Financial Decision Making Report: Panini Ltd, BM 414 Analysis

VerifiedAdded on 2023/06/10

|10

|3014

|118

Report

AI Summary

This report provides a detailed financial analysis of Panini Ltd, a medium-sized bread-making company, focusing on financial decision-making. It begins with an introduction to financial decision-making and outlines the duties and responsibilities of accounting and finance departments. The report then delves into specific functions within these departments, including financial accounting, management accounting, tax, auditing, investment, financing, dividend, and working capital. Furthermore, the report explores various sources of finance available to Panini Ltd for expansion purposes, distinguishing between long-term and short-term financing options. A significant portion of the report is dedicated to ratio analysis, where eight key financial ratios are calculated for 2018 and 2019, including gross profit margin, operating profit margin, ROCE, current ratio, quick ratio, inventory turnover days, debtor’s collection period, and creditor’s collection period. Each ratio is analyzed individually, comparing the results between the two years and discussing the implications of the changes. The report concludes with recommendations for improving the financial performance of the company based on the ratio analysis and the overall financial data.

BM 414 Financial

Decision Making

Report

Decision Making

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Contents

INTRODUCTION...........................................................................................................................

TASK...............................................................................................................................................

Identify the functions related to finance and accounting departments.............................

PART B...........................................................................................................................................

Calculate the ratios...................................................................................................................

CONCLUSION.............................................................................................................................

REFERENCES............................................................................................................................

Contents

INTRODUCTION...........................................................................................................................

TASK...............................................................................................................................................

Identify the functions related to finance and accounting departments.............................

PART B...........................................................................................................................................

Calculate the ratios...................................................................................................................

CONCLUSION.............................................................................................................................

REFERENCES............................................................................................................................

Introduction

Financial decision making is a decision made by the Finance Manager in

order to know about the finance matrix of the management. Financial decision

making mainly focuses on borrowing and allocation of funds. Funds can be arranged

by an organisation by two sources namely its own capital and from outside the

organisation (Abu-Rahma and Jaleel, 2019). In the following it explains about the duty

and responsibilities of Panini. Ltd. It also provides various accounting functions

performed and duties of the management. It also helps in determining the objective

and goals of the management. Further various ratios are calculated to know the

performance of Panini Ltd. And also advice on the various methods which helps in

improving the performance of the company.

TASK 1

Part a: Accounting and Finance departments

For each of the below two departments, you need to provide a brief

introduction, before you proceed to the analysis of each function.

The following two departments along with their functions should be covered:

1. Accounting department:

a) Financial accounting function: The element of bookkeeping the

monetary activity. This system helps in dealing with the past records of

the management. It further helps in arranging the past records for the

future plans and goals purpose. It also aids in managing the expenses

and monetary figures. There are few elements of bookkeeping:

It helps in keeping the monetary transactions of the organisation: This method helps

in mainting the association with the accounts and bookkeeping in order to know the

the records of the firm (Dilawar and et.al., 2021).

b) Management accounting function: management helps supervisor to

know the actual association between the management and association.

It helps in breaking, deciding, deciphering the data and convey the

information. Association helps in accomplish the goals of the

management.

c) Tax function: this function helps in knowing the implication and

consequences of the transactions and report those transaction to the

stakeholders which helps helps them to know what is going in the

organization.

d) Auditing function: Audit function is conducted by the auditor of the

company and ensures that all the financial statements are accurate

and truthful.

2. Finance department:

Financial decision making is a decision made by the Finance Manager in

order to know about the finance matrix of the management. Financial decision

making mainly focuses on borrowing and allocation of funds. Funds can be arranged

by an organisation by two sources namely its own capital and from outside the

organisation (Abu-Rahma and Jaleel, 2019). In the following it explains about the duty

and responsibilities of Panini. Ltd. It also provides various accounting functions

performed and duties of the management. It also helps in determining the objective

and goals of the management. Further various ratios are calculated to know the

performance of Panini Ltd. And also advice on the various methods which helps in

improving the performance of the company.

TASK 1

Part a: Accounting and Finance departments

For each of the below two departments, you need to provide a brief

introduction, before you proceed to the analysis of each function.

The following two departments along with their functions should be covered:

1. Accounting department:

a) Financial accounting function: The element of bookkeeping the

monetary activity. This system helps in dealing with the past records of

the management. It further helps in arranging the past records for the

future plans and goals purpose. It also aids in managing the expenses

and monetary figures. There are few elements of bookkeeping:

It helps in keeping the monetary transactions of the organisation: This method helps

in mainting the association with the accounts and bookkeeping in order to know the

the records of the firm (Dilawar and et.al., 2021).

b) Management accounting function: management helps supervisor to

know the actual association between the management and association.

It helps in breaking, deciding, deciphering the data and convey the

information. Association helps in accomplish the goals of the

management.

c) Tax function: this function helps in knowing the implication and

consequences of the transactions and report those transaction to the

stakeholders which helps helps them to know what is going in the

organization.

d) Auditing function: Audit function is conducted by the auditor of the

company and ensures that all the financial statements are accurate

and truthful.

2. Finance department:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a) Investment function: Investment is related with the purchase of shares

and stocks, dentures, equities and government bond. These

investment only includes financial investment and not the real

investment (Dinçer, Yüksel and Çetiner, 2019).

b) Financing function: This function is related with the management which

helps in providing funds which is needed by the organizations in order

to funds the business activities of the businesses.

c) Dividend function: This function aids in distribution of profits to the

shareholders of the company. The amount of dividend is determined by

the help and under the guidance of board of directors of the

organisation. Dividends are the payments made by the company to its

shareholders for investing in the company.

d) Working capital function: It is the amount of funds needed by the

organisation in order to determine the needs to funds to meet the short

term debt obligation of the firm. If an organisation have enough working

capital then it will be able to pay off its suppliers and employees of the

organisation.

Part b: Sources of finance

Source of finance is used to finance activity for running and managing the business

activities. In the following case, Panini Ltd. Uses various sources of finance which is

available to the organisation to manage the business operations. These source of

finance includes equity, debt, working capital loan, term loan, etc. these funds are

used to finance the business activities and development of the business operational

activities (Fu and Chen, 2021).

It also plays a vital role in the marketing and economic activities of the business.

These activities supports the innovation, quality of owner and financial support.

There are two sources of finance:

Long term finance: long term source of finance is used to finance the business

activities and operations which are related with the long term profitability of the

business. Long term finance are mainly used for the project which the business is

going to undertake in order to upsurge the effectiveness and profitability of the

organization.

Short Term finance are taken to pay off the debt obligations which is considered for

paying the short term debt of the company. It helps in managing positive cash flow in

the management. Short term finance includes working capital loans, trade credit,

working capital loan (Kayanda, Busagala and Tedre, 2019).

TASK 2

Part a: Calculation of the 8 ratios below using the correct formulas

(i) Gross profit margin: Gross profit/ Net sales * 100

2018: 3500/ 10000 * 100 = 35%

and stocks, dentures, equities and government bond. These

investment only includes financial investment and not the real

investment (Dinçer, Yüksel and Çetiner, 2019).

b) Financing function: This function is related with the management which

helps in providing funds which is needed by the organizations in order

to funds the business activities of the businesses.

c) Dividend function: This function aids in distribution of profits to the

shareholders of the company. The amount of dividend is determined by

the help and under the guidance of board of directors of the

organisation. Dividends are the payments made by the company to its

shareholders for investing in the company.

d) Working capital function: It is the amount of funds needed by the

organisation in order to determine the needs to funds to meet the short

term debt obligation of the firm. If an organisation have enough working

capital then it will be able to pay off its suppliers and employees of the

organisation.

Part b: Sources of finance

Source of finance is used to finance activity for running and managing the business

activities. In the following case, Panini Ltd. Uses various sources of finance which is

available to the organisation to manage the business operations. These source of

finance includes equity, debt, working capital loan, term loan, etc. these funds are

used to finance the business activities and development of the business operational

activities (Fu and Chen, 2021).

It also plays a vital role in the marketing and economic activities of the business.

These activities supports the innovation, quality of owner and financial support.

There are two sources of finance:

Long term finance: long term source of finance is used to finance the business

activities and operations which are related with the long term profitability of the

business. Long term finance are mainly used for the project which the business is

going to undertake in order to upsurge the effectiveness and profitability of the

organization.

Short Term finance are taken to pay off the debt obligations which is considered for

paying the short term debt of the company. It helps in managing positive cash flow in

the management. Short term finance includes working capital loans, trade credit,

working capital loan (Kayanda, Busagala and Tedre, 2019).

TASK 2

Part a: Calculation of the 8 ratios below using the correct formulas

(i) Gross profit margin: Gross profit/ Net sales * 100

2018: 3500/ 10000 * 100 = 35%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

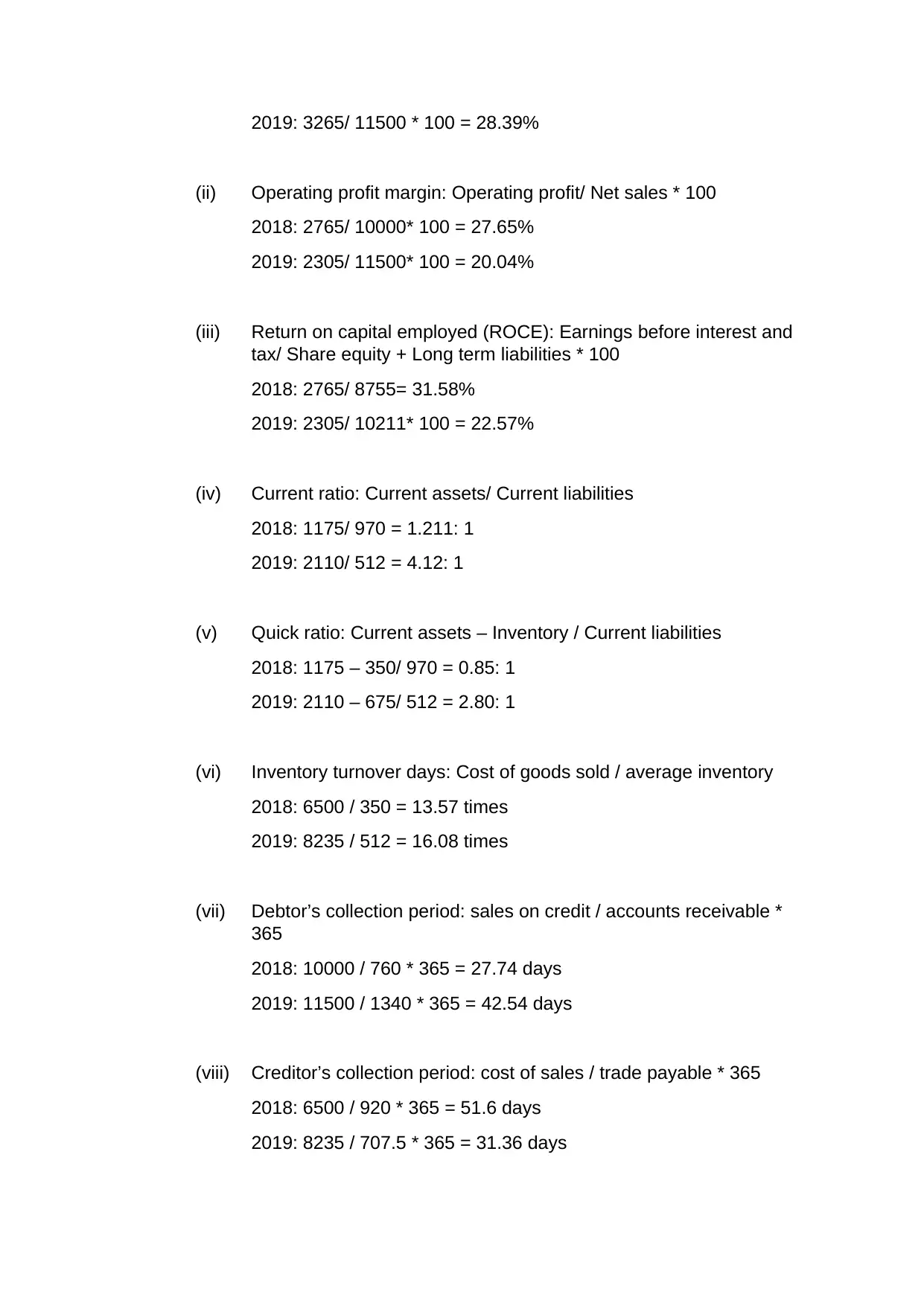

2019: 3265/ 11500 * 100 = 28.39%

(ii) Operating profit margin: Operating profit/ Net sales * 100

2018: 2765/ 10000* 100 = 27.65%

2019: 2305/ 11500* 100 = 20.04%

(iii) Return on capital employed (ROCE): Earnings before interest and

tax/ Share equity + Long term liabilities * 100

2018: 2765/ 8755= 31.58%

2019: 2305/ 10211* 100 = 22.57%

(iv) Current ratio: Current assets/ Current liabilities

2018: 1175/ 970 = 1.211: 1

2019: 2110/ 512 = 4.12: 1

(v) Quick ratio: Current assets – Inventory / Current liabilities

2018: 1175 – 350/ 970 = 0.85: 1

2019: 2110 – 675/ 512 = 2.80: 1

(vi) Inventory turnover days: Cost of goods sold / average inventory

2018: 6500 / 350 = 13.57 times

2019: 8235 / 512 = 16.08 times

(vii) Debtor’s collection period: sales on credit / accounts receivable *

365

2018: 10000 / 760 * 365 = 27.74 days

2019: 11500 / 1340 * 365 = 42.54 days

(viii) Creditor’s collection period: cost of sales / trade payable * 365

2018: 6500 / 920 * 365 = 51.6 days

2019: 8235 / 707.5 * 365 = 31.36 days

(ii) Operating profit margin: Operating profit/ Net sales * 100

2018: 2765/ 10000* 100 = 27.65%

2019: 2305/ 11500* 100 = 20.04%

(iii) Return on capital employed (ROCE): Earnings before interest and

tax/ Share equity + Long term liabilities * 100

2018: 2765/ 8755= 31.58%

2019: 2305/ 10211* 100 = 22.57%

(iv) Current ratio: Current assets/ Current liabilities

2018: 1175/ 970 = 1.211: 1

2019: 2110/ 512 = 4.12: 1

(v) Quick ratio: Current assets – Inventory / Current liabilities

2018: 1175 – 350/ 970 = 0.85: 1

2019: 2110 – 675/ 512 = 2.80: 1

(vi) Inventory turnover days: Cost of goods sold / average inventory

2018: 6500 / 350 = 13.57 times

2019: 8235 / 512 = 16.08 times

(vii) Debtor’s collection period: sales on credit / accounts receivable *

365

2018: 10000 / 760 * 365 = 27.74 days

2019: 11500 / 1340 * 365 = 42.54 days

(viii) Creditor’s collection period: cost of sales / trade payable * 365

2018: 6500 / 920 * 365 = 51.6 days

2019: 8235 / 707.5 * 365 = 31.36 days

Part b: Individual analysis of each ratio based on the numerical results from

part a

(i) Gross profit margin

a. Gross profit is calculated by subtracting the cost of goods sold from the

revenue of the organisation.

b. What does the ratio indicate about the company’s performance: This

ratio states the profitability of the organisation after deduction the

expenses incurred by the organisation. This ratio is calculated by

dividing the gross profit by sales to determine the percentage of profits

earned by the organisation.

c. Compare 2018 figures with the 2019 figures calculated above: The

change in profits of the company is because of the decrease in the

gross profits and increase in the sales of the company. Increase in the

sales have reduced the profitability of the business. The profit margin

has reduced because production of extra unit have caused to increase

the cost of the operation of the company (Laletas, 2019).

d. Ways to improve the value of the ratio in the future: The company can

improve the ratio by decreasing their cost of operations taking

corrective measure to reduce the operations which incurs more costs.

Further the organisation can use its existing resources to optimise the

cost of production. These activities of the further needs to monitor for

the proper functioning of the management.

(ii) Operating profit margin

a. Operating profit determine the profit earned by the operating activity of

the management.

b. What does the ratio indicate about the company’s performance: This

ratio indicates the profits earned by the organization from operating

activity of the firm.

c. Reasons for changes in the ratio between 2018 and 2019: operating

profits of the organisation have reduced which have reduce the

profitability of the company.

d. Ways to improve the value of the ratio in the future: The business

needs to work upon its working and managing the cost of production to

increase the operating profit of the business. It helps in proper utilising

the available resources to its best use which makes it cost effective

(Mason, Narcum and Mason, 2020).

(iii) ROCE

a. this ratio helps in calculating the profit earned from the capital

employed in the business. It helps in knowing how much profits are

part a

(i) Gross profit margin

a. Gross profit is calculated by subtracting the cost of goods sold from the

revenue of the organisation.

b. What does the ratio indicate about the company’s performance: This

ratio states the profitability of the organisation after deduction the

expenses incurred by the organisation. This ratio is calculated by

dividing the gross profit by sales to determine the percentage of profits

earned by the organisation.

c. Compare 2018 figures with the 2019 figures calculated above: The

change in profits of the company is because of the decrease in the

gross profits and increase in the sales of the company. Increase in the

sales have reduced the profitability of the business. The profit margin

has reduced because production of extra unit have caused to increase

the cost of the operation of the company (Laletas, 2019).

d. Ways to improve the value of the ratio in the future: The company can

improve the ratio by decreasing their cost of operations taking

corrective measure to reduce the operations which incurs more costs.

Further the organisation can use its existing resources to optimise the

cost of production. These activities of the further needs to monitor for

the proper functioning of the management.

(ii) Operating profit margin

a. Operating profit determine the profit earned by the operating activity of

the management.

b. What does the ratio indicate about the company’s performance: This

ratio indicates the profits earned by the organization from operating

activity of the firm.

c. Reasons for changes in the ratio between 2018 and 2019: operating

profits of the organisation have reduced which have reduce the

profitability of the company.

d. Ways to improve the value of the ratio in the future: The business

needs to work upon its working and managing the cost of production to

increase the operating profit of the business. It helps in proper utilising

the available resources to its best use which makes it cost effective

(Mason, Narcum and Mason, 2020).

(iii) ROCE

a. this ratio helps in calculating the profit earned from the capital

employed in the business. It helps in knowing how much profits are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

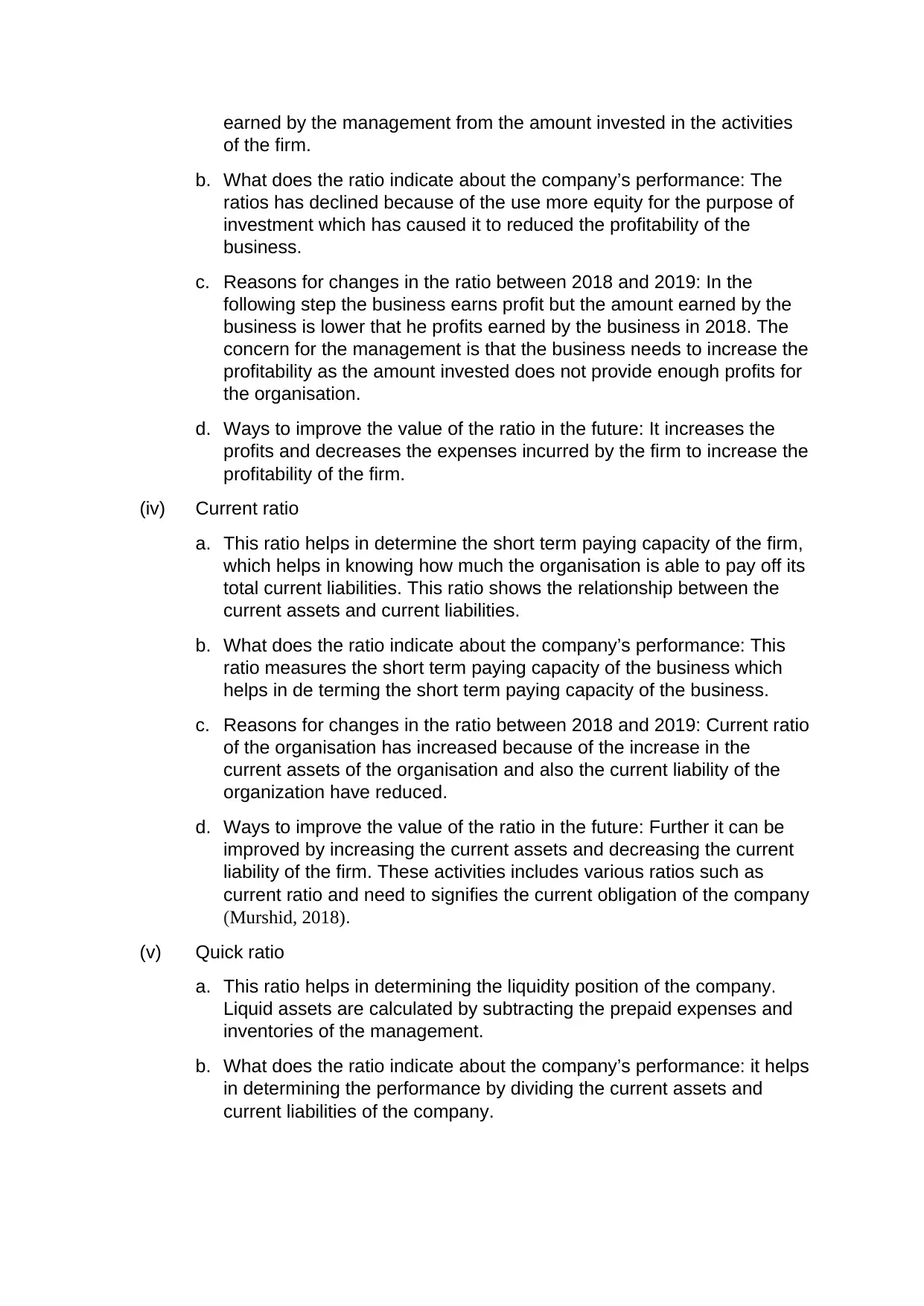

earned by the management from the amount invested in the activities

of the firm.

b. What does the ratio indicate about the company’s performance: The

ratios has declined because of the use more equity for the purpose of

investment which has caused it to reduced the profitability of the

business.

c. Reasons for changes in the ratio between 2018 and 2019: In the

following step the business earns profit but the amount earned by the

business is lower that he profits earned by the business in 2018. The

concern for the management is that the business needs to increase the

profitability as the amount invested does not provide enough profits for

the organisation.

d. Ways to improve the value of the ratio in the future: It increases the

profits and decreases the expenses incurred by the firm to increase the

profitability of the firm.

(iv) Current ratio

a. This ratio helps in determine the short term paying capacity of the firm,

which helps in knowing how much the organisation is able to pay off its

total current liabilities. This ratio shows the relationship between the

current assets and current liabilities.

b. What does the ratio indicate about the company’s performance: This

ratio measures the short term paying capacity of the business which

helps in de terming the short term paying capacity of the business.

c. Reasons for changes in the ratio between 2018 and 2019: Current ratio

of the organisation has increased because of the increase in the

current assets of the organisation and also the current liability of the

organization have reduced.

d. Ways to improve the value of the ratio in the future: Further it can be

improved by increasing the current assets and decreasing the current

liability of the firm. These activities includes various ratios such as

current ratio and need to signifies the current obligation of the company

(Murshid, 2018).

(v) Quick ratio

a. This ratio helps in determining the liquidity position of the company.

Liquid assets are calculated by subtracting the prepaid expenses and

inventories of the management.

b. What does the ratio indicate about the company’s performance: it helps

in determining the performance by dividing the current assets and

current liabilities of the company.

of the firm.

b. What does the ratio indicate about the company’s performance: The

ratios has declined because of the use more equity for the purpose of

investment which has caused it to reduced the profitability of the

business.

c. Reasons for changes in the ratio between 2018 and 2019: In the

following step the business earns profit but the amount earned by the

business is lower that he profits earned by the business in 2018. The

concern for the management is that the business needs to increase the

profitability as the amount invested does not provide enough profits for

the organisation.

d. Ways to improve the value of the ratio in the future: It increases the

profits and decreases the expenses incurred by the firm to increase the

profitability of the firm.

(iv) Current ratio

a. This ratio helps in determine the short term paying capacity of the firm,

which helps in knowing how much the organisation is able to pay off its

total current liabilities. This ratio shows the relationship between the

current assets and current liabilities.

b. What does the ratio indicate about the company’s performance: This

ratio measures the short term paying capacity of the business which

helps in de terming the short term paying capacity of the business.

c. Reasons for changes in the ratio between 2018 and 2019: Current ratio

of the organisation has increased because of the increase in the

current assets of the organisation and also the current liability of the

organization have reduced.

d. Ways to improve the value of the ratio in the future: Further it can be

improved by increasing the current assets and decreasing the current

liability of the firm. These activities includes various ratios such as

current ratio and need to signifies the current obligation of the company

(Murshid, 2018).

(v) Quick ratio

a. This ratio helps in determining the liquidity position of the company.

Liquid assets are calculated by subtracting the prepaid expenses and

inventories of the management.

b. What does the ratio indicate about the company’s performance: it helps

in determining the performance by dividing the current assets and

current liabilities of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

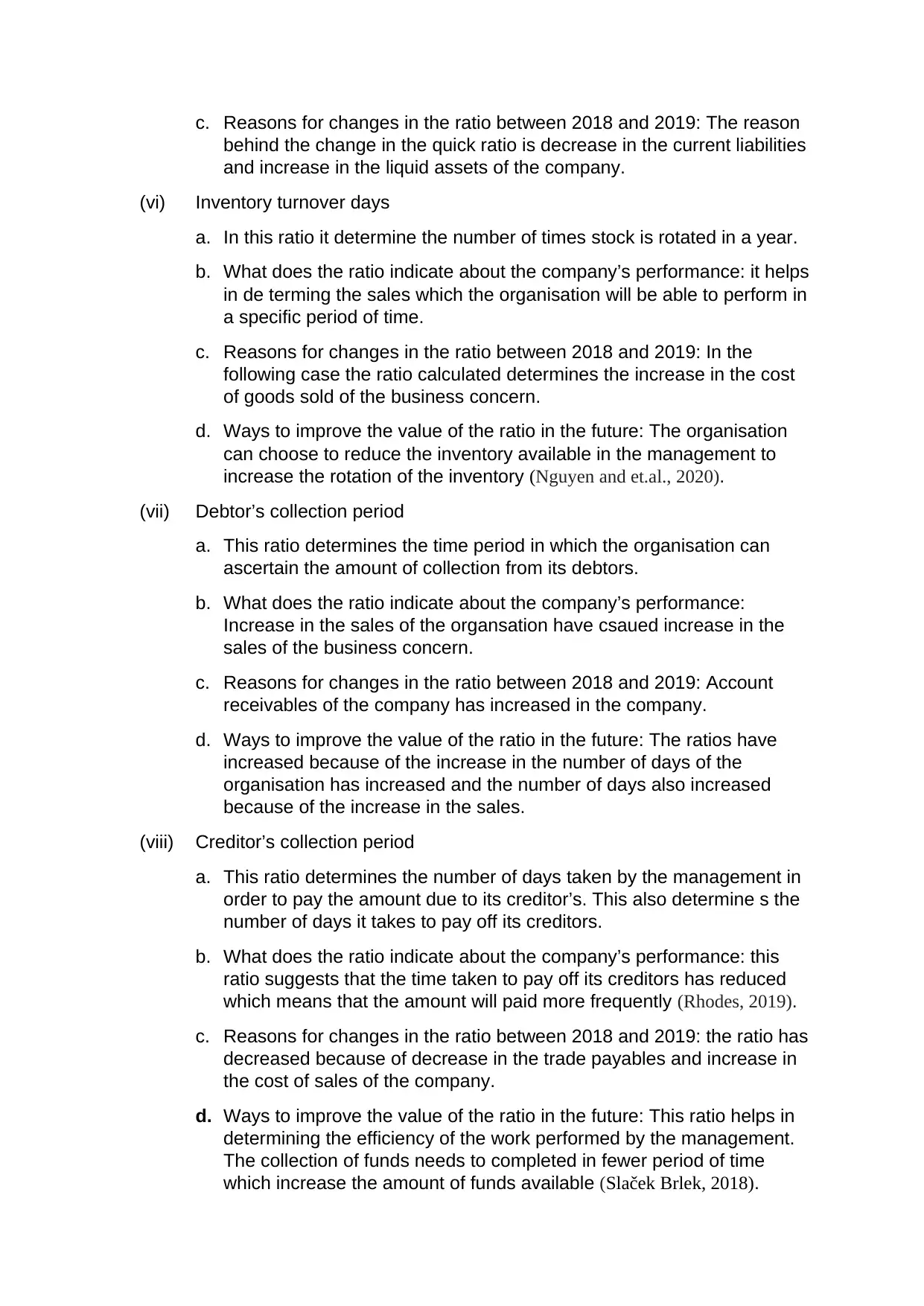

c. Reasons for changes in the ratio between 2018 and 2019: The reason

behind the change in the quick ratio is decrease in the current liabilities

and increase in the liquid assets of the company.

(vi) Inventory turnover days

a. In this ratio it determine the number of times stock is rotated in a year.

b. What does the ratio indicate about the company’s performance: it helps

in de terming the sales which the organisation will be able to perform in

a specific period of time.

c. Reasons for changes in the ratio between 2018 and 2019: In the

following case the ratio calculated determines the increase in the cost

of goods sold of the business concern.

d. Ways to improve the value of the ratio in the future: The organisation

can choose to reduce the inventory available in the management to

increase the rotation of the inventory (Nguyen and et.al., 2020).

(vii) Debtor’s collection period

a. This ratio determines the time period in which the organisation can

ascertain the amount of collection from its debtors.

b. What does the ratio indicate about the company’s performance:

Increase in the sales of the organsation have csaued increase in the

sales of the business concern.

c. Reasons for changes in the ratio between 2018 and 2019: Account

receivables of the company has increased in the company.

d. Ways to improve the value of the ratio in the future: The ratios have

increased because of the increase in the number of days of the

organisation has increased and the number of days also increased

because of the increase in the sales.

(viii) Creditor’s collection period

a. This ratio determines the number of days taken by the management in

order to pay the amount due to its creditor’s. This also determine s the

number of days it takes to pay off its creditors.

b. What does the ratio indicate about the company’s performance: this

ratio suggests that the time taken to pay off its creditors has reduced

which means that the amount will paid more frequently (Rhodes, 2019).

c. Reasons for changes in the ratio between 2018 and 2019: the ratio has

decreased because of decrease in the trade payables and increase in

the cost of sales of the company.

d. Ways to improve the value of the ratio in the future: This ratio helps in

determining the efficiency of the work performed by the management.

The collection of funds needs to completed in fewer period of time

which increase the amount of funds available (Slaček Brlek, 2018).

behind the change in the quick ratio is decrease in the current liabilities

and increase in the liquid assets of the company.

(vi) Inventory turnover days

a. In this ratio it determine the number of times stock is rotated in a year.

b. What does the ratio indicate about the company’s performance: it helps

in de terming the sales which the organisation will be able to perform in

a specific period of time.

c. Reasons for changes in the ratio between 2018 and 2019: In the

following case the ratio calculated determines the increase in the cost

of goods sold of the business concern.

d. Ways to improve the value of the ratio in the future: The organisation

can choose to reduce the inventory available in the management to

increase the rotation of the inventory (Nguyen and et.al., 2020).

(vii) Debtor’s collection period

a. This ratio determines the time period in which the organisation can

ascertain the amount of collection from its debtors.

b. What does the ratio indicate about the company’s performance:

Increase in the sales of the organsation have csaued increase in the

sales of the business concern.

c. Reasons for changes in the ratio between 2018 and 2019: Account

receivables of the company has increased in the company.

d. Ways to improve the value of the ratio in the future: The ratios have

increased because of the increase in the number of days of the

organisation has increased and the number of days also increased

because of the increase in the sales.

(viii) Creditor’s collection period

a. This ratio determines the number of days taken by the management in

order to pay the amount due to its creditor’s. This also determine s the

number of days it takes to pay off its creditors.

b. What does the ratio indicate about the company’s performance: this

ratio suggests that the time taken to pay off its creditors has reduced

which means that the amount will paid more frequently (Rhodes, 2019).

c. Reasons for changes in the ratio between 2018 and 2019: the ratio has

decreased because of decrease in the trade payables and increase in

the cost of sales of the company.

d. Ways to improve the value of the ratio in the future: This ratio helps in

determining the efficiency of the work performed by the management.

The collection of funds needs to completed in fewer period of time

which increase the amount of funds available (Slaček Brlek, 2018).

Conclusion

From the above report it can be concluded that Panini Ltd. Performance and

various functions which needs to analysed. It also suggests the areas where the

organisation needs to work upon. These functions help in future profitability of the

organisation in the long run. Further various ratios are premeditated to determine the

monetarist situation of the corporation and tries to maintain and enhance the

profitability of the business.

From the above report it can be concluded that Panini Ltd. Performance and

various functions which needs to analysed. It also suggests the areas where the

organisation needs to work upon. These functions help in future profitability of the

organisation in the long run. Further various ratios are premeditated to determine the

monetarist situation of the corporation and tries to maintain and enhance the

profitability of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference

Abu-Rahma, A. and Jaleel, B., 2019. Perceived uncertainty and use of environmental

information in decision making: The case of the United Arab

Emirates. International journal of organizational analysis.

Dilawar, S.M and et.al., 2021. Decision-making in highly stressful emergencies: The

interactive effects of trait emotional intelligence. Current Psychology, 40(6),

pp.2988-3005.

Dinçer, H., Yüksel, S. and Çetiner, İ.T., 2019. Strategy selection for organizational

performance of Turkish banking sector with the integrated multi-dimensional

decision-making approach. In Handbook of research on contemporary approaches

in management and organizational strategy (pp. 273-291). IGI Global.

Fu, C.H. and Chen, C.Y., 2021, May. A Study on Training Course for Staffs to Solve

Expertise Issues with Multiple Criteria Decision Making Methodology–a Case of

PC-based Information Security Monitoring Tool Development. In 2021 IEEE 3rd

Eurasia Conference on Biomedical Engineering, Healthcare and Sustainability

(ECBIOS) (pp. 134-137). IEEE.

Kayanda, A., Busagala, L. and Tedre, M., 2019, September. Design and implementation of

timetabling software for an improved decision making at the Tanzanian higher

education context: a design science approach. In 2019 IEEE AFRICON (pp. 1-4).

IEEE.

Laletas, S., 2019. Ethical decision making for professional school counsellors: Use of

practice-based models in secondary school settings. British Journal of Guidance &

Counselling, 47(3), pp.283-291.

Mason, A., Narcum, J. and Mason, K., 2020. Changes in consumer decision-making resulting

from the COVID-19 pandemic. Journal of Customer Behaviour, 19(4), pp.299-321.

Murshid, N.S., 2018. Microfinance participation and women's decision-making power in the

household in Bangladesh. Journal of Social Service Research, 44(3), pp.308-318.

Nguyen, T. and et.al., 2020, June. Investment Decision-Making for Transport Infrastructure

Projects: optimizing vs. Satisficing. In 2020 IEEE 15th International Conference of

System of Systems Engineering (SoSE) (pp. 41-46). IEEE.

Rhodes, E.M., 2019. Ethics Courses in Accounting Curriculum: A Qualitative Study of

Competencies, Judgement, and Decision-Making (Doctoral dissertation,

Northcentral University).

Slaček Brlek, A.S., 2018. Audience metrics as a decision-making factor in Slovene online

news organizations. In Technologies of Labour and the Politics of

Contradiction (pp. 211-232). Palgrave Macmillan, Cham.

Walker, K.L. and Moran, N., 2019. Consumer information for data-driven decision making:

Teaching socially responsible use of data. Journal of Marketing Education, 41(2),

pp.109-126.

Abu-Rahma, A. and Jaleel, B., 2019. Perceived uncertainty and use of environmental

information in decision making: The case of the United Arab

Emirates. International journal of organizational analysis.

Dilawar, S.M and et.al., 2021. Decision-making in highly stressful emergencies: The

interactive effects of trait emotional intelligence. Current Psychology, 40(6),

pp.2988-3005.

Dinçer, H., Yüksel, S. and Çetiner, İ.T., 2019. Strategy selection for organizational

performance of Turkish banking sector with the integrated multi-dimensional

decision-making approach. In Handbook of research on contemporary approaches

in management and organizational strategy (pp. 273-291). IGI Global.

Fu, C.H. and Chen, C.Y., 2021, May. A Study on Training Course for Staffs to Solve

Expertise Issues with Multiple Criteria Decision Making Methodology–a Case of

PC-based Information Security Monitoring Tool Development. In 2021 IEEE 3rd

Eurasia Conference on Biomedical Engineering, Healthcare and Sustainability

(ECBIOS) (pp. 134-137). IEEE.

Kayanda, A., Busagala, L. and Tedre, M., 2019, September. Design and implementation of

timetabling software for an improved decision making at the Tanzanian higher

education context: a design science approach. In 2019 IEEE AFRICON (pp. 1-4).

IEEE.

Laletas, S., 2019. Ethical decision making for professional school counsellors: Use of

practice-based models in secondary school settings. British Journal of Guidance &

Counselling, 47(3), pp.283-291.

Mason, A., Narcum, J. and Mason, K., 2020. Changes in consumer decision-making resulting

from the COVID-19 pandemic. Journal of Customer Behaviour, 19(4), pp.299-321.

Murshid, N.S., 2018. Microfinance participation and women's decision-making power in the

household in Bangladesh. Journal of Social Service Research, 44(3), pp.308-318.

Nguyen, T. and et.al., 2020, June. Investment Decision-Making for Transport Infrastructure

Projects: optimizing vs. Satisficing. In 2020 IEEE 15th International Conference of

System of Systems Engineering (SoSE) (pp. 41-46). IEEE.

Rhodes, E.M., 2019. Ethics Courses in Accounting Curriculum: A Qualitative Study of

Competencies, Judgement, and Decision-Making (Doctoral dissertation,

Northcentral University).

Slaček Brlek, A.S., 2018. Audience metrics as a decision-making factor in Slovene online

news organizations. In Technologies of Labour and the Politics of

Contradiction (pp. 211-232). Palgrave Macmillan, Cham.

Walker, K.L. and Moran, N., 2019. Consumer information for data-driven decision making:

Teaching socially responsible use of data. Journal of Marketing Education, 41(2),

pp.109-126.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.