Advance Finance for Decision Makers: Financial Decision-Making Report

VerifiedAdded on 2023/01/13

|25

|6105

|55

Report

AI Summary

This report, designed for advanced finance decision-makers, delves into the crucial financial factors that influence business choices. It examines topics such as return on investment, competition, social responsibility, and brand image. The report then compares accrual and cash flow accounting methods, analyzing their implications in financial reporting and decision-making processes. It explores the structure and content of financial statements, including income statements, balance sheets, and cash flow statements, highlighting their use in business decision-making. The report also covers accounting ethics, business ethics, corporate governance, and the roles of finance directors. Furthermore, it discusses long-term financing, working capital management, capital investment decisions, and the benefits and drawbacks of off-balance sheet financing. Finally, it analyzes the financial implications of various business ownership structures, emphasizing the significance of return on capital employed and other performance measures for long-term business sustainability. This report provides a comprehensive overview of financial decision-making principles and practices.

Advance Finance for Decision

Makers

Makers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

Section 1...........................................................................................................................................4

1.1 Examining various factors that drives for decision making of the business .........................4

1.2 Assessing importance of the financial factors in the business decision making ...................5

1.3 Determining features of the business risk that affects business decision and financials ......5

1.4 Summarising financial priorities which requires to be taken into account at the time of

making the financial decisions ....................................................................................................6

Section 2...........................................................................................................................................6

2.1 Comparing accrual and cash flow approaches to the accounting and financial reporting and

their implications in decision making..........................................................................................6

2.2 Structure and content of final accounts and its use in decision making. ..............................7

2.3 Financial financial information and difference between sets of accounts...........................13

2.4 Difference between decisions relating to revenue and capital expenditure.........................14

2.5 Ratios used in decision making............................................................................................14

2.6 Key requirements for published accounts of public limited company................................15

Section 3.........................................................................................................................................15

3.1 Stating the difference between accounting ethics, business ethics and the governance in

order to ensure control on the business accountability .............................................................15

3.2 Assessing role of finance director as the guardian of the business ethics ..........................16

3.3 Analysing important principles and the concept of the corporate governance that might

impacts business decisions ........................................................................................................17

3.4 Examining the national and an international reporting standards which are relevant to the

business decisions......................................................................................................................17

Section 4.........................................................................................................................................17

4.1 Difference between the long term financing and working capital needs of business. ........17

4.2 Sources of long term finances and working capital finance. ..............................................19

4.3 Reasons behind accessibility of working capital for the business continuity......................19

4.4 Techniques needed for managing cash flows and impact of cash flows on business..........20

4.5 Methods of making capital investment decisions. ..............................................................20

INTRODUCTION...........................................................................................................................4

Section 1...........................................................................................................................................4

1.1 Examining various factors that drives for decision making of the business .........................4

1.2 Assessing importance of the financial factors in the business decision making ...................5

1.3 Determining features of the business risk that affects business decision and financials ......5

1.4 Summarising financial priorities which requires to be taken into account at the time of

making the financial decisions ....................................................................................................6

Section 2...........................................................................................................................................6

2.1 Comparing accrual and cash flow approaches to the accounting and financial reporting and

their implications in decision making..........................................................................................6

2.2 Structure and content of final accounts and its use in decision making. ..............................7

2.3 Financial financial information and difference between sets of accounts...........................13

2.4 Difference between decisions relating to revenue and capital expenditure.........................14

2.5 Ratios used in decision making............................................................................................14

2.6 Key requirements for published accounts of public limited company................................15

Section 3.........................................................................................................................................15

3.1 Stating the difference between accounting ethics, business ethics and the governance in

order to ensure control on the business accountability .............................................................15

3.2 Assessing role of finance director as the guardian of the business ethics ..........................16

3.3 Analysing important principles and the concept of the corporate governance that might

impacts business decisions ........................................................................................................17

3.4 Examining the national and an international reporting standards which are relevant to the

business decisions......................................................................................................................17

Section 4.........................................................................................................................................17

4.1 Difference between the long term financing and working capital needs of business. ........17

4.2 Sources of long term finances and working capital finance. ..............................................19

4.3 Reasons behind accessibility of working capital for the business continuity......................19

4.4 Techniques needed for managing cash flows and impact of cash flows on business..........20

4.5 Methods of making capital investment decisions. ..............................................................20

4.6 Benefits and Drawbacks of off balance sheet financing......................................................22

Section 5 ........................................................................................................................................22

5.1 Financial implications of various business ownership structures. ......................................22

5.2 Analysing corporate governance, legal and regulatory environments of different ownership

structures of business. ...............................................................................................................23

5.3 Comparing and contrasting interests of managers and owners in decision making............23

5.4 Significance of return on capital employed and other performance measures for long term

business sustainability................................................................................................................24

5.5 Examining importance of the EPS as measure business performance................................24

CONCLUSION..............................................................................................................................24

REFERENCES................................................................................................................................1

Section 5 ........................................................................................................................................22

5.1 Financial implications of various business ownership structures. ......................................22

5.2 Analysing corporate governance, legal and regulatory environments of different ownership

structures of business. ...............................................................................................................23

5.3 Comparing and contrasting interests of managers and owners in decision making............23

5.4 Significance of return on capital employed and other performance measures for long term

business sustainability................................................................................................................24

5.5 Examining importance of the EPS as measure business performance................................24

CONCLUSION..............................................................................................................................24

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every business is aware of the fact that profitability of company is affected by the

decisions taken. Financial managers have a crucial role in the growth and success of business as

all the business activities run on the decisions taken. Decision making is process of gathering all

the information and facts relating to the aspect for which business is to be taken. The study

provide the understanding about the various financial factors influencing the decision making. It

will also provide about the concepts and tools used by the managers in taking financial decisions

of company. It will also cover accountability for financial reporting, sources of finance and

financial performance of different ownership structures.

Section 1

1.1 Examining various factors that drives for decision making of the business

Return on investment- It is reflected as the difference in between the money that is

invested in the things such as inventory, marketing, actual return and potential. ROI controls the

modifying risk of investment and it influences and drives both type of business decisions that

includes pre-investment and the post-investment.

Competition- This factor is said as one of the major aspect which strongly recommends

within the process of the decision making (Kumar, 2017). Today's world is seen as dynamic and

highly competitive so it is important for an organization to pay attention towards the challenges

and the operation of the business. Thus, at the time of making decisions in relation to the future

developments, business needs to consider the competitors and their respective plans for business

development.

Social responsibility- It is also a crucial factor that influences the decision making in the

business. In such concept, business needs to be acting in an interest of the society for the sake of

their common good.

Brand image- Managing brand image also influences the decision making that emphasize

on intangible gains in respect of the public perceptions (Diouf and Hebb, 2016). It concentrates

on differentiating business from the rivalry and developing faithfulness among the customers,

encourages the decisions regarding estimating, exhibiting products & the services at a standard

level.

Every business is aware of the fact that profitability of company is affected by the

decisions taken. Financial managers have a crucial role in the growth and success of business as

all the business activities run on the decisions taken. Decision making is process of gathering all

the information and facts relating to the aspect for which business is to be taken. The study

provide the understanding about the various financial factors influencing the decision making. It

will also provide about the concepts and tools used by the managers in taking financial decisions

of company. It will also cover accountability for financial reporting, sources of finance and

financial performance of different ownership structures.

Section 1

1.1 Examining various factors that drives for decision making of the business

Return on investment- It is reflected as the difference in between the money that is

invested in the things such as inventory, marketing, actual return and potential. ROI controls the

modifying risk of investment and it influences and drives both type of business decisions that

includes pre-investment and the post-investment.

Competition- This factor is said as one of the major aspect which strongly recommends

within the process of the decision making (Kumar, 2017). Today's world is seen as dynamic and

highly competitive so it is important for an organization to pay attention towards the challenges

and the operation of the business. Thus, at the time of making decisions in relation to the future

developments, business needs to consider the competitors and their respective plans for business

development.

Social responsibility- It is also a crucial factor that influences the decision making in the

business. In such concept, business needs to be acting in an interest of the society for the sake of

their common good.

Brand image- Managing brand image also influences the decision making that emphasize

on intangible gains in respect of the public perceptions (Diouf and Hebb, 2016). It concentrates

on differentiating business from the rivalry and developing faithfulness among the customers,

encourages the decisions regarding estimating, exhibiting products & the services at a standard

level.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Assessing importance of the financial factors in the business decision making

Accounts receivable- It is the major financial factors that leads to business growth and

requires an unanticipated bank loans. In order to run its business smoothly it is essential for the

business firm to consider at the indicators like turnover of the accounts receivable, cash

collection, credit policies and an ageing of the receivables.

Net income- This factor is counted as essential because it shows the profits earned by the

company after meeting all its expenses, costs and the tax liabilities (Rubin and Patel, 2017). This

factor helps the company in making decision relating to keeping control over the cost so and

increasing the percentage of the revenue so that higher profitability could be attained.

Working capital- It is stated as the difference between the current liabilities and the

assets. Without adequate working capital, business enterprise cannot run its business smoothly.

Thus, it acts as the most important financial factor as it helps the firm in making the decisions

regarding optimum use of the resources so that efficient and effective working capital can be

maintained for achieving objectives of the business.

Sales or operating revenue- It referred as the financial factor that shows the revenue

generated by an entity through selling its stock (Parent, Kalenkoski and Cardella, 2018). Higher

sales depicts higher profitability and growth rate of the company so it is very important for the

firm to seek appropriate measures in meeting the sales target. This in turn helps in making the

decision regarding the operational activities and in relation to demand of the customers.

1.3 Determining features of the business risk that affects business decision and financials

Time- In the present scenario, time is been characterized by an intense competition,

globalization of an economy, advanced technology. In the future periods or coming periods

business risk are tend to increase in an intensity. This affects and impacts the financial and the

business decision to great extent as for surviving in the business it is important for it to cope up

with the changes.

Nature of the business risk- In case the business is engaged in the manufacturing or

buying of the basic necessity items such as cloth, oil and the sugar. There seems to be less risk as

demand for majority of the items is counted as inelastic (Boatright, 2017). However, in case the

company is engaged in manufacturing of the luxury items are seen as exposed towards the

business risk due to the demand for the luxury items is reflected as highly elastic. In this way the

business and the financial decision of an entity are influenced.

Accounts receivable- It is the major financial factors that leads to business growth and

requires an unanticipated bank loans. In order to run its business smoothly it is essential for the

business firm to consider at the indicators like turnover of the accounts receivable, cash

collection, credit policies and an ageing of the receivables.

Net income- This factor is counted as essential because it shows the profits earned by the

company after meeting all its expenses, costs and the tax liabilities (Rubin and Patel, 2017). This

factor helps the company in making decision relating to keeping control over the cost so and

increasing the percentage of the revenue so that higher profitability could be attained.

Working capital- It is stated as the difference between the current liabilities and the

assets. Without adequate working capital, business enterprise cannot run its business smoothly.

Thus, it acts as the most important financial factor as it helps the firm in making the decisions

regarding optimum use of the resources so that efficient and effective working capital can be

maintained for achieving objectives of the business.

Sales or operating revenue- It referred as the financial factor that shows the revenue

generated by an entity through selling its stock (Parent, Kalenkoski and Cardella, 2018). Higher

sales depicts higher profitability and growth rate of the company so it is very important for the

firm to seek appropriate measures in meeting the sales target. This in turn helps in making the

decision regarding the operational activities and in relation to demand of the customers.

1.3 Determining features of the business risk that affects business decision and financials

Time- In the present scenario, time is been characterized by an intense competition,

globalization of an economy, advanced technology. In the future periods or coming periods

business risk are tend to increase in an intensity. This affects and impacts the financial and the

business decision to great extent as for surviving in the business it is important for it to cope up

with the changes.

Nature of the business risk- In case the business is engaged in the manufacturing or

buying of the basic necessity items such as cloth, oil and the sugar. There seems to be less risk as

demand for majority of the items is counted as inelastic (Boatright, 2017). However, in case the

company is engaged in manufacturing of the luxury items are seen as exposed towards the

business risk due to the demand for the luxury items is reflected as highly elastic. In this way the

business and the financial decision of an entity are influenced.

Sales term- If the business conducts its sales on the cash basis, the risk of the business are

seen as zero as possibility of the bad debts is concerned with. On the other state, an enterprise

conducting the business on the large credit sales are highly exposed with the risk regarding bad

debts.

1.4 Summarising financial priorities which requires to be taken into account at the time of

making the financial decisions

Understanding financial goals- prior to making financial decision it is important that the

company makes sets its financial goals. This helps in making suitable decisions in respect of

raising the funds and performing tasks in the common direction to achieve the financial

objectives.

Having the plan relating to debt pay-off- While making finance related decisions, an

enterprise needs to look over the debt obligation by way of preparing the pay-off plan. This

ensures prevention of the firm in taking too much of the loan amount in future periods.

Spending wisely- It is the another most important priority that could be made by effective

planning. This in turn ensures a good future in respect of generating higher profitability.

Safeguarding the financial documents- In order to keep the track record of all the final

investments in the document form is considered as cumbersome (Şahin, 2018). It is very crucial

for an enterprise to keep proper record and maintenance of its financial documents as such

documents act as evidence.

Performing for routine financial check-ups- There present a need for performing the

regular check-ups or review of an investment plans because it enables in making effective plan.

Routine review ensures that their investments directly aligned with their spending requirements.

Thus, it is critical for an organization for keeping a constant check on the financial planning.

This helps in making suitable financial decisions with regards to raising of the funds and its

allocation so that larger amount of profits can be generated.

Section 2

2.1 Comparing accrual and cash flow approaches to the accounting and financial reporting and

their implications in decision making.

Cash Basis – The accounting method only recognises the revenues when the cash is received

similarly the expenses are recorded when they are actually paid. The cash accounting method do

not records accounts payable or accounts receivable.

seen as zero as possibility of the bad debts is concerned with. On the other state, an enterprise

conducting the business on the large credit sales are highly exposed with the risk regarding bad

debts.

1.4 Summarising financial priorities which requires to be taken into account at the time of

making the financial decisions

Understanding financial goals- prior to making financial decision it is important that the

company makes sets its financial goals. This helps in making suitable decisions in respect of

raising the funds and performing tasks in the common direction to achieve the financial

objectives.

Having the plan relating to debt pay-off- While making finance related decisions, an

enterprise needs to look over the debt obligation by way of preparing the pay-off plan. This

ensures prevention of the firm in taking too much of the loan amount in future periods.

Spending wisely- It is the another most important priority that could be made by effective

planning. This in turn ensures a good future in respect of generating higher profitability.

Safeguarding the financial documents- In order to keep the track record of all the final

investments in the document form is considered as cumbersome (Şahin, 2018). It is very crucial

for an enterprise to keep proper record and maintenance of its financial documents as such

documents act as evidence.

Performing for routine financial check-ups- There present a need for performing the

regular check-ups or review of an investment plans because it enables in making effective plan.

Routine review ensures that their investments directly aligned with their spending requirements.

Thus, it is critical for an organization for keeping a constant check on the financial planning.

This helps in making suitable financial decisions with regards to raising of the funds and its

allocation so that larger amount of profits can be generated.

Section 2

2.1 Comparing accrual and cash flow approaches to the accounting and financial reporting and

their implications in decision making.

Cash Basis – The accounting method only recognises the revenues when the cash is received

similarly the expenses are recorded when they are actually paid. The cash accounting method do

not records accounts payable or accounts receivable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accrual Basis – In this method expenses and revenues are recorded at the moment business has

earned them. The method do not allow company to wait till the transactions are actually paid or

received.

Both accrual and cash basis of accounting are separate methods used for recording the

accounting and financial transactions. Core underlying difference in the two methods is of

timings of recording the transactions. On aggregation results under both the approaches is same.

Timing difference among two methods is there because under cash system revenues are delayed

till the payment is received in actual from customers same is case in recording the expenses

(Minnis and Sutherland, 2017). On the other hand accrual system requires company to record

income and expenses as they are earned without depending on cash outflow.

The impact over decisions is not major as the end results under bot system is same. But

accrual systems reflects actual performance of company where the cash system do not reflect

actual position. Company may have completed a big project but is not recorded due to payments

in arrears. Therefore companies follow accrual basis of accounting to reflect true position of

company.

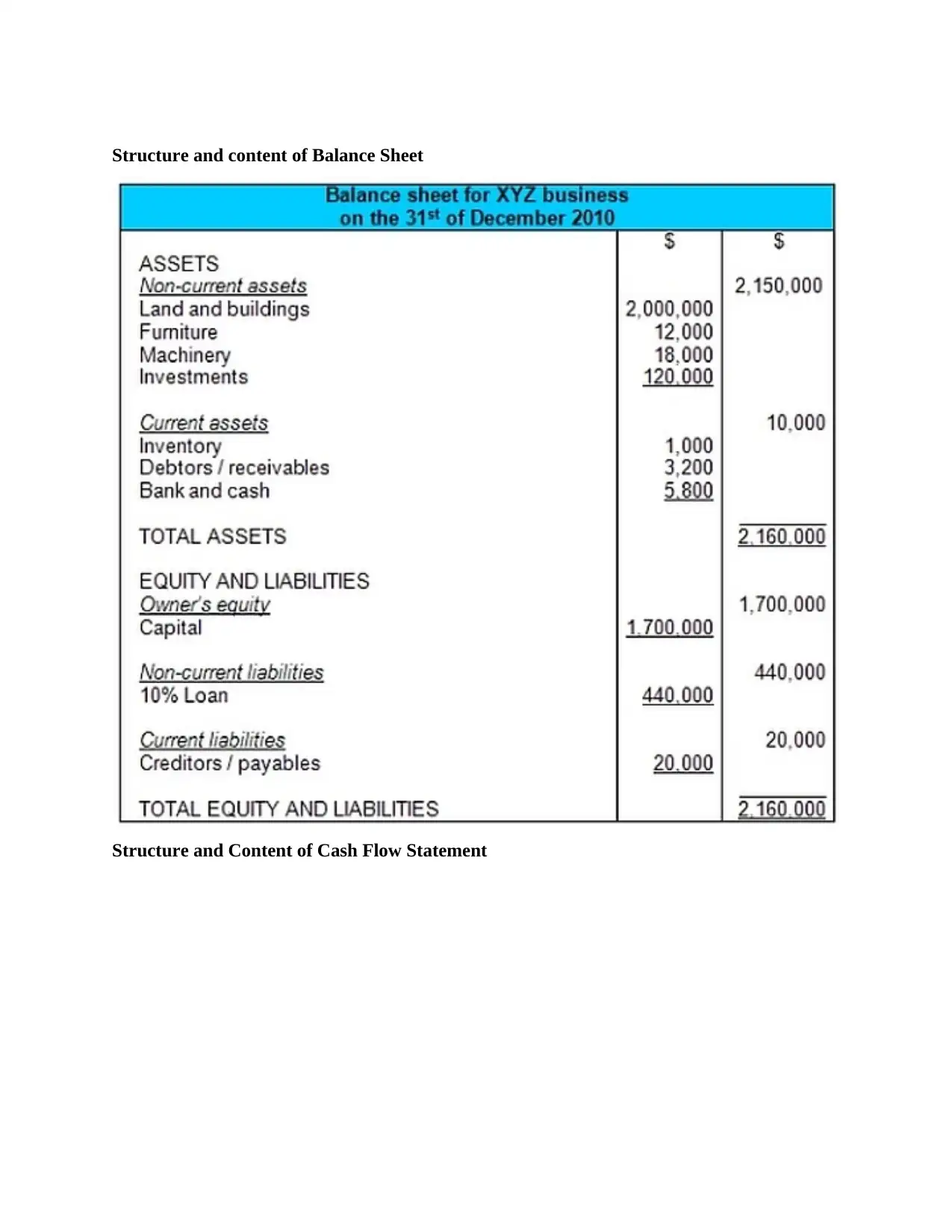

2.2 Structure and content of final accounts and its use in decision making.

Final accounts comprises mainly of the Income Statements, balance sheet and cash flows

statements of company.

Structure and contents of different final accounts.

Structure and contents of Income Statement

Income Statement

Year Ended April 30, 2017

Sales Revenue .($000)

Sales Revenue 117

Cost of Goods Sold 14

Gross Profit 103

earned them. The method do not allow company to wait till the transactions are actually paid or

received.

Both accrual and cash basis of accounting are separate methods used for recording the

accounting and financial transactions. Core underlying difference in the two methods is of

timings of recording the transactions. On aggregation results under both the approaches is same.

Timing difference among two methods is there because under cash system revenues are delayed

till the payment is received in actual from customers same is case in recording the expenses

(Minnis and Sutherland, 2017). On the other hand accrual system requires company to record

income and expenses as they are earned without depending on cash outflow.

The impact over decisions is not major as the end results under bot system is same. But

accrual systems reflects actual performance of company where the cash system do not reflect

actual position. Company may have completed a big project but is not recorded due to payments

in arrears. Therefore companies follow accrual basis of accounting to reflect true position of

company.

2.2 Structure and content of final accounts and its use in decision making.

Final accounts comprises mainly of the Income Statements, balance sheet and cash flows

statements of company.

Structure and contents of different final accounts.

Structure and contents of Income Statement

Income Statement

Year Ended April 30, 2017

Sales Revenue .($000)

Sales Revenue 117

Cost of Goods Sold 14

Gross Profit 103

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

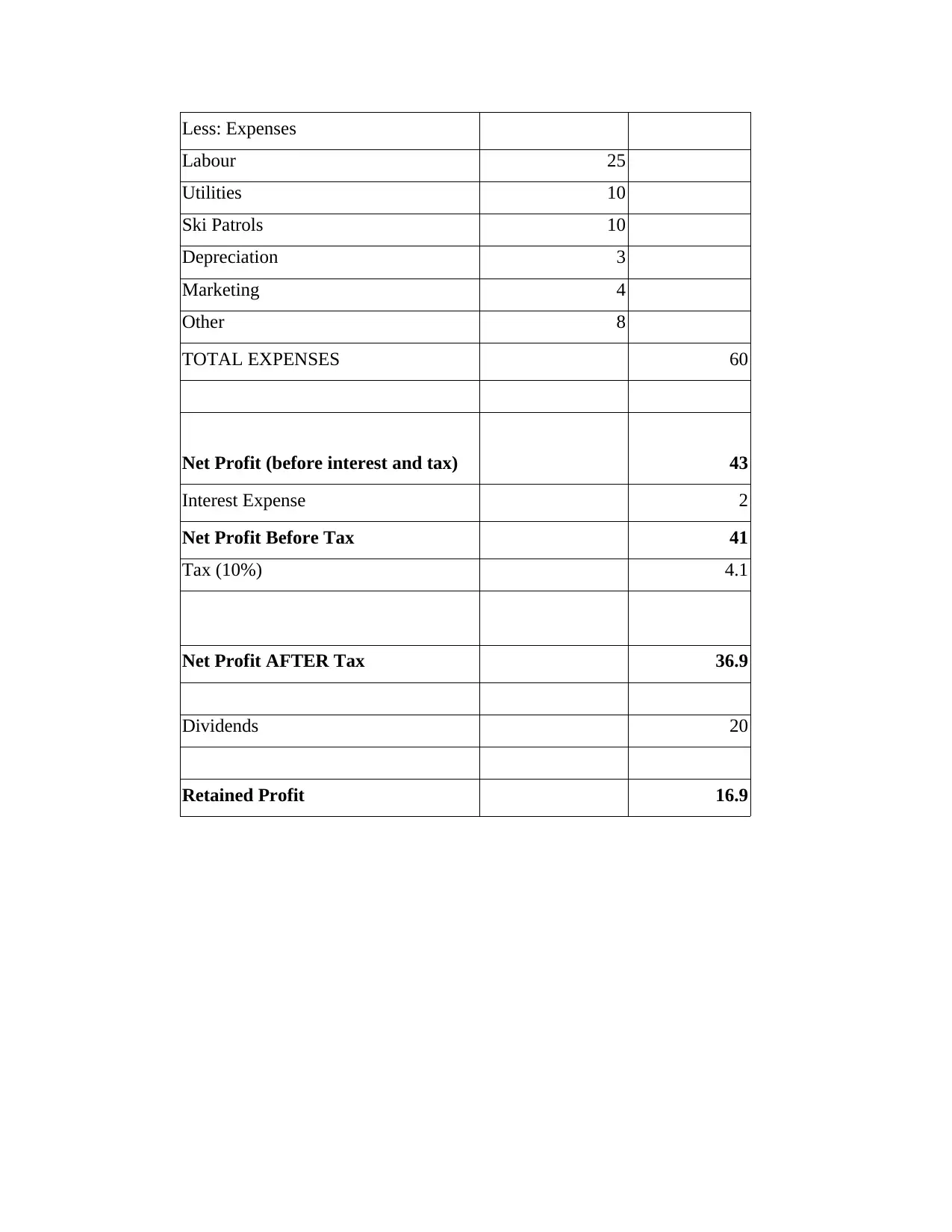

Less: Expenses

Labour 25

Utilities 10

Ski Patrols 10

Depreciation 3

Marketing 4

Other 8

TOTAL EXPENSES 60

Net Profit (before interest and tax) 43

Interest Expense 2

Net Profit Before Tax 41

Tax (10%) 4.1

Net Profit AFTER Tax 36.9

Dividends 20

Retained Profit 16.9

Labour 25

Utilities 10

Ski Patrols 10

Depreciation 3

Marketing 4

Other 8

TOTAL EXPENSES 60

Net Profit (before interest and tax) 43

Interest Expense 2

Net Profit Before Tax 41

Tax (10%) 4.1

Net Profit AFTER Tax 36.9

Dividends 20

Retained Profit 16.9

Structure and content of Balance Sheet

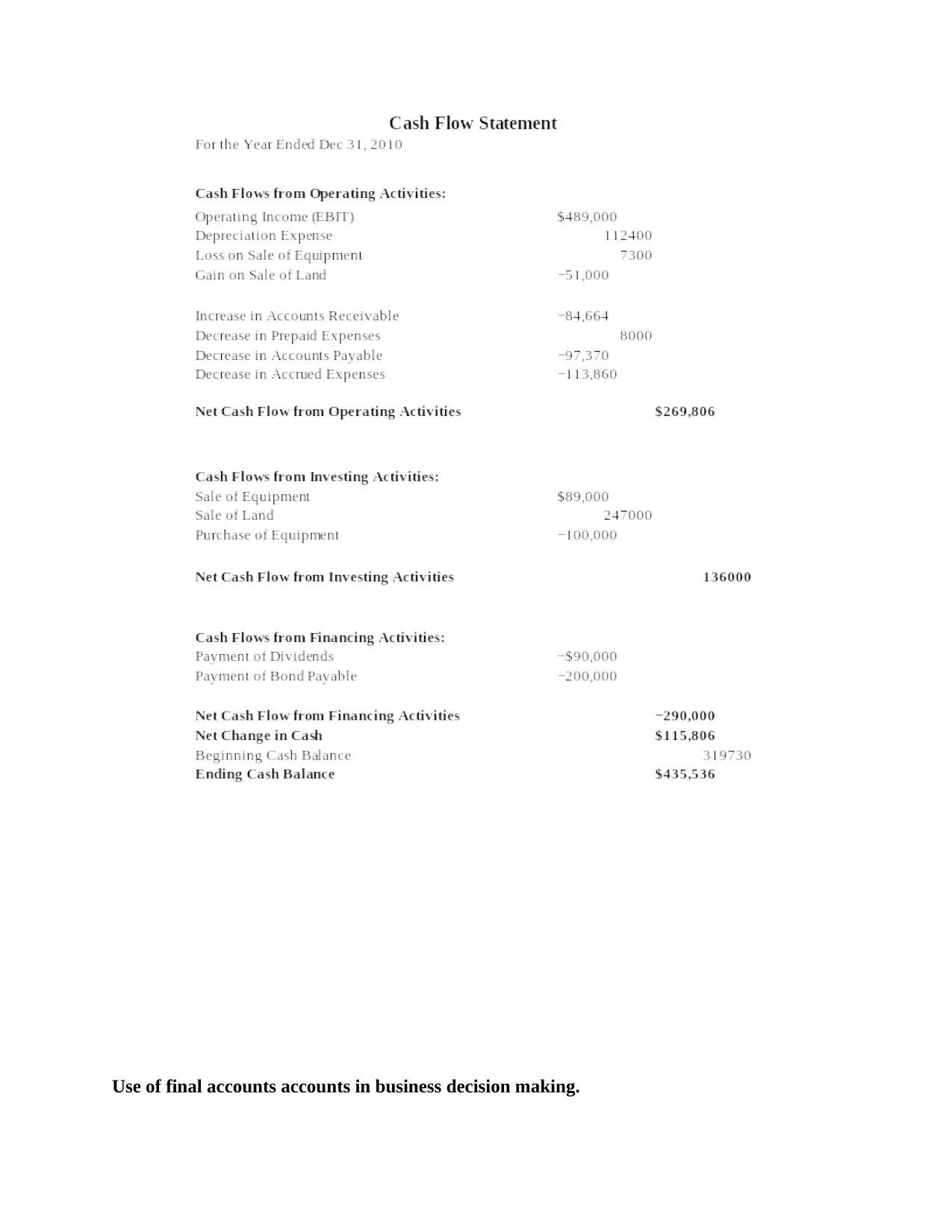

Structure and Content of Cash Flow Statement

Structure and Content of Cash Flow Statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Use of final accounts accounts in business decision making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income Statements – Income statements provides the management with the profitability form

carrying on business it also provide the information related to its revenues and expenses based on

which future strategies are framed.

Balance Sheet – Balance sheet of company informs the management about the position of the

company at year end. The changes in its assets and liabilities are assessed from balance sheet.

Make decisions comparing the statements with competitors (Vanauken, Ascigil and Carraher,

2017).

Cash Flow Statements – Cash Flows helps the management in identifying the inflows and

outflows of cash from different activities. This helps management in paying attention towards

productive activities.

2.3 Financial financial information and difference between sets of accounts.

Financial information obtained from the financial statements.

Income – It shows that company is having sufficient profits after carrying out all the expenses of

company. Efficiency of the company in managing its operations is judged by it.

COGS – It could be interpreted that company has managed to control its costs. Company is

having effective strategies to control its costs.

Gross profit – Company is having high gross profits, that means company is available with

sufficient profits to carry out further operations of business.

Stock holders equity – It shows that company has not issued any share capital in the given year.

Changes in equity have essential part in decision making.

Cash and equivalents – Company is having enough funds to carry its operations smoothly. It

will not be requiring to raise short term loans to meet its working capital requirements.

Difference between different sets of accounts.

Balance sheet Income Statement Fund Flows statements

Balance sheet

represents and records

the assets and liabilities

of company

Income Statements

reflects the income

generated and

expenditures incurred

in the business.

Fund flow statement

represent the inflow

and outflow of cash

from different activities

like operating,

financing and

investment (Berger,

carrying on business it also provide the information related to its revenues and expenses based on

which future strategies are framed.

Balance Sheet – Balance sheet of company informs the management about the position of the

company at year end. The changes in its assets and liabilities are assessed from balance sheet.

Make decisions comparing the statements with competitors (Vanauken, Ascigil and Carraher,

2017).

Cash Flow Statements – Cash Flows helps the management in identifying the inflows and

outflows of cash from different activities. This helps management in paying attention towards

productive activities.

2.3 Financial financial information and difference between sets of accounts.

Financial information obtained from the financial statements.

Income – It shows that company is having sufficient profits after carrying out all the expenses of

company. Efficiency of the company in managing its operations is judged by it.

COGS – It could be interpreted that company has managed to control its costs. Company is

having effective strategies to control its costs.

Gross profit – Company is having high gross profits, that means company is available with

sufficient profits to carry out further operations of business.

Stock holders equity – It shows that company has not issued any share capital in the given year.

Changes in equity have essential part in decision making.

Cash and equivalents – Company is having enough funds to carry its operations smoothly. It

will not be requiring to raise short term loans to meet its working capital requirements.

Difference between different sets of accounts.

Balance sheet Income Statement Fund Flows statements

Balance sheet

represents and records

the assets and liabilities

of company

Income Statements

reflects the income

generated and

expenditures incurred

in the business.

Fund flow statement

represent the inflow

and outflow of cash

from different activities

like operating,

financing and

investment (Berger,

Minnis and Sutherland,

2017).

2.4 Difference between decisions relating to revenue and capital expenditure.

Capital expenditure - Capital expenditures are generally related to fixed assets. These are

productive assets over the long term period. These expenditures involves high investment of

funds.

Revenue expenditure – Revenue expenditures are related to the particular revenue transaction

for operating period. They are the operational costs incurred for running the business.

Both have influence over the decisions taken by the business. It depends on the size and

the funds involved in the expenditures. Capital expenditures have major expenditures, therefore

company is required to have adequate information for coming at informed decisions. Revenue

expenditures of company are of routine in nature and managers do not pay much focus on

making decisions about them.

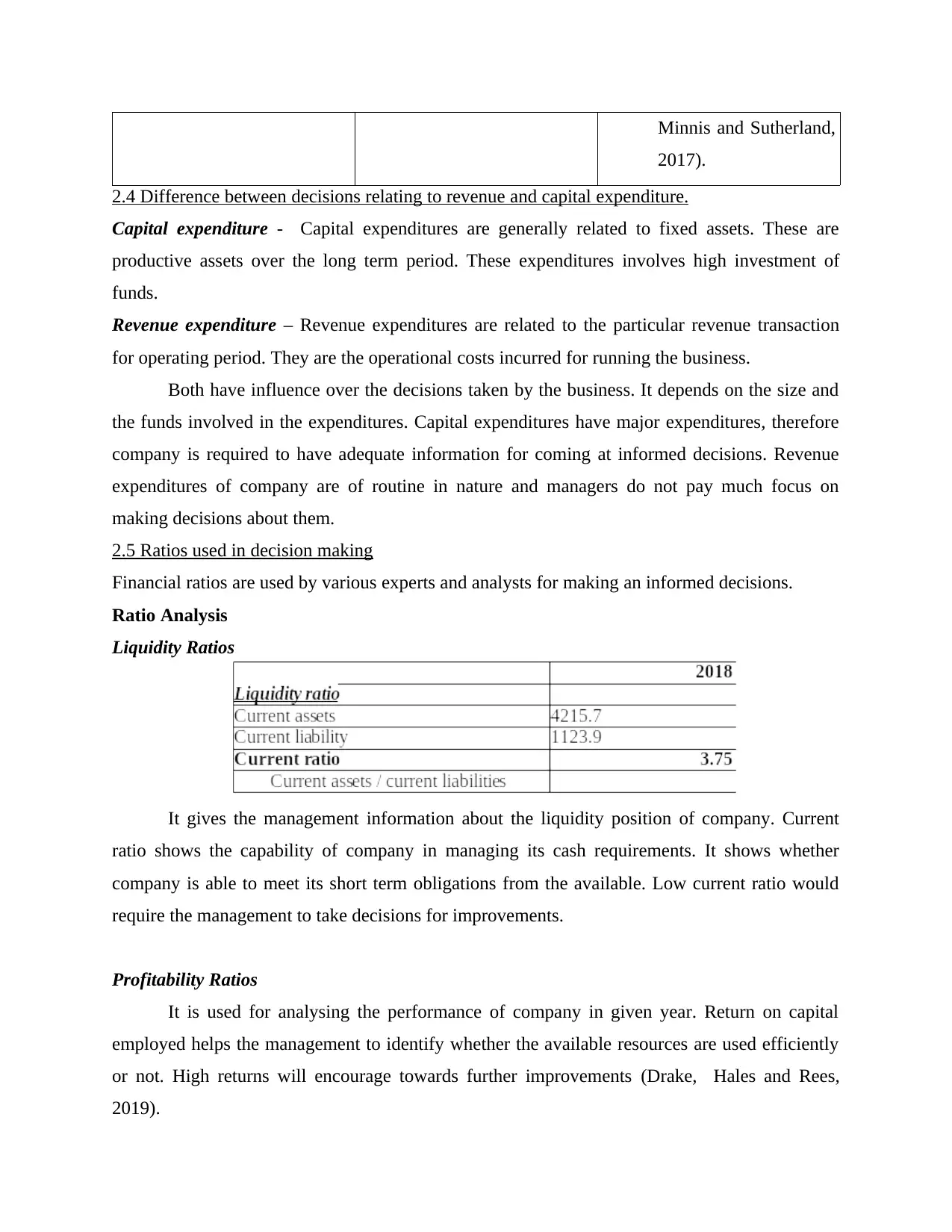

2.5 Ratios used in decision making

Financial ratios are used by various experts and analysts for making an informed decisions.

Ratio Analysis

Liquidity Ratios

It gives the management information about the liquidity position of company. Current

ratio shows the capability of company in managing its cash requirements. It shows whether

company is able to meet its short term obligations from the available. Low current ratio would

require the management to take decisions for improvements.

Profitability Ratios

It is used for analysing the performance of company in given year. Return on capital

employed helps the management to identify whether the available resources are used efficiently

or not. High returns will encourage towards further improvements (Drake, Hales and Rees,

2019).

2017).

2.4 Difference between decisions relating to revenue and capital expenditure.

Capital expenditure - Capital expenditures are generally related to fixed assets. These are

productive assets over the long term period. These expenditures involves high investment of

funds.

Revenue expenditure – Revenue expenditures are related to the particular revenue transaction

for operating period. They are the operational costs incurred for running the business.

Both have influence over the decisions taken by the business. It depends on the size and

the funds involved in the expenditures. Capital expenditures have major expenditures, therefore

company is required to have adequate information for coming at informed decisions. Revenue

expenditures of company are of routine in nature and managers do not pay much focus on

making decisions about them.

2.5 Ratios used in decision making

Financial ratios are used by various experts and analysts for making an informed decisions.

Ratio Analysis

Liquidity Ratios

It gives the management information about the liquidity position of company. Current

ratio shows the capability of company in managing its cash requirements. It shows whether

company is able to meet its short term obligations from the available. Low current ratio would

require the management to take decisions for improvements.

Profitability Ratios

It is used for analysing the performance of company in given year. Return on capital

employed helps the management to identify whether the available resources are used efficiently

or not. High returns will encourage towards further improvements (Drake, Hales and Rees,

2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.