Financial Decision Making and Ratio Analysis Report for SKANSKA PLC

VerifiedAdded on 2022/12/06

|16

|4261

|280

Report

AI Summary

This report examines financial decision-making processes and the application of various management accounting techniques within the context of SKANSKA PLC. It begins with an introduction to financial decision-making and its importance, followed by an exploration of management accounting techniques such as financial planning, cost accounting, cash flow analysis, standard costing, budgetary control, and decision-making accounting. The report then evaluates these techniques, highlighting their role in planning, controlling, and decision-making. The second part of the report focuses on ratio analysis, including the calculation and interpretation of key ratios such as Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, Debtor Collection Period, and Creditor Collection Period. The report provides a comprehensive overview of financial performance and its importance for stakeholders.

FINNACIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK-1 FINANCIAL DECISION MAKING................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................4

Management accounting technique.............................................................................................4

Evaluation....................................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................1

TASK-2 RATIO ANALYSIS..........................................................................................................2

Calculation of ratios.....................................................................................................................2

Performance of SKANSKA PLC................................................................................................3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

TASK-1 FINANCIAL DECISION MAKING................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................4

Management accounting technique.............................................................................................4

Evaluation....................................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................1

TASK-2 RATIO ANALYSIS..........................................................................................................2

Calculation of ratios.....................................................................................................................2

Performance of SKANSKA PLC................................................................................................3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

TASK-1 FINANCIAL DECISION MAKING

INTRODUCTION

SKANSKA PLC is one of the famous construction company of the world and the UK. It was

started in 1984. It operates its function in many country including Sweden, Norway, Finland,

Denmark, Poland, Romania US and various other. The number of employees in the company is

approximately 32463 with an operating income of SEK 7.8 billion (Skanska UK in brief, 2021).

It performs its business operation in the field of construction project. It is counted as top

construction project handling company. Like other company, the role of accounting and finance

function also plays an important role in SKANSKA PLC too.

Accounting function refers to the function that is concerned with recording of financial

transactions along with preparation of financial statement. Likewise, finance is also an important

function that is concerned with financing activity of the company. through the performance of

this function an adequate availability of the money is being g ensured in every department of the

company (Pretorius, 2020). Performance of accounting function would enable the company

including the SKANSKA PLC to have an analysation of the financial performance, this means

that as financial statements are being prepared in the performance of accounting functions, so

through these statement company can make self-evaluation of its financial position. This will

also be beneficial for the other stakeholder including the shareholders, owners, investors,

customers and various other for determining the financial position and situation of the company

(Popescu, 2020).

In the same manner by performing the finance function along with its various associated

functions and decision in the form of investment, financing and dividend, companies including

SKANSKA PLC can determine and ensure the adequate availability of finance in the company.

Through the performance of this function SKANSKA can easily carry out its business operation.

it would not be wrong to said that performance of finance and accounting function including the

management accounting the company can take adequate decision and make future plan and

strategies.

This report will discuss about the concept of management accounting and its various

techniques including budgeting, costing, standard costing and various other. Management

accounting is also an important element of accounting that plays a major role in controlling and

INTRODUCTION

SKANSKA PLC is one of the famous construction company of the world and the UK. It was

started in 1984. It operates its function in many country including Sweden, Norway, Finland,

Denmark, Poland, Romania US and various other. The number of employees in the company is

approximately 32463 with an operating income of SEK 7.8 billion (Skanska UK in brief, 2021).

It performs its business operation in the field of construction project. It is counted as top

construction project handling company. Like other company, the role of accounting and finance

function also plays an important role in SKANSKA PLC too.

Accounting function refers to the function that is concerned with recording of financial

transactions along with preparation of financial statement. Likewise, finance is also an important

function that is concerned with financing activity of the company. through the performance of

this function an adequate availability of the money is being g ensured in every department of the

company (Pretorius, 2020). Performance of accounting function would enable the company

including the SKANSKA PLC to have an analysation of the financial performance, this means

that as financial statements are being prepared in the performance of accounting functions, so

through these statement company can make self-evaluation of its financial position. This will

also be beneficial for the other stakeholder including the shareholders, owners, investors,

customers and various other for determining the financial position and situation of the company

(Popescu, 2020).

In the same manner by performing the finance function along with its various associated

functions and decision in the form of investment, financing and dividend, companies including

SKANSKA PLC can determine and ensure the adequate availability of finance in the company.

Through the performance of this function SKANSKA can easily carry out its business operation.

it would not be wrong to said that performance of finance and accounting function including the

management accounting the company can take adequate decision and make future plan and

strategies.

This report will discuss about the concept of management accounting and its various

techniques including budgeting, costing, standard costing and various other. Management

accounting is also an important element of accounting that plays a major role in controlling and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making. This accounting is solely concerned with the managers and used for the internal

purpose. On the basis of this accounting the plans and policies are being determined. At last a

critical evaluation of the concept of management accounting is being included along with the

context of SKANSKA PLC.

MAIN BODY

Management accounting technique

Management accounting:

It is that part or branch of accounting that link the management with the accounting. This

means the accounting that is concerned with the use of management and for the internal use

would be counted as management accounting (Abdusalomova, 2019). It would also be right to

said that the information that is used for decision making is all related with the management

accounting. It is only be used for the internal purpose by the management of the company. in

simple words the management accounting means the presentation of accounting information in

such a manner that is being used by the managers in taking decisions and framing policies and

strategies.

Techniques:

Financial planning:

As the main objective of every business organization is to maximize its profit share. As,

management accounting help in financial planning, so by making the plan regarding the future

the company including the SKANSKA PLC can be directed towards the direction of its goal

accomplishment in the form of raising of profit.

Cost accounting:

This is also an important element and technique associated with the management

accounting. As under this accounting the cost that is being associated with the product, process,

department and various other are being determined that may act as a guide to the company in

order to determine the cost or the operation cost.

Cash flow analysis:

It is also an important technique associated with the management accounting. As per this

the movement of cash along with the period is being determined and analysed (Pradhan, Swain

purpose. On the basis of this accounting the plans and policies are being determined. At last a

critical evaluation of the concept of management accounting is being included along with the

context of SKANSKA PLC.

MAIN BODY

Management accounting technique

Management accounting:

It is that part or branch of accounting that link the management with the accounting. This

means the accounting that is concerned with the use of management and for the internal use

would be counted as management accounting (Abdusalomova, 2019). It would also be right to

said that the information that is used for decision making is all related with the management

accounting. It is only be used for the internal purpose by the management of the company. in

simple words the management accounting means the presentation of accounting information in

such a manner that is being used by the managers in taking decisions and framing policies and

strategies.

Techniques:

Financial planning:

As the main objective of every business organization is to maximize its profit share. As,

management accounting help in financial planning, so by making the plan regarding the future

the company including the SKANSKA PLC can be directed towards the direction of its goal

accomplishment in the form of raising of profit.

Cost accounting:

This is also an important element and technique associated with the management

accounting. As under this accounting the cost that is being associated with the product, process,

department and various other are being determined that may act as a guide to the company in

order to determine the cost or the operation cost.

Cash flow analysis:

It is also an important technique associated with the management accounting. As per this

the movement of cash along with the period is being determined and analysed (Pradhan, Swain

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and Dash, 2018). This statement and technique shows the inward and outward flow with respect

to the SKANSKA PLC.

Standard costing:

This is also a technique of management accounting. As per this, the standard cost is being

determined (Ameen, Ahmed and Abd Hafez, 2018). This determination of the cost may be

related to any process or the department. This is useful in terms of analysation and evaluation

between the actual cost and the standard one.

Budgetary control:

As per this technique the budgets regarding the future need are being prepared in

advance. Budget refer to a statement that provide the information regarding the estimated

revenue and the expenditure. This is an important technique because through this the SKANSKA

PLC can evaluate and analyse the actual expenses with the budgeted.

Decision making:

This is one of the important and critical technique that is being associated with the

management accounting. As decision regarding choosing of alternative is one of the important

task and any wrong decision may bring an adverse effect towards the company (Argenti, 2018).

However, evaluating the best alternative and selecting the most suitable for SKANSKA PLC is

being done through decision making accounting of management accounting. Under that the cost

is being evaluated.

Marginal costing:

This is also an important technique related with the management accounting. Under this the

selling price is being determined by keeping adequate margin for the company. here selecting the

best sales mix, best use of resources, determination of buying decision all being taken under the

SKANSKA PLC.

Evaluation

From the above technique it can be evaluated that management accounting plays an

important role in terms of planning, controlling, and decision making in the company including

the SKANSKA PLC. As under management accounting the various techniques including the

financial planning, standard costing, cash flow and various other are being included which

directly contribute their role in terms of planning and controlling. This can be understood as if

to the SKANSKA PLC.

Standard costing:

This is also a technique of management accounting. As per this, the standard cost is being

determined (Ameen, Ahmed and Abd Hafez, 2018). This determination of the cost may be

related to any process or the department. This is useful in terms of analysation and evaluation

between the actual cost and the standard one.

Budgetary control:

As per this technique the budgets regarding the future need are being prepared in

advance. Budget refer to a statement that provide the information regarding the estimated

revenue and the expenditure. This is an important technique because through this the SKANSKA

PLC can evaluate and analyse the actual expenses with the budgeted.

Decision making:

This is one of the important and critical technique that is being associated with the

management accounting. As decision regarding choosing of alternative is one of the important

task and any wrong decision may bring an adverse effect towards the company (Argenti, 2018).

However, evaluating the best alternative and selecting the most suitable for SKANSKA PLC is

being done through decision making accounting of management accounting. Under that the cost

is being evaluated.

Marginal costing:

This is also an important technique related with the management accounting. Under this the

selling price is being determined by keeping adequate margin for the company. here selecting the

best sales mix, best use of resources, determination of buying decision all being taken under the

SKANSKA PLC.

Evaluation

From the above technique it can be evaluated that management accounting plays an

important role in terms of planning, controlling, and decision making in the company including

the SKANSKA PLC. As under management accounting the various techniques including the

financial planning, standard costing, cash flow and various other are being included which

directly contribute their role in terms of planning and controlling. This can be understood as if

the standard cost is being set and determined with reference to any activity and the process and

then the actual performance and the associated cost is being compared then it will directly lead to

controlling and determination of fluctuation. Likewise, making of financial planning also enable

the company including the SKANSKA PLC to make the plan regarding the future.

In the same manner, decision making accounting also enable the company including the

SKANSKA PLC to determine the best alternative so that the most appropriate decision would be

taken. It is also to be noted that the company by adopting and using the management accounting

technique can have a better analysis and control over their daily operation and business operation

because under this accounting a direct check over the operation is being established.

Through the adoption and execution of this accounting practice by the SKANSKA PLC, it

can better operate its business operation along with keeping a good controlling. This means as

through this technique it will perform various technique and thereby as a result of those it can

better perform its business and move in the direction of the accomplishment of its objectives.

Likewise, an association of cost and the budgetary technique also guide the company regarding

the estimation of the required cost or the estimated budgets regarding the future. This means that

through management accounting the SKANKA PLC can determine the cost element of the

process along with determination of the estimated future expenses and the revenue. this will not

only assist it to have an adequate controlling but it will also act as a guide to carry out its

business operating activities.

However, on a critical note it is to be noted that the installation cost of the management

accounting technique is usually high that the normal and the small business can’t afford it. Thus,

determination of its usage and advantages and the cost associated is to be considered before

implementing this accounting. Likewise, in the same manner the approximation percentage

associated with the management accounting is also high (Shil, Hoque and Akter, 2019). This

means the data that is being derived and forecasted is based on approximation and not 100%

accurate. Thus, before adopting and implementing this management accounting into practice by

the SKANSKA PLC this point is also needed to be considered that the forecasted budgets and

the costing is just approximate and not 100% accurate.

then the actual performance and the associated cost is being compared then it will directly lead to

controlling and determination of fluctuation. Likewise, making of financial planning also enable

the company including the SKANSKA PLC to make the plan regarding the future.

In the same manner, decision making accounting also enable the company including the

SKANSKA PLC to determine the best alternative so that the most appropriate decision would be

taken. It is also to be noted that the company by adopting and using the management accounting

technique can have a better analysis and control over their daily operation and business operation

because under this accounting a direct check over the operation is being established.

Through the adoption and execution of this accounting practice by the SKANSKA PLC, it

can better operate its business operation along with keeping a good controlling. This means as

through this technique it will perform various technique and thereby as a result of those it can

better perform its business and move in the direction of the accomplishment of its objectives.

Likewise, an association of cost and the budgetary technique also guide the company regarding

the estimation of the required cost or the estimated budgets regarding the future. This means that

through management accounting the SKANKA PLC can determine the cost element of the

process along with determination of the estimated future expenses and the revenue. this will not

only assist it to have an adequate controlling but it will also act as a guide to carry out its

business operating activities.

However, on a critical note it is to be noted that the installation cost of the management

accounting technique is usually high that the normal and the small business can’t afford it. Thus,

determination of its usage and advantages and the cost associated is to be considered before

implementing this accounting. Likewise, in the same manner the approximation percentage

associated with the management accounting is also high (Shil, Hoque and Akter, 2019). This

means the data that is being derived and forecasted is based on approximation and not 100%

accurate. Thus, before adopting and implementing this management accounting into practice by

the SKANSKA PLC this point is also needed to be considered that the forecasted budgets and

the costing is just approximate and not 100% accurate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above report it is concluded that management accounting plays an important role

in terms of financial decision making along with controlling. This means that through the

concept of management accounting the company can make the financial planning along with

controlling its expenditure through the use of standard costing and other technique. This report

also summarizes that SKANKA PLC by having an implementation of the management

accounting can make and operate their business activities with better controlling. Management

accounting also enable the company to take the most appropriate decision by having an

evaluation of various available alternatives. Through this report an understanding about the

various techniques of management accounting is also being understood that how they play an

important role in terms of decision making, controlling and planning regarding the future.

From the above report it is concluded that management accounting plays an important role

in terms of financial decision making along with controlling. This means that through the

concept of management accounting the company can make the financial planning along with

controlling its expenditure through the use of standard costing and other technique. This report

also summarizes that SKANKA PLC by having an implementation of the management

accounting can make and operate their business activities with better controlling. Management

accounting also enable the company to take the most appropriate decision by having an

evaluation of various available alternatives. Through this report an understanding about the

various techniques of management accounting is also being understood that how they play an

important role in terms of decision making, controlling and planning regarding the future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting. 2019(3). p.2.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Argenti, J., 2018. Management techniques: a practical guide. Routledge.

Popescu, A.M., 2020. The Importance of Accounting Information for Stakeholders. Ovidius

University Annals, Economic Sciences Series. 20(2). pp.1117-1121.

Pradhan, D., Swain, P.K. and Dash, M., 2018. Effect of management accounting techniques on

supply chain and firm performance: An empirical study. International Journal of

Mechanical Engineering and Technology. 9(5). pp.1049-1057.

Pretorius, P., 2020, July. Finance function as a business system. In INCOSE International

Symposium (Vol. 30, No. 1, pp. 1606-1620).

Shil, N.C., Hoque, M. and Akter, M., 2019. Revisiting Management Accounting Practice Gap: A

Proposed PERAPPGAP Model. Journal of Accounting and Finance. 19(1). pp.135-155.

Online references

Skanska UK in brief., 2021. [Online]. Available through < https://www.skanska.co.uk/about-

skanska/skanska-in-the-uk/skanska-uk-in-brief/ >

1

Books and journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting. 2019(3). p.2.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Argenti, J., 2018. Management techniques: a practical guide. Routledge.

Popescu, A.M., 2020. The Importance of Accounting Information for Stakeholders. Ovidius

University Annals, Economic Sciences Series. 20(2). pp.1117-1121.

Pradhan, D., Swain, P.K. and Dash, M., 2018. Effect of management accounting techniques on

supply chain and firm performance: An empirical study. International Journal of

Mechanical Engineering and Technology. 9(5). pp.1049-1057.

Pretorius, P., 2020, July. Finance function as a business system. In INCOSE International

Symposium (Vol. 30, No. 1, pp. 1606-1620).

Shil, N.C., Hoque, M. and Akter, M., 2019. Revisiting Management Accounting Practice Gap: A

Proposed PERAPPGAP Model. Journal of Accounting and Finance. 19(1). pp.135-155.

Online references

Skanska UK in brief., 2021. [Online]. Available through < https://www.skanska.co.uk/about-

skanska/skanska-in-the-uk/skanska-uk-in-brief/ >

1

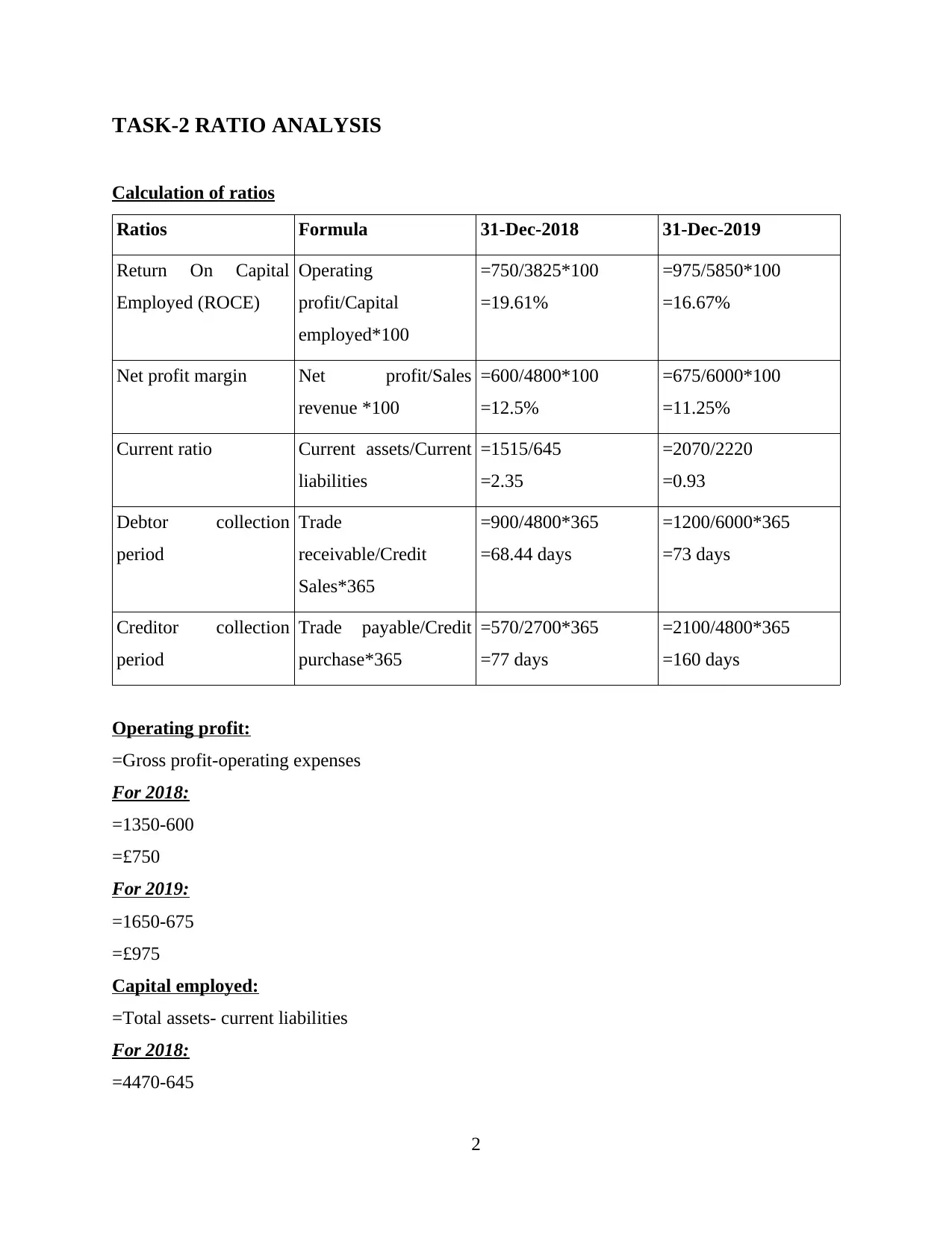

TASK-2 RATIO ANALYSIS

Calculation of ratios

Ratios Formula 31-Dec-2018 31-Dec-2019

Return On Capital

Employed (ROCE)

Operating

profit/Capital

employed*100

=750/3825*100

=19.61%

=975/5850*100

=16.67%

Net profit margin Net profit/Sales

revenue *100

=600/4800*100

=12.5%

=675/6000*100

=11.25%

Current ratio Current assets/Current

liabilities

=1515/645

=2.35

=2070/2220

=0.93

Debtor collection

period

Trade

receivable/Credit

Sales*365

=900/4800*365

=68.44 days

=1200/6000*365

=73 days

Creditor collection

period

Trade payable/Credit

purchase*365

=570/2700*365

=77 days

=2100/4800*365

=160 days

Operating profit:

=Gross profit-operating expenses

For 2018:

=1350-600

=£750

For 2019:

=1650-675

=£975

Capital employed:

=Total assets- current liabilities

For 2018:

=4470-645

2

Calculation of ratios

Ratios Formula 31-Dec-2018 31-Dec-2019

Return On Capital

Employed (ROCE)

Operating

profit/Capital

employed*100

=750/3825*100

=19.61%

=975/5850*100

=16.67%

Net profit margin Net profit/Sales

revenue *100

=600/4800*100

=12.5%

=675/6000*100

=11.25%

Current ratio Current assets/Current

liabilities

=1515/645

=2.35

=2070/2220

=0.93

Debtor collection

period

Trade

receivable/Credit

Sales*365

=900/4800*365

=68.44 days

=1200/6000*365

=73 days

Creditor collection

period

Trade payable/Credit

purchase*365

=570/2700*365

=77 days

=2100/4800*365

=160 days

Operating profit:

=Gross profit-operating expenses

For 2018:

=1350-600

=£750

For 2019:

=1650-675

=£975

Capital employed:

=Total assets- current liabilities

For 2018:

=4470-645

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=3825

For 2019:

=8070-2220

= 5850

Performance of SKANSKA PLC

Accounting ratio and their importance:

Accounting ratio:

It refers to the comparison of two or more financial data of the company and drawing

interferences and on the basis of analysation of the financial statement. In simple words, these

ratios are used to be calculated with the reference of financial statement of the company (Wild,

2019). It is counted as an important tool for the stakeholders of the company in terms of

measuring the profitability and financial performance of the company.

Importance:

It is important for the calculation of accounting ratio because through their calculation the

company including SKANSKA PLC can determine its efficiency along with its financial

performance. These ratio act as a base that help the company to make self-evaluation and

analysation of its performance. It is also important in determining the relation between the

variables of accounting with one another.

Return on capital employed (ROCE):

It is an important financial ratio that measure the amount of return that is being earned

over the capital employed. This means that through this ratio the profitability and efficiency of

the company can be analysed (Hague, 2018). In simple words this ratio helps to determine the

what the company is being generating from the capital being employed and used.

Importance:

This ratio is highly important for the SKANSKA PLC because through this ratio it can

determine the actual profit that is being earned by the company from the capital employed or the

capital operation. This means that through the calculation of this ratio the company can

determine its efficiency of business operation and the capital that is being used and implemented

into the company (Andjelic and Vesic, 2017).

3

For 2019:

=8070-2220

= 5850

Performance of SKANSKA PLC

Accounting ratio and their importance:

Accounting ratio:

It refers to the comparison of two or more financial data of the company and drawing

interferences and on the basis of analysation of the financial statement. In simple words, these

ratios are used to be calculated with the reference of financial statement of the company (Wild,

2019). It is counted as an important tool for the stakeholders of the company in terms of

measuring the profitability and financial performance of the company.

Importance:

It is important for the calculation of accounting ratio because through their calculation the

company including SKANSKA PLC can determine its efficiency along with its financial

performance. These ratio act as a base that help the company to make self-evaluation and

analysation of its performance. It is also important in determining the relation between the

variables of accounting with one another.

Return on capital employed (ROCE):

It is an important financial ratio that measure the amount of return that is being earned

over the capital employed. This means that through this ratio the profitability and efficiency of

the company can be analysed (Hague, 2018). In simple words this ratio helps to determine the

what the company is being generating from the capital being employed and used.

Importance:

This ratio is highly important for the SKANSKA PLC because through this ratio it can

determine the actual profit that is being earned by the company from the capital employed or the

capital operation. This means that through the calculation of this ratio the company can

determine its efficiency of business operation and the capital that is being used and implemented

into the company (Andjelic and Vesic, 2017).

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Comparison:

While comparing the ROCE of 2018 and 2019 of SKANSKA PLC it can be analysed that

the ratio decreases from 19.61 to 16.67%. a decline in the ratio is an indication of the poor

efficiency of the company with regard to the business operation. as the ratio is declining which

can also mean that the company is not efficiently utilising its capital

Cause:

The main cause behind such declining ratio may include improper planning of the

SKANSKA PLC with regard to the use of the capital. As the ratio usually decline because of the

raising capital employed which means that either the capital is more than required or there is

shortage which is ultimately declining the ratio.

Improvement:

The SKANSKA PLC can improve this ratio if it will focus over the proper utilisation of

the capital. It can also be raised if the company will focus on reducing the cost and raising the

percentage of sales (SUGARA, 2017). Likewise, disposal of un-useful assets may also improve

the ratio.

Net profit margin:

This ratio is concerned with the generation and the measurement of the net profit and the

margin that is being earned by the company over its revenue. this means that through this ratio

the company can determine the net profit that is being earned by it over its revenue (Soboleva

and et.al., 2018).

Importance:

This is an important ratio because through its calculation SKANSKA PLC can determine

that whether it is performing or operating its business towards the direction of its objective or

not. As the main aim of every company is to earn profit so this ratio would help the company to

have an analysis that whether they have achieved their objective or not.

Comparison:

While comparing the net profit ratio of SKANSKA PLC it is being analysed that the ratio

was 12.5% in 2018 which decline to 11.25% in 2019. This means that the company’s capacity of

earning profit decline from the previous year. In simple words the company’s ability to earn

profit is decline.

4

While comparing the ROCE of 2018 and 2019 of SKANSKA PLC it can be analysed that

the ratio decreases from 19.61 to 16.67%. a decline in the ratio is an indication of the poor

efficiency of the company with regard to the business operation. as the ratio is declining which

can also mean that the company is not efficiently utilising its capital

Cause:

The main cause behind such declining ratio may include improper planning of the

SKANSKA PLC with regard to the use of the capital. As the ratio usually decline because of the

raising capital employed which means that either the capital is more than required or there is

shortage which is ultimately declining the ratio.

Improvement:

The SKANSKA PLC can improve this ratio if it will focus over the proper utilisation of

the capital. It can also be raised if the company will focus on reducing the cost and raising the

percentage of sales (SUGARA, 2017). Likewise, disposal of un-useful assets may also improve

the ratio.

Net profit margin:

This ratio is concerned with the generation and the measurement of the net profit and the

margin that is being earned by the company over its revenue. this means that through this ratio

the company can determine the net profit that is being earned by it over its revenue (Soboleva

and et.al., 2018).

Importance:

This is an important ratio because through its calculation SKANSKA PLC can determine

that whether it is performing or operating its business towards the direction of its objective or

not. As the main aim of every company is to earn profit so this ratio would help the company to

have an analysis that whether they have achieved their objective or not.

Comparison:

While comparing the net profit ratio of SKANSKA PLC it is being analysed that the ratio

was 12.5% in 2018 which decline to 11.25% in 2019. This means that the company’s capacity of

earning profit decline from the previous year. In simple words the company’s ability to earn

profit is decline.

4

Cause:

The main cause of declining ratio with the SKANSKA PLC may include poor cost

structure or the inadequate pricing policy of the company. This means that an incurring high cost

of operation and low selling price may lead to decline in the net profit margin for the company.

Improvement:

However, it can be improved if the company will focus over reducing the cost of

operation along with raising the sales of its project. This means that if the company will improve

the sale and minimise the operating profit then its share or percentage of profit margin will

automatically raise.

Current ratio:

It is the ratio of current asset to current liability. This ratio is also known as liquidity

ratio. This ratio indicates that how easily the company can meet its short term obligation and pay

its short term debts (Sengupta, 2020). This ratio tells the investors that how the company can

maximise its assets in order to satisfy its debts and liabilities.

Importance:

This is most important ratio for the investor to analyse and know that whether the

company is efficient in order to cover and meet its short terms debts and liabilities (Rashid,

2018). This is also an important ratio for SKANSKA PLC too because through this ratio it can

also make self-evaluation about its liquidity position.

Comparison:

With regard to current ratio of SKANSKA PLC of 2018 and 2019, it is being seen that

the ratio is declining from 2.35 to 0.93. this shows that the ability of the company with regard to

meeting the short terms obligations are also declining and reducing. This reducing percentage

also shows that company’s current liabilities are also raising with respect to time.

Cause:

The main cause for such declining ratio could be the non-availability of sufficient funds

for the payment of liabilities. It may also be due to improper use of business resources with

respect to payment of debts. Likewise, as it is seen that current liabilities are increased so it may

also be counted as a major cause.

Improvement:

5

The main cause of declining ratio with the SKANSKA PLC may include poor cost

structure or the inadequate pricing policy of the company. This means that an incurring high cost

of operation and low selling price may lead to decline in the net profit margin for the company.

Improvement:

However, it can be improved if the company will focus over reducing the cost of

operation along with raising the sales of its project. This means that if the company will improve

the sale and minimise the operating profit then its share or percentage of profit margin will

automatically raise.

Current ratio:

It is the ratio of current asset to current liability. This ratio is also known as liquidity

ratio. This ratio indicates that how easily the company can meet its short term obligation and pay

its short term debts (Sengupta, 2020). This ratio tells the investors that how the company can

maximise its assets in order to satisfy its debts and liabilities.

Importance:

This is most important ratio for the investor to analyse and know that whether the

company is efficient in order to cover and meet its short terms debts and liabilities (Rashid,

2018). This is also an important ratio for SKANSKA PLC too because through this ratio it can

also make self-evaluation about its liquidity position.

Comparison:

With regard to current ratio of SKANSKA PLC of 2018 and 2019, it is being seen that

the ratio is declining from 2.35 to 0.93. this shows that the ability of the company with regard to

meeting the short terms obligations are also declining and reducing. This reducing percentage

also shows that company’s current liabilities are also raising with respect to time.

Cause:

The main cause for such declining ratio could be the non-availability of sufficient funds

for the payment of liabilities. It may also be due to improper use of business resources with

respect to payment of debts. Likewise, as it is seen that current liabilities are increased so it may

also be counted as a major cause.

Improvement:

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.