Financial Decision Making Report: BM414, Financial Analysis, 2020

VerifiedAdded on 2023/01/12

|12

|3563

|70

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making, focusing on two key areas. The first section delves into the role of accounting and finance, examining the structure of financial statements, the terms used within them, and the application of management accounting techniques within Camden Limited, a leading UK manufacturer. The report details financial planning, financial statement analysis, historical cost accounting, and budgetary control. The second section focuses on financial performance analysis, particularly through ratio analysis. The report calculates and interprets various financial ratios for Alpha Limited, including Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, Debtor Collection Period, and Creditor Collection Period. It provides insights into the financial health and performance of both companies, offering valuable information for understanding financial decision-making processes and evaluating business performance.

Financial

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

CONCLUSION................................................................................................................................6

INTRODUCTION...........................................................................................................................7

TASK 2............................................................................................................................................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

CONCLUSION................................................................................................................................6

INTRODUCTION...........................................................................................................................7

TASK 2............................................................................................................................................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial decision-taking includes the systematic and structured process of choosing the most

suitable and successful option among the multiple alternative course of action relevant to fiscal

operations (Ball, 2013). The main aim or the motto of the project is to include and select new or

creative measures in order to accomplish the company objective, vision and task. Report offers

details on different elements such as terms, report form and use of the management accounting

technologies in the Camden limited. It is the largest retailer and manufacturer of UPVC doors

and windows in the United Kingdom.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company:

In UK, Camden Limited is most prominent manufacturer and distributor of u PVC door,

entrance and windows. Company provides customised layout of windows and door according to

customer’s preference. Company is headquartered in Antrim, Northern Ireland and operates

throughout the United Kingdom. Company's layout and variety of screens, openings are known

for their awkward appearance. Because of its 36 years of experience and unique product

consistency in manufacturing, it has achieved the position. It manufactures and sells long-term

goods that follow safety standards. Recently company made investment in recycling of u PVC

items and give recycling of its old products. Business with its unique ideas and creativity

offering tuff rivalry in u PVC sector (Camden Group. 2019). It has a commodity range that

replaces the changing environment and nature with standard challenging goods. It sells domestic

and industrial goods to the United Kingdom.

Structure of and terms used within the financial statements:

Financial statements include primarily profit or profits or loss accounts, balance sheets or

financial situation analysis and capital adjustment or investment fund adjustment, cash flow

document, etc. The balance sheet arrangement involves equities, investments and other

properties of the proprietor. Accounts reflected in the accounts shall be calculated at a defined

date for both liabilities and properties which includes debt, capital assets, and current year

Financial decision-taking includes the systematic and structured process of choosing the most

suitable and successful option among the multiple alternative course of action relevant to fiscal

operations (Ball, 2013). The main aim or the motto of the project is to include and select new or

creative measures in order to accomplish the company objective, vision and task. Report offers

details on different elements such as terms, report form and use of the management accounting

technologies in the Camden limited. It is the largest retailer and manufacturer of UPVC doors

and windows in the United Kingdom.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company:

In UK, Camden Limited is most prominent manufacturer and distributor of u PVC door,

entrance and windows. Company provides customised layout of windows and door according to

customer’s preference. Company is headquartered in Antrim, Northern Ireland and operates

throughout the United Kingdom. Company's layout and variety of screens, openings are known

for their awkward appearance. Because of its 36 years of experience and unique product

consistency in manufacturing, it has achieved the position. It manufactures and sells long-term

goods that follow safety standards. Recently company made investment in recycling of u PVC

items and give recycling of its old products. Business with its unique ideas and creativity

offering tuff rivalry in u PVC sector (Camden Group. 2019). It has a commodity range that

replaces the changing environment and nature with standard challenging goods. It sells domestic

and industrial goods to the United Kingdom.

Structure of and terms used within the financial statements:

Financial statements include primarily profit or profits or loss accounts, balance sheets or

financial situation analysis and capital adjustment or investment fund adjustment, cash flow

document, etc. The balance sheet arrangement involves equities, investments and other

properties of the proprietor. Accounts reflected in the accounts shall be calculated at a defined

date for both liabilities and properties which includes debt, capital assets, and current year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profits. The shareholder's fund or shares. Liabilities are classified into current liabilities and non-

current liabilities. Assets are also classified as non-current assets, i.e. real securities, fictional

assets, etc. and current assets, like inventory, currency, etc. The sales framework covers total

production, goods sold, gross income, direct and indirect costs, and net income. Revenue figures

mix the income & loss record with trading accounts. Gross profit estimate is shown in the trading

account section. Gross profit is determined by calculating store opening and closing and direct

expenses from the total sales value (Bryer, 2013). Whereas all indirect expenditures and sales are

shown, as in the net profit section. The net profit is determined by all indirect costs excluded

from indirect sales. Indirect costs and profits are benefits and losses that do not directly relate to

core business operations.

Role of management accounting techniques:

The Management Account provides the most important activities that allow

administrators to help employees / officials in the decision-making process by taking knowledge

or aggregations. The whole of system and interested activities of management accounting

concentrates toward more use of particular relevant methods and techniques that to take

smoothness in method of regulating, judgment-making and planning. The main purpose of big

business officials is here to make a significant difference in the key business processes and

effectiveness. For large companies such as Camden LTD accountants or executives use different

methods to achieve the desired processes and work efficiencies of the business. It also helps to

increase and increasing transparency through the organized collection and distribution of money

and tax capital. Companies follow approaches that lay down rules and strategies to enforce

business and management activities. The most widely accepted management accounting methods

include financial planning, cash flow analyses, financial statement reviews, fund performance

accounts, etc. There are multipurpose strategies required to fully establish internal and external

procedures and provide them with output. The following is a summary of various management

techniques:

Financial Planning- This basically means that companies have certain roles and duties to

project results and to quantify the money and to assess the need for resources by keeping

strategic factors into consideration. It helps to create financial policies and guidance on

the acquisition and control of funds collected from various sources within a business.

current liabilities. Assets are also classified as non-current assets, i.e. real securities, fictional

assets, etc. and current assets, like inventory, currency, etc. The sales framework covers total

production, goods sold, gross income, direct and indirect costs, and net income. Revenue figures

mix the income & loss record with trading accounts. Gross profit estimate is shown in the trading

account section. Gross profit is determined by calculating store opening and closing and direct

expenses from the total sales value (Bryer, 2013). Whereas all indirect expenditures and sales are

shown, as in the net profit section. The net profit is determined by all indirect costs excluded

from indirect sales. Indirect costs and profits are benefits and losses that do not directly relate to

core business operations.

Role of management accounting techniques:

The Management Account provides the most important activities that allow

administrators to help employees / officials in the decision-making process by taking knowledge

or aggregations. The whole of system and interested activities of management accounting

concentrates toward more use of particular relevant methods and techniques that to take

smoothness in method of regulating, judgment-making and planning. The main purpose of big

business officials is here to make a significant difference in the key business processes and

effectiveness. For large companies such as Camden LTD accountants or executives use different

methods to achieve the desired processes and work efficiencies of the business. It also helps to

increase and increasing transparency through the organized collection and distribution of money

and tax capital. Companies follow approaches that lay down rules and strategies to enforce

business and management activities. The most widely accepted management accounting methods

include financial planning, cash flow analyses, financial statement reviews, fund performance

accounts, etc. There are multipurpose strategies required to fully establish internal and external

procedures and provide them with output. The following is a summary of various management

techniques:

Financial Planning- This basically means that companies have certain roles and duties to

project results and to quantify the money and to assess the need for resources by keeping

strategic factors into consideration. It helps to create financial policies and guidance on

the acquisition and control of funds collected from various sources within a business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Camden limited management is also designing systems that advise of the amount and

adequacy of resources or assets in the short and long term and enable fast investment

decisions by financial planning (Chiang, Nouri and Samanta, 2014). It provides ease of

preparation and creation of a guided platform for the management of finance and

financial activities. As per the current results and financial framework of the

organization, managers assess and predict the needs of funds. It assesses the effect of

funding streams and assures near-term utilization of funds over the long term.

Analysis of financial statements- It is a core method of measuring results and success

over a given span using financial records and similar documents for almost all business

organizations. General annual statements include the balance sheet, revenue tax,

adjustments to the shareholder's fund account, etc. These also represent a broad variety of

facets of the organization. For illustration, the balance sheet shows the financial value of

the company's properties and its responsibilities as of the date of end of the year. A

thorough review can allow managers to prepare and determine, because the annual

statements show actual outcomes. The annual reporting and review for Camden LTD

users and management is used for decision-making. These analyzes are carried out in

order to evaluate growth prospects, sources of financing, variables impacting market

success and to recognize possible or contingent responsibilities. The annual statement

allows it possible to measure statistics and assets over a span of one year and recognize

the company's vulnerability.

Historical Cost Accounting- Managers and accountants use this method of tracking

various properties of the business at historical cost. Historical cost is referred to as the

original base price charged when the properties were purchased (Hope, Thomas and

Vyas, 2013). This methodology undergirds a hypothesis that properties that are inherently

measurable capital properties are expected to be viewed at cost rates charged for

transactions and other costs that are appropriate for the usage of assets rather than market

value. All the investments are not reported, however, at historic values such as

marketable securities. It is more comprehensive, since interest can easily be checked by

supporting records. The effective usage of resource may be managed in the

organizational context. Administration can also determine and create strategies for

purchase and sale of properties.

adequacy of resources or assets in the short and long term and enable fast investment

decisions by financial planning (Chiang, Nouri and Samanta, 2014). It provides ease of

preparation and creation of a guided platform for the management of finance and

financial activities. As per the current results and financial framework of the

organization, managers assess and predict the needs of funds. It assesses the effect of

funding streams and assures near-term utilization of funds over the long term.

Analysis of financial statements- It is a core method of measuring results and success

over a given span using financial records and similar documents for almost all business

organizations. General annual statements include the balance sheet, revenue tax,

adjustments to the shareholder's fund account, etc. These also represent a broad variety of

facets of the organization. For illustration, the balance sheet shows the financial value of

the company's properties and its responsibilities as of the date of end of the year. A

thorough review can allow managers to prepare and determine, because the annual

statements show actual outcomes. The annual reporting and review for Camden LTD

users and management is used for decision-making. These analyzes are carried out in

order to evaluate growth prospects, sources of financing, variables impacting market

success and to recognize possible or contingent responsibilities. The annual statement

allows it possible to measure statistics and assets over a span of one year and recognize

the company's vulnerability.

Historical Cost Accounting- Managers and accountants use this method of tracking

various properties of the business at historical cost. Historical cost is referred to as the

original base price charged when the properties were purchased (Hope, Thomas and

Vyas, 2013). This methodology undergirds a hypothesis that properties that are inherently

measurable capital properties are expected to be viewed at cost rates charged for

transactions and other costs that are appropriate for the usage of assets rather than market

value. All the investments are not reported, however, at historic values such as

marketable securities. It is more comprehensive, since interest can easily be checked by

supporting records. The effective usage of resource may be managed in the

organizational context. Administration can also determine and create strategies for

purchase and sale of properties.

Budgetary Control- Almost all businesses forecast spending and profits and plan

multiple expenditures according to their specific targets. The key goal of framing is to

establish systems and to manage all the enterprise's budgetary operations, thereby

strongly connecting expenditure and budgetary controls (Lawrence, 2013). Budget

management involves modelling procedures as well as tracking the usage and fluctuation

of funds. Camden LTD provides budgetary control to the management of funds plans the

usage of funds and makes budgetary decisions. This also offers a comprehensive

comparative review of numerous financial factors to promote quick and reliable decision-

making. This adds to the concept of planning as budgets focused on efficient preparation.

It controls prices and minimizes prices by removing unnecessary duplication in industry,

contributing to optimum profits overall.

CONCLUSION

On the basis of above project report this can be concluded that financial accounts and

management accounts are too crucial for business entities. As by help of these companies

can manage their overall expenses and income in an effective manner. It becomes possible

because under the management accounting vital range of techniques are included that leads

to better financial management.

multiple expenditures according to their specific targets. The key goal of framing is to

establish systems and to manage all the enterprise's budgetary operations, thereby

strongly connecting expenditure and budgetary controls (Lawrence, 2013). Budget

management involves modelling procedures as well as tracking the usage and fluctuation

of funds. Camden LTD provides budgetary control to the management of funds plans the

usage of funds and makes budgetary decisions. This also offers a comprehensive

comparative review of numerous financial factors to promote quick and reliable decision-

making. This adds to the concept of planning as budgets focused on efficient preparation.

It controls prices and minimizes prices by removing unnecessary duplication in industry,

contributing to optimum profits overall.

CONCLUSION

On the basis of above project report this can be concluded that financial accounts and

management accounts are too crucial for business entities. As by help of these companies

can manage their overall expenses and income in an effective manner. It becomes possible

because under the management accounting vital range of techniques are included that leads

to better financial management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

TASK 2

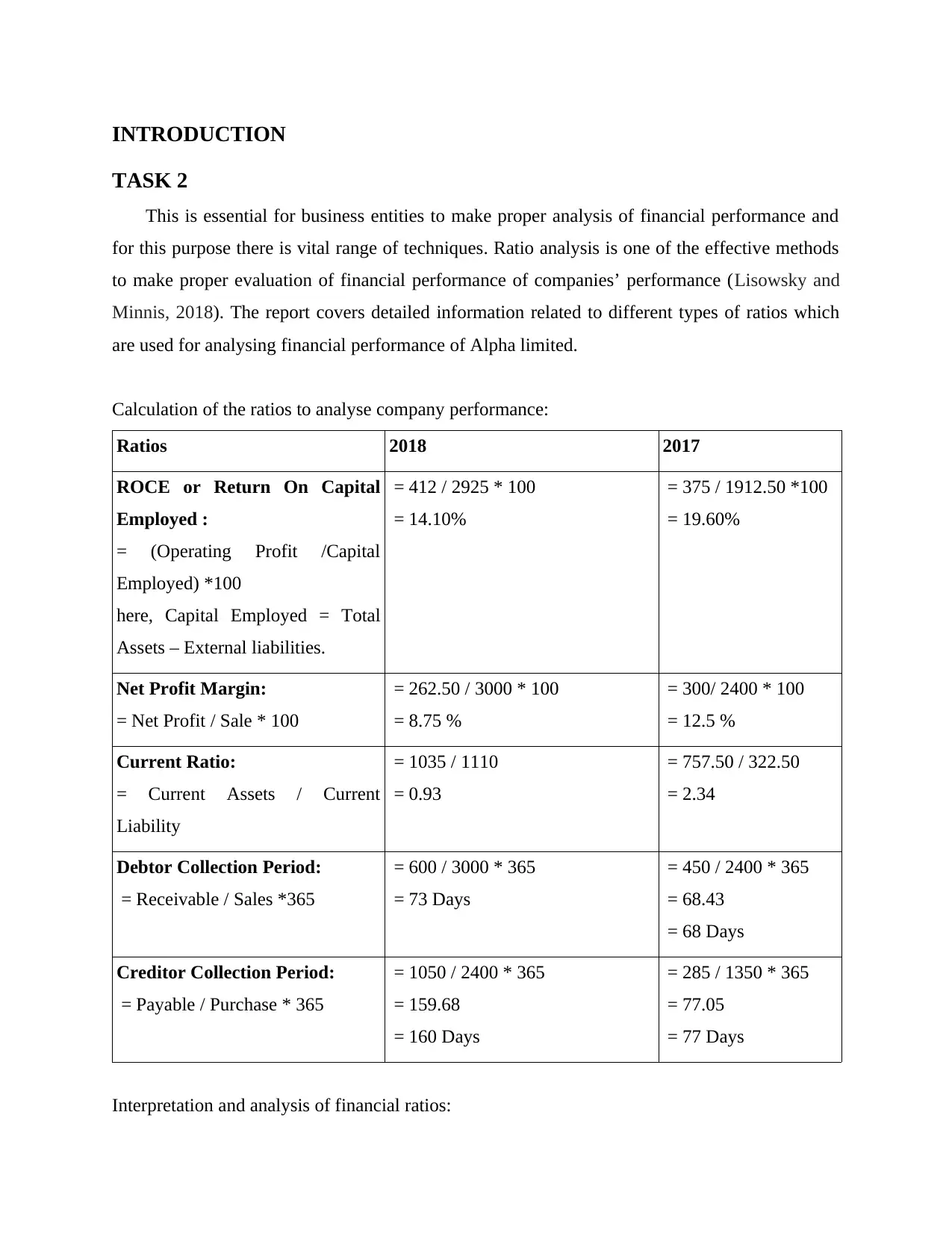

This is essential for business entities to make proper analysis of financial performance and

for this purpose there is vital range of techniques. Ratio analysis is one of the effective methods

to make proper evaluation of financial performance of companies’ performance (Lisowsky and

Minnis, 2018). The report covers detailed information related to different types of ratios which

are used for analysing financial performance of Alpha limited.

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

TASK 2

This is essential for business entities to make proper analysis of financial performance and

for this purpose there is vital range of techniques. Ratio analysis is one of the effective methods

to make proper evaluation of financial performance of companies’ performance (Lisowsky and

Minnis, 2018). The report covers detailed information related to different types of ratios which

are used for analysing financial performance of Alpha limited.

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial factors are essential for the evaluation and measurement of the trade entity's

fiscal and financial results. It helps to define risk and effects, to measure productivity, to

use output and the role of solvency. It helps to analyze patterns established over more than

one year across these ratios. Ratio analysis offers comprehensiveness in all facets of the

evaluation of financial statements. When evaluating different financial factors, the

consequences of current situations can accurately be calculated when company entities and

uncertain challenges may be established. This also enables them to be addressed early in

order to produce lasting outcomes and development. The analysis of financial ratios for

quick financial decisions by creditors and involved parties is important. The following

explains the results of ALPHA LTD dependent on financial ratio analysis:

1. Return on Capital Employed:

It is a sort of financial ratio that helps to determine the effective usage of resources and

productivity for firms to make income from employed capital. This is a benefit measure utilized

by creditors on the most successful project at the point of the screening (Mio, 2016). To measure

the ratio of EBIT and net capital employed, two main things are needed. EBIT here applies to

earnings received before tax and interest rates are excluded. It is also regarded as company

income. The capital employed is determined by extracting from the valuation of the current

assets the balance of all existing liabilities.

Return on capital employed = EBIT or Operating Profit / Capital Employed

The operating profit of ALPHA LTD in 2017 is of £412000 and £375000 in 2018

respectively, which is calculated only from gross profit when deducting operating

expenditures. The total value of capital employed in 2018 was of 2925000 and 1912500

in 2017 which is calculated as gross assets minus all current liabilities. Therefore, the

business returned on working investments in 2018 and 2017 respectively at 14.10% and

19.60%. A fall in this ratio that suggests a drop in the return on investment. By growing

its corporate income, managing its operational costs and rising the resources employees,

the corporation will increase this ratio. Investor-specific factors are particularly important

when evaluating this formula while investing.

2. Net profit margin:

It is the profit remaining when all capital expenses, debt, royalties and preferred share

distributions have been excluded. In order to measure net profit margin, all such items are

fiscal and financial results. It helps to define risk and effects, to measure productivity, to

use output and the role of solvency. It helps to analyze patterns established over more than

one year across these ratios. Ratio analysis offers comprehensiveness in all facets of the

evaluation of financial statements. When evaluating different financial factors, the

consequences of current situations can accurately be calculated when company entities and

uncertain challenges may be established. This also enables them to be addressed early in

order to produce lasting outcomes and development. The analysis of financial ratios for

quick financial decisions by creditors and involved parties is important. The following

explains the results of ALPHA LTD dependent on financial ratio analysis:

1. Return on Capital Employed:

It is a sort of financial ratio that helps to determine the effective usage of resources and

productivity for firms to make income from employed capital. This is a benefit measure utilized

by creditors on the most successful project at the point of the screening (Mio, 2016). To measure

the ratio of EBIT and net capital employed, two main things are needed. EBIT here applies to

earnings received before tax and interest rates are excluded. It is also regarded as company

income. The capital employed is determined by extracting from the valuation of the current

assets the balance of all existing liabilities.

Return on capital employed = EBIT or Operating Profit / Capital Employed

The operating profit of ALPHA LTD in 2017 is of £412000 and £375000 in 2018

respectively, which is calculated only from gross profit when deducting operating

expenditures. The total value of capital employed in 2018 was of 2925000 and 1912500

in 2017 which is calculated as gross assets minus all current liabilities. Therefore, the

business returned on working investments in 2018 and 2017 respectively at 14.10% and

19.60%. A fall in this ratio that suggests a drop in the return on investment. By growing

its corporate income, managing its operational costs and rising the resources employees,

the corporation will increase this ratio. Investor-specific factors are particularly important

when evaluating this formula while investing.

2. Net profit margin:

It is the profit remaining when all capital expenses, debt, royalties and preferred share

distributions have been excluded. In order to measure net profit margin, all such items are

deleted from company total sales. It is a net profit-to-income ratio for a business. The profit

margin is in percentage form but can also be shown in decimal form for ease. It indicates how

much a corporation generates with one pound with sales through income. It is one of the main

variables of financial performance for businesses (Omar, Johari and Smith, 2017). Through

maintaining track of its net profit margin increase and decline, an organization may determine

whether its existing plans are successful or whether performance-based performance can be

expected. Investors can help to assess the status of a business if it is capable of raising profits

from revenue and whether the operating expenses and overhead costs are verified. The specific

industries, company growth ambitions, sustainability and scale are some significant

considerations deciding what a decent net profit margin in Alpha Ltd. The overall income margin

in 2017 was 12.5 percent, while the profit margin for 2018 was 8.75 percent, indicating that the

ratio dropped in 2018 compared with 2017, which is a negative indication to the business of

Alpha Ltd. The net income margin can be improved by decreased extra spending not part of core

operations, decreased goods and services that are not doing well, by raising clients and facilities

and at times, by increasing costs that are hard to determine, but essential for company

sustainability.

3. Current ratio:

The liquidity ratio measures an enterprise's capacity to fulfill its current assets' short-term

liabilities. This calculation is critical because it assess the liabilities of the company over the next

year. This warns the organization that its short-sighted liabilities must be fulfilled. The new

estimate for the ratio involves capital assets including currency, cash reserves and marketable

securities as they can be turned into cash in short time (Zeff, Van der Wel and Camfferman,

2016). Enterprises with a broad base of current assets can effectively repay existing liabilities as

they come due without the need to sell substantial long-term investments. The ratio of net assets

to current liabilities is clear. The optimal current ratio for a company is 2:1 for every sector. The

further value the present ratio will favour the company. This assumes the new 4:1 ratio implies

the net assets are 4 times liquid in contrast to total liabilities of Alpha limited. Had a current ratio

of 2.34 in 2017 and 0.93 in 2018, indicating that in 2017 it had more liquidity and that in 2018 it

was very illiquid. Alpha Ltd. Alpha Ltd. Can increase its current ratio by the implementation of

rapid conversion steps for debtors or debt accounts, through the settlement of existing liabilities,

margin is in percentage form but can also be shown in decimal form for ease. It indicates how

much a corporation generates with one pound with sales through income. It is one of the main

variables of financial performance for businesses (Omar, Johari and Smith, 2017). Through

maintaining track of its net profit margin increase and decline, an organization may determine

whether its existing plans are successful or whether performance-based performance can be

expected. Investors can help to assess the status of a business if it is capable of raising profits

from revenue and whether the operating expenses and overhead costs are verified. The specific

industries, company growth ambitions, sustainability and scale are some significant

considerations deciding what a decent net profit margin in Alpha Ltd. The overall income margin

in 2017 was 12.5 percent, while the profit margin for 2018 was 8.75 percent, indicating that the

ratio dropped in 2018 compared with 2017, which is a negative indication to the business of

Alpha Ltd. The net income margin can be improved by decreased extra spending not part of core

operations, decreased goods and services that are not doing well, by raising clients and facilities

and at times, by increasing costs that are hard to determine, but essential for company

sustainability.

3. Current ratio:

The liquidity ratio measures an enterprise's capacity to fulfill its current assets' short-term

liabilities. This calculation is critical because it assess the liabilities of the company over the next

year. This warns the organization that its short-sighted liabilities must be fulfilled. The new

estimate for the ratio involves capital assets including currency, cash reserves and marketable

securities as they can be turned into cash in short time (Zeff, Van der Wel and Camfferman,

2016). Enterprises with a broad base of current assets can effectively repay existing liabilities as

they come due without the need to sell substantial long-term investments. The ratio of net assets

to current liabilities is clear. The optimal current ratio for a company is 2:1 for every sector. The

further value the present ratio will favour the company. This assumes the new 4:1 ratio implies

the net assets are 4 times liquid in contrast to total liabilities of Alpha limited. Had a current ratio

of 2.34 in 2017 and 0.93 in 2018, indicating that in 2017 it had more liquidity and that in 2018 it

was very illiquid. Alpha Ltd. Alpha Ltd. Can increase its current ratio by the implementation of

rapid conversion steps for debtors or debt accounts, through the settlement of existing liabilities,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the reduction of unproductive properties, a increasing of shareholders resources to satisfy their

funding needs, and finally by sweeping bank accounts.

4. Debtor Collection Period:

It is the ratio which requires the debtor to pay the business by the time or days. This ratio

can effectively ensure suitability of cash to satisfy liabilities. This helps to understand the debtors

may be insolvent in the immediate term (Tang, Chen and Lin, 2016). The business can track the

quantity of bed loans and suspicious conditions by catching possible insolvent debtors early.

Managers can easily devise credit practices inside a corporate enterprise utilizing this measure.

In order for the business to function regularly, this ratio must be determined. The total amount to

be earned from industrial receivables or debtors' balance from the selling of credit is determined

from dividing it. The amount collected could be determined by the number of days to reach the

target. Alpha Ltd has accounts receivable in 2017 for trade of 450,000 and in 2018 of 600,000.

Company revenues in the year 2017 were 2400000 and 3000000 in 2018. Credit sales are

expected to be measured in the estimation of the overall percentage. The total 2018 collection

duration of the Company is 73 days and in 2017 it was 68 days. The estimated period for

collection is declined to suggest that the capacity of Alpha Ltd to recover debtors has dropped

and that it is possible that surplus capital would be inadequate to perform its operations in the

immediate future. By the lending revenue and maximizing the repayment cycle for its debtors,

the organization will increase this percentage.

5. Creditors Collection Period

It's a kind of financial ratio that indicates average days that the business pays its

borrowers and accounts payable. That involves investors, main lenders and other short-term

lending firms. The percentage is measured annually or monthly, so that indicates how much

longer time it takes the company's revenue outflows to cover the different debts. The greater

creditor collection duration (Williams and Dobelman, 2017). This is the company's liquidity

efficiency. This states the productivity declines and that the investors are reluctant to

compensate. This ratio often influences the credits word issued by the creditors. In the years

2017 and 2018 respectively, Alpha Ltd reported trade payable quantities of 285000 and 1050000.

For the years 2018 and 2017, business sales are 2400000 and 1350000. In this situation all retail

is considered to be on loan. The total length of payment for the organization in 2018 is 160 days,

funding needs, and finally by sweeping bank accounts.

4. Debtor Collection Period:

It is the ratio which requires the debtor to pay the business by the time or days. This ratio

can effectively ensure suitability of cash to satisfy liabilities. This helps to understand the debtors

may be insolvent in the immediate term (Tang, Chen and Lin, 2016). The business can track the

quantity of bed loans and suspicious conditions by catching possible insolvent debtors early.

Managers can easily devise credit practices inside a corporate enterprise utilizing this measure.

In order for the business to function regularly, this ratio must be determined. The total amount to

be earned from industrial receivables or debtors' balance from the selling of credit is determined

from dividing it. The amount collected could be determined by the number of days to reach the

target. Alpha Ltd has accounts receivable in 2017 for trade of 450,000 and in 2018 of 600,000.

Company revenues in the year 2017 were 2400000 and 3000000 in 2018. Credit sales are

expected to be measured in the estimation of the overall percentage. The total 2018 collection

duration of the Company is 73 days and in 2017 it was 68 days. The estimated period for

collection is declined to suggest that the capacity of Alpha Ltd to recover debtors has dropped

and that it is possible that surplus capital would be inadequate to perform its operations in the

immediate future. By the lending revenue and maximizing the repayment cycle for its debtors,

the organization will increase this percentage.

5. Creditors Collection Period

It's a kind of financial ratio that indicates average days that the business pays its

borrowers and accounts payable. That involves investors, main lenders and other short-term

lending firms. The percentage is measured annually or monthly, so that indicates how much

longer time it takes the company's revenue outflows to cover the different debts. The greater

creditor collection duration (Williams and Dobelman, 2017). This is the company's liquidity

efficiency. This states the productivity declines and that the investors are reluctant to

compensate. This ratio often influences the credits word issued by the creditors. In the years

2017 and 2018 respectively, Alpha Ltd reported trade payable quantities of 285000 and 1050000.

For the years 2018 and 2017, business sales are 2400000 and 1350000. In this situation all retail

is considered to be on loan. The total length of payment for the organization in 2018 is 160 days,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

it was 77 days. There has been an rise in the total repayment time that suggests that the company

has decreased its capacity to fund the numerous payment expenses.

CONCLUSION

On the basis of above task of project report this can be concluded that financial performance

of Alpha limited is in average condition. This is so because most of the ratios are showing

average result for year 2017 and 2018. In order to support, evaluation of financial

performance of above company different types of ratios are measured such as current ratio,

debtors’ collection period and many more.

has decreased its capacity to fund the numerous payment expenses.

CONCLUSION

On the basis of above task of project report this can be concluded that financial performance

of Alpha limited is in average condition. This is so because most of the ratios are showing

average result for year 2017 and 2018. In order to support, evaluation of financial

performance of above company different types of ratios are measured such as current ratio,

debtors’ collection period and many more.

REFERENCES

Books and journal:

Ball, R., 2013. Accounting informs investors and earnings management is rife: Two

questionable beliefs. Accounting Horizons. 27(4). pp.847-853.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Chiang, B., Nouri, H. and Samanta, S., 2014. The effects of different teaching approaches in

introductory financial accounting. Accounting Education. 23(1). pp.42-53.

Hope, O. K., Thomas, W. B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review. 88(5). pp.1715-1742.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics. 56(1). pp.130-147.

Lisowsky, P. and Minnis, M., 2018. The Silent majority: Private US firms and financial reporting

choices. Chicago Booth Research Paper, (14-01).

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Omar, N., Johari, Z. A. and Smith, M., 2017. Predicting fraudulent financial reporting using

artificial neural network. Journal of Financial Crime. 24(2). pp.362-387.

Tang, Q., Chen, H. and Lin, Z., 2016. How to measure country-level financial reporting quality?.

Journal of Financial Reporting and Accounting. 14(2). pp.230-265.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Zeff, S. A., Van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Online

Camden Group. 2019 [Online] Available Through. <https://www.camdengroup.co.uk/about>

Books and journal:

Ball, R., 2013. Accounting informs investors and earnings management is rife: Two

questionable beliefs. Accounting Horizons. 27(4). pp.847-853.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Chiang, B., Nouri, H. and Samanta, S., 2014. The effects of different teaching approaches in

introductory financial accounting. Accounting Education. 23(1). pp.42-53.

Hope, O. K., Thomas, W. B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review. 88(5). pp.1715-1742.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics. 56(1). pp.130-147.

Lisowsky, P. and Minnis, M., 2018. The Silent majority: Private US firms and financial reporting

choices. Chicago Booth Research Paper, (14-01).

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Omar, N., Johari, Z. A. and Smith, M., 2017. Predicting fraudulent financial reporting using

artificial neural network. Journal of Financial Crime. 24(2). pp.362-387.

Tang, Q., Chen, H. and Lin, Z., 2016. How to measure country-level financial reporting quality?.

Journal of Financial Reporting and Accounting. 14(2). pp.230-265.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Zeff, S. A., Van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Online

Camden Group. 2019 [Online] Available Through. <https://www.camdengroup.co.uk/about>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.