Financial Management: Techniques, Strategies, and Analysis Report

VerifiedAdded on 2022/12/28

|16

|3760

|333

Report

AI Summary

This report delves into the core functions of management accounting and its benefits to organizations. It explores various techniques like trend analysis, margin analysis, and capital budgeting, highlighting their role in formulating effective financial decisions for enhanced profitability. The report outlines the principles guiding financial success, emphasizing shareholder wealth maximization. Furthermore, it examines the role of management accountants in financial control and fraud detection, offering recommendations to improve financial decision-making. Part 2 presents a detailed ratio analysis of Amcor PLC, assessing its liquidity and financial position. The report also discusses the significance of ratio analysis in operational and strategic decisions, comparing investment appraisal techniques and highlighting the roles of cash flow statements and break-even analysis in financial decision-making. Finally, it provides recommendations on utilizing management accounting techniques to enhance decision-making and ensure the long-term stability of the company.

UNIT-15 FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART-1............................................................................................................................................3

1. Techniques and approaches used by the management accountant..........................................3

2. Principles guiding effective financial strategies to maximize the wealth of shareholders and

their stakeholders.........................................................................................................................4

3. Evaluation the role and function of the management accountant in regard to financial

control and monitoring................................................................................................................5

4. Techniques and approaches for detection of fraud.................................................................6

5. Recommendations for improve financial decision making by management accountants.......7

PART 2............................................................................................................................................7

1. Ratio analysis of Amcor PLC..................................................................................................7

2. Role of ratio analysis in operational and strategic decisions...................................................9

3. Comparing the role of investment appraisal techniques in maximizing return on investment9

4. Role of cash flow statements and break even analysis in financial decision making............10

5. Recommendation on use of management accounting techniques to improve decision making

and ensure long term stability of company................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART-1............................................................................................................................................3

1. Techniques and approaches used by the management accountant..........................................3

2. Principles guiding effective financial strategies to maximize the wealth of shareholders and

their stakeholders.........................................................................................................................4

3. Evaluation the role and function of the management accountant in regard to financial

control and monitoring................................................................................................................5

4. Techniques and approaches for detection of fraud.................................................................6

5. Recommendations for improve financial decision making by management accountants.......7

PART 2............................................................................................................................................7

1. Ratio analysis of Amcor PLC..................................................................................................7

2. Role of ratio analysis in operational and strategic decisions...................................................9

3. Comparing the role of investment appraisal techniques in maximizing return on investment9

4. Role of cash flow statements and break even analysis in financial decision making............10

5. Recommendation on use of management accounting techniques to improve decision making

and ensure long term stability of company................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

This project shall be highlighting the functions of the management accountant and how they

benefit the organization. It shall be reflecting the various techniques like trend analysis, margin

analysis, capital budgeting which are used to formulate effective and efficient decisions for the

profitability of the company. It shall also disclose the principles that guide financial success of

the shareholders as are used by the management of the organization. It shall be showing the

major role-played in monitoring the operations and establishing due control such that frauds

could be easily detected. The recommendations which can be used to improve the financial

decision-making in the organization. The second part of the project shall be disclosing the ratios

for the Amcor plc. And on the basis of that shall determine the liquidity and the financial

position of the company.

PART-1

MA in an organization plays crucial role in the decision-making process. This decision-

making is facilitated by the usage of several techniques and approaches which help in budgeting

the level of activities that are to be undertaken in the future. On the basis of these predictions the

control and coordination is maintained in the organization with regard to the resource

availability, human resource management, profitability and future growth prospects.

1. Techniques and approaches used by the management accountant1. Trend analysis and forecasting- This is one of the most prominent techniques used by

the in the managerial accounting in which they study the past data, based on which

predict the future trends (Harelimana, 2017). Such forecasting is beneficial as it helps in

knowing the level of operations, associated costs, profitability and to assess the

requirements of the various resources.

Advantages

Helps in effective budgeting Optimum allocation of resources

Disadvantages

Market is uncertain Avoids flexibility of operations

This project shall be highlighting the functions of the management accountant and how they

benefit the organization. It shall be reflecting the various techniques like trend analysis, margin

analysis, capital budgeting which are used to formulate effective and efficient decisions for the

profitability of the company. It shall also disclose the principles that guide financial success of

the shareholders as are used by the management of the organization. It shall be showing the

major role-played in monitoring the operations and establishing due control such that frauds

could be easily detected. The recommendations which can be used to improve the financial

decision-making in the organization. The second part of the project shall be disclosing the ratios

for the Amcor plc. And on the basis of that shall determine the liquidity and the financial

position of the company.

PART-1

MA in an organization plays crucial role in the decision-making process. This decision-

making is facilitated by the usage of several techniques and approaches which help in budgeting

the level of activities that are to be undertaken in the future. On the basis of these predictions the

control and coordination is maintained in the organization with regard to the resource

availability, human resource management, profitability and future growth prospects.

1. Techniques and approaches used by the management accountant1. Trend analysis and forecasting- This is one of the most prominent techniques used by

the in the managerial accounting in which they study the past data, based on which

predict the future trends (Harelimana, 2017). Such forecasting is beneficial as it helps in

knowing the level of operations, associated costs, profitability and to assess the

requirements of the various resources.

Advantages

Helps in effective budgeting Optimum allocation of resources

Disadvantages

Market is uncertain Avoids flexibility of operations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Margin analysis- Another important technique used by the management of the company

to judge the optimal mix for the sales of the period. It helps in evaluating the break-even

point of the operations so that maximum benefit in terms of profit can be gained.

Advantages

At-least the cost are realized Assessing the optimum level of operations

Disadvantages

The breakeven shows the lower end and not the highest possible outcome. Actual results differ from the forecasted.3. Constraint analysis- This technique again proves to be beneficial in deciding the

bottlenecks of the company that are contributing to the various inefficiencies (Palepu and

et.al., 2020). Identifying such bottlenecks which can be in the form of process of

operations, product lines etc. can be rather beneficial as this can improve its profitability

and chances of growth.

Advantages

Avoiding inefficiencies Maximizing operational efficiency

Disadvantages

Certain bottlenecks are unavoidable Hampers the routine operations4. Capital budgeting- This is the approach that is used by the management accountant in

order to analyse and select the profitable long term capital expenditure decisions of the

company. Based on the net present value and the internal rate of return it can be decided

that whether a project should be accepted or rejected.

Advantages

Making the accept-reject decisions Derives long term profitability of the business.

Disadvantages

Complex procedure

Requires highly efficient staff

to judge the optimal mix for the sales of the period. It helps in evaluating the break-even

point of the operations so that maximum benefit in terms of profit can be gained.

Advantages

At-least the cost are realized Assessing the optimum level of operations

Disadvantages

The breakeven shows the lower end and not the highest possible outcome. Actual results differ from the forecasted.3. Constraint analysis- This technique again proves to be beneficial in deciding the

bottlenecks of the company that are contributing to the various inefficiencies (Palepu and

et.al., 2020). Identifying such bottlenecks which can be in the form of process of

operations, product lines etc. can be rather beneficial as this can improve its profitability

and chances of growth.

Advantages

Avoiding inefficiencies Maximizing operational efficiency

Disadvantages

Certain bottlenecks are unavoidable Hampers the routine operations4. Capital budgeting- This is the approach that is used by the management accountant in

order to analyse and select the profitable long term capital expenditure decisions of the

company. Based on the net present value and the internal rate of return it can be decided

that whether a project should be accepted or rejected.

Advantages

Making the accept-reject decisions Derives long term profitability of the business.

Disadvantages

Complex procedure

Requires highly efficient staff

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Principles guiding effective financial strategies to maximize the wealth of shareholders and

their stakeholders

Management accounting process plays a key role in developing effective financial strategies that

determine the maximization of the wealth and stability of the various stakeholders of the

company. There are certain essential principles that guide the success of the stakeholders which

can be namely:-

In order to generate better returns to the shareholders of the company the management

tries to maximize their earnings per share, better distribution of the dividends, bonus

issue etc. this contributes to the wealth management of the shareholders.

The financial strategies like expansions, mergers and collaborative alliances can be a

contributing factor to the maximization of wealth of the shareholders (Edmonds, Smith

and Stallings, 2018). As the growth prospects of the company will at one end lead to

higher profitability leading to higher EPS and on the other hand shall be contributing to

the increase in the value of shares.

The cost-cutting measures taken by the management like the application of the 4R's will

reduce the cost as well as satisfy the social responsibilities of the organization. The

reduced cost shall contribute to the profitability maximizing the wealth of shareholders

and fulfilment of the social responsibility shall lead to satisfaction for the other

stakeholders who are part of the society.

By the constraint analysis they identify the inefficient areas and discontinue the

operations which are contributing to the costs but are not providing with the simultaneous

profits (Kutsenko, 2019). This derives better gains for the stakeholders of the company.

The capital budgeting decisions are also important financial strategies that optimize the

operations of the company further maximizing the value for the money of the customers.

These can be some financial strategies as implemented by the management in order to ensure

maximum benefit to the various stakeholders of the company ultimately boosting their

satisfaction level which retains them with the company.

On the critical note it can be examined that if the principles are not adopted which helps

in maximizing the financial efficiency, then the expectations of the stakeholders won't be met

and this shall decrease their satisfaction as well as the loyalty with the company. Also, certain

their stakeholders

Management accounting process plays a key role in developing effective financial strategies that

determine the maximization of the wealth and stability of the various stakeholders of the

company. There are certain essential principles that guide the success of the stakeholders which

can be namely:-

In order to generate better returns to the shareholders of the company the management

tries to maximize their earnings per share, better distribution of the dividends, bonus

issue etc. this contributes to the wealth management of the shareholders.

The financial strategies like expansions, mergers and collaborative alliances can be a

contributing factor to the maximization of wealth of the shareholders (Edmonds, Smith

and Stallings, 2018). As the growth prospects of the company will at one end lead to

higher profitability leading to higher EPS and on the other hand shall be contributing to

the increase in the value of shares.

The cost-cutting measures taken by the management like the application of the 4R's will

reduce the cost as well as satisfy the social responsibilities of the organization. The

reduced cost shall contribute to the profitability maximizing the wealth of shareholders

and fulfilment of the social responsibility shall lead to satisfaction for the other

stakeholders who are part of the society.

By the constraint analysis they identify the inefficient areas and discontinue the

operations which are contributing to the costs but are not providing with the simultaneous

profits (Kutsenko, 2019). This derives better gains for the stakeholders of the company.

The capital budgeting decisions are also important financial strategies that optimize the

operations of the company further maximizing the value for the money of the customers.

These can be some financial strategies as implemented by the management in order to ensure

maximum benefit to the various stakeholders of the company ultimately boosting their

satisfaction level which retains them with the company.

On the critical note it can be examined that if the principles are not adopted which helps

in maximizing the financial efficiency, then the expectations of the stakeholders won't be met

and this shall decrease their satisfaction as well as the loyalty with the company. Also, certain

decisions involve huge sums and long term success of the company which should be wisely

undertaken and if not then will cause loss to the company and affect its market position.

3. Evaluation the role and function of the management accountant in regard to financial control

and monitoring

Roles and functions of the management accountant

management accountant plays a crucial role in performing day to day functions of

managerial level in the organizations. They play a significant role in collecting, compiling,

reporting and analysing accounting information to its actual users. There are many functions and

role perform by them which are as follows:

1. Planning of accounting functions: Planning is all about what to do, how to do and for

whom to do. The management accountant looks into the various aspects of cost which

results into carrying out effective planning in order to meet with the financial

requirements of the business, budgeting and attaining the cost standards set.

2. Organising: After making a proper plan of the targets, they establish an organisational

structure and delegating the responsibility to the staff within the firm for the purpose of

achieving the desired goals and objectives. In order to carry out this process effectively,

different segments and branches can be created.

3. Ascertain Optimum capital structure: MA works on ensuring that the funds which are

acquired are utilized effectively and needs to ensure that proper balance is being

maintained between debt and equity. The MA identifies the right source of fund which

can be utilized for the business needs along with ensuring the improvized financial

performance of the company.

4. Controlling: It is the another function of MA pertaining to monitoring, measuring,

analysing, and correcting actual results to ensure about the organisational targets are

achieved or not. It supports in control functions by producing performance and variances

reports which mainly highlights the deviations between actual and budgeted

performance.

5. Decision -making: In each, three management functions stated above decision making is

required the most a manager take decisions from choosing among different alternatives.

MA provides relevant information to the top management which assists them in taking

important business decisions. It involves the aspects like product pricing, investment

undertaken and if not then will cause loss to the company and affect its market position.

3. Evaluation the role and function of the management accountant in regard to financial control

and monitoring

Roles and functions of the management accountant

management accountant plays a crucial role in performing day to day functions of

managerial level in the organizations. They play a significant role in collecting, compiling,

reporting and analysing accounting information to its actual users. There are many functions and

role perform by them which are as follows:

1. Planning of accounting functions: Planning is all about what to do, how to do and for

whom to do. The management accountant looks into the various aspects of cost which

results into carrying out effective planning in order to meet with the financial

requirements of the business, budgeting and attaining the cost standards set.

2. Organising: After making a proper plan of the targets, they establish an organisational

structure and delegating the responsibility to the staff within the firm for the purpose of

achieving the desired goals and objectives. In order to carry out this process effectively,

different segments and branches can be created.

3. Ascertain Optimum capital structure: MA works on ensuring that the funds which are

acquired are utilized effectively and needs to ensure that proper balance is being

maintained between debt and equity. The MA identifies the right source of fund which

can be utilized for the business needs along with ensuring the improvized financial

performance of the company.

4. Controlling: It is the another function of MA pertaining to monitoring, measuring,

analysing, and correcting actual results to ensure about the organisational targets are

achieved or not. It supports in control functions by producing performance and variances

reports which mainly highlights the deviations between actual and budgeted

performance.

5. Decision -making: In each, three management functions stated above decision making is

required the most a manager take decisions from choosing among different alternatives.

MA provides relevant information to the top management which assists them in taking

important business decisions. It involves the aspects like product pricing, investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

appraisal, product mix and so forth.

4. Tools and approaches for detection of fraud

Financial frauds can be referred as the international use of unauthorized methods or

practices for the purpose of obtaining financial gain. Some common techniques of detection of

frauds are as follows:

Strict internal control system: Mismanagement of cash is the easiest way of fraud held

in organisation where there is none linkage in between management and cashier. For

avoiding this type of frauds accountant should have followed stricter internal control

system in receipts and payments of cash so that after completion of work by single person

is check by another person at the same time.

Reconciliation of physical stock: Sometimes stock may be stolen by employees or

through the way of issuance of the false credit notes to customers in respect to the goods

returned (Riwayati, 2017). Identification of misapplication of goods is more complex

where management is not sound and appropriate system of security is not available. In

respect implementing control over the physical review and monitoring of the goods with

respect to the books along with the sales invoices on the continuous basis.

Internal Auditing in accounts: Manipulation of accounts are mainly done by senior

management to mislead the accounts for some specific objective. Sometimes

management misrepresent finance data in such a way that it seems better than what it

actually is. To keep control on manipulation of accounts internal auditing of accounts on

regular basis is necessary. Internal auditor keep check everything in at the time of

auditing and prepare an official report of financial statements. So this report will help in

detection of frauds and errors by management.

Approaches to Ethical Decision Making

Utilitarian Approach: As per this approach the moral actions are those that provide the greatest

balance of good over bad.

Right Approach: This approach ensures that individual have the capacity to make their

decisions freely (Chan and Abdul-Aziz, 2017).

Justice in Approach: This approach allows that opportunity to person which reflects if the

actions is fair to the people.

4. Tools and approaches for detection of fraud

Financial frauds can be referred as the international use of unauthorized methods or

practices for the purpose of obtaining financial gain. Some common techniques of detection of

frauds are as follows:

Strict internal control system: Mismanagement of cash is the easiest way of fraud held

in organisation where there is none linkage in between management and cashier. For

avoiding this type of frauds accountant should have followed stricter internal control

system in receipts and payments of cash so that after completion of work by single person

is check by another person at the same time.

Reconciliation of physical stock: Sometimes stock may be stolen by employees or

through the way of issuance of the false credit notes to customers in respect to the goods

returned (Riwayati, 2017). Identification of misapplication of goods is more complex

where management is not sound and appropriate system of security is not available. In

respect implementing control over the physical review and monitoring of the goods with

respect to the books along with the sales invoices on the continuous basis.

Internal Auditing in accounts: Manipulation of accounts are mainly done by senior

management to mislead the accounts for some specific objective. Sometimes

management misrepresent finance data in such a way that it seems better than what it

actually is. To keep control on manipulation of accounts internal auditing of accounts on

regular basis is necessary. Internal auditor keep check everything in at the time of

auditing and prepare an official report of financial statements. So this report will help in

detection of frauds and errors by management.

Approaches to Ethical Decision Making

Utilitarian Approach: As per this approach the moral actions are those that provide the greatest

balance of good over bad.

Right Approach: This approach ensures that individual have the capacity to make their

decisions freely (Chan and Abdul-Aziz, 2017).

Justice in Approach: This approach allows that opportunity to person which reflects if the

actions is fair to the people.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Common Good Approach: This will help in identifying the actions taken by ourselves is good

for society or not.

Virtue Approach: This approach shows on what kind of person you should be and what it will

do to your character.

5. Recommendations for improve financial decision making by management accountants

management accountant has the ability to turn qualitative information into quantitative

reports. It uses information from operations to produce reports that provide deep in-depth

knowledge into business performance, such as profit margins. management accounting helps the

accountant in improving financial decision making by providing proper financial statements

through which companies plan, forecast and budget an enterprise level to ensure about long term

success of the company. It is used internally to make efficiency improvement within the

company.

PART 2

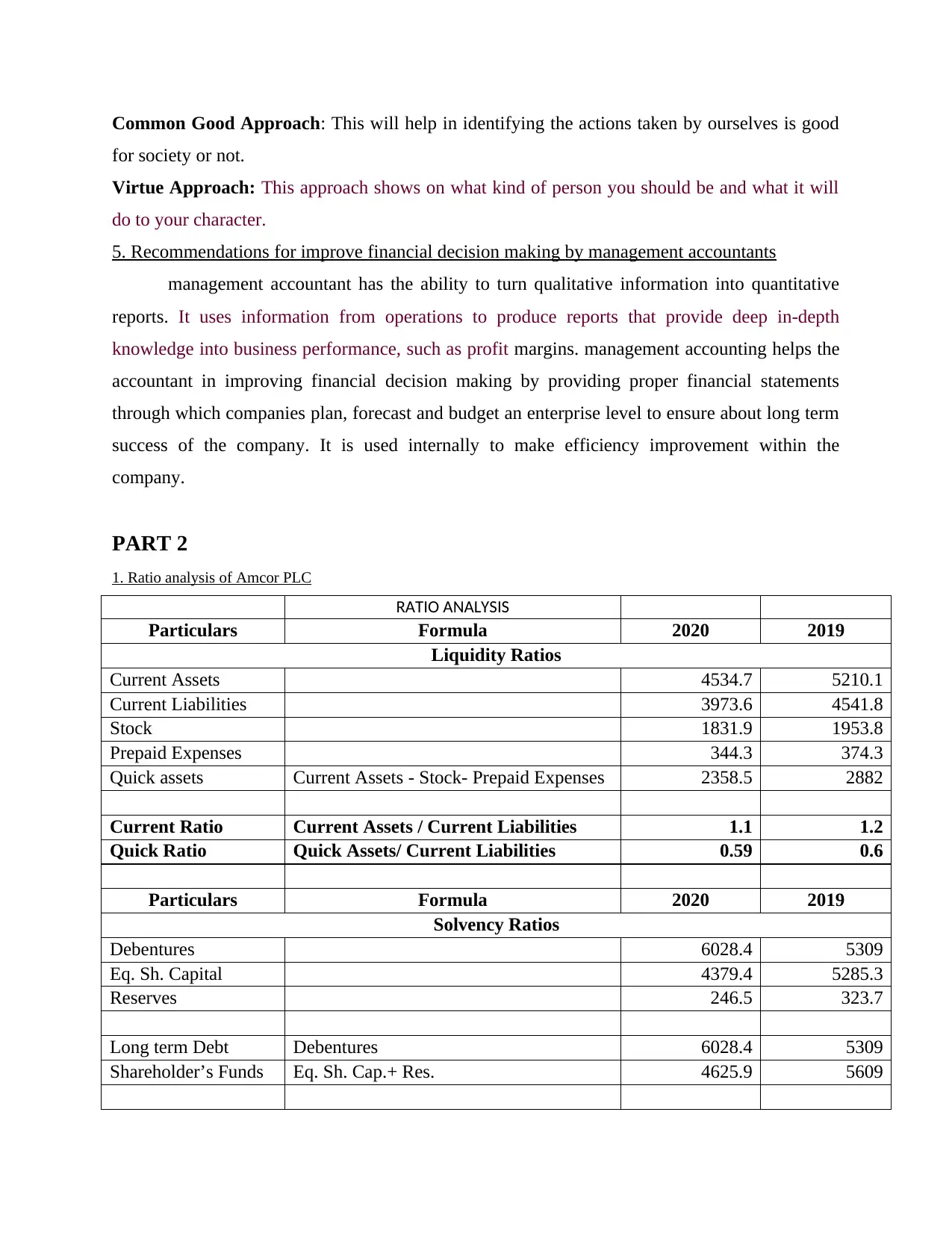

1. Ratio analysis of Amcor PLC

RATIO ANALYSIS

Particulars Formula 2020 2019

Liquidity Ratios

Current Assets 4534.7 5210.1

Current Liabilities 3973.6 4541.8

Stock 1831.9 1953.8

Prepaid Expenses 344.3 374.3

Quick assets Current Assets - Stock- Prepaid Expenses 2358.5 2882

Current Ratio Current Assets / Current Liabilities 1.1 1.2

Quick Ratio Quick Assets/ Current Liabilities 0.59 0.6

Particulars Formula 2020 2019

Solvency Ratios

Debentures 6028.4 5309

Eq. Sh. Capital 4379.4 5285.3

Reserves 246.5 323.7

Long term Debt Debentures 6028.4 5309

Shareholder’s Funds Eq. Sh. Cap.+ Res. 4625.9 5609

for society or not.

Virtue Approach: This approach shows on what kind of person you should be and what it will

do to your character.

5. Recommendations for improve financial decision making by management accountants

management accountant has the ability to turn qualitative information into quantitative

reports. It uses information from operations to produce reports that provide deep in-depth

knowledge into business performance, such as profit margins. management accounting helps the

accountant in improving financial decision making by providing proper financial statements

through which companies plan, forecast and budget an enterprise level to ensure about long term

success of the company. It is used internally to make efficiency improvement within the

company.

PART 2

1. Ratio analysis of Amcor PLC

RATIO ANALYSIS

Particulars Formula 2020 2019

Liquidity Ratios

Current Assets 4534.7 5210.1

Current Liabilities 3973.6 4541.8

Stock 1831.9 1953.8

Prepaid Expenses 344.3 374.3

Quick assets Current Assets - Stock- Prepaid Expenses 2358.5 2882

Current Ratio Current Assets / Current Liabilities 1.1 1.2

Quick Ratio Quick Assets/ Current Liabilities 0.59 0.6

Particulars Formula 2020 2019

Solvency Ratios

Debentures 6028.4 5309

Eq. Sh. Capital 4379.4 5285.3

Reserves 246.5 323.7

Long term Debt Debentures 6028.4 5309

Shareholder’s Funds Eq. Sh. Cap.+ Res. 4625.9 5609

Debt Equity Ratio Long term Debt/ Shareholders Funds 1.3 1.0

Particulars Formula 2020 2019

Profitability Ratio

Gross Profit 2535.5 1799.1

Operating Profit 994 791.7

Net Profit/ Income 638.3 432.6

Net Sales 12467.5 9458.2

Total Assets 16442.1 17165

Current Liabilities 3973.6 4541.8

Equity at beginning 5609 626.6

Equity at end 4625.9 5609

Average Sh. Equity (Equity at beginning + equity at end)/ 2 5117.45 3117.8

EBIT 1009.9 795.2

Capital Employed Total Assets - Current Liabilities 12468.5 12623.2

Gross Profit Ratio Gross Profit/ Net Sales 20% 19%

Net profit Ratio Net Profit/ Net Sales 5% 5%

Operating Profit

Ratio

Operating Profit/ Net Sales 8% 8%

Return on

Investment

Net Profit/ Total Assets 4% 3%

Return on Equity Net Profit/ Average Shareholder Equity 12% 14%

Return on Capital

Employed

EBIT/ Capital Employed 8% 6%

Particulars Formula 2020 2019

Efficiency Ratio

COGS 9932 7659.1

Average Inventory (Opening + Closing Inventory)/ 2 1892.85 1656.3

Average Total Assets (Opening + Closing Total Assets)/ 2 16803.55 13111.25

Net Sales 12467.5 9458.2

Inventory Turnover

Ratio

COGS/ Average Inventory 5.3 4.6

Asset Turnover

Ratio

Net Sales/ Average Total Assets 0.7 0.7

Particulars Formula 2020 2019

Earnings Ratio

Earnings for Equity

shareholders

612.2 430.2

Particulars Formula 2020 2019

Profitability Ratio

Gross Profit 2535.5 1799.1

Operating Profit 994 791.7

Net Profit/ Income 638.3 432.6

Net Sales 12467.5 9458.2

Total Assets 16442.1 17165

Current Liabilities 3973.6 4541.8

Equity at beginning 5609 626.6

Equity at end 4625.9 5609

Average Sh. Equity (Equity at beginning + equity at end)/ 2 5117.45 3117.8

EBIT 1009.9 795.2

Capital Employed Total Assets - Current Liabilities 12468.5 12623.2

Gross Profit Ratio Gross Profit/ Net Sales 20% 19%

Net profit Ratio Net Profit/ Net Sales 5% 5%

Operating Profit

Ratio

Operating Profit/ Net Sales 8% 8%

Return on

Investment

Net Profit/ Total Assets 4% 3%

Return on Equity Net Profit/ Average Shareholder Equity 12% 14%

Return on Capital

Employed

EBIT/ Capital Employed 8% 6%

Particulars Formula 2020 2019

Efficiency Ratio

COGS 9932 7659.1

Average Inventory (Opening + Closing Inventory)/ 2 1892.85 1656.3

Average Total Assets (Opening + Closing Total Assets)/ 2 16803.55 13111.25

Net Sales 12467.5 9458.2

Inventory Turnover

Ratio

COGS/ Average Inventory 5.3 4.6

Asset Turnover

Ratio

Net Sales/ Average Total Assets 0.7 0.7

Particulars Formula 2020 2019

Earnings Ratio

Earnings for Equity

shareholders

612.2 430.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

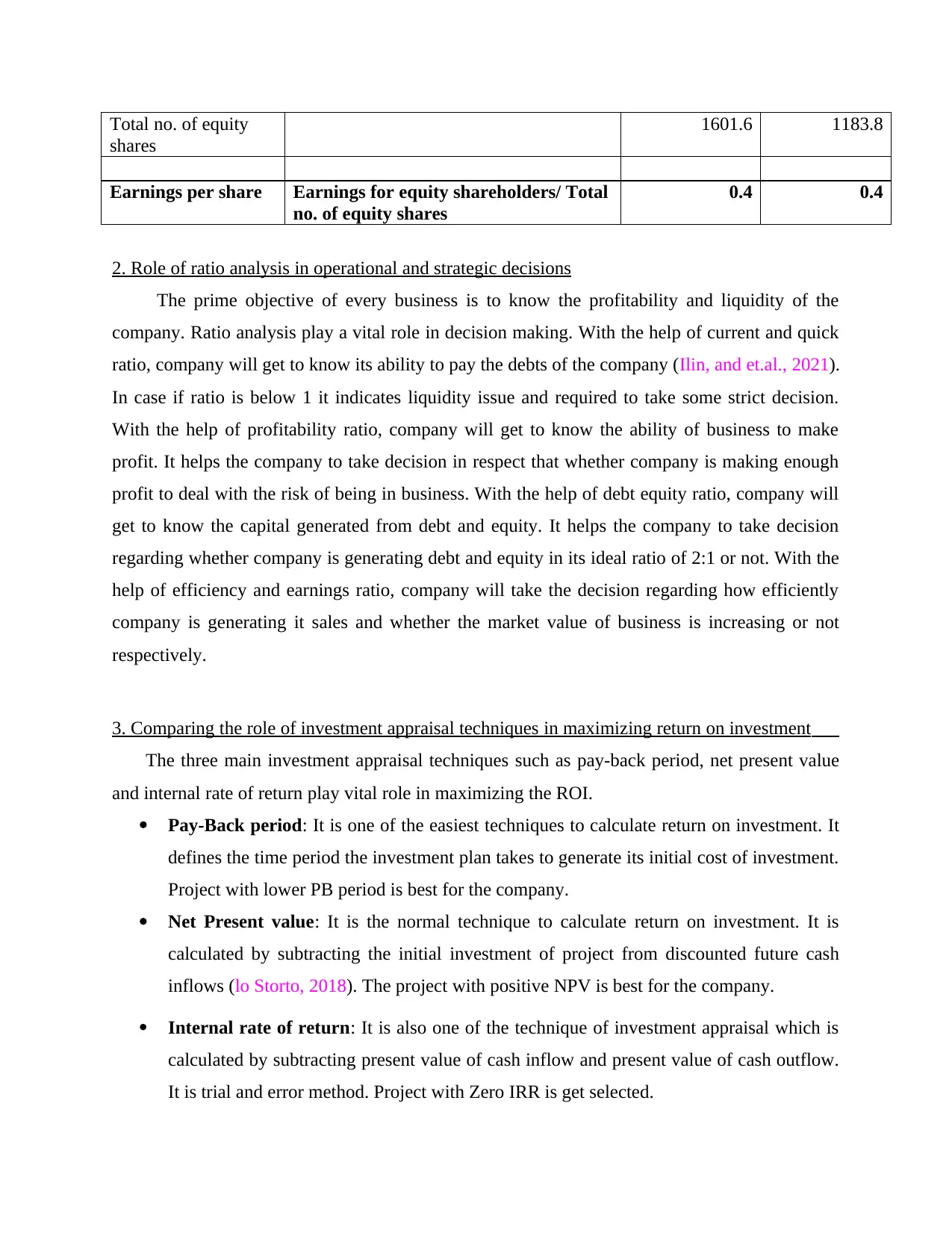

Total no. of equity

shares

1601.6 1183.8

Earnings per share Earnings for equity shareholders/ Total

no. of equity shares

0.4 0.4

2. Role of ratio analysis in operational and strategic decisions

The prime objective of every business is to know the profitability and liquidity of the

company. Ratio analysis play a vital role in decision making. With the help of current and quick

ratio, company will get to know its ability to pay the debts of the company (Ilin, and et.al., 2021).

In case if ratio is below 1 it indicates liquidity issue and required to take some strict decision.

With the help of profitability ratio, company will get to know the ability of business to make

profit. It helps the company to take decision in respect that whether company is making enough

profit to deal with the risk of being in business. With the help of debt equity ratio, company will

get to know the capital generated from debt and equity. It helps the company to take decision

regarding whether company is generating debt and equity in its ideal ratio of 2:1 or not. With the

help of efficiency and earnings ratio, company will take the decision regarding how efficiently

company is generating it sales and whether the market value of business is increasing or not

respectively.

3. Comparing the role of investment appraisal techniques in maximizing return on investment

The three main investment appraisal techniques such as pay-back period, net present value

and internal rate of return play vital role in maximizing the ROI.

Pay-Back period: It is one of the easiest techniques to calculate return on investment. It

defines the time period the investment plan takes to generate its initial cost of investment.

Project with lower PB period is best for the company.

Net Present value: It is the normal technique to calculate return on investment. It is

calculated by subtracting the initial investment of project from discounted future cash

inflows (lo Storto, 2018). The project with positive NPV is best for the company.

Internal rate of return: It is also one of the technique of investment appraisal which is

calculated by subtracting present value of cash inflow and present value of cash outflow.

It is trial and error method. Project with Zero IRR is get selected.

shares

1601.6 1183.8

Earnings per share Earnings for equity shareholders/ Total

no. of equity shares

0.4 0.4

2. Role of ratio analysis in operational and strategic decisions

The prime objective of every business is to know the profitability and liquidity of the

company. Ratio analysis play a vital role in decision making. With the help of current and quick

ratio, company will get to know its ability to pay the debts of the company (Ilin, and et.al., 2021).

In case if ratio is below 1 it indicates liquidity issue and required to take some strict decision.

With the help of profitability ratio, company will get to know the ability of business to make

profit. It helps the company to take decision in respect that whether company is making enough

profit to deal with the risk of being in business. With the help of debt equity ratio, company will

get to know the capital generated from debt and equity. It helps the company to take decision

regarding whether company is generating debt and equity in its ideal ratio of 2:1 or not. With the

help of efficiency and earnings ratio, company will take the decision regarding how efficiently

company is generating it sales and whether the market value of business is increasing or not

respectively.

3. Comparing the role of investment appraisal techniques in maximizing return on investment

The three main investment appraisal techniques such as pay-back period, net present value

and internal rate of return play vital role in maximizing the ROI.

Pay-Back period: It is one of the easiest techniques to calculate return on investment. It

defines the time period the investment plan takes to generate its initial cost of investment.

Project with lower PB period is best for the company.

Net Present value: It is the normal technique to calculate return on investment. It is

calculated by subtracting the initial investment of project from discounted future cash

inflows (lo Storto, 2018). The project with positive NPV is best for the company.

Internal rate of return: It is also one of the technique of investment appraisal which is

calculated by subtracting present value of cash inflow and present value of cash outflow.

It is trial and error method. Project with Zero IRR is get selected.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Role of cash flow statements and break even analysis in financial decision making

Role of cash flow statement: Role of cash flow statement is important because it involve only

cash income and expenses while income statement involve both cash and noncash income

and expenses (Lin, Chang and Fang, 2020). It shows all cash income and expenses on the

basis of operating, investing and financing criteria. It helps the manager of the company to

know the cash profit and loss of the business.

Role of break-even analysis: Role of break-even analysis is to help the mangers to know

the point at which company neither earn profit nor incurred losses. It helps them to take

appropriate decision or plan a strategy to increase the sales revenue and reduce cost in

order to achieve the objectives of the business.

5. Recommendation on use of management accounting techniques to improve decision making

and ensure long term stability of company.

With the help of cost analysis, manager will examine the cost of the product by distributing

it into fixed and variable, normal and abnormal. It helps them to take decision regarding whether

to add product line or to shut down the operation. With the help of management accounting

techniques, manager will analyse and take decision regarding whether to make components of

the product in house or buy it from the suppliers (Kamar 2017). It also helps the company to stop

suppliers to take monopoly and bargaining power advantages. By utilizing the data provided by

the financial statement of the company, managers can take proper decisions such as financing

decision, investment decision and dividend decision.

CONCLUSION

Management accounting is important in order to take and improve the financial decision

making. This report concludes the techniques and principle of the management accounting with

the role and function of management accountant. Through this report, we also understand the

role of ratio analysis, cash flow statement, break even analysis and management accounting

techniques on decision making. This report also includes the financial ratio of Amcor plc. This

report also states the techniques and approaches to detection of fraud.

Role of cash flow statement: Role of cash flow statement is important because it involve only

cash income and expenses while income statement involve both cash and noncash income

and expenses (Lin, Chang and Fang, 2020). It shows all cash income and expenses on the

basis of operating, investing and financing criteria. It helps the manager of the company to

know the cash profit and loss of the business.

Role of break-even analysis: Role of break-even analysis is to help the mangers to know

the point at which company neither earn profit nor incurred losses. It helps them to take

appropriate decision or plan a strategy to increase the sales revenue and reduce cost in

order to achieve the objectives of the business.

5. Recommendation on use of management accounting techniques to improve decision making

and ensure long term stability of company.

With the help of cost analysis, manager will examine the cost of the product by distributing

it into fixed and variable, normal and abnormal. It helps them to take decision regarding whether

to add product line or to shut down the operation. With the help of management accounting

techniques, manager will analyse and take decision regarding whether to make components of

the product in house or buy it from the suppliers (Kamar 2017). It also helps the company to stop

suppliers to take monopoly and bargaining power advantages. By utilizing the data provided by

the financial statement of the company, managers can take proper decisions such as financing

decision, investment decision and dividend decision.

CONCLUSION

Management accounting is important in order to take and improve the financial decision

making. This report concludes the techniques and principle of the management accounting with

the role and function of management accountant. Through this report, we also understand the

role of ratio analysis, cash flow statement, break even analysis and management accounting

techniques on decision making. This report also includes the financial ratio of Amcor plc. This

report also states the techniques and approaches to detection of fraud.

REFERENCES

Books and journals

Harelimana, J. B., 2017. The role of risk management on financial performance of banking

institutions in Rwanda. Global Journal of Management and Business Research.

Palepu, K. G., and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Edmonds, M. A., Smith, D. B. and Stallings, M. A., 2018. Financial statement comparability and

segment disclosure. Research in Accounting Regulation. 30(2). pp.103-111.

Kutsenko, D., 2019. Orienters of strategic management of financial and economic security of

enterprises: interests, challenges, risks. Bulletin of the Cherkasy Bohdan Khmelnytsky

National University. Economic Sciences, (2).

Chan, T. K. and Abdul-Aziz, A. R., 2017. Financial performance and operating strategies of

Malaysian property development companies during the global financial crisis. Journal

of Financial Management of Property and Construction.

Riwayati, H. E., 2017. Financial Inclusion of business players in mediating the success of small

and medium enterprises in Indonesia. International Journal of Economics and

Financial Issues, 7(4).

Kamar, K., 2017. Analysis of the effect of return on equity (ROE) and debt to equity ratio (DER)

on stock price on cement industry listed in Indonesia stock exchange (IDX) in the year

of 2011-2015. IOSR Journal of Business and Management, 19(05), pp.66-76.

Lin, X., Chang, C. L. and Fang, M., 2020. Investment-Cash Flow Sensitivity and Companies’

Financial Conditions. Design Engineering, pp.883-889.

lo Storto, C., 2018. A double-DEA framework to support decision-making in the choice of

advanced manufacturing technologies. Management Decision.

Ilin, I. V. and et.al., 2021. Investment Models for Enterprise Architecture (EA) and IT

Architecture Projects within the Open Innovation Concept. Journal of Open

Innovation: Technology, Market, and Complexity, 7(1), p.69.

1

Books and journals

Harelimana, J. B., 2017. The role of risk management on financial performance of banking

institutions in Rwanda. Global Journal of Management and Business Research.

Palepu, K. G., and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Edmonds, M. A., Smith, D. B. and Stallings, M. A., 2018. Financial statement comparability and

segment disclosure. Research in Accounting Regulation. 30(2). pp.103-111.

Kutsenko, D., 2019. Orienters of strategic management of financial and economic security of

enterprises: interests, challenges, risks. Bulletin of the Cherkasy Bohdan Khmelnytsky

National University. Economic Sciences, (2).

Chan, T. K. and Abdul-Aziz, A. R., 2017. Financial performance and operating strategies of

Malaysian property development companies during the global financial crisis. Journal

of Financial Management of Property and Construction.

Riwayati, H. E., 2017. Financial Inclusion of business players in mediating the success of small

and medium enterprises in Indonesia. International Journal of Economics and

Financial Issues, 7(4).

Kamar, K., 2017. Analysis of the effect of return on equity (ROE) and debt to equity ratio (DER)

on stock price on cement industry listed in Indonesia stock exchange (IDX) in the year

of 2011-2015. IOSR Journal of Business and Management, 19(05), pp.66-76.

Lin, X., Chang, C. L. and Fang, M., 2020. Investment-Cash Flow Sensitivity and Companies’

Financial Conditions. Design Engineering, pp.883-889.

lo Storto, C., 2018. A double-DEA framework to support decision-making in the choice of

advanced manufacturing technologies. Management Decision.

Ilin, I. V. and et.al., 2021. Investment Models for Enterprise Architecture (EA) and IT

Architecture Projects within the Open Innovation Concept. Journal of Open

Innovation: Technology, Market, and Complexity, 7(1), p.69.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.