Financial Performance Analysis Report for Cordon Bleu PLC (FIN 7040)

VerifiedAdded on 2022/11/13

|21

|5038

|412

Report

AI Summary

This report presents a financial analysis of Cordon Bleu PLC, a company operating in the restaurant industry. The analysis examines the company's performance using financial statements and ratio analysis, including profitability, liquidity, and solvency ratios. The report assesses the impact of recent acquisitions on the company's financial health and provides insights into its performance in 2017 and 2018. Furthermore, the report discusses the company's plans for growth through food delivery services, suggesting potential sources of finance and considering non-financial factors. The analysis covers key aspects like gross profit ratio, net profit ratio, return on equity, current ratio, quick ratio, debt ratio, debt to equity ratio, and equity ratio to evaluate the company's financial position and suggest areas for improvement. Investment appraisal techniques and sources of finance are also discussed to support future developments.

Running head: FINANCIAL DECISION MAKING

Financial decision making

5/26/2019

Financial decision making

5/26/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 1

Executive summary

The intent of this report is to present the financial analysis of Cordon Bleu Plc., which offers

tasty and quality food through restaurants. The report is analyzing the performance of the

business in order to suggest future developments to the managers of the company. The report

has calculated the ratio analysis to evaluate the company’s performance as per different

perspective that is solvency, profitability, efficiency, and liquidity. From the analysis, it has

been identified that the company has recently acquired two chains of a restaurant to increase

its share in the market. However, in the initial phase, the business is not able to make must

effect on the customer, which could be seen from its financial statement. The company is also

planning to grow through food delivery service market for which the report has suggested

some finance sources and significant non-financial factors.

Executive summary

The intent of this report is to present the financial analysis of Cordon Bleu Plc., which offers

tasty and quality food through restaurants. The report is analyzing the performance of the

business in order to suggest future developments to the managers of the company. The report

has calculated the ratio analysis to evaluate the company’s performance as per different

perspective that is solvency, profitability, efficiency, and liquidity. From the analysis, it has

been identified that the company has recently acquired two chains of a restaurant to increase

its share in the market. However, in the initial phase, the business is not able to make must

effect on the customer, which could be seen from its financial statement. The company is also

planning to grow through food delivery service market for which the report has suggested

some finance sources and significant non-financial factors.

FINANCIAL DECISION MAKING 2

Table of Contents

Executive summary....................................................................................................................1

Part 1: Business Performance Analysis......................................................................................3

1.1 Statement of profit and loss of.........................................................................................3

Profitability Ratio...............................................................................................................3

1.2 Statement of Financial Position.......................................................................................5

Liquidity ratio.....................................................................................................................5

Solvency ratio.....................................................................................................................6

1.3 Statement Cash Flows......................................................................................................8

Operating Cash Cycle........................................................................................................8

Dividend.............................................................................................................................8

1.4 Market Segment Analysis................................................................................................9

Strategies for Value Segment...........................................................................................10

Strategies for Premium Segment......................................................................................10

Strategy for Classic Segment...........................................................................................11

Part 2 Investment Appraisal.....................................................................................................11

2.1.........................................................................................................................................11

a. Management Forecast...................................................................................................11

b. Investment Appraisal Techniques................................................................................11

2.2 Sources of Finance.........................................................................................................13

2.3 Non-Financial Factors 5 250..........................................................................................14

References................................................................................................................................16

Table of Contents

Executive summary....................................................................................................................1

Part 1: Business Performance Analysis......................................................................................3

1.1 Statement of profit and loss of.........................................................................................3

Profitability Ratio...............................................................................................................3

1.2 Statement of Financial Position.......................................................................................5

Liquidity ratio.....................................................................................................................5

Solvency ratio.....................................................................................................................6

1.3 Statement Cash Flows......................................................................................................8

Operating Cash Cycle........................................................................................................8

Dividend.............................................................................................................................8

1.4 Market Segment Analysis................................................................................................9

Strategies for Value Segment...........................................................................................10

Strategies for Premium Segment......................................................................................10

Strategy for Classic Segment...........................................................................................11

Part 2 Investment Appraisal.....................................................................................................11

2.1.........................................................................................................................................11

a. Management Forecast...................................................................................................11

b. Investment Appraisal Techniques................................................................................11

2.2 Sources of Finance.........................................................................................................13

2.3 Non-Financial Factors 5 250..........................................................................................14

References................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL DECISION MAKING 3

Part 1: Business Performance Analysis

1.1 Statement of profit and loss

A profit and loss statement is the document that evaluates and lists the expenses and revenue

of the business for the particular time period. It highlights the financial progress and status of

the company during the surveyed time. It is very important for every business organization to

prepare an income statement because it provides in details the capability of the company in

generating profit by driving revenue and cutting cost (Knight, 2012). This statement provides

detail categories of expenses and revenue which comprise the cost of goods sold, gross

margin, net profit, net sales, administrative expenses, and selling. With the help of the details

of profit and loss statement, the business can calculate some of the key ratios in order to

analyze its performance (Brief and Peasnell, 2013).

Profitability Ratio

A profitability ratio is a type of financial metrics that are utilized to assess the capability of

the business in order to generate earning relative to its balance sheets, shareholder’s equity,

revenue, and operating costs by making use of the data from the particular point. For the

effective profitability ratios, it is important to have a higher relative value in comparison to

the relative of competitors to a similar ratio from the specific time period (Velnampy and

Niresh, 2012). Besides this, if the ratio of a single company is higher than the previous year

of the same company indicates that the business is performing well in the competitive market.

Ratios are said to be more informative as well as useful when practices to compare the

subject company with other company, with the company's own history. Some of the

profitability ratio are Gross Profit ratio, net profit ratio, and return on equity.

Profitability 2017 2018

Part 1: Business Performance Analysis

1.1 Statement of profit and loss

A profit and loss statement is the document that evaluates and lists the expenses and revenue

of the business for the particular time period. It highlights the financial progress and status of

the company during the surveyed time. It is very important for every business organization to

prepare an income statement because it provides in details the capability of the company in

generating profit by driving revenue and cutting cost (Knight, 2012). This statement provides

detail categories of expenses and revenue which comprise the cost of goods sold, gross

margin, net profit, net sales, administrative expenses, and selling. With the help of the details

of profit and loss statement, the business can calculate some of the key ratios in order to

analyze its performance (Brief and Peasnell, 2013).

Profitability Ratio

A profitability ratio is a type of financial metrics that are utilized to assess the capability of

the business in order to generate earning relative to its balance sheets, shareholder’s equity,

revenue, and operating costs by making use of the data from the particular point. For the

effective profitability ratios, it is important to have a higher relative value in comparison to

the relative of competitors to a similar ratio from the specific time period (Velnampy and

Niresh, 2012). Besides this, if the ratio of a single company is higher than the previous year

of the same company indicates that the business is performing well in the competitive market.

Ratios are said to be more informative as well as useful when practices to compare the

subject company with other company, with the company's own history. Some of the

profitability ratio are Gross Profit ratio, net profit ratio, and return on equity.

Profitability 2017 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 4

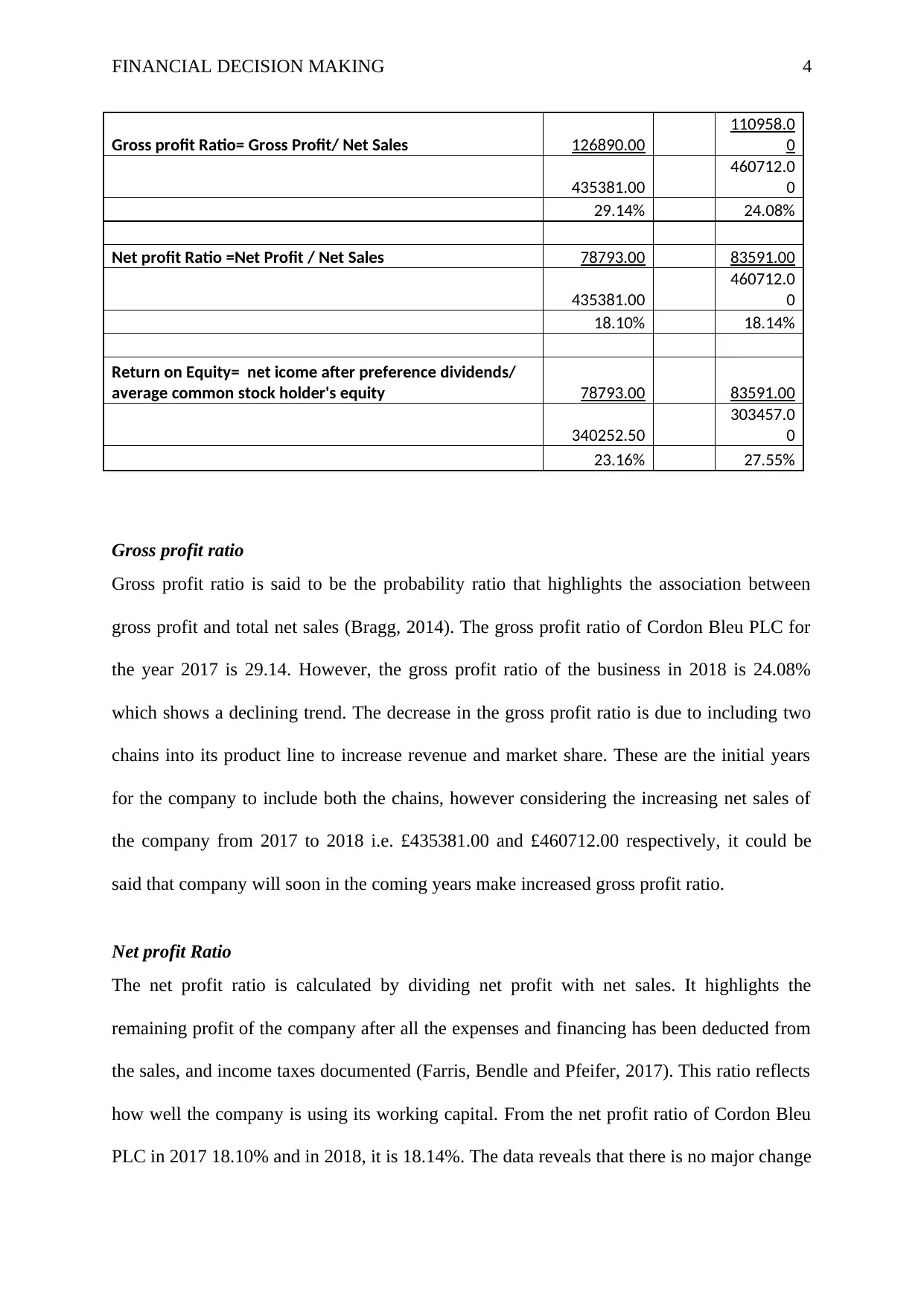

Gross profit Ratio= Gross Profit/ Net Sales 126890.00

110958.0

0

435381.00

460712.0

0

29.14% 24.08%

Net profit Ratio =Net Profit / Net Sales 78793.00 83591.00

435381.00

460712.0

0

18.10% 18.14%

Return on Equity= net icome after preference dividends/

average common stock holder's equity 78793.00 83591.00

340252.50

303457.0

0

23.16% 27.55%

Gross profit ratio

Gross profit ratio is said to be the probability ratio that highlights the association between

gross profit and total net sales (Bragg, 2014). The gross profit ratio of Cordon Bleu PLC for

the year 2017 is 29.14. However, the gross profit ratio of the business in 2018 is 24.08%

which shows a declining trend. The decrease in the gross profit ratio is due to including two

chains into its product line to increase revenue and market share. These are the initial years

for the company to include both the chains, however considering the increasing net sales of

the company from 2017 to 2018 i.e. £435381.00 and £460712.00 respectively, it could be

said that company will soon in the coming years make increased gross profit ratio.

Net profit Ratio

The net profit ratio is calculated by dividing net profit with net sales. It highlights the

remaining profit of the company after all the expenses and financing has been deducted from

the sales, and income taxes documented (Farris, Bendle and Pfeifer, 2017). This ratio reflects

how well the company is using its working capital. From the net profit ratio of Cordon Bleu

PLC in 2017 18.10% and in 2018, it is 18.14%. The data reveals that there is no major change

Gross profit Ratio= Gross Profit/ Net Sales 126890.00

110958.0

0

435381.00

460712.0

0

29.14% 24.08%

Net profit Ratio =Net Profit / Net Sales 78793.00 83591.00

435381.00

460712.0

0

18.10% 18.14%

Return on Equity= net icome after preference dividends/

average common stock holder's equity 78793.00 83591.00

340252.50

303457.0

0

23.16% 27.55%

Gross profit ratio

Gross profit ratio is said to be the probability ratio that highlights the association between

gross profit and total net sales (Bragg, 2014). The gross profit ratio of Cordon Bleu PLC for

the year 2017 is 29.14. However, the gross profit ratio of the business in 2018 is 24.08%

which shows a declining trend. The decrease in the gross profit ratio is due to including two

chains into its product line to increase revenue and market share. These are the initial years

for the company to include both the chains, however considering the increasing net sales of

the company from 2017 to 2018 i.e. £435381.00 and £460712.00 respectively, it could be

said that company will soon in the coming years make increased gross profit ratio.

Net profit Ratio

The net profit ratio is calculated by dividing net profit with net sales. It highlights the

remaining profit of the company after all the expenses and financing has been deducted from

the sales, and income taxes documented (Farris, Bendle and Pfeifer, 2017). This ratio reflects

how well the company is using its working capital. From the net profit ratio of Cordon Bleu

PLC in 2017 18.10% and in 2018, it is 18.14%. The data reveals that there is no major change

FINANCIAL DECISION MAKING 5

in the company's net profit ratio of 2018 when compared to 2017. This highlights that the

acquisition of two chains has not impacted the net profit ratio of the company and there is no

major difference in the profit of the company. However, with the increasing time company

must work on increasing its net profit ratio.

Return on Equity

Return on equity is said to be the financial performance measure that is calculated by

dividing the net income of the company by shareholder's equity. The shareholder's equity is

used because it is equal to the company’s asset minus its debt (IntroBooks, 2019). ROE is

taken as the measure to examine how effectively the management of the organization is

making use of the asset in order to generate profits. The return on equity of Cordon Bleu PLC

in 2017 is 23.16% and in 2018 it is 27.55%. From the analysis, it could be observed that the

return on equity of the company is growing, which means the management of the

organization is making the best use of the assets and generating profits.

1.2 Statement of Financial Position

A statement of the financial position also termed as balance sheet, which reports regarding

the shareholder's equity, assets and liabilities of the company at a specific time frame and

supports in evaluating the capital structure (Makoujy, 2010). It is a financial statement which

offers a picture of what is own and owes by a company, along with the amount invested by

the company's shareholders. This statement is utilized along with different essential financial

statements like cash flow and income statement while conducting the performance analysis or

computing financial ratios. The balance sheet of every company is prepared by following the

accounting equation that is – Assets= Liabilities + Shareholders’ Equity (Ramachandran,

2013).

in the company's net profit ratio of 2018 when compared to 2017. This highlights that the

acquisition of two chains has not impacted the net profit ratio of the company and there is no

major difference in the profit of the company. However, with the increasing time company

must work on increasing its net profit ratio.

Return on Equity

Return on equity is said to be the financial performance measure that is calculated by

dividing the net income of the company by shareholder's equity. The shareholder's equity is

used because it is equal to the company’s asset minus its debt (IntroBooks, 2019). ROE is

taken as the measure to examine how effectively the management of the organization is

making use of the asset in order to generate profits. The return on equity of Cordon Bleu PLC

in 2017 is 23.16% and in 2018 it is 27.55%. From the analysis, it could be observed that the

return on equity of the company is growing, which means the management of the

organization is making the best use of the assets and generating profits.

1.2 Statement of Financial Position

A statement of the financial position also termed as balance sheet, which reports regarding

the shareholder's equity, assets and liabilities of the company at a specific time frame and

supports in evaluating the capital structure (Makoujy, 2010). It is a financial statement which

offers a picture of what is own and owes by a company, along with the amount invested by

the company's shareholders. This statement is utilized along with different essential financial

statements like cash flow and income statement while conducting the performance analysis or

computing financial ratios. The balance sheet of every company is prepared by following the

accounting equation that is – Assets= Liabilities + Shareholders’ Equity (Ramachandran,

2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL DECISION MAKING 6

With the help of balance sheet, this report has calculated some of the key ratios such as

solvency ratio, liquidity ratio, and efficiency ratio.

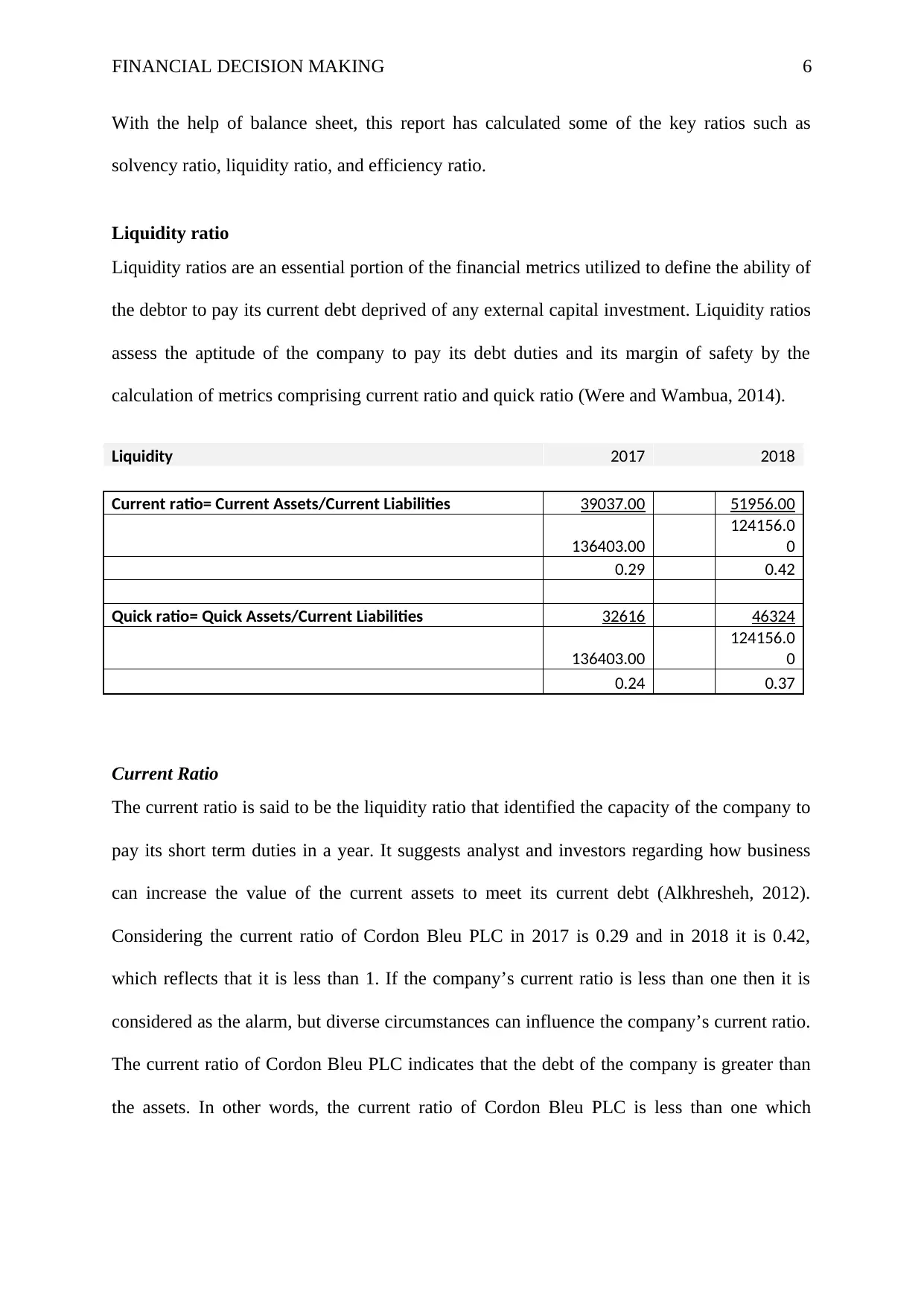

Liquidity ratio

Liquidity ratios are an essential portion of the financial metrics utilized to define the ability of

the debtor to pay its current debt deprived of any external capital investment. Liquidity ratios

assess the aptitude of the company to pay its debt duties and its margin of safety by the

calculation of metrics comprising current ratio and quick ratio (Were and Wambua, 2014).

Liquidity 2017 2018

Current ratio= Current Assets/Current Liabilities 39037.00 51956.00

136403.00

124156.0

0

0.29 0.42

Quick ratio= Quick Assets/Current Liabilities 32616 46324

136403.00

124156.0

0

0.24 0.37

Current Ratio

The current ratio is said to be the liquidity ratio that identified the capacity of the company to

pay its short term duties in a year. It suggests analyst and investors regarding how business

can increase the value of the current assets to meet its current debt (Alkhresheh, 2012).

Considering the current ratio of Cordon Bleu PLC in 2017 is 0.29 and in 2018 it is 0.42,

which reflects that it is less than 1. If the company’s current ratio is less than one then it is

considered as the alarm, but diverse circumstances can influence the company’s current ratio.

The current ratio of Cordon Bleu PLC indicates that the debt of the company is greater than

the assets. In other words, the current ratio of Cordon Bleu PLC is less than one which

With the help of balance sheet, this report has calculated some of the key ratios such as

solvency ratio, liquidity ratio, and efficiency ratio.

Liquidity ratio

Liquidity ratios are an essential portion of the financial metrics utilized to define the ability of

the debtor to pay its current debt deprived of any external capital investment. Liquidity ratios

assess the aptitude of the company to pay its debt duties and its margin of safety by the

calculation of metrics comprising current ratio and quick ratio (Were and Wambua, 2014).

Liquidity 2017 2018

Current ratio= Current Assets/Current Liabilities 39037.00 51956.00

136403.00

124156.0

0

0.29 0.42

Quick ratio= Quick Assets/Current Liabilities 32616 46324

136403.00

124156.0

0

0.24 0.37

Current Ratio

The current ratio is said to be the liquidity ratio that identified the capacity of the company to

pay its short term duties in a year. It suggests analyst and investors regarding how business

can increase the value of the current assets to meet its current debt (Alkhresheh, 2012).

Considering the current ratio of Cordon Bleu PLC in 2017 is 0.29 and in 2018 it is 0.42,

which reflects that it is less than 1. If the company’s current ratio is less than one then it is

considered as the alarm, but diverse circumstances can influence the company’s current ratio.

The current ratio of Cordon Bleu PLC indicates that the debt of the company is greater than

the assets. In other words, the current ratio of Cordon Bleu PLC is less than one which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 7

highlights that the company lacks in the capital in hand is, therefore, will be unable to meet

its short term debt.

Quick Ratio

The quick ratio is the indicator of the position of the short term liquidity of the organization

and evaluates the aptitude of the business to cover its short term duties by using its liquid

assets (Li, 2011). The quick ratio of Cordon Bleu PLC in 2017 is 0.24 and in 2018 it is 0.37.

This data of quick ratio of Cordon Bleu PLC is less than 1 which indicates that the

organization is incapable to pay its current liabilities in the short time duration. However,

considering the analysis, it could be observed that the company is gradually working on its

performance and increasing its liquidity position in the market.

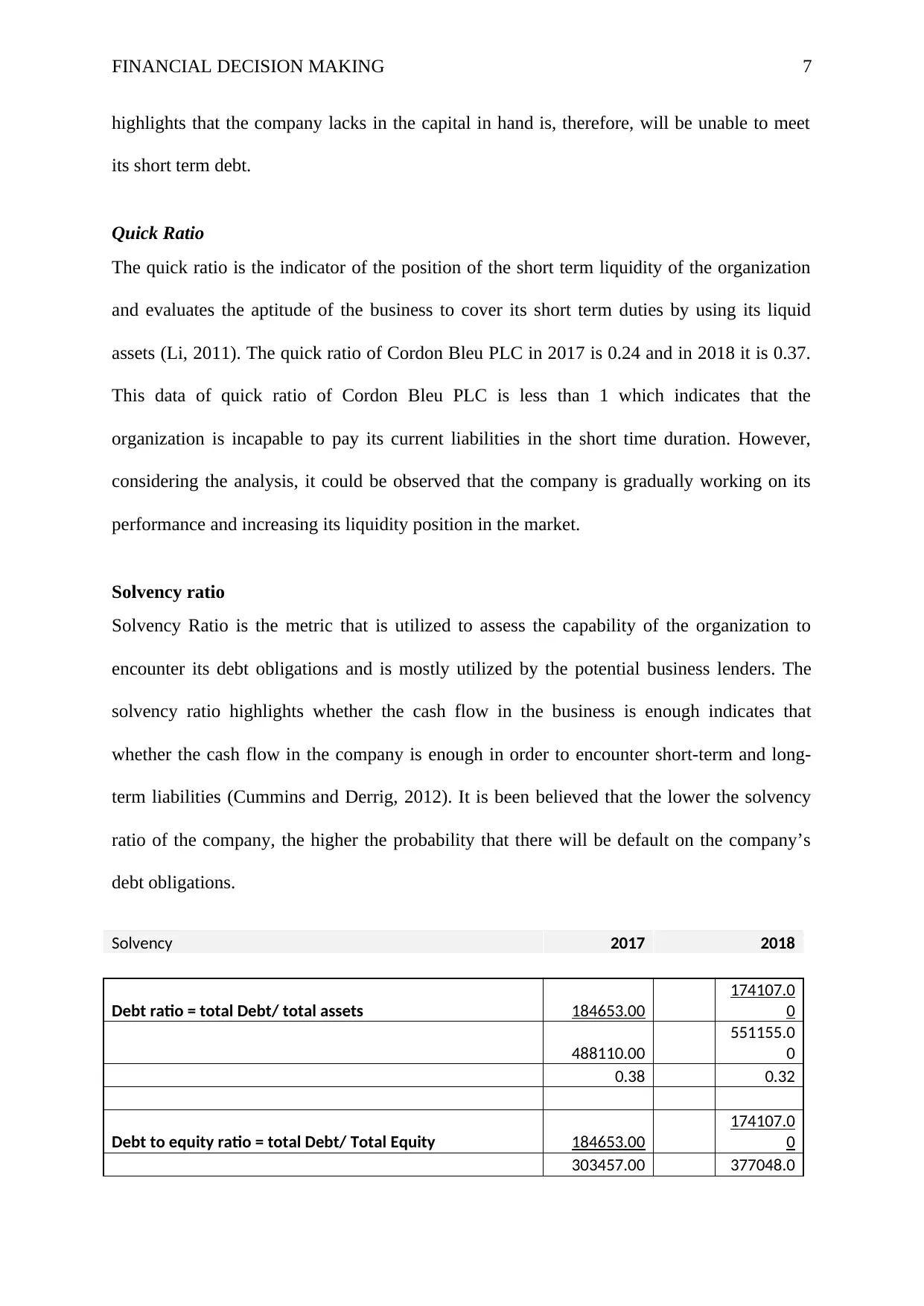

Solvency ratio

Solvency Ratio is the metric that is utilized to assess the capability of the organization to

encounter its debt obligations and is mostly utilized by the potential business lenders. The

solvency ratio highlights whether the cash flow in the business is enough indicates that

whether the cash flow in the company is enough in order to encounter short-term and long-

term liabilities (Cummins and Derrig, 2012). It is been believed that the lower the solvency

ratio of the company, the higher the probability that there will be default on the company’s

debt obligations.

Solvency 2017 2018

Debt ratio = total Debt/ total assets 184653.00

174107.0

0

488110.00

551155.0

0

0.38 0.32

Debt to equity ratio = total Debt/ Total Equity 184653.00

174107.0

0

303457.00 377048.0

highlights that the company lacks in the capital in hand is, therefore, will be unable to meet

its short term debt.

Quick Ratio

The quick ratio is the indicator of the position of the short term liquidity of the organization

and evaluates the aptitude of the business to cover its short term duties by using its liquid

assets (Li, 2011). The quick ratio of Cordon Bleu PLC in 2017 is 0.24 and in 2018 it is 0.37.

This data of quick ratio of Cordon Bleu PLC is less than 1 which indicates that the

organization is incapable to pay its current liabilities in the short time duration. However,

considering the analysis, it could be observed that the company is gradually working on its

performance and increasing its liquidity position in the market.

Solvency ratio

Solvency Ratio is the metric that is utilized to assess the capability of the organization to

encounter its debt obligations and is mostly utilized by the potential business lenders. The

solvency ratio highlights whether the cash flow in the business is enough indicates that

whether the cash flow in the company is enough in order to encounter short-term and long-

term liabilities (Cummins and Derrig, 2012). It is been believed that the lower the solvency

ratio of the company, the higher the probability that there will be default on the company’s

debt obligations.

Solvency 2017 2018

Debt ratio = total Debt/ total assets 184653.00

174107.0

0

488110.00

551155.0

0

0.38 0.32

Debt to equity ratio = total Debt/ Total Equity 184653.00

174107.0

0

303457.00 377048.0

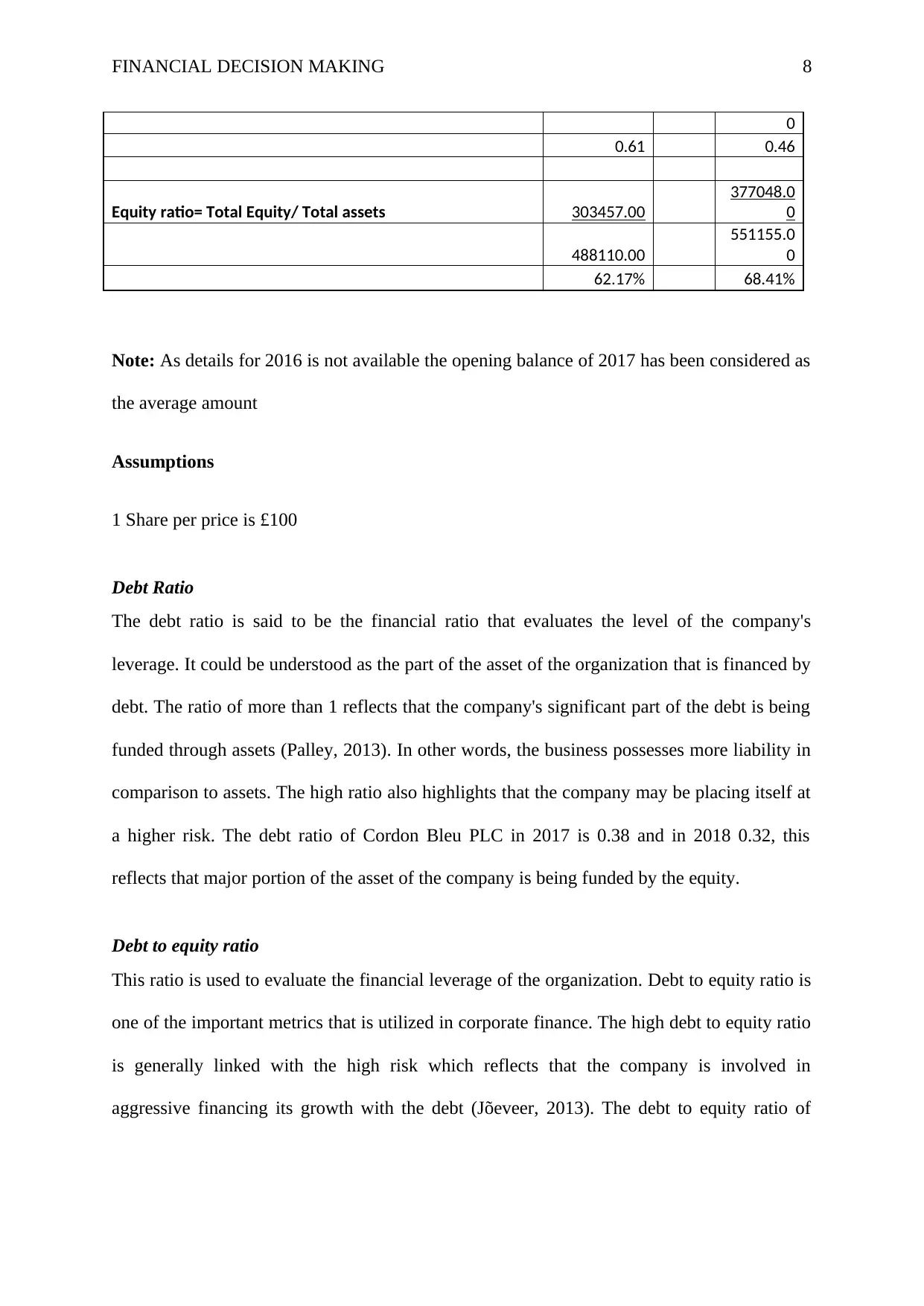

FINANCIAL DECISION MAKING 8

0

0.61 0.46

Equity ratio= Total Equity/ Total assets 303457.00

377048.0

0

488110.00

551155.0

0

62.17% 68.41%

Note: As details for 2016 is not available the opening balance of 2017 has been considered as

the average amount

Assumptions

1 Share per price is £100

Debt Ratio

The debt ratio is said to be the financial ratio that evaluates the level of the company's

leverage. It could be understood as the part of the asset of the organization that is financed by

debt. The ratio of more than 1 reflects that the company's significant part of the debt is being

funded through assets (Palley, 2013). In other words, the business possesses more liability in

comparison to assets. The high ratio also highlights that the company may be placing itself at

a higher risk. The debt ratio of Cordon Bleu PLC in 2017 is 0.38 and in 2018 0.32, this

reflects that major portion of the asset of the company is being funded by the equity.

Debt to equity ratio

This ratio is used to evaluate the financial leverage of the organization. Debt to equity ratio is

one of the important metrics that is utilized in corporate finance. The high debt to equity ratio

is generally linked with the high risk which reflects that the company is involved in

aggressive financing its growth with the debt (Jõeveer, 2013). The debt to equity ratio of

0

0.61 0.46

Equity ratio= Total Equity/ Total assets 303457.00

377048.0

0

488110.00

551155.0

0

62.17% 68.41%

Note: As details for 2016 is not available the opening balance of 2017 has been considered as

the average amount

Assumptions

1 Share per price is £100

Debt Ratio

The debt ratio is said to be the financial ratio that evaluates the level of the company's

leverage. It could be understood as the part of the asset of the organization that is financed by

debt. The ratio of more than 1 reflects that the company's significant part of the debt is being

funded through assets (Palley, 2013). In other words, the business possesses more liability in

comparison to assets. The high ratio also highlights that the company may be placing itself at

a higher risk. The debt ratio of Cordon Bleu PLC in 2017 is 0.38 and in 2018 0.32, this

reflects that major portion of the asset of the company is being funded by the equity.

Debt to equity ratio

This ratio is used to evaluate the financial leverage of the organization. Debt to equity ratio is

one of the important metrics that is utilized in corporate finance. The high debt to equity ratio

is generally linked with the high risk which reflects that the company is involved in

aggressive financing its growth with the debt (Jõeveer, 2013). The debt to equity ratio of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL DECISION MAKING 9

Cordon Bleu PLC in 2017 is 0.61 and in 2018 0.46. This data reveals that the business is not

taking high risk in the market and making a perfect portion of debt and equity in its portfolio.

Equity Ratio

The equity rate is said to be the leverage ratio that evaluates the resources portion of the

company that is funded by the equity participants and its earnings. Businesses with high ratio

are called as conservative business (Bekaert, Harvey and Siegel, 2011). The equity ratio of

Cordon Bleu PLC in 2017 is 62.17% and in 2018 68.41%. This reveals that the company

holds more than 50% of the ratio which says that the company makes use of more equity and

less of debts. Hence, Cordon Bleu PLC is a conservative company.

1.3 Statement Cash Flows

The cash flow statement or the statement of cash is one of the financial statement that

précises the cash amount and cash equivalents leaving and entering a company. This

statement helps in measuring how a business manages its position of the cash, or how makes

money to pay off its debt and fund its operating income statement and is a mandatory part of

the financial reports of the company (Bhandari and Iyer, 2013).

From the analysis of the cash flow statement of Cordon Bleu PLC, it can be analyzed that

company has generated cash from the operating activity that is £40041 by excluding all the

deductions and expenses that were required. The cash from investment activity showed a

negative amount of (£34300) and cash from financing activities is £1701. From the analysis,

it could be said that in the beginning company invested £2745 and at the year end the cash

and cash equivalent are £10187, which means that there is an increase in the cash and cash

equivalent of £7442.

Cordon Bleu PLC in 2017 is 0.61 and in 2018 0.46. This data reveals that the business is not

taking high risk in the market and making a perfect portion of debt and equity in its portfolio.

Equity Ratio

The equity rate is said to be the leverage ratio that evaluates the resources portion of the

company that is funded by the equity participants and its earnings. Businesses with high ratio

are called as conservative business (Bekaert, Harvey and Siegel, 2011). The equity ratio of

Cordon Bleu PLC in 2017 is 62.17% and in 2018 68.41%. This reveals that the company

holds more than 50% of the ratio which says that the company makes use of more equity and

less of debts. Hence, Cordon Bleu PLC is a conservative company.

1.3 Statement Cash Flows

The cash flow statement or the statement of cash is one of the financial statement that

précises the cash amount and cash equivalents leaving and entering a company. This

statement helps in measuring how a business manages its position of the cash, or how makes

money to pay off its debt and fund its operating income statement and is a mandatory part of

the financial reports of the company (Bhandari and Iyer, 2013).

From the analysis of the cash flow statement of Cordon Bleu PLC, it can be analyzed that

company has generated cash from the operating activity that is £40041 by excluding all the

deductions and expenses that were required. The cash from investment activity showed a

negative amount of (£34300) and cash from financing activities is £1701. From the analysis,

it could be said that in the beginning company invested £2745 and at the year end the cash

and cash equivalent are £10187, which means that there is an increase in the cash and cash

equivalent of £7442.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL DECISION MAKING 10

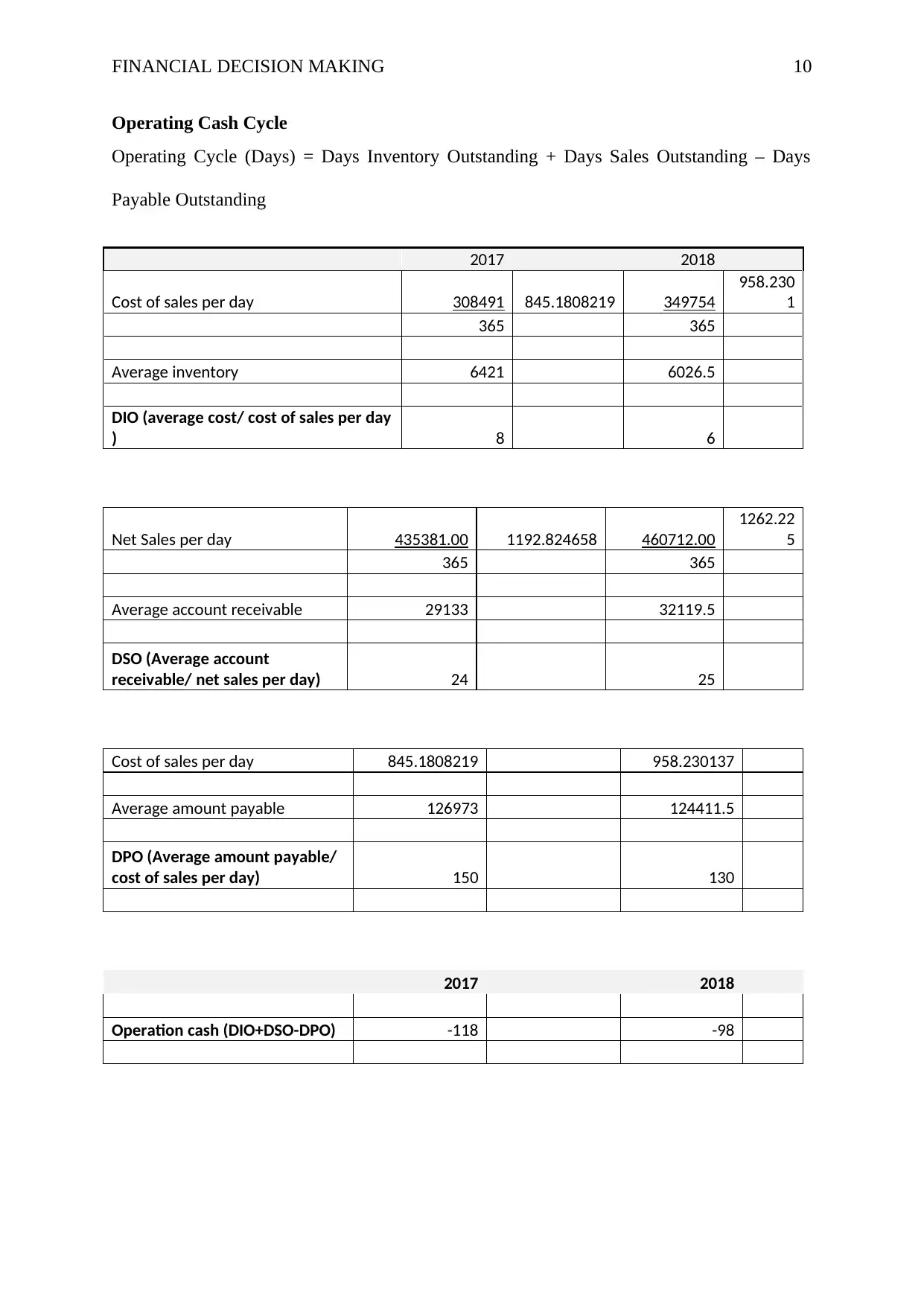

Operating Cash Cycle

Operating Cycle (Days) = Days Inventory Outstanding + Days Sales Outstanding – Days

Payable Outstanding

2017 2018

Cost of sales per day 308491 845.1808219 349754

958.230

1

365 365

Average inventory 6421 6026.5

DIO (average cost/ cost of sales per day

) 8 6

Net Sales per day 435381.00 1192.824658 460712.00

1262.22

5

365 365

Average account receivable 29133 32119.5

DSO (Average account

receivable/ net sales per day) 24 25

Cost of sales per day 845.1808219 958.230137

Average amount payable 126973 124411.5

DPO (Average amount payable/

cost of sales per day) 150 130

2017 2018

Operation cash (DIO+DSO-DPO) -118 -98

Operating Cash Cycle

Operating Cycle (Days) = Days Inventory Outstanding + Days Sales Outstanding – Days

Payable Outstanding

2017 2018

Cost of sales per day 308491 845.1808219 349754

958.230

1

365 365

Average inventory 6421 6026.5

DIO (average cost/ cost of sales per day

) 8 6

Net Sales per day 435381.00 1192.824658 460712.00

1262.22

5

365 365

Average account receivable 29133 32119.5

DSO (Average account

receivable/ net sales per day) 24 25

Cost of sales per day 845.1808219 958.230137

Average amount payable 126973 124411.5

DPO (Average amount payable/

cost of sales per day) 150 130

2017 2018

Operation cash (DIO+DSO-DPO) -118 -98

FINANCIAL DECISION MAKING 11

The negative operating cash cycle highlights that company is borrowing money from the

creditors but not paying back. Besides this, this money is being used for different small

expenses and for maintaining the cash in hand.

Dividend

From the report of the Chairman of the company, it has been analyzed that company was

involved in the acquisition of two premium restaurants during 2017 and 2018 and for this, the

company has announced major investment for the redesigning the restaurants. Besides this,

the company also invested in providing training to the 1800 employees in the new value

chain. The strategy of the company is to invest more in their kitchens for productivity. The

company has declared that it will pay 17.7 per share as the dividend despite the challenges it

is dealing with. According to the analysis, it could be said that announcing dividend on

increased amount can result in increasing challenges for the company because presently it is

not even able to pay off its short term debts which can impact the business if the situations of

the business did not improve. In addition to this, the decision of acquiring two premium

restaurants has not reflected the complete positive results for the company, hence without

performing proper financial analysis of the company it will be irrelevant to offer a dividend.

1.4 Market Segment Analysis

Value segment – From the segmental analysis of Cordon Bleu Plc., it could be noticed that

the value segment of the company is growing with time. The revenue of this segment 2017

was £46520 and it increased to £53190, which is said to be a major change in this segment. In

addition to this, the cost of sales for the same segment has been increased. There is increase

in the gross profit of the business from 2017 to 2018. The positive reflection is that the

operating profit of the company in 2017 was in negative that is (£2669) but it increased and

converted into a positive amount in 2018 to £2554. This highlights that value segment of the

The negative operating cash cycle highlights that company is borrowing money from the

creditors but not paying back. Besides this, this money is being used for different small

expenses and for maintaining the cash in hand.

Dividend

From the report of the Chairman of the company, it has been analyzed that company was

involved in the acquisition of two premium restaurants during 2017 and 2018 and for this, the

company has announced major investment for the redesigning the restaurants. Besides this,

the company also invested in providing training to the 1800 employees in the new value

chain. The strategy of the company is to invest more in their kitchens for productivity. The

company has declared that it will pay 17.7 per share as the dividend despite the challenges it

is dealing with. According to the analysis, it could be said that announcing dividend on

increased amount can result in increasing challenges for the company because presently it is

not even able to pay off its short term debts which can impact the business if the situations of

the business did not improve. In addition to this, the decision of acquiring two premium

restaurants has not reflected the complete positive results for the company, hence without

performing proper financial analysis of the company it will be irrelevant to offer a dividend.

1.4 Market Segment Analysis

Value segment – From the segmental analysis of Cordon Bleu Plc., it could be noticed that

the value segment of the company is growing with time. The revenue of this segment 2017

was £46520 and it increased to £53190, which is said to be a major change in this segment. In

addition to this, the cost of sales for the same segment has been increased. There is increase

in the gross profit of the business from 2017 to 2018. The positive reflection is that the

operating profit of the company in 2017 was in negative that is (£2669) but it increased and

converted into a positive amount in 2018 to £2554. This highlights that value segment of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.