Financial Analysis: Project Evaluation Using NPV and WACC Methods

VerifiedAdded on 2023/06/03

|3

|528

|440

Report

AI Summary

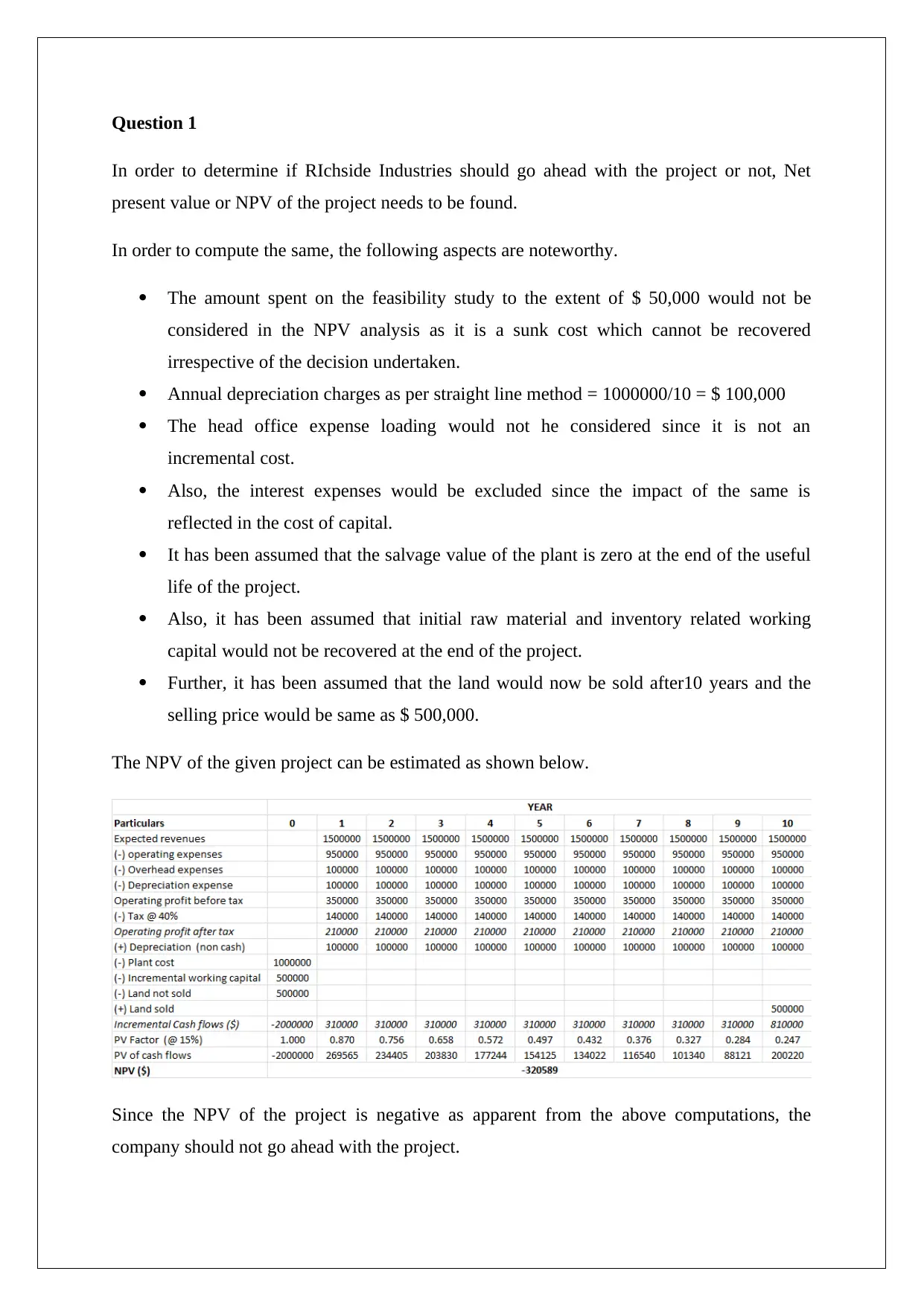

This report assesses whether Richside Industries should proceed with a plant extension project by calculating the Net Present Value (NPV). The analysis excludes sunk costs like the feasibility study expenses and non-incremental costs such as head office expense loading and interest expenses. It assumes a zero salvage value for the plant and no recovery of initial working capital. The NPV calculation incorporates annual revenues, operating expenses, depreciation, and tax implications, ultimately advising against the project due to a negative NPV. Furthermore, the report calculates the Weighted Average Cost of Capital (WACC) using the Capital Asset Pricing Model (CAPM) to determine the cost of equity and post-tax costs of debentures, also determining the pre-tax interest rate on a mortgage loan to reconcile with the given WACC. Desklib offers similar solved assignments and past papers for students.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.