Financial Decision Making Report: Finance and Accounting Functions

VerifiedAdded on 2023/01/05

|13

|3989

|54

Report

AI Summary

This report delves into the significance of accounting and finance functions within the context of SKANSA PLC. It explores the crucial roles these functions play in maintaining financial records, mitigating legal issues, setting budgets, analyzing performance, and facilitating both internal and external communication. The report outlines the duties of various accounting and finance roles, including financial accounting, financial systems, accounts payable and receivable, payroll, and financial reporting. Furthermore, it presents a ratio analysis, calculating and interpreting the Return on Capital Employed (ROCE), Net Profit Margin, and Current Ratio for SKANSA PLC, offering insights into the company's profitability and liquidity. The analysis includes calculations for 2018 and 2019, providing a comparative view of the company's financial performance over the period.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1 Report................................................................................................................................3

Introduction..................................................................................................................................3

Importance of Accounting and Finance functions.......................................................................3

Roles and duties of Accounting and Finance functions within SKANSA PLC..........................5

Conclusions..................................................................................................................................7

TASK 2 Ratio Analyses...................................................................................................................8

a. Calculation of Ratios................................................................................................................8

b. Results....................................................................................................................................12

References......................................................................................................................................13

TASK 1 Report................................................................................................................................3

Introduction..................................................................................................................................3

Importance of Accounting and Finance functions.......................................................................3

Roles and duties of Accounting and Finance functions within SKANSA PLC..........................5

Conclusions..................................................................................................................................7

TASK 2 Ratio Analyses...................................................................................................................8

a. Calculation of Ratios................................................................................................................8

b. Results....................................................................................................................................12

References......................................................................................................................................13

TASK 1 Report

Introduction

This report presents (express) the importance of accounting and finance in the business of

SKANSA PLS. Moreover, it contains the functions used by departments like finance and

accounting to help businesses setting up budgets or making sure the business stays profitable.

Importance of Accounting and Finance functions

Accounting and finance are involved in accounting and auditing business practices.

Understanding where inbound and outbound capital will help the client for better options that

push forward to maintain a strategic distance from disappointment.

Some of the importance of Accounting and Finance functions are as under:

1. Keep financial records

An organization chart is the place where accountants and business owners can keep track of

business expenses and expenses from day to day. A detailed group account registration can allow

a company to manage their future budget and understand their revenue (Jetter and Walker, 2017).

2. Stay away from legal problems

Keeping a cash register simply follows important business laws. Neglecting details can have a

profound effect on the board. Budget makers need to understand what expenses need to be

deducted, which valuations should be paid and when these responsibilities should be covered. An

incorrect budget account could scrutinize an organization and lead to an unnecessary legitimate

problem. Additionally, overseeing the updating of an office's accounts can result in the

organization failing to comply with the guidelines of the security law (Jetter and Walker, 2017).

3. Set a budget

Using budget ledgers and understanding revenue can help create a cost plan, and it is the

spending plan that keeps the business afloat. Cost provides a standard view of the financial

situation and examines the industry for future development and development. While making a

full spending gain, you need to consider costs, goals and anticipate sudden changes. Staying at

these numbers is crucial to keeping track of business, so it’s important to keep an eye on startups

Introduction

This report presents (express) the importance of accounting and finance in the business of

SKANSA PLS. Moreover, it contains the functions used by departments like finance and

accounting to help businesses setting up budgets or making sure the business stays profitable.

Importance of Accounting and Finance functions

Accounting and finance are involved in accounting and auditing business practices.

Understanding where inbound and outbound capital will help the client for better options that

push forward to maintain a strategic distance from disappointment.

Some of the importance of Accounting and Finance functions are as under:

1. Keep financial records

An organization chart is the place where accountants and business owners can keep track of

business expenses and expenses from day to day. A detailed group account registration can allow

a company to manage their future budget and understand their revenue (Jetter and Walker, 2017).

2. Stay away from legal problems

Keeping a cash register simply follows important business laws. Neglecting details can have a

profound effect on the board. Budget makers need to understand what expenses need to be

deducted, which valuations should be paid and when these responsibilities should be covered. An

incorrect budget account could scrutinize an organization and lead to an unnecessary legitimate

problem. Additionally, overseeing the updating of an office's accounts can result in the

organization failing to comply with the guidelines of the security law (Jetter and Walker, 2017).

3. Set a budget

Using budget ledgers and understanding revenue can help create a cost plan, and it is the

spending plan that keeps the business afloat. Cost provides a standard view of the financial

situation and examines the industry for future development and development. While making a

full spending gain, you need to consider costs, goals and anticipate sudden changes. Staying at

these numbers is crucial to keeping track of business, so it’s important to keep an eye on startups

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and change regularly as you go along. Good accounting sets the direction for business

management and provides a solid foundation for strength and performance (Jetter and Walker,

2017).

4. Performance analysis

Efficient entrepreneurs are always signing up to see how their business is doing. An organization

can assess its financial position by looking at its historical and current records of liabilities and

resources and other balance sheets. An entrepreneur can use this data to see how the organization

is performing. These records provide an opportunity to take advantage of past messages and

decide on more informed choices about how to create a more useful future. Fulfilling the current

financial position can help identify new development zones that will help meet the key

responsibility (Jetter and Walker, 2017).

5. External communication

Matching financial data is important when managing external meetings. Clear accounting and

money for operators can be useful in getting down payments from a bank or attracting similar

speculators. Big money management makes it easier to provide tax reports to outside partners.

External clients will evaluate these relationships to determine how to continue to integrate them

into their business (Jetter and Walker, 2017).

6. Internal Communication

Financial reporting can also help entrepreneurs provide data to internal partners. This data may

be relevant to employees interested in sharing benefits and share-based compensation. Likewise,

these records allow owners to share the characteristics and shortcomings of their business with

their organizations. A licensing entity can achieve its financial strength through a reward

structure that can be used as a profit incentive (Jetter and Walker, 2017).

7. Developing strategy

Accounting and finance management encourage a sensible approach. Once you've created a

spending plan and broken down the information completely, it should be easier to have a better

deal to build a way to fulfill your primary responsibility. Looking at budget records will make it

easier to set up money-related educational options on everything from staff to flexible board.

management and provides a solid foundation for strength and performance (Jetter and Walker,

2017).

4. Performance analysis

Efficient entrepreneurs are always signing up to see how their business is doing. An organization

can assess its financial position by looking at its historical and current records of liabilities and

resources and other balance sheets. An entrepreneur can use this data to see how the organization

is performing. These records provide an opportunity to take advantage of past messages and

decide on more informed choices about how to create a more useful future. Fulfilling the current

financial position can help identify new development zones that will help meet the key

responsibility (Jetter and Walker, 2017).

5. External communication

Matching financial data is important when managing external meetings. Clear accounting and

money for operators can be useful in getting down payments from a bank or attracting similar

speculators. Big money management makes it easier to provide tax reports to outside partners.

External clients will evaluate these relationships to determine how to continue to integrate them

into their business (Jetter and Walker, 2017).

6. Internal Communication

Financial reporting can also help entrepreneurs provide data to internal partners. This data may

be relevant to employees interested in sharing benefits and share-based compensation. Likewise,

these records allow owners to share the characteristics and shortcomings of their business with

their organizations. A licensing entity can achieve its financial strength through a reward

structure that can be used as a profit incentive (Jetter and Walker, 2017).

7. Developing strategy

Accounting and finance management encourage a sensible approach. Once you've created a

spending plan and broken down the information completely, it should be easier to have a better

deal to build a way to fulfill your primary responsibility. Looking at budget records will make it

easier to set up money-related educational options on everything from staff to flexible board.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The financial recording, summarizing, analyzing and recording of financial transactions help

owners, managers and investors evaluate a company’s financial health. The realization of this

data suggests multiple key business options (Jetter and Walker, 2017).

Roles and duties of Accounting and Finance functions within SKANSA PLC

Duties

Financial accounting - This involves keeping records, all that is considered, using a dual pass

accounting framework and designing the latest relevant ledgers to meet the requirements

different administrative needs for legal details, stock trading and tax assessment stock trading

experts. The budget accountant is the person responsible for this capability in medium to large

societies, who usually report to the account manager (Lichtenberg and et.al., 2018).

Financial systems - Medium-sized estimating societies can use a cadres accountant, which

analyzes society’s budget data needs and reviews existing cadres. It is responsible for designing

and supporting budget frameworks and providing an interface between the accounts and

innovation / frameworks departments. Within accounting and cash operations, a central

management accountant may be accountable to the cash accountant, executive accountant or

chief financial officer (Lichtenberg and et.al., 2018).

Accounts Payable (money out) - Trying to maintain amazing relationships with buyers is an

urgent task ensuring that everyone is paid on time. . The accounting department reminds you to

keep an eye out for opportunities to set aside money, for example, to determine if limits or

incentive forces are available to pay certain buyers significantly more. soon. In any case, the AP

should be retained to ensure that the minimum amount of money must be disbursed in

installments, i.e. no charges for late allowances (Lichtenberg and et.al., 2018).

Accounts Receivable and Revenue Tracking (money in) - Another key responsibility of the

accounting department is to produce and track receipts, including surprising research and all

necessary sorting actions. Available records are subject to research and monitoring. The

obligation here includes ensuring that customers pay for these applications on a per-schedule

basis, so it's important to arrange friendly updates (Lichtenberg and et.al., 2018).

Payroll - Payment is a key skill in the accounting industry and includes ensuring that all

representatives are paid accurately and conveniently. Additionally, appropriate liability is

owners, managers and investors evaluate a company’s financial health. The realization of this

data suggests multiple key business options (Jetter and Walker, 2017).

Roles and duties of Accounting and Finance functions within SKANSA PLC

Duties

Financial accounting - This involves keeping records, all that is considered, using a dual pass

accounting framework and designing the latest relevant ledgers to meet the requirements

different administrative needs for legal details, stock trading and tax assessment stock trading

experts. The budget accountant is the person responsible for this capability in medium to large

societies, who usually report to the account manager (Lichtenberg and et.al., 2018).

Financial systems - Medium-sized estimating societies can use a cadres accountant, which

analyzes society’s budget data needs and reviews existing cadres. It is responsible for designing

and supporting budget frameworks and providing an interface between the accounts and

innovation / frameworks departments. Within accounting and cash operations, a central

management accountant may be accountable to the cash accountant, executive accountant or

chief financial officer (Lichtenberg and et.al., 2018).

Accounts Payable (money out) - Trying to maintain amazing relationships with buyers is an

urgent task ensuring that everyone is paid on time. . The accounting department reminds you to

keep an eye out for opportunities to set aside money, for example, to determine if limits or

incentive forces are available to pay certain buyers significantly more. soon. In any case, the AP

should be retained to ensure that the minimum amount of money must be disbursed in

installments, i.e. no charges for late allowances (Lichtenberg and et.al., 2018).

Accounts Receivable and Revenue Tracking (money in) - Another key responsibility of the

accounting department is to produce and track receipts, including surprising research and all

necessary sorting actions. Available records are subject to research and monitoring. The

obligation here includes ensuring that customers pay for these applications on a per-schedule

basis, so it's important to arrange friendly updates (Lichtenberg and et.al., 2018).

Payroll - Payment is a key skill in the accounting industry and includes ensuring that all

representatives are paid accurately and conveniently. Additionally, appropriate liability is

assessed and cost indemnities are timely with state and government offices (Lichtenberg and

et.al., 2018).

Reporting and Financial Statements - The essential explanation is to gather information

appropriately in the accounting program to obtain ready-made budget reports that can be used for

planning, estimating and other dynamic cycles. Furthermore, these and different reports are

needed to communicate with various speculators, banks and experts who are taking action for the

development of your business (Lichtenberg and et.al., 2018).

Financial Controls - Financial controls include trade-offs, segregation of duties, and adherence

to GAAP accounting standards guidelines, all of which are implemented in terms of persistence,

misrepresentation, and the prospect of burglary. The administrator's job is to make sure the

systems are in place to go through that cycle without errors (Lichtenberg and et.al., 2018).

Roles

Chief Financial Officer (or CFO) - CFOs are usually the cash managers of large organizations.

They manage the finances, the welfare of the company and take care of the rest of the budget

office. CFOs are highly innovative and will help organizations monitor levels of improvement

and reduction. With their knowledge of the organization’s assets, they help senior management

understand the financial impact of ongoing options to ensure the financial performance of the

business (Lichtenberg and et.al., 2018).

Their duties include financial planning, reporting and controls, short and long term business

strategy, investments, hedging, mergers and acquisitions, cash management, internal risk

management, corporate finance, auditing and accounting.

Financial Controller - Financial regulators are vital partners within accounting departments and

work closely with CFOs, COOs and CFOs. Their capabilities and responsibilities include budget

accounting, access, publishing, auditing, design, boarding, and the sky is the limit. Their main

work as a whole focuses on quick cash issues and the board of directors (Lichtenberg and et.al.,

2018).

et.al., 2018).

Reporting and Financial Statements - The essential explanation is to gather information

appropriately in the accounting program to obtain ready-made budget reports that can be used for

planning, estimating and other dynamic cycles. Furthermore, these and different reports are

needed to communicate with various speculators, banks and experts who are taking action for the

development of your business (Lichtenberg and et.al., 2018).

Financial Controls - Financial controls include trade-offs, segregation of duties, and adherence

to GAAP accounting standards guidelines, all of which are implemented in terms of persistence,

misrepresentation, and the prospect of burglary. The administrator's job is to make sure the

systems are in place to go through that cycle without errors (Lichtenberg and et.al., 2018).

Roles

Chief Financial Officer (or CFO) - CFOs are usually the cash managers of large organizations.

They manage the finances, the welfare of the company and take care of the rest of the budget

office. CFOs are highly innovative and will help organizations monitor levels of improvement

and reduction. With their knowledge of the organization’s assets, they help senior management

understand the financial impact of ongoing options to ensure the financial performance of the

business (Lichtenberg and et.al., 2018).

Their duties include financial planning, reporting and controls, short and long term business

strategy, investments, hedging, mergers and acquisitions, cash management, internal risk

management, corporate finance, auditing and accounting.

Financial Controller - Financial regulators are vital partners within accounting departments and

work closely with CFOs, COOs and CFOs. Their capabilities and responsibilities include budget

accounting, access, publishing, auditing, design, boarding, and the sky is the limit. Their main

work as a whole focuses on quick cash issues and the board of directors (Lichtenberg and et.al.,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Treasury Manager - The job of an investment manager in the accounting department revolves

around detailing and promoting fortune making. This includes differentiating the best business

openings, creating amazing financial relationships, promoting credit bureaus, and limiting

account spending (Lichtenberg and et.al., 2018).

Accounting Manager - An accounting manager is responsible for group maintenance exercises

that include maintenance and provides details of both money-related and money-related expenses

but does not deal or organize. Accounting Manager elevates and adheres to accounting standards

in accordance with legal requirements and strategic audit (Lichtenberg and et.al., 2018).

Chief Accounting - The Accountant has similar responsibilities to the Accounting Manager, but

the role varies by job title.

Accounting Supervisor - Shares responsibilities as the accounting manager and offers

assistance as an individual from his organization.

Accountant: Accountants perform key tasks in financial areas, such as estimating and translating

balance sheet data. The results of their work promise sustainability and underpin more

transparent budgetary practices.

Clerks - Accountants provide the daily efforts that should record and analyze vital accounting

information. They usually don't play a big role.

Conclusions

These are just part of the main functions and elements of the accounting department in

organizations, there are many more functions that are the responsibility of the accounting

department and various sub-departments. These will depend on the specific business idea. For

example, control of investments and follow-up work, government resources and reporting of

responsibilities and fundraising may be other key areas of the center for which the accounting

office would be responsible. While the specific operations may vary from company to company,

one thing is certain: if the accounting department is not successfully and productively performing

these key skills, the organization could be difficult situation.

around detailing and promoting fortune making. This includes differentiating the best business

openings, creating amazing financial relationships, promoting credit bureaus, and limiting

account spending (Lichtenberg and et.al., 2018).

Accounting Manager - An accounting manager is responsible for group maintenance exercises

that include maintenance and provides details of both money-related and money-related expenses

but does not deal or organize. Accounting Manager elevates and adheres to accounting standards

in accordance with legal requirements and strategic audit (Lichtenberg and et.al., 2018).

Chief Accounting - The Accountant has similar responsibilities to the Accounting Manager, but

the role varies by job title.

Accounting Supervisor - Shares responsibilities as the accounting manager and offers

assistance as an individual from his organization.

Accountant: Accountants perform key tasks in financial areas, such as estimating and translating

balance sheet data. The results of their work promise sustainability and underpin more

transparent budgetary practices.

Clerks - Accountants provide the daily efforts that should record and analyze vital accounting

information. They usually don't play a big role.

Conclusions

These are just part of the main functions and elements of the accounting department in

organizations, there are many more functions that are the responsibility of the accounting

department and various sub-departments. These will depend on the specific business idea. For

example, control of investments and follow-up work, government resources and reporting of

responsibilities and fundraising may be other key areas of the center for which the accounting

office would be responsible. While the specific operations may vary from company to company,

one thing is certain: if the accounting department is not successfully and productively performing

these key skills, the organization could be difficult situation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2 Ratio Analyses

a. Calculation of Ratios

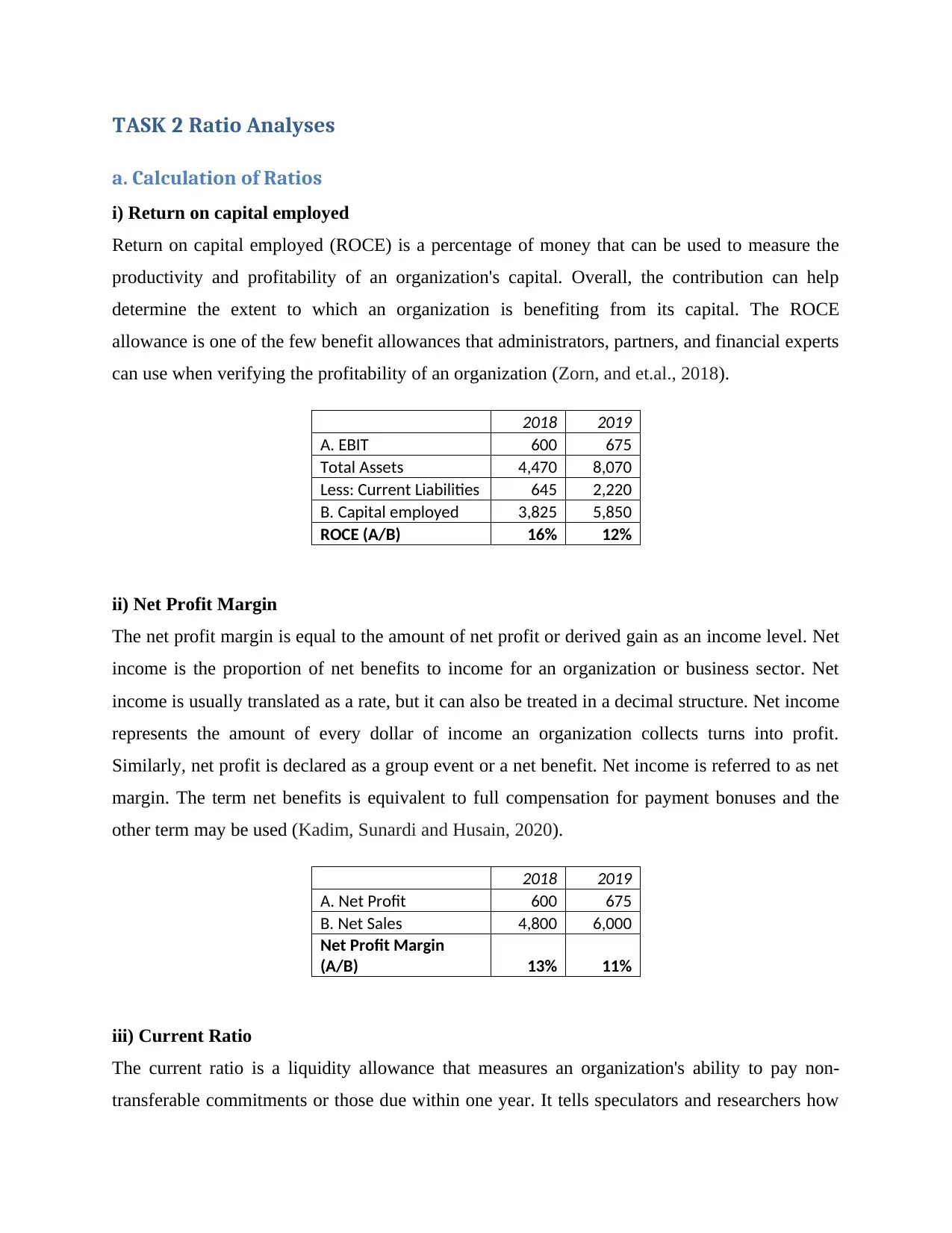

i) Return on capital employed

Return on capital employed (ROCE) is a percentage of money that can be used to measure the

productivity and profitability of an organization's capital. Overall, the contribution can help

determine the extent to which an organization is benefiting from its capital. The ROCE

allowance is one of the few benefit allowances that administrators, partners, and financial experts

can use when verifying the profitability of an organization (Zorn, and et.al., 2018).

2018 2019

A. EBIT 600 675

Total Assets 4,470 8,070

Less: Current Liabilities 645 2,220

B. Capital employed 3,825 5,850

ROCE (A/B) 16% 12%

ii) Net Profit Margin

The net profit margin is equal to the amount of net profit or derived gain as an income level. Net

income is the proportion of net benefits to income for an organization or business sector. Net

income is usually translated as a rate, but it can also be treated in a decimal structure. Net income

represents the amount of every dollar of income an organization collects turns into profit.

Similarly, net profit is declared as a group event or a net benefit. Net income is referred to as net

margin. The term net benefits is equivalent to full compensation for payment bonuses and the

other term may be used (Kadim, Sunardi and Husain, 2020).

2018 2019

A. Net Profit 600 675

B. Net Sales 4,800 6,000

Net Profit Margin

(A/B) 13% 11%

iii) Current Ratio

The current ratio is a liquidity allowance that measures an organization's ability to pay non-

transferable commitments or those due within one year. It tells speculators and researchers how

a. Calculation of Ratios

i) Return on capital employed

Return on capital employed (ROCE) is a percentage of money that can be used to measure the

productivity and profitability of an organization's capital. Overall, the contribution can help

determine the extent to which an organization is benefiting from its capital. The ROCE

allowance is one of the few benefit allowances that administrators, partners, and financial experts

can use when verifying the profitability of an organization (Zorn, and et.al., 2018).

2018 2019

A. EBIT 600 675

Total Assets 4,470 8,070

Less: Current Liabilities 645 2,220

B. Capital employed 3,825 5,850

ROCE (A/B) 16% 12%

ii) Net Profit Margin

The net profit margin is equal to the amount of net profit or derived gain as an income level. Net

income is the proportion of net benefits to income for an organization or business sector. Net

income is usually translated as a rate, but it can also be treated in a decimal structure. Net income

represents the amount of every dollar of income an organization collects turns into profit.

Similarly, net profit is declared as a group event or a net benefit. Net income is referred to as net

margin. The term net benefits is equivalent to full compensation for payment bonuses and the

other term may be used (Kadim, Sunardi and Husain, 2020).

2018 2019

A. Net Profit 600 675

B. Net Sales 4,800 6,000

Net Profit Margin

(A/B) 13% 11%

iii) Current Ratio

The current ratio is a liquidity allowance that measures an organization's ability to pay non-

transferable commitments or those due within one year. It tells speculators and researchers how

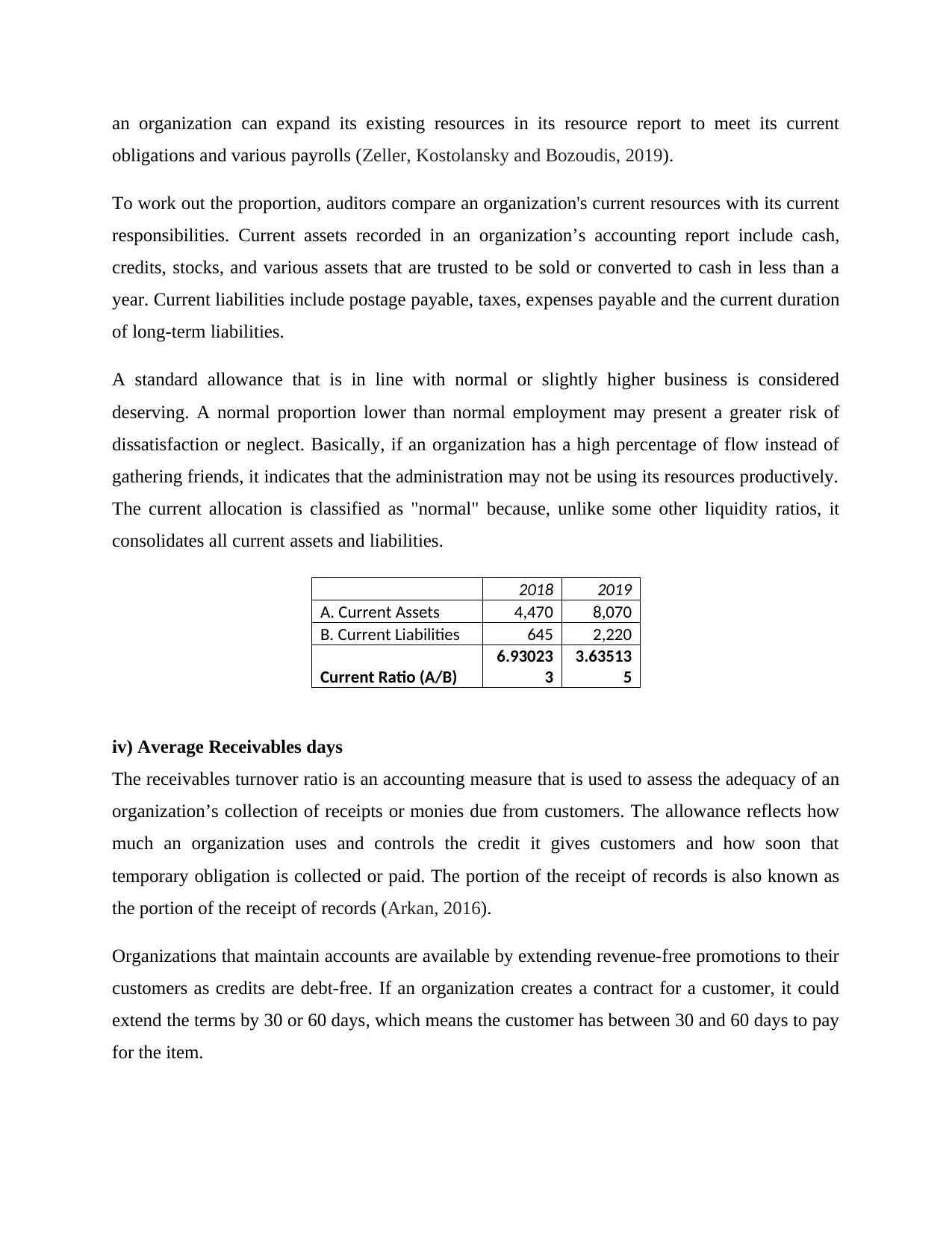

an organization can expand its existing resources in its resource report to meet its current

obligations and various payrolls (Zeller, Kostolansky and Bozoudis, 2019).

To work out the proportion, auditors compare an organization's current resources with its current

responsibilities. Current assets recorded in an organization’s accounting report include cash,

credits, stocks, and various assets that are trusted to be sold or converted to cash in less than a

year. Current liabilities include postage payable, taxes, expenses payable and the current duration

of long-term liabilities.

A standard allowance that is in line with normal or slightly higher business is considered

deserving. A normal proportion lower than normal employment may present a greater risk of

dissatisfaction or neglect. Basically, if an organization has a high percentage of flow instead of

gathering friends, it indicates that the administration may not be using its resources productively.

The current allocation is classified as "normal" because, unlike some other liquidity ratios, it

consolidates all current assets and liabilities.

2018 2019

A. Current Assets 4,470 8,070

B. Current Liabilities 645 2,220

Current Ratio (A/B)

6.93023

3

3.63513

5

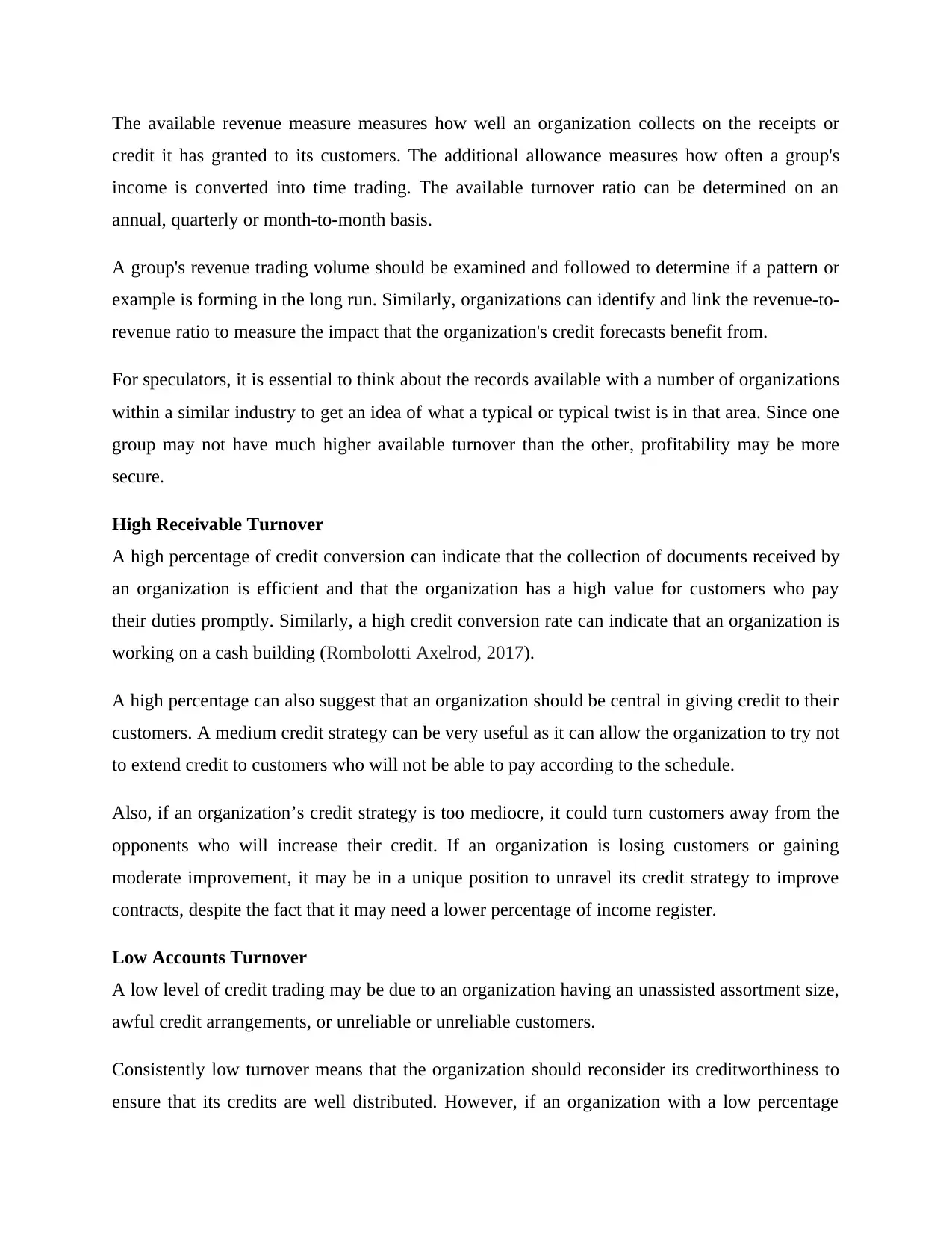

iv) Average Receivables days

The receivables turnover ratio is an accounting measure that is used to assess the adequacy of an

organization’s collection of receipts or monies due from customers. The allowance reflects how

much an organization uses and controls the credit it gives customers and how soon that

temporary obligation is collected or paid. The portion of the receipt of records is also known as

the portion of the receipt of records (Arkan, 2016).

Organizations that maintain accounts are available by extending revenue-free promotions to their

customers as credits are debt-free. If an organization creates a contract for a customer, it could

extend the terms by 30 or 60 days, which means the customer has between 30 and 60 days to pay

for the item.

obligations and various payrolls (Zeller, Kostolansky and Bozoudis, 2019).

To work out the proportion, auditors compare an organization's current resources with its current

responsibilities. Current assets recorded in an organization’s accounting report include cash,

credits, stocks, and various assets that are trusted to be sold or converted to cash in less than a

year. Current liabilities include postage payable, taxes, expenses payable and the current duration

of long-term liabilities.

A standard allowance that is in line with normal or slightly higher business is considered

deserving. A normal proportion lower than normal employment may present a greater risk of

dissatisfaction or neglect. Basically, if an organization has a high percentage of flow instead of

gathering friends, it indicates that the administration may not be using its resources productively.

The current allocation is classified as "normal" because, unlike some other liquidity ratios, it

consolidates all current assets and liabilities.

2018 2019

A. Current Assets 4,470 8,070

B. Current Liabilities 645 2,220

Current Ratio (A/B)

6.93023

3

3.63513

5

iv) Average Receivables days

The receivables turnover ratio is an accounting measure that is used to assess the adequacy of an

organization’s collection of receipts or monies due from customers. The allowance reflects how

much an organization uses and controls the credit it gives customers and how soon that

temporary obligation is collected or paid. The portion of the receipt of records is also known as

the portion of the receipt of records (Arkan, 2016).

Organizations that maintain accounts are available by extending revenue-free promotions to their

customers as credits are debt-free. If an organization creates a contract for a customer, it could

extend the terms by 30 or 60 days, which means the customer has between 30 and 60 days to pay

for the item.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The available revenue measure measures how well an organization collects on the receipts or

credit it has granted to its customers. The additional allowance measures how often a group's

income is converted into time trading. The available turnover ratio can be determined on an

annual, quarterly or month-to-month basis.

A group's revenue trading volume should be examined and followed to determine if a pattern or

example is forming in the long run. Similarly, organizations can identify and link the revenue-to-

revenue ratio to measure the impact that the organization's credit forecasts benefit from.

For speculators, it is essential to think about the records available with a number of organizations

within a similar industry to get an idea of what a typical or typical twist is in that area. Since one

group may not have much higher available turnover than the other, profitability may be more

secure.

High Receivable Turnover

A high percentage of credit conversion can indicate that the collection of documents received by

an organization is efficient and that the organization has a high value for customers who pay

their duties promptly. Similarly, a high credit conversion rate can indicate that an organization is

working on a cash building (Rombolotti Axelrod, 2017).

A high percentage can also suggest that an organization should be central in giving credit to their

customers. A medium credit strategy can be very useful as it can allow the organization to try not

to extend credit to customers who will not be able to pay according to the schedule.

Also, if an organization’s credit strategy is too mediocre, it could turn customers away from the

opponents who will increase their credit. If an organization is losing customers or gaining

moderate improvement, it may be in a unique position to unravel its credit strategy to improve

contracts, despite the fact that it may need a lower percentage of income register.

Low Accounts Turnover

A low level of credit trading may be due to an organization having an unassisted assortment size,

awful credit arrangements, or unreliable or unreliable customers.

Consistently low turnover means that the organization should reconsider its creditworthiness to

ensure that its credits are well distributed. However, if an organization with a low percentage

credit it has granted to its customers. The additional allowance measures how often a group's

income is converted into time trading. The available turnover ratio can be determined on an

annual, quarterly or month-to-month basis.

A group's revenue trading volume should be examined and followed to determine if a pattern or

example is forming in the long run. Similarly, organizations can identify and link the revenue-to-

revenue ratio to measure the impact that the organization's credit forecasts benefit from.

For speculators, it is essential to think about the records available with a number of organizations

within a similar industry to get an idea of what a typical or typical twist is in that area. Since one

group may not have much higher available turnover than the other, profitability may be more

secure.

High Receivable Turnover

A high percentage of credit conversion can indicate that the collection of documents received by

an organization is efficient and that the organization has a high value for customers who pay

their duties promptly. Similarly, a high credit conversion rate can indicate that an organization is

working on a cash building (Rombolotti Axelrod, 2017).

A high percentage can also suggest that an organization should be central in giving credit to their

customers. A medium credit strategy can be very useful as it can allow the organization to try not

to extend credit to customers who will not be able to pay according to the schedule.

Also, if an organization’s credit strategy is too mediocre, it could turn customers away from the

opponents who will increase their credit. If an organization is losing customers or gaining

moderate improvement, it may be in a unique position to unravel its credit strategy to improve

contracts, despite the fact that it may need a lower percentage of income register.

Low Accounts Turnover

A low level of credit trading may be due to an organization having an unassisted assortment size,

awful credit arrangements, or unreliable or unreliable customers.

Consistently low turnover means that the organization should reconsider its creditworthiness to

ensure that its credits are well distributed. However, if an organization with a low percentage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

improves its restriction cycle, it can collect money from collecting old beliefs or credentials

(Rombolotti Axelrod, 2017).

2018 2019

A. Average receivables 900 1200

B. Net Sales 4800 6000

Average Receivable

days ((A/B) * 365) 68.4375 73

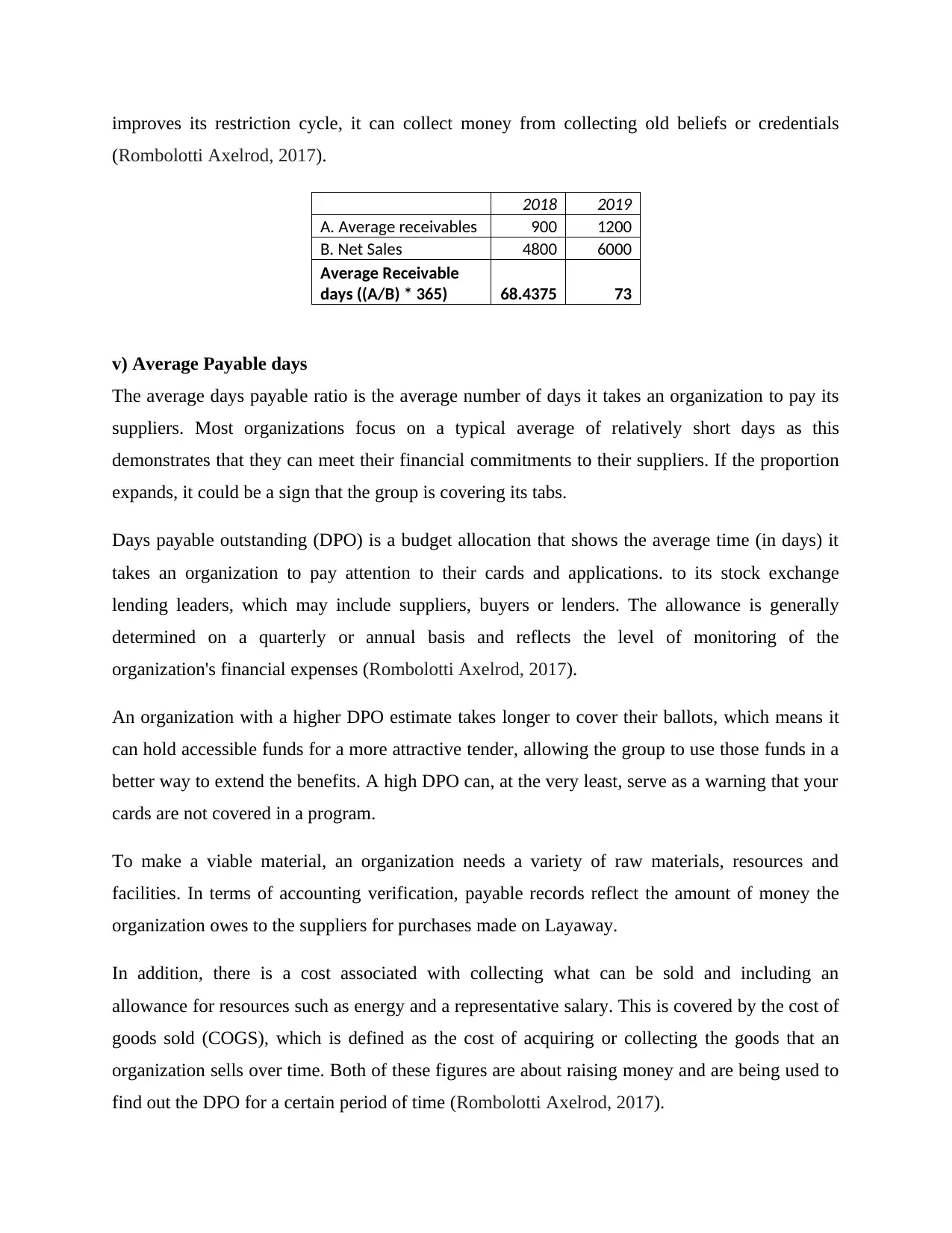

v) Average Payable days

The average days payable ratio is the average number of days it takes an organization to pay its

suppliers. Most organizations focus on a typical average of relatively short days as this

demonstrates that they can meet their financial commitments to their suppliers. If the proportion

expands, it could be a sign that the group is covering its tabs.

Days payable outstanding (DPO) is a budget allocation that shows the average time (in days) it

takes an organization to pay attention to their cards and applications. to its stock exchange

lending leaders, which may include suppliers, buyers or lenders. The allowance is generally

determined on a quarterly or annual basis and reflects the level of monitoring of the

organization's financial expenses (Rombolotti Axelrod, 2017).

An organization with a higher DPO estimate takes longer to cover their ballots, which means it

can hold accessible funds for a more attractive tender, allowing the group to use those funds in a

better way to extend the benefits. A high DPO can, at the very least, serve as a warning that your

cards are not covered in a program.

To make a viable material, an organization needs a variety of raw materials, resources and

facilities. In terms of accounting verification, payable records reflect the amount of money the

organization owes to the suppliers for purchases made on Layaway.

In addition, there is a cost associated with collecting what can be sold and including an

allowance for resources such as energy and a representative salary. This is covered by the cost of

goods sold (COGS), which is defined as the cost of acquiring or collecting the goods that an

organization sells over time. Both of these figures are about raising money and are being used to

find out the DPO for a certain period of time (Rombolotti Axelrod, 2017).

(Rombolotti Axelrod, 2017).

2018 2019

A. Average receivables 900 1200

B. Net Sales 4800 6000

Average Receivable

days ((A/B) * 365) 68.4375 73

v) Average Payable days

The average days payable ratio is the average number of days it takes an organization to pay its

suppliers. Most organizations focus on a typical average of relatively short days as this

demonstrates that they can meet their financial commitments to their suppliers. If the proportion

expands, it could be a sign that the group is covering its tabs.

Days payable outstanding (DPO) is a budget allocation that shows the average time (in days) it

takes an organization to pay attention to their cards and applications. to its stock exchange

lending leaders, which may include suppliers, buyers or lenders. The allowance is generally

determined on a quarterly or annual basis and reflects the level of monitoring of the

organization's financial expenses (Rombolotti Axelrod, 2017).

An organization with a higher DPO estimate takes longer to cover their ballots, which means it

can hold accessible funds for a more attractive tender, allowing the group to use those funds in a

better way to extend the benefits. A high DPO can, at the very least, serve as a warning that your

cards are not covered in a program.

To make a viable material, an organization needs a variety of raw materials, resources and

facilities. In terms of accounting verification, payable records reflect the amount of money the

organization owes to the suppliers for purchases made on Layaway.

In addition, there is a cost associated with collecting what can be sold and including an

allowance for resources such as energy and a representative salary. This is covered by the cost of

goods sold (COGS), which is defined as the cost of acquiring or collecting the goods that an

organization sells over time. Both of these figures are about raising money and are being used to

find out the DPO for a certain period of time (Rombolotti Axelrod, 2017).

It is generally accepted that the number of days in the relevant timeframe is 365 for a year and 90

for a quarter. The recipe estimates the organization’s normal daily cost of selling something. The

figure speaks for large proportions. The net factor gives the normal number of days it takes for

the organization to fulfill its promises after receiving bills.

Two distinct variations of the DPO recipe are used based on accounting evidence. In one of the

changes, the amount payable in the records is considered to be the exact figure towards the end

of the accounting period, such as near the end of the financial year / quarter ended 30 September.

This form refers to the DPO's estimate "at" the reference date (Rombolotti Axelrod, 2017).

2018 2019

A. Average Payables 570 2,100

B. COGS 3,450 4,350

Average Payable

days ((A/B) * 365)

60.3043

5

176.206

9

b. Results

i. The result of capital employed shows that it has been declined as compared with 2018 due to

less increment in EBIT as compared to Capital employed. Due to this gap; return on capital

employed has decreased in 2019 and hence, indicates bad performance by the company.

ii. Net Profit Margin of the company has also declined from 2018 to 2019, due to increase in

Cost of sales more than sales revenue. This indicates bad performance of the company.

iii. Current Ratio has also declined in 2019, due to increase in current liabilities. This indicates

good efficiency of the company to manage its funds.

iv. Average receivables in days are increased in 2019; this indicates bad credit policy of the

company in 2019 to return its payment back to the business from debtors.

v. Average payables in days are also increased upto 3 times of 2018. This is good from business

prospective; but from market point of view, it could result in bad image of the company (Rey and

Santelli, 2017).

for a quarter. The recipe estimates the organization’s normal daily cost of selling something. The

figure speaks for large proportions. The net factor gives the normal number of days it takes for

the organization to fulfill its promises after receiving bills.

Two distinct variations of the DPO recipe are used based on accounting evidence. In one of the

changes, the amount payable in the records is considered to be the exact figure towards the end

of the accounting period, such as near the end of the financial year / quarter ended 30 September.

This form refers to the DPO's estimate "at" the reference date (Rombolotti Axelrod, 2017).

2018 2019

A. Average Payables 570 2,100

B. COGS 3,450 4,350

Average Payable

days ((A/B) * 365)

60.3043

5

176.206

9

b. Results

i. The result of capital employed shows that it has been declined as compared with 2018 due to

less increment in EBIT as compared to Capital employed. Due to this gap; return on capital

employed has decreased in 2019 and hence, indicates bad performance by the company.

ii. Net Profit Margin of the company has also declined from 2018 to 2019, due to increase in

Cost of sales more than sales revenue. This indicates bad performance of the company.

iii. Current Ratio has also declined in 2019, due to increase in current liabilities. This indicates

good efficiency of the company to manage its funds.

iv. Average receivables in days are increased in 2019; this indicates bad credit policy of the

company in 2019 to return its payment back to the business from debtors.

v. Average payables in days are also increased upto 3 times of 2018. This is good from business

prospective; but from market point of view, it could result in bad image of the company (Rey and

Santelli, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.