Financial Decision-Making: Analysis of Investment Appraisal Techniques

VerifiedAdded on 2023/01/07

|8

|1481

|99

Report

AI Summary

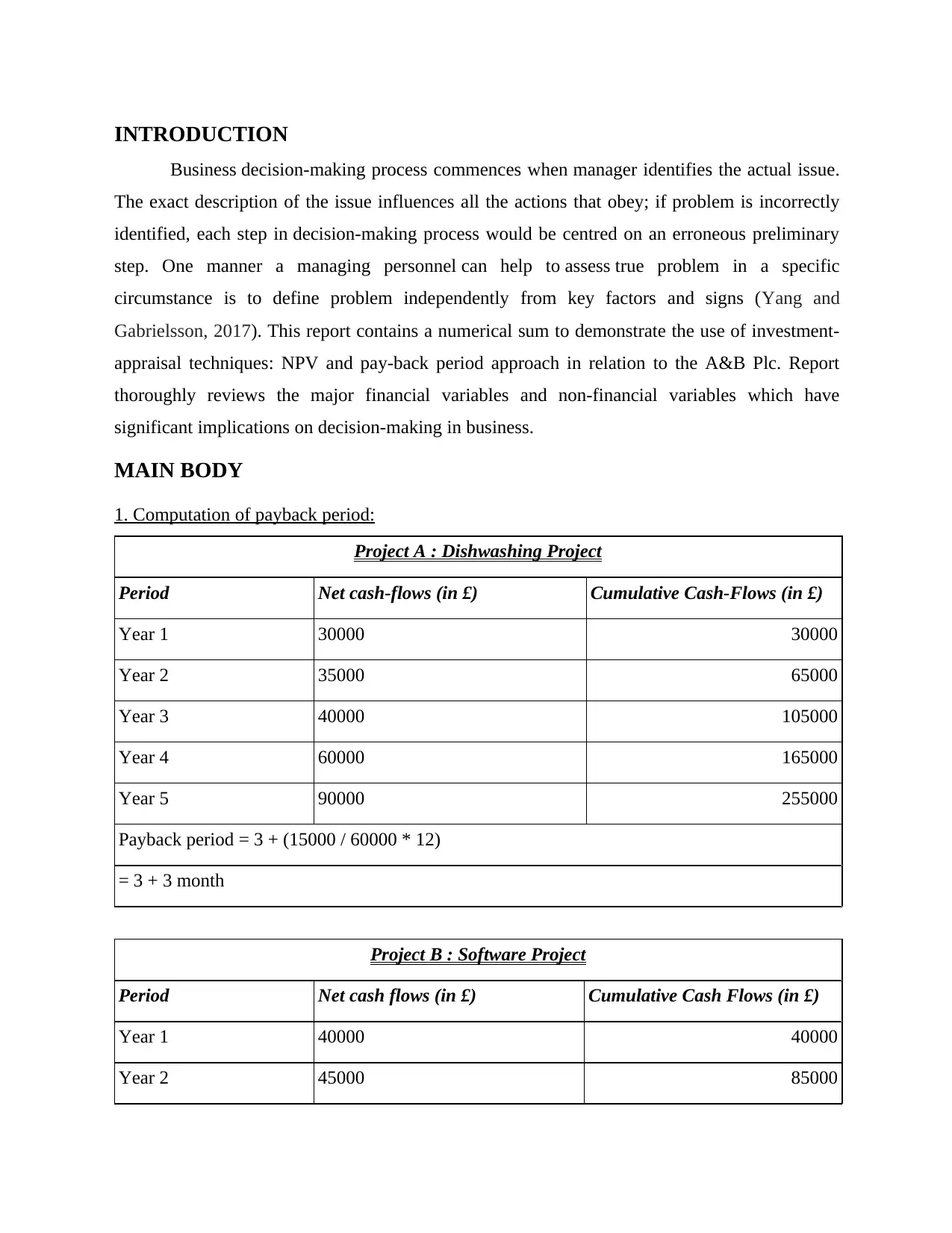

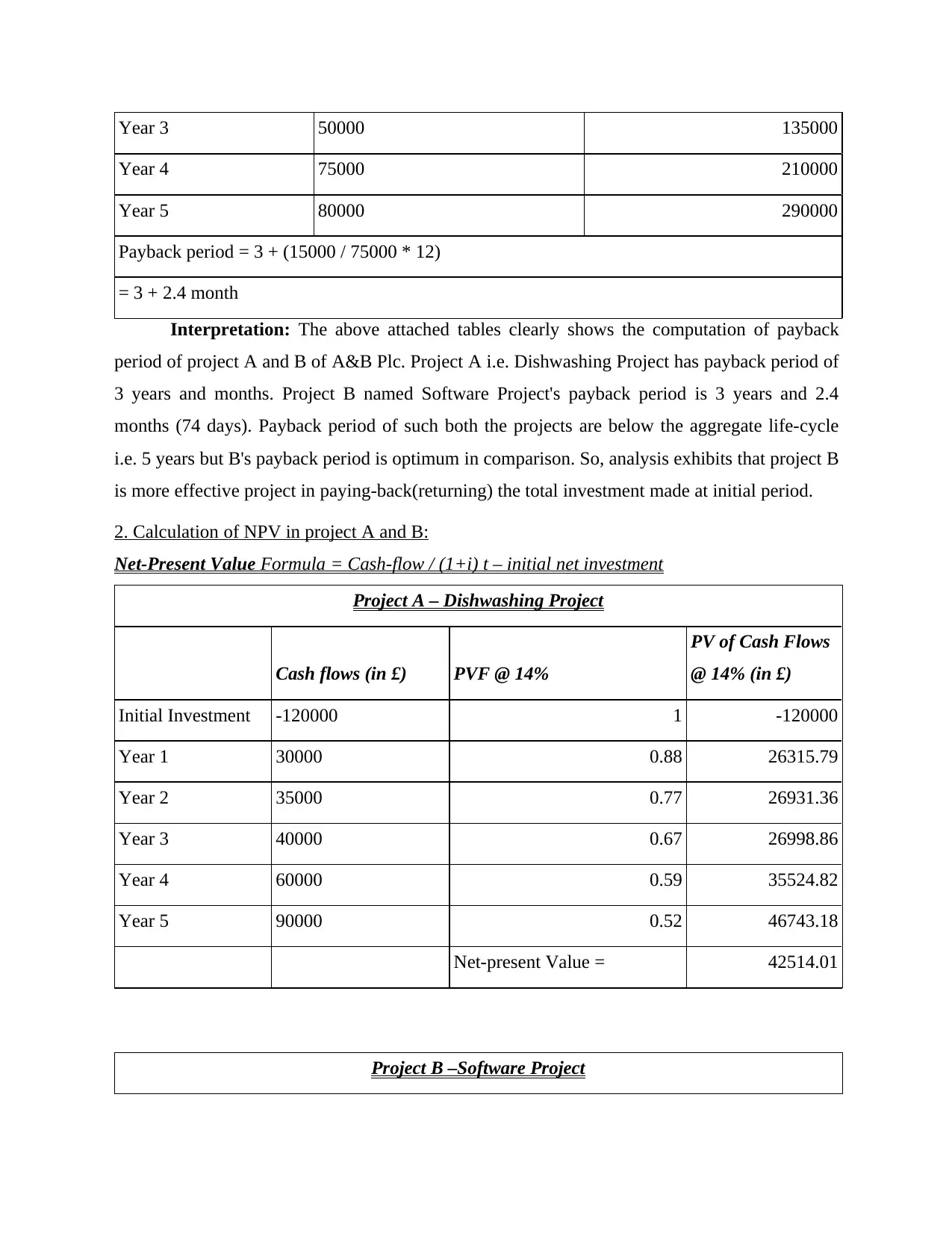

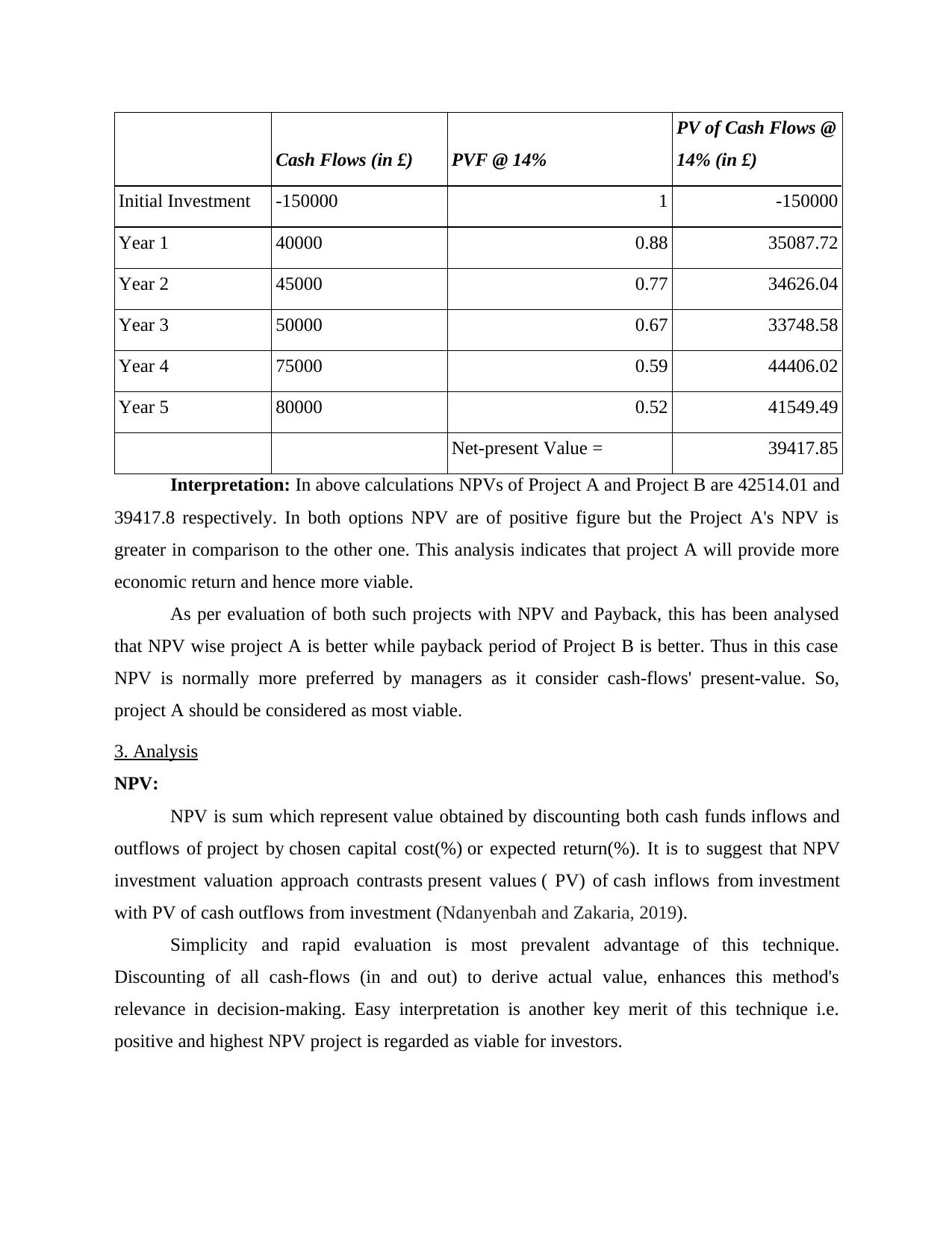

This report delves into the crucial realm of business decision-making, focusing on the application of investment appraisal techniques, specifically Net Present Value (NPV) and payback period, within the context of A&B Plc. The report begins by outlining the importance of accurately identifying the core issue in any business decision-making process and then proceeds to numerically demonstrate the use of these financial tools. The main body of the report includes the computation of the payback period for two projects (Dishwashing and Software), and the calculation of NPV for both projects. The analysis section offers an interpretation of the findings, comparing the effectiveness of each project based on these metrics. The report also discusses the significance of both financial and non-financial factors that influence business decisions, such as gross profit margin, economic growth rate, and competition. The conclusion highlights the importance of investment appraisal in facilitating quick reviews of a business's current position and enabling momentous decisions. The report also offers a discussion of the advantages and disadvantages of both the NPV and payback period methods, and it concludes by emphasizing that NPV is usually preferred by managers as it considers the present value of cash flows. The report includes a list of references to scholarly articles and books that support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.