Financial Decision Making Report: Analysis of Skanska PLC - BM414

VerifiedAdded on 2022/12/12

|13

|4067

|418

Report

AI Summary

This report delves into the realm of financial decision-making, focusing on the application of management accounting techniques within Skanska PLC, a multinational construction and development company. The report begins with an introduction to financial decision-making and its importance, followed by an overview of Skanska PLC's background and key practices. The main body explores the role of various management accounting techniques such as financial planning, analysis of financial statements, standard costing, budgetary control, and marginal costing in planning, control, and decision-making processes. An evaluation section critically analyzes the application of these techniques within Skanska PLC, highlighting their impact on the company's operations. Furthermore, the report calculates and interprets key financial ratios, including return on capital employed, net profit margin, current ratio, debtors collection period, and creditors collection period, for the years 2018 and 2019, providing insights into Skanska PLC's financial performance and identifying potential causes for changes in these ratios. The conclusion summarizes the key findings and emphasizes the importance of efficient managerial accounting techniques for the company's success.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TASK 1............................................................................................................................................3

INTRODUCTION.......................................................................................................................3

MAIN BODY..............................................................................................................................3

EVALUATION...........................................................................................................................5

CONCLUSION............................................................................................................................6

TASK 2............................................................................................................................................7

RATIO CALCULATION............................................................................................................7

1. a Return on capital employed and its importance (100)..........................................................8

b. Performance of SKANSKAPLC by comparing results and positions of 2 years (150)..........8

2. a Net profit margin and its importance....................................................................................9

b. Comparing results and position SKANSAPLC on the basis of net profit...............................9

3. a What is current ratio and its importance for company..........................................................9

b Position of SKANSAPLC on the basis of results of current ratio............................................9

4. a. What is average receivable days or debtors collection period...........................................10

b. Results and position of SKANSAPLC between 2 years with appropriate causes of changes

...................................................................................................................................................10

5. a. Creditors collection period.................................................................................................10

b. Performance of the company between two years..................................................................11

CONCLUSION..........................................................................................................................11

REFERENCES..............................................................................................................................12

TASK 1............................................................................................................................................3

INTRODUCTION.......................................................................................................................3

MAIN BODY..............................................................................................................................3

EVALUATION...........................................................................................................................5

CONCLUSION............................................................................................................................6

TASK 2............................................................................................................................................7

RATIO CALCULATION............................................................................................................7

1. a Return on capital employed and its importance (100)..........................................................8

b. Performance of SKANSKAPLC by comparing results and positions of 2 years (150)..........8

2. a Net profit margin and its importance....................................................................................9

b. Comparing results and position SKANSAPLC on the basis of net profit...............................9

3. a What is current ratio and its importance for company..........................................................9

b Position of SKANSAPLC on the basis of results of current ratio............................................9

4. a. What is average receivable days or debtors collection period...........................................10

b. Results and position of SKANSAPLC between 2 years with appropriate causes of changes

...................................................................................................................................................10

5. a. Creditors collection period.................................................................................................10

b. Performance of the company between two years..................................................................11

CONCLUSION..........................................................................................................................11

REFERENCES..............................................................................................................................12

TASK 1

INTRODUCTION

Financial decision making is basically a process whose responsibility is taking all the

decisions which are related to the stockholder’s equity and the liabilities of the company along

with the issue of bonds. The funding of the company is also decided by the financial situation of

the company along with the characteristics of the finance source. The decisions related to the

finances are concerned with the long-term assets use which is useful in the very important

process of production. The financial decisions must be accurate as profit is earned by selling the

produced goods (Honggowati and et.al., 2017). There are various financial functions which

include the acquiring and utilising of funds which are required for performing efficient

operations. In order to run the things smoothly in the organisations, financial functions are

considered as the lifeblood of business (Nitzl and Chin, 2017). Skanska plc. is a multinational

construction and development company based in UK and headquartered in Sweden. The

company deals in commercial property development, residential development, infrastructure

development, Public private partnerships and many more other areas. It is considered as the

world leading project development and the group of construction which aims at building for the

improvement in the society (Skanska, 2021). The company not only performs its operations in

Sweden but in many other countries like Europe, United States etc. It has more than 33,000

employees working all over the world and more than 5,000 employees in UK which made it a

leading player in the construction market of UK (Skanska is building for a better society, 2021).

The financial operations in the company need to be accurate as it affects the overall business and

the country’s economy (Accounting and Finance, 2021). The report will shed light on the

financial functions and the management accounting techniques in decision making process of

Skanska and will also calculate and describe the financial ratios of the company by critically

analysing the performance in two years.

MAIN BODY

Role of management accounting techniques

There are various techniques of management accounting which plays a major role in

managing the overall finances of the company like Skanska plc. Some of them are as follows:

Financial planning

3

INTRODUCTION

Financial decision making is basically a process whose responsibility is taking all the

decisions which are related to the stockholder’s equity and the liabilities of the company along

with the issue of bonds. The funding of the company is also decided by the financial situation of

the company along with the characteristics of the finance source. The decisions related to the

finances are concerned with the long-term assets use which is useful in the very important

process of production. The financial decisions must be accurate as profit is earned by selling the

produced goods (Honggowati and et.al., 2017). There are various financial functions which

include the acquiring and utilising of funds which are required for performing efficient

operations. In order to run the things smoothly in the organisations, financial functions are

considered as the lifeblood of business (Nitzl and Chin, 2017). Skanska plc. is a multinational

construction and development company based in UK and headquartered in Sweden. The

company deals in commercial property development, residential development, infrastructure

development, Public private partnerships and many more other areas. It is considered as the

world leading project development and the group of construction which aims at building for the

improvement in the society (Skanska, 2021). The company not only performs its operations in

Sweden but in many other countries like Europe, United States etc. It has more than 33,000

employees working all over the world and more than 5,000 employees in UK which made it a

leading player in the construction market of UK (Skanska is building for a better society, 2021).

The financial operations in the company need to be accurate as it affects the overall business and

the country’s economy (Accounting and Finance, 2021). The report will shed light on the

financial functions and the management accounting techniques in decision making process of

Skanska and will also calculate and describe the financial ratios of the company by critically

analysing the performance in two years.

MAIN BODY

Role of management accounting techniques

There are various techniques of management accounting which plays a major role in

managing the overall finances of the company like Skanska plc. Some of them are as follows:

Financial planning

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main aim of the company is to earn as much profit as they can. This is possible only

when there is sound and proper financial planning. This is considered as the act in which the

financial activities are decided in prior for achieving the business objectives. These include

deciding the long term and short term financial objectives (Andrei, Gâlmeanu and Radu,, 2018).

This also involves formulating the financial policies for achieving the maximum return on the

capital employed. These deal in determining the amount of capital required, governing the

determination, distributing the income, determining the optimum level of investment etc.

Analysing of financial statements

The important financial statements include the profit and loss account and balance sheets.

These helps the management of the company in knowing the rate of growth of the business

concerns in Skanska. This analysis can be done through the common size statements,

comparative financial statements and the ratio analysis. It also helps in presenting the

information which can help the investors, creditors and the business executives.

Standard costing

This technique helps in establishing the standard costs under the most effective and

efficient operating conditions and compares the actual with the standard, calculating and

analysing of the variance for knowing the reasons and pinpointing the responsibility for taking

the remedial actions so that the adverse things can be eliminated (Sohrabi, 2017). This helps in

controlling the cost. The management comes to know about the reasons to differentiate these

costs and then make decisions.

Budgetary Control

The management account of the company makes use of the budgetary control to plan and

control the various business activities. This is the most important technique which directs the

business operations in appropriate and desired direction which means it helps in achieving the

satisfactory return on the investment which is made by the company.

Marginal costing

4

when there is sound and proper financial planning. This is considered as the act in which the

financial activities are decided in prior for achieving the business objectives. These include

deciding the long term and short term financial objectives (Andrei, Gâlmeanu and Radu,, 2018).

This also involves formulating the financial policies for achieving the maximum return on the

capital employed. These deal in determining the amount of capital required, governing the

determination, distributing the income, determining the optimum level of investment etc.

Analysing of financial statements

The important financial statements include the profit and loss account and balance sheets.

These helps the management of the company in knowing the rate of growth of the business

concerns in Skanska. This analysis can be done through the common size statements,

comparative financial statements and the ratio analysis. It also helps in presenting the

information which can help the investors, creditors and the business executives.

Standard costing

This technique helps in establishing the standard costs under the most effective and

efficient operating conditions and compares the actual with the standard, calculating and

analysing of the variance for knowing the reasons and pinpointing the responsibility for taking

the remedial actions so that the adverse things can be eliminated (Sohrabi, 2017). This helps in

controlling the cost. The management comes to know about the reasons to differentiate these

costs and then make decisions.

Budgetary Control

The management account of the company makes use of the budgetary control to plan and

control the various business activities. This is the most important technique which directs the

business operations in appropriate and desired direction which means it helps in achieving the

satisfactory return on the investment which is made by the company.

Marginal costing

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This technique of marginal costing is used by the management accountants for making

various financial decisions of the company. Along with this the break even analysis is also used

for controlling the cost as well as maximizing the profit. This can also help the company for

fixing the selling price, selecting the best sales mix, using the scarce raw materials or the

resources in the best possible way, accepting and rejecting the bulk order and the foreign order,

taking any decision and many more other functions. This technique is based on the variable cost,

fixed cost and the contribution (Appelbaum and et.al., 2017).

Statistical and Graphical techniques

These graphical and statistical techniques are used by the management accountant for

making the information more presentable and meaningful which helps them in making the

decisions easier and quicker. The various statistical and graphical techniques used are investment

chart, master chart, linear programming, statistical quality control, chart of sales etc.

EVALUATION

Managerial Accounting is also known as cost accounting or management accounting is

basically a branch of accounting which deals in identifying, measuring, analysing and

interpreting the information related to the accounts which helps the managers in making

operational decisions. Skanska plc. can be facilitated by this as it focuses on the reporting and

coordinating of the financial transactions of the company to the outsiders such as lenders and

investors. This is more focused on the internal reporting of the company for aiding the decision

making. The fifth largest construction company in the world i.e., Skanska plc. is making use of

the managerial accounts techniques for analysing various events and the operational metrics for

translating the data into various useful information. This is then used by the management of the

company for making various decisions in the decision making process (Myllynpää and Hanosh,

2018). The main aim of these techniques is to provide detailed information related to the

operations of the company by analysing the line of products separately, facilities, operating

activities etc. Skanska deals in residential properties, constructions etc. where a minute mistake

can lead to loss of data as well as capital. This is why it is must for the company to use the

techniques of managerial accounting very efficiently so that the large amount of data can be

managed and used for performing various operations. The professionals at this company are also

5

various financial decisions of the company. Along with this the break even analysis is also used

for controlling the cost as well as maximizing the profit. This can also help the company for

fixing the selling price, selecting the best sales mix, using the scarce raw materials or the

resources in the best possible way, accepting and rejecting the bulk order and the foreign order,

taking any decision and many more other functions. This technique is based on the variable cost,

fixed cost and the contribution (Appelbaum and et.al., 2017).

Statistical and Graphical techniques

These graphical and statistical techniques are used by the management accountant for

making the information more presentable and meaningful which helps them in making the

decisions easier and quicker. The various statistical and graphical techniques used are investment

chart, master chart, linear programming, statistical quality control, chart of sales etc.

EVALUATION

Managerial Accounting is also known as cost accounting or management accounting is

basically a branch of accounting which deals in identifying, measuring, analysing and

interpreting the information related to the accounts which helps the managers in making

operational decisions. Skanska plc. can be facilitated by this as it focuses on the reporting and

coordinating of the financial transactions of the company to the outsiders such as lenders and

investors. This is more focused on the internal reporting of the company for aiding the decision

making. The fifth largest construction company in the world i.e., Skanska plc. is making use of

the managerial accounts techniques for analysing various events and the operational metrics for

translating the data into various useful information. This is then used by the management of the

company for making various decisions in the decision making process (Myllynpää and Hanosh,

2018). The main aim of these techniques is to provide detailed information related to the

operations of the company by analysing the line of products separately, facilities, operating

activities etc. Skanska deals in residential properties, constructions etc. where a minute mistake

can lead to loss of data as well as capital. This is why it is must for the company to use the

techniques of managerial accounting very efficiently so that the large amount of data can be

managed and used for performing various operations. The professionals at this company are also

5

much experienced so that they can help in contributing towards a better society. Also, the

company makes use of the past experiences and the lessons which are learned on the previous

projects to deliver the best possible results (Doktoralina and Apollo, 2019). The main reason

behind this is the sound financial practices at Skanska plc. The management of the company use

these techniques like marginal costing, ratio analysis, statistical analysis, inflation accounting,

reporting communicating etc. Skanska plc. uses these techniques among which the inflation

accounting is used to ensure the maintenance of original capital under the fluctuating price

conditions which can be referred as inflation. This also impacts the financial statements of the

company. The reporting communicating technique is used by the company for communicating

the desired financial information related to the financial statements to the clients which helps in

making right decisions at the right times and also helps in determining the future courses of the

actions. Skanska also prefer presenting the information of the constructors, expenses,

contractors, brokers, capital and many others in the forms of statistics and graphs through the

statistical analysis technique which makes the financial reports more meaningful along with

developing comparative studies (Vítková, Chovancová and Veselý, 2017). The various statistical

techniques include the time series data, measure of dispersion, correlation and regression etc.

facilitates the management accountants of the Skanska plc. Company. This is also evaluated that

the financial planning technique is also used by Skanska Company to formulate the financial

policies which helps in financial proceedings to contribute towards better society.

CONCLUSION

The above section concluded about the various management accounting techniques which

are implemented by the management accountant for supplying the required desired information

to the management. These techniques help in discharging the various functions like planning,

organising, directing, staffing and controlling the various financial operations of the company.

The above task also described some of the major techniques of the managerial accounting which

can be used by the company to manage the large amount of data and finances which can help in

analysing the profitability of the company. The Skanska company is not only the best

construction company in various countries like UK but also one of the leading contracts having a

responsible and inclusive business which helps in building better society. This is observed that in

order to maintain the profitability and the position in the market, the financial accounting and the

6

company makes use of the past experiences and the lessons which are learned on the previous

projects to deliver the best possible results (Doktoralina and Apollo, 2019). The main reason

behind this is the sound financial practices at Skanska plc. The management of the company use

these techniques like marginal costing, ratio analysis, statistical analysis, inflation accounting,

reporting communicating etc. Skanska plc. uses these techniques among which the inflation

accounting is used to ensure the maintenance of original capital under the fluctuating price

conditions which can be referred as inflation. This also impacts the financial statements of the

company. The reporting communicating technique is used by the company for communicating

the desired financial information related to the financial statements to the clients which helps in

making right decisions at the right times and also helps in determining the future courses of the

actions. Skanska also prefer presenting the information of the constructors, expenses,

contractors, brokers, capital and many others in the forms of statistics and graphs through the

statistical analysis technique which makes the financial reports more meaningful along with

developing comparative studies (Vítková, Chovancová and Veselý, 2017). The various statistical

techniques include the time series data, measure of dispersion, correlation and regression etc.

facilitates the management accountants of the Skanska plc. Company. This is also evaluated that

the financial planning technique is also used by Skanska Company to formulate the financial

policies which helps in financial proceedings to contribute towards better society.

CONCLUSION

The above section concluded about the various management accounting techniques which

are implemented by the management accountant for supplying the required desired information

to the management. These techniques help in discharging the various functions like planning,

organising, directing, staffing and controlling the various financial operations of the company.

The above task also described some of the major techniques of the managerial accounting which

can be used by the company to manage the large amount of data and finances which can help in

analysing the profitability of the company. The Skanska company is not only the best

construction company in various countries like UK but also one of the leading contracts having a

responsible and inclusive business which helps in building better society. This is observed that in

order to maintain the profitability and the position in the market, the financial accounting and the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managerial accounting of the company must be appropriate and efficient. The above report also

evaluated the ways in which the company uses the various managerial accounting techniques

such as standard costing, budgetary control, marginal costing, decision making, revaluation

accounting etc. This is how, the report overall focussed on the use of efficient managerial

accounting techniques which led to the rapid success and growth of the companies like Skanska

plc. in UK.

TASK 2

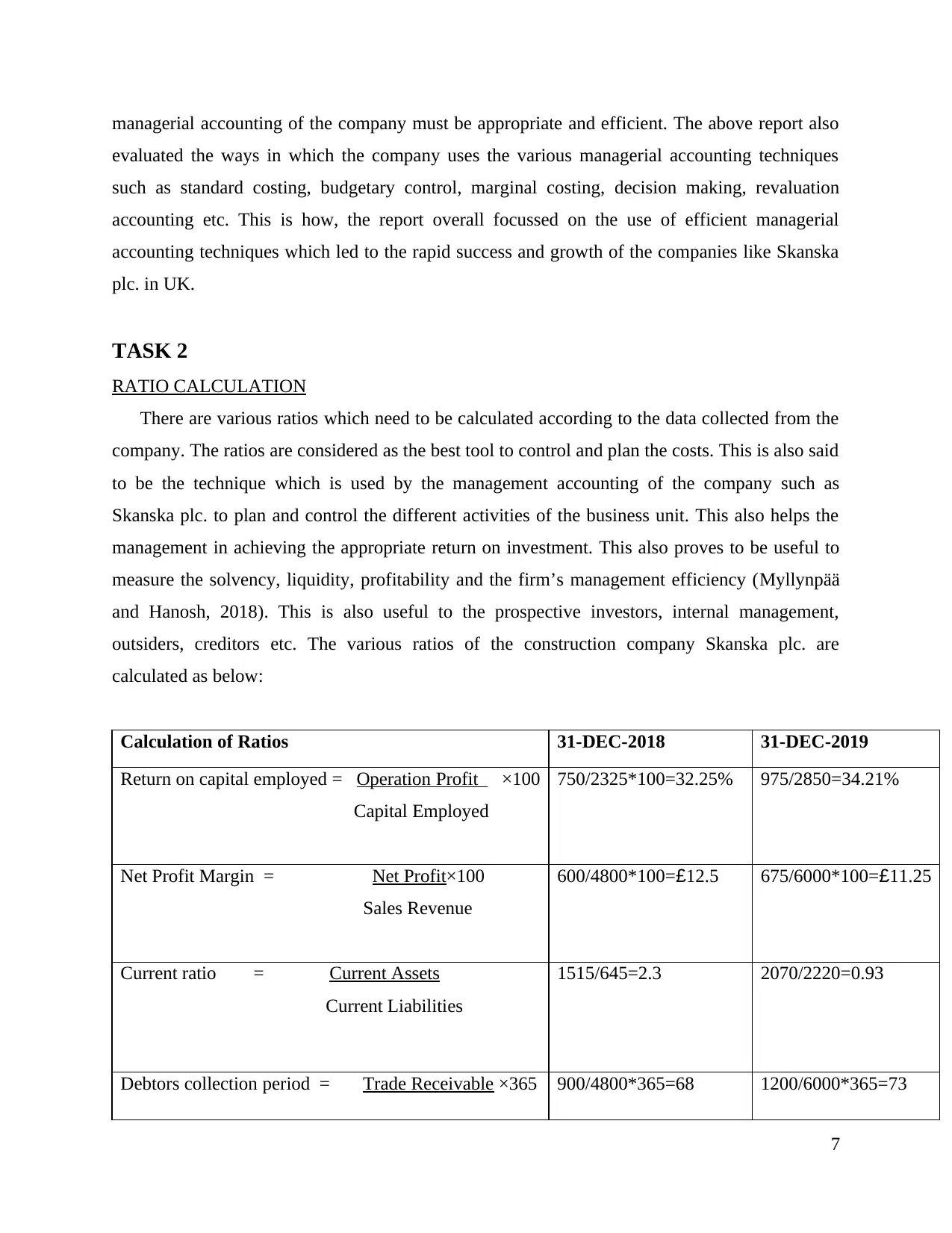

RATIO CALCULATION

There are various ratios which need to be calculated according to the data collected from the

company. The ratios are considered as the best tool to control and plan the costs. This is also said

to be the technique which is used by the management accounting of the company such as

Skanska plc. to plan and control the different activities of the business unit. This also helps the

management in achieving the appropriate return on investment. This also proves to be useful to

measure the solvency, liquidity, profitability and the firm’s management efficiency (Myllynpää

and Hanosh, 2018). This is also useful to the prospective investors, internal management,

outsiders, creditors etc. The various ratios of the construction company Skanska plc. are

calculated as below:

Calculation of Ratios 31-DEC-2018 31-DEC-2019

Return on capital employed = Operation Profit ×100

Capital Employed

750/2325*100=32.25% 975/2850=34.21%

Net Profit Margin = Net Profit×100

Sales Revenue

600/4800*100=£12.5 675/6000*100=£11.25

Current ratio = Current Assets

Current Liabilities

1515/645=2.3 2070/2220=0.93

Debtors collection period = Trade Receivable ×365 900/4800*365=68 1200/6000*365=73

7

evaluated the ways in which the company uses the various managerial accounting techniques

such as standard costing, budgetary control, marginal costing, decision making, revaluation

accounting etc. This is how, the report overall focussed on the use of efficient managerial

accounting techniques which led to the rapid success and growth of the companies like Skanska

plc. in UK.

TASK 2

RATIO CALCULATION

There are various ratios which need to be calculated according to the data collected from the

company. The ratios are considered as the best tool to control and plan the costs. This is also said

to be the technique which is used by the management accounting of the company such as

Skanska plc. to plan and control the different activities of the business unit. This also helps the

management in achieving the appropriate return on investment. This also proves to be useful to

measure the solvency, liquidity, profitability and the firm’s management efficiency (Myllynpää

and Hanosh, 2018). This is also useful to the prospective investors, internal management,

outsiders, creditors etc. The various ratios of the construction company Skanska plc. are

calculated as below:

Calculation of Ratios 31-DEC-2018 31-DEC-2019

Return on capital employed = Operation Profit ×100

Capital Employed

750/2325*100=32.25% 975/2850=34.21%

Net Profit Margin = Net Profit×100

Sales Revenue

600/4800*100=£12.5 675/6000*100=£11.25

Current ratio = Current Assets

Current Liabilities

1515/645=2.3 2070/2220=0.93

Debtors collection period = Trade Receivable ×365 900/4800*365=68 1200/6000*365=73

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

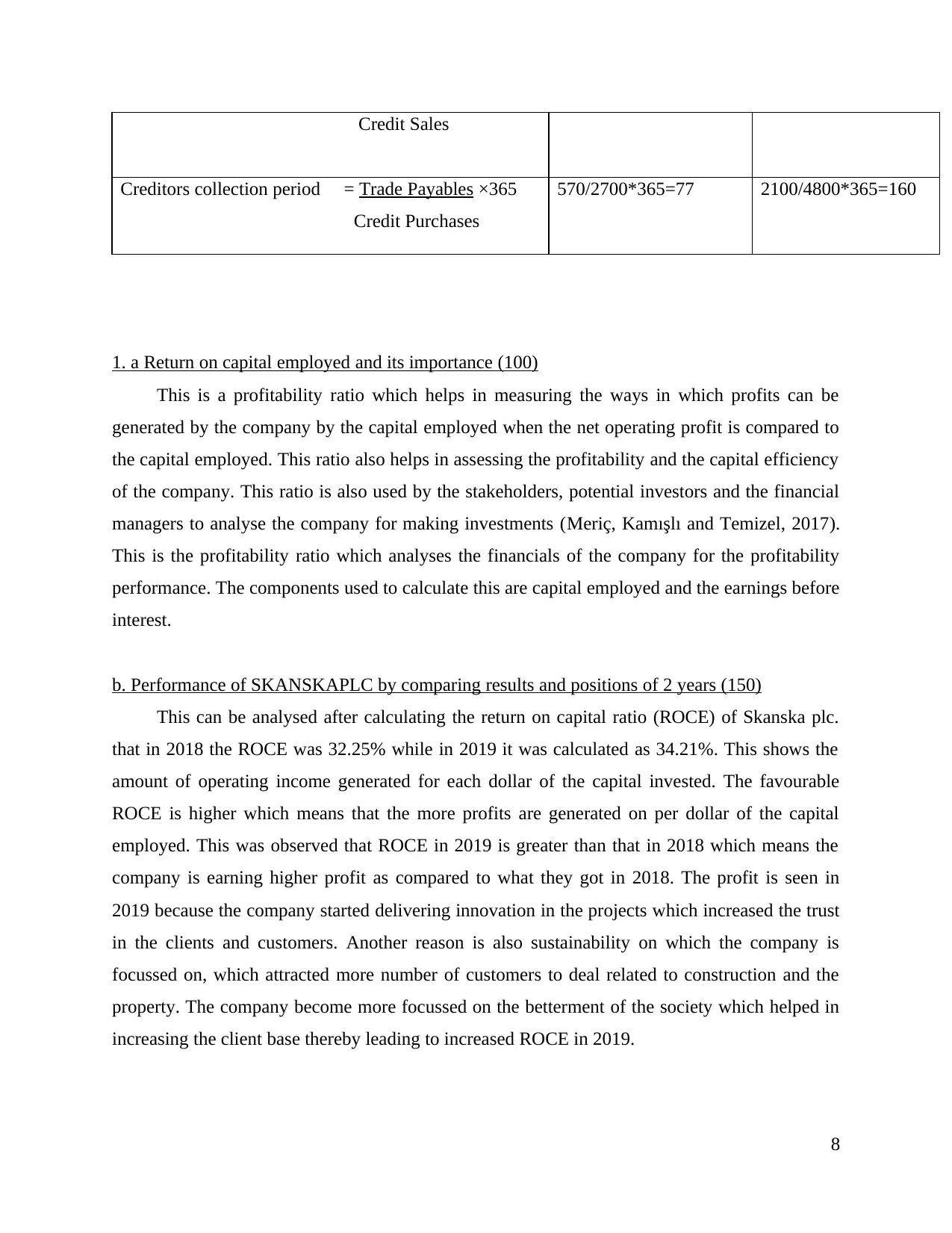

Credit Sales

Creditors collection period = Trade Payables ×365

Credit Purchases

570/2700*365=77 2100/4800*365=160

1. a Return on capital employed and its importance (100)

This is a profitability ratio which helps in measuring the ways in which profits can be

generated by the company by the capital employed when the net operating profit is compared to

the capital employed. This ratio also helps in assessing the profitability and the capital efficiency

of the company. This ratio is also used by the stakeholders, potential investors and the financial

managers to analyse the company for making investments (Meriç, Kamışlı and Temizel, 2017).

This is the profitability ratio which analyses the financials of the company for the profitability

performance. The components used to calculate this are capital employed and the earnings before

interest.

b. Performance of SKANSKAPLC by comparing results and positions of 2 years (150)

This can be analysed after calculating the return on capital ratio (ROCE) of Skanska plc.

that in 2018 the ROCE was 32.25% while in 2019 it was calculated as 34.21%. This shows the

amount of operating income generated for each dollar of the capital invested. The favourable

ROCE is higher which means that the more profits are generated on per dollar of the capital

employed. This was observed that ROCE in 2019 is greater than that in 2018 which means the

company is earning higher profit as compared to what they got in 2018. The profit is seen in

2019 because the company started delivering innovation in the projects which increased the trust

in the clients and customers. Another reason is also sustainability on which the company is

focussed on, which attracted more number of customers to deal related to construction and the

property. The company become more focussed on the betterment of the society which helped in

increasing the client base thereby leading to increased ROCE in 2019.

8

Creditors collection period = Trade Payables ×365

Credit Purchases

570/2700*365=77 2100/4800*365=160

1. a Return on capital employed and its importance (100)

This is a profitability ratio which helps in measuring the ways in which profits can be

generated by the company by the capital employed when the net operating profit is compared to

the capital employed. This ratio also helps in assessing the profitability and the capital efficiency

of the company. This ratio is also used by the stakeholders, potential investors and the financial

managers to analyse the company for making investments (Meriç, Kamışlı and Temizel, 2017).

This is the profitability ratio which analyses the financials of the company for the profitability

performance. The components used to calculate this are capital employed and the earnings before

interest.

b. Performance of SKANSKAPLC by comparing results and positions of 2 years (150)

This can be analysed after calculating the return on capital ratio (ROCE) of Skanska plc.

that in 2018 the ROCE was 32.25% while in 2019 it was calculated as 34.21%. This shows the

amount of operating income generated for each dollar of the capital invested. The favourable

ROCE is higher which means that the more profits are generated on per dollar of the capital

employed. This was observed that ROCE in 2019 is greater than that in 2018 which means the

company is earning higher profit as compared to what they got in 2018. The profit is seen in

2019 because the company started delivering innovation in the projects which increased the trust

in the clients and customers. Another reason is also sustainability on which the company is

focussed on, which attracted more number of customers to deal related to construction and the

property. The company become more focussed on the betterment of the society which helped in

increasing the client base thereby leading to increased ROCE in 2019.

8

2. a Net profit margin and its importance

Net profit is the main key amount that shows effectiveness and success of company. It

refers the amount or profit that company made after all working expenses. In another words it

can be said that it refers total profit of company that it earns by minimizing all expenses and cost.

For knowing success of company and accomplishing goals, it is important to know about net

profit (Amalya, 2018). In regard to importance of net profit margin, it can be said that it helps

investors access as investors make decision about investing amount in company only on the basis

of net profit. If company makes good net profit then company can attract numbers of investors.

b. Comparing results and position SKANSAPLC on the basis of net profit

On the basis of above data and calculation, it can be said that in the year of 2018,

SKANSAPLC made £12.5 net profit margin and in the year of 2019 it made £11.25 profit

margin. So, on this basis, it can be said that in previous or in the year of 2018, this company

made a great success and in 1 year profit margin decreased. On the basis of comparison, it can

also be said that in the year of 2018, this company was successful and it needs to identify reasons

as why net profit margin is decreased. It can also be said that increased net profit margin shows

success and effectiveness of company and lower profit margin indicates that there is poor

management or poor operations.

3. a What is current ratio and its importance for company

In regard to current ratio, it can be said that it refers liquidity ratio that measures ability of

company to pay short term obligations that are due within 1 year because of some reasons. It

helps companies in telling about ways by which it can maximize current assets on its balance

sheet and satisfy current payables or debts (Solihin, 2019). If company pays to debts then it

improves its image in the market and helps company in attracting investors. Overall, it can be

said that it helps companies out to measure short term financial strength of company.

b Position of SKANSAPLC on the basis of results of current ratio

On the basis of above data and calculations it can be said that this SKANSAPLC was

much more capable in the year of 2018 as compared to 2019. In the year of 2018 current ratio of

this company was 0.23 and in the year of 2019, it was only 0.93. On this basis, it can be said that

9

Net profit is the main key amount that shows effectiveness and success of company. It

refers the amount or profit that company made after all working expenses. In another words it

can be said that it refers total profit of company that it earns by minimizing all expenses and cost.

For knowing success of company and accomplishing goals, it is important to know about net

profit (Amalya, 2018). In regard to importance of net profit margin, it can be said that it helps

investors access as investors make decision about investing amount in company only on the basis

of net profit. If company makes good net profit then company can attract numbers of investors.

b. Comparing results and position SKANSAPLC on the basis of net profit

On the basis of above data and calculation, it can be said that in the year of 2018,

SKANSAPLC made £12.5 net profit margin and in the year of 2019 it made £11.25 profit

margin. So, on this basis, it can be said that in previous or in the year of 2018, this company

made a great success and in 1 year profit margin decreased. On the basis of comparison, it can

also be said that in the year of 2018, this company was successful and it needs to identify reasons

as why net profit margin is decreased. It can also be said that increased net profit margin shows

success and effectiveness of company and lower profit margin indicates that there is poor

management or poor operations.

3. a What is current ratio and its importance for company

In regard to current ratio, it can be said that it refers liquidity ratio that measures ability of

company to pay short term obligations that are due within 1 year because of some reasons. It

helps companies in telling about ways by which it can maximize current assets on its balance

sheet and satisfy current payables or debts (Solihin, 2019). If company pays to debts then it

improves its image in the market and helps company in attracting investors. Overall, it can be

said that it helps companies out to measure short term financial strength of company.

b Position of SKANSAPLC on the basis of results of current ratio

On the basis of above data and calculations it can be said that this SKANSAPLC was

much more capable in the year of 2018 as compared to 2019. In the year of 2018 current ratio of

this company was 0.23 and in the year of 2019, it was only 0.93. On this basis, it can be said that

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in the year of 2018, it has much capability of paying amount to all debts and improving financial

strengths. The reason behind decreasing current ratio may be decline in inventory, changes in

available cash and backlogs of bills to pay. Decreased cash ratio indicates high risk and on this

basis, it can be suggested to SKANSAPLC that it should focus on increasing sales by providing

qualitative goods and decreasing debts.

4. a. What is average receivable days or debtors collection period

Average receivable days or debtors collection period refers number of days until customers

invoice is outstanding before it is collected by company. In regard to good average debtors

collection period it can be said that company can improve its financial strengths when it has

around 30 days. Lower days indicate effectiveness and tell investors that collection of company

is good. More days of average receivable indicate ineffectiveness and shows incapability of

company of collection (Meriam, Achsani and Novianti, 2017). It also helps investors in knowing

about effectiveness of company’s credit and collection policies.

b. Results and position of SKANSAPLC between 2 years with appropriate causes of changes

On the basis of above data, average receivable days or debtors collection period can be

discussed and in the year of 2018, this period was 68 days. In the year of 2019, debtors collection

period was 73 days. It is discussed above that higher day’s shows ineffectiveness and good

debtors’ collection period is one that has fewer days of collecting debts. So, on this basis, it can

be said that in the year of 2018, SKANSAPLC was much effective than 2019 because in 2018, it

was 68 days in which company can collect amount from debtors. Some causes behind higher

receivable days may include: poor management and poor credit policy. So, on this basis, it can

be suggested that company should focus on improving its management and granting fewer credit

to customers along with focusing on increasing sales.

5. a. Creditors collection period

This is the average number of days which are needed for collecting the receivables from

the customers. This is measured as the interval from the invoice issuance to the cash receipt from

the customer. This must always be low. This is similar to the debtor day which is useful indicator

to assess the liquidity position of a business (Myšková and Hájek, 2017). The low average

10

strengths. The reason behind decreasing current ratio may be decline in inventory, changes in

available cash and backlogs of bills to pay. Decreased cash ratio indicates high risk and on this

basis, it can be suggested to SKANSAPLC that it should focus on increasing sales by providing

qualitative goods and decreasing debts.

4. a. What is average receivable days or debtors collection period

Average receivable days or debtors collection period refers number of days until customers

invoice is outstanding before it is collected by company. In regard to good average debtors

collection period it can be said that company can improve its financial strengths when it has

around 30 days. Lower days indicate effectiveness and tell investors that collection of company

is good. More days of average receivable indicate ineffectiveness and shows incapability of

company of collection (Meriam, Achsani and Novianti, 2017). It also helps investors in knowing

about effectiveness of company’s credit and collection policies.

b. Results and position of SKANSAPLC between 2 years with appropriate causes of changes

On the basis of above data, average receivable days or debtors collection period can be

discussed and in the year of 2018, this period was 68 days. In the year of 2019, debtors collection

period was 73 days. It is discussed above that higher day’s shows ineffectiveness and good

debtors’ collection period is one that has fewer days of collecting debts. So, on this basis, it can

be said that in the year of 2018, SKANSAPLC was much effective than 2019 because in 2018, it

was 68 days in which company can collect amount from debtors. Some causes behind higher

receivable days may include: poor management and poor credit policy. So, on this basis, it can

be suggested that company should focus on improving its management and granting fewer credit

to customers along with focusing on increasing sales.

5. a. Creditors collection period

This is the average number of days which are needed for collecting the receivables from

the customers. This is measured as the interval from the invoice issuance to the cash receipt from

the customer. This must always be low. This is similar to the debtor day which is useful indicator

to assess the liquidity position of a business (Myšková and Hájek, 2017). The low average

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

collection period means the organisation is collecting the payments faster as compared to other

companies. On the other hand, when it is high, this means the company is facing trouble while

collecting the accounts which leads to trouble with the cash flows.

b. Performance of the company between two years

This can be analysed by the calculated credit collection period in Skanska Plc. that in 2018,

it is 77 while in 2019 it grew to 160 which means the company faced more problems in 2019 to

collect the accounts and managing the cash flows. In 2018, this was lesser as compared to 2019

which means the company was able to collect the cash from the customers easily. The company

can decrease these days by defining the credit policies, offering the discounts on the early

payments, rewarding timely payments, discouraging late payments, analysing the report and

many more (Zorn and et.al., 2018). These strategies were not applied by the company in 2019

which increased the collection period.

CONCLUSION

The above section concluded about the various types of financial ratios such as Return on

capital employed, Net Profit Margin, Current ratio, Debtors collection period and Creditors

collection period. This helped in analysing the performance of the company Skanska plc. The

various ratios were defined and their importance of these ratios was highlighted. The

performance of the company was compared by analysing these ratios in 2018 and 2019. This

helped in analysing the performance of the company in two different years. This is how; the

importance of these ratios was highlighted with respect to the Skanska Company and its growth

of profitability.

11

companies. On the other hand, when it is high, this means the company is facing trouble while

collecting the accounts which leads to trouble with the cash flows.

b. Performance of the company between two years

This can be analysed by the calculated credit collection period in Skanska Plc. that in 2018,

it is 77 while in 2019 it grew to 160 which means the company faced more problems in 2019 to

collect the accounts and managing the cash flows. In 2018, this was lesser as compared to 2019

which means the company was able to collect the cash from the customers easily. The company

can decrease these days by defining the credit policies, offering the discounts on the early

payments, rewarding timely payments, discouraging late payments, analysing the report and

many more (Zorn and et.al., 2018). These strategies were not applied by the company in 2019

which increased the collection period.

CONCLUSION

The above section concluded about the various types of financial ratios such as Return on

capital employed, Net Profit Margin, Current ratio, Debtors collection period and Creditors

collection period. This helped in analysing the performance of the company Skanska plc. The

various ratios were defined and their importance of these ratios was highlighted. The

performance of the company was compared by analysing these ratios in 2018 and 2019. This

helped in analysing the performance of the company in two different years. This is how; the

importance of these ratios was highlighted with respect to the Skanska Company and its growth

of profitability.

11

REFERENCES

Books and Journals

Andrei, G., Gâlmeanu, R. and Radu, F., 2018. Managerial accounting-an essential component of

the information system. Valahian Journal of Economic Studies. 9(2). pp.109-114.

Appelbaum, D. and et.al., 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems. 25.

pp.29-44.

Doktoralina, C. and Apollo, A., 2019. The contribution of strategic management accounting in

supply chain outcomes and logistic firm profitability. Uncertain Supply Chain

Management. 7(2). pp.145-156.

Honggowati, S. and et.al., 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1).

pp.23-30.

Meriç, E., Kamışlı, M. and Temizel, F., 2017. Interactions among Stock Price and Financial

Ratios: The Case of Turkish Banking Sector. Applied Economics and Finance. 4(6).

pp.107-115.

Myllynpää, O. and Hanosh, J., 2018. Collaboration between companies in sharing economy and

Skanska.

Myšková, R. and Hájek, P., 2017. Comprehensive assessment of firm financial performance

using financial ratios and linguistic analysis of annual reports. Journal of International

Studies, volume 10, issue: 4.

Nitzl, C. and Chin, W.W., 2017. The case of partial least squares (PLS) path modeling in

managerial accounting research. Journal of Management Control. 28(2). pp.137-156.

Sohrabi, M., 2017. The Relationship between Non-Financial Innovative Management

Accounting Tools and Risk and Return of Iranian Stock Market Listed

Companies. Dutch Journal of Finance and Management. 1(2). p.40.

Vítková, E., Chovancová, J. and Veselý, D., 2017. Value Driver and Its Impact on Operational

Profit in Construction Company. Procedia computer science. 121. pp.364-369.

Zorn, A. and et.al., 2018. Financial ratios as indicators of economic sustainability: A quantitative

analysis for swiss dairy farms. Sustainability. 10(8). p.2942.

Online

12

Books and Journals

Andrei, G., Gâlmeanu, R. and Radu, F., 2018. Managerial accounting-an essential component of

the information system. Valahian Journal of Economic Studies. 9(2). pp.109-114.

Appelbaum, D. and et.al., 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems. 25.

pp.29-44.

Doktoralina, C. and Apollo, A., 2019. The contribution of strategic management accounting in

supply chain outcomes and logistic firm profitability. Uncertain Supply Chain

Management. 7(2). pp.145-156.

Honggowati, S. and et.al., 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1).

pp.23-30.

Meriç, E., Kamışlı, M. and Temizel, F., 2017. Interactions among Stock Price and Financial

Ratios: The Case of Turkish Banking Sector. Applied Economics and Finance. 4(6).

pp.107-115.

Myllynpää, O. and Hanosh, J., 2018. Collaboration between companies in sharing economy and

Skanska.

Myšková, R. and Hájek, P., 2017. Comprehensive assessment of firm financial performance

using financial ratios and linguistic analysis of annual reports. Journal of International

Studies, volume 10, issue: 4.

Nitzl, C. and Chin, W.W., 2017. The case of partial least squares (PLS) path modeling in

managerial accounting research. Journal of Management Control. 28(2). pp.137-156.

Sohrabi, M., 2017. The Relationship between Non-Financial Innovative Management

Accounting Tools and Risk and Return of Iranian Stock Market Listed

Companies. Dutch Journal of Finance and Management. 1(2). p.40.

Vítková, E., Chovancová, J. and Veselý, D., 2017. Value Driver and Its Impact on Operational

Profit in Construction Company. Procedia computer science. 121. pp.364-369.

Zorn, A. and et.al., 2018. Financial ratios as indicators of economic sustainability: A quantitative

analysis for swiss dairy farms. Sustainability. 10(8). p.2942.

Online

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.