Financial Decision Making Report: Accounting Techniques at Tesco

VerifiedAdded on 2023/01/12

|14

|4128

|31

Report

AI Summary

This report delves into the realm of financial decision-making, emphasizing the crucial role of management accounting techniques within organizations. Using Tesco as a case study, the report evaluates the application of techniques such as financial planning, budgetary control, margin analysis, and cash flow statement analysis in the context of organizational planning, control, and decision-making processes. It explores how these techniques facilitate effective management and contribute to achieving organizational objectives. The analysis includes an assessment of how these techniques can be strategically applied to enhance business practices, ultimately leading to improved financial outcomes and sustainable growth. The report also touches on the importance of skilled personnel for the successful implementation of these techniques. The report concludes by highlighting the significance of financial decision-making and management accounting techniques in driving organizational success.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

Role of management accounting techniques..........................................................................3

EVALUATION..........................................................................................................................5

CONCLUSION..........................................................................................................................6

REFERENCES...........................................................................................................................7

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

Role of management accounting techniques..........................................................................3

EVALUATION..........................................................................................................................5

CONCLUSION..........................................................................................................................6

REFERENCES...........................................................................................................................7

INTRODUCTION

Financial decision making is the process in which decisions are made with respect to the

managing finance of the business. Management accounting plays a key role in taking various financial

decisions of the business which are based on the information mainly available to the internal

management team. This information is not disclosed to outsiders. There are different roles of

accounting and finance which has great importance in the businesses. It does not have its own theory

but is borrowed from the other fields like economics and sociology. As per the agency theory, which

is a branch of finance economics whose main objective is to look into the conflicts between

shareholders and managers and works with the purpose to align goals in such a way that no conflict

arises (KOPP, 2019). Also, according to positive accounting theory, derived from contracting

literature in economics, which explains the consequences of interest of managers and financial

accounting and reporting (Kaya, 2017). It translates the predictions of real-world events into

accounting terms. In this, the firms can maximize their prospects for future survival by efficiently

organizing themselves. All this makes the role of accounting and finance very important and crucial.

In this report, Tesco is taken as an organization. It is the British multinational retailer,

headquartered in UK. It was founded in 1919. It has diversified its products into books, clothing,

furniture, software, financial services, internet services etc. Tesco has effectively implemented

management accounting techniques which helps it in effective management of its business (Palermo,

2017). The key management accounting techniques implemented by Tesco are capital budgeting,

margin analysis, cash flow statement analysis and financial planning. This report is about evaluating

the role of management accounting techniques in the process of organizational planning, controlling

and decision-making process. Also, critically evaluating how it can be applied for enhancing the

organization’s practices.

MAIN BODY

Role of management accounting techniques

There are different management accounting techniques that are used by the organizations with

the sole purpose to do effective planning, controlling and decision making (Nespeca and Chiucchi,

2018). It is very much required to analyse the various events and operational metrics for converting

data into useful information which can be used by the management for better decision making. Some

of the techniques are stated below.

Financial planning

Financial planning helps in determining the capital required for accomplishing the business

plan. It is the process in which a complete plan is formulated for achieving the required objective after

taking into consideration the market and competitor analysis, resources required and available both

Financial decision making is the process in which decisions are made with respect to the

managing finance of the business. Management accounting plays a key role in taking various financial

decisions of the business which are based on the information mainly available to the internal

management team. This information is not disclosed to outsiders. There are different roles of

accounting and finance which has great importance in the businesses. It does not have its own theory

but is borrowed from the other fields like economics and sociology. As per the agency theory, which

is a branch of finance economics whose main objective is to look into the conflicts between

shareholders and managers and works with the purpose to align goals in such a way that no conflict

arises (KOPP, 2019). Also, according to positive accounting theory, derived from contracting

literature in economics, which explains the consequences of interest of managers and financial

accounting and reporting (Kaya, 2017). It translates the predictions of real-world events into

accounting terms. In this, the firms can maximize their prospects for future survival by efficiently

organizing themselves. All this makes the role of accounting and finance very important and crucial.

In this report, Tesco is taken as an organization. It is the British multinational retailer,

headquartered in UK. It was founded in 1919. It has diversified its products into books, clothing,

furniture, software, financial services, internet services etc. Tesco has effectively implemented

management accounting techniques which helps it in effective management of its business (Palermo,

2017). The key management accounting techniques implemented by Tesco are capital budgeting,

margin analysis, cash flow statement analysis and financial planning. This report is about evaluating

the role of management accounting techniques in the process of organizational planning, controlling

and decision-making process. Also, critically evaluating how it can be applied for enhancing the

organization’s practices.

MAIN BODY

Role of management accounting techniques

There are different management accounting techniques that are used by the organizations with

the sole purpose to do effective planning, controlling and decision making (Nespeca and Chiucchi,

2018). It is very much required to analyse the various events and operational metrics for converting

data into useful information which can be used by the management for better decision making. Some

of the techniques are stated below.

Financial planning

Financial planning helps in determining the capital required for accomplishing the business

plan. It is the process in which a complete plan is formulated for achieving the required objective after

taking into consideration the market and competitor analysis, resources required and available both

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial and non-financial (Pradhan, Swain and Dash, 2018). This technique is implemented by

Tesco which helps in reducing the impact of uncertainty and also helps in ensuring stability and

profitability of the organization. The financial plan has the complete details about the different

sources of finance from where funds can be arranged for effective implementation of business plan for

achieving growth and success.

Budgetary control

This technique is mainly concerned with the all the relevant information which are required

for taking necessary decisions with respect to capital and revenue expenditure. It is the way to control

the organization where multiple budgets are made as per the requirement. Tesco uses budgetary

control which helps it in identifying its weak points so that correction actions can be taken

(Miyazhdenovna and et.al, 2020). It mostly uses variance analysis for managing its performance and

productivity. These budgets are prepared based on trend analysis and forecasting which helps

identifying the changing market trends based on which budgets are set.

Margin analysis

This analysis is mostly concerned with the additional or incremental benefits that is arising

from the increased production. This technique is the most essential in management accounting as it

analyses the complexities present in the system and tries to find a way to maximize profits ( Yassin

and Guindy, 2017). Tesco uses this technique because it includes break even point analysis and cost

volume profit which provides information which assist in taking better decisions. It is used as a profit

maximization tool which performs cost benefit analysis for every marginal change in the number of

products produced. It shows how an increment in production can impact the business operation.

Cash flow statement analysis

This technique is very helped for the business entities as it will indicate from where the cash

is generated and the application of it over a specific period. It is important for analysing the liquidity

and solvency position of the business. It is segmented into operating activities, investing activities and

financing activities (Golyagina and Valuckas, 2016). Tesco uses this as it helps it in identifying the

various sources of cash and also how much cash flow it is having from it operating activities which is

very important. This helps in knowing the cash flow position of the business in respect to the ability

of the business carry out its day to day business activities and meeting its short-term obligations.

Tesco which helps in reducing the impact of uncertainty and also helps in ensuring stability and

profitability of the organization. The financial plan has the complete details about the different

sources of finance from where funds can be arranged for effective implementation of business plan for

achieving growth and success.

Budgetary control

This technique is mainly concerned with the all the relevant information which are required

for taking necessary decisions with respect to capital and revenue expenditure. It is the way to control

the organization where multiple budgets are made as per the requirement. Tesco uses budgetary

control which helps it in identifying its weak points so that correction actions can be taken

(Miyazhdenovna and et.al, 2020). It mostly uses variance analysis for managing its performance and

productivity. These budgets are prepared based on trend analysis and forecasting which helps

identifying the changing market trends based on which budgets are set.

Margin analysis

This analysis is mostly concerned with the additional or incremental benefits that is arising

from the increased production. This technique is the most essential in management accounting as it

analyses the complexities present in the system and tries to find a way to maximize profits ( Yassin

and Guindy, 2017). Tesco uses this technique because it includes break even point analysis and cost

volume profit which provides information which assist in taking better decisions. It is used as a profit

maximization tool which performs cost benefit analysis for every marginal change in the number of

products produced. It shows how an increment in production can impact the business operation.

Cash flow statement analysis

This technique is very helped for the business entities as it will indicate from where the cash

is generated and the application of it over a specific period. It is important for analysing the liquidity

and solvency position of the business. It is segmented into operating activities, investing activities and

financing activities (Golyagina and Valuckas, 2016). Tesco uses this as it helps it in identifying the

various sources of cash and also how much cash flow it is having from it operating activities which is

very important. This helps in knowing the cash flow position of the business in respect to the ability

of the business carry out its day to day business activities and meeting its short-term obligations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All these techniques play an important role in organization’s planning, controlling and

decision-making process.

EVALUATION

Planning, controlling and decision making all these three are very important part of the

management process. All these together enables the employees to work towards achieving the

objectives of the organization (KÖSE and AĞDENİZ, 2019). Planning has an essential role in the

growth and sustainability of the entity which requires the manager to understand the current position

of the business and identify the areas of important. Tesco Group conducts an annual strategic planning

process which includes complete assessment of its objectives and evaluation of long-term

opportunities. The Chief Operating Decision Maker (CODM) monitors and evaluates the performance

based on which it takes decisions (Annual Report and Financial Statements. 2019). Management

accounting (MA) techniques is very significant as it provides important information based on the past

performance which play a critical role in planning process for the future performance. MA helps in

establishing the budget essential in planning. The Board of the company is the main decision taking

body and has taken into consideration financial performance and budgets, long term planning and

annual budget which has helped it in attaining its objectives. The margin analysis, financial planning

and budgetary controls are very effective in formulating plan, exercising control and taking better

decisions (Taylor, 2018). The company was able to effectively reach its gross operating margin of

3.45% in 2019. The cash flow analysis is also very useful in effective planning as it will provide

details about the cash available with the company to meet its daily requirement and also the minimum

cash it required to run the business smoothly for specific period. MA is also useful in control process

as based on the budgets prepared actual results are compared which helps in determining any

variances in the result. If there are any difference, the reason for the same is identified and relevant

and corrective actions are taken to reduce the variance. These techniques established certain control

parameters which warns the managers about the uncertain activities or events which were not earlier

included in the plan (TUOVILA, 2020). Identification of these events are critical in ensuring the

objective of the organization will be achieved or not.

Different MA techniques are used by the organization which helps in taking proper decisions

such as what should be sold, whether to invest in machinery or not. These techniques help in

determining the optimum activities required for effective production. It helps in gathering various

relevant information considering the different aspects of the business which helps in undertaking

proper evaluation based on which decision is taken. This decision is for the achieving the

organizational objectives as per the plan and within the budget set. It helps in growth and

sustainability of the business (El-Shishini, 2017). But, in order to execute and implement these

techniques requires highly skilled personnel having experience in planning, control and effective

decision making. Thus, it can be said that management accounting techniques have a very important

decision-making process.

EVALUATION

Planning, controlling and decision making all these three are very important part of the

management process. All these together enables the employees to work towards achieving the

objectives of the organization (KÖSE and AĞDENİZ, 2019). Planning has an essential role in the

growth and sustainability of the entity which requires the manager to understand the current position

of the business and identify the areas of important. Tesco Group conducts an annual strategic planning

process which includes complete assessment of its objectives and evaluation of long-term

opportunities. The Chief Operating Decision Maker (CODM) monitors and evaluates the performance

based on which it takes decisions (Annual Report and Financial Statements. 2019). Management

accounting (MA) techniques is very significant as it provides important information based on the past

performance which play a critical role in planning process for the future performance. MA helps in

establishing the budget essential in planning. The Board of the company is the main decision taking

body and has taken into consideration financial performance and budgets, long term planning and

annual budget which has helped it in attaining its objectives. The margin analysis, financial planning

and budgetary controls are very effective in formulating plan, exercising control and taking better

decisions (Taylor, 2018). The company was able to effectively reach its gross operating margin of

3.45% in 2019. The cash flow analysis is also very useful in effective planning as it will provide

details about the cash available with the company to meet its daily requirement and also the minimum

cash it required to run the business smoothly for specific period. MA is also useful in control process

as based on the budgets prepared actual results are compared which helps in determining any

variances in the result. If there are any difference, the reason for the same is identified and relevant

and corrective actions are taken to reduce the variance. These techniques established certain control

parameters which warns the managers about the uncertain activities or events which were not earlier

included in the plan (TUOVILA, 2020). Identification of these events are critical in ensuring the

objective of the organization will be achieved or not.

Different MA techniques are used by the organization which helps in taking proper decisions

such as what should be sold, whether to invest in machinery or not. These techniques help in

determining the optimum activities required for effective production. It helps in gathering various

relevant information considering the different aspects of the business which helps in undertaking

proper evaluation based on which decision is taken. This decision is for the achieving the

organizational objectives as per the plan and within the budget set. It helps in growth and

sustainability of the business (El-Shishini, 2017). But, in order to execute and implement these

techniques requires highly skilled personnel having experience in planning, control and effective

decision making. Thus, it can be said that management accounting techniques have a very important

and crucial role to play in for effectively managing the planning, controlling and decision making of

the organization.

These MA techniques can be effectively applied as per the business requirement like in Tesco

margin analysis, budgetary control, cashflow statement analysis are used. Margin analysis can eb

applied when the business is looking for expanding its business or introducing new product in the

market (Jarwal, 2018). Budgetary control can be used to achieve the estimated target based on the

market research and past performance. Cash flow statement analysis will be used for knowing the

liquidity position of the business and funds available to meet the short term needs before investing

into new project or plan. Thus, in this way it can be applied for enhancing the business practice.

CONCLUSION

From the above it can be concluded that management accounting techniques has an important

part to play in the business. It provides complete assistance to the organization in varied ways for

meeting the organizational needs. These techniques help in effective management of the business

activities with respect to the plan set up by the organization. These techniques have clearly shown the

role of account and finance in an organization. The benefits associated with financial planning,

budgetary control, margin analysis etc. is extremely high and can be effectively and actively used by

the businesses with further enhancing their practices. It can result into accomplishing the

organizational goals and objective in an efficient and rightly and reduces any loss that may arise

because of uncertainty. Thus, it can be said that financial decision making is the crucial part for very

organization as each and every aspect is required to be studied before taking any decision. For making

it right, the various management accounting techniques are developed which has an important role to

play in planning, controlling and in taking effective decisions. Therefore, financial decision making

along with management accounting techniques is very essential.

the organization.

These MA techniques can be effectively applied as per the business requirement like in Tesco

margin analysis, budgetary control, cashflow statement analysis are used. Margin analysis can eb

applied when the business is looking for expanding its business or introducing new product in the

market (Jarwal, 2018). Budgetary control can be used to achieve the estimated target based on the

market research and past performance. Cash flow statement analysis will be used for knowing the

liquidity position of the business and funds available to meet the short term needs before investing

into new project or plan. Thus, in this way it can be applied for enhancing the business practice.

CONCLUSION

From the above it can be concluded that management accounting techniques has an important

part to play in the business. It provides complete assistance to the organization in varied ways for

meeting the organizational needs. These techniques help in effective management of the business

activities with respect to the plan set up by the organization. These techniques have clearly shown the

role of account and finance in an organization. The benefits associated with financial planning,

budgetary control, margin analysis etc. is extremely high and can be effectively and actively used by

the businesses with further enhancing their practices. It can result into accomplishing the

organizational goals and objective in an efficient and rightly and reduces any loss that may arise

because of uncertainty. Thus, it can be said that financial decision making is the crucial part for very

organization as each and every aspect is required to be studied before taking any decision. For making

it right, the various management accounting techniques are developed which has an important role to

play in planning, controlling and in taking effective decisions. Therefore, financial decision making

along with management accounting techniques is very essential.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

El-Shishini, H. M., 2017. The use of management accounting techniques at hotels in Bahrain. Review

of Integrative Business and Economics Research. 6(2). p.78.

Golyagina, A. and Valuckas, D., 2016. Representation of knowledge on some management

accounting techniques in textbooks. Accounting Education. 25(5). pp.479-501.

Jarwal, C. S., 2018. Management Accounting: A Tool to Achieve Entrepreneurial Goals. IUP Journal

of Accounting Research & Audit Practices. 17(4).

KÖSE, T. and AĞDENİZ, Ş., 2019. The Role of Management Accounting in Risk

Management. Journal of Accounting & Finance.

Miyazhdenovna, N. and et.al, 2020. The role of management accounting techniques in determining

the relationship between purchasing and supplier management: A case study of retail firms in

Kazakhstan. Uncertain Supply Chain Management. 8(1). pp.149-164.

Nespeca, A. and Chiucchi, M. S., 2018. The impact of business intelligence systems on management

accounting systems: The consultant’s perspective. In Network, smart and open (pp. 283-297).

Springer, Cham.

Pradhan, D., Swain, P. K. and Dash, M., 2018. Effect of management accounting techniques on

supply chain and firm performance: An empirical study. International Journal of Mechanical

Engineering and Technology. 9(5). pp.1049-1057.

Yassin, M. and Guindy, M. E., 2017. Management Accounting Change and the Contemporary

Business Environment: An Article Review. Journal of Empirical Research in Accounting &

Auditing. 4(01). pp.7-22.

Kaya, İ., 2017. Accounting Choices in Corporate Financial Reporting: A Literature Review of

Positive Accounting Theory. Accounting and Corporate Reporting. p.129.

Palermo, T., 2017. Risk and performance management. The Routledge Companion to Accounting and

Risk, p.137.

Online

TUOVILA, A., 2020. Managerial Accounting. [Online]. Available Through:<

https://www.investopedia.com/terms/m/managerialaccounting.asp>. Thur. 30 Jan. 2020.

Taylor, J., 2018. Planning, Control and Decision making. [Online]. Available Through:<

https://www.essaytyping.com/planning-control-and-decision-making/>. Tue. 5 Nov. 2018.

KOPP, C., 2019. Agency Theory. [Online]. Available Through:<

https://www.investopedia.com/terms/a/agencytheory.asp>. Sat.18 April. 2019.

Annual Report and Financial Statements. 2019. [Online]. Available Through:<

https://www.tescoplc.com/media/476422/tesco_ara2019_full_report_web.pdf>. Sat. 23

Feb. 2019.

Books and Journals

El-Shishini, H. M., 2017. The use of management accounting techniques at hotels in Bahrain. Review

of Integrative Business and Economics Research. 6(2). p.78.

Golyagina, A. and Valuckas, D., 2016. Representation of knowledge on some management

accounting techniques in textbooks. Accounting Education. 25(5). pp.479-501.

Jarwal, C. S., 2018. Management Accounting: A Tool to Achieve Entrepreneurial Goals. IUP Journal

of Accounting Research & Audit Practices. 17(4).

KÖSE, T. and AĞDENİZ, Ş., 2019. The Role of Management Accounting in Risk

Management. Journal of Accounting & Finance.

Miyazhdenovna, N. and et.al, 2020. The role of management accounting techniques in determining

the relationship between purchasing and supplier management: A case study of retail firms in

Kazakhstan. Uncertain Supply Chain Management. 8(1). pp.149-164.

Nespeca, A. and Chiucchi, M. S., 2018. The impact of business intelligence systems on management

accounting systems: The consultant’s perspective. In Network, smart and open (pp. 283-297).

Springer, Cham.

Pradhan, D., Swain, P. K. and Dash, M., 2018. Effect of management accounting techniques on

supply chain and firm performance: An empirical study. International Journal of Mechanical

Engineering and Technology. 9(5). pp.1049-1057.

Yassin, M. and Guindy, M. E., 2017. Management Accounting Change and the Contemporary

Business Environment: An Article Review. Journal of Empirical Research in Accounting &

Auditing. 4(01). pp.7-22.

Kaya, İ., 2017. Accounting Choices in Corporate Financial Reporting: A Literature Review of

Positive Accounting Theory. Accounting and Corporate Reporting. p.129.

Palermo, T., 2017. Risk and performance management. The Routledge Companion to Accounting and

Risk, p.137.

Online

TUOVILA, A., 2020. Managerial Accounting. [Online]. Available Through:<

https://www.investopedia.com/terms/m/managerialaccounting.asp>. Thur. 30 Jan. 2020.

Taylor, J., 2018. Planning, Control and Decision making. [Online]. Available Through:<

https://www.essaytyping.com/planning-control-and-decision-making/>. Tue. 5 Nov. 2018.

KOPP, C., 2019. Agency Theory. [Online]. Available Through:<

https://www.investopedia.com/terms/a/agencytheory.asp>. Sat.18 April. 2019.

Annual Report and Financial Statements. 2019. [Online]. Available Through:<

https://www.tescoplc.com/media/476422/tesco_ara2019_full_report_web.pdf>. Sat. 23

Feb. 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION....................................................................................................................10

Calculation of ratios.............................................................................................................10

Performance of the ratios.....................................................................................................12

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION....................................................................................................................10

Calculation of ratios.............................................................................................................10

Performance of the ratios.....................................................................................................12

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

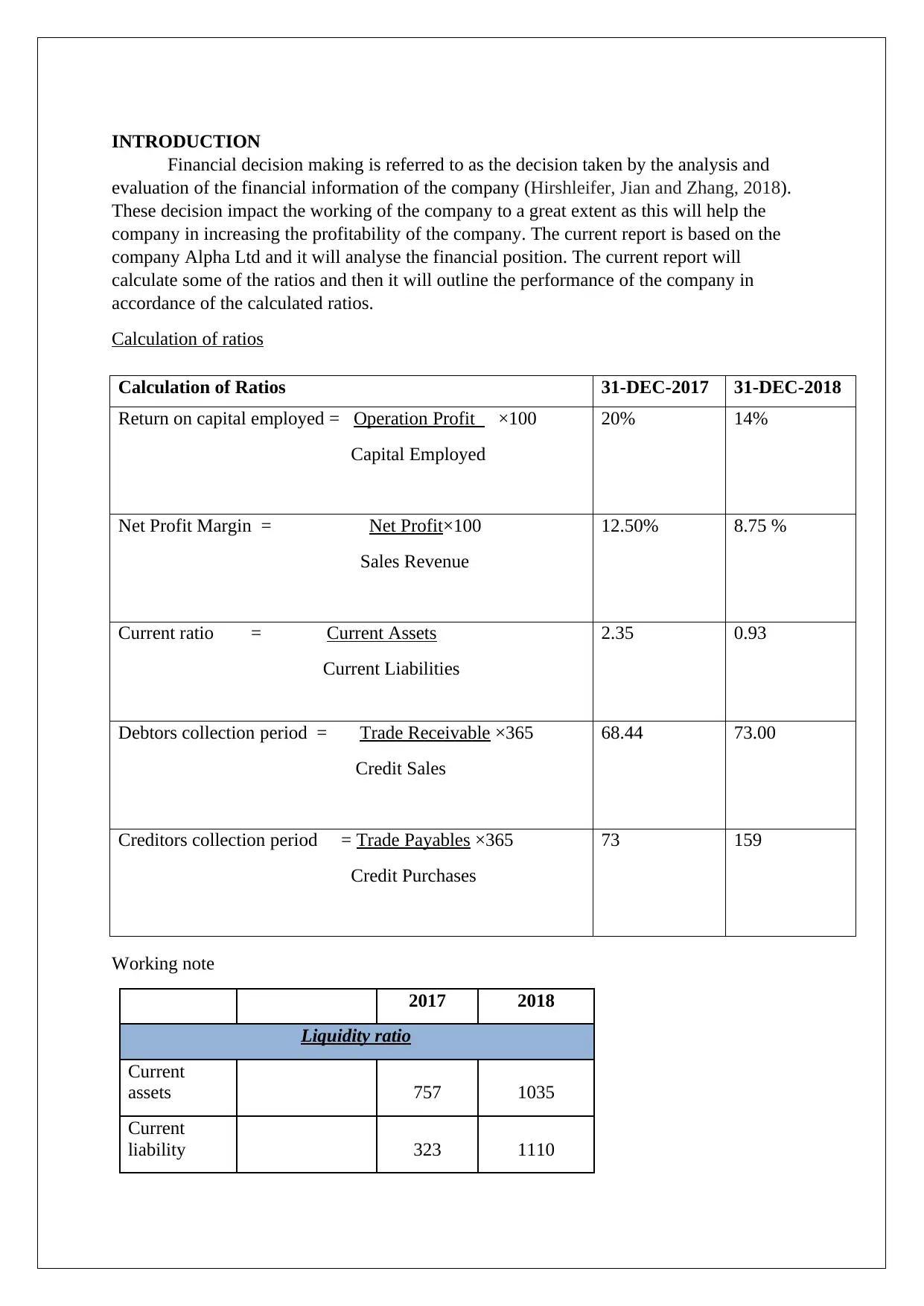

INTRODUCTION

Financial decision making is referred to as the decision taken by the analysis and

evaluation of the financial information of the company (Hirshleifer, Jian and Zhang, 2018).

These decision impact the working of the company to a great extent as this will help the

company in increasing the profitability of the company. The current report is based on the

company Alpha Ltd and it will analyse the financial position. The current report will

calculate some of the ratios and then it will outline the performance of the company in

accordance of the calculated ratios.

Calculation of ratios

Working note

2017 2018

Liquidity ratio

Current

assets 757 1035

Current

liability 323 1110

Calculation of Ratios 31-DEC-2017 31-DEC-2018

Return on capital employed = Operation Profit ×100

Capital Employed

20% 14%

Net Profit Margin = Net Profit×100

Sales Revenue

12.50% 8.75 %

Current ratio = Current Assets

Current Liabilities

2.35 0.93

Debtors collection period = Trade Receivable ×365

Credit Sales

68.44 73.00

Creditors collection period = Trade Payables ×365

Credit Purchases

73 159

Financial decision making is referred to as the decision taken by the analysis and

evaluation of the financial information of the company (Hirshleifer, Jian and Zhang, 2018).

These decision impact the working of the company to a great extent as this will help the

company in increasing the profitability of the company. The current report is based on the

company Alpha Ltd and it will analyse the financial position. The current report will

calculate some of the ratios and then it will outline the performance of the company in

accordance of the calculated ratios.

Calculation of ratios

Working note

2017 2018

Liquidity ratio

Current

assets 757 1035

Current

liability 323 1110

Calculation of Ratios 31-DEC-2017 31-DEC-2018

Return on capital employed = Operation Profit ×100

Capital Employed

20% 14%

Net Profit Margin = Net Profit×100

Sales Revenue

12.50% 8.75 %

Current ratio = Current Assets

Current Liabilities

2.35 0.93

Debtors collection period = Trade Receivable ×365

Credit Sales

68.44 73.00

Creditors collection period = Trade Payables ×365

Credit Purchases

73 159

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory 255 375

Quick Assets 502 660

Current

ratio

Current assets /

current

liabilities 2.35 0.93

Profitability ratio

Employed

Capital

(Total Assets -

Current

Liabilities) 1913 2925

Net profit 300 263

Return on

capital

employed

Net operating

profit/Employed

Capital 20% 14%

Net Income 300 263

Shareholder'

s Equity 1163 1425

Net profit 300 263

Sales 2400 3000

Net profit

ratio

Operating

Income/ Net

Sales 12.50% 8.75%

Efficiency Ratios

Trade

Payables 285 1050

Trade

Receivables 450 600

Net Assets 1163 1425

Cost of Sales 1725 2250

Sales 2400 3000

Accounts

Payable

Days

Sales /

Inventory *365 73 159

Quick Assets 502 660

Current

ratio

Current assets /

current

liabilities 2.35 0.93

Profitability ratio

Employed

Capital

(Total Assets -

Current

Liabilities) 1913 2925

Net profit 300 263

Return on

capital

employed

Net operating

profit/Employed

Capital 20% 14%

Net Income 300 263

Shareholder'

s Equity 1163 1425

Net profit 300 263

Sales 2400 3000

Net profit

ratio

Operating

Income/ Net

Sales 12.50% 8.75%

Efficiency Ratios

Trade

Payables 285 1050

Trade

Receivables 450 600

Net Assets 1163 1425

Cost of Sales 1725 2250

Sales 2400 3000

Accounts

Payable

Days

Sales /

Inventory *365 73 159

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Account

receivable

days

Sales /

Accounts

Receivable *

365 68.44 73.00

Performance of the ratios

Accounting ratios are the tools which are used by the company in order to compare

the financial data of one financial statement with that of the other (Lu, Won and Cheng,

2016). This comparison is done on the two different year’s data that is current year and the

previous year. This is an important tool which will help the company in comparing its

financial position and the deviation in the financial performance with the last year and to find

areas where the company need to make some improvement. This area of improvement need

to be found out because of the fact that if this will not be analysed then the company will not

be able to improve its financial position.

Return on capital employed

The return on capital employed or ROCE is a profitability ratio which is used by the

company in order to measure the fact that how efficiently the company is able to generate

profits from the capital which they have employed (Lieber and Skimmyhorn, 2018). This

ratio is very important to be calculated because this ratio helps the investor in comparing the

company and its performance with other competitors and then to decide in which company to

invest. This is because if the ROCE is high then it means that investors are getting more

income on the capital which they are investing in the company.

From the above calculation it is clear that ROCE need to be high because this states

that company gives a good return over the capital employed by the investors. In the year 2017

the ROCE was 20% but in 2018 this decreased to 14%. This means that the amount or profit

earned against the capital employed within the business has reduced. This suggest that

company need to increase its operation so that it can give higher return to investors.

Net profit margin

This is also an important profitability ratio which is referred to as percentage of

revenue which left after deducting of all the expenses have been deducted from the sales of

company. The net profit margin ratio is very important for the company because of the fact

that this helps the company in measuring overall success of the company. The higher profit

margin suggests that business is using right pricing strategies and this help company in

increasing high profit.

In case of Alpha Ltd and calculation of the net profit margin it was observed that the

profitability of the company in 2017 was good as the net profit ratio was 12.50%. But this

was not in case of 2018 as in this the profit margin reduced to 8.75% and this means that the

profit earning capacity of the company reduced by 3.75% and this is not a good position. This

states that company need to take measures in improving the sales of company and this can be

done with many different steps and measures.

Current ratio

receivable

days

Sales /

Accounts

Receivable *

365 68.44 73.00

Performance of the ratios

Accounting ratios are the tools which are used by the company in order to compare

the financial data of one financial statement with that of the other (Lu, Won and Cheng,

2016). This comparison is done on the two different year’s data that is current year and the

previous year. This is an important tool which will help the company in comparing its

financial position and the deviation in the financial performance with the last year and to find

areas where the company need to make some improvement. This area of improvement need

to be found out because of the fact that if this will not be analysed then the company will not

be able to improve its financial position.

Return on capital employed

The return on capital employed or ROCE is a profitability ratio which is used by the

company in order to measure the fact that how efficiently the company is able to generate

profits from the capital which they have employed (Lieber and Skimmyhorn, 2018). This

ratio is very important to be calculated because this ratio helps the investor in comparing the

company and its performance with other competitors and then to decide in which company to

invest. This is because if the ROCE is high then it means that investors are getting more

income on the capital which they are investing in the company.

From the above calculation it is clear that ROCE need to be high because this states

that company gives a good return over the capital employed by the investors. In the year 2017

the ROCE was 20% but in 2018 this decreased to 14%. This means that the amount or profit

earned against the capital employed within the business has reduced. This suggest that

company need to increase its operation so that it can give higher return to investors.

Net profit margin

This is also an important profitability ratio which is referred to as percentage of

revenue which left after deducting of all the expenses have been deducted from the sales of

company. The net profit margin ratio is very important for the company because of the fact

that this helps the company in measuring overall success of the company. The higher profit

margin suggests that business is using right pricing strategies and this help company in

increasing high profit.

In case of Alpha Ltd and calculation of the net profit margin it was observed that the

profitability of the company in 2017 was good as the net profit ratio was 12.50%. But this

was not in case of 2018 as in this the profit margin reduced to 8.75% and this means that the

profit earning capacity of the company reduced by 3.75% and this is not a good position. This

states that company need to take measures in improving the sales of company and this can be

done with many different steps and measures.

Current ratio

Current ratio is referred to as the liquidity ratio which is helpful for the company in

measuring the ability of the company to pay its current liabilities with the cash being made

from the current asset (Kim, Gutter and Spangler, 2017). The current ratio measurement is

important for the company because this outline the capacity of company to meet its short

term liabilities with the given current asset and cash for a period of financial year. This is

calculated by deducting the current liabilities from the current assets of the companies.

From the assessment and evaluation of the above calculation and its interpretation it is

clear that if the current ratio of the company is good then it means that company is in position

of paying of the current liabilities with their current asset only. This is in case of year 2017

wherein the current ratio is 2.35 this means that the current assets are 2.35 times more than

the current liabilities. On the contrary in the year 2018 the current ratio decreased to 0.93 and

this states that the company has only 0.93 times the current asset more than the current

liabilities. If the liabilities are more than the company had to take loans from other people to

pay off their current liabilities.

Average collection period/ debtor collection period

The average collection period is referred to as a ratio which is calculated as the

average of the balance of account receivable by the total credit sales for a period of financial

year. This is the most important ratio for the company who rely majorly on the credit sales

and the receivables (Valaskova, Bartosova and Kubala, 2019). The major importance of this

ratio for the company is that these ratios help the company in predicting the time in which the

company is able to recover all its payment.

At time of calculation and its interpretation it was seen that the debtor collection

period in 2017 was 68.44 but in 2018 it was 73.00. This data suggest that in the year 2017 the

speed of collecting the receivables was fast as compared to the period of 2018. But in the year

2018 it increased to 73 which means that the speed or the time taken in receiving the due

amount reduced by 4.56 times. Hence, the performance of Alpha ltd reduced as now the

company is able to recover its money at a slow pace. Also, it is suggested to the company that

as they are not able to recover the more amount so they must stop the credit sales. This is

because if credit sales will not be done then no money needs to be recovered by the company.

Average payable days/ creditors collection period

This is an efficiency ratio which helps the company in calculating the average

payment which the company has to do for all the credit purchases they have made during the

financial period (Greenberg and Hershfield, 2019). Also, known as creditor turnover ratio this

indicates the time involved during the credit sales which is make the current liabilities

outstanding fir the company and this need to be paid. This ratio is important as this indicates

the time when the company is able to pay off all its debts and is in pure liquid position.

With help of calculation of the average payable days it was seen that in 2017 this was

70 but in the year 2018 it was 159. This suggest that in the year 2017 it was good but in the

year 2018 it increased drastically which is not at all good for the company. Having this higher

collection period in 2018 suggest that the company is not able to pay off its current asset on

time and in proper manner that is full. Also, this higher number of creditor collection period

suggests that the company is not having proper communication with the consumer and

because of this the sales of company is reducing and for this the company need to take loans

measuring the ability of the company to pay its current liabilities with the cash being made

from the current asset (Kim, Gutter and Spangler, 2017). The current ratio measurement is

important for the company because this outline the capacity of company to meet its short

term liabilities with the given current asset and cash for a period of financial year. This is

calculated by deducting the current liabilities from the current assets of the companies.

From the assessment and evaluation of the above calculation and its interpretation it is

clear that if the current ratio of the company is good then it means that company is in position

of paying of the current liabilities with their current asset only. This is in case of year 2017

wherein the current ratio is 2.35 this means that the current assets are 2.35 times more than

the current liabilities. On the contrary in the year 2018 the current ratio decreased to 0.93 and

this states that the company has only 0.93 times the current asset more than the current

liabilities. If the liabilities are more than the company had to take loans from other people to

pay off their current liabilities.

Average collection period/ debtor collection period

The average collection period is referred to as a ratio which is calculated as the

average of the balance of account receivable by the total credit sales for a period of financial

year. This is the most important ratio for the company who rely majorly on the credit sales

and the receivables (Valaskova, Bartosova and Kubala, 2019). The major importance of this

ratio for the company is that these ratios help the company in predicting the time in which the

company is able to recover all its payment.

At time of calculation and its interpretation it was seen that the debtor collection

period in 2017 was 68.44 but in 2018 it was 73.00. This data suggest that in the year 2017 the

speed of collecting the receivables was fast as compared to the period of 2018. But in the year

2018 it increased to 73 which means that the speed or the time taken in receiving the due

amount reduced by 4.56 times. Hence, the performance of Alpha ltd reduced as now the

company is able to recover its money at a slow pace. Also, it is suggested to the company that

as they are not able to recover the more amount so they must stop the credit sales. This is

because if credit sales will not be done then no money needs to be recovered by the company.

Average payable days/ creditors collection period

This is an efficiency ratio which helps the company in calculating the average

payment which the company has to do for all the credit purchases they have made during the

financial period (Greenberg and Hershfield, 2019). Also, known as creditor turnover ratio this

indicates the time involved during the credit sales which is make the current liabilities

outstanding fir the company and this need to be paid. This ratio is important as this indicates

the time when the company is able to pay off all its debts and is in pure liquid position.

With help of calculation of the average payable days it was seen that in 2017 this was

70 but in the year 2018 it was 159. This suggest that in the year 2017 it was good but in the

year 2018 it increased drastically which is not at all good for the company. Having this higher

collection period in 2018 suggest that the company is not able to pay off its current asset on

time and in proper manner that is full. Also, this higher number of creditor collection period

suggests that the company is not having proper communication with the consumer and

because of this the sales of company is reducing and for this the company need to take loans

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.