FIN 7040 - Financial Decision Making: ABC Consulting LLP Case Study

VerifiedAdded on 2023/06/09

|18

|4805

|400

Case Study

AI Summary

This report evaluates the financial condition and investment appraisal policy of ABC Consulting LLP, a UK-based consultancy. Financial ratios indicate a decline in performance in 2018 due to falling market revenue, though the US subsidiary showed improvement, prompting an expansion plan. The management's forecasts, while subject to limitations, support the expansion. Investment appraisal techniques suggest accepting the project to maximize return on investment and profitability, with funding primarily from equity and less from debt. Non-financial factors should also be considered before finalizing the investment proposal. Desklib provides access to similar case studies and solved assignments for students.

Running head: FINANCIAL DECISION MAKING

Programme MSc Management

Module name Financial Decision Making

QAA Level 7

Schedule Term Summer Term 2018

Student Reference Number (SRN)

Report/Assignment Title CASE STUDY – ABC CONSULTING LLP

Date of Submission

(Please attach the confirmation of

any extension received)

Declaration of Original Work:

I hereby declare that I have read and understood BPP’s regulations on plagiarism and that

this is my original work, researched, undertaken, completed and submitted in accordance

with the requirements of BPP Business School.

The word count, excluding contents table, bibliography and appendices, is ___ words.

Student Reference Number: ___________ Date: __________

By submitting this coursework you agree to all rules and regulations of BPP regarding

assessments and awards for programmes. Please note, submission is your declaration you

are fit to sit.

BPP University reserves the right to use all submitted work for educational purposes and may

request that work be published for a wider audience.

BPP Business School

Programme MSc Management

Module name Financial Decision Making

QAA Level 7

Schedule Term Summer Term 2018

Student Reference Number (SRN)

Report/Assignment Title CASE STUDY – ABC CONSULTING LLP

Date of Submission

(Please attach the confirmation of

any extension received)

Declaration of Original Work:

I hereby declare that I have read and understood BPP’s regulations on plagiarism and that

this is my original work, researched, undertaken, completed and submitted in accordance

with the requirements of BPP Business School.

The word count, excluding contents table, bibliography and appendices, is ___ words.

Student Reference Number: ___________ Date: __________

By submitting this coursework you agree to all rules and regulations of BPP regarding

assessments and awards for programmes. Please note, submission is your declaration you

are fit to sit.

BPP University reserves the right to use all submitted work for educational purposes and may

request that work be published for a wider audience.

BPP Business School

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL DECISION MAKING

Financial Decision Making

[FIN 7040]

Author’s Note:

Financial Decision Making

[FIN 7040]

Author’s Note:

2FINANCIAL DECISION MAKING

Table of Contents

Executive Summary:..................................................................................................................3

Part 1: Business Performance Analysis......................................................................................4

1.1 Statement of Profit or Loss:.............................................................................................4

1.2 Statement of Financial Position:......................................................................................6

1.3 Statement of Cash Flows:...............................................................................................11

1.4 Segmental Analysis:.......................................................................................................13

Part 2: Investment Appraisal and Sources of Finance.............................................................14

2.1 Investment Appraisal:....................................................................................................14

2.1.1 Management Forecast:............................................................................................14

2.1.2 Investment Appraisal Techniques:..........................................................................14

2.1.3 Payback Period:.......................................................................................................15

2.1.4 Accounting Rate of Return:....................................................................................15

2.1.5 Net Present Value:...................................................................................................15

2.2 Sources of Finance:........................................................................................................16

2.3 Non-Financial Factors:...................................................................................................16

References:...............................................................................................................................17

Table of Contents

Executive Summary:..................................................................................................................3

Part 1: Business Performance Analysis......................................................................................4

1.1 Statement of Profit or Loss:.............................................................................................4

1.2 Statement of Financial Position:......................................................................................6

1.3 Statement of Cash Flows:...............................................................................................11

1.4 Segmental Analysis:.......................................................................................................13

Part 2: Investment Appraisal and Sources of Finance.............................................................14

2.1 Investment Appraisal:....................................................................................................14

2.1.1 Management Forecast:............................................................................................14

2.1.2 Investment Appraisal Techniques:..........................................................................14

2.1.3 Payback Period:.......................................................................................................15

2.1.4 Accounting Rate of Return:....................................................................................15

2.1.5 Net Present Value:...................................................................................................15

2.2 Sources of Finance:........................................................................................................16

2.3 Non-Financial Factors:...................................................................................................16

References:...............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL DECISION MAKING

Executive Summary:

The current report deals with evaluating the financial condition and investment

appraisal policy of ABC Consulting LLP, which is an UK based organisation providing

consultancy services in UK, US and Australia. From the various financial ratios computed, it

has been found that the organisation has experienced a decline in its performance and

position in 2018 compared to the previous year due to the significant fall in market revenue

owing to declining market demand. However, performance improvements could be observed

in its US subsidiary, due to which it has planned to make an expansion plan in the project.

In order to conduct the expansion plan, the management of ABC Consulting LLP has

made certain forecasts, which are subject to certain limitations. The most significant

limitation is that since forecasts are based on assumptions, any decision taken might not be

irreversible in future. By using the various investment appraisal techniques, it has been

advised to the management of the organisation to accept the project, as the assumptions made

would help in maximising their overall return on investment and profitability. Moreover, in

order to raise funds for the expansion program, it is advised to raise maximum funds from

equity and lower funds from debt. Finally, ABC Consulting LLP needs to take into account

certain non-financial factors for arriving at the final decision before undertaking the

investment proposal.

Executive Summary:

The current report deals with evaluating the financial condition and investment

appraisal policy of ABC Consulting LLP, which is an UK based organisation providing

consultancy services in UK, US and Australia. From the various financial ratios computed, it

has been found that the organisation has experienced a decline in its performance and

position in 2018 compared to the previous year due to the significant fall in market revenue

owing to declining market demand. However, performance improvements could be observed

in its US subsidiary, due to which it has planned to make an expansion plan in the project.

In order to conduct the expansion plan, the management of ABC Consulting LLP has

made certain forecasts, which are subject to certain limitations. The most significant

limitation is that since forecasts are based on assumptions, any decision taken might not be

irreversible in future. By using the various investment appraisal techniques, it has been

advised to the management of the organisation to accept the project, as the assumptions made

would help in maximising their overall return on investment and profitability. Moreover, in

order to raise funds for the expansion program, it is advised to raise maximum funds from

equity and lower funds from debt. Finally, ABC Consulting LLP needs to take into account

certain non-financial factors for arriving at the final decision before undertaking the

investment proposal.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL DECISION MAKING

Part 1: Business Performance Analysis

The report would deal with analysing the business performance of ABC Consulting

LLP, which is a reputed organisation providing professional services in London, UK. It

operates as a limited liability partnership since 2001 and it has gained popularity for being a

popular provider of consultancy support for aiding in transforming businesses operating in

different industrial sectors. In order to conduct its business performance analysis, ratio

analysis is deemed fit for the purpose to analyse its various financial statements like income

statement, balance sheet statement and cash flow statement.

1.1 Statement of Profit or Loss:

By using Exhibit 1 provided in the case study, the statement of profit or loss of ABC

Consulting LLP has been evaluated with the help of the following ratios, which are

demonstrated briefly as follows:

Table 1: Profitability ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

Part 1: Business Performance Analysis

The report would deal with analysing the business performance of ABC Consulting

LLP, which is a reputed organisation providing professional services in London, UK. It

operates as a limited liability partnership since 2001 and it has gained popularity for being a

popular provider of consultancy support for aiding in transforming businesses operating in

different industrial sectors. In order to conduct its business performance analysis, ratio

analysis is deemed fit for the purpose to analyse its various financial statements like income

statement, balance sheet statement and cash flow statement.

1.1 Statement of Profit or Loss:

By using Exhibit 1 provided in the case study, the statement of profit or loss of ABC

Consulting LLP has been evaluated with the help of the following ratios, which are

demonstrated briefly as follows:

Table 1: Profitability ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

5FINANCIAL DECISION MAKING

Net margin Return on

capital

employed

(ROCE)

Return on

equity (ROE) Operating

margin

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

160.00%

Profitability Ratios

2017

2018

Percent change

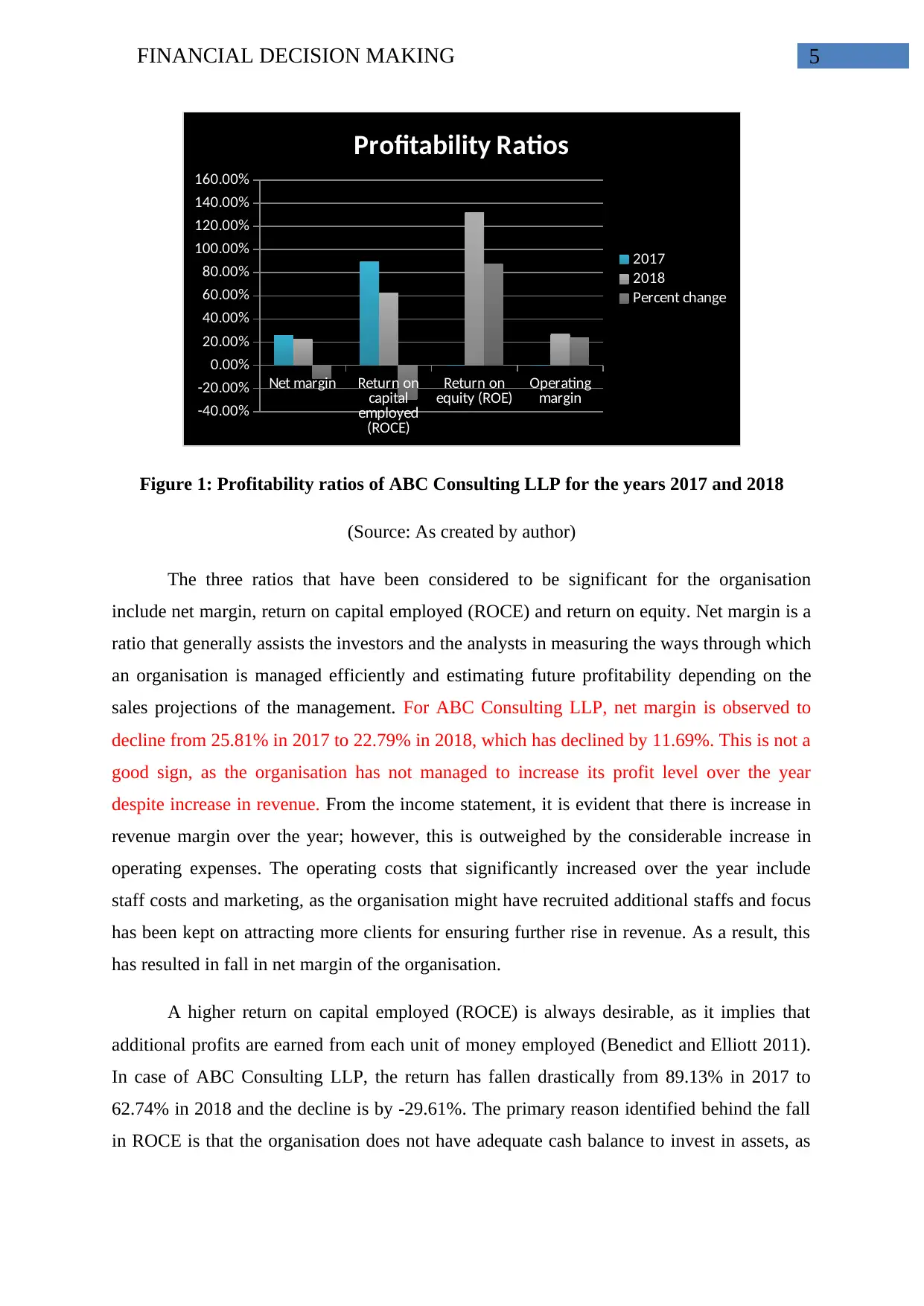

Figure 1: Profitability ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

The three ratios that have been considered to be significant for the organisation

include net margin, return on capital employed (ROCE) and return on equity. Net margin is a

ratio that generally assists the investors and the analysts in measuring the ways through which

an organisation is managed efficiently and estimating future profitability depending on the

sales projections of the management. For ABC Consulting LLP, net margin is observed to

decline from 25.81% in 2017 to 22.79% in 2018, which has declined by 11.69%. This is not a

good sign, as the organisation has not managed to increase its profit level over the year

despite increase in revenue. From the income statement, it is evident that there is increase in

revenue margin over the year; however, this is outweighed by the considerable increase in

operating expenses. The operating costs that significantly increased over the year include

staff costs and marketing, as the organisation might have recruited additional staffs and focus

has been kept on attracting more clients for ensuring further rise in revenue. As a result, this

has resulted in fall in net margin of the organisation.

A higher return on capital employed (ROCE) is always desirable, as it implies that

additional profits are earned from each unit of money employed (Benedict and Elliott 2011).

In case of ABC Consulting LLP, the return has fallen drastically from 89.13% in 2017 to

62.74% in 2018 and the decline is by -29.61%. The primary reason identified behind the fall

in ROCE is that the organisation does not have adequate cash balance to invest in assets, as

Net margin Return on

capital

employed

(ROCE)

Return on

equity (ROE) Operating

margin

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

160.00%

Profitability Ratios

2017

2018

Percent change

Figure 1: Profitability ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

The three ratios that have been considered to be significant for the organisation

include net margin, return on capital employed (ROCE) and return on equity. Net margin is a

ratio that generally assists the investors and the analysts in measuring the ways through which

an organisation is managed efficiently and estimating future profitability depending on the

sales projections of the management. For ABC Consulting LLP, net margin is observed to

decline from 25.81% in 2017 to 22.79% in 2018, which has declined by 11.69%. This is not a

good sign, as the organisation has not managed to increase its profit level over the year

despite increase in revenue. From the income statement, it is evident that there is increase in

revenue margin over the year; however, this is outweighed by the considerable increase in

operating expenses. The operating costs that significantly increased over the year include

staff costs and marketing, as the organisation might have recruited additional staffs and focus

has been kept on attracting more clients for ensuring further rise in revenue. As a result, this

has resulted in fall in net margin of the organisation.

A higher return on capital employed (ROCE) is always desirable, as it implies that

additional profits are earned from each unit of money employed (Benedict and Elliott 2011).

In case of ABC Consulting LLP, the return has fallen drastically from 89.13% in 2017 to

62.74% in 2018 and the decline is by -29.61%. The primary reason identified behind the fall

in ROCE is that the organisation does not have adequate cash balance to invest in assets, as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL DECISION MAKING

they are utilised for settling off the existing dues and obligations. If this ratio is declining, it is

an early signal for the investors to sell the shares that they hold in order to avoid losses.

Return on equity (ROE) gauges the efficacy of an organisation in using the money

from the shareholders for generating profits along with ensuring business growth (McClaney

and Atrill 2014). In case of ABC Consulting LLP, the ROE of the organisation has fallen

from 132.19% in 2017 to 87.23% in 2018 and the decline is by 34.01%. This implies for

every pound of shareholders’ equity, earnings have been £1.32 in 2017 and £0.87 in 2018.

This ratio is considered to be significantly high for the organisation, even though decline

could be observed in the current year. Thus, ABC Consulting LLP has managed a stable

growth over the years. Finally, operating margin has fallen by 10.45% in 2018 due to the rise

in operating costs and hence, adequate profit level is not maintained despite the rise in

revenue in 2018.

Based on the above evaluation, it could be stated that the organisation is experiencing

decline in its profitability aspect.

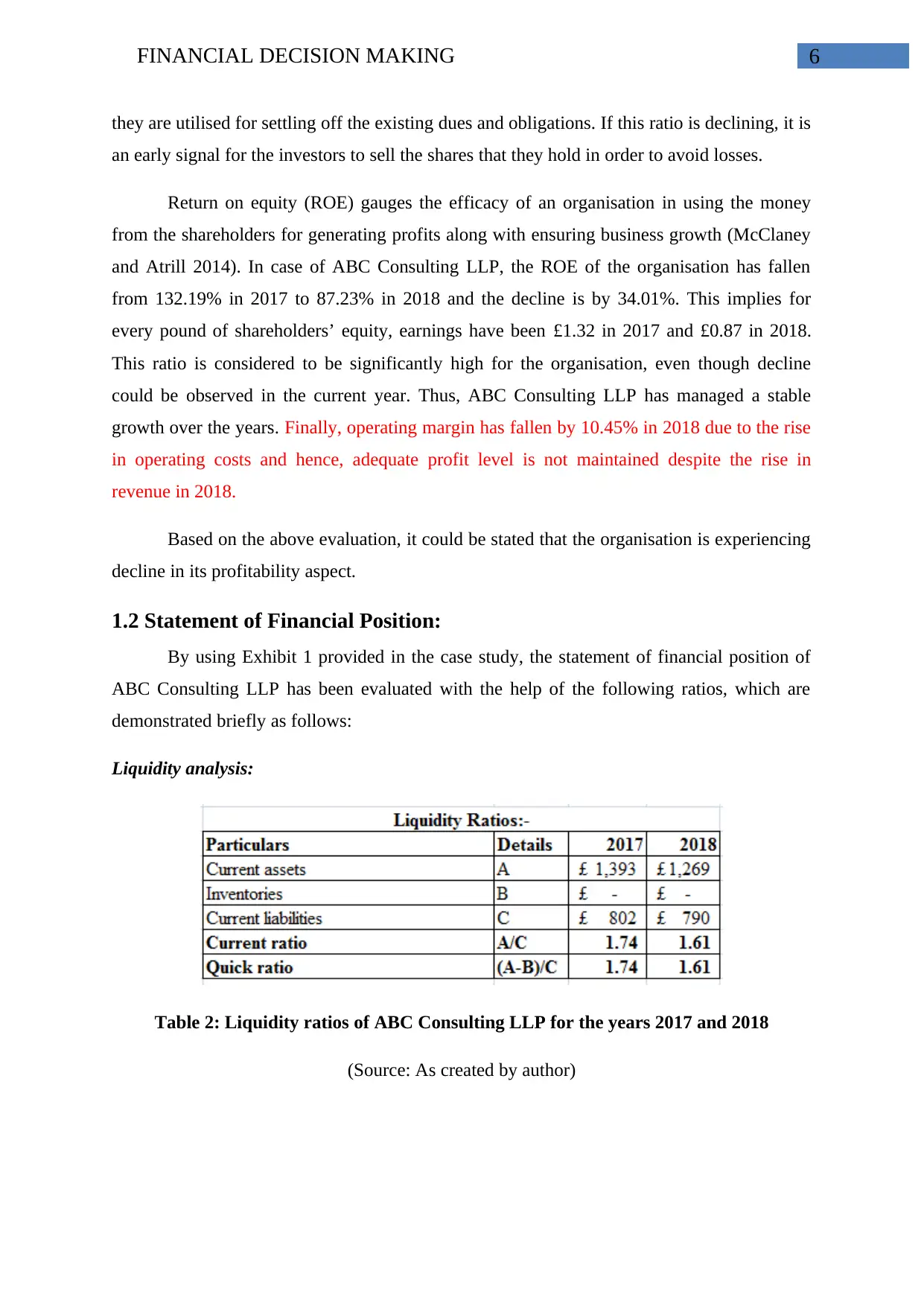

1.2 Statement of Financial Position:

By using Exhibit 1 provided in the case study, the statement of financial position of

ABC Consulting LLP has been evaluated with the help of the following ratios, which are

demonstrated briefly as follows:

Liquidity analysis:

Table 2: Liquidity ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

they are utilised for settling off the existing dues and obligations. If this ratio is declining, it is

an early signal for the investors to sell the shares that they hold in order to avoid losses.

Return on equity (ROE) gauges the efficacy of an organisation in using the money

from the shareholders for generating profits along with ensuring business growth (McClaney

and Atrill 2014). In case of ABC Consulting LLP, the ROE of the organisation has fallen

from 132.19% in 2017 to 87.23% in 2018 and the decline is by 34.01%. This implies for

every pound of shareholders’ equity, earnings have been £1.32 in 2017 and £0.87 in 2018.

This ratio is considered to be significantly high for the organisation, even though decline

could be observed in the current year. Thus, ABC Consulting LLP has managed a stable

growth over the years. Finally, operating margin has fallen by 10.45% in 2018 due to the rise

in operating costs and hence, adequate profit level is not maintained despite the rise in

revenue in 2018.

Based on the above evaluation, it could be stated that the organisation is experiencing

decline in its profitability aspect.

1.2 Statement of Financial Position:

By using Exhibit 1 provided in the case study, the statement of financial position of

ABC Consulting LLP has been evaluated with the help of the following ratios, which are

demonstrated briefly as follows:

Liquidity analysis:

Table 2: Liquidity ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL DECISION MAKING

2017 2018

1.50

1.55

1.60

1.65

1.70

1.75 1.74

1.61

1.74

1.61

Liquidity Ratios

Current ratio

Quick ratio

Figure 2: Liquidity ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

From the above figure, both current ratio and quick ratio have identical figures, as

both the ratios have declined from 1.74 in 2017 to 1.61 in 2018. The ideal current ratio is

considered as 2, while the ideal quick ratio is considered as 1. The two ratios have remained

identical due to the fact that the organisation does not maintain any inventory or incur prepaid

expenses in conducting its business operations (Collier 2015). These two ratios help in

measuring the liquidity position of an organisation by assessing its efficiency in clearing off

its short-term dues with the existing short-term asset base available. Since the quick ratio is

above 1, it denotes that ABC Consulting LLP has huge amount of idle working capital, which

has remained unutilised, since trade receivables are observed to increase from £1,179 in 2017

to £1,194 in 2018. However, there is significant decline in cash balance over the year from

£214 in 2017 to £75 in 2018, due to which a slight decline could be observed in 2018.

Hence, in terms of liquidity, ABC Consulting LLP is not placed in a favourable

position due to the declining trend of current ratio and quick ratio owing to huge amount of

idle cash stuck in the hands of the clients.

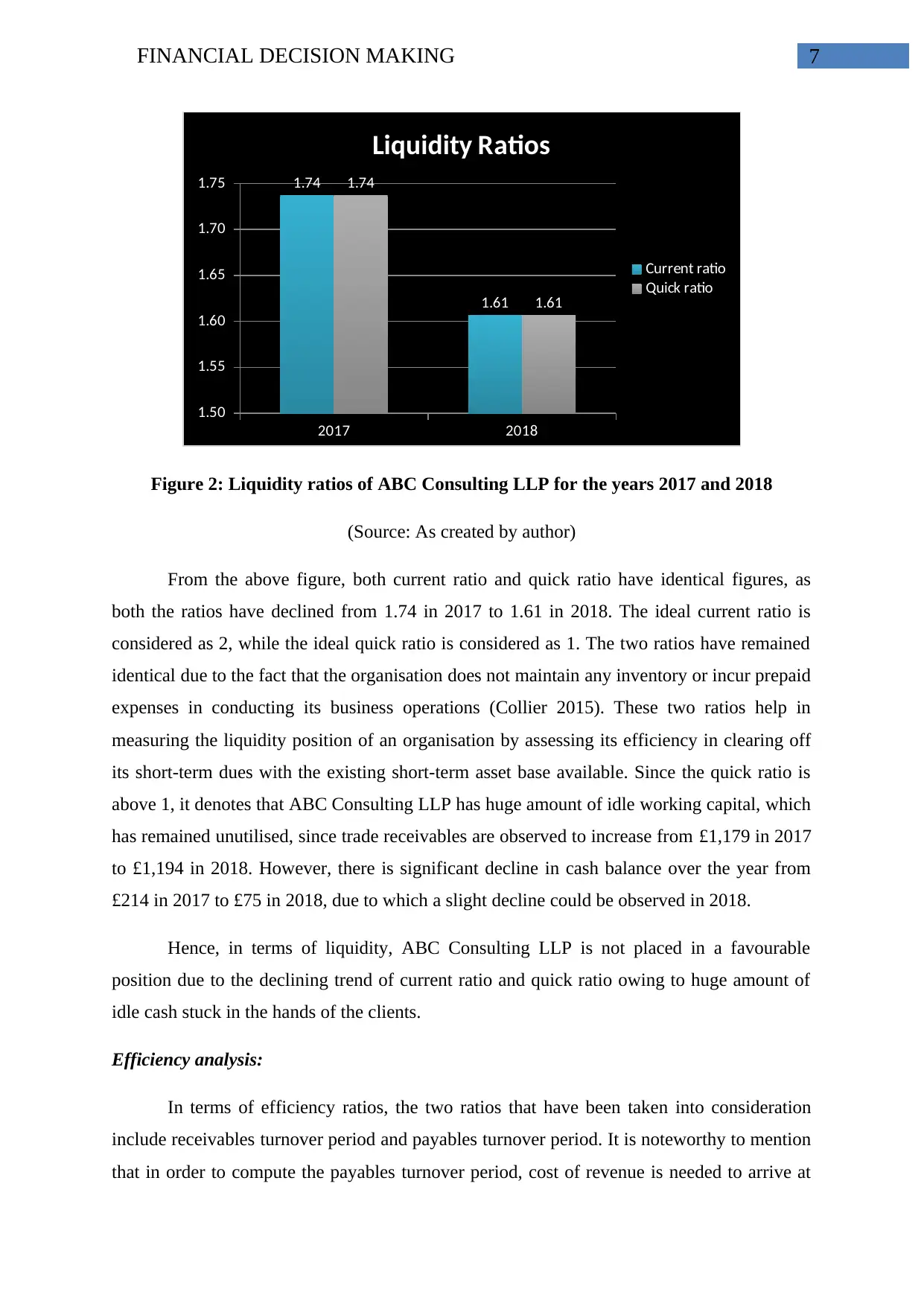

Efficiency analysis:

In terms of efficiency ratios, the two ratios that have been taken into consideration

include receivables turnover period and payables turnover period. It is noteworthy to mention

that in order to compute the payables turnover period, cost of revenue is needed to arrive at

2017 2018

1.50

1.55

1.60

1.65

1.70

1.75 1.74

1.61

1.74

1.61

Liquidity Ratios

Current ratio

Quick ratio

Figure 2: Liquidity ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

From the above figure, both current ratio and quick ratio have identical figures, as

both the ratios have declined from 1.74 in 2017 to 1.61 in 2018. The ideal current ratio is

considered as 2, while the ideal quick ratio is considered as 1. The two ratios have remained

identical due to the fact that the organisation does not maintain any inventory or incur prepaid

expenses in conducting its business operations (Collier 2015). These two ratios help in

measuring the liquidity position of an organisation by assessing its efficiency in clearing off

its short-term dues with the existing short-term asset base available. Since the quick ratio is

above 1, it denotes that ABC Consulting LLP has huge amount of idle working capital, which

has remained unutilised, since trade receivables are observed to increase from £1,179 in 2017

to £1,194 in 2018. However, there is significant decline in cash balance over the year from

£214 in 2017 to £75 in 2018, due to which a slight decline could be observed in 2018.

Hence, in terms of liquidity, ABC Consulting LLP is not placed in a favourable

position due to the declining trend of current ratio and quick ratio owing to huge amount of

idle cash stuck in the hands of the clients.

Efficiency analysis:

In terms of efficiency ratios, the two ratios that have been taken into consideration

include receivables turnover period and payables turnover period. It is noteworthy to mention

that in order to compute the payables turnover period, cost of revenue is needed to arrive at

8FINANCIAL DECISION MAKING

the desired figure. However, in case of ABC Consulting LLP, the staffs costs are taken into

consideration as cost of sales for calculating payables turnover period. In addition, inventory

turnover period could not be calculated, as the organisation does not maintain any inventory

level, since it is mainly involved in providing consultancy services (Thomas and Ward 2015).

Therefore, the results of the two ratios computed are illustrated briefly as follows:

Table 3: Efficiency ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

Receivables turnover period (in

days) Payables turnover period (in

days)

-

20

40

60

80

100

120

140 125

82

121

77

Efficiency Ratios

2017

2018

Figure 3: Efficiency ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

From the above figure, it could be clearly seen that there is a slight decline in

receivables turnover period of ABC Consulting LLP from 125 days in 2017 to 121 days in

2018. Receivables collection period gauges the ability of a business organisation to collect

receivables in an efficient manner. A lower period in terms of days is always favourable,

the desired figure. However, in case of ABC Consulting LLP, the staffs costs are taken into

consideration as cost of sales for calculating payables turnover period. In addition, inventory

turnover period could not be calculated, as the organisation does not maintain any inventory

level, since it is mainly involved in providing consultancy services (Thomas and Ward 2015).

Therefore, the results of the two ratios computed are illustrated briefly as follows:

Table 3: Efficiency ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

Receivables turnover period (in

days) Payables turnover period (in

days)

-

20

40

60

80

100

120

140 125

82

121

77

Efficiency Ratios

2017

2018

Figure 3: Efficiency ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

From the above figure, it could be clearly seen that there is a slight decline in

receivables turnover period of ABC Consulting LLP from 125 days in 2017 to 121 days in

2018. Receivables collection period gauges the ability of a business organisation to collect

receivables in an efficient manner. A lower period in terms of days is always favourable,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL DECISION MAKING

since it implies that the organisation is collecting amounts from the debtors more frequently

in a year. For ABC Consulting LLP, it has managed to minimise such period to a certain

extent in 2018, as it huge amount of idle cash stuck with the clients. Moreover, since the sales

are made on credit, ABC Consulting LLP needs to wait 121 days in 2018 to collect the

amount from the debtors from those sales in contrast to 125 days in 2017.

The payables turnover period signifies the capability of an organisation in paying off

its vendors, which is used by the creditors as well as the suppliers to determine whether to

grant credit terms to any business organisation. If the period is higher in terms of days, it

implies that the organisation makes frequent and timely payments to the creditors and the

suppliers. However, clearing the amount before the stipulated time might lead to cash

shortage for the concerned organisation. For ABC Consulting LLP, payables turnover period

is observed to fall from 184 days in 2017 to 171 days, as the creditors are unwilling to extend

their terms due to slight fall in market demand causing the creditors to implement stringent

terms and policies on the organisation.

Thus, in terms of efficiency, ABC Consulting LLP needs to undertake efforts for

minimising the settlement period of debtors to further, since the creditors have reduced their

collection period for receiving payments.

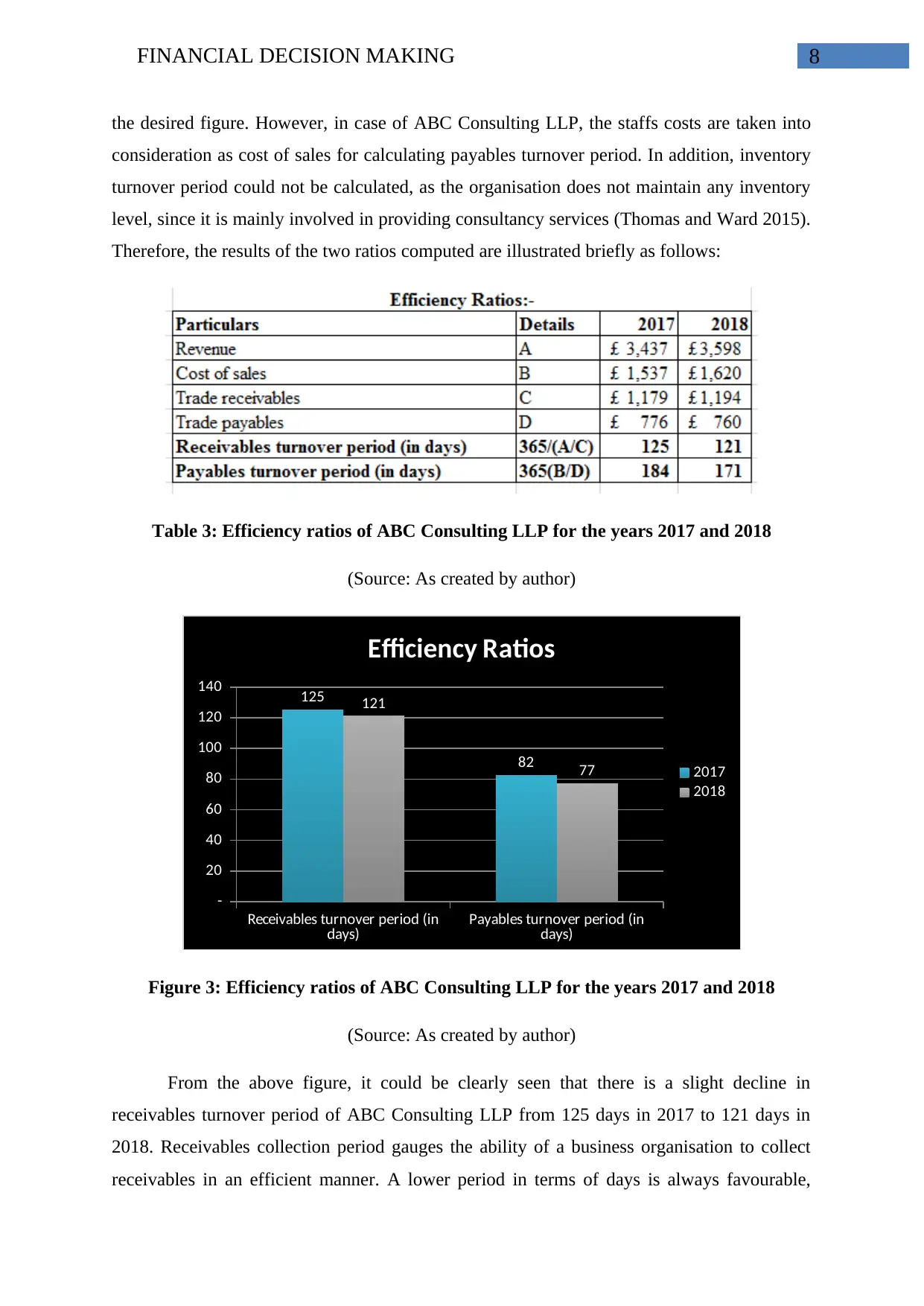

Solvency analysis:

The four ratios that have been chosen to conduct the solvency analysis of ABC

Consulting LLP include debt-to-equity ratio, debt ratio, equity ratio and interest cover ratio

and their detailed calculations are presented as follows:

Table 4: Solvency ratios of ABC Consulting LLP for the years 2017 and 2018

since it implies that the organisation is collecting amounts from the debtors more frequently

in a year. For ABC Consulting LLP, it has managed to minimise such period to a certain

extent in 2018, as it huge amount of idle cash stuck with the clients. Moreover, since the sales

are made on credit, ABC Consulting LLP needs to wait 121 days in 2018 to collect the

amount from the debtors from those sales in contrast to 125 days in 2017.

The payables turnover period signifies the capability of an organisation in paying off

its vendors, which is used by the creditors as well as the suppliers to determine whether to

grant credit terms to any business organisation. If the period is higher in terms of days, it

implies that the organisation makes frequent and timely payments to the creditors and the

suppliers. However, clearing the amount before the stipulated time might lead to cash

shortage for the concerned organisation. For ABC Consulting LLP, payables turnover period

is observed to fall from 184 days in 2017 to 171 days, as the creditors are unwilling to extend

their terms due to slight fall in market demand causing the creditors to implement stringent

terms and policies on the organisation.

Thus, in terms of efficiency, ABC Consulting LLP needs to undertake efforts for

minimising the settlement period of debtors to further, since the creditors have reduced their

collection period for receiving payments.

Solvency analysis:

The four ratios that have been chosen to conduct the solvency analysis of ABC

Consulting LLP include debt-to-equity ratio, debt ratio, equity ratio and interest cover ratio

and their detailed calculations are presented as follows:

Table 4: Solvency ratios of ABC Consulting LLP for the years 2017 and 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL DECISION MAKING

(Source: As created by author)

Debt-to-equity ratio Debt ratio Equity ratio

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1.75

0.64

0.36

1.31

0.57 0.43

Solvency Ratios

2017

2018

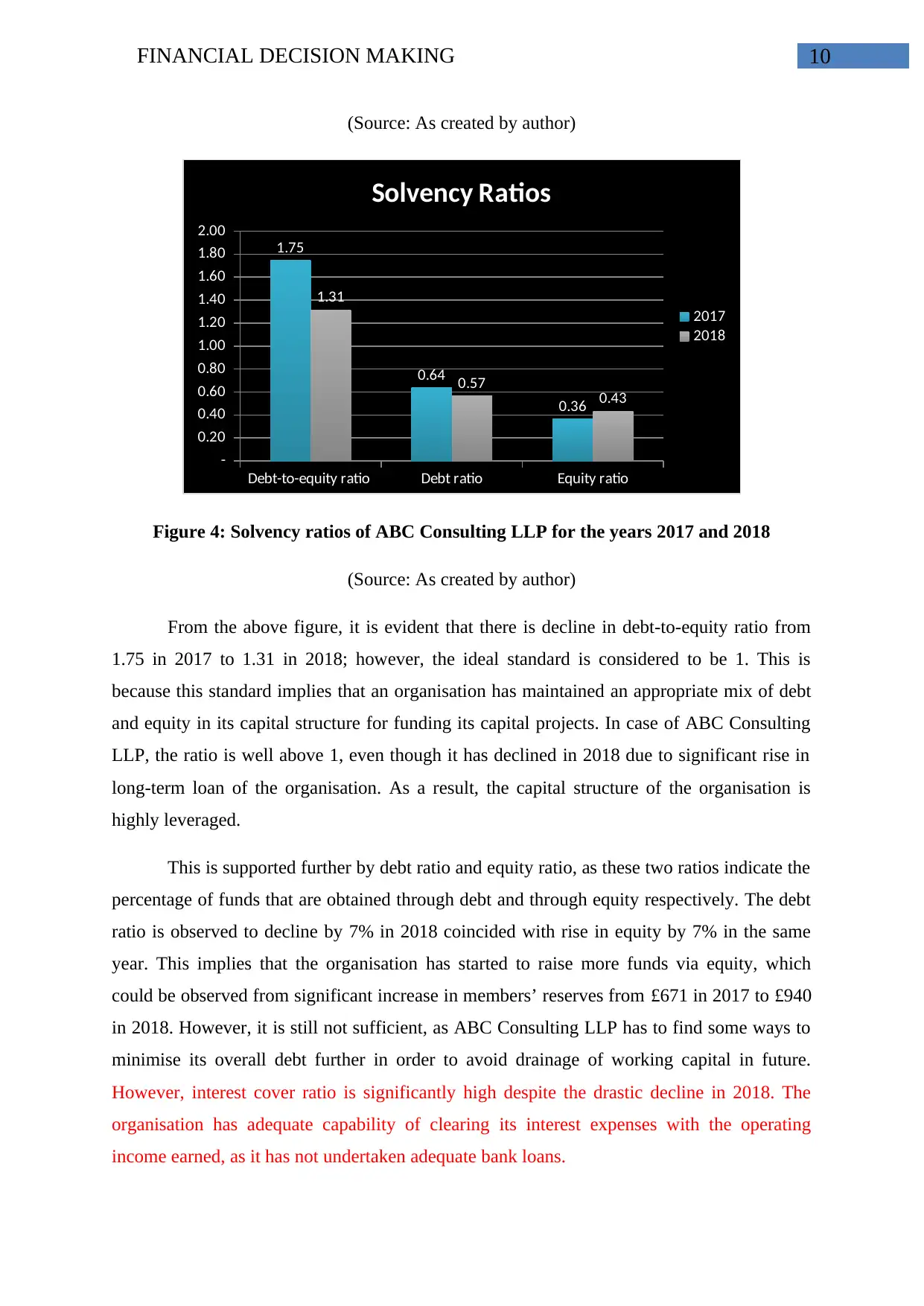

Figure 4: Solvency ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

From the above figure, it is evident that there is decline in debt-to-equity ratio from

1.75 in 2017 to 1.31 in 2018; however, the ideal standard is considered to be 1. This is

because this standard implies that an organisation has maintained an appropriate mix of debt

and equity in its capital structure for funding its capital projects. In case of ABC Consulting

LLP, the ratio is well above 1, even though it has declined in 2018 due to significant rise in

long-term loan of the organisation. As a result, the capital structure of the organisation is

highly leveraged.

This is supported further by debt ratio and equity ratio, as these two ratios indicate the

percentage of funds that are obtained through debt and through equity respectively. The debt

ratio is observed to decline by 7% in 2018 coincided with rise in equity by 7% in the same

year. This implies that the organisation has started to raise more funds via equity, which

could be observed from significant increase in members’ reserves from £671 in 2017 to £940

in 2018. However, it is still not sufficient, as ABC Consulting LLP has to find some ways to

minimise its overall debt further in order to avoid drainage of working capital in future.

However, interest cover ratio is significantly high despite the drastic decline in 2018. The

organisation has adequate capability of clearing its interest expenses with the operating

income earned, as it has not undertaken adequate bank loans.

(Source: As created by author)

Debt-to-equity ratio Debt ratio Equity ratio

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1.75

0.64

0.36

1.31

0.57 0.43

Solvency Ratios

2017

2018

Figure 4: Solvency ratios of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

From the above figure, it is evident that there is decline in debt-to-equity ratio from

1.75 in 2017 to 1.31 in 2018; however, the ideal standard is considered to be 1. This is

because this standard implies that an organisation has maintained an appropriate mix of debt

and equity in its capital structure for funding its capital projects. In case of ABC Consulting

LLP, the ratio is well above 1, even though it has declined in 2018 due to significant rise in

long-term loan of the organisation. As a result, the capital structure of the organisation is

highly leveraged.

This is supported further by debt ratio and equity ratio, as these two ratios indicate the

percentage of funds that are obtained through debt and through equity respectively. The debt

ratio is observed to decline by 7% in 2018 coincided with rise in equity by 7% in the same

year. This implies that the organisation has started to raise more funds via equity, which

could be observed from significant increase in members’ reserves from £671 in 2017 to £940

in 2018. However, it is still not sufficient, as ABC Consulting LLP has to find some ways to

minimise its overall debt further in order to avoid drainage of working capital in future.

However, interest cover ratio is significantly high despite the drastic decline in 2018. The

organisation has adequate capability of clearing its interest expenses with the operating

income earned, as it has not undertaken adequate bank loans.

11FINANCIAL DECISION MAKING

Henceforth, in terms of solvency, the organisation is not placed in a favourable

position in the industry due to more reliance on obtaining funds through debt financing.

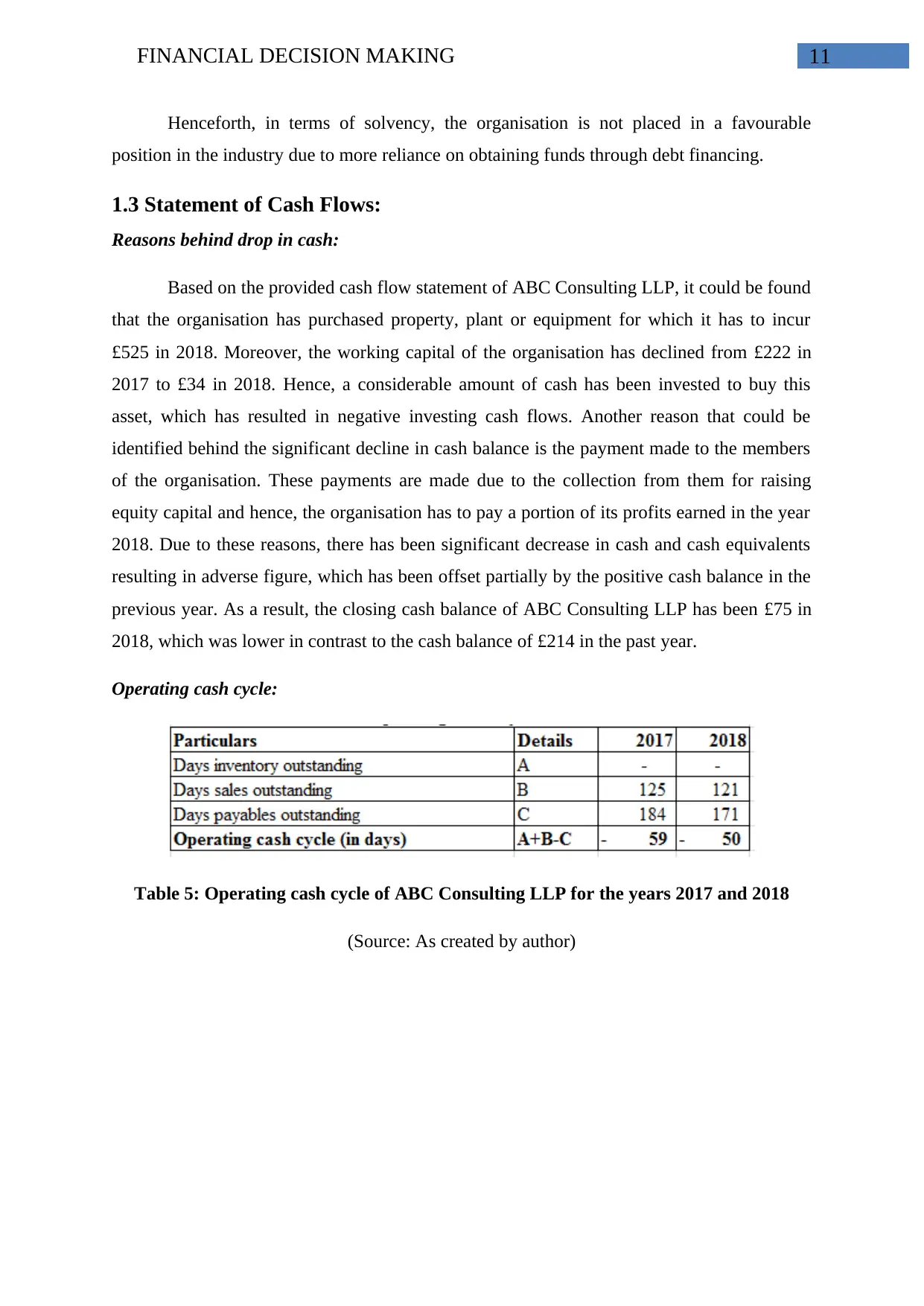

1.3 Statement of Cash Flows:

Reasons behind drop in cash:

Based on the provided cash flow statement of ABC Consulting LLP, it could be found

that the organisation has purchased property, plant or equipment for which it has to incur

£525 in 2018. Moreover, the working capital of the organisation has declined from £222 in

2017 to £34 in 2018. Hence, a considerable amount of cash has been invested to buy this

asset, which has resulted in negative investing cash flows. Another reason that could be

identified behind the significant decline in cash balance is the payment made to the members

of the organisation. These payments are made due to the collection from them for raising

equity capital and hence, the organisation has to pay a portion of its profits earned in the year

2018. Due to these reasons, there has been significant decrease in cash and cash equivalents

resulting in adverse figure, which has been offset partially by the positive cash balance in the

previous year. As a result, the closing cash balance of ABC Consulting LLP has been £75 in

2018, which was lower in contrast to the cash balance of £214 in the past year.

Operating cash cycle:

Table 5: Operating cash cycle of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

Henceforth, in terms of solvency, the organisation is not placed in a favourable

position in the industry due to more reliance on obtaining funds through debt financing.

1.3 Statement of Cash Flows:

Reasons behind drop in cash:

Based on the provided cash flow statement of ABC Consulting LLP, it could be found

that the organisation has purchased property, plant or equipment for which it has to incur

£525 in 2018. Moreover, the working capital of the organisation has declined from £222 in

2017 to £34 in 2018. Hence, a considerable amount of cash has been invested to buy this

asset, which has resulted in negative investing cash flows. Another reason that could be

identified behind the significant decline in cash balance is the payment made to the members

of the organisation. These payments are made due to the collection from them for raising

equity capital and hence, the organisation has to pay a portion of its profits earned in the year

2018. Due to these reasons, there has been significant decrease in cash and cash equivalents

resulting in adverse figure, which has been offset partially by the positive cash balance in the

previous year. As a result, the closing cash balance of ABC Consulting LLP has been £75 in

2018, which was lower in contrast to the cash balance of £214 in the past year.

Operating cash cycle:

Table 5: Operating cash cycle of ABC Consulting LLP for the years 2017 and 2018

(Source: As created by author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.