Financial Decision Making Report: Costing, Budgeting, Appraisal

VerifiedAdded on 2023/01/06

|10

|1704

|37

Report

AI Summary

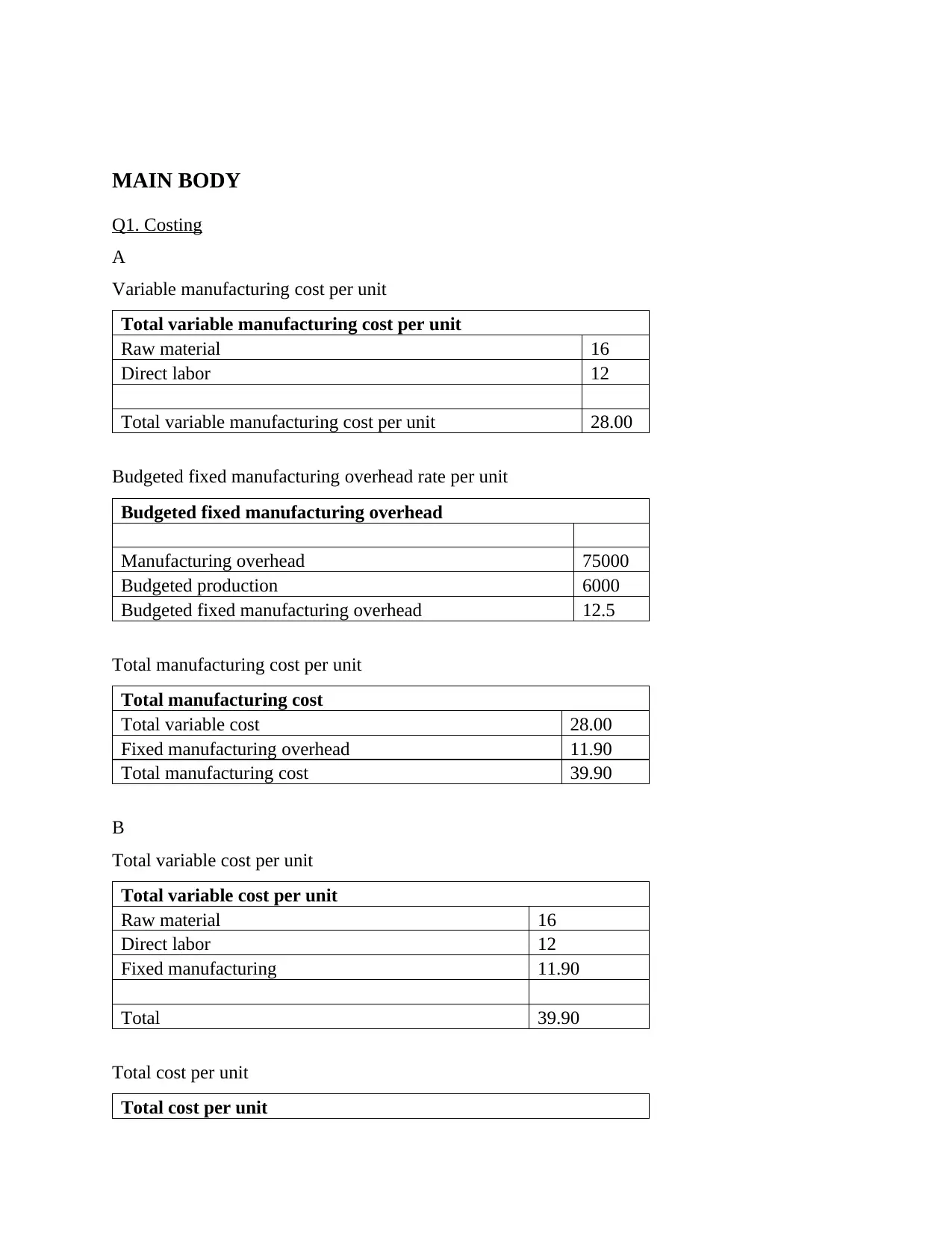

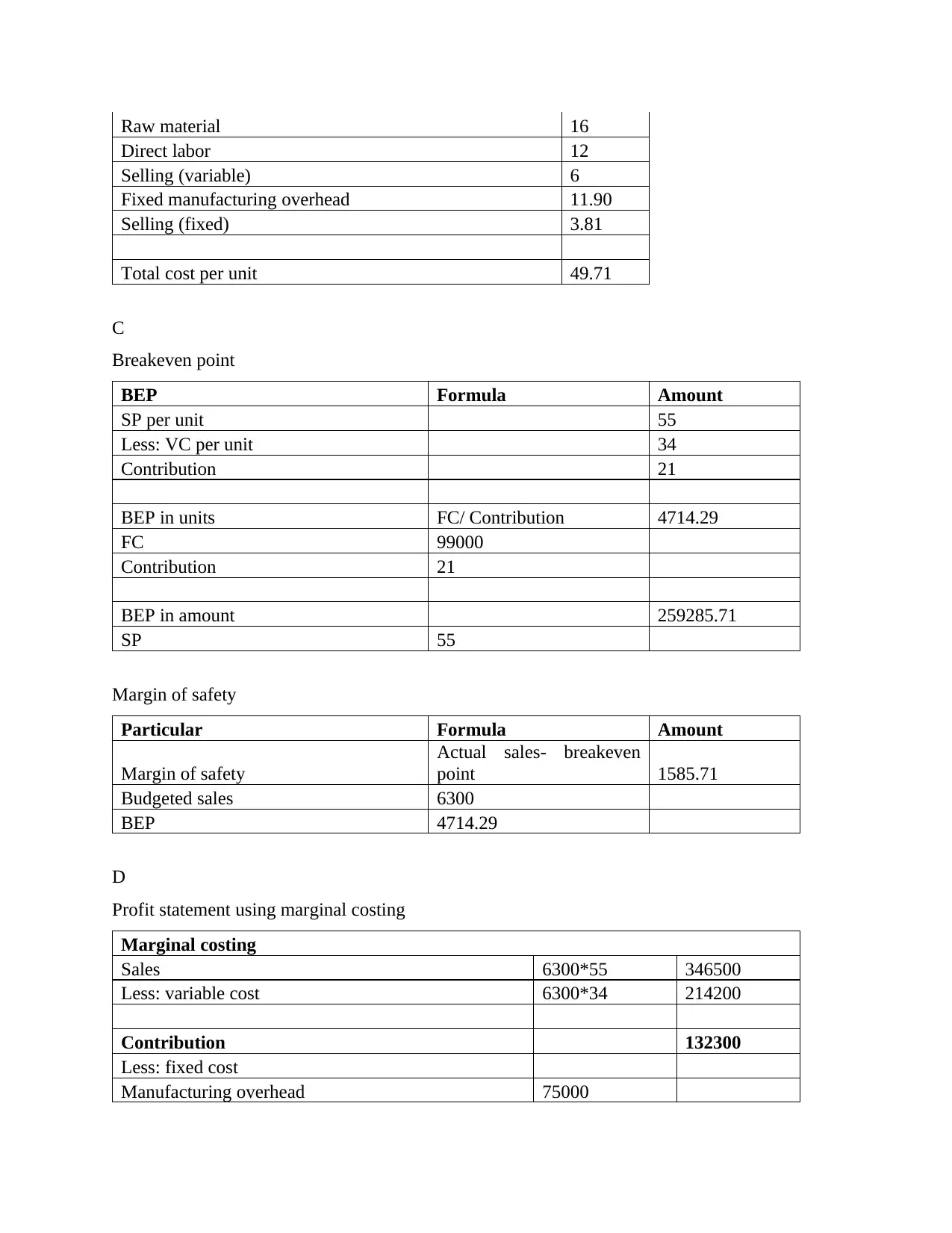

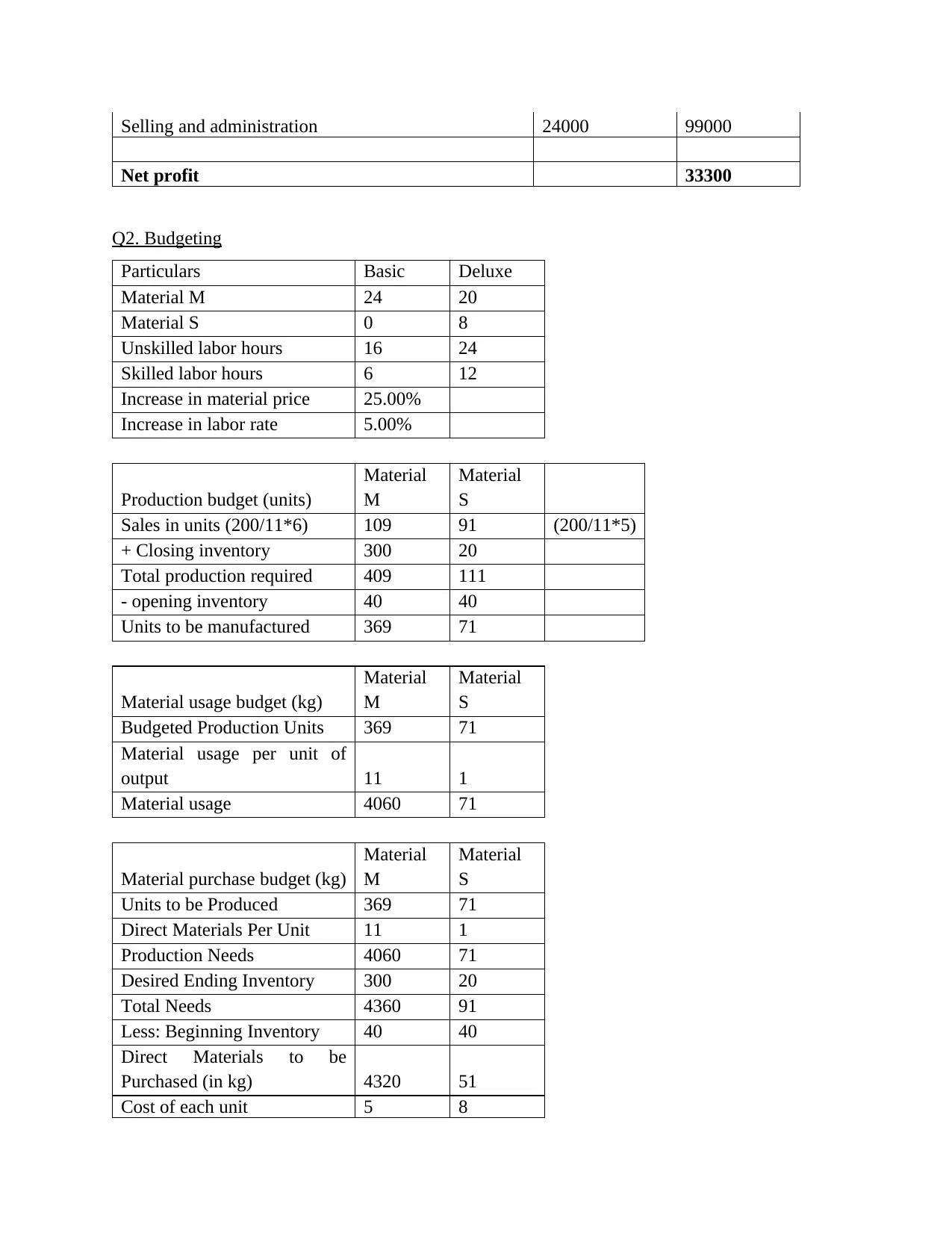

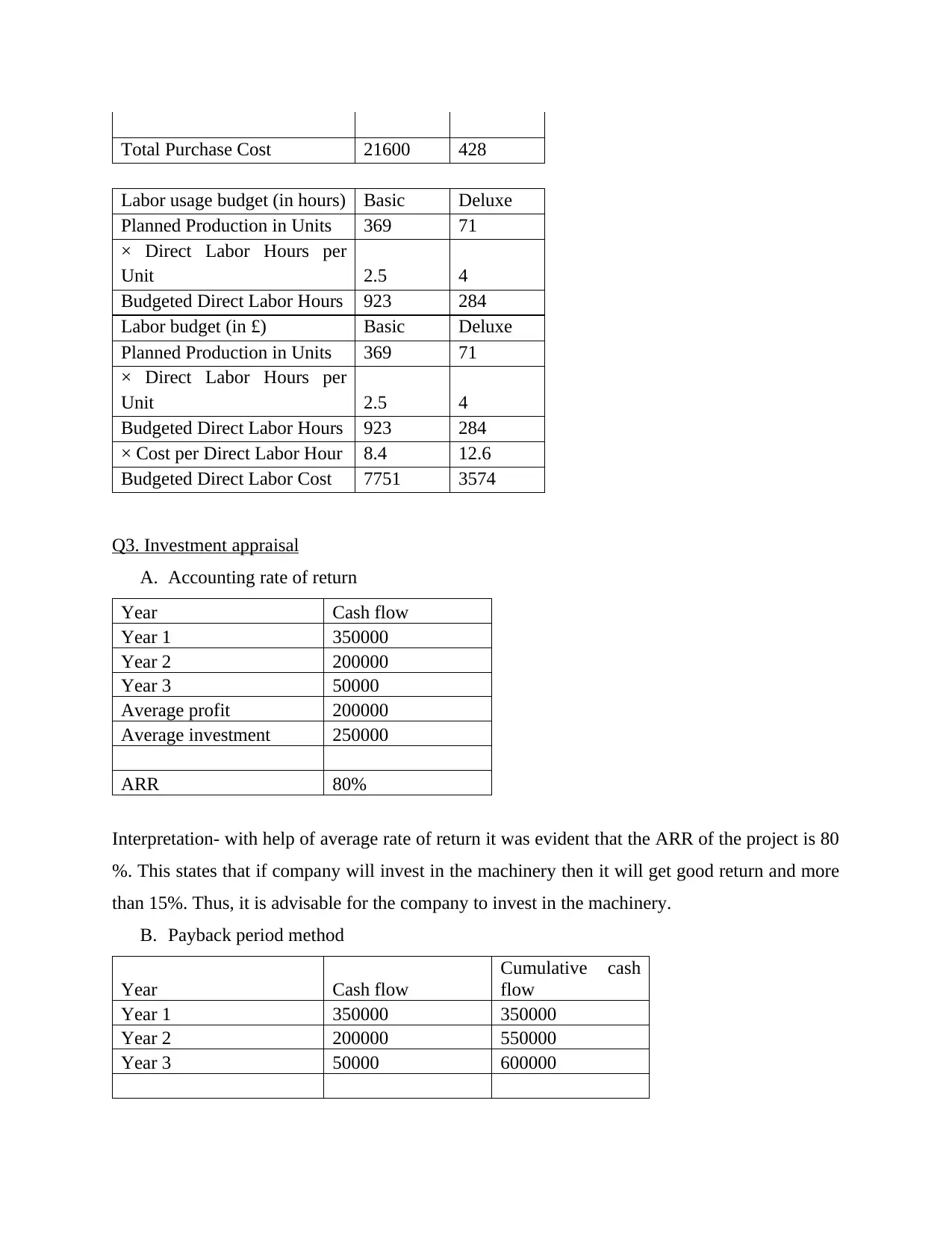

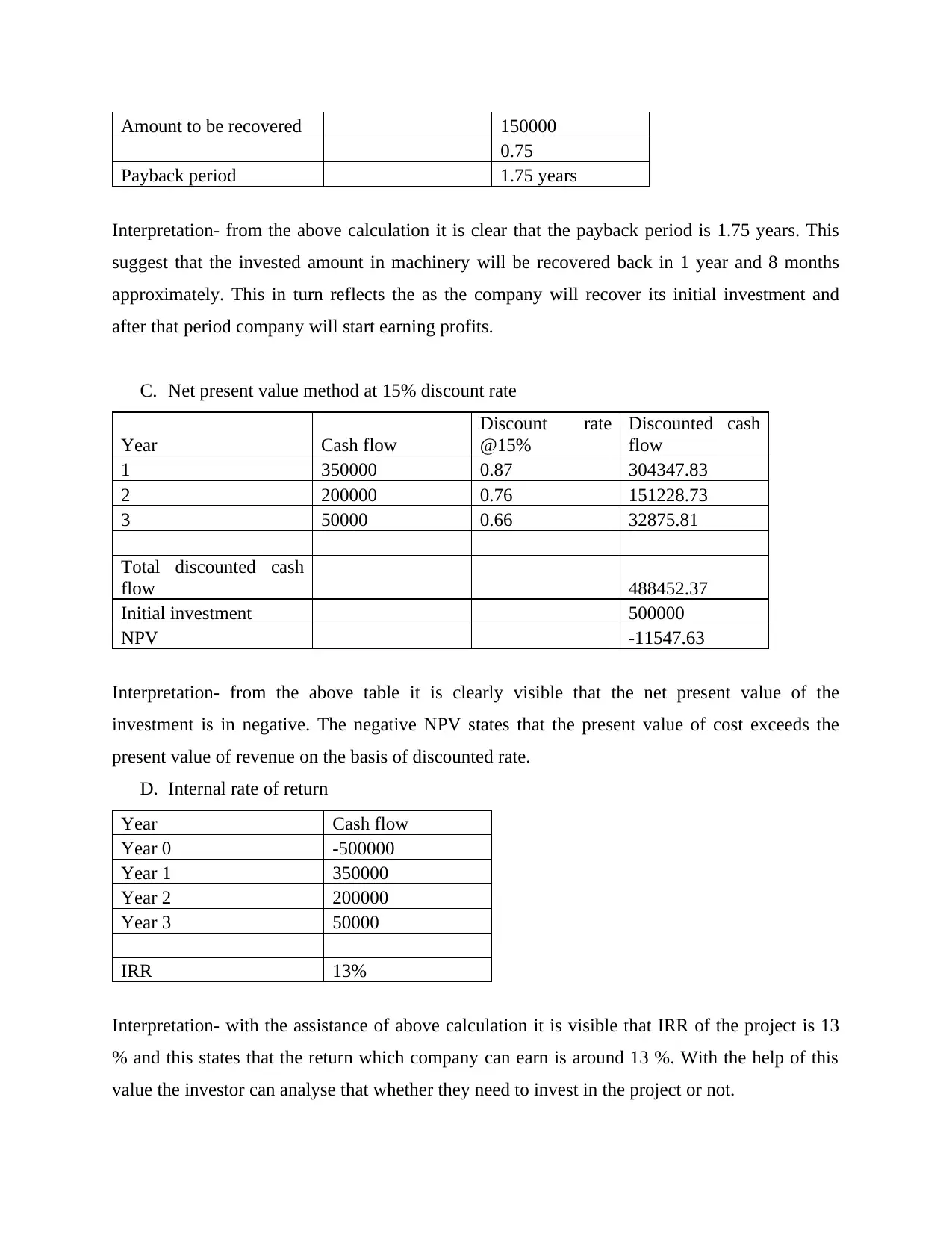

This report provides a comprehensive analysis of financial decision-making, covering key areas such as costing, budgeting, and investment appraisal. The costing section examines variable and fixed costs, calculating total manufacturing costs and breakeven points. Budgeting includes material and labor usage budgets, along with purchase budgets. Investment appraisal techniques such as accounting rate of return, payback period, net present value, and internal rate of return are applied to evaluate a project's financial viability. The report also explores sources of finance, including financial institutions, share issues, and debentures, along with short-term financing options like short-term loans and trade credit, and also includes the advantages and disadvantages of each method. The report utilizes marginal costing and provides profit statements, offering a detailed overview of financial management principles.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.