Financial Decision Making Analysis: Morrisons and ALPHA Ltd Report

VerifiedAdded on 2023/01/11

|14

|4055

|20

Report

AI Summary

This report presents a comprehensive analysis of financial decision-making within organizations, using Morrisons and ALPHA Ltd as case studies. Task 1 delves into the significance of accounting and finance departments, outlining their roles and importance. It covers financial accounting, management accounting, tax and auditing functions within the accounting department and investment, financing, dividend, and working capital functions within the finance department. Task 2 focuses on the financial performance of ALPHA Ltd through ratio analysis, assessing profitability, liquidity, efficiency, and solvency. The report interprets key financial ratios, including Return on Capital Employed (ROCE) and Net Profit Margin, highlighting trends and implications for investors. The analysis reveals a decline in ALPHA Ltd.'s financial performance, recommending against immediate investment until improvements are made. The report underscores the critical role of financial management in business success, providing insights into the practical application of financial principles.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report presented is about the financial decision making in an organization. In this

Morrisons is taken as an organization. The report is divided into two parts, that is, task 1 and

task 2. Task 1 presents about the meaning and importance of accounting and financing

department in Morrisons. It also covers the various role of each of these department in

context to Morrisons. These roles are critically evaluated with the objective to know its

significance. The task 2 states about the financial position and performance of ALPHA Ltd

by analysing its financial ratios. These ratios were in respect to its profitability, liquidity,

efficiency and solvency. Based on the finding, it is concluded that the investors should not

invest in the company as of now, until its performance is improved.

The report presented is about the financial decision making in an organization. In this

Morrisons is taken as an organization. The report is divided into two parts, that is, task 1 and

task 2. Task 1 presents about the meaning and importance of accounting and financing

department in Morrisons. It also covers the various role of each of these department in

context to Morrisons. These roles are critically evaluated with the objective to know its

significance. The task 2 states about the financial position and performance of ALPHA Ltd

by analysing its financial ratios. These ratios were in respect to its profitability, liquidity,

efficiency and solvency. Based on the finding, it is concluded that the investors should not

invest in the company as of now, until its performance is improved.

TABLE OF CONTENTS

Task 1.........................................................................................................................................4

INTRODUCTION......................................................................................................................4

ACCOUNTING AND FINANCE DEPARTMENT.................................................................4

IMPORTANCE OF ACCOUNTING AND FINANCE DEPARTMENT................................4

ROLE OF ACCOUNTS DEPARTMENT.................................................................................5

Financial accounting..............................................................................................................5

Management accounting........................................................................................................5

Tax function...........................................................................................................................6

Auditing function...................................................................................................................6

ROLE OF FINANCE DEPARTMENT.....................................................................................6

Investment function................................................................................................................6

Financing function.................................................................................................................6

Dividend function...................................................................................................................7

Working capital function........................................................................................................7

TASK 2......................................................................................................................................7

Ratio analysis.........................................................................................................................7

Interpretation and analysis.....................................................................................................9

REFERENCES.........................................................................................................................13

Task 1.........................................................................................................................................4

INTRODUCTION......................................................................................................................4

ACCOUNTING AND FINANCE DEPARTMENT.................................................................4

IMPORTANCE OF ACCOUNTING AND FINANCE DEPARTMENT................................4

ROLE OF ACCOUNTS DEPARTMENT.................................................................................5

Financial accounting..............................................................................................................5

Management accounting........................................................................................................5

Tax function...........................................................................................................................6

Auditing function...................................................................................................................6

ROLE OF FINANCE DEPARTMENT.....................................................................................6

Investment function................................................................................................................6

Financing function.................................................................................................................6

Dividend function...................................................................................................................7

Working capital function........................................................................................................7

TASK 2......................................................................................................................................7

Ratio analysis.........................................................................................................................7

Interpretation and analysis.....................................................................................................9

REFERENCES.........................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

INTRODUCTION

Financial decision making is the process of taking relevant steps and decision with

respect to the financial resources of the organization. These decisions are very crucial for

effectively managing the business. In this report, Morrisons is taken as an organization,

which is the leading supermarket chain in UK. It is headquartered in Bradford, England. It

was founded in 1899 by William Morrison. It has over 500 stores in UK and its business is

mostly into food and grocery. This report states about the role importance of accounting and

finance department with respect to the organization.

ACCOUNTING AND FINANCE DEPARTMENT

Accounting department

It is the part of company’s administration which is responsible for setting up the

financial reports by keeping up with the general ledger, paying bills, payroll, cost accounting

and financial analysis and more. The head of the accounting department also has the title of

controller (accounting department definition. 2020). The staff members of the company deal

with the accounting. In small companies, one or two people handles the all accounting affairs.

In large organizations, there are multiple sub-departments for handling different task such as

taxation, account receivables and so forth.

Finance department

Finance department is that part of the organization that manages money of the

organization (finance department. 2020). The business function of the finance department

mainly incorporates planning, organizing, accounting, auditing and the controlling and

managing the company’s financial statements. The finance department assesses the

organizational health which helps in taking decisions regarding short term and long-term

plans.

IMPORTANCE OF ACCOUNTING AND FINANCE DEPARTMENT

Accounting and finance department is very important for an organization for

navigating the business. They play an essential role in effectively managing the business. All

the companies operate on money because of which it is very important to handle it carefully.

The accounting and finance department of Morrisons, maintains the complete record of the

INTRODUCTION

Financial decision making is the process of taking relevant steps and decision with

respect to the financial resources of the organization. These decisions are very crucial for

effectively managing the business. In this report, Morrisons is taken as an organization,

which is the leading supermarket chain in UK. It is headquartered in Bradford, England. It

was founded in 1899 by William Morrison. It has over 500 stores in UK and its business is

mostly into food and grocery. This report states about the role importance of accounting and

finance department with respect to the organization.

ACCOUNTING AND FINANCE DEPARTMENT

Accounting department

It is the part of company’s administration which is responsible for setting up the

financial reports by keeping up with the general ledger, paying bills, payroll, cost accounting

and financial analysis and more. The head of the accounting department also has the title of

controller (accounting department definition. 2020). The staff members of the company deal

with the accounting. In small companies, one or two people handles the all accounting affairs.

In large organizations, there are multiple sub-departments for handling different task such as

taxation, account receivables and so forth.

Finance department

Finance department is that part of the organization that manages money of the

organization (finance department. 2020). The business function of the finance department

mainly incorporates planning, organizing, accounting, auditing and the controlling and

managing the company’s financial statements. The finance department assesses the

organizational health which helps in taking decisions regarding short term and long-term

plans.

IMPORTANCE OF ACCOUNTING AND FINANCE DEPARTMENT

Accounting and finance department is very important for an organization for

navigating the business. They play an essential role in effectively managing the business. All

the companies operate on money because of which it is very important to handle it carefully.

The accounting and finance department of Morrisons, maintains the complete record of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial activities of the business and keeps track of the income and expenses of the

business. By maintaining the accurate financial records, helps the organization in managing

their financial future and the cash flow. It also helps in following the business law as even a

minor detail can have a huge impact on the tax management (Accounting and Finance: Why

Is It Important to Your Business? 2020). The financial managers of the organization, analyses

the different needs of the businesses and also has the complete understanding about what

expenses need to be deducted and when to pay tax. The poor management of financial

recording will lead the company being audited and may result into unnecessary legal

consequences to be faced by the company. The information provided by the each of these

department helps the financial manager of Morrisons in taking valuable decisions by taking

into account the financial performance and position of the business. It helps the organization

in knowing whether the project will be profitable to the business or not and also how much

capital is required to fund the business.

ROLE OF ACCOUNTS DEPARTMENT

Accounting department plays a crucial role in an organization. A detailed description

is given below.

Financial accounting

It is concerned with keeping the proper record of all the financial transactions using

double entry bookkeeping and preparing the final accounts which are suitable for meeting the

various regulatory requirements. The accounts department is responsible for keeping record

of each financial transactions. It is used by both internal and external users. In Morrisons, its

accounts department is very effective in managing its transaction and preparing the report for

the same. But it requires complete knowledge of accounting and the regulatory requirements

that the company is required to follow.

Management accounting

It is concerned with the analysing the information with the purpose of taking

decisions in order to assist the day to day business operation (Peysakhova and

Anyushenkova, 2018). The information is used by only internal management team. In

management accounting, the role of accounts department is to collect all the relevant data

from the different organizational units and observing and analysing the budget and funding

and allocation of resources. In Morrisons, separate management accountant is hired to carry

out these activities. It estimates the cost of production, marketing and other company’s

business. By maintaining the accurate financial records, helps the organization in managing

their financial future and the cash flow. It also helps in following the business law as even a

minor detail can have a huge impact on the tax management (Accounting and Finance: Why

Is It Important to Your Business? 2020). The financial managers of the organization, analyses

the different needs of the businesses and also has the complete understanding about what

expenses need to be deducted and when to pay tax. The poor management of financial

recording will lead the company being audited and may result into unnecessary legal

consequences to be faced by the company. The information provided by the each of these

department helps the financial manager of Morrisons in taking valuable decisions by taking

into account the financial performance and position of the business. It helps the organization

in knowing whether the project will be profitable to the business or not and also how much

capital is required to fund the business.

ROLE OF ACCOUNTS DEPARTMENT

Accounting department plays a crucial role in an organization. A detailed description

is given below.

Financial accounting

It is concerned with keeping the proper record of all the financial transactions using

double entry bookkeeping and preparing the final accounts which are suitable for meeting the

various regulatory requirements. The accounts department is responsible for keeping record

of each financial transactions. It is used by both internal and external users. In Morrisons, its

accounts department is very effective in managing its transaction and preparing the report for

the same. But it requires complete knowledge of accounting and the regulatory requirements

that the company is required to follow.

Management accounting

It is concerned with the analysing the information with the purpose of taking

decisions in order to assist the day to day business operation (Peysakhova and

Anyushenkova, 2018). The information is used by only internal management team. In

management accounting, the role of accounts department is to collect all the relevant data

from the different organizational units and observing and analysing the budget and funding

and allocation of resources. In Morrisons, separate management accountant is hired to carry

out these activities. It estimates the cost of production, marketing and other company’s

internal costs which helps in estimating the budget more accurately. On the other hand,

management accountant requires to highly qualified and should be aware of everything so

that organization can prepared itself.

Tax function

The most important role of accountant is to plan the tax liabilities of the organization.

It includes managing the tax matters, return filing, making representations in front of

authorities and settling the tax liability under various laws. The accountants of Morrisons are

well versed with their responsibility in respect to taxation and always makes sure that

everything is properly documented. But it requires highly skilled person who is having

knowledge of taxation and maintaining all records even for small things in written is difficult.

Auditing function

In this, the internal staff of the organization carries out internal audit to ensure that all

the financial transaction pertaining to the accounting to yea is recorded or not. It also makes

sure that accounting policies are followed by the organization. Morrisons carries out internal

audit to know the accuracy of its financial information and identify any discrepancies as well.

This may cause changes in the financial report which may not be beneficial for the company.

ROLE OF FINANCE DEPARTMENT

There are various roles of finance department few of them are stated below.

Investment function

It is the most important role of finance department which is related to capital

budgeting. This function is very crucial for effectively managing and allocating the capital

resources in the long-term projects which in result gets maximum yield in future. This

function assists the Morrisons in effectively evaluating the feasibility of the project and the

profitability associated with it so that right decision can be taken. But in contrast, it uses

discounting rate which is by the organization which may turn out to be inaccurate leading to

wrongful investment decision.

Financing function

Financing function involves the function of acquiring the funds for the business. It

covers the various sources of finance that can be used by the organizations to meet their

capital requirements (Fatema, 2017). The finance department of Morrison is highly skilled in

managing the capital structure of the company by effectively having the nix of debt and

management accountant requires to highly qualified and should be aware of everything so

that organization can prepared itself.

Tax function

The most important role of accountant is to plan the tax liabilities of the organization.

It includes managing the tax matters, return filing, making representations in front of

authorities and settling the tax liability under various laws. The accountants of Morrisons are

well versed with their responsibility in respect to taxation and always makes sure that

everything is properly documented. But it requires highly skilled person who is having

knowledge of taxation and maintaining all records even for small things in written is difficult.

Auditing function

In this, the internal staff of the organization carries out internal audit to ensure that all

the financial transaction pertaining to the accounting to yea is recorded or not. It also makes

sure that accounting policies are followed by the organization. Morrisons carries out internal

audit to know the accuracy of its financial information and identify any discrepancies as well.

This may cause changes in the financial report which may not be beneficial for the company.

ROLE OF FINANCE DEPARTMENT

There are various roles of finance department few of them are stated below.

Investment function

It is the most important role of finance department which is related to capital

budgeting. This function is very crucial for effectively managing and allocating the capital

resources in the long-term projects which in result gets maximum yield in future. This

function assists the Morrisons in effectively evaluating the feasibility of the project and the

profitability associated with it so that right decision can be taken. But in contrast, it uses

discounting rate which is by the organization which may turn out to be inaccurate leading to

wrongful investment decision.

Financing function

Financing function involves the function of acquiring the funds for the business. It

covers the various sources of finance that can be used by the organizations to meet their

capital requirements (Fatema, 2017). The finance department of Morrison is highly skilled in

managing the capital structure of the company by effectively having the nix of debt and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

equity. But the identifying the which source of finance is appropriate for the company is very

essential from the long-term perspective.

Dividend function

In this, the finance department determines how much and how frequently and in what

form the company should pay or return cash to its owners. A balance is decided between

profits retained and amount paid for dividend. The finance team of Morrison is responsible

for taking decision to maintain the optimum dividend payout ratio. While making decision it

is important to consider the interest of the shareholders which might be affected due to less or

non-payment of dividend.

Working capital function

This role of finance department is crucial in maintaining the liquidity of the business.

The firms’ liquidity, profitability and risk is associated with the investment in current assets

and divestment in current liabilities. Morrisons is highly effective in maintaining the its

working capital to meet the short term needs of the business. But in order to do this, it is

required to be analysed time to time and dispose off the assets which are no longer available.

TASK 2

Ratio analysis

Ratio analysis refers to analysing and interpreting the financial statements of the

business. It helps in evaluating the number of issues that the business faces in terms of

liquidity, solvency, profitability and efficiency (Patil, 2018). This tool is mostly used by the

outside user of financial information such as investors, creditors, government authorities,

customers, suppliers etc. It helps the users in identify and analysing the trends of the

company based on which decision is made.

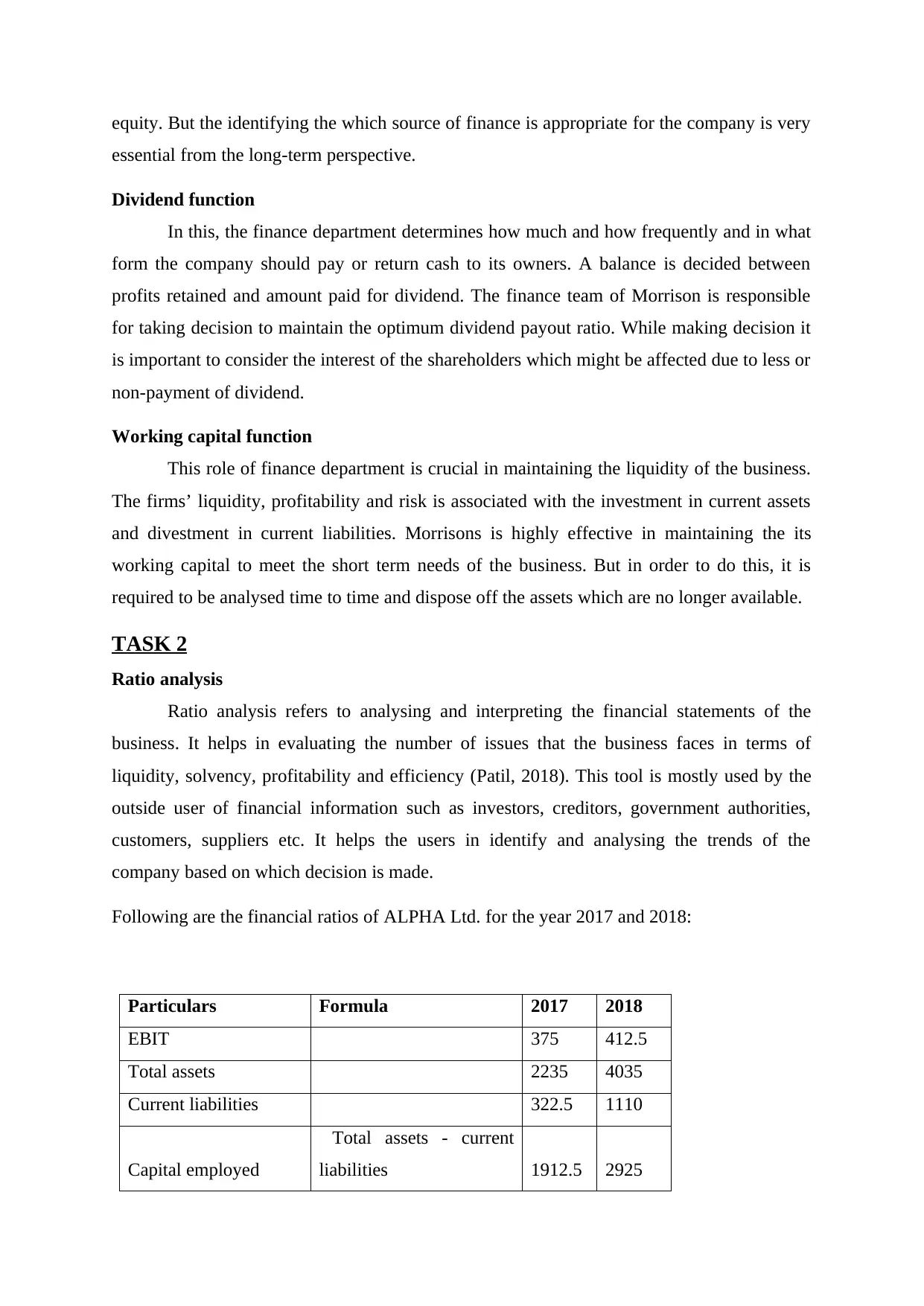

Following are the financial ratios of ALPHA Ltd. for the year 2017 and 2018:

Particulars Formula 2017 2018

EBIT 375 412.5

Total assets 2235 4035

Current liabilities 322.5 1110

Capital employed

Total assets - current

liabilities 1912.5 2925

essential from the long-term perspective.

Dividend function

In this, the finance department determines how much and how frequently and in what

form the company should pay or return cash to its owners. A balance is decided between

profits retained and amount paid for dividend. The finance team of Morrison is responsible

for taking decision to maintain the optimum dividend payout ratio. While making decision it

is important to consider the interest of the shareholders which might be affected due to less or

non-payment of dividend.

Working capital function

This role of finance department is crucial in maintaining the liquidity of the business.

The firms’ liquidity, profitability and risk is associated with the investment in current assets

and divestment in current liabilities. Morrisons is highly effective in maintaining the its

working capital to meet the short term needs of the business. But in order to do this, it is

required to be analysed time to time and dispose off the assets which are no longer available.

TASK 2

Ratio analysis

Ratio analysis refers to analysing and interpreting the financial statements of the

business. It helps in evaluating the number of issues that the business faces in terms of

liquidity, solvency, profitability and efficiency (Patil, 2018). This tool is mostly used by the

outside user of financial information such as investors, creditors, government authorities,

customers, suppliers etc. It helps the users in identify and analysing the trends of the

company based on which decision is made.

Following are the financial ratios of ALPHA Ltd. for the year 2017 and 2018:

Particulars Formula 2017 2018

EBIT 375 412.5

Total assets 2235 4035

Current liabilities 322.5 1110

Capital employed

Total assets - current

liabilities 1912.5 2925

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Return on capital

employed 20% 14%

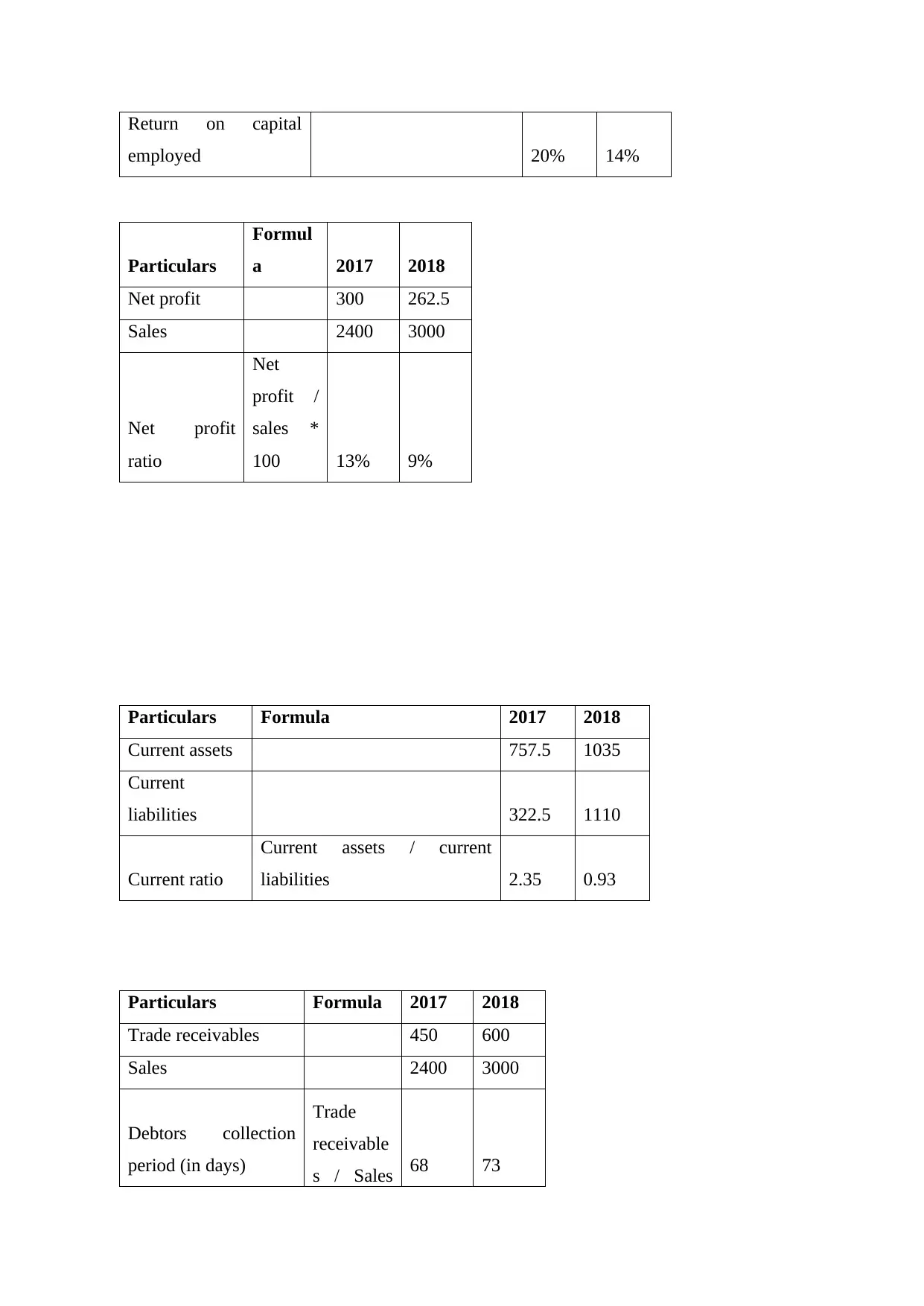

Particulars

Formul

a 2017 2018

Net profit 300 262.5

Sales 2400 3000

Net profit

ratio

Net

profit /

sales *

100 13% 9%

Particulars Formula 2017 2018

Current assets 757.5 1035

Current

liabilities 322.5 1110

Current ratio

Current assets / current

liabilities 2.35 0.93

Particulars Formula 2017 2018

Trade receivables 450 600

Sales 2400 3000

Debtors collection

period (in days)

Trade

receivable

s / Sales 68 73

employed 20% 14%

Particulars

Formul

a 2017 2018

Net profit 300 262.5

Sales 2400 3000

Net profit

ratio

Net

profit /

sales *

100 13% 9%

Particulars Formula 2017 2018

Current assets 757.5 1035

Current

liabilities 322.5 1110

Current ratio

Current assets / current

liabilities 2.35 0.93

Particulars Formula 2017 2018

Trade receivables 450 600

Sales 2400 3000

Debtors collection

period (in days)

Trade

receivable

s / Sales 68 73

*365

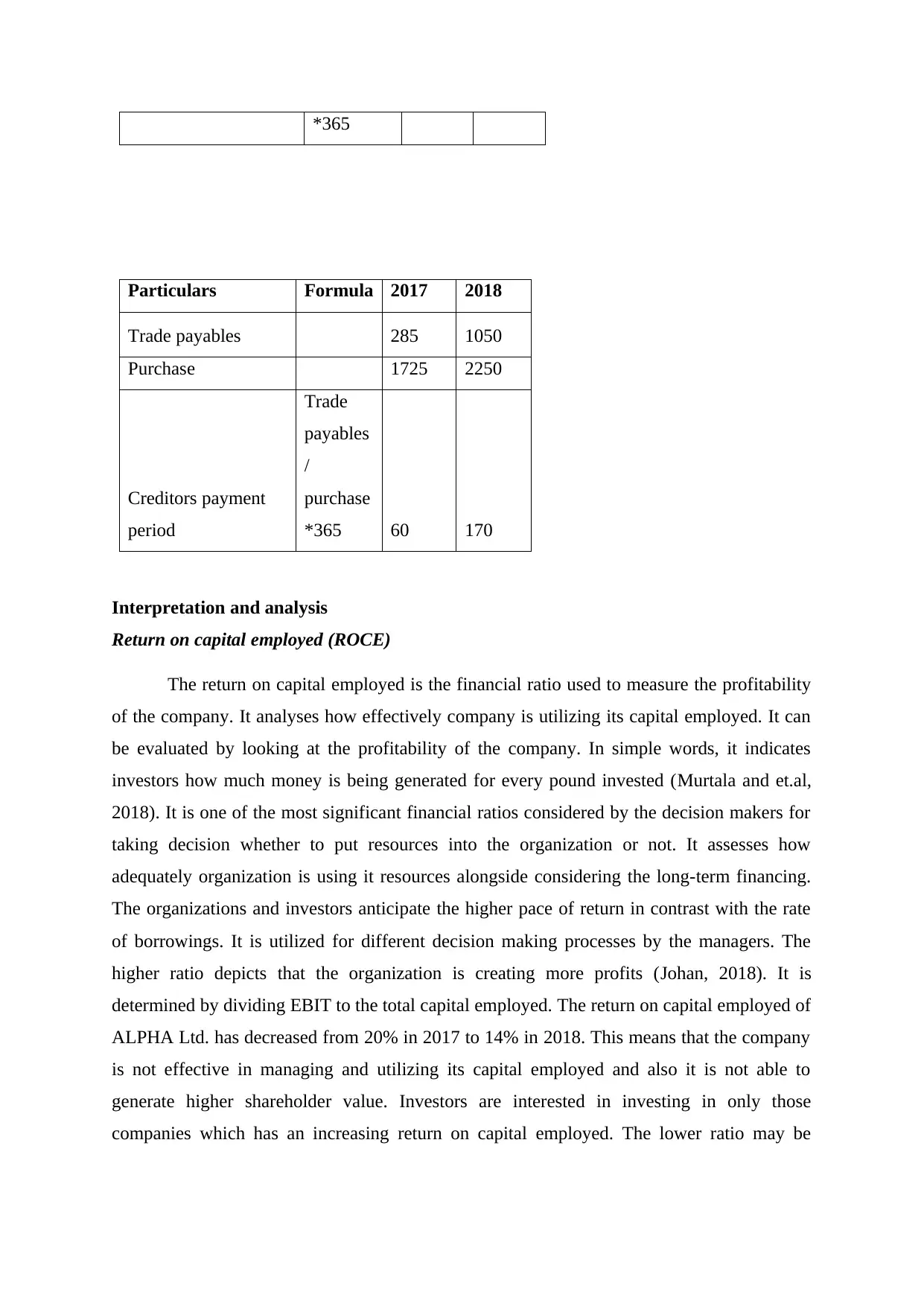

Particulars Formula 2017 2018

Trade payables 285 1050

Purchase 1725 2250

Creditors payment

period

Trade

payables

/

purchase

*365 60 170

Interpretation and analysis

Return on capital employed (ROCE)

The return on capital employed is the financial ratio used to measure the profitability

of the company. It analyses how effectively company is utilizing its capital employed. It can

be evaluated by looking at the profitability of the company. In simple words, it indicates

investors how much money is being generated for every pound invested (Murtala and et.al,

2018). It is one of the most significant financial ratios considered by the decision makers for

taking decision whether to put resources into the organization or not. It assesses how

adequately organization is using it resources alongside considering the long-term financing.

The organizations and investors anticipate the higher pace of return in contrast with the rate

of borrowings. It is utilized for different decision making processes by the managers. The

higher ratio depicts that the organization is creating more profits (Johan, 2018). It is

determined by dividing EBIT to the total capital employed. The return on capital employed of

ALPHA Ltd. has decreased from 20% in 2017 to 14% in 2018. This means that the company

is not effective in managing and utilizing its capital employed and also it is not able to

generate higher shareholder value. Investors are interested in investing in only those

companies which has an increasing return on capital employed. The lower ratio may be

Particulars Formula 2017 2018

Trade payables 285 1050

Purchase 1725 2250

Creditors payment

period

Trade

payables

/

purchase

*365 60 170

Interpretation and analysis

Return on capital employed (ROCE)

The return on capital employed is the financial ratio used to measure the profitability

of the company. It analyses how effectively company is utilizing its capital employed. It can

be evaluated by looking at the profitability of the company. In simple words, it indicates

investors how much money is being generated for every pound invested (Murtala and et.al,

2018). It is one of the most significant financial ratios considered by the decision makers for

taking decision whether to put resources into the organization or not. It assesses how

adequately organization is using it resources alongside considering the long-term financing.

The organizations and investors anticipate the higher pace of return in contrast with the rate

of borrowings. It is utilized for different decision making processes by the managers. The

higher ratio depicts that the organization is creating more profits (Johan, 2018). It is

determined by dividing EBIT to the total capital employed. The return on capital employed of

ALPHA Ltd. has decreased from 20% in 2017 to 14% in 2018. This means that the company

is not effective in managing and utilizing its capital employed and also it is not able to

generate higher shareholder value. Investors are interested in investing in only those

companies which has an increasing return on capital employed. The lower ratio may be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because of decrease in profit or increase in cost. Therefore, ALPHA Ltd. needs to monitor its

capital employed and reasons for such fall as it is a big concern for the company.

Net profit margin ratio

Net profit margin ratio is the profitability ratio which measures and expresses the

relationship between net profit and net sales. This ratio assists the company in identifying

whether the company is able to generate sufficient profits from its revenue and also it is an

important indicator of financial health of the company (Lacinka, Fathoni and Gagah, 2018). It

is derived by dividing net profit of the business with the total revenue. This ratio is used by

the investors and creditors in evaluating the efficiency of the business in converting its sales

into income. The lower net profit margin indicates that the company is having higher

expenses as against its sales and management is required to take control over the unnecessary

expenses which will result into increase in profits (Kuswanto, Raharjo and Andini, 2017).

Therefore, this ratio is a strong indicator of the organization’s growth and success. In case of

ALPHA Ltd., the net profit margin has reduced from 13% to 9% in 2018. This fall in the ratio

shows that the company is not actively focussing on its business operation. This also means

that the ALPHA Ltd. is not effective in managing its cost structure and is also required to

look after its pricing strategy. Therefore, this lower ratio might be because of inefficient

management, higher expenses and weak pricing strategies. In order to improve the net profit

margin of the company the only and the most effective way is to boost the revenue of the

company. This can be either done by increasing or decreasing the price of the product. Also,

the company analyse its operating expenses in order to identify the unnecessary expenses

which can be eliminated.

Current ratio

Current ratio is the liquidity ratio which is used to measure the liquidity position of

the business. It measures and monitors the ability of the business in meeting its short-term

obligation against its current assets without any need to take additional funds (Small, Dollie

and Yasseen, 2019). This ratio is very important for manufacturing concerns as it involves lot

of raw material and product cycle. It is determined by dividing current assets by current

liabilities. The higher ratio indicates that the company is having more than enough amount of

cash to discharge its short term obligations. The ideal current ratio is 1. Having ratio less than

1 indicates that company is not having sufficient amount of current assets to meet its current

liabilities. In case of ALPHA Ltd., it can be clearly seen that there is a decrease in current

capital employed and reasons for such fall as it is a big concern for the company.

Net profit margin ratio

Net profit margin ratio is the profitability ratio which measures and expresses the

relationship between net profit and net sales. This ratio assists the company in identifying

whether the company is able to generate sufficient profits from its revenue and also it is an

important indicator of financial health of the company (Lacinka, Fathoni and Gagah, 2018). It

is derived by dividing net profit of the business with the total revenue. This ratio is used by

the investors and creditors in evaluating the efficiency of the business in converting its sales

into income. The lower net profit margin indicates that the company is having higher

expenses as against its sales and management is required to take control over the unnecessary

expenses which will result into increase in profits (Kuswanto, Raharjo and Andini, 2017).

Therefore, this ratio is a strong indicator of the organization’s growth and success. In case of

ALPHA Ltd., the net profit margin has reduced from 13% to 9% in 2018. This fall in the ratio

shows that the company is not actively focussing on its business operation. This also means

that the ALPHA Ltd. is not effective in managing its cost structure and is also required to

look after its pricing strategy. Therefore, this lower ratio might be because of inefficient

management, higher expenses and weak pricing strategies. In order to improve the net profit

margin of the company the only and the most effective way is to boost the revenue of the

company. This can be either done by increasing or decreasing the price of the product. Also,

the company analyse its operating expenses in order to identify the unnecessary expenses

which can be eliminated.

Current ratio

Current ratio is the liquidity ratio which is used to measure the liquidity position of

the business. It measures and monitors the ability of the business in meeting its short-term

obligation against its current assets without any need to take additional funds (Small, Dollie

and Yasseen, 2019). This ratio is very important for manufacturing concerns as it involves lot

of raw material and product cycle. It is determined by dividing current assets by current

liabilities. The higher ratio indicates that the company is having more than enough amount of

cash to discharge its short term obligations. The ideal current ratio is 1. Having ratio less than

1 indicates that company is not having sufficient amount of current assets to meet its current

liabilities. In case of ALPHA Ltd., it can be clearly seen that there is a decrease in current

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ratio, which is, 0.93 times in 2018 in comparison to 2.35 times in 2017. There has been a

massive drop in the ratio which increases the need for the company to either increase its

current assets or reduce its current liabilities (Husna and Satria, 2019). This will help in

achieving the ideal current ratio and improving its liquidity position. ALPHA Ltd., should

consider this as a warning signal to work effectively otherwise it will lead to cash crunch

situation. The company also needs to understand that its ratio should not be more than 3 as it

means that company is blocking lot cash and is not properly managing its working capital.

For improving its current ratio company needs to analyse its credit policy, amount blocked by

the debtors, provision for bad debts created. Also, it should make an effort to decrease its

current liabilities by paying off its short-term liabilities as soon as possible which will result

into decreasing the interest liabilities as well.

Average receivable/collection days

The average receivable days is the time period it takes to a business organization to

collect the payment for its customers to whom goods are sold on a credit which is known as

accounts receivable. This can be calculated by dividing trade receivables/sales multiplied by

365 days. This ratio is very crucial for the business entities which mostly rely on the credit

sales (Ejike and Agha, 2018). It represents the number of the days from the date a credit sale

is made to the customer and the date of receiving the payment for it. The lower ratio shows

that the company is very efficient in collecting its payment from the customers within the

time frame which is very favourable. The longer collection period means that the business

entity is struggling in recovering the amount from its account receivables. The debtor

collection period of ALPHA Ltd. is 73 days in 2018 and 68 days in 2017. This indicates that

the there is an increase in 5 days which the company needs to look after and identify the

reason for the same (Sawarni, Narayanasamy and Ayyalusamy, 2020). Mostly the cause of it

can be the weak credit policy of the company which may provide more credit to the

customers with the objective to increase the sales. Another factor can be economic slowdown

which is affecting the cash flow the customers and this has consequently led to the delay in

payments. One more reason is that the ALPHA Ltd. must be having not so effective

collection team and increase in employee turnover which is influencing the collection process

of the company. In order to improve its average receivable, the company needs t implement a

strict credit policy to its customers and on non-payment of it on time, it will no longer enter

into a deal with that customer in future.

massive drop in the ratio which increases the need for the company to either increase its

current assets or reduce its current liabilities (Husna and Satria, 2019). This will help in

achieving the ideal current ratio and improving its liquidity position. ALPHA Ltd., should

consider this as a warning signal to work effectively otherwise it will lead to cash crunch

situation. The company also needs to understand that its ratio should not be more than 3 as it

means that company is blocking lot cash and is not properly managing its working capital.

For improving its current ratio company needs to analyse its credit policy, amount blocked by

the debtors, provision for bad debts created. Also, it should make an effort to decrease its

current liabilities by paying off its short-term liabilities as soon as possible which will result

into decreasing the interest liabilities as well.

Average receivable/collection days

The average receivable days is the time period it takes to a business organization to

collect the payment for its customers to whom goods are sold on a credit which is known as

accounts receivable. This can be calculated by dividing trade receivables/sales multiplied by

365 days. This ratio is very crucial for the business entities which mostly rely on the credit

sales (Ejike and Agha, 2018). It represents the number of the days from the date a credit sale

is made to the customer and the date of receiving the payment for it. The lower ratio shows

that the company is very efficient in collecting its payment from the customers within the

time frame which is very favourable. The longer collection period means that the business

entity is struggling in recovering the amount from its account receivables. The debtor

collection period of ALPHA Ltd. is 73 days in 2018 and 68 days in 2017. This indicates that

the there is an increase in 5 days which the company needs to look after and identify the

reason for the same (Sawarni, Narayanasamy and Ayyalusamy, 2020). Mostly the cause of it

can be the weak credit policy of the company which may provide more credit to the

customers with the objective to increase the sales. Another factor can be economic slowdown

which is affecting the cash flow the customers and this has consequently led to the delay in

payments. One more reason is that the ALPHA Ltd. must be having not so effective

collection team and increase in employee turnover which is influencing the collection process

of the company. In order to improve its average receivable, the company needs t implement a

strict credit policy to its customers and on non-payment of it on time, it will no longer enter

into a deal with that customer in future.

Average payable days

Average payable days is the one of the solvency ratios which is used for determining

the average number of days its takes for a business to pay off its debts to its suppliers and

vendors from whom it has purchased goods on credit. The increase in the days indicates that

the company is making payment very slowly (Riaz, 2019). On the other hand, if the company

is paying the due amount quickly it means that the supplier must be having a strict credit

policy and a strong collection team. In ALPHA Ltd., the average payable days has shown a

rise from 60 days to 170 days. This increase can be beneficial for the company as it has the

chance to retain its cash for the long term which will help in continuing its business operation

smoothly. ALPHA Ltd. can also take advantage of it by investing the excess cash in the short

term investment plan for gaining additional income. In contrast, ALPHA Ltd. also needs to

take into account the negative outcomes of it (Jikia and Kharabadze, 2018). If the company

takes a long time in making payment it may also mean that the company is not having enough

cash to make payment. It will also result int making suppliers and vendors unhappy which

may affect the future dealings like suppliers may refuse to extend the credit facility or any

other favourable terms. Thus, higher payable period, would mean that either supplier is

providing better credit terms or company has inability to pay on time.

Therefore, it can be said from the above that the financial position and performance of

ALPHA Ltd. is not that good. It needs to effectively work on its business operation and

monitor it on timely basis in order to avoid any discrepancy in the process. This is very well

connected with its fall in return on capital employed (ROCE), net profit margins, lower,

current ratio and the higher collection period. Apart from this, the higher accounts payable

period, should not be considered much in favour of the company. Thus, it can be said that,

from investors point of view, investors should not invest in the company as it is not feasible

and profitable.

Average payable days is the one of the solvency ratios which is used for determining

the average number of days its takes for a business to pay off its debts to its suppliers and

vendors from whom it has purchased goods on credit. The increase in the days indicates that

the company is making payment very slowly (Riaz, 2019). On the other hand, if the company

is paying the due amount quickly it means that the supplier must be having a strict credit

policy and a strong collection team. In ALPHA Ltd., the average payable days has shown a

rise from 60 days to 170 days. This increase can be beneficial for the company as it has the

chance to retain its cash for the long term which will help in continuing its business operation

smoothly. ALPHA Ltd. can also take advantage of it by investing the excess cash in the short

term investment plan for gaining additional income. In contrast, ALPHA Ltd. also needs to

take into account the negative outcomes of it (Jikia and Kharabadze, 2018). If the company

takes a long time in making payment it may also mean that the company is not having enough

cash to make payment. It will also result int making suppliers and vendors unhappy which

may affect the future dealings like suppliers may refuse to extend the credit facility or any

other favourable terms. Thus, higher payable period, would mean that either supplier is

providing better credit terms or company has inability to pay on time.

Therefore, it can be said from the above that the financial position and performance of

ALPHA Ltd. is not that good. It needs to effectively work on its business operation and

monitor it on timely basis in order to avoid any discrepancy in the process. This is very well

connected with its fall in return on capital employed (ROCE), net profit margins, lower,

current ratio and the higher collection period. Apart from this, the higher accounts payable

period, should not be considered much in favour of the company. Thus, it can be said that,

from investors point of view, investors should not invest in the company as it is not feasible

and profitable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.