Financial Decision Making: Analysis of Poundland Group plc Performance

VerifiedAdded on 2020/01/28

|14

|3331

|6338

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making, using the financial data of Poundland Group plc. The report begins by exploring financial and non-financial factors that influence decision-making, along with the impact of business risks and the differences between accrual and cash flow approaches. It then delves into cash flow management techniques. The second part of the report includes a detailed description and interpretation of Poundland's income statement and balance sheet, along with a thorough analysis of key financial ratios. The report assesses the value of Earnings Per Share (EPS) and Return on Capital Employed (ROCE) to determine the sustainability of Poundland's financial performance. It also provides examples of capital and revenue expenditures and discusses financial sources for long-term and working capital financing, including the pros and cons of off-balance sheet financing. The report concludes with a summary of the findings and provides references to support the analysis.

Financial

decision making

decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Examination of financial and non financial factors that assists in decision making process......3

Impact of business risks on financial decisions...........................................................................4

Difference between accrual and cash flow approaches in financial reporting.............................4

Techniques for management of cash flow...................................................................................5

Task 2...............................................................................................................................................6

Description of income statement and balance sheet of Poundland..............................................6

Interpretation of financial statements of Poundland....................................................................6

Assessment of the value of EPS and ROCE for determination of sustainability of Poundland. .8

Examples of capital and revenue expenditure that could be occurred by Poundland..................8

Financial sources for long-term financing and working

capital financing..........................................................................................................................9

Pros and Cons of off-balance sheet financing..............................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Examination of financial and non financial factors that assists in decision making process......3

Impact of business risks on financial decisions...........................................................................4

Difference between accrual and cash flow approaches in financial reporting.............................4

Techniques for management of cash flow...................................................................................5

Task 2...............................................................................................................................................6

Description of income statement and balance sheet of Poundland..............................................6

Interpretation of financial statements of Poundland....................................................................6

Assessment of the value of EPS and ROCE for determination of sustainability of Poundland. .8

Examples of capital and revenue expenditure that could be occurred by Poundland..................8

Financial sources for long-term financing and working

capital financing..........................................................................................................................9

Pros and Cons of off-balance sheet financing..............................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

2

ILLUSTRATION INDEX

Illustration 1: Difference between accrual and cash flow approach................................................5

3

Illustration 1: Difference between accrual and cash flow approach................................................5

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Decision making is crucial task in a business entity because it has direct link with

profitability and growth opportunities. By considering this aspect, management of organization is

required to make viable decisions for business after appropriate analysis (Shim and et.al. 2008).

Present study is focused on description of various financial and non-financial factors required to

be consider in process of decision making. Described tools and techniques will be applied on the

given business information of Poundland Group plc in order to evaluate their financial position.

TASK 1

Examination of financial and non financial factors that assists in decision making process

Financial factors and non-financial factors both have crucial role in decision making

because it defines impact on profitability and feasibility. In order to make viable decision

following factors are required to be considered by management:

Financial factors Return on investment: Management of entities are required to consider rate of return

provided by the project or the decision taken by them (Wahlen and et.al., 2011). By

considering this factor they will be able to determine proposed decision is able to provide

expected returns or not. Cost and benefit: By considering cost and benefit appropriate decision can be taken by

management. It is because; it will provide comparison of potential revenue in against of

expenditure incurred by entity (Zawawi and Hoque, 2010). On the basis of this factor,

organization can make optimum utilization of available resources in order to enhance

profitability.

Non-financial factors Market research: In accordance with the economist Rob Hyndman, each business is

required to evaluate market environment prior to make any decision (Beenhakker, 2006).

With this research, management will be able to act in accordance with the customer

demand and prevailing trend in market. Competition: Competition is another non-financial factor that influence procedure of

decision making in business (Keller, 2013). It is because; management are required to

4

Decision making is crucial task in a business entity because it has direct link with

profitability and growth opportunities. By considering this aspect, management of organization is

required to make viable decisions for business after appropriate analysis (Shim and et.al. 2008).

Present study is focused on description of various financial and non-financial factors required to

be consider in process of decision making. Described tools and techniques will be applied on the

given business information of Poundland Group plc in order to evaluate their financial position.

TASK 1

Examination of financial and non financial factors that assists in decision making process

Financial factors and non-financial factors both have crucial role in decision making

because it defines impact on profitability and feasibility. In order to make viable decision

following factors are required to be considered by management:

Financial factors Return on investment: Management of entities are required to consider rate of return

provided by the project or the decision taken by them (Wahlen and et.al., 2011). By

considering this factor they will be able to determine proposed decision is able to provide

expected returns or not. Cost and benefit: By considering cost and benefit appropriate decision can be taken by

management. It is because; it will provide comparison of potential revenue in against of

expenditure incurred by entity (Zawawi and Hoque, 2010). On the basis of this factor,

organization can make optimum utilization of available resources in order to enhance

profitability.

Non-financial factors Market research: In accordance with the economist Rob Hyndman, each business is

required to evaluate market environment prior to make any decision (Beenhakker, 2006).

With this research, management will be able to act in accordance with the customer

demand and prevailing trend in market. Competition: Competition is another non-financial factor that influence procedure of

decision making in business (Keller, 2013). It is because; management are required to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consider strategies of their competitor in order to survive in highly competitive

environment.

Legal feasibility and social responsibility: In addition to the above described factor,

organization is also required to consider that proposed decision is not in contradiction

with the legal provisions or with their social responsibility.

Impact of business risks on financial decisions

Management of business organization is required to weigh up the business risks and costs

in order to attain better growth opportunities. For this aspect they are required to mitigate the

business risks in an effective manner (Sutter, 2006). In order to weigh up the risks from the

business, management is required to consider risk assessment analysis. Amount of risk involved

in business is based on following factors:

Severity of consequences of making wrong decision

Advantages for making right decision

Impact of risk on future activities

By considering this factor acceptability of risk can be determined by the organization and

safe decision can be taken. For this aspect, business can prepare portfolio by considering risk and

profitability opportunities of multiple strategies in different directions.

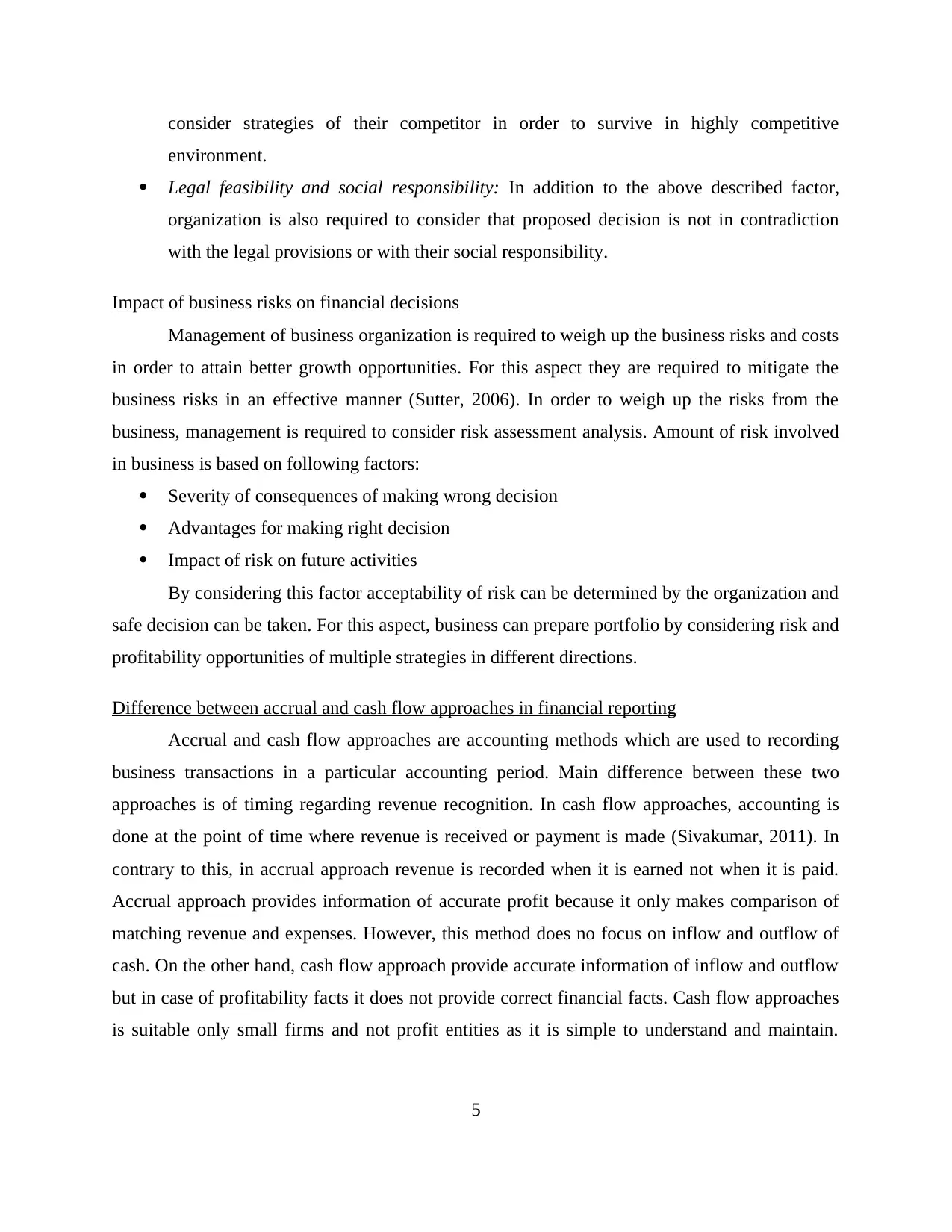

Difference between accrual and cash flow approaches in financial reporting

Accrual and cash flow approaches are accounting methods which are used to recording

business transactions in a particular accounting period. Main difference between these two

approaches is of timing regarding revenue recognition. In cash flow approaches, accounting is

done at the point of time where revenue is received or payment is made (Sivakumar, 2011). In

contrary to this, in accrual approach revenue is recorded when it is earned not when it is paid.

Accrual approach provides information of accurate profit because it only makes comparison of

matching revenue and expenses. However, this method does no focus on inflow and outflow of

cash. On the other hand, cash flow approach provide accurate information of inflow and outflow

but in case of profitability facts it does not provide correct financial facts. Cash flow approaches

is suitable only small firms and not profit entities as it is simple to understand and maintain.

5

environment.

Legal feasibility and social responsibility: In addition to the above described factor,

organization is also required to consider that proposed decision is not in contradiction

with the legal provisions or with their social responsibility.

Impact of business risks on financial decisions

Management of business organization is required to weigh up the business risks and costs

in order to attain better growth opportunities. For this aspect they are required to mitigate the

business risks in an effective manner (Sutter, 2006). In order to weigh up the risks from the

business, management is required to consider risk assessment analysis. Amount of risk involved

in business is based on following factors:

Severity of consequences of making wrong decision

Advantages for making right decision

Impact of risk on future activities

By considering this factor acceptability of risk can be determined by the organization and

safe decision can be taken. For this aspect, business can prepare portfolio by considering risk and

profitability opportunities of multiple strategies in different directions.

Difference between accrual and cash flow approaches in financial reporting

Accrual and cash flow approaches are accounting methods which are used to recording

business transactions in a particular accounting period. Main difference between these two

approaches is of timing regarding revenue recognition. In cash flow approaches, accounting is

done at the point of time where revenue is received or payment is made (Sivakumar, 2011). In

contrary to this, in accrual approach revenue is recorded when it is earned not when it is paid.

Accrual approach provides information of accurate profit because it only makes comparison of

matching revenue and expenses. However, this method does no focus on inflow and outflow of

cash. On the other hand, cash flow approach provide accurate information of inflow and outflow

but in case of profitability facts it does not provide correct financial facts. Cash flow approaches

is suitable only small firms and not profit entities as it is simple to understand and maintain.

5

Further, large enterprises are required to consider accrual approach because it provides accurate

assessment of the financial position.

Techniques for management of cash flow

Management of cash flow is important business practice because it creates balance

between income and expenses. In addition to this, poor management of cash and cash equivalents

create liquidity issues for business. In order to manage cash in an effective manner organization

is required to make use of following techniques: Cash flow targets: Organization can set cash flow targets on periodical basis by

forecasting inflow and outflow (Collis and Hussey, 2013). On the basis of this target,

management can develop control on expenses and consequently they can plan to make

reduction in it. Cash credit: In order to prevent delay payment and bad debts from debtors management

can provide cash credit to the parties. In this manner, they will be able to collect quick

cash and use it for daily operational activities.

6

Illustr

assessment of the financial position.

Techniques for management of cash flow

Management of cash flow is important business practice because it creates balance

between income and expenses. In addition to this, poor management of cash and cash equivalents

create liquidity issues for business. In order to manage cash in an effective manner organization

is required to make use of following techniques: Cash flow targets: Organization can set cash flow targets on periodical basis by

forecasting inflow and outflow (Collis and Hussey, 2013). On the basis of this target,

management can develop control on expenses and consequently they can plan to make

reduction in it. Cash credit: In order to prevent delay payment and bad debts from debtors management

can provide cash credit to the parties. In this manner, they will be able to collect quick

cash and use it for daily operational activities.

6

Illustr

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefit of credit policy: Business entity can select suppliers with maximum credit period

policy in order to reduce period of operating cash cycle. With this approach, management

can use these funds for other activities without arranging loans from short term finance.

This will make reduction in interest cost (Davies and Crawford, 2011). However, in this

strategy, organization is required to consider the fact additional charge by creditor should

not be more than interest by financial institutions or any other opportunity cost.

TASK 2

Description of income statement and balance sheet of Poundland

Income statement

Income statement comprises figures of revenue and expenditure occurred in a particular

accounting period. On the basis of these financial values, net income or loss is computed earned

by business is shown in operating section. Income statement of Poundland Group plc shows that

net profit in 2014 is 13.8 million which is increased in 2015 by 14.54 million. This increase has

been occurred because increase in revenue is higher than increase in expenses. This profit is

attributable to the equity shareholders of the company.

Position statement

Position statement shows financial situation of an organization in a particular accounting

period. It comprises two sections i.e. liability and asset. Liability section shows sum of owner's

capital and outsider obligations. In accordance with the accounting equation, assets are

equivalent to the sum of outsider liability and capital fund. Position statement of Poundland

Group plc shows that equity in 2014 and 2015 is 186.48 million and 226.67 million respectively.

Further, as per accounting equation net assets of company in 2014 and 2015 is 186.48 million

and 226.67 million respectively.

Interpretation of financial statements of Poundland

For the interpretation of financial statements of Poundland ratio analysis is as follows:

Table 1: Computation of financial ratios of Poundland Group plc

Ratios Formula 2015 2014

Activity Ratios

Net Sales 1116.95 997.8

7

policy in order to reduce period of operating cash cycle. With this approach, management

can use these funds for other activities without arranging loans from short term finance.

This will make reduction in interest cost (Davies and Crawford, 2011). However, in this

strategy, organization is required to consider the fact additional charge by creditor should

not be more than interest by financial institutions or any other opportunity cost.

TASK 2

Description of income statement and balance sheet of Poundland

Income statement

Income statement comprises figures of revenue and expenditure occurred in a particular

accounting period. On the basis of these financial values, net income or loss is computed earned

by business is shown in operating section. Income statement of Poundland Group plc shows that

net profit in 2014 is 13.8 million which is increased in 2015 by 14.54 million. This increase has

been occurred because increase in revenue is higher than increase in expenses. This profit is

attributable to the equity shareholders of the company.

Position statement

Position statement shows financial situation of an organization in a particular accounting

period. It comprises two sections i.e. liability and asset. Liability section shows sum of owner's

capital and outsider obligations. In accordance with the accounting equation, assets are

equivalent to the sum of outsider liability and capital fund. Position statement of Poundland

Group plc shows that equity in 2014 and 2015 is 186.48 million and 226.67 million respectively.

Further, as per accounting equation net assets of company in 2014 and 2015 is 186.48 million

and 226.67 million respectively.

Interpretation of financial statements of Poundland

For the interpretation of financial statements of Poundland ratio analysis is as follows:

Table 1: Computation of financial ratios of Poundland Group plc

Ratios Formula 2015 2014

Activity Ratios

Net Sales 1116.95 997.8

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Assets 398.66 367.06

Total Assets Turnover Ratio Net Sales/ Total Assets 2.80 2.72

Cost of goods sold 1079.75 970.1

Inventory 113.31 89.56

Inventory Turnover ratio COGS/Inventory 9.53 10.83

Liquidity ratios

Current Assets 167.41 140.67

Current Liabilities 148.49 130.27

Closing Stock 113.31 89.56

Current Ratio

Current Assets / current

Liabilities 1.13 1.08

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.36 0.39

Solvency ratios

Debt 23.5 50.31

Equity 226.67 186.48

Debt Equity Ratio Debt/ Equity 0.10 0.27

Net income 28.4 13.86

Annual Interest Expense 1.05 6.22

Times Interest Ratio Net Income/ Interest expense 27.05 2.23

Equity 226.67 186.48

Total Assets 398.66 367.06

Equity ratio Equity/total assets 0.57 0.51

Short term liabilities 148.49 130.27

Long term liabilities 23.50 50.31

Total Assets 398.66 367.06

Debt ratio Total liabilities/ Total assets 0.43 0.49

Profitability ratios

Operating profit 37.2 27.7

Net profit 28.4 13.86

Net Sales 1116.95 997.8

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 3.33% 2.78%

Net Profit Ratio (Net Profit/ Net Sales) *100 2.54% 1.39%

Activity ratios: Activity ratio show fluctuating position of the company. It is because;

some ratios are increase while some are decreasing (De Franco and et. al., 2011).

Company had made increase in their efficiency for utilization of asset but efficiency in

inventory management has been reduced.

8

Total Assets Turnover Ratio Net Sales/ Total Assets 2.80 2.72

Cost of goods sold 1079.75 970.1

Inventory 113.31 89.56

Inventory Turnover ratio COGS/Inventory 9.53 10.83

Liquidity ratios

Current Assets 167.41 140.67

Current Liabilities 148.49 130.27

Closing Stock 113.31 89.56

Current Ratio

Current Assets / current

Liabilities 1.13 1.08

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.36 0.39

Solvency ratios

Debt 23.5 50.31

Equity 226.67 186.48

Debt Equity Ratio Debt/ Equity 0.10 0.27

Net income 28.4 13.86

Annual Interest Expense 1.05 6.22

Times Interest Ratio Net Income/ Interest expense 27.05 2.23

Equity 226.67 186.48

Total Assets 398.66 367.06

Equity ratio Equity/total assets 0.57 0.51

Short term liabilities 148.49 130.27

Long term liabilities 23.50 50.31

Total Assets 398.66 367.06

Debt ratio Total liabilities/ Total assets 0.43 0.49

Profitability ratios

Operating profit 37.2 27.7

Net profit 28.4 13.86

Net Sales 1116.95 997.8

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 3.33% 2.78%

Net Profit Ratio (Net Profit/ Net Sales) *100 2.54% 1.39%

Activity ratios: Activity ratio show fluctuating position of the company. It is because;

some ratios are increase while some are decreasing (De Franco and et. al., 2011).

Company had made increase in their efficiency for utilization of asset but efficiency in

inventory management has been reduced.

8

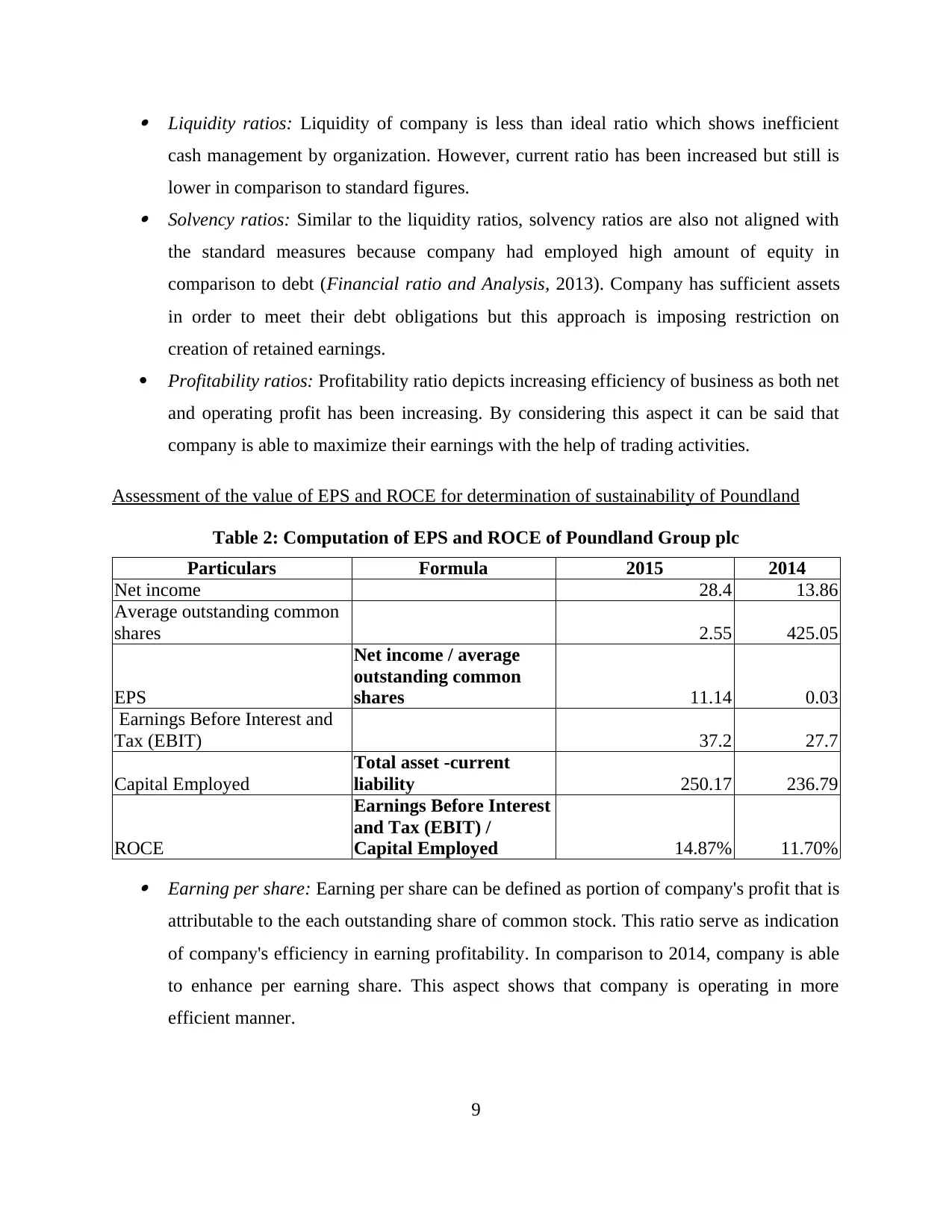

Liquidity ratios: Liquidity of company is less than ideal ratio which shows inefficient

cash management by organization. However, current ratio has been increased but still is

lower in comparison to standard figures. Solvency ratios: Similar to the liquidity ratios, solvency ratios are also not aligned with

the standard measures because company had employed high amount of equity in

comparison to debt (Financial ratio and Analysis, 2013). Company has sufficient assets

in order to meet their debt obligations but this approach is imposing restriction on

creation of retained earnings.

Profitability ratios: Profitability ratio depicts increasing efficiency of business as both net

and operating profit has been increasing. By considering this aspect it can be said that

company is able to maximize their earnings with the help of trading activities.

Assessment of the value of EPS and ROCE for determination of sustainability of Poundland

Table 2: Computation of EPS and ROCE of Poundland Group plc

Particulars Formula 2015 2014

Net income 28.4 13.86

Average outstanding common

shares 2.55 425.05

EPS

Net income / average

outstanding common

shares 11.14 0.03

Earnings Before Interest and

Tax (EBIT) 37.2 27.7

Capital Employed

Total asset -current

liability 250.17 236.79

ROCE

Earnings Before Interest

and Tax (EBIT) /

Capital Employed 14.87% 11.70% Earning per share: Earning per share can be defined as portion of company's profit that is

attributable to the each outstanding share of common stock. This ratio serve as indication

of company's efficiency in earning profitability. In comparison to 2014, company is able

to enhance per earning share. This aspect shows that company is operating in more

efficient manner.

9

cash management by organization. However, current ratio has been increased but still is

lower in comparison to standard figures. Solvency ratios: Similar to the liquidity ratios, solvency ratios are also not aligned with

the standard measures because company had employed high amount of equity in

comparison to debt (Financial ratio and Analysis, 2013). Company has sufficient assets

in order to meet their debt obligations but this approach is imposing restriction on

creation of retained earnings.

Profitability ratios: Profitability ratio depicts increasing efficiency of business as both net

and operating profit has been increasing. By considering this aspect it can be said that

company is able to maximize their earnings with the help of trading activities.

Assessment of the value of EPS and ROCE for determination of sustainability of Poundland

Table 2: Computation of EPS and ROCE of Poundland Group plc

Particulars Formula 2015 2014

Net income 28.4 13.86

Average outstanding common

shares 2.55 425.05

EPS

Net income / average

outstanding common

shares 11.14 0.03

Earnings Before Interest and

Tax (EBIT) 37.2 27.7

Capital Employed

Total asset -current

liability 250.17 236.79

ROCE

Earnings Before Interest

and Tax (EBIT) /

Capital Employed 14.87% 11.70% Earning per share: Earning per share can be defined as portion of company's profit that is

attributable to the each outstanding share of common stock. This ratio serve as indication

of company's efficiency in earning profitability. In comparison to 2014, company is able

to enhance per earning share. This aspect shows that company is operating in more

efficient manner.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on capital employed: ROCE can be termed as financial ratio used for the

measurement of company's profitability and efficiency in comparison to the employed

capital (Gray and et. al., 2013). Increasing trend of ROCE shows efficient use of capital.

Further, ROCE of company is also showing increasing trend by which it can be said that

organization is making efficient use of available resources.

Examples of capital and revenue expenditure that could be occurred by Poundland

Capital expenditure is the expense which provides economic benefit for more than one

year. These expenses are non-recurring in nature and it provides value addition to the business.

Poundland Group Plc can incurred capital expenditure for purchase of asset or investment. With

this expenditure, management of company will be able to enhance efficiency and productivity.

Further, they can also expand their business in order to avail better growth opportunities (Gibson,

2010). On the other hand, revenue expenditure can be defined as amount incurred to attain

economic benefit for current accounting period. Example of revenue expenditure by considering

nature of Poundland Group Plc is repair and maintenance expenses.

Financial sources for long-term financing and working capital financing

In order to generate funds for long term financing management of Poundland Group Plc can

make use of following financial sources: Equity capital: Poundland Group plc can issue their ordinary share to the public in order

to generate capital funds. For this financial source they will be required to pay dividend

i.e. a portion of profit (Sources of finance, 2013). Further, there will be no obligation of

repayment of principal amount during the business life.

Debt capital: Management of company can also generate funds from financial

institutions. For this financial source they will be required to pay interest cost to the

lenders. This source will also increase long term obligation of business.

In accordance with the capital structure of the company management is required to

generate funds from debt capital in order to optimize their financial cost. With this source,

company have fixed obligation along with the benefit of tax shield (Acquiring and managing

financial resources, N.d.). Thus, by this source additional earning will be transferred for creation

of retained earnings.

10

measurement of company's profitability and efficiency in comparison to the employed

capital (Gray and et. al., 2013). Increasing trend of ROCE shows efficient use of capital.

Further, ROCE of company is also showing increasing trend by which it can be said that

organization is making efficient use of available resources.

Examples of capital and revenue expenditure that could be occurred by Poundland

Capital expenditure is the expense which provides economic benefit for more than one

year. These expenses are non-recurring in nature and it provides value addition to the business.

Poundland Group Plc can incurred capital expenditure for purchase of asset or investment. With

this expenditure, management of company will be able to enhance efficiency and productivity.

Further, they can also expand their business in order to avail better growth opportunities (Gibson,

2010). On the other hand, revenue expenditure can be defined as amount incurred to attain

economic benefit for current accounting period. Example of revenue expenditure by considering

nature of Poundland Group Plc is repair and maintenance expenses.

Financial sources for long-term financing and working capital financing

In order to generate funds for long term financing management of Poundland Group Plc can

make use of following financial sources: Equity capital: Poundland Group plc can issue their ordinary share to the public in order

to generate capital funds. For this financial source they will be required to pay dividend

i.e. a portion of profit (Sources of finance, 2013). Further, there will be no obligation of

repayment of principal amount during the business life.

Debt capital: Management of company can also generate funds from financial

institutions. For this financial source they will be required to pay interest cost to the

lenders. This source will also increase long term obligation of business.

In accordance with the capital structure of the company management is required to

generate funds from debt capital in order to optimize their financial cost. With this source,

company have fixed obligation along with the benefit of tax shield (Acquiring and managing

financial resources, N.d.). Thus, by this source additional earning will be transferred for creation

of retained earnings.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For working capital financing following financial source will be suitable for the organization: Bank overdraft: Organization can take benefit of bank overdraft services on their current

account. With this facility, they will be entitled to withdraw excessive amount in

comparison to their balance. For this source, they will be required to pay bank charges.

Credit policies and cash credit: In order to make delay payment of creditor they can

select supplier who provide benefit of credit policy. Further, for quick collection of cash

management can introduce policy of cash credit or take services of factoring.

Pros and Cons of off-balance sheet financing

It is a form of financing in which large capital expenditure are not reflected in the

position statements by making use of various classification method. General examples of off

balance sheet items are factoring, leasing, special projects, outsourcing and securitization. Major

benefit of this approach is that it assists in making reduction in debt equity ratio and leverage

ratio. This approach is also beneficial for mitigating the risk and reducing cost of borrowings as

lenders are not aware of the unrecorded liabilities. This approach also assists in avoiding

violation of some debt covenants as restrictions are applicable in the debt agreement for the

protection of lenders. Generally, these restrictions are imposed by adding condition of

maintaining particular ratio. In off-balance sheet, financing organization do not record obligation

due to which they can borrow funds without violating conditions that are stipulated by other

lenders. However, this approach enhances the risk for company because off balance sheet items

can become potential liability for business. Further, it also reduces the accuracy of financial

position of company as it has severe impact on the financial ratios of business. Mainly, it affects

the financing ratio because denominator i.e. debt is reduced and shows favourable position of

business which is not correct.

CONCLUSION

In accordance with the present study, conclusion can be drawn that financial decisions are

important for the success of business. Management of business entities are required to consider

proper analysis prior to making decision for the entity. With this approach, they will be able to

reduce risk in operational activities and can attain growth opportunities for the success. Financial

11

account. With this facility, they will be entitled to withdraw excessive amount in

comparison to their balance. For this source, they will be required to pay bank charges.

Credit policies and cash credit: In order to make delay payment of creditor they can

select supplier who provide benefit of credit policy. Further, for quick collection of cash

management can introduce policy of cash credit or take services of factoring.

Pros and Cons of off-balance sheet financing

It is a form of financing in which large capital expenditure are not reflected in the

position statements by making use of various classification method. General examples of off

balance sheet items are factoring, leasing, special projects, outsourcing and securitization. Major

benefit of this approach is that it assists in making reduction in debt equity ratio and leverage

ratio. This approach is also beneficial for mitigating the risk and reducing cost of borrowings as

lenders are not aware of the unrecorded liabilities. This approach also assists in avoiding

violation of some debt covenants as restrictions are applicable in the debt agreement for the

protection of lenders. Generally, these restrictions are imposed by adding condition of

maintaining particular ratio. In off-balance sheet, financing organization do not record obligation

due to which they can borrow funds without violating conditions that are stipulated by other

lenders. However, this approach enhances the risk for company because off balance sheet items

can become potential liability for business. Further, it also reduces the accuracy of financial

position of company as it has severe impact on the financial ratios of business. Mainly, it affects

the financing ratio because denominator i.e. debt is reduced and shows favourable position of

business which is not correct.

CONCLUSION

In accordance with the present study, conclusion can be drawn that financial decisions are

important for the success of business. Management of business entities are required to consider

proper analysis prior to making decision for the entity. With this approach, they will be able to

reduce risk in operational activities and can attain growth opportunities for the success. Financial

11

position of Poundland Group plc depicts that financial position of company has been improved

as they are able to enhance their profitability from trading activities. However, company is

required to make modifications in their capital structure for optimization of financial cost.

12

as they are able to enhance their profitability from trading activities. However, company is

required to make modifications in their capital structure for optimization of financial cost.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.