Financial Resource Management and Decision Making Report for GSK

VerifiedAdded on 2019/12/03

|17

|4540

|29

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and decision-making, focusing on the case of Glaxosmithkline. The report begins by identifying various sources of finance available to the business, including equity, debentures, retained earnings, and consortium finance, and discusses the implications of each. It then assesses the appropriateness of these sources for Glaxosmithkline, highlighting the importance of equity and retained earnings. The report further delves into the cost of different sources of finance and the significance of financial planning. It examines the information needs of various decision-makers, such as managers, shareholders, government, and creditors, and analyzes the impact of finance on financial statements. The analysis includes a detailed budget review, unit cost calculations, and project evaluation techniques. Finally, the report concludes with a ratio analysis of Glaxosmithkline's financial performance, offering valuable insights into the company's financial health and strategic decision-making.

MANAGING FINANCIAL

RESOURCES AND DECISON

MAKING

RESOURCES AND DECISON

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available to business..........................................................................1

1.2 Implications of different source of finance......................................................................2

1.3 Appropriate source of finance..........................................................................................2

TASK 2............................................................................................................................................3

2.1 Cost of different source of finance...................................................................................3

2.2 Importance of financial planning .....................................................................................4

2.3 Information needs of different decision makers...............................................................4

2.4 Impact of finance on financial statements .......................................................................5

TASK 3............................................................................................................................................5

3.1 Analysis of budget............................................................................................................5

3.2 Calculation of unit cost ....................................................................................................6

3.3 Project evaluation techniques...........................................................................................6

TASK 4............................................................................................................................................9

4.1 Financial statements.........................................................................................................9

4.2 Format of financial statements for the firm......................................................................9

4.3 Ratio analysis .................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available to business..........................................................................1

1.2 Implications of different source of finance......................................................................2

1.3 Appropriate source of finance..........................................................................................2

TASK 2............................................................................................................................................3

2.1 Cost of different source of finance...................................................................................3

2.2 Importance of financial planning .....................................................................................4

2.3 Information needs of different decision makers...............................................................4

2.4 Impact of finance on financial statements .......................................................................5

TASK 3............................................................................................................................................5

3.1 Analysis of budget............................................................................................................5

3.2 Calculation of unit cost ....................................................................................................6

3.3 Project evaluation techniques...........................................................................................6

TASK 4............................................................................................................................................9

4.1 Financial statements.........................................................................................................9

4.2 Format of financial statements for the firm......................................................................9

4.3 Ratio analysis .................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INDEX OF TABLES

Table 1: Calculation of budget ........................................................................................................5

Table 2: Calculation of unity cost....................................................................................................6

Table 3: Calculation of IRR.............................................................................................................7

Table 4: Calculation of pay back period method.............................................................................8

Table 5: Ratio analysis of Glaxosmithkline...................................................................................10

Table 1: Calculation of budget ........................................................................................................5

Table 2: Calculation of unity cost....................................................................................................6

Table 3: Calculation of IRR.............................................................................................................7

Table 4: Calculation of pay back period method.............................................................................8

Table 5: Ratio analysis of Glaxosmithkline...................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Glaxosmithkline is the UK’s giant pharmaceutical company which is operating its

business across several nations of the world. In this report, sources of finance are described in

detail and their appropriateness for an organization is also determined. Further, budget is also

discussed in detail and comments on same are given. After that, project evaluation techniques are

discussed and practically applied on the firm’s cash flows. At the end of the report, ratio analysis

of Glaxosmithkline is done and comments are done on the performance of company.

TASK 1

1.1 Sources of finance available to business

Sources of finance available to Glaxosmithkline are as follows: Equity- Glaxosmithkline is primarily listed in UK and it is also listed on other recognized

stock exchanges like NYSE, NSE and BSE. Company for expanding its business can

raise capital through issuing FPO. Firm by using capital raised from issue of equity can

develop its distribution system and can invest money in its R&D activities. Debenture- Glaxosmithkline can also issue debentures in order to take loan from the

public at the specific interest rate (Brici, Hodkinson and Sullivan-Mort, 2013). Company

in return will be required to pay interest annually irrespective of its profitability. Thus, in

case of late execution of development of new or generic drug project, firm may find it

difficult to pay interest on time. Retained earnings- Like other companies, Glaxosmithkline can also use retained

earnings to finance its day to day working capital requirements. Effective utilization of

retained earnings will reduce the firm’s dependability on debt for performing day to day

operations.

Consortium finance- Under this source of finance, a group of banks finance a single

project that belongs to an individual firm. One of these banks acts as the leader of cartel

of banks and coordinates all financing and group discussion activity among member

banks (Collis and Jarvis, 2002). By using this source of finance, large projects easily get

financed and due to this reason, this source of finance is very popular in USA and UK.

1.2 Implications of different source of finance

Following are the implications of different sources of finance:

1

Glaxosmithkline is the UK’s giant pharmaceutical company which is operating its

business across several nations of the world. In this report, sources of finance are described in

detail and their appropriateness for an organization is also determined. Further, budget is also

discussed in detail and comments on same are given. After that, project evaluation techniques are

discussed and practically applied on the firm’s cash flows. At the end of the report, ratio analysis

of Glaxosmithkline is done and comments are done on the performance of company.

TASK 1

1.1 Sources of finance available to business

Sources of finance available to Glaxosmithkline are as follows: Equity- Glaxosmithkline is primarily listed in UK and it is also listed on other recognized

stock exchanges like NYSE, NSE and BSE. Company for expanding its business can

raise capital through issuing FPO. Firm by using capital raised from issue of equity can

develop its distribution system and can invest money in its R&D activities. Debenture- Glaxosmithkline can also issue debentures in order to take loan from the

public at the specific interest rate (Brici, Hodkinson and Sullivan-Mort, 2013). Company

in return will be required to pay interest annually irrespective of its profitability. Thus, in

case of late execution of development of new or generic drug project, firm may find it

difficult to pay interest on time. Retained earnings- Like other companies, Glaxosmithkline can also use retained

earnings to finance its day to day working capital requirements. Effective utilization of

retained earnings will reduce the firm’s dependability on debt for performing day to day

operations.

Consortium finance- Under this source of finance, a group of banks finance a single

project that belongs to an individual firm. One of these banks acts as the leader of cartel

of banks and coordinates all financing and group discussion activity among member

banks (Collis and Jarvis, 2002). By using this source of finance, large projects easily get

financed and due to this reason, this source of finance is very popular in USA and UK.

1.2 Implications of different source of finance

Following are the implications of different sources of finance:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Equity- Issue of FPO will dilute the control of existing shareholders in company. In other

words, it can also be said that existing shareholders of Glaxosmithkline will lose their

control in organization. As a result, existing shareholders will not be able to take freely

their business related decisions (Keller, 2013). Lack of consensus among new and old

shareholders may create problems to some extent for company’s management in taking

decisions quickly. Debentures- Issue of debentures will make payment of interest inevitable for the firm. In

case of downturn in economy and negative change in pharmaceutical policy in terms of

price control and frequency of issue of tender may reduce the profitability of

Glaxosmithkline. In that case, finance cost may create burden on company and its net

profit may decline sharply due to mentioned reasons. Retained earnings- Retained earnings must be invested in a prudent manner so that firm

reduces its dependence on other sources of finance (Nga and Ken Yien, 2013). Use of

this source of finance does not dilute the control of existing shareholders and due to this

reason; it can be termed as cost free source of finance.

Consortium finance- Under this source of finance, as mentioned above, one bank takes

loan from several banks at fixed or floating interest rate. In case of fluctuation in

currency, firm’s aggregate interest amount may elevate. Thus, this source of finance must

be used with care.

1.3 Appropriate source of finance

Equity- This source of finance is appropriate for Glaxosmithkline and there are many

reasons for proving the appropriateness of equity for company. Some of the reasons are given

below: USFDA – USFDA is the USA’s largest authority that gives clearance to launch of API

(Active pharmaceutical ingredients) and generic medicines. Ban on sale of medicines

from USFDA certainly create problems for Glaxosmithkline (Srinivasan, 2012). This will

ultimately lead to fall in revenue or winding up of operations in USA which is world’s

largest market for generic drugs. In such a case, huge debt in firm’s balance sheet may

create problems for company in the future. Failure to complete project on time- Glaxosmithkline management determines the

completion time of project and accordingly, they make their expenditures. Late

2

words, it can also be said that existing shareholders of Glaxosmithkline will lose their

control in organization. As a result, existing shareholders will not be able to take freely

their business related decisions (Keller, 2013). Lack of consensus among new and old

shareholders may create problems to some extent for company’s management in taking

decisions quickly. Debentures- Issue of debentures will make payment of interest inevitable for the firm. In

case of downturn in economy and negative change in pharmaceutical policy in terms of

price control and frequency of issue of tender may reduce the profitability of

Glaxosmithkline. In that case, finance cost may create burden on company and its net

profit may decline sharply due to mentioned reasons. Retained earnings- Retained earnings must be invested in a prudent manner so that firm

reduces its dependence on other sources of finance (Nga and Ken Yien, 2013). Use of

this source of finance does not dilute the control of existing shareholders and due to this

reason; it can be termed as cost free source of finance.

Consortium finance- Under this source of finance, as mentioned above, one bank takes

loan from several banks at fixed or floating interest rate. In case of fluctuation in

currency, firm’s aggregate interest amount may elevate. Thus, this source of finance must

be used with care.

1.3 Appropriate source of finance

Equity- This source of finance is appropriate for Glaxosmithkline and there are many

reasons for proving the appropriateness of equity for company. Some of the reasons are given

below: USFDA – USFDA is the USA’s largest authority that gives clearance to launch of API

(Active pharmaceutical ingredients) and generic medicines. Ban on sale of medicines

from USFDA certainly create problems for Glaxosmithkline (Srinivasan, 2012). This will

ultimately lead to fall in revenue or winding up of operations in USA which is world’s

largest market for generic drugs. In such a case, huge debt in firm’s balance sheet may

create problems for company in the future. Failure to complete project on time- Glaxosmithkline management determines the

completion time of project and accordingly, they make their expenditures. Late

2

completion of project will result in delaying expected cash inflows while there will be

little change in the cash outflow. Mismanagement between both variables will create the

problem for Glaxosmithkline and this may find it difficult to pay interest on time. Issue of

FPO protects the firm from facing such kind of problems because payment of dividend

each year is not necessary.

Expiry of patent- When patent of any drug gets expired, many generic medicines

launched in the market by several companies. Expiry of patent and intensification of

competition to a large extent reduces the firm’s profitability. Payment of interest further

fuel problem for Glaxosmithkline (Tauringana and Afrifa, 2013). Issue of shares protects

the firm from reducing such kind of problems and helps in running business smoothly

even if business conditions are unfavorable.

Thus, by considering these factors, equity and retained earnings are considered as the

appropriate sources of finance for Glaxosmithkline.

TASK 2

2.1 Cost of different sources of finance

Following are the costs of different sources of finance: Equity- In case of issue of shares, firm is required to pay dividend to its shareholders.

Normally, companies follow specific dividend policy in relation to dividend payment. It

has been seen that rate of dividend is always higher than interest. Hence, this source of

finance is much dearer than debt or consortium finance. However, the big relaxation that

equity gives to company is that payment of dividend is not necessary in case of this

source of finance (Vance, 2002). Debenture- In case of debenture, interest is paid and it is cost this source of finance. This

interest rate remains fixed irrespective of change in currency and interest rates. Hence,

issue of debentures is much better than borrowing a corpus form banks or NBFC'S. Retained earnings- There is not any cost of this source of finance because retained

earnings is a part of revenue that firm earns on sales. However, cost of retained earnings

is calculated and is done by using CAPM model. This model gives minimum return that

shareholders must earn on their investment in the firm. Hence, Glaxosmithkline must

earn this minimum return on the investment of retained earnings.

3

little change in the cash outflow. Mismanagement between both variables will create the

problem for Glaxosmithkline and this may find it difficult to pay interest on time. Issue of

FPO protects the firm from facing such kind of problems because payment of dividend

each year is not necessary.

Expiry of patent- When patent of any drug gets expired, many generic medicines

launched in the market by several companies. Expiry of patent and intensification of

competition to a large extent reduces the firm’s profitability. Payment of interest further

fuel problem for Glaxosmithkline (Tauringana and Afrifa, 2013). Issue of shares protects

the firm from reducing such kind of problems and helps in running business smoothly

even if business conditions are unfavorable.

Thus, by considering these factors, equity and retained earnings are considered as the

appropriate sources of finance for Glaxosmithkline.

TASK 2

2.1 Cost of different sources of finance

Following are the costs of different sources of finance: Equity- In case of issue of shares, firm is required to pay dividend to its shareholders.

Normally, companies follow specific dividend policy in relation to dividend payment. It

has been seen that rate of dividend is always higher than interest. Hence, this source of

finance is much dearer than debt or consortium finance. However, the big relaxation that

equity gives to company is that payment of dividend is not necessary in case of this

source of finance (Vance, 2002). Debenture- In case of debenture, interest is paid and it is cost this source of finance. This

interest rate remains fixed irrespective of change in currency and interest rates. Hence,

issue of debentures is much better than borrowing a corpus form banks or NBFC'S. Retained earnings- There is not any cost of this source of finance because retained

earnings is a part of revenue that firm earns on sales. However, cost of retained earnings

is calculated and is done by using CAPM model. This model gives minimum return that

shareholders must earn on their investment in the firm. Hence, Glaxosmithkline must

earn this minimum return on the investment of retained earnings.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Consortium finance- Like debentures in case of consortium finance also, interest is paid

to banks at specific interest rate (Way and Jeanine Meyers, 2013). Under this source of

finance, Glaxosmithkline is not exposed to currency fluctuation because all banks in

cartel belong to domestic land. However, interest charged by these banks may be

different from each other.

2.2 Importance of financial planning

Financial planning helps Glaxosmithkline in making all expenses in alignment with the

expected cash inflows. Further, this also helps in the allocation of fund among several

organizations for different activities like R&D activity, expansion of distribution system and

hedging activities. With respect to this, management of Glaxosmithkline will determine an

aggregate amount (Siano and Confetto, 2010). After determining the budgeted amount, this value

will be divided into these three mentioned activities. Such kind of financial planning will help

the managers in effective utilization of cash for the benefit of an organization.

2.3 Information needs of different decision makers Managers- They are operating at top, middle and lower level of management and needs

accounting information in order to identify the position where company stands. On the

basis of such kind of information, managers take strategic decisions in order to make

their position strong on weak areas. Shareholders- The shareholders are one that makes investment in the firm and due to this

reason, they need accounting information for taking decision regarding keeping

investment in the organization or withdrawing same from company (Lascu, 2013).

Hence, they are keenly waiting for company’s quarterly results. Government- Company pay tax to the government authorities and these bodies are

interested in identifying that whether the firm is paying loan on time or not. If on

identification, it is found that firm is not paying full amount of tax then these bodies take

strict actions against the culprit firm.

Creditors- These entities give loan to company and that debt amount may be secured or

unsecured in nature. Creditors by using firm’s financial statements can evaluate its

current financial position and performance on the basis of various parameters (Galloway,

4

to banks at specific interest rate (Way and Jeanine Meyers, 2013). Under this source of

finance, Glaxosmithkline is not exposed to currency fluctuation because all banks in

cartel belong to domestic land. However, interest charged by these banks may be

different from each other.

2.2 Importance of financial planning

Financial planning helps Glaxosmithkline in making all expenses in alignment with the

expected cash inflows. Further, this also helps in the allocation of fund among several

organizations for different activities like R&D activity, expansion of distribution system and

hedging activities. With respect to this, management of Glaxosmithkline will determine an

aggregate amount (Siano and Confetto, 2010). After determining the budgeted amount, this value

will be divided into these three mentioned activities. Such kind of financial planning will help

the managers in effective utilization of cash for the benefit of an organization.

2.3 Information needs of different decision makers Managers- They are operating at top, middle and lower level of management and needs

accounting information in order to identify the position where company stands. On the

basis of such kind of information, managers take strategic decisions in order to make

their position strong on weak areas. Shareholders- The shareholders are one that makes investment in the firm and due to this

reason, they need accounting information for taking decision regarding keeping

investment in the organization or withdrawing same from company (Lascu, 2013).

Hence, they are keenly waiting for company’s quarterly results. Government- Company pay tax to the government authorities and these bodies are

interested in identifying that whether the firm is paying loan on time or not. If on

identification, it is found that firm is not paying full amount of tax then these bodies take

strict actions against the culprit firm.

Creditors- These entities give loan to company and that debt amount may be secured or

unsecured in nature. Creditors by using firm’s financial statements can evaluate its

current financial position and performance on the basis of various parameters (Galloway,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Morrison and Deakins, 2002). On the basis of this evaluation, they decide whether to give

loan to company or not.

2.4 Impact of finance on financial statements

Finance to a large extent has an effect on financial statements of the firm. Every year

Glaxosmithkline takes a loan in order to finance its long and short term finance requirements.

When firm takes loan, its liability side gets increased by loan amount under the head “Creditors”.

Firm receives cash and due to this reason, same amount is added to cash in the current assets in

asset side of the balance sheet (Ingram and Albright, 2006). If company takes loan then it has to

pay interest on same and this interest is shown in the P&L statement. Similarly, if

Glaxosmithkline issues equity shares then shareholder’s equity will get enhanced by issue of

capital at face value. Premium amount can be added to reserves and surplus head which are

appeared in the asset side of balance sheet. In this way, debt and issue of share capital affects the

firm’s financial statements.

TASK 3

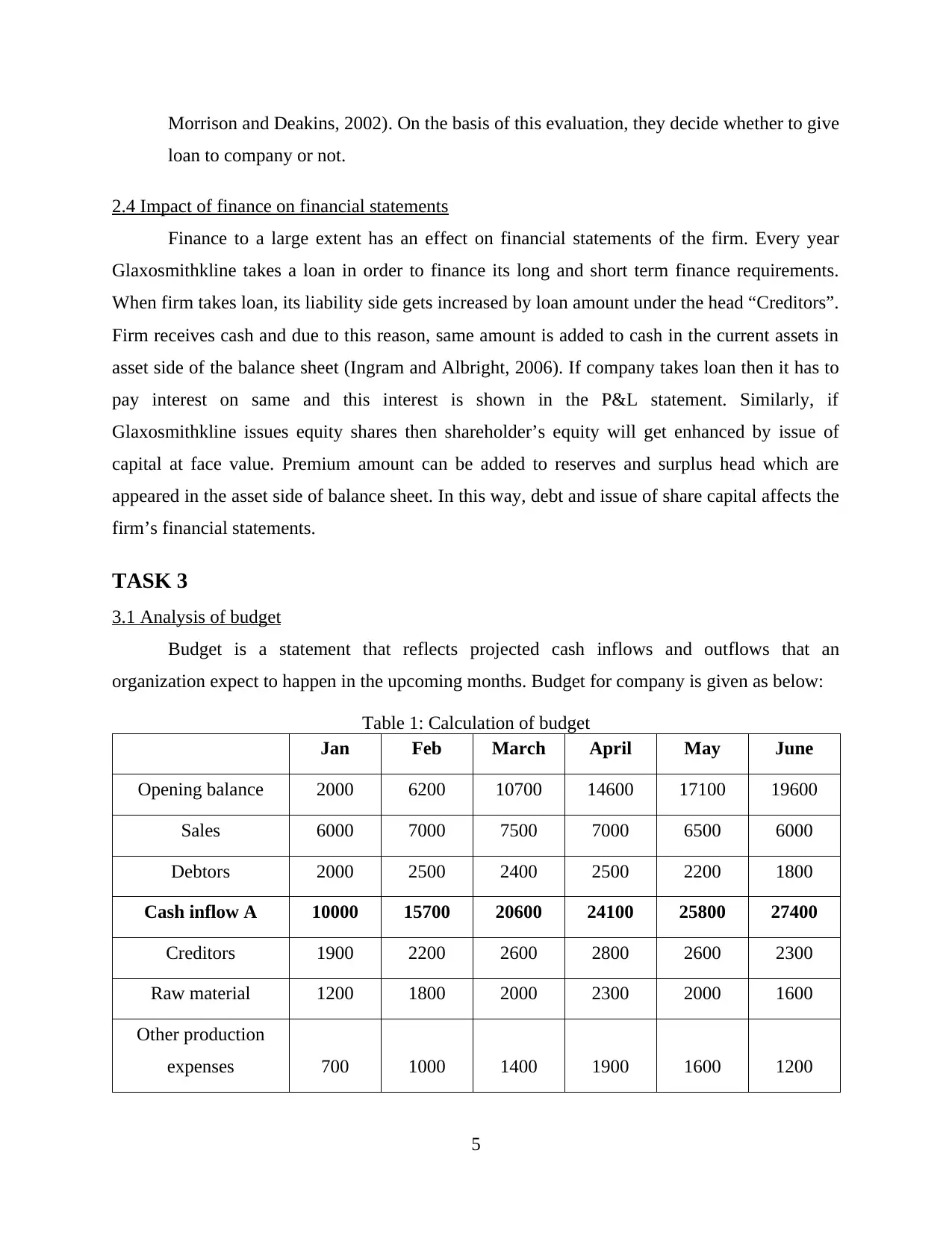

3.1 Analysis of budget

Budget is a statement that reflects projected cash inflows and outflows that an

organization expect to happen in the upcoming months. Budget for company is given as below:

Table 1: Calculation of budget

Jan Feb March April May June

Opening balance 2000 6200 10700 14600 17100 19600

Sales 6000 7000 7500 7000 6500 6000

Debtors 2000 2500 2400 2500 2200 1800

Cash inflow A 10000 15700 20600 24100 25800 27400

Creditors 1900 2200 2600 2800 2600 2300

Raw material 1200 1800 2000 2300 2000 1600

Other production

expenses 700 1000 1400 1900 1600 1200

5

loan to company or not.

2.4 Impact of finance on financial statements

Finance to a large extent has an effect on financial statements of the firm. Every year

Glaxosmithkline takes a loan in order to finance its long and short term finance requirements.

When firm takes loan, its liability side gets increased by loan amount under the head “Creditors”.

Firm receives cash and due to this reason, same amount is added to cash in the current assets in

asset side of the balance sheet (Ingram and Albright, 2006). If company takes loan then it has to

pay interest on same and this interest is shown in the P&L statement. Similarly, if

Glaxosmithkline issues equity shares then shareholder’s equity will get enhanced by issue of

capital at face value. Premium amount can be added to reserves and surplus head which are

appeared in the asset side of balance sheet. In this way, debt and issue of share capital affects the

firm’s financial statements.

TASK 3

3.1 Analysis of budget

Budget is a statement that reflects projected cash inflows and outflows that an

organization expect to happen in the upcoming months. Budget for company is given as below:

Table 1: Calculation of budget

Jan Feb March April May June

Opening balance 2000 6200 10700 14600 17100 19600

Sales 6000 7000 7500 7000 6500 6000

Debtors 2000 2500 2400 2500 2200 1800

Cash inflow A 10000 15700 20600 24100 25800 27400

Creditors 1900 2200 2600 2800 2600 2300

Raw material 1200 1800 2000 2300 2000 1600

Other production

expenses 700 1000 1400 1900 1600 1200

5

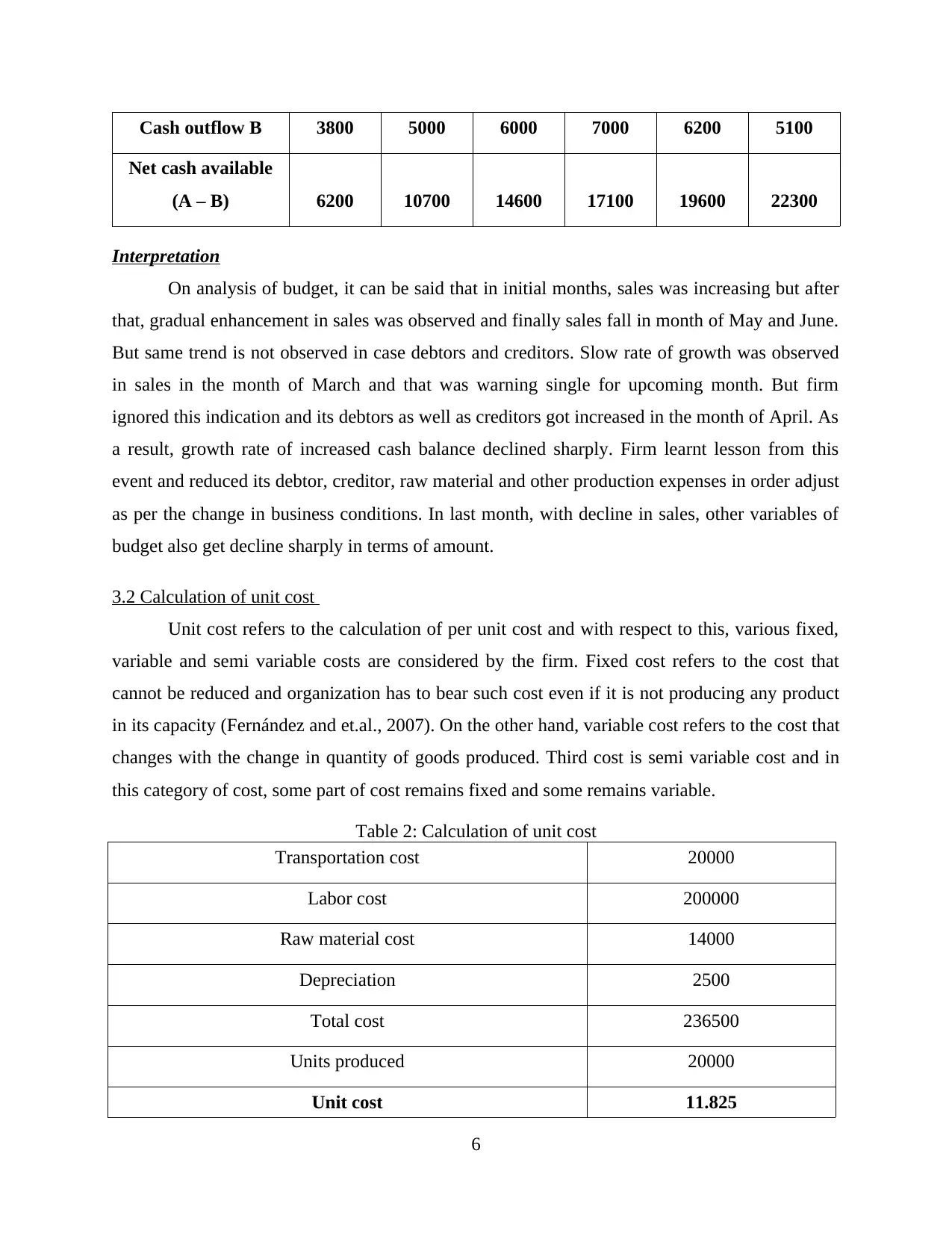

Cash outflow B 3800 5000 6000 7000 6200 5100

Net cash available

(A – B) 6200 10700 14600 17100 19600 22300

Interpretation

On analysis of budget, it can be said that in initial months, sales was increasing but after

that, gradual enhancement in sales was observed and finally sales fall in month of May and June.

But same trend is not observed in case debtors and creditors. Slow rate of growth was observed

in sales in the month of March and that was warning single for upcoming month. But firm

ignored this indication and its debtors as well as creditors got increased in the month of April. As

a result, growth rate of increased cash balance declined sharply. Firm learnt lesson from this

event and reduced its debtor, creditor, raw material and other production expenses in order adjust

as per the change in business conditions. In last month, with decline in sales, other variables of

budget also get decline sharply in terms of amount.

3.2 Calculation of unit cost

Unit cost refers to the calculation of per unit cost and with respect to this, various fixed,

variable and semi variable costs are considered by the firm. Fixed cost refers to the cost that

cannot be reduced and organization has to bear such cost even if it is not producing any product

in its capacity (Fernández and et.al., 2007). On the other hand, variable cost refers to the cost that

changes with the change in quantity of goods produced. Third cost is semi variable cost and in

this category of cost, some part of cost remains fixed and some remains variable.

Table 2: Calculation of unit cost

Transportation cost 20000

Labor cost 200000

Raw material cost 14000

Depreciation 2500

Total cost 236500

Units produced 20000

Unit cost 11.825

6

Net cash available

(A – B) 6200 10700 14600 17100 19600 22300

Interpretation

On analysis of budget, it can be said that in initial months, sales was increasing but after

that, gradual enhancement in sales was observed and finally sales fall in month of May and June.

But same trend is not observed in case debtors and creditors. Slow rate of growth was observed

in sales in the month of March and that was warning single for upcoming month. But firm

ignored this indication and its debtors as well as creditors got increased in the month of April. As

a result, growth rate of increased cash balance declined sharply. Firm learnt lesson from this

event and reduced its debtor, creditor, raw material and other production expenses in order adjust

as per the change in business conditions. In last month, with decline in sales, other variables of

budget also get decline sharply in terms of amount.

3.2 Calculation of unit cost

Unit cost refers to the calculation of per unit cost and with respect to this, various fixed,

variable and semi variable costs are considered by the firm. Fixed cost refers to the cost that

cannot be reduced and organization has to bear such cost even if it is not producing any product

in its capacity (Fernández and et.al., 2007). On the other hand, variable cost refers to the cost that

changes with the change in quantity of goods produced. Third cost is semi variable cost and in

this category of cost, some part of cost remains fixed and some remains variable.

Table 2: Calculation of unit cost

Transportation cost 20000

Labor cost 200000

Raw material cost 14000

Depreciation 2500

Total cost 236500

Units produced 20000

Unit cost 11.825

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unit cost= Total cost/ number of units produced

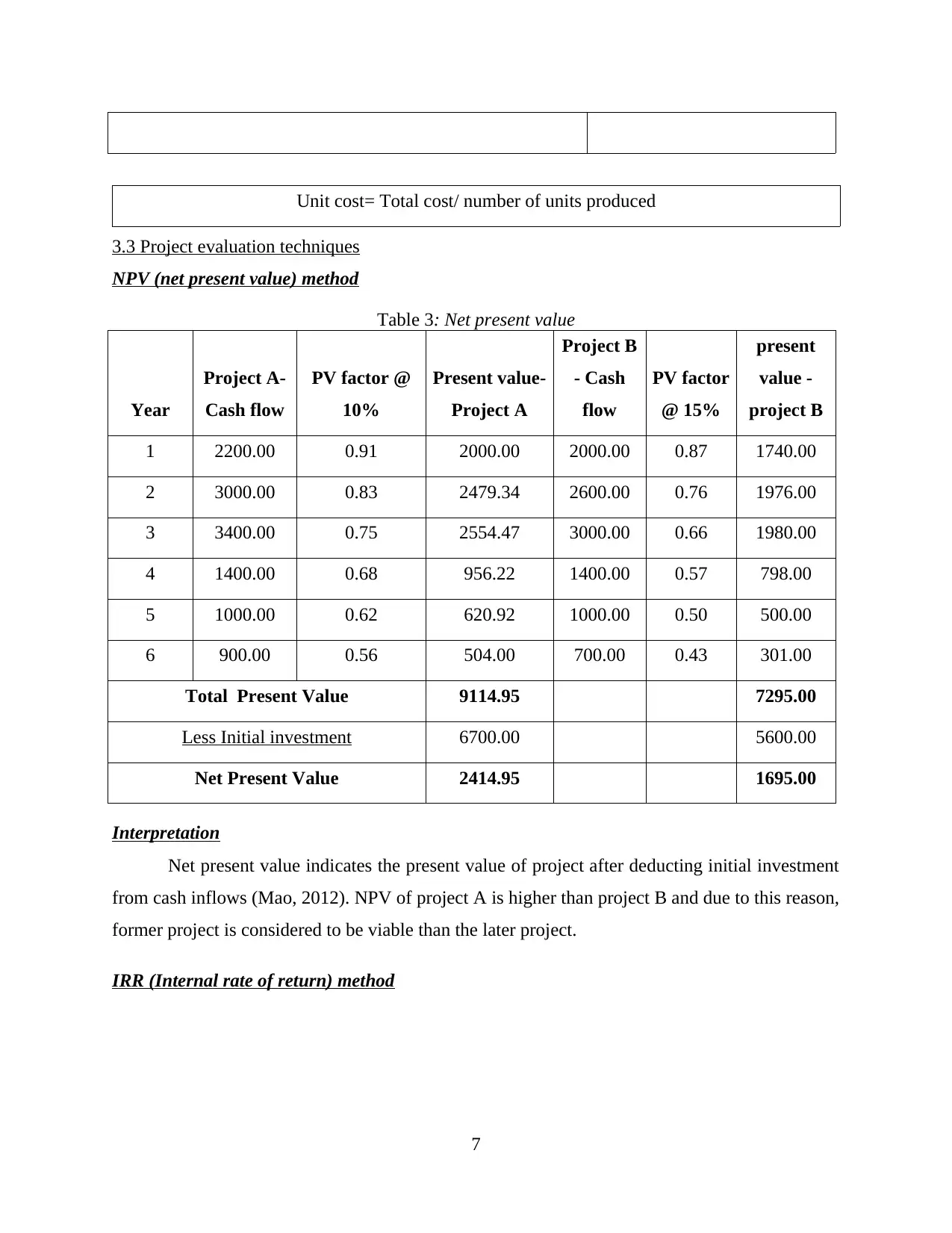

3.3 Project evaluation techniques

NPV (net present value) method

Table 3: Net present value

Year

Project A-

Cash flow

PV factor @

10%

Present value-

Project A

Project B

- Cash

flow

PV factor

@ 15%

present

value -

project B

1 2200.00 0.91 2000.00 2000.00 0.87 1740.00

2 3000.00 0.83 2479.34 2600.00 0.76 1976.00

3 3400.00 0.75 2554.47 3000.00 0.66 1980.00

4 1400.00 0.68 956.22 1400.00 0.57 798.00

5 1000.00 0.62 620.92 1000.00 0.50 500.00

6 900.00 0.56 504.00 700.00 0.43 301.00

Total Present Value 9114.95 7295.00

Less Initial investment 6700.00 5600.00

Net Present Value 2414.95 1695.00

Interpretation

Net present value indicates the present value of project after deducting initial investment

from cash inflows (Mao, 2012). NPV of project A is higher than project B and due to this reason,

former project is considered to be viable than the later project.

IRR (Internal rate of return) method

7

3.3 Project evaluation techniques

NPV (net present value) method

Table 3: Net present value

Year

Project A-

Cash flow

PV factor @

10%

Present value-

Project A

Project B

- Cash

flow

PV factor

@ 15%

present

value -

project B

1 2200.00 0.91 2000.00 2000.00 0.87 1740.00

2 3000.00 0.83 2479.34 2600.00 0.76 1976.00

3 3400.00 0.75 2554.47 3000.00 0.66 1980.00

4 1400.00 0.68 956.22 1400.00 0.57 798.00

5 1000.00 0.62 620.92 1000.00 0.50 500.00

6 900.00 0.56 504.00 700.00 0.43 301.00

Total Present Value 9114.95 7295.00

Less Initial investment 6700.00 5600.00

Net Present Value 2414.95 1695.00

Interpretation

Net present value indicates the present value of project after deducting initial investment

from cash inflows (Mao, 2012). NPV of project A is higher than project B and due to this reason,

former project is considered to be viable than the later project.

IRR (Internal rate of return) method

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

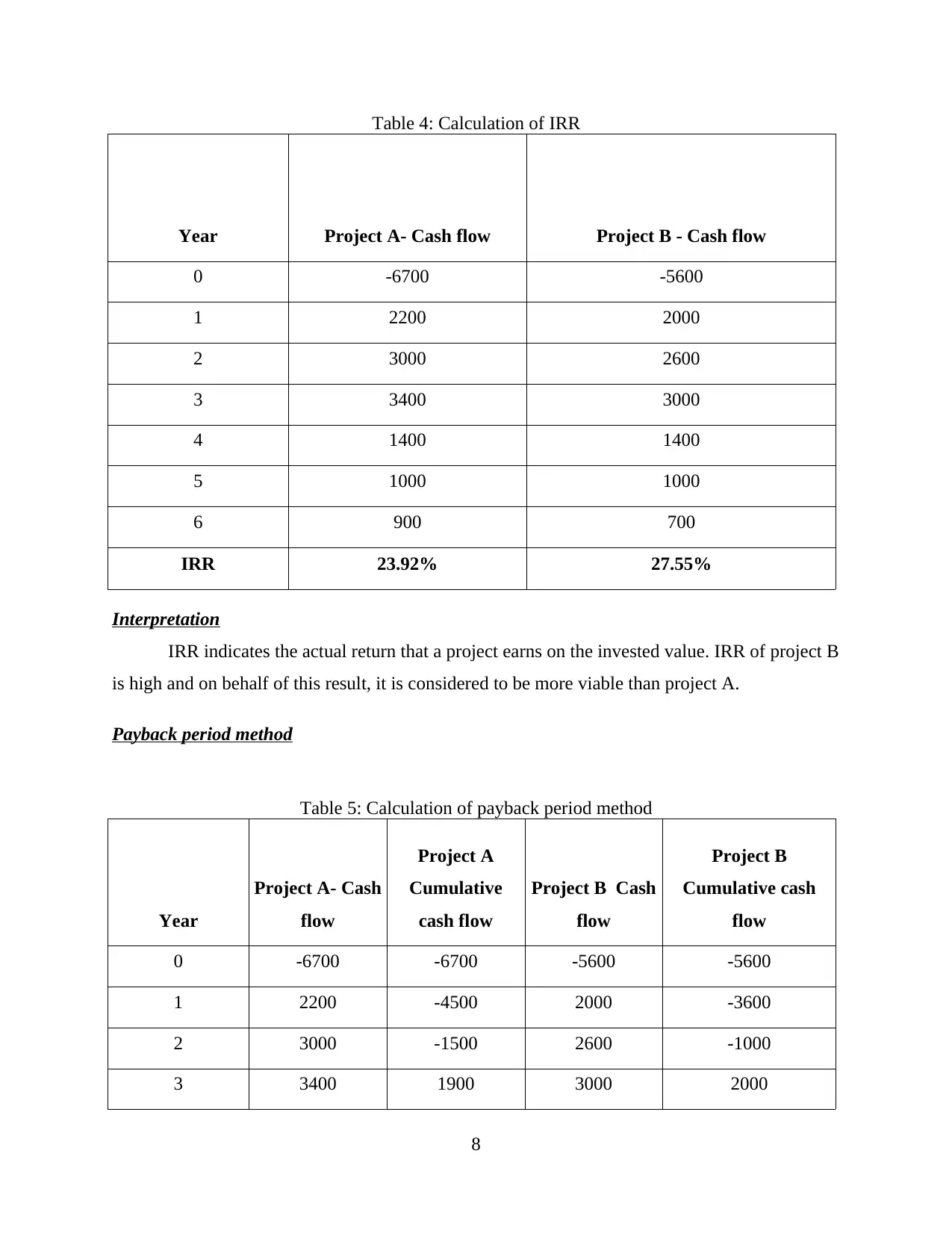

Table 4: Calculation of IRR

Year Project A- Cash flow Project B - Cash flow

0 -6700 -5600

1 2200 2000

2 3000 2600

3 3400 3000

4 1400 1400

5 1000 1000

6 900 700

IRR 23.92% 27.55%

Interpretation

IRR indicates the actual return that a project earns on the invested value. IRR of project B

is high and on behalf of this result, it is considered to be more viable than project A.

Payback period method

Table 5: Calculation of payback period method

Year

Project A- Cash

flow

Project A

Cumulative

cash flow

Project B Cash

flow

Project B

Cumulative cash

flow

0 -6700 -6700 -5600 -5600

1 2200 -4500 2000 -3600

2 3000 -1500 2600 -1000

3 3400 1900 3000 2000

8

Year Project A- Cash flow Project B - Cash flow

0 -6700 -5600

1 2200 2000

2 3000 2600

3 3400 3000

4 1400 1400

5 1000 1000

6 900 700

IRR 23.92% 27.55%

Interpretation

IRR indicates the actual return that a project earns on the invested value. IRR of project B

is high and on behalf of this result, it is considered to be more viable than project A.

Payback period method

Table 5: Calculation of payback period method

Year

Project A- Cash

flow

Project A

Cumulative

cash flow

Project B Cash

flow

Project B

Cumulative cash

flow

0 -6700 -6700 -5600 -5600

1 2200 -4500 2000 -3600

2 3000 -1500 2600 -1000

3 3400 1900 3000 2000

8

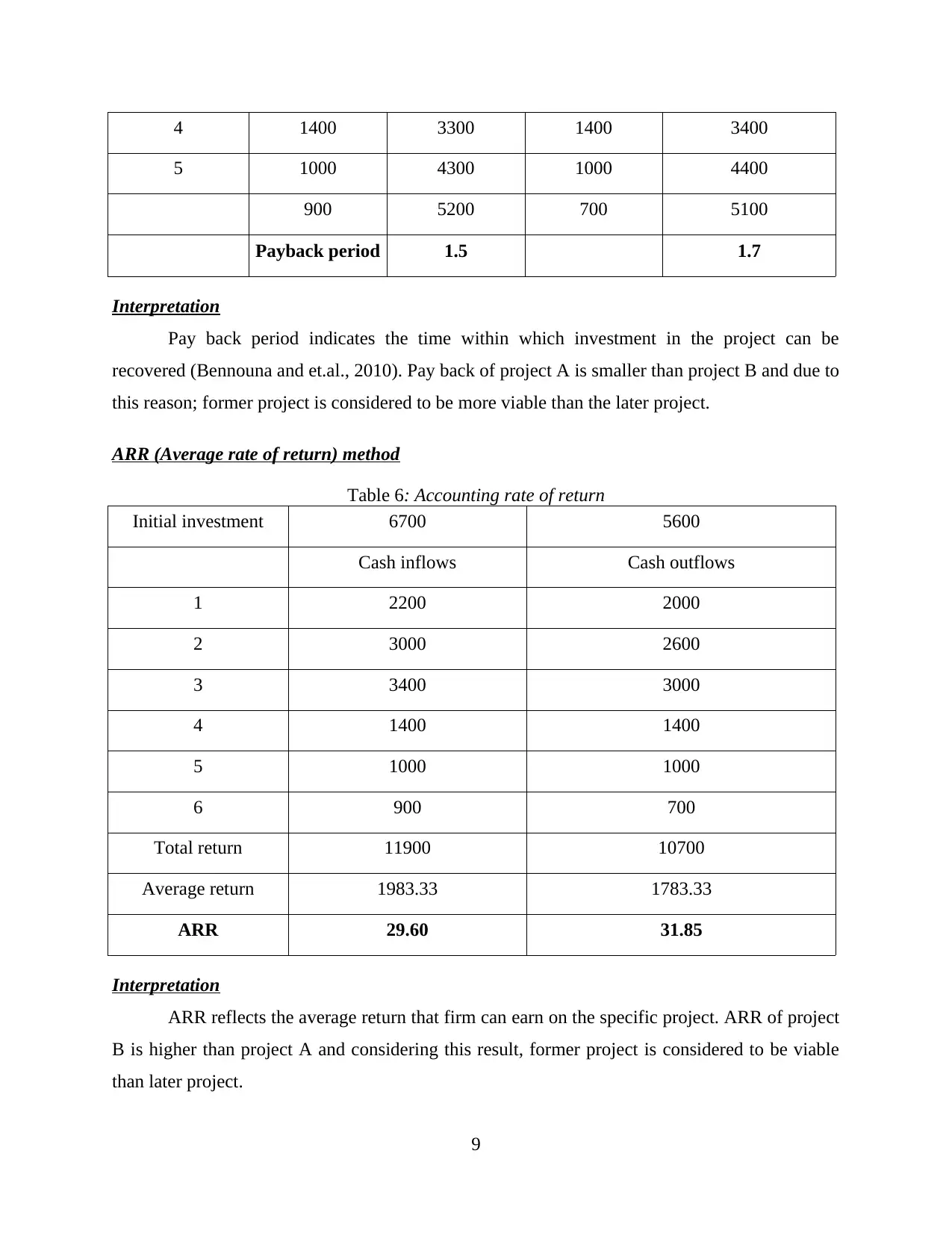

4 1400 3300 1400 3400

5 1000 4300 1000 4400

900 5200 700 5100

Payback period 1.5 1.7

Interpretation

Pay back period indicates the time within which investment in the project can be

recovered (Bennouna and et.al., 2010). Pay back of project A is smaller than project B and due to

this reason; former project is considered to be more viable than the later project.

ARR (Average rate of return) method

Table 6: Accounting rate of return

Initial investment 6700 5600

Cash inflows Cash outflows

1 2200 2000

2 3000 2600

3 3400 3000

4 1400 1400

5 1000 1000

6 900 700

Total return 11900 10700

Average return 1983.33 1783.33

ARR 29.60 31.85

Interpretation

ARR reflects the average return that firm can earn on the specific project. ARR of project

B is higher than project A and considering this result, former project is considered to be viable

than later project.

9

5 1000 4300 1000 4400

900 5200 700 5100

Payback period 1.5 1.7

Interpretation

Pay back period indicates the time within which investment in the project can be

recovered (Bennouna and et.al., 2010). Pay back of project A is smaller than project B and due to

this reason; former project is considered to be more viable than the later project.

ARR (Average rate of return) method

Table 6: Accounting rate of return

Initial investment 6700 5600

Cash inflows Cash outflows

1 2200 2000

2 3000 2600

3 3400 3000

4 1400 1400

5 1000 1000

6 900 700

Total return 11900 10700

Average return 1983.33 1783.33

ARR 29.60 31.85

Interpretation

ARR reflects the average return that firm can earn on the specific project. ARR of project

B is higher than project A and considering this result, former project is considered to be viable

than later project.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.