Financial Decision Making Report - FIN 7040, Autumn 2019, BPP Uni

VerifiedAdded on 2022/09/02

|23

|4663

|18

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making within the UK coffee industry. It begins with an industry review, identifying key players like Costa and Starbucks, and highlights industry trends, opportunities, and threats. The report then delves into a business performance analysis, including a detailed examination of the statement of profit or loss, statement of financial position, and statement of cash flows, along with ratio analysis. The operating cash cycle is calculated and discussed. Further, the report explores dividend policy, investment appraisal techniques such as payback period, accounting rate of return, and net present value, along with management forecasts. Finally, the report discusses various sources of finance, their advantages and disadvantages, and concludes with references. The analysis includes a detailed look at the financial statements, performance metrics, and strategic considerations relevant to financial decision-making.

FINANCIAL DECISION MAKING 1

FINANCIAL

DECISION

MAKING

FINANCIAL

DECISION

MAKING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL DECISION MAKING 2

Executive summary:

The report undertakes the discussion of the key players in the UK coffee industry, the threats

and the challenges that the company faces and the highlights of the UK coffee industry. This

is further accompanied with the ratio analysis, the advantages and the disadvantages of the

various techniques and discussion of the various sources of finance.

Executive summary:

The report undertakes the discussion of the key players in the UK coffee industry, the threats

and the challenges that the company faces and the highlights of the UK coffee industry. This

is further accompanied with the ratio analysis, the advantages and the disadvantages of the

various techniques and discussion of the various sources of finance.

FINANCIAL DECISION MAKING 3

Contents

Industry review:.........................................................................................................................4

Business performance analysis:.................................................................................................5

Statement of profit or loss:.....................................................................................................5

Statement of financial position:..............................................................................................7

Statement of cash flows:.......................................................................................................10

Operating cash cycle:...........................................................................................................12

Dividend policy:...................................................................................................................12

Investment Appraisal:..............................................................................................................13

Management forecast:..........................................................................................................13

Payback period:....................................................................................................................13

Accounting rate of return:....................................................................................................14

Net present value:.................................................................................................................15

Sources of finance:...................................................................................................................16

The following are its disadvantages:...................................................................................17

References:...............................................................................................................................19

Contents

Industry review:.........................................................................................................................4

Business performance analysis:.................................................................................................5

Statement of profit or loss:.....................................................................................................5

Statement of financial position:..............................................................................................7

Statement of cash flows:.......................................................................................................10

Operating cash cycle:...........................................................................................................12

Dividend policy:...................................................................................................................12

Investment Appraisal:..............................................................................................................13

Management forecast:..........................................................................................................13

Payback period:....................................................................................................................13

Accounting rate of return:....................................................................................................14

Net present value:.................................................................................................................15

Sources of finance:...................................................................................................................16

The following are its disadvantages:...................................................................................17

References:...............................................................................................................................19

FINANCIAL DECISION MAKING 4

Industry review:

The key players in the UK coffee industries are the following:

Costa Ltd,

Pret A Manger (Europe) Ltd,

Starbucks Coffee Company (UK) Limited and

Caffe Nero Group Holdings Ltd (IBIS world, 2019).

The following are the highlights of the UK coffee industry:

Keeping in mind Considering the fact that the coffee is grown close to equator, the

supply hence the domestic value chain starts with the importerimporters and the sale

agents as at the point of entry when entering into UK.into the UK

The imported coffee is being affected by many other channels to the consumer retail

and in home consumption.

Green coffee is being imported into UK. Even then, the supply chain arrangements

are in place and these are roasted coffee and soluble coffee which is of a greater value

from the rest of the world.

Majority share of the retail coffee is sold through hypermarkets and the supermarket

which accounts for 35% and 37% of all of the coffee retailing respectively.

UK is majorly known for instant coffee.

UK is mainly known for instant coffee but the volume sales of the instant coffee are

decreasing after the introduction of the wider products into the markets such as coffee

pods

The total estimated GVA contribution to the GDP of UK was £3.7 billion during the

year which is equal to 1/9th of the GVA of the entire food service sector.

The total estimated full time employees employed were 133,965 during the year 2017

in the UK coffee industry which is equal to 7.5% of the workforce of the entire

foodservice sector (British coffee association, 2018).

The following are the opportunities that are available for the company:

1. Expansion into the developing markets: The Companycompany has coffee houses

mainly in US and hence, there are many countries in which the brand could expand its

business operations in.

Industry review:

The key players in the UK coffee industries are the following:

Costa Ltd,

Pret A Manger (Europe) Ltd,

Starbucks Coffee Company (UK) Limited and

Caffe Nero Group Holdings Ltd (IBIS world, 2019).

The following are the highlights of the UK coffee industry:

Keeping in mind Considering the fact that the coffee is grown close to equator, the

supply hence the domestic value chain starts with the importerimporters and the sale

agents as at the point of entry when entering into UK.into the UK

The imported coffee is being affected by many other channels to the consumer retail

and in home consumption.

Green coffee is being imported into UK. Even then, the supply chain arrangements

are in place and these are roasted coffee and soluble coffee which is of a greater value

from the rest of the world.

Majority share of the retail coffee is sold through hypermarkets and the supermarket

which accounts for 35% and 37% of all of the coffee retailing respectively.

UK is majorly known for instant coffee.

UK is mainly known for instant coffee but the volume sales of the instant coffee are

decreasing after the introduction of the wider products into the markets such as coffee

pods

The total estimated GVA contribution to the GDP of UK was £3.7 billion during the

year which is equal to 1/9th of the GVA of the entire food service sector.

The total estimated full time employees employed were 133,965 during the year 2017

in the UK coffee industry which is equal to 7.5% of the workforce of the entire

foodservice sector (British coffee association, 2018).

The following are the opportunities that are available for the company:

1. Expansion into the developing markets: The Companycompany has coffee houses

mainly in US and hence, there are many countries in which the brand could expand its

business operations in.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL DECISION MAKING 5

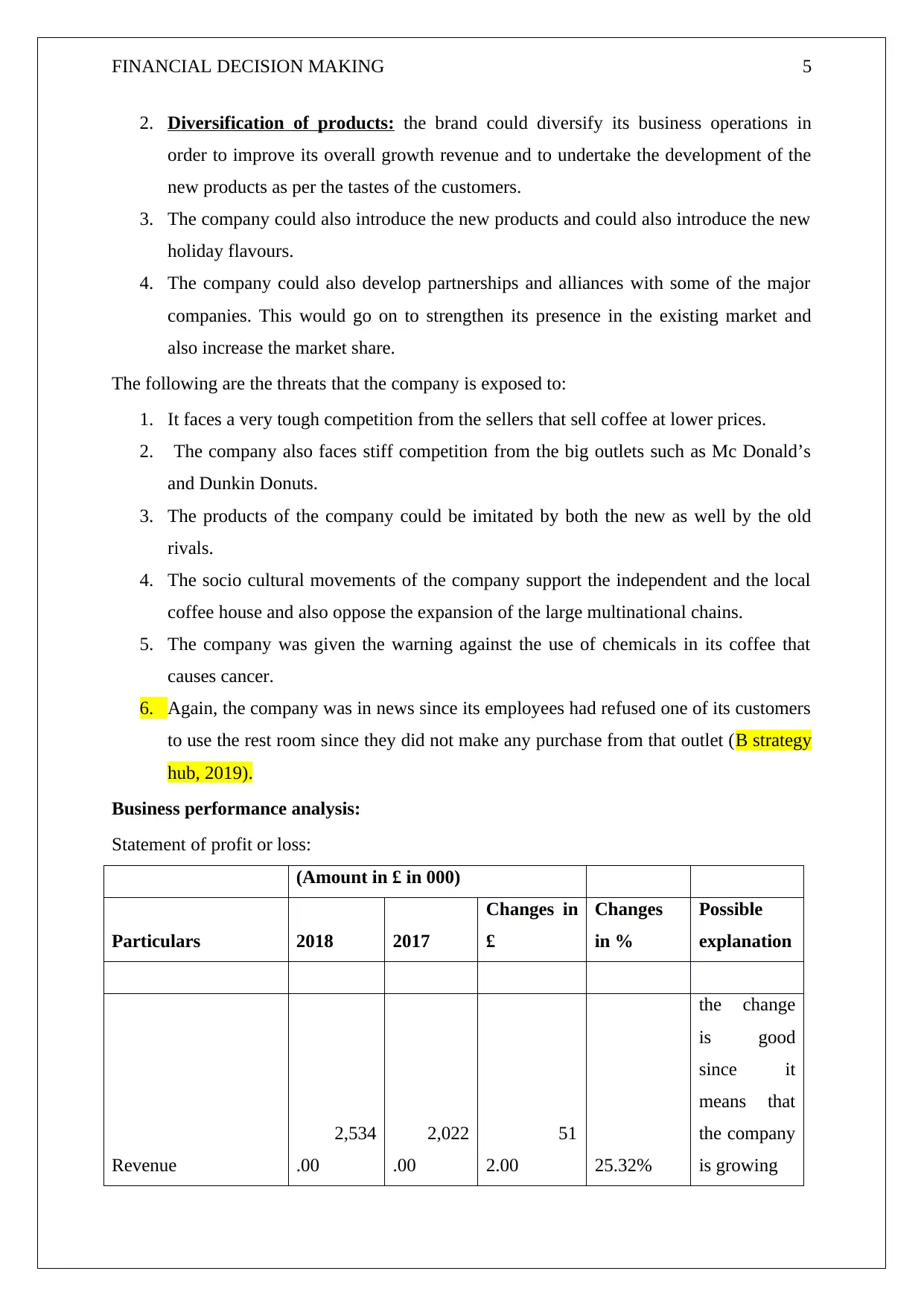

2. Diversification of products: the brand could diversify its business operations in

order to improve its overall growth revenue and to undertake the development of the

new products as per the tastes of the customers.

3. The company could also introduce the new products and could also introduce the new

holiday flavours.

4. The company could also develop partnerships and alliances with some of the major

companies. This would go on to strengthen its presence in the existing market and

also increase the market share.

The following are the threats that the company is exposed to:

1. It faces a very tough competition from the sellers that sell coffee at lower prices.

2. The company also faces stiff competition from the big outlets such as Mc Donald’s

and Dunkin Donuts.

3. The products of the company could be imitated by both the new as well by the old

rivals.

4. The socio cultural movements of the company support the independent and the local

coffee house and also oppose the expansion of the large multinational chains.

5. The company was given the warning against the use of chemicals in its coffee that

causes cancer.

6. Again, the company was in news since its employees had refused one of its customers

to use the rest room since they did not make any purchase from that outlet (B strategy

hub, 2019).

Business performance analysis:

Statement of profit or loss:

(Amount in £ in 000)

Particulars 2018 2017

Changes in

£

Changes

in %

Possible

explanation

Revenue

2,534

.00

2,022

.00

51

2.00 25.32%

the change

is good

since it

means that

the company

is growing

2. Diversification of products: the brand could diversify its business operations in

order to improve its overall growth revenue and to undertake the development of the

new products as per the tastes of the customers.

3. The company could also introduce the new products and could also introduce the new

holiday flavours.

4. The company could also develop partnerships and alliances with some of the major

companies. This would go on to strengthen its presence in the existing market and

also increase the market share.

The following are the threats that the company is exposed to:

1. It faces a very tough competition from the sellers that sell coffee at lower prices.

2. The company also faces stiff competition from the big outlets such as Mc Donald’s

and Dunkin Donuts.

3. The products of the company could be imitated by both the new as well by the old

rivals.

4. The socio cultural movements of the company support the independent and the local

coffee house and also oppose the expansion of the large multinational chains.

5. The company was given the warning against the use of chemicals in its coffee that

causes cancer.

6. Again, the company was in news since its employees had refused one of its customers

to use the rest room since they did not make any purchase from that outlet (B strategy

hub, 2019).

Business performance analysis:

Statement of profit or loss:

(Amount in £ in 000)

Particulars 2018 2017

Changes in

£

Changes

in %

Possible

explanation

Revenue

2,534

.00

2,022

.00

51

2.00 25.32%

the change

is good

since it

means that

the company

is growing

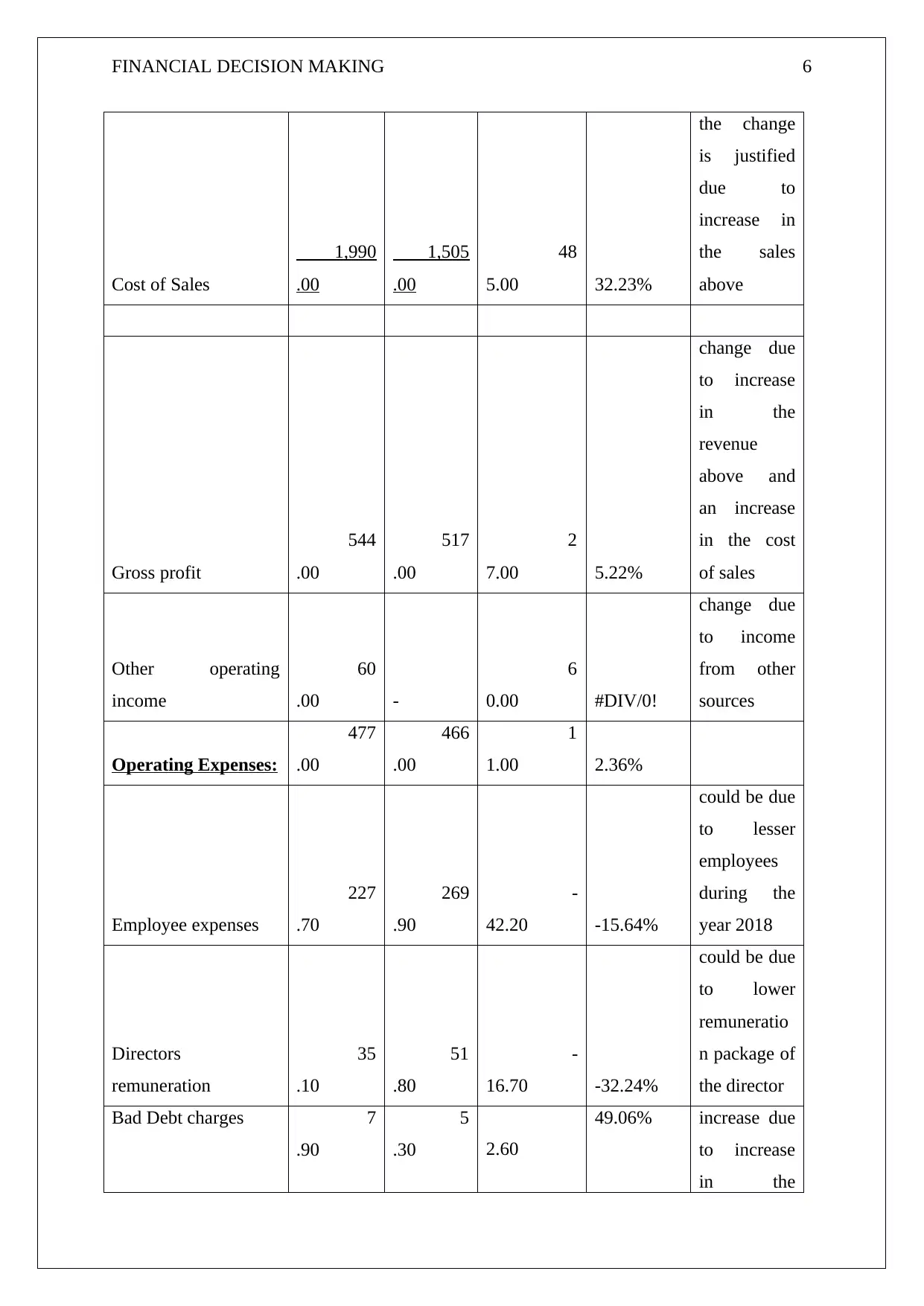

FINANCIAL DECISION MAKING 6

Cost of Sales

1,990

.00

1,505

.00

48

5.00 32.23%

the change

is justified

due to

increase in

the sales

above

Gross profit

544

.00

517

.00

2

7.00 5.22%

change due

to increase

in the

revenue

above and

an increase

in the cost

of sales

Other operating

income

60

.00 -

6

0.00 #DIV/0!

change due

to income

from other

sources

Operating Expenses:

477

.00

466

.00

1

1.00 2.36%

Employee expenses

227

.70

269

.90

-

42.20 -15.64%

could be due

to lesser

employees

during the

year 2018

Directors

remuneration

35

.10

51

.80

-

16.70 -32.24%

could be due

to lower

remuneratio

n package of

the director

Bad Debt charges 7

.90

5

.30 2.60

49.06% increase due

to increase

in the

Cost of Sales

1,990

.00

1,505

.00

48

5.00 32.23%

the change

is justified

due to

increase in

the sales

above

Gross profit

544

.00

517

.00

2

7.00 5.22%

change due

to increase

in the

revenue

above and

an increase

in the cost

of sales

Other operating

income

60

.00 -

6

0.00 #DIV/0!

change due

to income

from other

sources

Operating Expenses:

477

.00

466

.00

1

1.00 2.36%

Employee expenses

227

.70

269

.90

-

42.20 -15.64%

could be due

to lesser

employees

during the

year 2018

Directors

remuneration

35

.10

51

.80

-

16.70 -32.24%

could be due

to lower

remuneratio

n package of

the director

Bad Debt charges 7

.90

5

.30 2.60

49.06% increase due

to increase

in the

FINANCIAL DECISION MAKING 7

amount of

the revenue

Utility costs

22

.80

26

.20

-

3.40 -12.98%

increase due

to efficiency

on the part

of

management

Legal and

Professional fees

3

.60

28

.70

-

25.10 -87.46%

decrease due

to settlement

of the cases

and lower

suits

Depreciation charges

31

.70

20

.90

1

0.80 51.67%

increase due

to more

machinery

Store maintenance

72

.20

27

.60

4

4.60 161.59%

increase due

to expansion

in the

revenue

Distribution costs

29

.20

8

.90

2

0.30 228.09%

increase due

to more

sales

Marketing &

Advertising costs

46

.80

26

.70

2

0.10 75.28%

again due to

more sales

Operating

Profit/(Loss)

127

.00

51

.00

7

6.00 149.02%

increase due

to more

revenue

generated by

the company

during the

year 2018

Finance costs 26 6 2 333.33%

amount of

the revenue

Utility costs

22

.80

26

.20

-

3.40 -12.98%

increase due

to efficiency

on the part

of

management

Legal and

Professional fees

3

.60

28

.70

-

25.10 -87.46%

decrease due

to settlement

of the cases

and lower

suits

Depreciation charges

31

.70

20

.90

1

0.80 51.67%

increase due

to more

machinery

Store maintenance

72

.20

27

.60

4

4.60 161.59%

increase due

to expansion

in the

revenue

Distribution costs

29

.20

8

.90

2

0.30 228.09%

increase due

to more

sales

Marketing &

Advertising costs

46

.80

26

.70

2

0.10 75.28%

again due to

more sales

Operating

Profit/(Loss)

127

.00

51

.00

7

6.00 149.02%

increase due

to more

revenue

generated by

the company

during the

year 2018

Finance costs 26 6 2 333.33%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 8

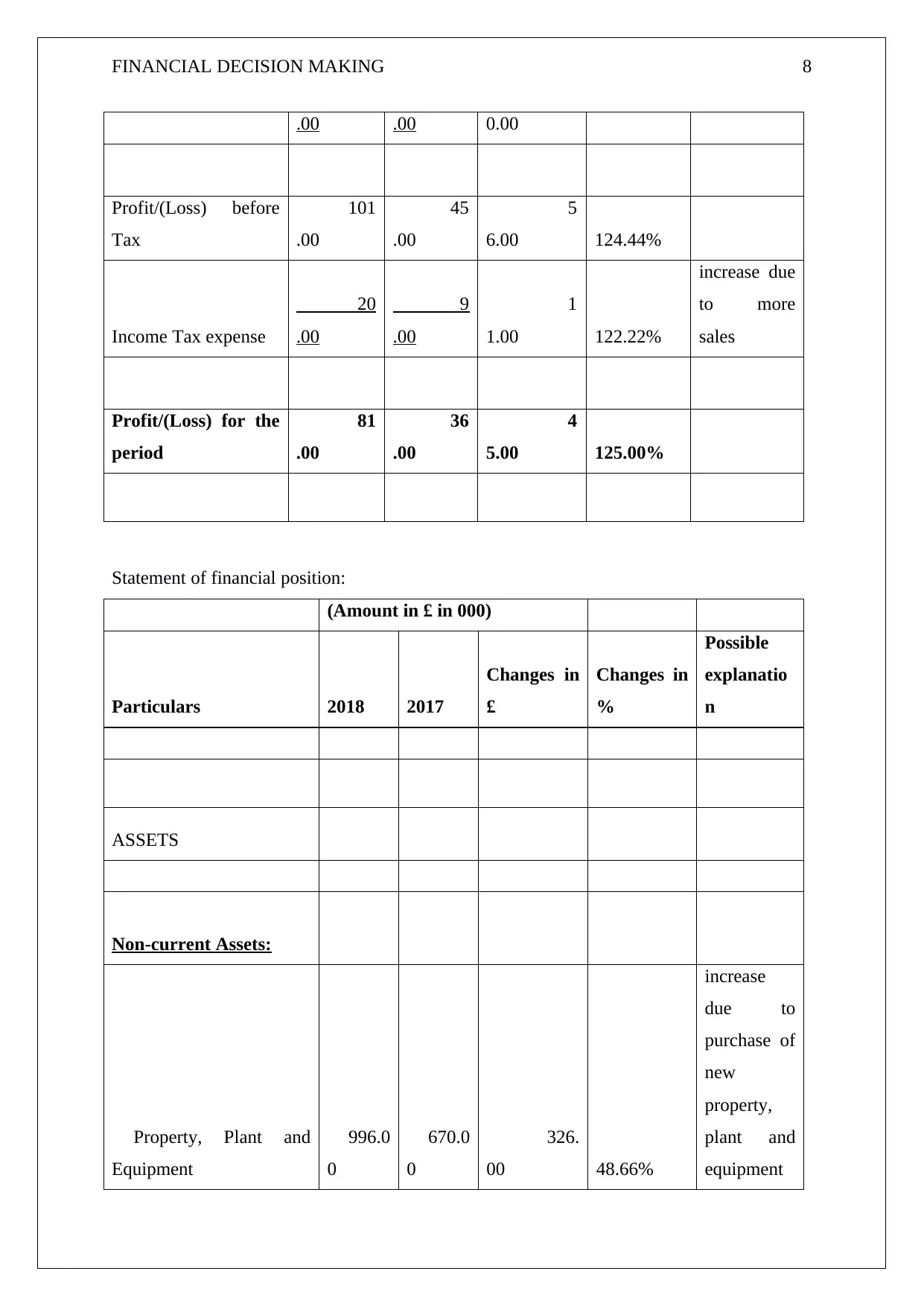

.00 .00 0.00

Profit/(Loss) before

Tax

101

.00

45

.00

5

6.00 124.44%

Income Tax expense

20

.00

9

.00

1

1.00 122.22%

increase due

to more

sales

Profit/(Loss) for the

period

81

.00

36

.00

4

5.00 125.00%

Statement of financial position:

(Amount in £ in 000)

Particulars 2018 2017

Changes in

£

Changes in

%

Possible

explanatio

n

ASSETS

Non-current Assets:

Property, Plant and

Equipment

996.0

0

670.0

0

326.

00 48.66%

increase

due to

purchase of

new

property,

plant and

equipment

.00 .00 0.00

Profit/(Loss) before

Tax

101

.00

45

.00

5

6.00 124.44%

Income Tax expense

20

.00

9

.00

1

1.00 122.22%

increase due

to more

sales

Profit/(Loss) for the

period

81

.00

36

.00

4

5.00 125.00%

Statement of financial position:

(Amount in £ in 000)

Particulars 2018 2017

Changes in

£

Changes in

%

Possible

explanatio

n

ASSETS

Non-current Assets:

Property, Plant and

Equipment

996.0

0

670.0

0

326.

00 48.66%

increase

due to

purchase of

new

property,

plant and

equipment

FINANCIAL DECISION MAKING 9

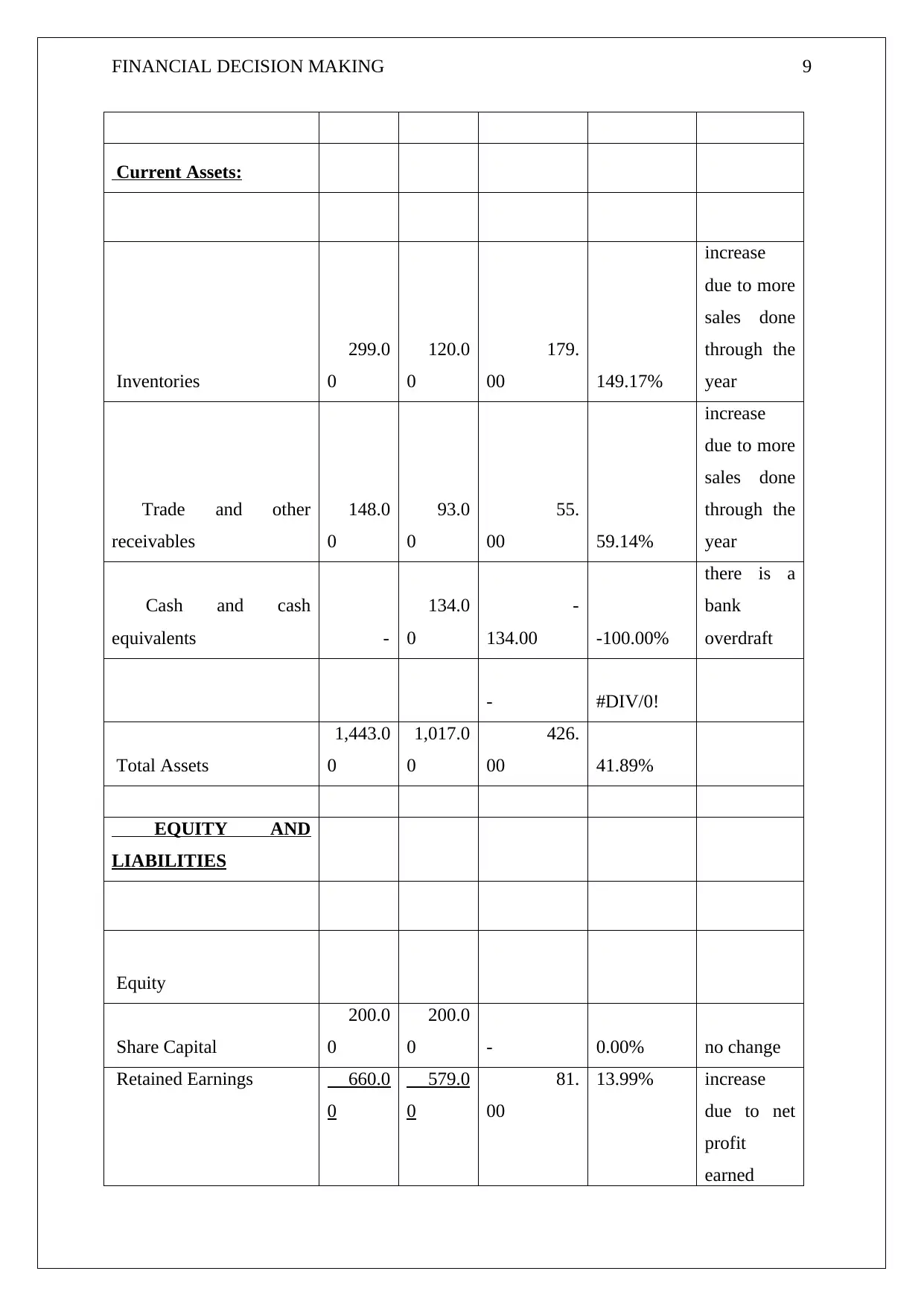

Current Assets:

Inventories

299.0

0

120.0

0

179.

00 149.17%

increase

due to more

sales done

through the

year

Trade and other

receivables

148.0

0

93.0

0

55.

00 59.14%

increase

due to more

sales done

through the

year

Cash and cash

equivalents -

134.0

0

-

134.00 -100.00%

there is a

bank

overdraft

- #DIV/0!

Total Assets

1,443.0

0

1,017.0

0

426.

00 41.89%

EQUITY AND

LIABILITIES

Equity

Share Capital

200.0

0

200.0

0 - 0.00% no change

Retained Earnings 660.0

0

579.0

0

81.

00

13.99% increase

due to net

profit

earned

Current Assets:

Inventories

299.0

0

120.0

0

179.

00 149.17%

increase

due to more

sales done

through the

year

Trade and other

receivables

148.0

0

93.0

0

55.

00 59.14%

increase

due to more

sales done

through the

year

Cash and cash

equivalents -

134.0

0

-

134.00 -100.00%

there is a

bank

overdraft

- #DIV/0!

Total Assets

1,443.0

0

1,017.0

0

426.

00 41.89%

EQUITY AND

LIABILITIES

Equity

Share Capital

200.0

0

200.0

0 - 0.00% no change

Retained Earnings 660.0

0

579.0

0

81.

00

13.99% increase

due to net

profit

earned

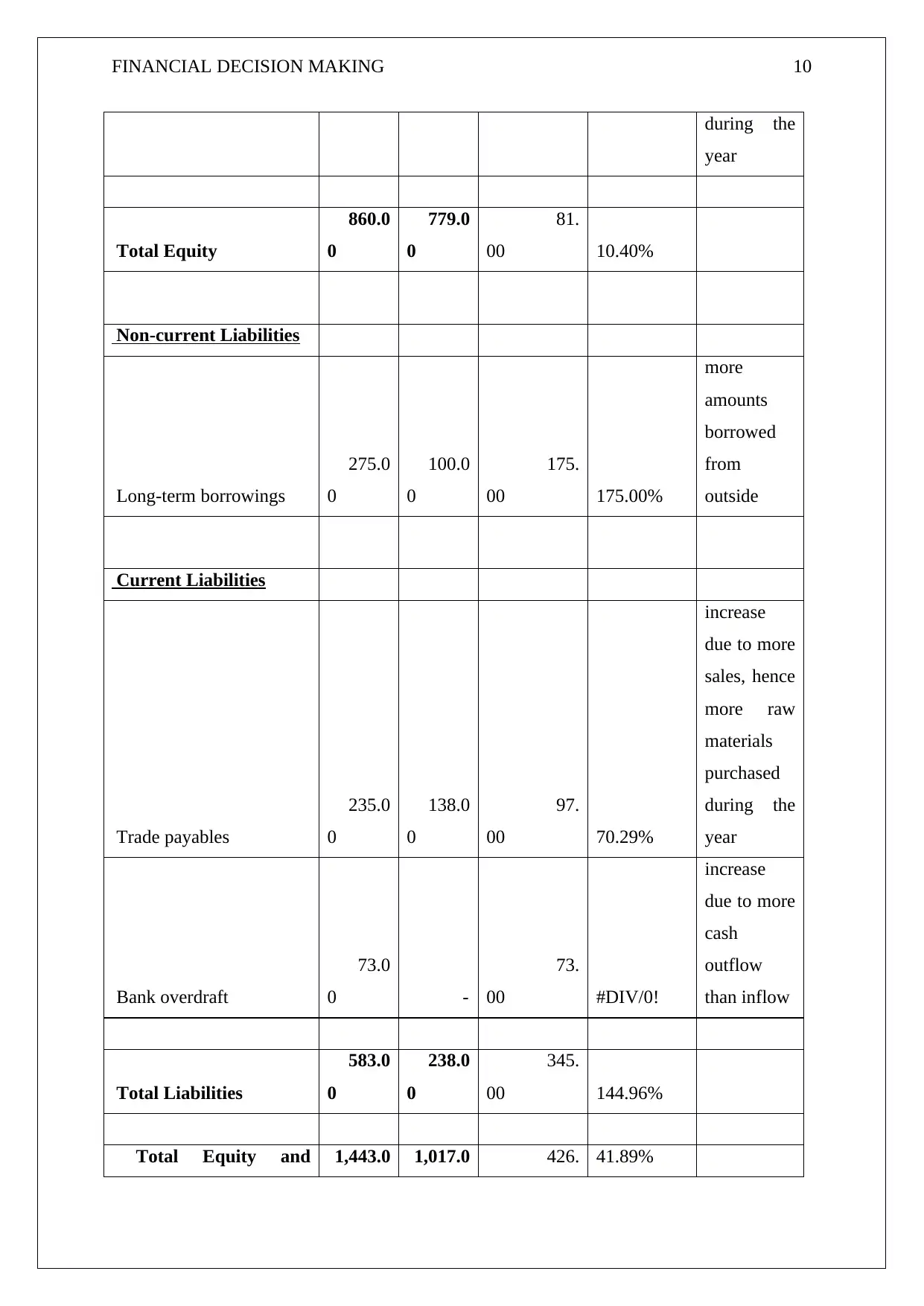

FINANCIAL DECISION MAKING 10

during the

year

Total Equity

860.0

0

779.0

0

81.

00 10.40%

Non-current Liabilities

Long-term borrowings

275.0

0

100.0

0

175.

00 175.00%

more

amounts

borrowed

from

outside

Current Liabilities

Trade payables

235.0

0

138.0

0

97.

00 70.29%

increase

due to more

sales, hence

more raw

materials

purchased

during the

year

Bank overdraft

73.0

0 -

73.

00 #DIV/0!

increase

due to more

cash

outflow

than inflow

Total Liabilities

583.0

0

238.0

0

345.

00 144.96%

Total Equity and 1,443.0 1,017.0 426. 41.89%

during the

year

Total Equity

860.0

0

779.0

0

81.

00 10.40%

Non-current Liabilities

Long-term borrowings

275.0

0

100.0

0

175.

00 175.00%

more

amounts

borrowed

from

outside

Current Liabilities

Trade payables

235.0

0

138.0

0

97.

00 70.29%

increase

due to more

sales, hence

more raw

materials

purchased

during the

year

Bank overdraft

73.0

0 -

73.

00 #DIV/0!

increase

due to more

cash

outflow

than inflow

Total Liabilities

583.0

0

238.0

0

345.

00 144.96%

Total Equity and 1,443.0 1,017.0 426. 41.89%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

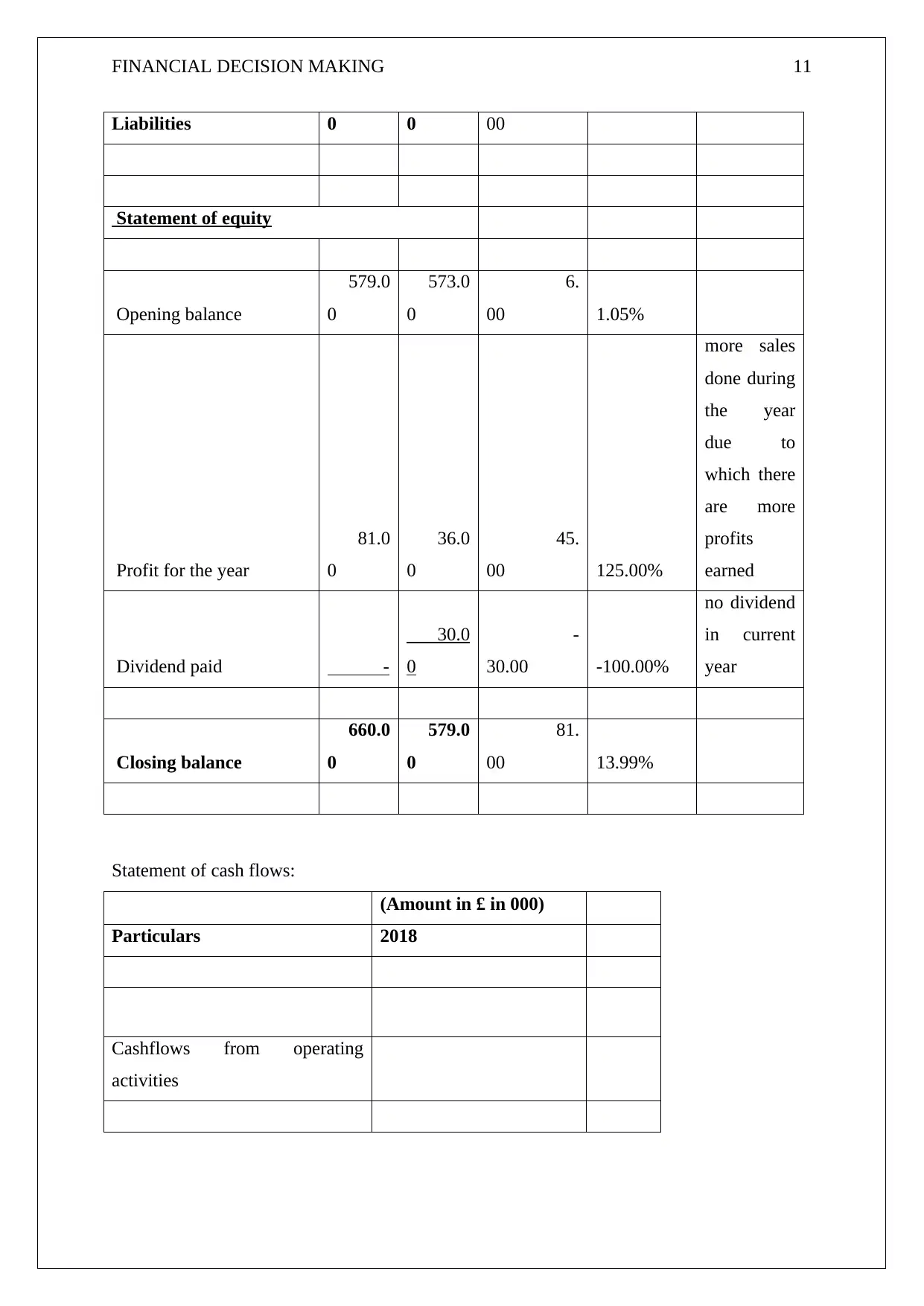

FINANCIAL DECISION MAKING 11

Liabilities 0 0 00

Statement of equity

Opening balance

579.0

0

573.0

0

6.

00 1.05%

Profit for the year

81.0

0

36.0

0

45.

00 125.00%

more sales

done during

the year

due to

which there

are more

profits

earned

Dividend paid -

30.0

0

-

30.00 -100.00%

no dividend

in current

year

Closing balance

660.0

0

579.0

0

81.

00 13.99%

Statement of cash flows:

(Amount in £ in 000)

Particulars 2018

Cashflows from operating

activities

Liabilities 0 0 00

Statement of equity

Opening balance

579.0

0

573.0

0

6.

00 1.05%

Profit for the year

81.0

0

36.0

0

45.

00 125.00%

more sales

done during

the year

due to

which there

are more

profits

earned

Dividend paid -

30.0

0

-

30.00 -100.00%

no dividend

in current

year

Closing balance

660.0

0

579.0

0

81.

00 13.99%

Statement of cash flows:

(Amount in £ in 000)

Particulars 2018

Cashflows from operating

activities

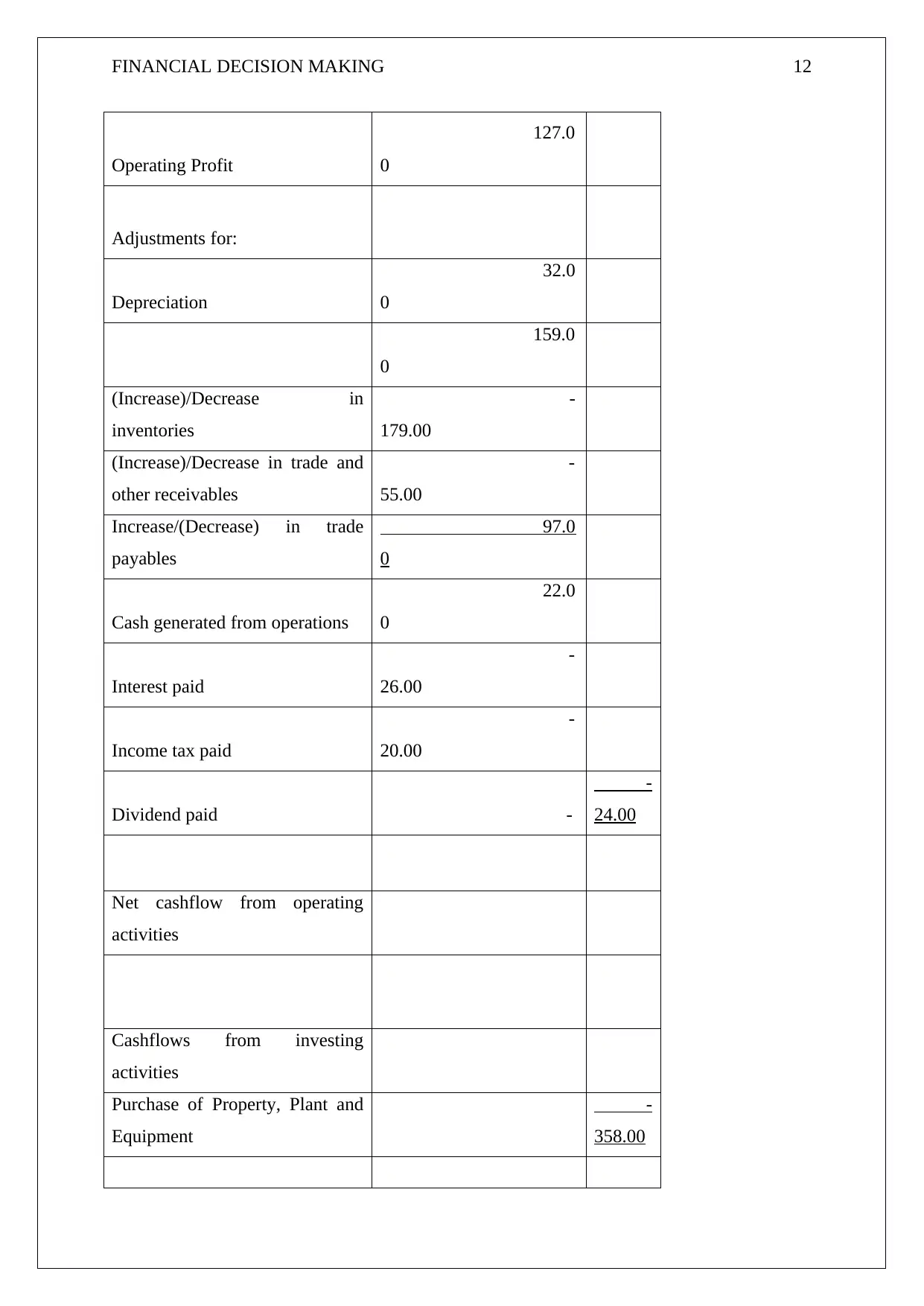

FINANCIAL DECISION MAKING 12

Operating Profit

127.0

0

Adjustments for:

Depreciation

32.0

0

159.0

0

(Increase)/Decrease in

inventories

-

179.00

(Increase)/Decrease in trade and

other receivables

-

55.00

Increase/(Decrease) in trade

payables

97.0

0

Cash generated from operations

22.0

0

Interest paid

-

26.00

Income tax paid

-

20.00

Dividend paid -

-

24.00

Net cashflow from operating

activities

Cashflows from investing

activities

Purchase of Property, Plant and

Equipment

-

358.00

Operating Profit

127.0

0

Adjustments for:

Depreciation

32.0

0

159.0

0

(Increase)/Decrease in

inventories

-

179.00

(Increase)/Decrease in trade and

other receivables

-

55.00

Increase/(Decrease) in trade

payables

97.0

0

Cash generated from operations

22.0

0

Interest paid

-

26.00

Income tax paid

-

20.00

Dividend paid -

-

24.00

Net cashflow from operating

activities

Cashflows from investing

activities

Purchase of Property, Plant and

Equipment

-

358.00

FINANCIAL DECISION MAKING 13

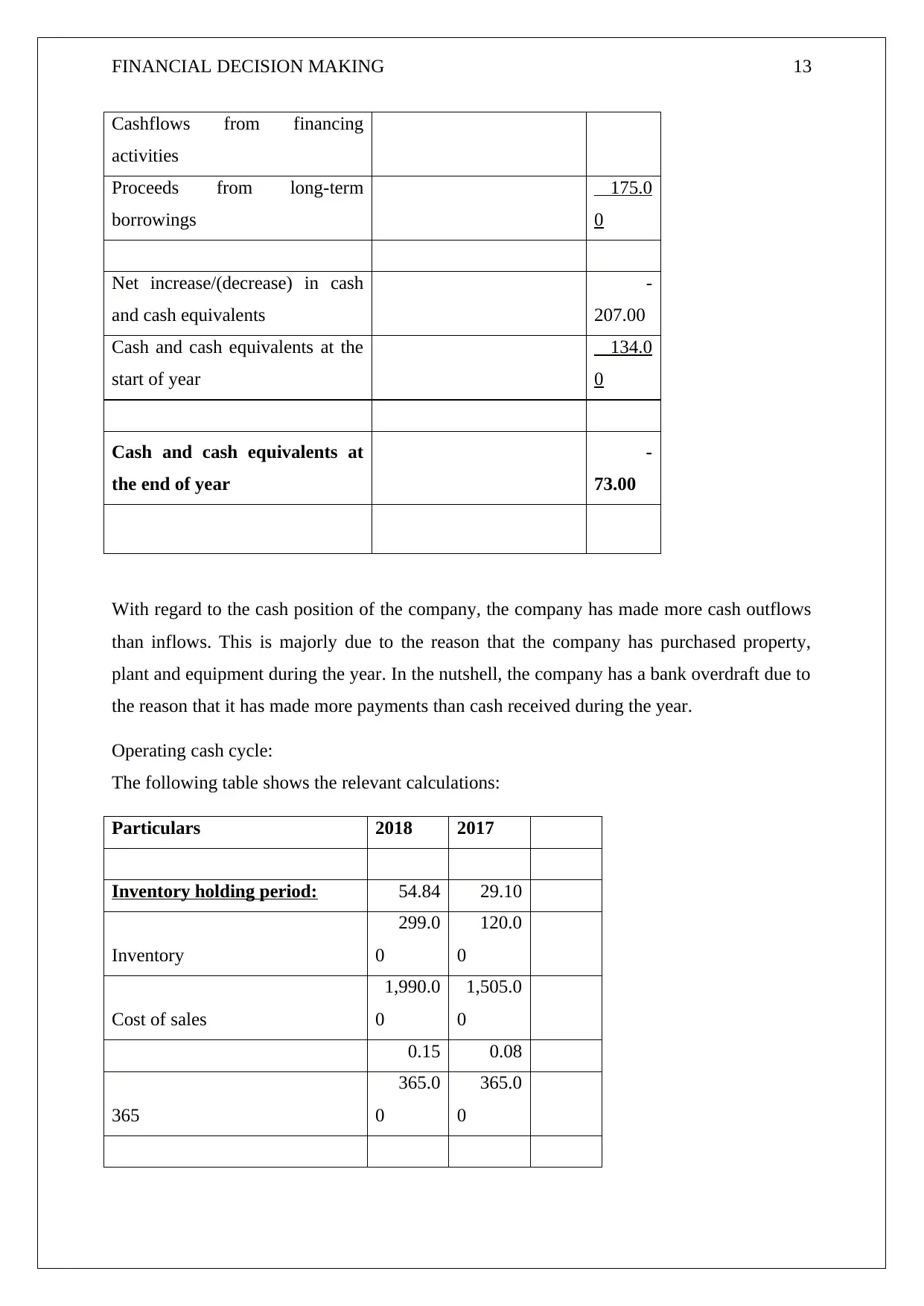

Cashflows from financing

activities

Proceeds from long-term

borrowings

175.0

0

Net increase/(decrease) in cash

and cash equivalents

-

207.00

Cash and cash equivalents at the

start of year

134.0

0

Cash and cash equivalents at

the end of year

-

73.00

With regard to the cash position of the company, the company has made more cash outflows

than inflows. This is majorly due to the reason that the company has purchased property,

plant and equipment during the year. In the nutshell, the company has a bank overdraft due to

the reason that it has made more payments than cash received during the year.

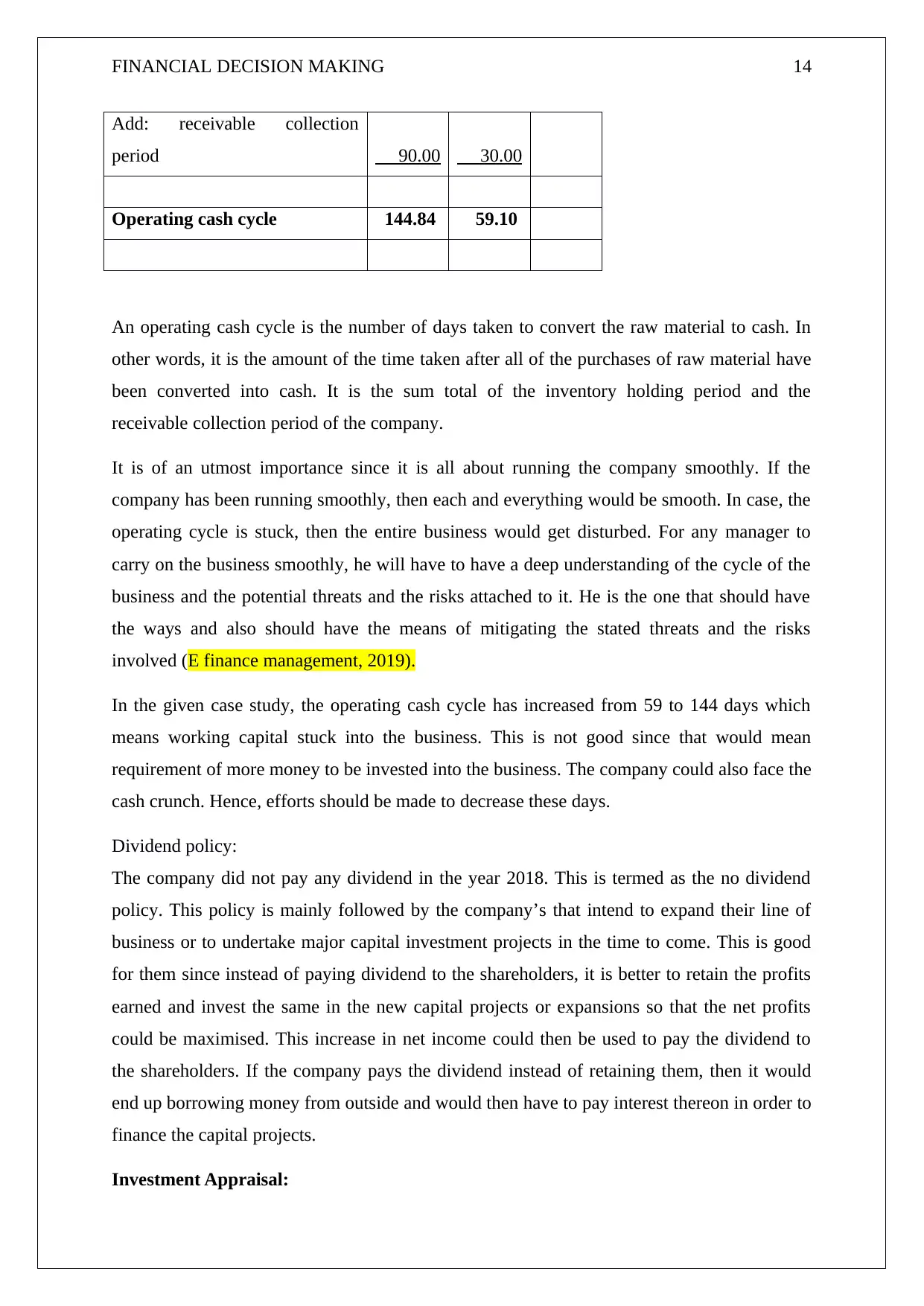

Operating cash cycle:

The following table shows the relevant calculations:

Particulars 2018 2017

Inventory holding period: 54.84 29.10

Inventory

299.0

0

120.0

0

Cost of sales

1,990.0

0

1,505.0

0

0.15 0.08

365

365.0

0

365.0

0

Cashflows from financing

activities

Proceeds from long-term

borrowings

175.0

0

Net increase/(decrease) in cash

and cash equivalents

-

207.00

Cash and cash equivalents at the

start of year

134.0

0

Cash and cash equivalents at

the end of year

-

73.00

With regard to the cash position of the company, the company has made more cash outflows

than inflows. This is majorly due to the reason that the company has purchased property,

plant and equipment during the year. In the nutshell, the company has a bank overdraft due to

the reason that it has made more payments than cash received during the year.

Operating cash cycle:

The following table shows the relevant calculations:

Particulars 2018 2017

Inventory holding period: 54.84 29.10

Inventory

299.0

0

120.0

0

Cost of sales

1,990.0

0

1,505.0

0

0.15 0.08

365

365.0

0

365.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 14

Add: receivable collection

period 90.00 30.00

Operating cash cycle 144.84 59.10

An operating cash cycle is the number of days taken to convert the raw material to cash. In

other words, it is the amount of the time taken after all of the purchases of raw material have

been converted into cash. It is the sum total of the inventory holding period and the

receivable collection period of the company.

It is of an utmost importance since it is all about running the company smoothly. If the

company has been running smoothly, then each and everything would be smooth. In case, the

operating cycle is stuck, then the entire business would get disturbed. For any manager to

carry on the business smoothly, he will have to have a deep understanding of the cycle of the

business and the potential threats and the risks attached to it. He is the one that should have

the ways and also should have the means of mitigating the stated threats and the risks

involved (E finance management, 2019).

In the given case study, the operating cash cycle has increased from 59 to 144 days which

means working capital stuck into the business. This is not good since that would mean

requirement of more money to be invested into the business. The company could also face the

cash crunch. Hence, efforts should be made to decrease these days.

Dividend policy:

The company did not pay any dividend in the year 2018. This is termed as the no dividend

policy. This policy is mainly followed by the company’s that intend to expand their line of

business or to undertake major capital investment projects in the time to come. This is good

for them since instead of paying dividend to the shareholders, it is better to retain the profits

earned and invest the same in the new capital projects or expansions so that the net profits

could be maximised. This increase in net income could then be used to pay the dividend to

the shareholders. If the company pays the dividend instead of retaining them, then it would

end up borrowing money from outside and would then have to pay interest thereon in order to

finance the capital projects.

Investment Appraisal:

Add: receivable collection

period 90.00 30.00

Operating cash cycle 144.84 59.10

An operating cash cycle is the number of days taken to convert the raw material to cash. In

other words, it is the amount of the time taken after all of the purchases of raw material have

been converted into cash. It is the sum total of the inventory holding period and the

receivable collection period of the company.

It is of an utmost importance since it is all about running the company smoothly. If the

company has been running smoothly, then each and everything would be smooth. In case, the

operating cycle is stuck, then the entire business would get disturbed. For any manager to

carry on the business smoothly, he will have to have a deep understanding of the cycle of the

business and the potential threats and the risks attached to it. He is the one that should have

the ways and also should have the means of mitigating the stated threats and the risks

involved (E finance management, 2019).

In the given case study, the operating cash cycle has increased from 59 to 144 days which

means working capital stuck into the business. This is not good since that would mean

requirement of more money to be invested into the business. The company could also face the

cash crunch. Hence, efforts should be made to decrease these days.

Dividend policy:

The company did not pay any dividend in the year 2018. This is termed as the no dividend

policy. This policy is mainly followed by the company’s that intend to expand their line of

business or to undertake major capital investment projects in the time to come. This is good

for them since instead of paying dividend to the shareholders, it is better to retain the profits

earned and invest the same in the new capital projects or expansions so that the net profits

could be maximised. This increase in net income could then be used to pay the dividend to

the shareholders. If the company pays the dividend instead of retaining them, then it would

end up borrowing money from outside and would then have to pay interest thereon in order to

finance the capital projects.

Investment Appraisal:

FINANCIAL DECISION MAKING 15

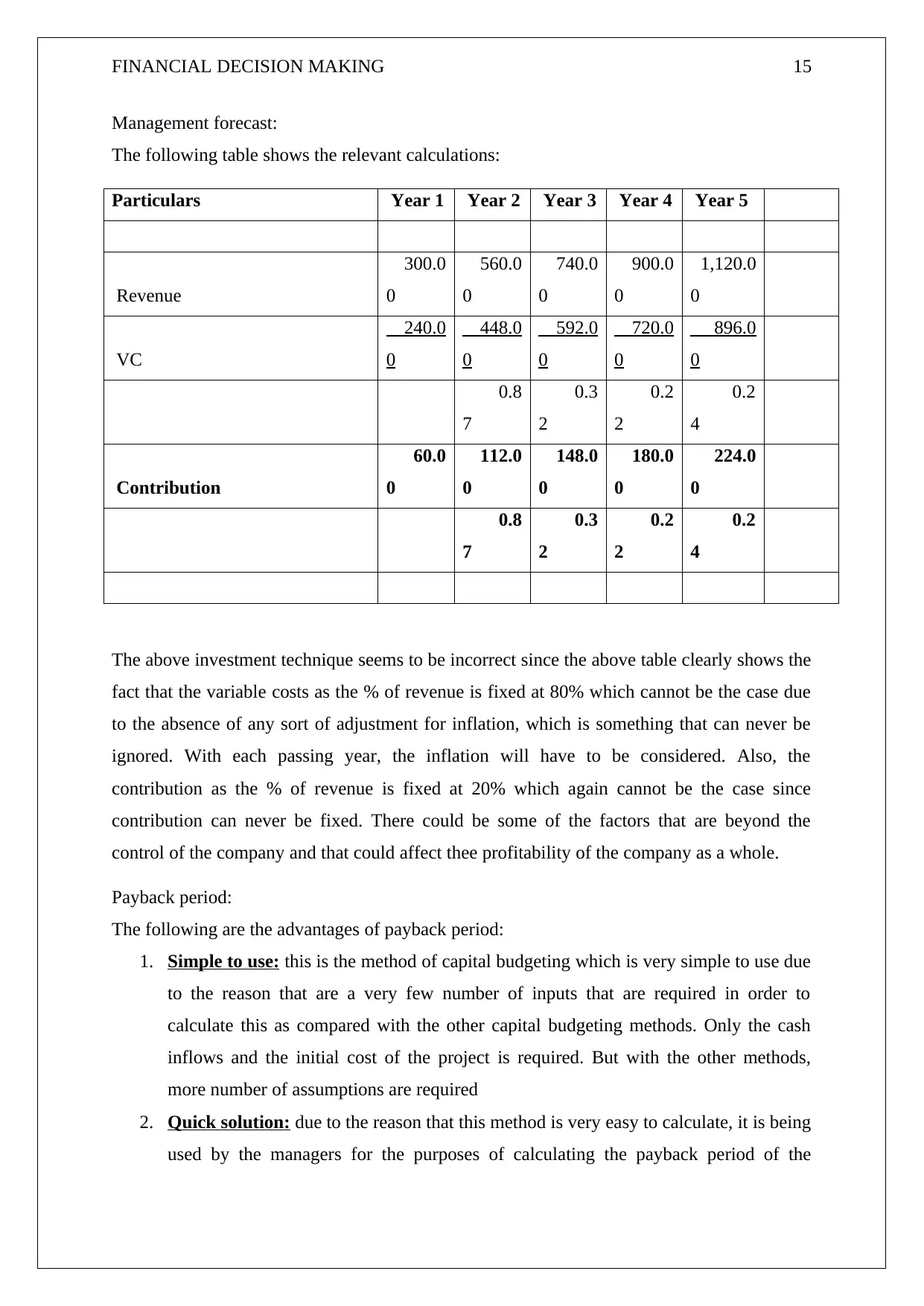

Management forecast:

The following table shows the relevant calculations:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Revenue

300.0

0

560.0

0

740.0

0

900.0

0

1,120.0

0

VC

240.0

0

448.0

0

592.0

0

720.0

0

896.0

0

0.8

7

0.3

2

0.2

2

0.2

4

Contribution

60.0

0

112.0

0

148.0

0

180.0

0

224.0

0

0.8

7

0.3

2

0.2

2

0.2

4

The above investment technique seems to be incorrect since the above table clearly shows the

fact that the variable costs as the % of revenue is fixed at 80% which cannot be the case due

to the absence of any sort of adjustment for inflation, which is something that can never be

ignored. With each passing year, the inflation will have to be considered. Also, the

contribution as the % of revenue is fixed at 20% which again cannot be the case since

contribution can never be fixed. There could be some of the factors that are beyond the

control of the company and that could affect thee profitability of the company as a whole.

Payback period:

The following are the advantages of payback period:

1. Simple to use: this is the method of capital budgeting which is very simple to use due

to the reason that are a very few number of inputs that are required in order to

calculate this as compared with the other capital budgeting methods. Only the cash

inflows and the initial cost of the project is required. But with the other methods,

more number of assumptions are required

2. Quick solution: due to the reason that this method is very easy to calculate, it is being

used by the managers for the purposes of calculating the payback period of the

Management forecast:

The following table shows the relevant calculations:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Revenue

300.0

0

560.0

0

740.0

0

900.0

0

1,120.0

0

VC

240.0

0

448.0

0

592.0

0

720.0

0

896.0

0

0.8

7

0.3

2

0.2

2

0.2

4

Contribution

60.0

0

112.0

0

148.0

0

180.0

0

224.0

0

0.8

7

0.3

2

0.2

2

0.2

4

The above investment technique seems to be incorrect since the above table clearly shows the

fact that the variable costs as the % of revenue is fixed at 80% which cannot be the case due

to the absence of any sort of adjustment for inflation, which is something that can never be

ignored. With each passing year, the inflation will have to be considered. Also, the

contribution as the % of revenue is fixed at 20% which again cannot be the case since

contribution can never be fixed. There could be some of the factors that are beyond the

control of the company and that could affect thee profitability of the company as a whole.

Payback period:

The following are the advantages of payback period:

1. Simple to use: this is the method of capital budgeting which is very simple to use due

to the reason that are a very few number of inputs that are required in order to

calculate this as compared with the other capital budgeting methods. Only the cash

inflows and the initial cost of the project is required. But with the other methods,

more number of assumptions are required

2. Quick solution: due to the reason that this method is very easy to calculate, it is being

used by the managers for the purposes of calculating the payback period of the

FINANCIAL DECISION MAKING 16

projects. These help the manager in making the quick decisions and this is something

which could prove to be helpful for the companies that have an access to a very

limited number of resources.

3. Preferences for liquidity: this method provides the most important information with

regard to the riskiness of the project. This is mainly due to the reason that the project

that is of a shorter duration is exposed to a lower amount of risk and hence, an

information like this could prove to be helpful for the company and then, the company

could use its limited amount of the resources in the most meaningful manner.

4. UncertaintyUseful in the case of uncertainty: this method could be used when the

industries are uncertain or that are exposed to rapid changes in technologies. When

there is so much uncertainty, then t becomes tough to predict the annual cash inflows

and hence, this method helps in the reduction of the chances of loss for the

companies.

The following are the disadvantages of this method:

1. Ignores time value of money: this is the method that ignores the time value of

money which is very important for the business. As per this concept, the money that is

being received today would be of worth less in the future period and when the

company fails to consider this, then that would mean change or distorted cash flows.

Hence, the true value of the cash inflows cannot be considered.

2. Cash flows are not covered: not all of the cash flows are covered under this method.

Only the cash outflow till the time of making the investment is recovered. The cash

flows in the later years are not considered. Facts like these could lead the company in

wasting its limited amount of the resources.

3. Not realistic: this is the technique which is so simple that the normal business

scenarios cannot be considered. Making of the capital investments is just a onetime

thing. Instead, projects would require more investments in the years to come with the

irregular cash flows (Small business chron, 2019).

4. Ignore profitability: it is not necessary that the project that is of a shorter duration is

profitable. The decision using only this method could prove to be false in case the

cash inflows stop in between the project or the same gets reduced after the payback

period. Also, the return on investment from the project is neglected since the

companies require the capital investments to earn the return well over the period of

time and also more than the required rate of return. But this method ignores the

projects rate of return (E finance management, 2019).

projects. These help the manager in making the quick decisions and this is something

which could prove to be helpful for the companies that have an access to a very

limited number of resources.

3. Preferences for liquidity: this method provides the most important information with

regard to the riskiness of the project. This is mainly due to the reason that the project

that is of a shorter duration is exposed to a lower amount of risk and hence, an

information like this could prove to be helpful for the company and then, the company

could use its limited amount of the resources in the most meaningful manner.

4. UncertaintyUseful in the case of uncertainty: this method could be used when the

industries are uncertain or that are exposed to rapid changes in technologies. When

there is so much uncertainty, then t becomes tough to predict the annual cash inflows

and hence, this method helps in the reduction of the chances of loss for the

companies.

The following are the disadvantages of this method:

1. Ignores time value of money: this is the method that ignores the time value of

money which is very important for the business. As per this concept, the money that is

being received today would be of worth less in the future period and when the

company fails to consider this, then that would mean change or distorted cash flows.

Hence, the true value of the cash inflows cannot be considered.

2. Cash flows are not covered: not all of the cash flows are covered under this method.

Only the cash outflow till the time of making the investment is recovered. The cash

flows in the later years are not considered. Facts like these could lead the company in

wasting its limited amount of the resources.

3. Not realistic: this is the technique which is so simple that the normal business

scenarios cannot be considered. Making of the capital investments is just a onetime

thing. Instead, projects would require more investments in the years to come with the

irregular cash flows (Small business chron, 2019).

4. Ignore profitability: it is not necessary that the project that is of a shorter duration is

profitable. The decision using only this method could prove to be false in case the

cash inflows stop in between the project or the same gets reduced after the payback

period. Also, the return on investment from the project is neglected since the

companies require the capital investments to earn the return well over the period of

time and also more than the required rate of return. But this method ignores the

projects rate of return (E finance management, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL DECISION MAKING 17

With regard to the From the point of view of payback period, which comes out to be 4 years,

the project is good when it comes to making an investment since the life of the project or the

revenue has been estimated for 5 years but the initial investment can be recovered within 4

years which is though not good, but fine.

Accounting rate of return:

This is the rate of return which is generated by the investment proposal rather than the cash

flows that are used for the purposes of evaluating the cash flows.

The following are the advantages of this method:

1. This is method which is very simple and is also straight forward when it comes to

computation

2. This method concentrates on the calculation of the net operating income. The

creditors and the investors use this method for the purposes of evaluating the

performance of the management.

The following are the disadvantages of using this method:

1. This technique of capital budgeting does not considertake into account the time value

of money. Under this method, the dollar amount in hand and the dollar amount to be

received in the future are assumed to be equal.

2. Cash is of an utmost importance for the companies but the ARRaccounting rate of

return does not consider this and concentrates only on the accounting net operating

income from the project rather than the cash flows.

3. This rate of equityreturn does not remain constant over the useful life of the project.

Hence, a project which seems to be desirable at one point of time may not be

desirable at another point of time (Accounting for management, 2019).

From the point of view of accounting rate of return, the target rate of return for the company

comes out to be 10% whereas the accounting rate of return for the project comes out to be

18% which is more than the target rate of return for the company. Hence, the project should

be accepted.

With regard to the From the point of view of payback period, which comes out to be 4 years,

the project is good when it comes to making an investment since the life of the project or the

revenue has been estimated for 5 years but the initial investment can be recovered within 4

years which is though not good, but fine.

Accounting rate of return:

This is the rate of return which is generated by the investment proposal rather than the cash

flows that are used for the purposes of evaluating the cash flows.

The following are the advantages of this method:

1. This is method which is very simple and is also straight forward when it comes to

computation

2. This method concentrates on the calculation of the net operating income. The

creditors and the investors use this method for the purposes of evaluating the

performance of the management.

The following are the disadvantages of using this method:

1. This technique of capital budgeting does not considertake into account the time value

of money. Under this method, the dollar amount in hand and the dollar amount to be

received in the future are assumed to be equal.

2. Cash is of an utmost importance for the companies but the ARRaccounting rate of

return does not consider this and concentrates only on the accounting net operating

income from the project rather than the cash flows.

3. This rate of equityreturn does not remain constant over the useful life of the project.

Hence, a project which seems to be desirable at one point of time may not be

desirable at another point of time (Accounting for management, 2019).

From the point of view of accounting rate of return, the target rate of return for the company

comes out to be 10% whereas the accounting rate of return for the project comes out to be

18% which is more than the target rate of return for the company. Hence, the project should

be accepted.

FINANCIAL DECISION MAKING 18

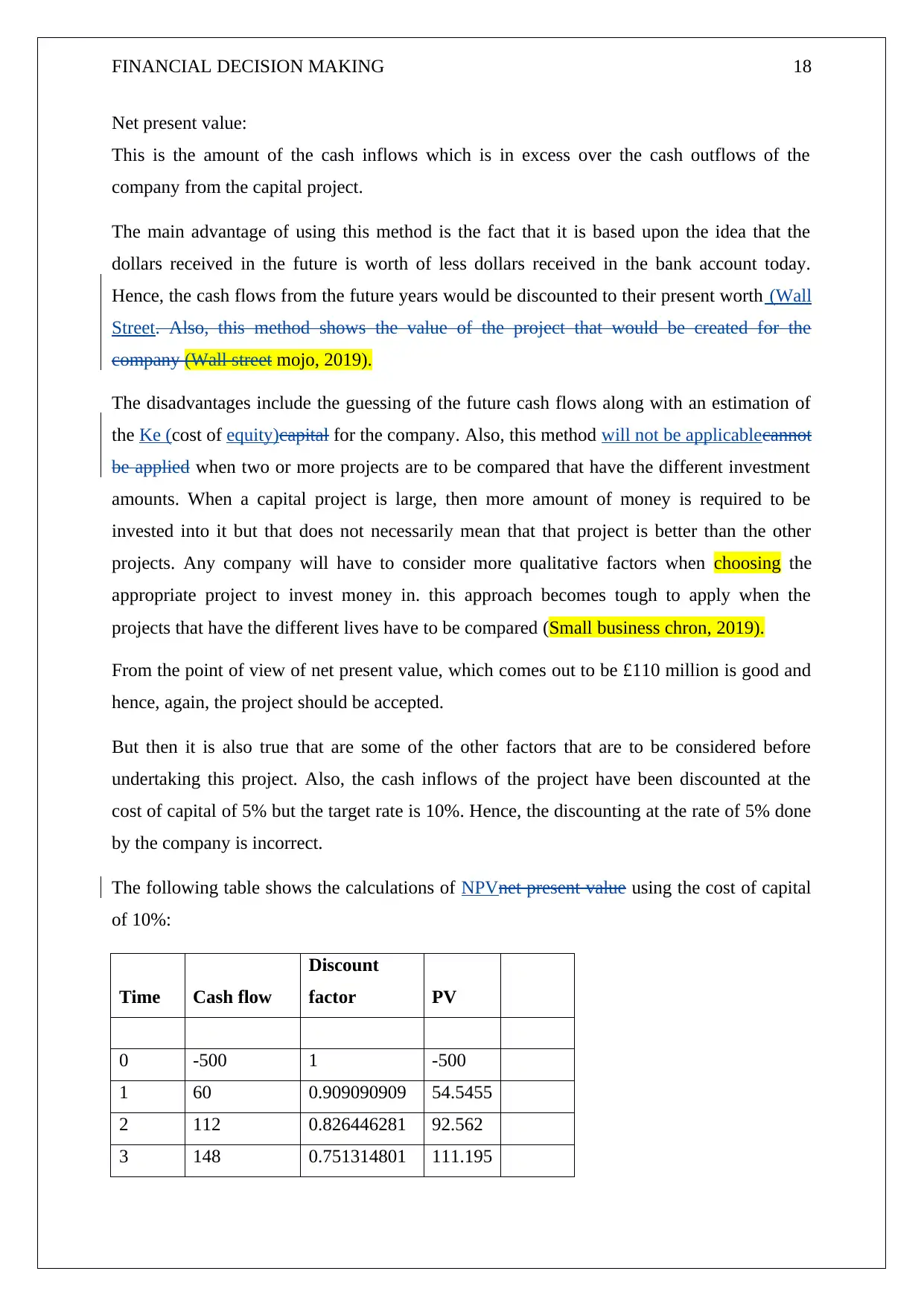

Net present value:

This is the amount of the cash inflows which is in excess over the cash outflows of the

company from the capital project.

The main advantage of using this method is the fact that it is based upon the idea that the

dollars received in the future is worth of less dollars received in the bank account today.

Hence, the cash flows from the future years would be discounted to their present worth (Wall

Street. Also, this method shows the value of the project that would be created for the

company (Wall street mojo, 2019).

The disadvantages include the guessing of the future cash flows along with an estimation of

the Ke (cost of equity)capital for the company. Also, this method will not be applicablecannot

be applied when two or more projects are to be compared that have the different investment

amounts. When a capital project is large, then more amount of money is required to be

invested into it but that does not necessarily mean that that project is better than the other

projects. Any company will have to consider more qualitative factors when choosing the

appropriate project to invest money in. this approach becomes tough to apply when the

projects that have the different lives have to be compared (Small business chron, 2019).

From the point of view of net present value, which comes out to be £110 million is good and

hence, again, the project should be accepted.

But then it is also true that are some of the other factors that are to be considered before

undertaking this project. Also, the cash inflows of the project have been discounted at the

cost of capital of 5% but the target rate is 10%. Hence, the discounting at the rate of 5% done

by the company is incorrect.

The following table shows the calculations of NPVnet present value using the cost of capital

of 10%:

Time Cash flow

Discount

factor PV

0 -500 1 -500

1 60 0.909090909 54.5455

2 112 0.826446281 92.562

3 148 0.751314801 111.195

Net present value:

This is the amount of the cash inflows which is in excess over the cash outflows of the

company from the capital project.

The main advantage of using this method is the fact that it is based upon the idea that the

dollars received in the future is worth of less dollars received in the bank account today.

Hence, the cash flows from the future years would be discounted to their present worth (Wall

Street. Also, this method shows the value of the project that would be created for the

company (Wall street mojo, 2019).

The disadvantages include the guessing of the future cash flows along with an estimation of

the Ke (cost of equity)capital for the company. Also, this method will not be applicablecannot

be applied when two or more projects are to be compared that have the different investment

amounts. When a capital project is large, then more amount of money is required to be

invested into it but that does not necessarily mean that that project is better than the other

projects. Any company will have to consider more qualitative factors when choosing the

appropriate project to invest money in. this approach becomes tough to apply when the

projects that have the different lives have to be compared (Small business chron, 2019).

From the point of view of net present value, which comes out to be £110 million is good and

hence, again, the project should be accepted.

But then it is also true that are some of the other factors that are to be considered before

undertaking this project. Also, the cash inflows of the project have been discounted at the

cost of capital of 5% but the target rate is 10%. Hence, the discounting at the rate of 5% done

by the company is incorrect.

The following table shows the calculations of NPVnet present value using the cost of capital

of 10%:

Time Cash flow

Discount

factor PV

0 -500 1 -500

1 60 0.909090909 54.5455

2 112 0.826446281 92.562

3 148 0.751314801 111.195

FINANCIAL DECISION MAKING 19

4 180 0.683013455 122.942

5 224 0.620921323 139.086

NPV 20.3308

So, the correct NPV comes out to be £ 20.3308 million.

Sources of finance:

The first source of finance is Venture capital firms. The Angel investors are the private

individuals that invest in the business of the others. They usually work in the small,

medium sized companies that have very limited amounts of funds. This sort of an investor

is more suitable for start-ups companies than the venture capital firms. They mainly invest

in the amounts from a few hundred thousand dollars up to $2 million as the start-up capital

for the company

The following are its advantages:

1. The venture capital equips the companies with an opportunity to new projects and

new expansionexpand. This would is not possible with the other options such as

bank loans. These firms are ready to invest into the business since they are confident

about the believe in the long term success of the company and therefore, the venture

capital financing is something which is beneficial for the start-ups with the high

initial cost and with a very limited operating history of the company.

2. These firms serve as guidance for the company with their expertise and

consultations. The member ofAny member from the venture capitalist becomes the

partcapital firm would be appointed in the board of the day to day business

operations ofcompany. This means an active involvement of the venture capitalist in

the decisions made by the company. Since the venture capitalists have an immense

amount of experience in the business, they could help the companies undertaking

the projects.

3. They also help in building networks and connections for the companies that they

invest in. these connections could be advantageous for the companies to make them

more successful. They could also help in the start-up so as to enter into alliances

with the potential customers or the business houses.

4 180 0.683013455 122.942

5 224 0.620921323 139.086

NPV 20.3308

So, the correct NPV comes out to be £ 20.3308 million.

Sources of finance:

The first source of finance is Venture capital firms. The Angel investors are the private

individuals that invest in the business of the others. They usually work in the small,

medium sized companies that have very limited amounts of funds. This sort of an investor

is more suitable for start-ups companies than the venture capital firms. They mainly invest

in the amounts from a few hundred thousand dollars up to $2 million as the start-up capital

for the company

The following are its advantages:

1. The venture capital equips the companies with an opportunity to new projects and

new expansionexpand. This would is not possible with the other options such as

bank loans. These firms are ready to invest into the business since they are confident

about the believe in the long term success of the company and therefore, the venture

capital financing is something which is beneficial for the start-ups with the high

initial cost and with a very limited operating history of the company.

2. These firms serve as guidance for the company with their expertise and

consultations. The member ofAny member from the venture capitalist becomes the

partcapital firm would be appointed in the board of the day to day business

operations ofcompany. This means an active involvement of the venture capitalist in

the decisions made by the company. Since the venture capitalists have an immense

amount of experience in the business, they could help the companies undertaking

the projects.

3. They also help in building networks and connections for the companies that they

invest in. these connections could be advantageous for the companies to make them

more successful. They could also help in the start-up so as to enter into alliances

with the potential customers or the business houses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 20

4. The business need not There is as such no obligation to repay the venture capitalist

in case, the business failsinvestors if the company fails or shuts down.

5. With the experience and the connections of these venture capitalists, the venture

capitalists are somewhat trustworthy in nature. They are also regulated by the

regulatory bodies.

6. They are quiet easy to locate. These firms are documented in various directories.

This leads to a reduction of time, efforts and also the money which is involved in

the search for the venture funding.

The following are its disadvantages:

1. Since the venture capitalists include a huge amount of money into the company and

therefore, they form the part of the board of the company, it leads to the dilution of

ownership and control of the company.

2. The venture capitalists could decide to redeem their investment within the period of 3

to 5 years.

3. The company seeking an investment will have to represent a detailed business plan to

the venture capitalists.

4. The decision so as to invest in the company by the venture capitalists is long, tedious

and could consume a considerable period of time.

5. They could release funds from time to time (E finance management, 2019).

The second source of finance is commercial loans.

The following are its advantages:

1. These are a cheap source of finance

2. They are usually of long term in nature which is between 3 t 10 years.

3. The lower interest rates and the extended plans of payment could decrease the

potential default which could go on to reduce the risk of investment

4. Offers a huge amount of money so that project could be funded from single loan.

5. These loans are unsecured and hence, no collateral is required

6. The company could retain the complete ownership of the company (the hart ford,

2019).

The following are its disadvantages:

4. The business need not There is as such no obligation to repay the venture capitalist

in case, the business failsinvestors if the company fails or shuts down.

5. With the experience and the connections of these venture capitalists, the venture

capitalists are somewhat trustworthy in nature. They are also regulated by the

regulatory bodies.

6. They are quiet easy to locate. These firms are documented in various directories.

This leads to a reduction of time, efforts and also the money which is involved in

the search for the venture funding.

The following are its disadvantages:

1. Since the venture capitalists include a huge amount of money into the company and

therefore, they form the part of the board of the company, it leads to the dilution of

ownership and control of the company.

2. The venture capitalists could decide to redeem their investment within the period of 3

to 5 years.

3. The company seeking an investment will have to represent a detailed business plan to

the venture capitalists.

4. The decision so as to invest in the company by the venture capitalists is long, tedious

and could consume a considerable period of time.

5. They could release funds from time to time (E finance management, 2019).

The second source of finance is commercial loans.

The following are its advantages:

1. These are a cheap source of finance

2. They are usually of long term in nature which is between 3 t 10 years.

3. The lower interest rates and the extended plans of payment could decrease the

potential default which could go on to reduce the risk of investment

4. Offers a huge amount of money so that project could be funded from single loan.

5. These loans are unsecured and hence, no collateral is required

6. The company could retain the complete ownership of the company (the hart ford,

2019).

The following are its disadvantages:

FINANCIAL DECISION MAKING 21

1. The funding is very challenging in nature and it could require excellent business

credit.

2. The process of making application or applying for loan is exhaustive and requires a

detailed financial report of the business which would provide an accurate assessment

of the projected revenues and the detailed information with regard to the business

risks connected with them.

3. The personal financial history will have to be given to the bank.

4. These loans provide a lesser personal autonomy when compared with the loan

options.

5. In case, the company fails to repay the loans, then the bank could seize any property

to recover the loan (Credibly, 2019).

After considering the above advantages and disadvantages of both options stated above, it is

better than the company goes for the venture capitalist firms due to the reason of their

experience, networking and consultation (Small business chron, 2019).

Also, since the new project has a positive net present value and the accounting rate of return

is more than the target rate of return and the payback period is also of 4 years when the

estimated revenue is for 5 years, Roast Ltd should be acquired by Starbucks since that would

prove to be successful.

1. The funding is very challenging in nature and it could require excellent business

credit.

2. The process of making application or applying for loan is exhaustive and requires a

detailed financial report of the business which would provide an accurate assessment

of the projected revenues and the detailed information with regard to the business

risks connected with them.

3. The personal financial history will have to be given to the bank.

4. These loans provide a lesser personal autonomy when compared with the loan

options.

5. In case, the company fails to repay the loans, then the bank could seize any property

to recover the loan (Credibly, 2019).

After considering the above advantages and disadvantages of both options stated above, it is

better than the company goes for the venture capitalist firms due to the reason of their

experience, networking and consultation (Small business chron, 2019).

Also, since the new project has a positive net present value and the accounting rate of return

is more than the target rate of return and the payback period is also of 4 years when the

estimated revenue is for 5 years, Roast Ltd should be acquired by Starbucks since that would

prove to be successful.

FINANCIAL DECISION MAKING 22

References:

Accounting for Management. (2019). Accounting rate of return (ARR) method - example,

formula, advantages and disadvantages | Accounting for Management. [online] Available at:

https://www.accountingformanagement.org/accounting-rate-of-return-method/ [Accessed 28

Dec. 2019].

Britishcoffeeassociation.org. (2018). The UK coffee market and its impact on the economy.

[online] Available at: https://www.britishcoffeeassociation.org/assets/files/uploads/BCA

%20CEBR%20-%20The%20economic%20value%20of%20coffee%20in%20the%20UK

%2020%20April_FINAL.pdf [Accessed 28 Dec. 2019].

Bstrategyhub.com. (2019). Coffee industry. [online] Available at:

https://bstrategyhub.com/swot-analysis-of-starbucks-starbucks-swot/ [Accessed 28 Dec.

2019].

Credibly. (2019). Commercial Loans for Business Growth: The Pros and Cons | Credibly.

[online] Available at: https://www.credibly.com/incredibly/business-capital-101/commercial-

loans-for-business/ [Accessed 28 Dec. 2019].

efinancemanagement.com. (2019). Operating cash cycle. [online] Available at:

https://efinancemanagement.com/working-capital-financing/operating-cycle-and-cash-

operating-icycle [Accessed 28 Dec. 2019].

eFinanceManagement.com. (2019). Advantages and Disadvantages of Venture Capital |

eFinanceManagement.com. [online] Available at: https://efinancemanagement.com/sources-

of-finance/advantages-and-disadvantages-of-venture-capital [Accessed 28 Dec. 2019].

eFinanceManagement.com. (2019). Disadvantages and Advantages of Payback Period |

eFinanceManagement. [online] Available at: https://efinancemanagement.com/investment-

decisions/advantages-and-disadvantages-of-payback-period [Accessed 28 Dec. 2019].

Ibisworld.com. (2019). IBISWorld - Industry Market Research, Reports, and Statistics.

[online] Available at:

https://www.ibisworld.com/united-kingdom/market-research-reports/cafes-coffee-shops-

industry/ [Accessed 28 Dec. 2019].

References:

Accounting for Management. (2019). Accounting rate of return (ARR) method - example,

formula, advantages and disadvantages | Accounting for Management. [online] Available at:

https://www.accountingformanagement.org/accounting-rate-of-return-method/ [Accessed 28

Dec. 2019].

Britishcoffeeassociation.org. (2018). The UK coffee market and its impact on the economy.

[online] Available at: https://www.britishcoffeeassociation.org/assets/files/uploads/BCA

%20CEBR%20-%20The%20economic%20value%20of%20coffee%20in%20the%20UK

%2020%20April_FINAL.pdf [Accessed 28 Dec. 2019].

Bstrategyhub.com. (2019). Coffee industry. [online] Available at:

https://bstrategyhub.com/swot-analysis-of-starbucks-starbucks-swot/ [Accessed 28 Dec.

2019].

Credibly. (2019). Commercial Loans for Business Growth: The Pros and Cons | Credibly.

[online] Available at: https://www.credibly.com/incredibly/business-capital-101/commercial-

loans-for-business/ [Accessed 28 Dec. 2019].

efinancemanagement.com. (2019). Operating cash cycle. [online] Available at:

https://efinancemanagement.com/working-capital-financing/operating-cycle-and-cash-

operating-icycle [Accessed 28 Dec. 2019].

eFinanceManagement.com. (2019). Advantages and Disadvantages of Venture Capital |

eFinanceManagement.com. [online] Available at: https://efinancemanagement.com/sources-

of-finance/advantages-and-disadvantages-of-venture-capital [Accessed 28 Dec. 2019].

eFinanceManagement.com. (2019). Disadvantages and Advantages of Payback Period |

eFinanceManagement. [online] Available at: https://efinancemanagement.com/investment-

decisions/advantages-and-disadvantages-of-payback-period [Accessed 28 Dec. 2019].

Ibisworld.com. (2019). IBISWorld - Industry Market Research, Reports, and Statistics.

[online] Available at:

https://www.ibisworld.com/united-kingdom/market-research-reports/cafes-coffee-shops-

industry/ [Accessed 28 Dec. 2019].

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL DECISION MAKING 23

Smallbusiness.chron.com. (2019). Advantages & Disadvantages of Payback Capital

Budgeting Method. [online] Available at: https://smallbusiness.chron.com/advantages-

disadvantages-payback-capital-budgeting-method-14206.html [Accessed 28 Dec. 2019].

Smallbusiness.chron.com. (2019). Advantages & Disadvantages of Net Present Value in

Project Selection. [online] Available at: https://smallbusiness.chron.com/advantages-

disadvantages-net-present-value-project-selection-54753.html [Accessed 28 Dec. 2019].

Smallbusiness.chron.com. (2019). Advantages & Disadvantages of Bank Loans. [online]

Available at: https://smallbusiness.chron.com/advantages-amp-disadvantages-bank-loans-

47377.html [Accessed 28 Dec. 2019].

Thehartford.com. (2019). Advantages vs. Disadvantages of Venture Capital | The Hartford.

[online] Available at: https://www.thehartford.com/business-insurance/strategy/business-

financing/venture-capital [Accessed 28 Dec. 2019].

Wallstreet Mojo. (2019). Advantages and Disadvantages of NPV (Net Present Value) |

Examples. [online] Available at: https://www.wallstreetmojo.com/advantages-and-

disadvantages-of-npv/ [Accessed 28 Dec. 2019].

Smallbusiness.chron.com. (2019). Advantages & Disadvantages of Payback Capital

Budgeting Method. [online] Available at: https://smallbusiness.chron.com/advantages-

disadvantages-payback-capital-budgeting-method-14206.html [Accessed 28 Dec. 2019].

Smallbusiness.chron.com. (2019). Advantages & Disadvantages of Net Present Value in

Project Selection. [online] Available at: https://smallbusiness.chron.com/advantages-

disadvantages-net-present-value-project-selection-54753.html [Accessed 28 Dec. 2019].

Smallbusiness.chron.com. (2019). Advantages & Disadvantages of Bank Loans. [online]

Available at: https://smallbusiness.chron.com/advantages-amp-disadvantages-bank-loans-

47377.html [Accessed 28 Dec. 2019].

Thehartford.com. (2019). Advantages vs. Disadvantages of Venture Capital | The Hartford.

[online] Available at: https://www.thehartford.com/business-insurance/strategy/business-

financing/venture-capital [Accessed 28 Dec. 2019].

Wallstreet Mojo. (2019). Advantages and Disadvantages of NPV (Net Present Value) |

Examples. [online] Available at: https://www.wallstreetmojo.com/advantages-and-

disadvantages-of-npv/ [Accessed 28 Dec. 2019].

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.