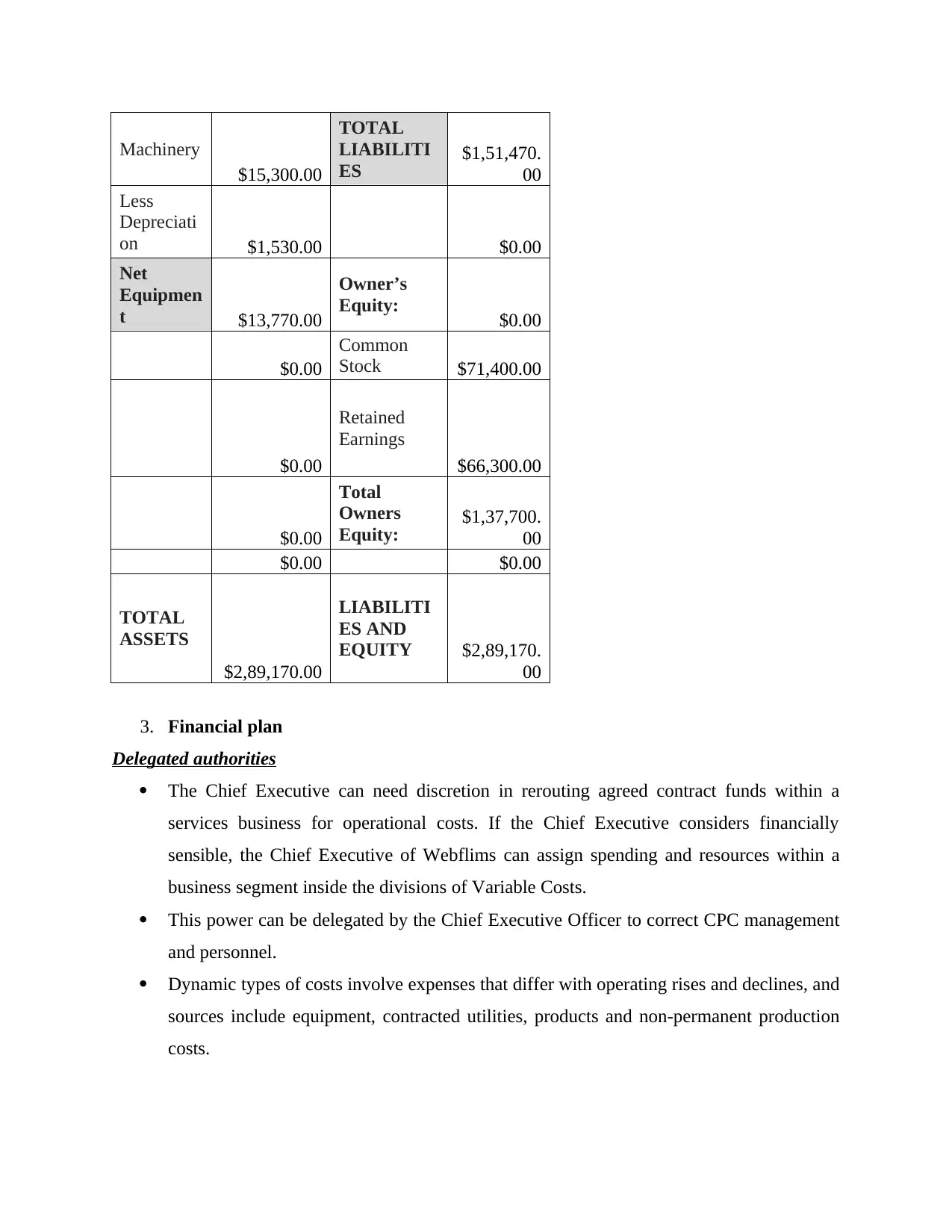

2. Analysis on current financial data, systems requirements

The important reports such as budget and balance sheet are prepared and presented by the

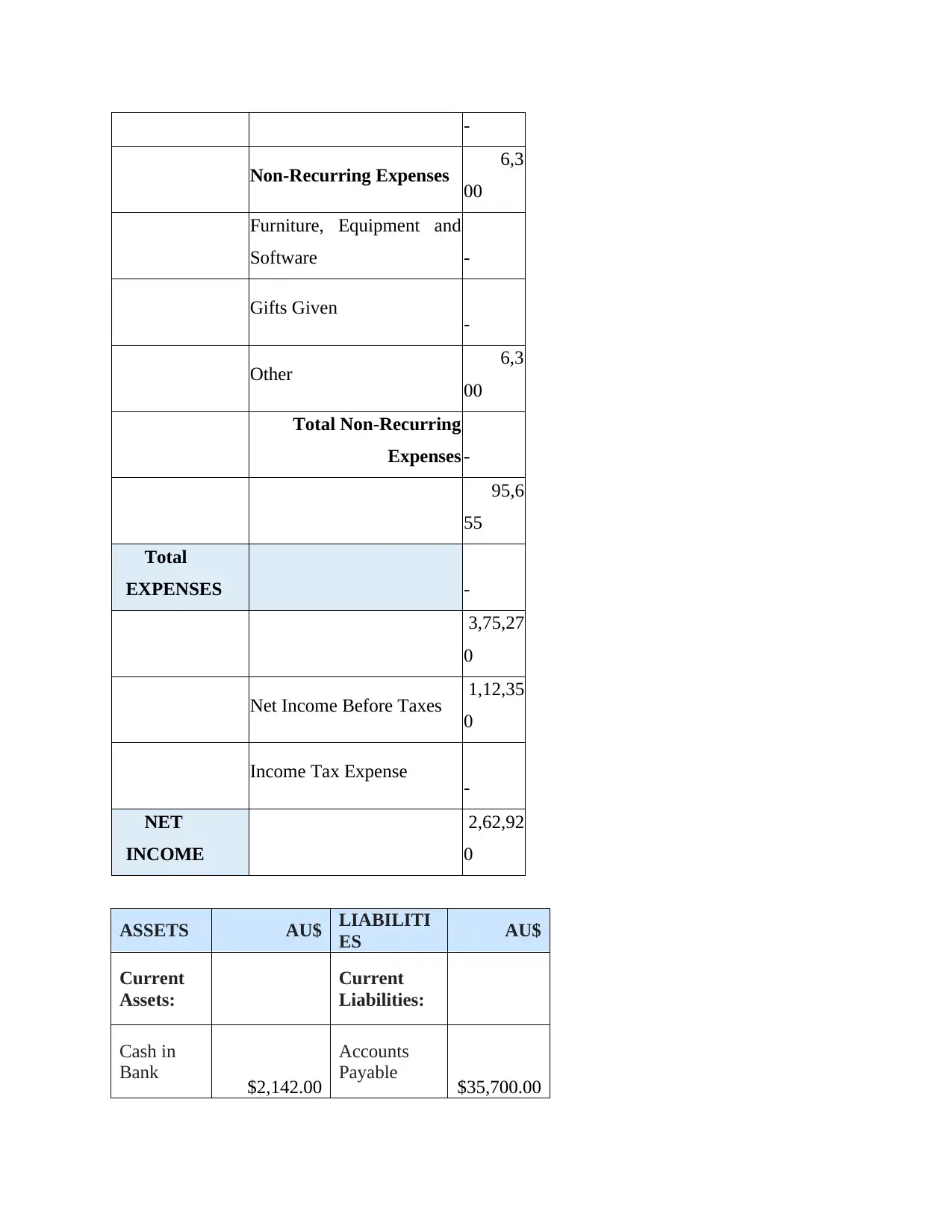

company for the period of 2019-20. The provided balance sheet gives the information about,

current assets which is $71200, net fixed assets $198800 and net equipment is $13500. On the

other side current liabilities is $101500, long term loans $47000 and owner equity is $13500 so

that both side shows equal amount which is $283500. Budget mainly shows the estimated

income from the different activities which are part of company. A deviation in budget is a

frequent calculation to calculate the discrepancy in between planned and real estimates under a

particular form of accounting. A flexible budget in Webflims is the budget corresponds to leads

to a positive or benefits; an adverse variance in the budget defines negative variance which

indicates losses or inefficiencies. Budget variances exist because forecasters cannot entirely

reliably predict projected expenses and profits. There have been a big difference within income

These two documents cover the useful information related to the different financial

transaction of company for a specific period of time. Such as balance sheet covers, the entire

information about the assets and liabilities of company and equity balance within an accounting

year. On the other side, budget includes within Webflims a detailed estimation about expenses on

different operations and total income to be generated through these activities in upcoming time.

It mainly relies over the past information so future results may vary (Bedi, Alpaslan and Green,

2016).

Strategic and tactical management

Strategic information management outcomes are a strategic benefit, input on issues to the

management, input on issues to clients, maintaining due diligence, reducing prices, fostering

trust with suppliers and through revenue as consumers know their data is secure. Trust and

transparency are guaranteed, enforcement is given with the legislative and legal specifications.

Risks are reduced, and regulate rises are made accessible and accessible data is given. The

tactical advantages have a beneficial influence mostly on interaction between the company and

its stakeholders. Operation administration includes managing the users' routine commands,

modes of entry, and procedures. The management and modification of access controls, such as

network controls as well as access rights, are instances. Keywords and rights to enter or leave an

entity must be generated or revoked.

2. Analysis on current financial data, systems requirements

The important reports such as budget and balance sheet are prepared and presented by the

company for the period of 2019-20. The provided balance sheet gives the information about,

current assets which is $71200, net fixed assets $198800 and net equipment is $13500. On the

other side current liabilities is $101500, long term loans $47000 and owner equity is $13500 so

that both side shows equal amount which is $283500. Budget mainly shows the estimated

income from the different activities which are part of company. A deviation in budget is a

frequent calculation to calculate the discrepancy in between planned and real estimates under a

particular form of accounting. A flexible budget in Webflims is the budget corresponds to leads

to a positive or benefits; an adverse variance in the budget defines negative variance which

indicates losses or inefficiencies. Budget variances exist because forecasters cannot entirely

reliably predict projected expenses and profits. There have been a big difference within income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

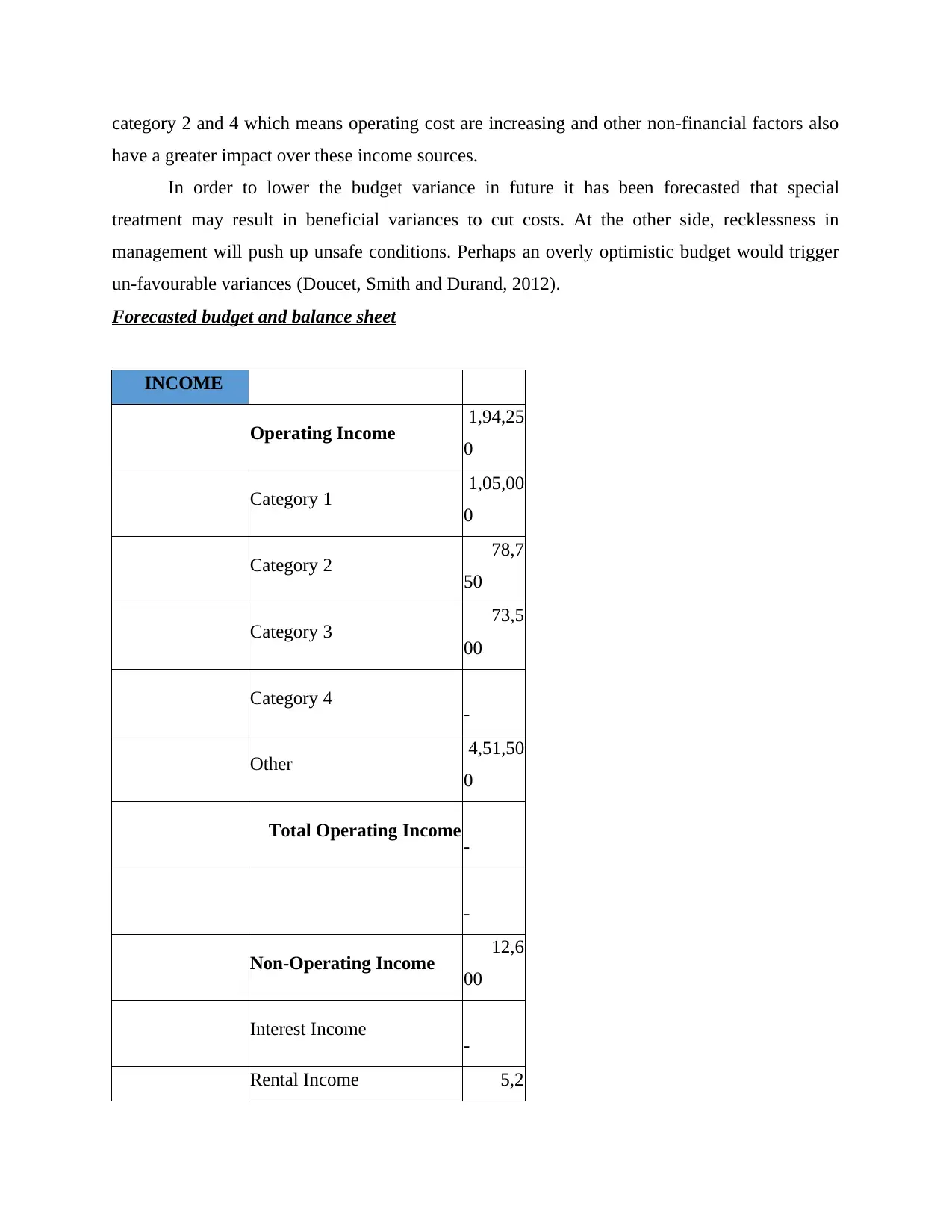

category 2 and 4 which means operating cost are increasing and other non-financial factors also

have a greater impact over these income sources.

In order to lower the budget variance in future it has been forecasted that special

treatment may result in beneficial variances to cut costs. At the other side, recklessness in

management will push up unsafe conditions. Perhaps an overly optimistic budget would trigger

un-favourable variances (Doucet, Smith and Durand, 2012).

Forecasted budget and balance sheet

INCOME

Operating Income 1,94,25

0

Category 1 1,05,00

0

Category 2 78,7

50

Category 3 73,5

00

Category 4 -

Other 4,51,50

0

Total Operating Income -

-

Non-Operating Income 12,6

00

Interest Income -

Rental Income 5,2

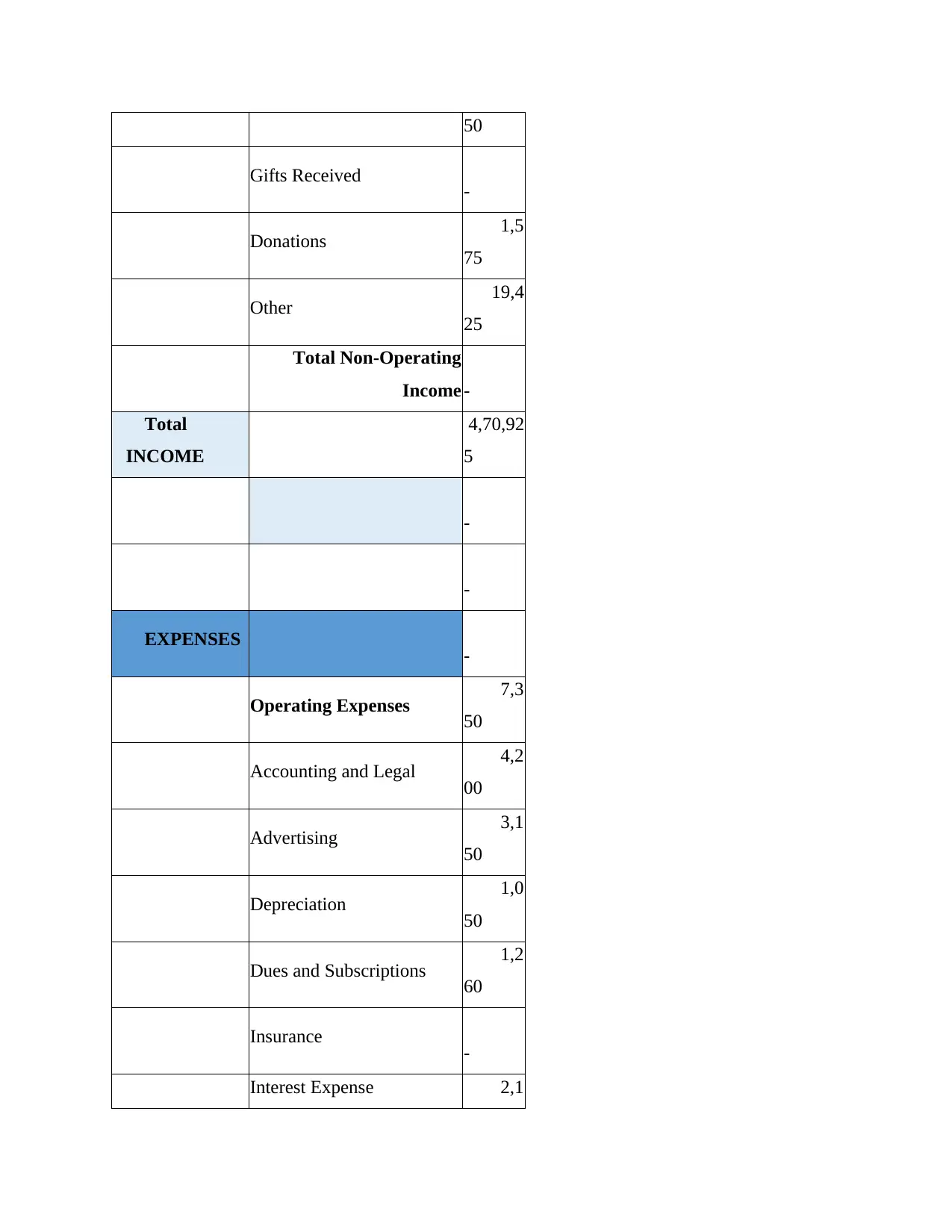

have a greater impact over these income sources.

In order to lower the budget variance in future it has been forecasted that special

treatment may result in beneficial variances to cut costs. At the other side, recklessness in

management will push up unsafe conditions. Perhaps an overly optimistic budget would trigger

un-favourable variances (Doucet, Smith and Durand, 2012).

Forecasted budget and balance sheet

INCOME

Operating Income 1,94,25

0

Category 1 1,05,00

0

Category 2 78,7

50

Category 3 73,5

00

Category 4 -

Other 4,51,50

0

Total Operating Income -

-

Non-Operating Income 12,6

00

Interest Income -

Rental Income 5,2

50

Gifts Received -

Donations 1,5

75

Other 19,4

25

Total Non-Operating

Income -

Total

INCOME

4,70,92

5

-

-

EXPENSES -

Operating Expenses 7,3

50

Accounting and Legal 4,2

00

Advertising 3,1

50

Depreciation 1,0

50

Dues and Subscriptions 1,2

60

Insurance -

Interest Expense 2,1

Gifts Received -

Donations 1,5

75

Other 19,4

25

Total Non-Operating

Income -

Total

INCOME

4,70,92

5

-

-

EXPENSES -

Operating Expenses 7,3

50

Accounting and Legal 4,2

00

Advertising 3,1

50

Depreciation 1,0

50

Dues and Subscriptions 1,2

60

Insurance -

Interest Expense 2,1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

00

Maintenance and Repairs 6

30

Office Supplies -

Payroll Expenses 6

30

Postage 13,6

50

Rent -

Research and Development 50,4

00

Salaries and Wages -

Taxes and Licenses 1,2

60

Telephone 1,5

75

Travel -

Utilities 1,5

75

Web Hosting and Domains 5

25

Other 89,3

55

Total Operating Expenses -

Maintenance and Repairs 6

30

Office Supplies -

Payroll Expenses 6

30

Postage 13,6

50

Rent -

Research and Development 50,4

00

Salaries and Wages -

Taxes and Licenses 1,2

60

Telephone 1,5

75

Travel -

Utilities 1,5

75

Web Hosting and Domains 5

25

Other 89,3

55

Total Operating Expenses -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-

Non-Recurring Expenses 6,3

00

Furniture, Equipment and

Software -

Gifts Given -

Other 6,3

00

Total Non-Recurring

Expenses -

95,6

55

Total

EXPENSES -

3,75,27

0

Net Income Before Taxes 1,12,35

0

Income Tax Expense -

NET

INCOME

2,62,92

0

ASSETS AU$ LIABILITI

ES AU$

Current

Assets:

Current

Liabilities:

Cash in

Bank $2,142.00

Accounts

Payable $35,700.00

Non-Recurring Expenses 6,3

00

Furniture, Equipment and

Software -

Gifts Given -

Other 6,3

00

Total Non-Recurring

Expenses -

95,6

55

Total

EXPENSES -

3,75,27

0

Net Income Before Taxes 1,12,35

0

Income Tax Expense -

NET

INCOME

2,62,92

0

ASSETS AU$ LIABILITI

ES AU$

Current

Assets:

Current

Liabilities:

Cash in

Bank $2,142.00

Accounts

Payable $35,700.00

Petty Cash $102.00

Wages

Payable $18,360.00

Inventory $27,540.00 Office Rent $25,500.00

Accounts

Receivable

$41,310.00

Utilities

$5,100.00

Prepaid

Insurance

$1,530.00

Federal

Income Tax

Payable $6,630.00

Total

Current

Assets $72,624.00

Customer

Deposits

$10,200.00

$0.00

Medical

Payable $2,040.00

Fixed

Assets:

$0.00

Total

Current

Liabilities $1,03,530.

00

Land $1,53,000.00 $0.00

Warehous

e

$51,000.00

Long-Term

Liabilities:

$0.00

Less

Depreciati

on $1,224.00

Long-Term

Loans $37,740.00

Net Fixed

Assets $2,02,776.00

Short-Term

Loans $10,200.00

$0.00

Total Long-

Term

Liabilities

$47,940.00

Equipmen

t: $0.00 $0.00

Wages

Payable $18,360.00

Inventory $27,540.00 Office Rent $25,500.00

Accounts

Receivable

$41,310.00

Utilities

$5,100.00

Prepaid

Insurance

$1,530.00

Federal

Income Tax

Payable $6,630.00

Total

Current

Assets $72,624.00

Customer

Deposits

$10,200.00

$0.00

Medical

Payable $2,040.00

Fixed

Assets:

$0.00

Total

Current

Liabilities $1,03,530.

00

Land $1,53,000.00 $0.00

Warehous

e

$51,000.00

Long-Term

Liabilities:

$0.00

Less

Depreciati

on $1,224.00

Long-Term

Loans $37,740.00

Net Fixed

Assets $2,02,776.00

Short-Term

Loans $10,200.00

$0.00

Total Long-

Term

Liabilities

$47,940.00

Equipmen

t: $0.00 $0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Machinery

$15,300.00

TOTAL

LIABILITI

ES $1,51,470.

00

Less

Depreciati

on $1,530.00 $0.00

Net

Equipmen

t $13,770.00

Owner’s

Equity: $0.00

$0.00

Common

Stock $71,400.00

$0.00

Retained

Earnings

$66,300.00

$0.00

Total

Owners

Equity: $1,37,700.

00

$0.00 $0.00

TOTAL

ASSETS

$2,89,170.00

LIABILITI

ES AND

EQUITY $2,89,170.

00

3. Financial plan

Delegated authorities

The Chief Executive can need discretion in rerouting agreed contract funds within a

services business for operational costs. If the Chief Executive considers financially

sensible, the Chief Executive of Webflims can assign spending and resources within a

business segment inside the divisions of Variable Costs.

This power can be delegated by the Chief Executive Officer to correct CPC management

and personnel.

Dynamic types of costs involve expenses that differ with operating rises and declines, and

sources include equipment, contracted utilities, products and non-permanent production

costs.

$15,300.00

TOTAL

LIABILITI

ES $1,51,470.

00

Less

Depreciati

on $1,530.00 $0.00

Net

Equipmen

t $13,770.00

Owner’s

Equity: $0.00

$0.00

Common

Stock $71,400.00

$0.00

Retained

Earnings

$66,300.00

$0.00

Total

Owners

Equity: $1,37,700.

00

$0.00 $0.00

TOTAL

ASSETS

$2,89,170.00

LIABILITI

ES AND

EQUITY $2,89,170.

00

3. Financial plan

Delegated authorities

The Chief Executive can need discretion in rerouting agreed contract funds within a

services business for operational costs. If the Chief Executive considers financially

sensible, the Chief Executive of Webflims can assign spending and resources within a

business segment inside the divisions of Variable Costs.

This power can be delegated by the Chief Executive Officer to correct CPC management

and personnel.

Dynamic types of costs involve expenses that differ with operating rises and declines, and

sources include equipment, contracted utilities, products and non-permanent production

costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Set types of costs involve expenses that remain reasonably stable irrespective of the scale

of the purchases and definitions include leases, electricity, taxes, insurance, interest rates

on loans and regular wages.

Internal control procedures

The budget provides a framework for performance evaluation (analysis of variances). A

budget is essentially a benchmark for calculating and evaluating real results. Comparisons of real

outcomes to the target schedule offer leverage. Therefore, expenditure withdrawals should be

explored and the causes for the discrepancies may be separated between controllable and

uncontrollable variables (Fok, Payne and Corey, 2016).

Reporting periods

Budgets generally cover future event time frames, including a new accounting year or a

genetic economic cycle. Annual expenditures plan in Webflims are often separated into quarter

and monthly modules for process management reasons. That's also beneficial in the timely

monitoring of the performance. Specific sums within a monthly / quarterly schedule are often

pure relative quantities of the annual sum. Continuous budgets are being planned in this sense of

company that can be continually revised to span the next 12 months or 4 quarters, etc. When one

cycle is finished, the forward-looking financial details are transferred to another. This approach

calls for constant control and planning, which helps administrators to respond to changing

circumstances with greater experience which response time.

4. Recommendations on budgeted expenses

Categorize the company's costs into divisions of expenses and efficiency. This will

support set the rates and decide things when cost-cutting is required. Total costs are

expenses incurred required to operate a company, rather than manufacturing a

commodity, such as payroll, marketing, leasing, equipment, telephones and office

workers.

The integration of a number of reports with an annual profit and cost forecast plan

produces a master budget that avoids anomalies that can delay or shut down the

company. In addition, u sing a range of valuable reports connected to the annual budget

to enhance financial monitoring and make manager awake to date anytime detail is

needed.

of the purchases and definitions include leases, electricity, taxes, insurance, interest rates

on loans and regular wages.

Internal control procedures

The budget provides a framework for performance evaluation (analysis of variances). A

budget is essentially a benchmark for calculating and evaluating real results. Comparisons of real

outcomes to the target schedule offer leverage. Therefore, expenditure withdrawals should be

explored and the causes for the discrepancies may be separated between controllable and

uncontrollable variables (Fok, Payne and Corey, 2016).

Reporting periods

Budgets generally cover future event time frames, including a new accounting year or a

genetic economic cycle. Annual expenditures plan in Webflims are often separated into quarter

and monthly modules for process management reasons. That's also beneficial in the timely

monitoring of the performance. Specific sums within a monthly / quarterly schedule are often

pure relative quantities of the annual sum. Continuous budgets are being planned in this sense of

company that can be continually revised to span the next 12 months or 4 quarters, etc. When one

cycle is finished, the forward-looking financial details are transferred to another. This approach

calls for constant control and planning, which helps administrators to respond to changing

circumstances with greater experience which response time.

4. Recommendations on budgeted expenses

Categorize the company's costs into divisions of expenses and efficiency. This will

support set the rates and decide things when cost-cutting is required. Total costs are

expenses incurred required to operate a company, rather than manufacturing a

commodity, such as payroll, marketing, leasing, equipment, telephones and office

workers.

The integration of a number of reports with an annual profit and cost forecast plan

produces a master budget that avoids anomalies that can delay or shut down the

company. In addition, u sing a range of valuable reports connected to the annual budget

to enhance financial monitoring and make manager awake to date anytime detail is

needed.

PART B

Responsibilities of the management and legal requirements for financial reporting

Australian Accounting Standards (SAC 1, 2, Framework AASB1001): Appropriate financial

information lets consumers make and assess choices about finite resource distribution. This lets

them make assumptions about future circumstances and shape beliefs, or it serves validity and

reliability responsibilities with regard to their previous evaluations. Financial statements of

Webflims can be important in the context of its origin, origin and importance, or in comparison

to its existence. In SAC third additional information is provided on significance about the

financial report which is very important to make decision (Groom, 2018). Reliable financial

knowledge conveys a strong the actual sales and other activities to customers. To be accurate on

financial statistics, it has to be bias-free. Reliable accounting reporting should not lead

consumers to assumptions which represent the specific needs, expectations or preconceived

notions of income statements preparers.

Corporations Act 2001: The Corporations law required firms and registration strategies to

preserve a membership register and, where appropriate, a register of choice owners and a sign up

of corporate debtor. Section 169 including its Act specifies that a members' list include such

information, along with the address and phone number of the individual, the period upon which

participant 's address was recorded in the list, and certain other information, including the

outstanding shares from each representative. It seems fairly obvious in its aspects that perhaps

the intent of corporate act 2001 is to safeguard stockholders' confidentiality by limiting

permissible uses of data collected from them about the database. The segment will not allow the

stockholders of products and services unconnected to their condition as stockholders for using

data on the registration for direct sales but it may be that even corporation authorization of use of

knowledge on the registration will be restricted by the National Privacy Principles with which

comparison has been already decided to make.

Financial Administration and Audit Act 1977: All community moneys except those needed by

this Legislation to be deposited into any bank account and specialized funds; and then all tax

money earning components fund through loan financing credit promptly preceding July 1, 1991.

The monies generated by the sale of acquired public properties or produced or compensated for

jobs from the consolidated budget, consolidated Revenue Account or Loan Scheme. Moneys

obtained by late payment or breakthroughs first from funds collected, the results achieved Fund

Responsibilities of the management and legal requirements for financial reporting

Australian Accounting Standards (SAC 1, 2, Framework AASB1001): Appropriate financial

information lets consumers make and assess choices about finite resource distribution. This lets

them make assumptions about future circumstances and shape beliefs, or it serves validity and

reliability responsibilities with regard to their previous evaluations. Financial statements of

Webflims can be important in the context of its origin, origin and importance, or in comparison

to its existence. In SAC third additional information is provided on significance about the

financial report which is very important to make decision (Groom, 2018). Reliable financial

knowledge conveys a strong the actual sales and other activities to customers. To be accurate on

financial statistics, it has to be bias-free. Reliable accounting reporting should not lead

consumers to assumptions which represent the specific needs, expectations or preconceived

notions of income statements preparers.

Corporations Act 2001: The Corporations law required firms and registration strategies to

preserve a membership register and, where appropriate, a register of choice owners and a sign up

of corporate debtor. Section 169 including its Act specifies that a members' list include such

information, along with the address and phone number of the individual, the period upon which

participant 's address was recorded in the list, and certain other information, including the

outstanding shares from each representative. It seems fairly obvious in its aspects that perhaps

the intent of corporate act 2001 is to safeguard stockholders' confidentiality by limiting

permissible uses of data collected from them about the database. The segment will not allow the

stockholders of products and services unconnected to their condition as stockholders for using

data on the registration for direct sales but it may be that even corporation authorization of use of

knowledge on the registration will be restricted by the National Privacy Principles with which

comparison has been already decided to make.

Financial Administration and Audit Act 1977: All community moneys except those needed by

this Legislation to be deposited into any bank account and specialized funds; and then all tax

money earning components fund through loan financing credit promptly preceding July 1, 1991.

The monies generated by the sale of acquired public properties or produced or compensated for

jobs from the consolidated budget, consolidated Revenue Account or Loan Scheme. Moneys

obtained by late payment or breakthroughs first from funds collected, the results achieved Fund

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.