Advanced Finance for Decision Making: Comprehensive Analysis Report

VerifiedAdded on 2021/01/03

|23

|7605

|19

Report

AI Summary

This report provides a comprehensive analysis of advanced finance for decision-making, covering crucial aspects such as financial priorities, business risks, and cash flow management. It examines the factors that guide business decisions, including return on investment, brand image, and opportunity cost. The report delves into the significance of financial factors in decision-making, including personnel costs, growth strategies, and cost-cutting measures. It identifies the characteristics of business risks, such as market fluctuations and competition, and their impact on financial decisions. Furthermore, it explores the differences between cash and accrual accounting methods, the structure and content of final accounts, and their uses in business decision-making. The report also addresses techniques for managing cash flow, the financial implications of various business ownership structures, and the role of corporate governance and business ethics in financial decision-making. It includes an analysis of financial statements, ratio analysis, and the importance of earnings per share (EPS) in measuring business performance, offering valuable insights for professionals in the field.

ADVANCE

FINANCE FOR

DECISION MAKING

FINANCE FOR

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................5

1.4 Summarize the financial priorities that need to be considered when making financial

decisions......................................................................................................................................7

SECTION 2......................................................................................................................................8

2.1- The method of cash focuses on the instant identification on the expenses and revenues

while accrual basis focuses on forecasting of incomes and expenses.........................................8

2.2- explain the structure and content of final accounts and their uses for business decision

making.........................................................................................................................................9

3- Statements of cash flow........................................................................................................10

2.3 interpret the financial information in the financial statements you have obtained and

illustrate differences between the sets of accounts...................................................................10

2.4..............................................................................................................................................11

2.5 Financial analysis of Morrison and also suggesting the u8efulness of ratios analysis in

decision making........................................................................................................................13

SECTION 3....................................................................................................................................14

5.1 Difference between business ethics, corporate governance and accounting ethics as

controls on business accountability...........................................................................................14

5.2 Assessing the role of the finance director/chief financial officer as a guardian of business

ethics.........................................................................................................................................14

5.3 Analysing the key concepts and principles of corporate governance that may impact on

business decisions.....................................................................................................................15

5.4 Examining key national and international financial reporting standards that are relevant to

business decisions.....................................................................................................................16

Requirement...................................................................................................................................17

3.4 Critically examine techniques needed to manage cash flow and the impact of cash flow on

key business decisions..............................................................................................................19

SECTION 5....................................................................................................................................21

4.1 Financial implication made by various business ownership structure................................21

4.2 Analysing the corporate governance, legal and regulatory environment............................21

INTRODUCTION...........................................................................................................................5

1.4 Summarize the financial priorities that need to be considered when making financial

decisions......................................................................................................................................7

SECTION 2......................................................................................................................................8

2.1- The method of cash focuses on the instant identification on the expenses and revenues

while accrual basis focuses on forecasting of incomes and expenses.........................................8

2.2- explain the structure and content of final accounts and their uses for business decision

making.........................................................................................................................................9

3- Statements of cash flow........................................................................................................10

2.3 interpret the financial information in the financial statements you have obtained and

illustrate differences between the sets of accounts...................................................................10

2.4..............................................................................................................................................11

2.5 Financial analysis of Morrison and also suggesting the u8efulness of ratios analysis in

decision making........................................................................................................................13

SECTION 3....................................................................................................................................14

5.1 Difference between business ethics, corporate governance and accounting ethics as

controls on business accountability...........................................................................................14

5.2 Assessing the role of the finance director/chief financial officer as a guardian of business

ethics.........................................................................................................................................14

5.3 Analysing the key concepts and principles of corporate governance that may impact on

business decisions.....................................................................................................................15

5.4 Examining key national and international financial reporting standards that are relevant to

business decisions.....................................................................................................................16

Requirement...................................................................................................................................17

3.4 Critically examine techniques needed to manage cash flow and the impact of cash flow on

key business decisions..............................................................................................................19

SECTION 5....................................................................................................................................21

4.1 Financial implication made by various business ownership structure................................21

4.2 Analysing the corporate governance, legal and regulatory environment............................21

4.3 Interest of stakeholders and managers in decision making.................................................22

4.4 Evaluating the significant return on capital employed as well as managing long term

solvency....................................................................................................................................22

4.5 Importance of EPS in measuring business performance.....................................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

4.4 Evaluating the significant return on capital employed as well as managing long term

solvency....................................................................................................................................22

4.5 Importance of EPS in measuring business performance.....................................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Implicating the advance finance for decision making will be helpful and adequate as per

analysing and making the appropriate decisions which will be relevant with the operations of the

business. In the present report there will be discussion based on various operational techniques,

budgeting methods etc. which will be helpful in meeting the level of revenue and structural

capital. Analysing the various outcomes which are comprised of making qualitative changes in

various operations which will be helpful and adequate as per meeting the goals and stabilising

the firm in ascertaining the financial requirement. The suggestion will be provided to the

professionals working in various organization as per controlling the costs as well as managing

the operations of firm.

SECTION1

1.1 Examine and Explain the factor that guide and drive business decision-making.

Decision making is one of the most important function in an organization. Every operation in a

company needs a decision on the working of the company. Decision-making is the crucial task

for the management, there are many factors which effect and influence the decision making in

the present and future. Some of these factors are:◦ Return On Investment: it is one of the main factor that influence the decision making

process in any organization. Considering the factor of profitability of the company at the

time of decision making is very important. Return on investment is the difference

between in the money which a company invest in different activities in the business like

marketing, operations , inventory etc. and the actual return a business is getting (Nash,

2018). By estimating the return on investment it is very east to decide for the business

weather the potential returns justifies the expenses and risks involved in creating

implementing different activity plan business.◦ Image and Brand Management: Decisions on where to advertise and sell and at what

price the product is to be sold, the social activities a company engaged in have a huge

impact o the brand image of the company. Brand image of the company focuses on public

perception and intangible gains for the company. At the time of making decisions ,

concerning about public perception can influence decisions about product, sponsorship

and public relation campaigns. Brand awareness can influence the sessions regarding

pricing, marketing and displaying products and services.

Implicating the advance finance for decision making will be helpful and adequate as per

analysing and making the appropriate decisions which will be relevant with the operations of the

business. In the present report there will be discussion based on various operational techniques,

budgeting methods etc. which will be helpful in meeting the level of revenue and structural

capital. Analysing the various outcomes which are comprised of making qualitative changes in

various operations which will be helpful and adequate as per meeting the goals and stabilising

the firm in ascertaining the financial requirement. The suggestion will be provided to the

professionals working in various organization as per controlling the costs as well as managing

the operations of firm.

SECTION1

1.1 Examine and Explain the factor that guide and drive business decision-making.

Decision making is one of the most important function in an organization. Every operation in a

company needs a decision on the working of the company. Decision-making is the crucial task

for the management, there are many factors which effect and influence the decision making in

the present and future. Some of these factors are:◦ Return On Investment: it is one of the main factor that influence the decision making

process in any organization. Considering the factor of profitability of the company at the

time of decision making is very important. Return on investment is the difference

between in the money which a company invest in different activities in the business like

marketing, operations , inventory etc. and the actual return a business is getting (Nash,

2018). By estimating the return on investment it is very east to decide for the business

weather the potential returns justifies the expenses and risks involved in creating

implementing different activity plan business.◦ Image and Brand Management: Decisions on where to advertise and sell and at what

price the product is to be sold, the social activities a company engaged in have a huge

impact o the brand image of the company. Brand image of the company focuses on public

perception and intangible gains for the company. At the time of making decisions ,

concerning about public perception can influence decisions about product, sponsorship

and public relation campaigns. Brand awareness can influence the sessions regarding

pricing, marketing and displaying products and services.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

◦ Opportunity cost: decision on making involves the best use of available resources which

involves the decision of choosing best alternatives between two or more options. An

opportunity cost trade off is an influencing factor in these type of decisions (Libby,

2017). what a business gets by choosing one alternative over another and what a business

has to give up is the trade off decision of a company.

1.2 Assess the significance of financial factors in business decision-making.

In decision-making process of any organization, finance is very important factor. It Is

the basic requirement for any activity in the business. Based on the revenue and outflow of

the business many decisions is taken. The significance of financial factor in business

decision-making are: Personnel: Labor is one of the most important costs for a business which it securely

sustains. Each employee in the company represents a significant dedicated cost, which it

expects a return on investment while hiring the employees. The cost of an employee is

considered as an investment in growth and revenue of the business, hiring more

employees is considered as business expansion and growth of companies capabilities.

When finance of the company allows, companies may take the personnel related risk to

achieve growth. Growth: any company wants to grow to increase revenues, margins and profits. The

financial position of the company is to be calculated in order to grow the size of

business, market, to ascertain risk management and ownership (Klychova and et.al.,

2015). Available capital includes cash in hand, available credits and investment capital is

the main resources for the growth of the company. Cost cutting: the company has to make decisions to cut the cost in order to preserve the

profit margins if the finance resources is not up-to the mark. If the revenue of the

company is decreasing, it may lead the company to become tighter on its various

activities like purchasing, training and equipment, travel expenses etc.

1.3 Identify the characteristics of business risks that impact on financial and business decisions.

Any difficulties in business and financial and operational activity in business can leads to

the possibilities of the business risk and uncertainties. Each risk carries different implications for

business owner to overcome. Financial and economic condition can also effect the financial and

involves the decision of choosing best alternatives between two or more options. An

opportunity cost trade off is an influencing factor in these type of decisions (Libby,

2017). what a business gets by choosing one alternative over another and what a business

has to give up is the trade off decision of a company.

1.2 Assess the significance of financial factors in business decision-making.

In decision-making process of any organization, finance is very important factor. It Is

the basic requirement for any activity in the business. Based on the revenue and outflow of

the business many decisions is taken. The significance of financial factor in business

decision-making are: Personnel: Labor is one of the most important costs for a business which it securely

sustains. Each employee in the company represents a significant dedicated cost, which it

expects a return on investment while hiring the employees. The cost of an employee is

considered as an investment in growth and revenue of the business, hiring more

employees is considered as business expansion and growth of companies capabilities.

When finance of the company allows, companies may take the personnel related risk to

achieve growth. Growth: any company wants to grow to increase revenues, margins and profits. The

financial position of the company is to be calculated in order to grow the size of

business, market, to ascertain risk management and ownership (Klychova and et.al.,

2015). Available capital includes cash in hand, available credits and investment capital is

the main resources for the growth of the company. Cost cutting: the company has to make decisions to cut the cost in order to preserve the

profit margins if the finance resources is not up-to the mark. If the revenue of the

company is decreasing, it may lead the company to become tighter on its various

activities like purchasing, training and equipment, travel expenses etc.

1.3 Identify the characteristics of business risks that impact on financial and business decisions.

Any difficulties in business and financial and operational activity in business can leads to

the possibilities of the business risk and uncertainties. Each risk carries different implications for

business owner to overcome. Financial and economic condition can also effect the financial and

business decision of the company. The business risk that will effect the financial and business

decision are: Market fluctuations: the fluctuations in the demand and supply of the product in the

market can effect both financial and business decisions. With the decline in the demand

of the product, the decision regarding operational management will be effected, as well as

the financial decision regarding the increase in production and inventory amount will be

effected. market fluctuation leads to worsened the gross margins and profitability which

leads the management to change the business decisions. Fluctuations in foreign currency and interest rates:since the cost and the value of assets

and debts of business operation are influenced by the fluctuations in interest rates or

currency rates in market, it will affect the financial condition of the business (Heitzman

and Huang, 2018). The business, than has to make new decisions regarding sales volume

and material volume in foreign currencies.

Competition: More the competition in the market more the risk of loosing the customer

for the business. The business has to take new marketing decision to attract the customer.

With the increase in competition in the market, the sells of the product will decrease

which leads the business to reduce its price which will affect the profit margin of the

company.

1.4 Summarize the financial priorities that need to be considered when making financial

decisions.

Before making financial decision, management should ascertain what are the financial

priorities of the company. Financial decisions is a comprehensive financial planning and wealth

management firm that helps high-net-worth business to achieve their financial goals. Financial

goals are made by making the financial priorities. The financial priorities to be considered for

decision making are: Cost control: this measure is used to reduce or control the business expenses. By

identifying and evaluating the business's expenses, management can determine weather

those cost are reasonable and affordable. For this a proper budget should be made, and on

the basis of this budget operation cost could be reduced through methods such as cutting

back,moving to a less expensive plan or changing service providers. Cost control is one

decision are: Market fluctuations: the fluctuations in the demand and supply of the product in the

market can effect both financial and business decisions. With the decline in the demand

of the product, the decision regarding operational management will be effected, as well as

the financial decision regarding the increase in production and inventory amount will be

effected. market fluctuation leads to worsened the gross margins and profitability which

leads the management to change the business decisions. Fluctuations in foreign currency and interest rates:since the cost and the value of assets

and debts of business operation are influenced by the fluctuations in interest rates or

currency rates in market, it will affect the financial condition of the business (Heitzman

and Huang, 2018). The business, than has to make new decisions regarding sales volume

and material volume in foreign currencies.

Competition: More the competition in the market more the risk of loosing the customer

for the business. The business has to take new marketing decision to attract the customer.

With the increase in competition in the market, the sells of the product will decrease

which leads the business to reduce its price which will affect the profit margin of the

company.

1.4 Summarize the financial priorities that need to be considered when making financial

decisions.

Before making financial decision, management should ascertain what are the financial

priorities of the company. Financial decisions is a comprehensive financial planning and wealth

management firm that helps high-net-worth business to achieve their financial goals. Financial

goals are made by making the financial priorities. The financial priorities to be considered for

decision making are: Cost control: this measure is used to reduce or control the business expenses. By

identifying and evaluating the business's expenses, management can determine weather

those cost are reasonable and affordable. For this a proper budget should be made, and on

the basis of this budget operation cost could be reduced through methods such as cutting

back,moving to a less expensive plan or changing service providers. Cost control is one

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of the financial priorities of the company to set a goal of cost effective measures of

operations. Profit Maximization: a companies most important goal is to make profit. Profit

maximization is the foremost important priority of a company. High operating profits can

mean that company has effective control of cost. To maintain the expenses the profit

maximization should be achieved. A specific measure should be set to determine weather

the company has achieved the the profit as per the aim or not (Pratt, 2016). For example,

the company has make a goal to attain 10% of profit margin of the business per year, so

the decision will be made according to aim set by the business.

Sales-revenue enhancement: sales revenue is company's sale over a given period of

time. Increasing in the sales revenue is to be considered before making financial

decision. Increasing in the sales revenue will increase the market share of the company at

the same rate as the total market. A business weather small or big will always want to

enhance its market share as it will enhance its sales revenue for the business.

SECTION 2

2.1- The method of cash focuses on the instant identification on the expenses and revenues while

accrual basis focuses on forecasting of incomes and expenses.

Basis of

comparison

Cash basis Accrual basis

Meaning The cash basis method of accounting

in which incomes are recorded in the

statement when the cash is actually

received and expenses are recorded

when they actually paid out.

The accrual basis is the accounting in

which incomes are earned, (yet not

received) recorded in the statements

and the expenses occurs (yet not paid)

are recorded in the statement.

Nature Cash basis of accounting is effortless

in nature

Accrual basis of accounting is

complex in nature

Method Cash basis of accounting is not

recognizing under the companies act

Accrual basis of accounting is

recognized by the method of

operations. Profit Maximization: a companies most important goal is to make profit. Profit

maximization is the foremost important priority of a company. High operating profits can

mean that company has effective control of cost. To maintain the expenses the profit

maximization should be achieved. A specific measure should be set to determine weather

the company has achieved the the profit as per the aim or not (Pratt, 2016). For example,

the company has make a goal to attain 10% of profit margin of the business per year, so

the decision will be made according to aim set by the business.

Sales-revenue enhancement: sales revenue is company's sale over a given period of

time. Increasing in the sales revenue is to be considered before making financial

decision. Increasing in the sales revenue will increase the market share of the company at

the same rate as the total market. A business weather small or big will always want to

enhance its market share as it will enhance its sales revenue for the business.

SECTION 2

2.1- The method of cash focuses on the instant identification on the expenses and revenues while

accrual basis focuses on forecasting of incomes and expenses.

Basis of

comparison

Cash basis Accrual basis

Meaning The cash basis method of accounting

in which incomes are recorded in the

statement when the cash is actually

received and expenses are recorded

when they actually paid out.

The accrual basis is the accounting in

which incomes are earned, (yet not

received) recorded in the statements

and the expenses occurs (yet not paid)

are recorded in the statement.

Nature Cash basis of accounting is effortless

in nature

Accrual basis of accounting is

complex in nature

Method Cash basis of accounting is not

recognizing under the companies act

Accrual basis of accounting is

recognized by the method of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 companies act 2013.

Income

statements

In this method of accounting,

statement of accounting shows the

lower income

In this accrual basis method, the

income statements show the high

income comparatively.

Applicability of

matching

concept

Cash accounting do not adjust with

the matching concept

Accrual accounting fully implies with

matching concept.

Recognition Cash is received in the case of income

and paid in the case of expenses

(Graham and et.al., 2017)

Revenue is earned in the case of

income and expenses incurred in the

case of expenses.

Suitability This method of accounting is more

suitable for the sole proprietorship or

contractors,

This method of accounting is more

suitable for, enterprises, firms.

The change in cash and accrual basis effect the business decision making as businesses

grow their financial need keeps on changing. Whether a company is experiencing a change in

revenue or in expenses.

2.2- explain the structure and content of final accounts and their uses for business decision

making

structure of final accounts consists of following -

1- Profitability account

Profitability account is an amended form of trading and profit loss account. It records all

the trading expenses through which the gross profit identifies and records all the expenses which

the part of trading is not (Bruch and Feinberg, 2017). The profitability account provides a deeper

insight of margin generated over the expenses. Profitability statement shows manager and

investors whether the company made or lost money during the period being reported.

Its sub content is

gross profit or loss

office expenses, selling and distribution expenses

miscellaneous expenses (Loan, interest on capital, repair charges etc.)

Income

statements

In this method of accounting,

statement of accounting shows the

lower income

In this accrual basis method, the

income statements show the high

income comparatively.

Applicability of

matching

concept

Cash accounting do not adjust with

the matching concept

Accrual accounting fully implies with

matching concept.

Recognition Cash is received in the case of income

and paid in the case of expenses

(Graham and et.al., 2017)

Revenue is earned in the case of

income and expenses incurred in the

case of expenses.

Suitability This method of accounting is more

suitable for the sole proprietorship or

contractors,

This method of accounting is more

suitable for, enterprises, firms.

The change in cash and accrual basis effect the business decision making as businesses

grow their financial need keeps on changing. Whether a company is experiencing a change in

revenue or in expenses.

2.2- explain the structure and content of final accounts and their uses for business decision

making

structure of final accounts consists of following -

1- Profitability account

Profitability account is an amended form of trading and profit loss account. It records all

the trading expenses through which the gross profit identifies and records all the expenses which

the part of trading is not (Bruch and Feinberg, 2017). The profitability account provides a deeper

insight of margin generated over the expenses. Profitability statement shows manager and

investors whether the company made or lost money during the period being reported.

Its sub content is

gross profit or loss

office expenses, selling and distribution expenses

miscellaneous expenses (Loan, interest on capital, repair charges etc.)

other income (rent received, commission earned etc)

2- Balance sheet

After making a profitability statement, balance sheet is prepared which shows the exact

financial position of the business (Veatch, 2017). To ascertain this balance sheet statement

contains all assets and liabilities of the enterprise.

The sub contents of asset and liabilities are as under

Current liabilities

Fixed liabilities

Reserves

Capital

Current assets

Fixed assets

3- Statements of cash flow

Cash flow is the statement which shows the inflow and outflow cash and cash equivalent.

It includes the following sub content -

Cash from Operating activities (receipts from sales of goods and services, interest

payments, income tax payments etc)

Cash from Investing activities (purchase or sale of an asset)

Cash from Financing activities (Issue and redemption of shares and debentures

etc)

2.3 interpret the financial information in the financial statements you have obtained and illustrate

differences between the sets of accounts

financial statements include a preparation of balance sheet and an income statement.

Preparation of balance sheet consist of assets and liabilities, equity of a specific date in time. And

the statement consists of company, revenue, expenses, and net income (Karl, 2018). The

interpretation of financial statement is an important management tool as it signifies the analysis.

Following procedure is to be followed to interpret the financial statement

Firstly, prepare the common sized balance sheet for the financial statement which shows

the dollar value of the income and expenses account.

2- Balance sheet

After making a profitability statement, balance sheet is prepared which shows the exact

financial position of the business (Veatch, 2017). To ascertain this balance sheet statement

contains all assets and liabilities of the enterprise.

The sub contents of asset and liabilities are as under

Current liabilities

Fixed liabilities

Reserves

Capital

Current assets

Fixed assets

3- Statements of cash flow

Cash flow is the statement which shows the inflow and outflow cash and cash equivalent.

It includes the following sub content -

Cash from Operating activities (receipts from sales of goods and services, interest

payments, income tax payments etc)

Cash from Investing activities (purchase or sale of an asset)

Cash from Financing activities (Issue and redemption of shares and debentures

etc)

2.3 interpret the financial information in the financial statements you have obtained and illustrate

differences between the sets of accounts

financial statements include a preparation of balance sheet and an income statement.

Preparation of balance sheet consist of assets and liabilities, equity of a specific date in time. And

the statement consists of company, revenue, expenses, and net income (Karl, 2018). The

interpretation of financial statement is an important management tool as it signifies the analysis.

Following procedure is to be followed to interpret the financial statement

Firstly, prepare the common sized balance sheet for the financial statement which shows

the dollar value of the income and expenses account.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

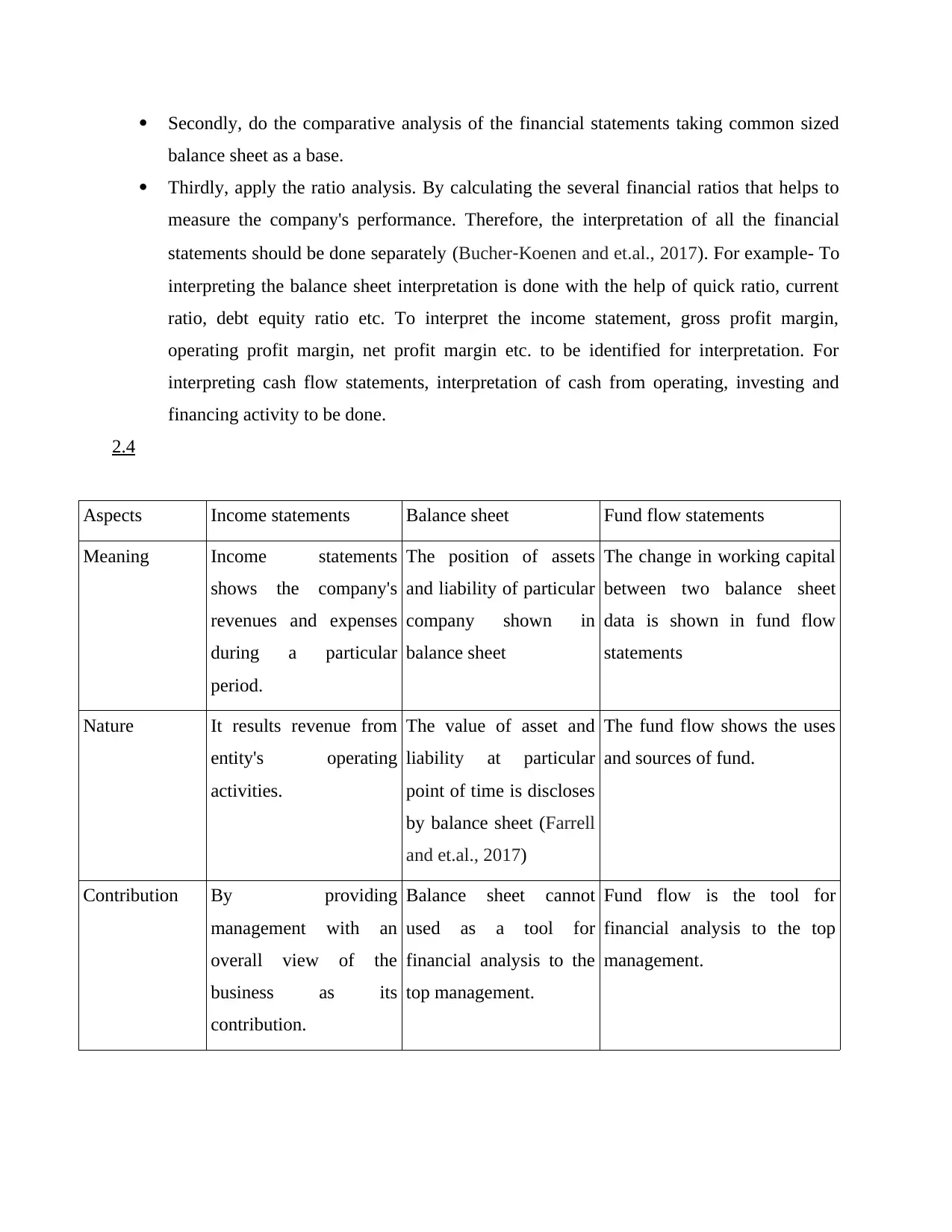

Secondly, do the comparative analysis of the financial statements taking common sized

balance sheet as a base.

Thirdly, apply the ratio analysis. By calculating the several financial ratios that helps to

measure the company's performance. Therefore, the interpretation of all the financial

statements should be done separately (Bucher‐Koenen and et.al., 2017). For example- To

interpreting the balance sheet interpretation is done with the help of quick ratio, current

ratio, debt equity ratio etc. To interpret the income statement, gross profit margin,

operating profit margin, net profit margin etc. to be identified for interpretation. For

interpreting cash flow statements, interpretation of cash from operating, investing and

financing activity to be done.

2.4

Aspects Income statements Balance sheet Fund flow statements

Meaning Income statements

shows the company's

revenues and expenses

during a particular

period.

The position of assets

and liability of particular

company shown in

balance sheet

The change in working capital

between two balance sheet

data is shown in fund flow

statements

Nature It results revenue from

entity's operating

activities.

The value of asset and

liability at particular

point of time is discloses

by balance sheet (Farrell

and et.al., 2017)

The fund flow shows the uses

and sources of fund.

Contribution By providing

management with an

overall view of the

business as its

contribution.

Balance sheet cannot

used as a tool for

financial analysis to the

top management.

Fund flow is the tool for

financial analysis to the top

management.

balance sheet as a base.

Thirdly, apply the ratio analysis. By calculating the several financial ratios that helps to

measure the company's performance. Therefore, the interpretation of all the financial

statements should be done separately (Bucher‐Koenen and et.al., 2017). For example- To

interpreting the balance sheet interpretation is done with the help of quick ratio, current

ratio, debt equity ratio etc. To interpret the income statement, gross profit margin,

operating profit margin, net profit margin etc. to be identified for interpretation. For

interpreting cash flow statements, interpretation of cash from operating, investing and

financing activity to be done.

2.4

Aspects Income statements Balance sheet Fund flow statements

Meaning Income statements

shows the company's

revenues and expenses

during a particular

period.

The position of assets

and liability of particular

company shown in

balance sheet

The change in working capital

between two balance sheet

data is shown in fund flow

statements

Nature It results revenue from

entity's operating

activities.

The value of asset and

liability at particular

point of time is discloses

by balance sheet (Farrell

and et.al., 2017)

The fund flow shows the uses

and sources of fund.

Contribution By providing

management with an

overall view of the

business as its

contribution.

Balance sheet cannot

used as a tool for

financial analysis to the

top management.

Fund flow is the tool for

financial analysis to the top

management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

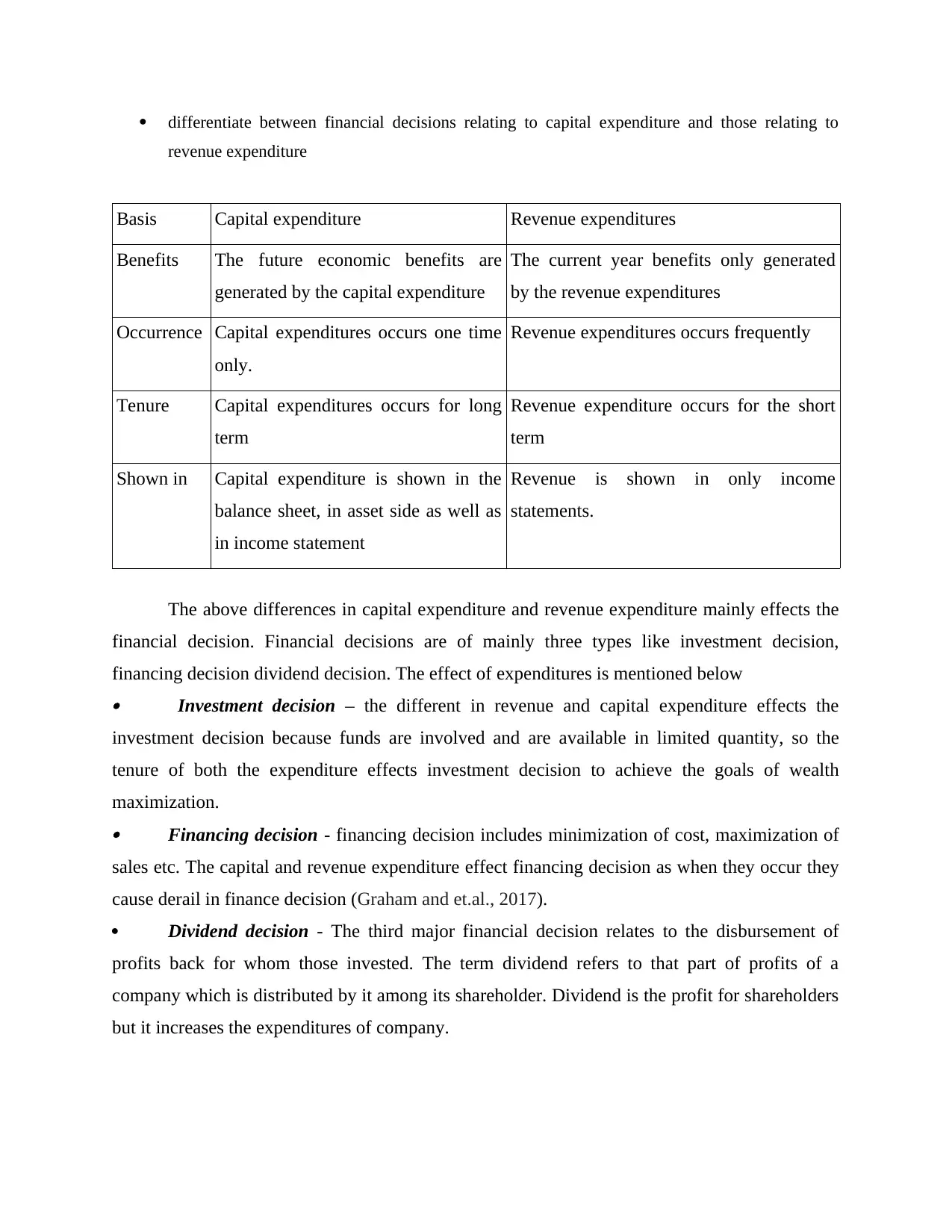

differentiate between financial decisions relating to capital expenditure and those relating to

revenue expenditure

Basis Capital expenditure Revenue expenditures

Benefits The future economic benefits are

generated by the capital expenditure

The current year benefits only generated

by the revenue expenditures

Occurrence Capital expenditures occurs one time

only.

Revenue expenditures occurs frequently

Tenure Capital expenditures occurs for long

term

Revenue expenditure occurs for the short

term

Shown in Capital expenditure is shown in the

balance sheet, in asset side as well as

in income statement

Revenue is shown in only income

statements.

The above differences in capital expenditure and revenue expenditure mainly effects the

financial decision. Financial decisions are of mainly three types like investment decision,

financing decision dividend decision. The effect of expenditures is mentioned below Investment decision – the different in revenue and capital expenditure effects the

investment decision because funds are involved and are available in limited quantity, so the

tenure of both the expenditure effects investment decision to achieve the goals of wealth

maximization. Financing decision - financing decision includes minimization of cost, maximization of

sales etc. The capital and revenue expenditure effect financing decision as when they occur they

cause derail in finance decision (Graham and et.al., 2017).

Dividend decision - The third major financial decision relates to the disbursement of

profits back for whom those invested. The term dividend refers to that part of profits of a

company which is distributed by it among its shareholder. Dividend is the profit for shareholders

but it increases the expenditures of company.

revenue expenditure

Basis Capital expenditure Revenue expenditures

Benefits The future economic benefits are

generated by the capital expenditure

The current year benefits only generated

by the revenue expenditures

Occurrence Capital expenditures occurs one time

only.

Revenue expenditures occurs frequently

Tenure Capital expenditures occurs for long

term

Revenue expenditure occurs for the short

term

Shown in Capital expenditure is shown in the

balance sheet, in asset side as well as

in income statement

Revenue is shown in only income

statements.

The above differences in capital expenditure and revenue expenditure mainly effects the

financial decision. Financial decisions are of mainly three types like investment decision,

financing decision dividend decision. The effect of expenditures is mentioned below Investment decision – the different in revenue and capital expenditure effects the

investment decision because funds are involved and are available in limited quantity, so the

tenure of both the expenditure effects investment decision to achieve the goals of wealth

maximization. Financing decision - financing decision includes minimization of cost, maximization of

sales etc. The capital and revenue expenditure effect financing decision as when they occur they

cause derail in finance decision (Graham and et.al., 2017).

Dividend decision - The third major financial decision relates to the disbursement of

profits back for whom those invested. The term dividend refers to that part of profits of a

company which is distributed by it among its shareholder. Dividend is the profit for shareholders

but it increases the expenditures of company.

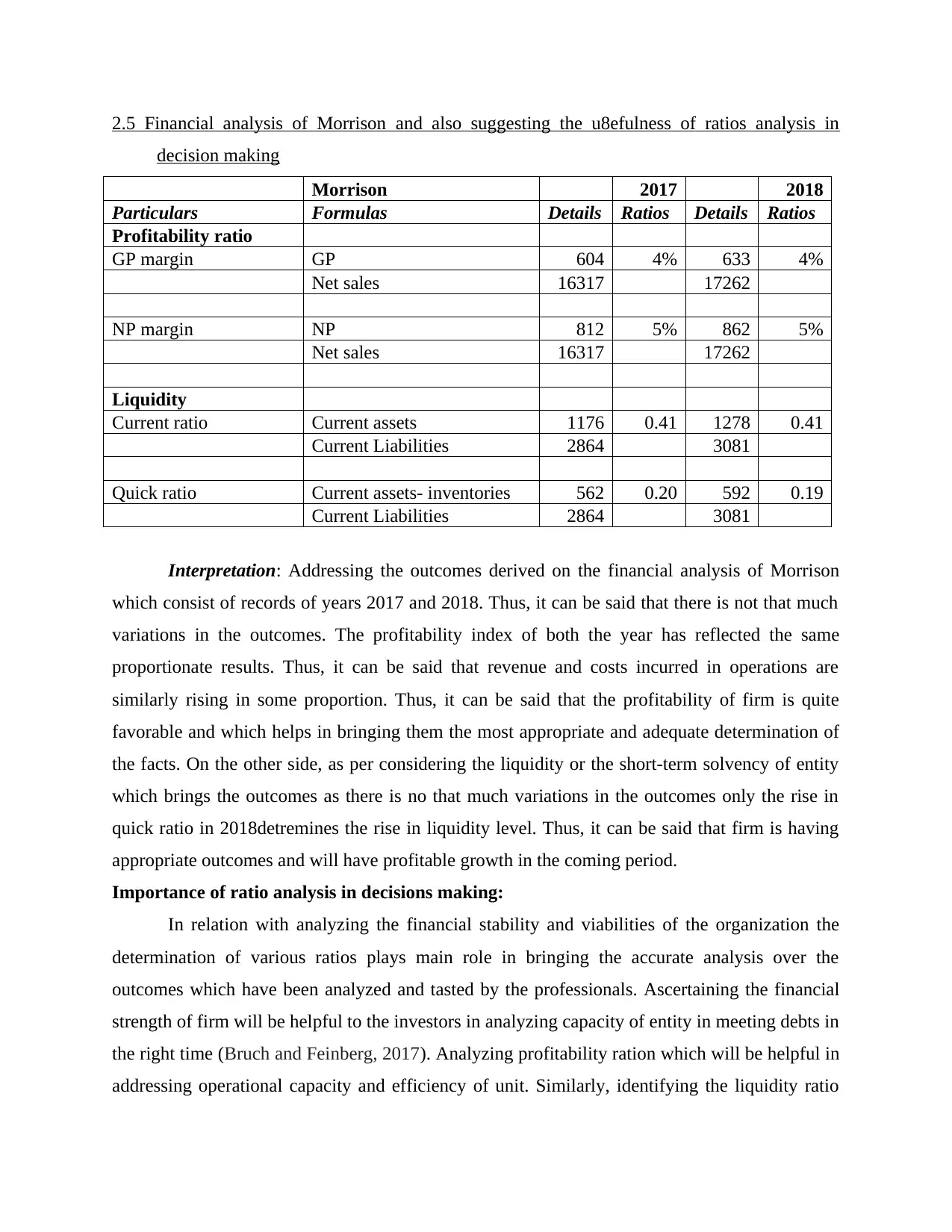

2.5 Financial analysis of Morrison and also suggesting the u8efulness of ratios analysis in

decision making

Morrison 2017 2018

Particulars Formulas Details Ratios Details Ratios

Profitability ratio

GP margin GP 604 4% 633 4%

Net sales 16317 17262

NP margin NP 812 5% 862 5%

Net sales 16317 17262

Liquidity

Current ratio Current assets 1176 0.41 1278 0.41

Current Liabilities 2864 3081

Quick ratio Current assets- inventories 562 0.20 592 0.19

Current Liabilities 2864 3081

Interpretation: Addressing the outcomes derived on the financial analysis of Morrison

which consist of records of years 2017 and 2018. Thus, it can be said that there is not that much

variations in the outcomes. The profitability index of both the year has reflected the same

proportionate results. Thus, it can be said that revenue and costs incurred in operations are

similarly rising in some proportion. Thus, it can be said that the profitability of firm is quite

favorable and which helps in bringing them the most appropriate and adequate determination of

the facts. On the other side, as per considering the liquidity or the short-term solvency of entity

which brings the outcomes as there is no that much variations in the outcomes only the rise in

quick ratio in 2018detremines the rise in liquidity level. Thus, it can be said that firm is having

appropriate outcomes and will have profitable growth in the coming period.

Importance of ratio analysis in decisions making:

In relation with analyzing the financial stability and viabilities of the organization the

determination of various ratios plays main role in bringing the accurate analysis over the

outcomes which have been analyzed and tasted by the professionals. Ascertaining the financial

strength of firm will be helpful to the investors in analyzing capacity of entity in meeting debts in

the right time (Bruch and Feinberg, 2017). Analyzing profitability ration which will be helpful in

addressing operational capacity and efficiency of unit. Similarly, identifying the liquidity ratio

decision making

Morrison 2017 2018

Particulars Formulas Details Ratios Details Ratios

Profitability ratio

GP margin GP 604 4% 633 4%

Net sales 16317 17262

NP margin NP 812 5% 862 5%

Net sales 16317 17262

Liquidity

Current ratio Current assets 1176 0.41 1278 0.41

Current Liabilities 2864 3081

Quick ratio Current assets- inventories 562 0.20 592 0.19

Current Liabilities 2864 3081

Interpretation: Addressing the outcomes derived on the financial analysis of Morrison

which consist of records of years 2017 and 2018. Thus, it can be said that there is not that much

variations in the outcomes. The profitability index of both the year has reflected the same

proportionate results. Thus, it can be said that revenue and costs incurred in operations are

similarly rising in some proportion. Thus, it can be said that the profitability of firm is quite

favorable and which helps in bringing them the most appropriate and adequate determination of

the facts. On the other side, as per considering the liquidity or the short-term solvency of entity

which brings the outcomes as there is no that much variations in the outcomes only the rise in

quick ratio in 2018detremines the rise in liquidity level. Thus, it can be said that firm is having

appropriate outcomes and will have profitable growth in the coming period.

Importance of ratio analysis in decisions making:

In relation with analyzing the financial stability and viabilities of the organization the

determination of various ratios plays main role in bringing the accurate analysis over the

outcomes which have been analyzed and tasted by the professionals. Ascertaining the financial

strength of firm will be helpful to the investors in analyzing capacity of entity in meeting debts in

the right time (Bruch and Feinberg, 2017). Analyzing profitability ration which will be helpful in

addressing operational capacity and efficiency of unit. Similarly, identifying the liquidity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.