Financial Decision Making Report: Starbucks & Roast Ltd Analysis

VerifiedAdded on 2022/08/19

|20

|5377

|20

Report

AI Summary

This report, prepared for a Financial Decision Making assignment, provides a comprehensive analysis of Roast Ltd. The report begins with an industry review of the UK coffee house market, highlighting its growth and key players. A detailed business performance analysis follows, evaluating Roast Ltd's profitability, liquidity, solvency, and efficiency through various financial ratios. The analysis reveals insights into the company's financial health and operational efficiency. The report then delves into investment appraisal, examining management forecasts and recommending suitable investment appraisal techniques like NPV. Finally, it explores potential financing sources, such as issuing bonds. The analysis suggests that Starbucks should consider acquiring Roast Ltd based on the company's potential for growth and financial improvement.

Running Head: FINANCIAL DECISION MAKING

FINANCIAL DECISION MAKING

Name of the Student

Name of the University

Author Note

FINANCIAL DECISION MAKING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL DECISION MAKING

Table of Contents

Executive Summary...................................................................................................................2

Part 1: Industry Review..............................................................................................................2

Part 2: Business Performance Analysis......................................................................................4

Statement of Profit or Loss....................................................................................................4

Statement of Financial Position.............................................................................................6

Statement of Cash Flows........................................................................................................9

Part 3: Investment Appraisal....................................................................................................11

3.1.a Management Forecast..................................................................................................11

3.1.b Investment Appraisal Techniques...............................................................................12

3.2 Finance Sources.............................................................................................................14

Reference..................................................................................................................................16

Table of Contents

Executive Summary...................................................................................................................2

Part 1: Industry Review..............................................................................................................2

Part 2: Business Performance Analysis......................................................................................4

Statement of Profit or Loss....................................................................................................4

Statement of Financial Position.............................................................................................6

Statement of Cash Flows........................................................................................................9

Part 3: Investment Appraisal....................................................................................................11

3.1.a Management Forecast..................................................................................................11

3.1.b Investment Appraisal Techniques...............................................................................12

3.2 Finance Sources.............................................................................................................14

Reference..................................................................................................................................16

2FINANCIAL DECISION MAKING

Executive Summary

Financial decision is the process, which is responsible for decisions that is related

with company’s shareholders’ equity and liabilities and issuance of bonds. Good decisions of

financial planning extend well-beyond how and where to invest. The ability of spending more

than one could otherwise indicates that assets are generating higher return that results in good

decision-making that makes high spending possible.

This report finds that the coffee house industry of UK indicates better growth of

industry in next five years. Secondly, the business performance of Roast Ltd. indicates that it

is at its expansion stage, but still company is doing well. The profitability condition of

company indicates that it has been improved in comparison to last year, the liquidity position

indicates that it is having the ability for paying short-term liabilities, solvency position

indicates that it is using more debt in comparison to equity, efficiency position indicates that

it is utilizing its assets efficiently and lastly, operating cash cycle indicates that operating

efficiency of company has been reduced in generating cash. Lastly, it has been found that

management forecast proves to be wrong, NPV method proves to be good investment

appraisal technique for the company and issuing of bond can be good sources of financing

option for company. Therefore, it can be said that Starbucks should acquire Roast Ltd

because there are great chances that company will do better, after its expansion in different

market.

Part 1: Industry Review

The industry of Coffee house is consisting all the specialist unlicensed institutions,

which is focused on the selling coffee with the cold and hot drinks or light snacks. The

industry’s performance is determined by the both social and economic factors, consisting of

growth in the real disposable income of household, greater interest of the consumer in the

Executive Summary

Financial decision is the process, which is responsible for decisions that is related

with company’s shareholders’ equity and liabilities and issuance of bonds. Good decisions of

financial planning extend well-beyond how and where to invest. The ability of spending more

than one could otherwise indicates that assets are generating higher return that results in good

decision-making that makes high spending possible.

This report finds that the coffee house industry of UK indicates better growth of

industry in next five years. Secondly, the business performance of Roast Ltd. indicates that it

is at its expansion stage, but still company is doing well. The profitability condition of

company indicates that it has been improved in comparison to last year, the liquidity position

indicates that it is having the ability for paying short-term liabilities, solvency position

indicates that it is using more debt in comparison to equity, efficiency position indicates that

it is utilizing its assets efficiently and lastly, operating cash cycle indicates that operating

efficiency of company has been reduced in generating cash. Lastly, it has been found that

management forecast proves to be wrong, NPV method proves to be good investment

appraisal technique for the company and issuing of bond can be good sources of financing

option for company. Therefore, it can be said that Starbucks should acquire Roast Ltd

because there are great chances that company will do better, after its expansion in different

market.

Part 1: Industry Review

The industry of Coffee house is consisting all the specialist unlicensed institutions,

which is focused on the selling coffee with the cold and hot drinks or light snacks. The

industry’s performance is determined by the both social and economic factors, consisting of

growth in the real disposable income of household, greater interest of the consumer in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL DECISION MAKING

coffee blends and origins & preferences for coffee house over the other social venues. Hence,

following are points that highlights top-line review of UK industry of coffee house:

Over recent years, industry has strongly performed aided by the greater demand

because culture of coffee is becoming much more popular among the consumers.

The coffee shops of UK have celebrated its twenty successive years of the growth of

market, with £10.1bn market continues to be robust in between tough conditions of

economy.

Total segment of branded coffee shops of UK added over around 1,300 in 2018 with

the slower growth rate of 5.8% compared to 7.1% in previous year.

The key UK coffee house players are “Costa”, “Starbucks” and “Caffe Nero”. Costa

was largest chain of coffee in UK by total outlets 2,655 as of January 2019 and

Starbucks was only non-British entity with around 992 stores.

Largest share of the retail coffee is being through the supermarkets and hypermarkets

that accounts for 35 percent and 37 percent of all the retailing of coffee.

Traditionally, UK was known for consuming instant coffee. The regular generated

instant coffee generates £810 million turnover that is equivalent to 54 percent of

overall turnover of £1.5 billion, which is generated by all the sold products of coffee

in the sector of retail.

The segment of “out-of-home” is the growing market and it signifies around 33% of

volume sales of all products of coffee.

The coffee house industry is expected to continue over the coming five-year period.

The rise in competition as well as continuing uncertainty surrounding exit of UK

from EU are expected to constrain growth.

The year 2020 will be crucial year for segment of UK Coffee shop, as operators

grapple with ramifications of the Brexit, seeking for consolidating M&A activities of

coffee blends and origins & preferences for coffee house over the other social venues. Hence,

following are points that highlights top-line review of UK industry of coffee house:

Over recent years, industry has strongly performed aided by the greater demand

because culture of coffee is becoming much more popular among the consumers.

The coffee shops of UK have celebrated its twenty successive years of the growth of

market, with £10.1bn market continues to be robust in between tough conditions of

economy.

Total segment of branded coffee shops of UK added over around 1,300 in 2018 with

the slower growth rate of 5.8% compared to 7.1% in previous year.

The key UK coffee house players are “Costa”, “Starbucks” and “Caffe Nero”. Costa

was largest chain of coffee in UK by total outlets 2,655 as of January 2019 and

Starbucks was only non-British entity with around 992 stores.

Largest share of the retail coffee is being through the supermarkets and hypermarkets

that accounts for 35 percent and 37 percent of all the retailing of coffee.

Traditionally, UK was known for consuming instant coffee. The regular generated

instant coffee generates £810 million turnover that is equivalent to 54 percent of

overall turnover of £1.5 billion, which is generated by all the sold products of coffee

in the sector of retail.

The segment of “out-of-home” is the growing market and it signifies around 33% of

volume sales of all products of coffee.

The coffee house industry is expected to continue over the coming five-year period.

The rise in competition as well as continuing uncertainty surrounding exit of UK

from EU are expected to constrain growth.

The year 2020 will be crucial year for segment of UK Coffee shop, as operators

grapple with ramifications of the Brexit, seeking for consolidating M&A activities of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL DECISION MAKING

2019 and maintaining loyalty of customer in fiercely competitive market

(Worldcoffeeportal.com. 2020).

Part 2: Business Performance Analysis

Statement of Profit or Loss

Profitability ratio of the Roast Limited will evaluate ability of entity in making

income in comparison to its expenses as well as other associated cost with income generation

during particular period. This helps in representing final outcome of entity. Hence, the first

ratio calculated for assessing the profitability of Roast Limited is gross profit margin ratio.

This ratio calculates the sales percentages, which exceeds cost of goods sold. It helps in

indicating performance of firm’s production and sales. In 2017, gross profit margin of Roast

was 26%, which reduced to 21% in 2018. It means that that the revenues left over after

paying off the cost of goods sold has been decreased by 5% (Dahmen and Rodríguez 2014).

“Operating profit margin ratio” is second ratio calculated for assessing profitability

of company. This ratio is the performance or profitability ratio, which reflects profit

percentage produced by the company from its operations, before subtracting interest charges

and taxes. It can be measured by dividing operating profit by the overall revenue and it is

expressed as percentage. Operating margin ratio of the Roast limited was 3% in year 2017

and 5% in 2017. It signifies that ratio has been increased by 2%. This increase in the ratio

indicates that ability of firm in making profit on sales after making payment for production’s

variable cost such as raw material and wages and before making payment of taxes and

interest has been increased. This shows proportion of the revenues available for covering

non-operating costs, for instance interest expense (Khadafi, Heikal and Ummah 2014).

“Net profit margin ratio” is the ratio, which is used for calculating percentage of the

profit that firm produces from its overall revenue. This measure amount of the net profit

2019 and maintaining loyalty of customer in fiercely competitive market

(Worldcoffeeportal.com. 2020).

Part 2: Business Performance Analysis

Statement of Profit or Loss

Profitability ratio of the Roast Limited will evaluate ability of entity in making

income in comparison to its expenses as well as other associated cost with income generation

during particular period. This helps in representing final outcome of entity. Hence, the first

ratio calculated for assessing the profitability of Roast Limited is gross profit margin ratio.

This ratio calculates the sales percentages, which exceeds cost of goods sold. It helps in

indicating performance of firm’s production and sales. In 2017, gross profit margin of Roast

was 26%, which reduced to 21% in 2018. It means that that the revenues left over after

paying off the cost of goods sold has been decreased by 5% (Dahmen and Rodríguez 2014).

“Operating profit margin ratio” is second ratio calculated for assessing profitability

of company. This ratio is the performance or profitability ratio, which reflects profit

percentage produced by the company from its operations, before subtracting interest charges

and taxes. It can be measured by dividing operating profit by the overall revenue and it is

expressed as percentage. Operating margin ratio of the Roast limited was 3% in year 2017

and 5% in 2017. It signifies that ratio has been increased by 2%. This increase in the ratio

indicates that ability of firm in making profit on sales after making payment for production’s

variable cost such as raw material and wages and before making payment of taxes and

interest has been increased. This shows proportion of the revenues available for covering

non-operating costs, for instance interest expense (Khadafi, Heikal and Ummah 2014).

“Net profit margin ratio” is the ratio, which is used for calculating percentage of the

profit that firm produces from its overall revenue. This measure amount of the net profit

5FINANCIAL DECISION MAKING

obtained by entity from per dollar of the sales generated. It is considered to be the bottom line

for the entity (Ehiedu 2014). It helps the investors in assessing that whether management of

company is generating sufficient profit from its total revenue and whether the overhead costs

and operating costs are being contained. It is the most significant indicator of firm’s financial

health. When it comes to Roast Ltd., net profit margin was 2% in 2017 and 3% in 2018. This

means that the ratio has been increased by 1%, but still it can be easily seen that compared to

sales, company is generating very less profit. This means cost of operations is higher. The

company need to control its cost for generating higher return (Kraft 2015).

Return on equity is measure of the financial performance that is measured by dividing

the net profit by total shareholders’ equity. If the ratio is higher, then it means management of

entity is more efficient in generating growth and income from its financing of equity

(Enekwe, Agu and Eziedo 2014). In case of the Roast Limited, the ROE was 5% in 2017 and

9% in 2018. This means that ROE of company has been increased by 4%. The rise in ratio

indicates that rate of the return on resources provided by the stockholders’ equity of company

has been increased. The business operations of Roast Limited are able to utilize successfully

the resources provided by accumulated profits of company and equity investors in generating

the income. However, still firm is not able to generate higher return compared to its total

equity (Yu et al. 2014).

Last, profitability ratio calculated is “return on assets”. It is financial ratio, which

shows percentage of the income earned by the firm in relation to its resources. Further, higher

is the ratio, the more will be efficiency of assets (Robinson et al. 2015). In Roast Limited,

ROA of firm was 4% in 2017 and 6% in 2018. It means that the ratio has been increased by

2%. This increase in the ratio indicates that firm is utilizing its assets in the most efficient

way. However, the rate of return in comparison to its assets is very less. Roast Limited is able

obtained by entity from per dollar of the sales generated. It is considered to be the bottom line

for the entity (Ehiedu 2014). It helps the investors in assessing that whether management of

company is generating sufficient profit from its total revenue and whether the overhead costs

and operating costs are being contained. It is the most significant indicator of firm’s financial

health. When it comes to Roast Ltd., net profit margin was 2% in 2017 and 3% in 2018. This

means that the ratio has been increased by 1%, but still it can be easily seen that compared to

sales, company is generating very less profit. This means cost of operations is higher. The

company need to control its cost for generating higher return (Kraft 2015).

Return on equity is measure of the financial performance that is measured by dividing

the net profit by total shareholders’ equity. If the ratio is higher, then it means management of

entity is more efficient in generating growth and income from its financing of equity

(Enekwe, Agu and Eziedo 2014). In case of the Roast Limited, the ROE was 5% in 2017 and

9% in 2018. This means that ROE of company has been increased by 4%. The rise in ratio

indicates that rate of the return on resources provided by the stockholders’ equity of company

has been increased. The business operations of Roast Limited are able to utilize successfully

the resources provided by accumulated profits of company and equity investors in generating

the income. However, still firm is not able to generate higher return compared to its total

equity (Yu et al. 2014).

Last, profitability ratio calculated is “return on assets”. It is financial ratio, which

shows percentage of the income earned by the firm in relation to its resources. Further, higher

is the ratio, the more will be efficiency of assets (Robinson et al. 2015). In Roast Limited,

ROA of firm was 4% in 2017 and 6% in 2018. It means that the ratio has been increased by

2%. This increase in the ratio indicates that firm is utilizing its assets in the most efficient

way. However, the rate of return in comparison to its assets is very less. Roast Limited is able

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL DECISION MAKING

to convert money it invests into the net profit, but the rate of converting the money is very

less (Carreras-Simó and Coenders 2019).

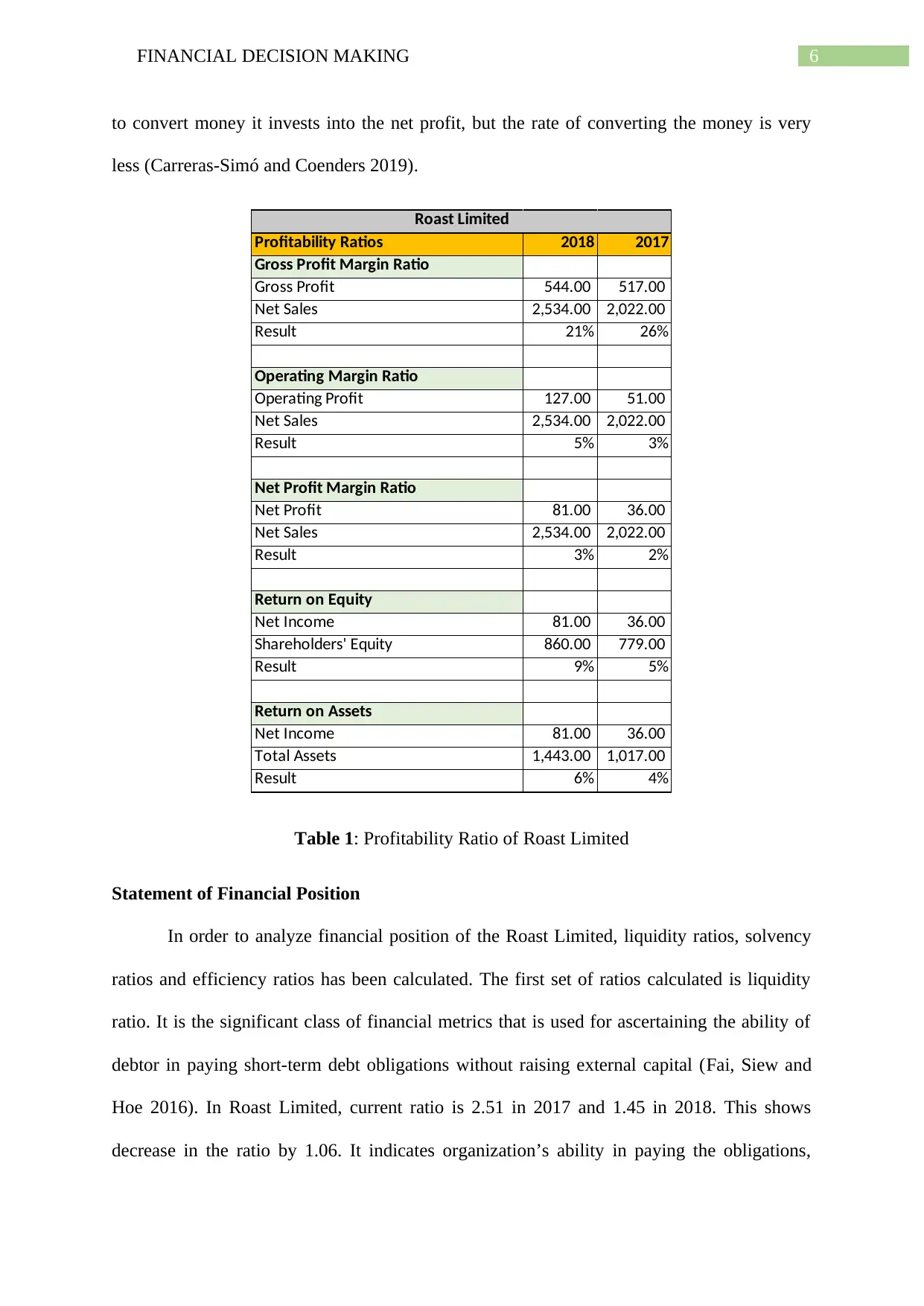

Profitability Ratios 2018 2017

Gross Profit Margin Ratio

Gross Profit 544.00 517.00

Net Sales 2,534.00 2,022.00

Result 21% 26%

Operating Margin Ratio

Operating Profit 127.00 51.00

Net Sales 2,534.00 2,022.00

Result 5% 3%

Net Profit Margin Ratio

Net Profit 81.00 36.00

Net Sales 2,534.00 2,022.00

Result 3% 2%

Return on Equity

Net Income 81.00 36.00

Shareholders' Equity 860.00 779.00

Result 9% 5%

Return on Assets

Net Income 81.00 36.00

Total Assets 1,443.00 1,017.00

Result 6% 4%

Roast Limited

Table 1: Profitability Ratio of Roast Limited

Statement of Financial Position

In order to analyze financial position of the Roast Limited, liquidity ratios, solvency

ratios and efficiency ratios has been calculated. The first set of ratios calculated is liquidity

ratio. It is the significant class of financial metrics that is used for ascertaining the ability of

debtor in paying short-term debt obligations without raising external capital (Fai, Siew and

Hoe 2016). In Roast Limited, current ratio is 2.51 in 2017 and 1.45 in 2018. This shows

decrease in the ratio by 1.06. It indicates organization’s ability in paying the obligations,

to convert money it invests into the net profit, but the rate of converting the money is very

less (Carreras-Simó and Coenders 2019).

Profitability Ratios 2018 2017

Gross Profit Margin Ratio

Gross Profit 544.00 517.00

Net Sales 2,534.00 2,022.00

Result 21% 26%

Operating Margin Ratio

Operating Profit 127.00 51.00

Net Sales 2,534.00 2,022.00

Result 5% 3%

Net Profit Margin Ratio

Net Profit 81.00 36.00

Net Sales 2,534.00 2,022.00

Result 3% 2%

Return on Equity

Net Income 81.00 36.00

Shareholders' Equity 860.00 779.00

Result 9% 5%

Return on Assets

Net Income 81.00 36.00

Total Assets 1,443.00 1,017.00

Result 6% 4%

Roast Limited

Table 1: Profitability Ratio of Roast Limited

Statement of Financial Position

In order to analyze financial position of the Roast Limited, liquidity ratios, solvency

ratios and efficiency ratios has been calculated. The first set of ratios calculated is liquidity

ratio. It is the significant class of financial metrics that is used for ascertaining the ability of

debtor in paying short-term debt obligations without raising external capital (Fai, Siew and

Hoe 2016). In Roast Limited, current ratio is 2.51 in 2017 and 1.45 in 2018. This shows

decrease in the ratio by 1.06. It indicates organization’s ability in paying the obligations,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL DECISION MAKING

which is due within the year has been reduced. Although the ratio still indicates that it is able

to pay the obligations of short-term with its assets of short-term, but in comparison to last

year, its ability is decreased (Yahaya, Fagbemi and Oyeniyi 2015).

Quick ratio is gauge of company’s liquidity position of the short-term and measures

entity’s ability in meeting its debts of the short-term with the most liquid assets. In case of

Roast Limited, company’s quick ratio was 1.64 in 2017 and 0.48 in 2018. This depicts that

firm’s ability in paying the short-term debts from its most liquidized assets has been reduced,

which means Roast Ltd. is not fully equipped with the sufficient assets for instantly

liquidating to pay its short-term debts (Altman et al. 2017).

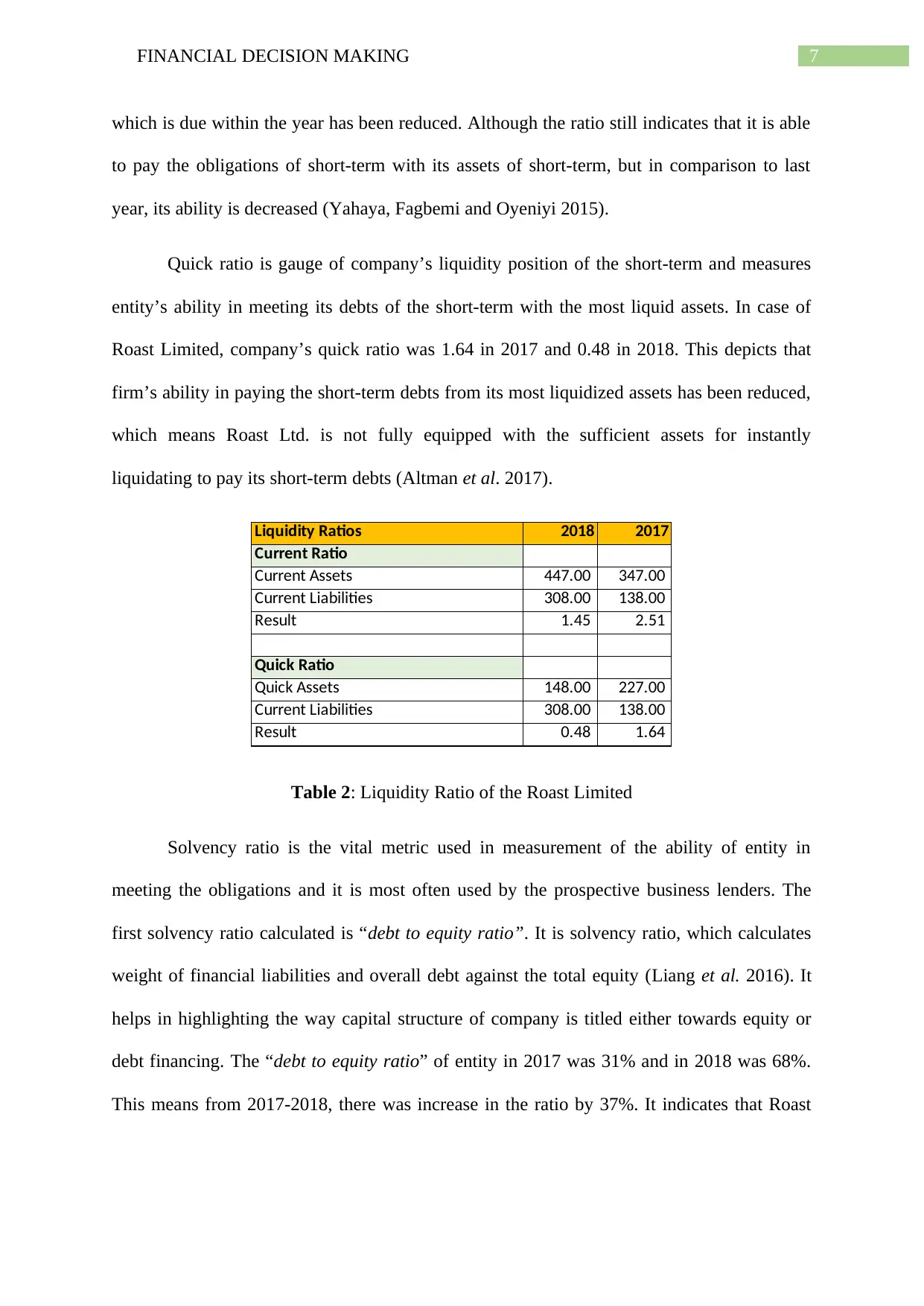

Liquidity Ratios 2018 2017

Current Ratio

Current Assets 447.00 347.00

Current Liabilities 308.00 138.00

Result 1.45 2.51

Quick Ratio

Quick Assets 148.00 227.00

Current Liabilities 308.00 138.00

Result 0.48 1.64

Table 2: Liquidity Ratio of the Roast Limited

Solvency ratio is the vital metric used in measurement of the ability of entity in

meeting the obligations and it is most often used by the prospective business lenders. The

first solvency ratio calculated is “debt to equity ratio”. It is solvency ratio, which calculates

weight of financial liabilities and overall debt against the total equity (Liang et al. 2016). It

helps in highlighting the way capital structure of company is titled either towards equity or

debt financing. The “debt to equity ratio” of entity in 2017 was 31% and in 2018 was 68%.

This means from 2017-2018, there was increase in the ratio by 37%. It indicates that Roast

which is due within the year has been reduced. Although the ratio still indicates that it is able

to pay the obligations of short-term with its assets of short-term, but in comparison to last

year, its ability is decreased (Yahaya, Fagbemi and Oyeniyi 2015).

Quick ratio is gauge of company’s liquidity position of the short-term and measures

entity’s ability in meeting its debts of the short-term with the most liquid assets. In case of

Roast Limited, company’s quick ratio was 1.64 in 2017 and 0.48 in 2018. This depicts that

firm’s ability in paying the short-term debts from its most liquidized assets has been reduced,

which means Roast Ltd. is not fully equipped with the sufficient assets for instantly

liquidating to pay its short-term debts (Altman et al. 2017).

Liquidity Ratios 2018 2017

Current Ratio

Current Assets 447.00 347.00

Current Liabilities 308.00 138.00

Result 1.45 2.51

Quick Ratio

Quick Assets 148.00 227.00

Current Liabilities 308.00 138.00

Result 0.48 1.64

Table 2: Liquidity Ratio of the Roast Limited

Solvency ratio is the vital metric used in measurement of the ability of entity in

meeting the obligations and it is most often used by the prospective business lenders. The

first solvency ratio calculated is “debt to equity ratio”. It is solvency ratio, which calculates

weight of financial liabilities and overall debt against the total equity (Liang et al. 2016). It

helps in highlighting the way capital structure of company is titled either towards equity or

debt financing. The “debt to equity ratio” of entity in 2017 was 31% and in 2018 was 68%.

This means from 2017-2018, there was increase in the ratio by 37%. It indicates that Roast

8FINANCIAL DECISION MAKING

Limited is using higher level of debt in comparison to the equity, which is quite risky (Minnis

and Sutherland 2017).

The capital gearing ratio is the most beneficial tools in analyzing the entity’s capital

structure. It is ratio between the total debt and total equity. It is the most vital metric for the

analysts when thinking about investing in any entity, as they want for comparing whether

right capital structure is hold by company or not. The “capital gearing ratio” of firm was

13% in year 2017 that increased to 24% in 2018. This indicates that the Roast Limited is high

geared, which means company is using more debt and they are required to give more interest

that ultimately increases the risk of investors (Feng et al. 2015).

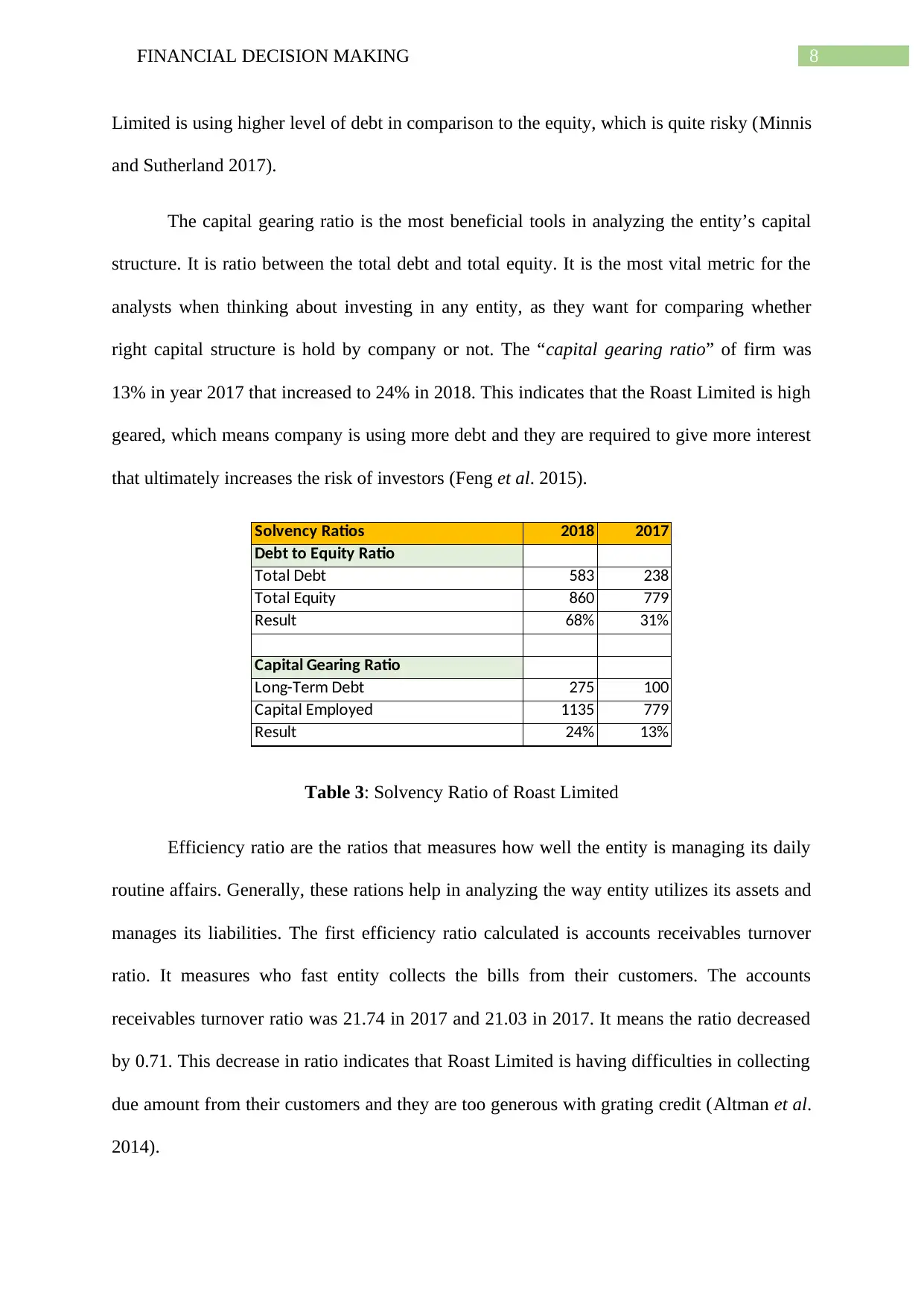

Solvency Ratios 2018 2017

Debt to Equity Ratio

Total Debt 583 238

Total Equity 860 779

Result 68% 31%

Capital Gearing Ratio

Long-Term Debt 275 100

Capital Employed 1135 779

Result 24% 13%

Table 3: Solvency Ratio of Roast Limited

Efficiency ratio are the ratios that measures how well the entity is managing its daily

routine affairs. Generally, these rations help in analyzing the way entity utilizes its assets and

manages its liabilities. The first efficiency ratio calculated is accounts receivables turnover

ratio. It measures who fast entity collects the bills from their customers. The accounts

receivables turnover ratio was 21.74 in 2017 and 21.03 in 2017. It means the ratio decreased

by 0.71. This decrease in ratio indicates that Roast Limited is having difficulties in collecting

due amount from their customers and they are too generous with grating credit (Altman et al.

2014).

Limited is using higher level of debt in comparison to the equity, which is quite risky (Minnis

and Sutherland 2017).

The capital gearing ratio is the most beneficial tools in analyzing the entity’s capital

structure. It is ratio between the total debt and total equity. It is the most vital metric for the

analysts when thinking about investing in any entity, as they want for comparing whether

right capital structure is hold by company or not. The “capital gearing ratio” of firm was

13% in year 2017 that increased to 24% in 2018. This indicates that the Roast Limited is high

geared, which means company is using more debt and they are required to give more interest

that ultimately increases the risk of investors (Feng et al. 2015).

Solvency Ratios 2018 2017

Debt to Equity Ratio

Total Debt 583 238

Total Equity 860 779

Result 68% 31%

Capital Gearing Ratio

Long-Term Debt 275 100

Capital Employed 1135 779

Result 24% 13%

Table 3: Solvency Ratio of Roast Limited

Efficiency ratio are the ratios that measures how well the entity is managing its daily

routine affairs. Generally, these rations help in analyzing the way entity utilizes its assets and

manages its liabilities. The first efficiency ratio calculated is accounts receivables turnover

ratio. It measures who fast entity collects the bills from their customers. The accounts

receivables turnover ratio was 21.74 in 2017 and 21.03 in 2017. It means the ratio decreased

by 0.71. This decrease in ratio indicates that Roast Limited is having difficulties in collecting

due amount from their customers and they are too generous with grating credit (Altman et al.

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL DECISION MAKING

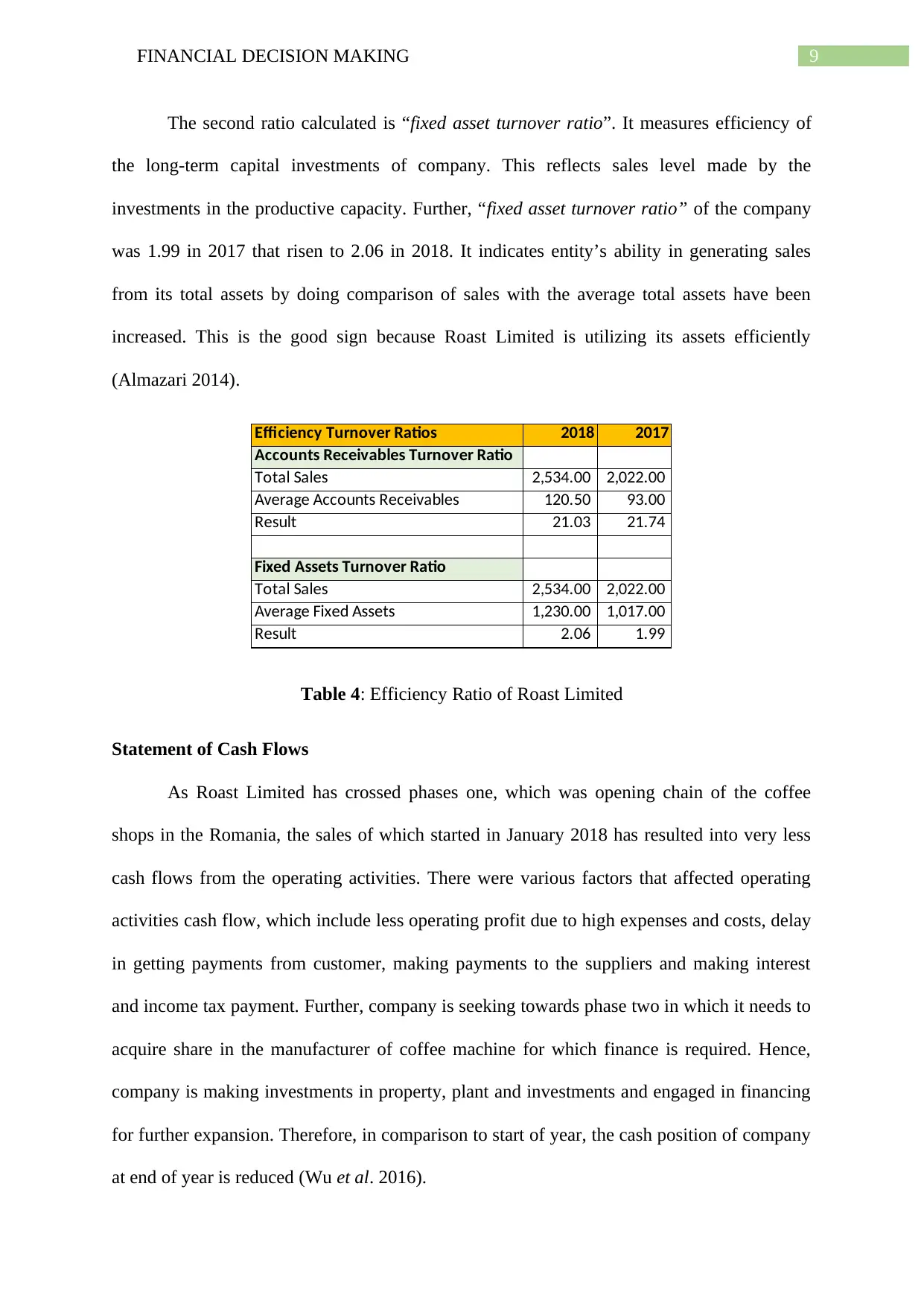

The second ratio calculated is “fixed asset turnover ratio”. It measures efficiency of

the long-term capital investments of company. This reflects sales level made by the

investments in the productive capacity. Further, “fixed asset turnover ratio” of the company

was 1.99 in 2017 that risen to 2.06 in 2018. It indicates entity’s ability in generating sales

from its total assets by doing comparison of sales with the average total assets have been

increased. This is the good sign because Roast Limited is utilizing its assets efficiently

(Almazari 2014).

Efficiency Turnover Ratios 2018 2017

Accounts Receivables Turnover Ratio

Total Sales 2,534.00 2,022.00

Average Accounts Receivables 120.50 93.00

Result 21.03 21.74

Fixed Assets Turnover Ratio

Total Sales 2,534.00 2,022.00

Average Fixed Assets 1,230.00 1,017.00

Result 2.06 1.99

Table 4: Efficiency Ratio of Roast Limited

Statement of Cash Flows

As Roast Limited has crossed phases one, which was opening chain of the coffee

shops in the Romania, the sales of which started in January 2018 has resulted into very less

cash flows from the operating activities. There were various factors that affected operating

activities cash flow, which include less operating profit due to high expenses and costs, delay

in getting payments from customer, making payments to the suppliers and making interest

and income tax payment. Further, company is seeking towards phase two in which it needs to

acquire share in the manufacturer of coffee machine for which finance is required. Hence,

company is making investments in property, plant and investments and engaged in financing

for further expansion. Therefore, in comparison to start of year, the cash position of company

at end of year is reduced (Wu et al. 2016).

The second ratio calculated is “fixed asset turnover ratio”. It measures efficiency of

the long-term capital investments of company. This reflects sales level made by the

investments in the productive capacity. Further, “fixed asset turnover ratio” of the company

was 1.99 in 2017 that risen to 2.06 in 2018. It indicates entity’s ability in generating sales

from its total assets by doing comparison of sales with the average total assets have been

increased. This is the good sign because Roast Limited is utilizing its assets efficiently

(Almazari 2014).

Efficiency Turnover Ratios 2018 2017

Accounts Receivables Turnover Ratio

Total Sales 2,534.00 2,022.00

Average Accounts Receivables 120.50 93.00

Result 21.03 21.74

Fixed Assets Turnover Ratio

Total Sales 2,534.00 2,022.00

Average Fixed Assets 1,230.00 1,017.00

Result 2.06 1.99

Table 4: Efficiency Ratio of Roast Limited

Statement of Cash Flows

As Roast Limited has crossed phases one, which was opening chain of the coffee

shops in the Romania, the sales of which started in January 2018 has resulted into very less

cash flows from the operating activities. There were various factors that affected operating

activities cash flow, which include less operating profit due to high expenses and costs, delay

in getting payments from customer, making payments to the suppliers and making interest

and income tax payment. Further, company is seeking towards phase two in which it needs to

acquire share in the manufacturer of coffee machine for which finance is required. Hence,

company is making investments in property, plant and investments and engaged in financing

for further expansion. Therefore, in comparison to start of year, the cash position of company

at end of year is reduced (Wu et al. 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL DECISION MAKING

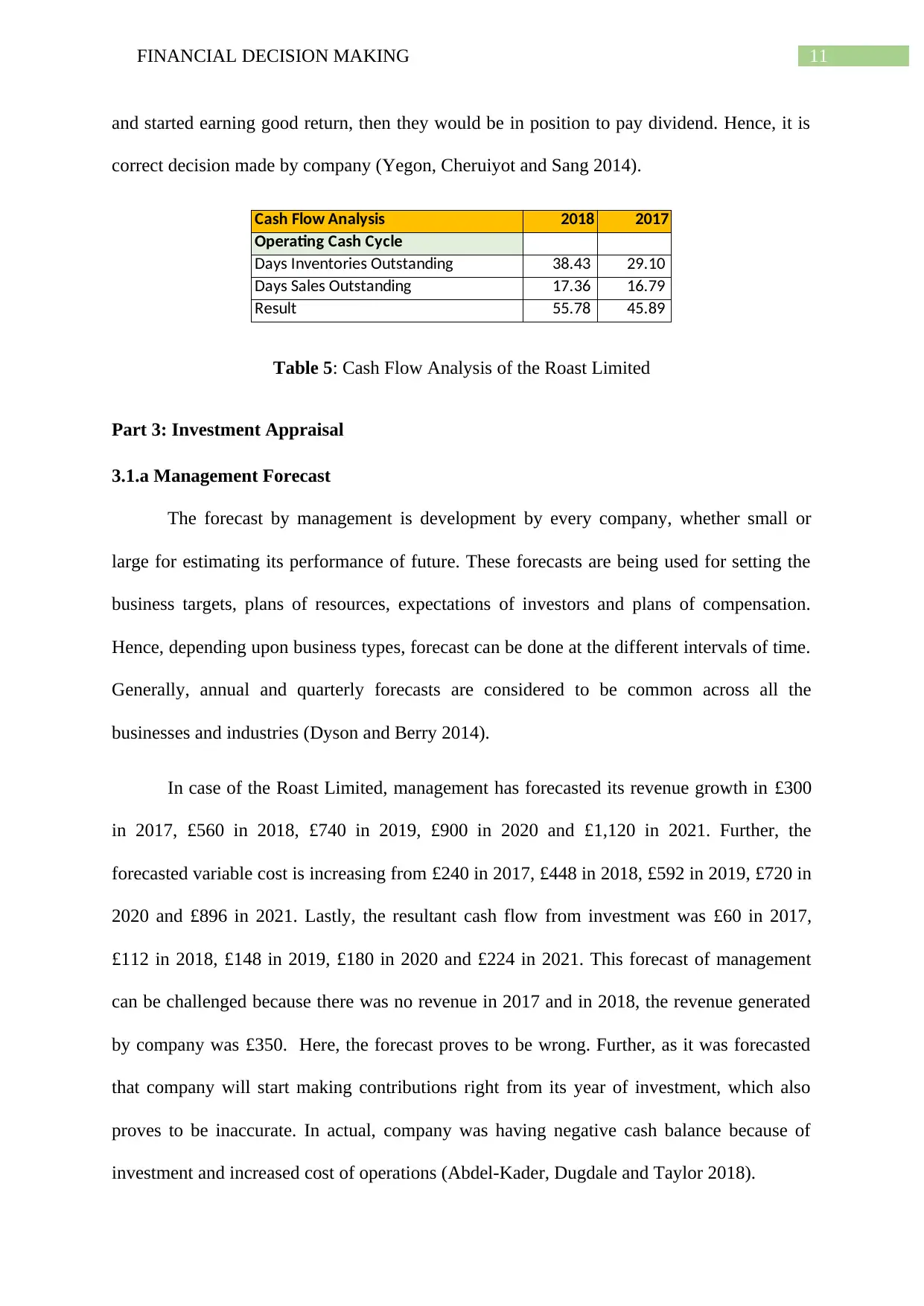

Operating cash cycle is the measure of cash amount generated by the normal business

operations of entity. It helps in indicating that whether entity is able to generate enough

positive flow of cash for growing and maintaining its business operations, otherwise,

company will need external financing for the expansion of capital. In case of Roast Limited,

the operating cash cycle was 45.89 in 2017 and in 2018 was 55.78. It means that the cycle of

operating cash has been increased by 9.89. This increase in operating cash cycle of entity

shows that the days required for the business for receiving inventory, selling it and collecting

the cash from selling inventory has been increased (Nobanee and Al Hajjar 2014). It gives the

insight that operating efficiency of the company has been reduced because entity’s ability for

recovering its investment of investment is taking more time and it does not possess enough

cash for meeting the obligations. This will create the problems of cash flow. Roast limited

can reduce its cycle of operating cash by speeding up its inventory sale and reducing required

time for collecting receivables (Kroes and Manikas 2014).

Lastly, the dividend policy of Roast Limited for 2018 can be easily visible through the

financial statements and notes from meeting in between the officer of loan at the Finance

bank and the CEO of Roast Limited. The company is planning to retain all its earning for its

second phase of expansion. This requires huge need of finance, for which company had

decided for not paying dividend for 2018 and retaining the earnings (Fairchild, Guney and

Thanatawee 2014).

Roast Limited was right in not making the dividend payment in 2018 because the

financial position of company was not that much robust that they would have given dividend.

The company is looking for retaining the earning so that it can be used for company’

development and expansion (Amoako-Adu, Baulkaran and Smith 2014). In order to grow,

company needs to invest huge amount of money and once it becomes established business

Operating cash cycle is the measure of cash amount generated by the normal business

operations of entity. It helps in indicating that whether entity is able to generate enough

positive flow of cash for growing and maintaining its business operations, otherwise,

company will need external financing for the expansion of capital. In case of Roast Limited,

the operating cash cycle was 45.89 in 2017 and in 2018 was 55.78. It means that the cycle of

operating cash has been increased by 9.89. This increase in operating cash cycle of entity

shows that the days required for the business for receiving inventory, selling it and collecting

the cash from selling inventory has been increased (Nobanee and Al Hajjar 2014). It gives the

insight that operating efficiency of the company has been reduced because entity’s ability for

recovering its investment of investment is taking more time and it does not possess enough

cash for meeting the obligations. This will create the problems of cash flow. Roast limited

can reduce its cycle of operating cash by speeding up its inventory sale and reducing required

time for collecting receivables (Kroes and Manikas 2014).

Lastly, the dividend policy of Roast Limited for 2018 can be easily visible through the

financial statements and notes from meeting in between the officer of loan at the Finance

bank and the CEO of Roast Limited. The company is planning to retain all its earning for its

second phase of expansion. This requires huge need of finance, for which company had

decided for not paying dividend for 2018 and retaining the earnings (Fairchild, Guney and

Thanatawee 2014).

Roast Limited was right in not making the dividend payment in 2018 because the

financial position of company was not that much robust that they would have given dividend.

The company is looking for retaining the earning so that it can be used for company’

development and expansion (Amoako-Adu, Baulkaran and Smith 2014). In order to grow,

company needs to invest huge amount of money and once it becomes established business

11FINANCIAL DECISION MAKING

and started earning good return, then they would be in position to pay dividend. Hence, it is

correct decision made by company (Yegon, Cheruiyot and Sang 2014).

Cash Flow Analysis 2018 2017

Operating Cash Cycle

Days Inventories Outstanding 38.43 29.10

Days Sales Outstanding 17.36 16.79

Result 55.78 45.89

Table 5: Cash Flow Analysis of the Roast Limited

Part 3: Investment Appraisal

3.1.a Management Forecast

The forecast by management is development by every company, whether small or

large for estimating its performance of future. These forecasts are being used for setting the

business targets, plans of resources, expectations of investors and plans of compensation.

Hence, depending upon business types, forecast can be done at the different intervals of time.

Generally, annual and quarterly forecasts are considered to be common across all the

businesses and industries (Dyson and Berry 2014).

In case of the Roast Limited, management has forecasted its revenue growth in £300

in 2017, £560 in 2018, £740 in 2019, £900 in 2020 and £1,120 in 2021. Further, the

forecasted variable cost is increasing from £240 in 2017, £448 in 2018, £592 in 2019, £720 in

2020 and £896 in 2021. Lastly, the resultant cash flow from investment was £60 in 2017,

£112 in 2018, £148 in 2019, £180 in 2020 and £224 in 2021. This forecast of management

can be challenged because there was no revenue in 2017 and in 2018, the revenue generated

by company was £350. Here, the forecast proves to be wrong. Further, as it was forecasted

that company will start making contributions right from its year of investment, which also

proves to be inaccurate. In actual, company was having negative cash balance because of

investment and increased cost of operations (Abdel-Kader, Dugdale and Taylor 2018).

and started earning good return, then they would be in position to pay dividend. Hence, it is

correct decision made by company (Yegon, Cheruiyot and Sang 2014).

Cash Flow Analysis 2018 2017

Operating Cash Cycle

Days Inventories Outstanding 38.43 29.10

Days Sales Outstanding 17.36 16.79

Result 55.78 45.89

Table 5: Cash Flow Analysis of the Roast Limited

Part 3: Investment Appraisal

3.1.a Management Forecast

The forecast by management is development by every company, whether small or

large for estimating its performance of future. These forecasts are being used for setting the

business targets, plans of resources, expectations of investors and plans of compensation.

Hence, depending upon business types, forecast can be done at the different intervals of time.

Generally, annual and quarterly forecasts are considered to be common across all the

businesses and industries (Dyson and Berry 2014).

In case of the Roast Limited, management has forecasted its revenue growth in £300

in 2017, £560 in 2018, £740 in 2019, £900 in 2020 and £1,120 in 2021. Further, the

forecasted variable cost is increasing from £240 in 2017, £448 in 2018, £592 in 2019, £720 in

2020 and £896 in 2021. Lastly, the resultant cash flow from investment was £60 in 2017,

£112 in 2018, £148 in 2019, £180 in 2020 and £224 in 2021. This forecast of management

can be challenged because there was no revenue in 2017 and in 2018, the revenue generated

by company was £350. Here, the forecast proves to be wrong. Further, as it was forecasted

that company will start making contributions right from its year of investment, which also

proves to be inaccurate. In actual, company was having negative cash balance because of

investment and increased cost of operations (Abdel-Kader, Dugdale and Taylor 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.