Financial Decision Making: Ratio Analysis and Insights for Panini Ltd

VerifiedAdded on 2023/06/10

|10

|3380

|411

Case Study

AI Summary

This case study provides a detailed financial analysis of Panini Ltd, focusing on the roles and responsibilities of its accounting and finance departments. It begins by outlining the core functions of these departments, including financial accounting, management accounting, tax functions, auditing, investment, financing, dividend, and working capital management. The study also explores various internal and external sources of finance available to the company. A significant portion of the analysis involves calculating and interpreting financial ratios, such as gross profit margin, operating profit margin, and ROCE, to assess the company's financial health and performance. The analysis includes a comparison of financial data from 2018 and 2019, providing insights into the trends and potential areas for improvement. This assignment, contributed by a student and available on Desklib, offers a comprehensive overview of financial decision-making principles applied to a real-world case.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Contents

INTRODUCTION...............................................................................................................3

TASK..................................................................................................................................3

Identify the functions related to finance and accounting departments......................3

PART B..............................................................................................................................6

Calculate the ratios....................................................................................................6

CONCLUSION.................................................................................................................11

REFERENCES................................................................................................................12

1

Contents

INTRODUCTION...............................................................................................................3

TASK..................................................................................................................................3

Identify the functions related to finance and accounting departments......................3

PART B..............................................................................................................................6

Calculate the ratios....................................................................................................6

CONCLUSION.................................................................................................................11

REFERENCES................................................................................................................12

1

INTRODUCTION

The case study of Panini Ltd describes the duties and responsibility of accounting

and finance function with in the enterprise. It also explains the basic concept of

accounting and finance function of panini Ltd. Before discussing the duties and

responsibility it’s important to understand the main purpose of accounting and finance

function, it is the centre part of every company which are answerable for ensuring the

effective or productive financial management and control to support the all company

tasks. Afterwards it shows the duties and main responsibilities of accounting function is

Bills payable, receivables and report financial related activities apart from this the roles

and responsibilities of finance function is, to prepare financial strategy, to keep the

books of accounts and analysing the funds which are raised by the business. In other

instance it discusses some basic finance sources which includes internal and external

sources. Also. In other task it analyses some various kinds of financial ratios which

indicates the financial situation of the entity. In other part it provides some reason, show

the performance and give suggestion on the basis of the above calculated ratios.

MAIN BODY

TASK 1

Part a: Accounting and Finance functions

Accounting Function: The Accounting function of panini Ltd plays a very

important role in the financial management of the company. Basically, it

maintains the documents of the organization it mainly pays off by the firm and

check the overall expenditure of the company is paid or not in a particular period

of time (Ahmed, 2019). It includes some kind of accounting functions along with

its duties and responsibility of these functions within the organization that are

given below:

Financial accounting: The financial accounting of the company is very crucial to

keep the details of historic transactions of the entity along with this it also provide

an assistance to the auditor of analysing the documents of the enterprise. Apart

from all this it manages the reports of the company and record the daily tasks

and accounting transactions of the firm.

Management accounting: The management accounting of Panini Ltd assists

the managers to create its self-owned decisions into the company. Generally, it

assists the entity for analysing, describing, identifying and conveying the full data

leader. It mainly assists for accomplishing the goals and objectives of the

company. Along with this it usually provides an assistance to create and

forecasting the plan to implement in the projected task of the company (Amaning

and et.al., 2021).

Tax function: The tax accounting function is mainly useful to handle the tax

which involved risk but for some other reasons it involves strategies work,

forecast the problem and give data about the plan to the staff members of the

company. Also, it suggests about the financial transaction of the organization.

They required to show higher concentration on their limits of transactions, for

paying less taxes.

Auditing function: The auditing function of accounting department is usually

helps to identify the time duration, nature and the growth of audit process. In this

2

The case study of Panini Ltd describes the duties and responsibility of accounting

and finance function with in the enterprise. It also explains the basic concept of

accounting and finance function of panini Ltd. Before discussing the duties and

responsibility it’s important to understand the main purpose of accounting and finance

function, it is the centre part of every company which are answerable for ensuring the

effective or productive financial management and control to support the all company

tasks. Afterwards it shows the duties and main responsibilities of accounting function is

Bills payable, receivables and report financial related activities apart from this the roles

and responsibilities of finance function is, to prepare financial strategy, to keep the

books of accounts and analysing the funds which are raised by the business. In other

instance it discusses some basic finance sources which includes internal and external

sources. Also. In other task it analyses some various kinds of financial ratios which

indicates the financial situation of the entity. In other part it provides some reason, show

the performance and give suggestion on the basis of the above calculated ratios.

MAIN BODY

TASK 1

Part a: Accounting and Finance functions

Accounting Function: The Accounting function of panini Ltd plays a very

important role in the financial management of the company. Basically, it

maintains the documents of the organization it mainly pays off by the firm and

check the overall expenditure of the company is paid or not in a particular period

of time (Ahmed, 2019). It includes some kind of accounting functions along with

its duties and responsibility of these functions within the organization that are

given below:

Financial accounting: The financial accounting of the company is very crucial to

keep the details of historic transactions of the entity along with this it also provide

an assistance to the auditor of analysing the documents of the enterprise. Apart

from all this it manages the reports of the company and record the daily tasks

and accounting transactions of the firm.

Management accounting: The management accounting of Panini Ltd assists

the managers to create its self-owned decisions into the company. Generally, it

assists the entity for analysing, describing, identifying and conveying the full data

leader. It mainly assists for accomplishing the goals and objectives of the

company. Along with this it usually provides an assistance to create and

forecasting the plan to implement in the projected task of the company (Amaning

and et.al., 2021).

Tax function: The tax accounting function is mainly useful to handle the tax

which involved risk but for some other reasons it involves strategies work,

forecast the problem and give data about the plan to the staff members of the

company. Also, it suggests about the financial transaction of the organization.

They required to show higher concentration on their limits of transactions, for

paying less taxes.

Auditing function: The auditing function of accounting department is usually

helps to identify the time duration, nature and the growth of audit process. In this

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

scenario, it required to measure the accounting of the organization and examine

the proper structure of accounting, the auditor of the company required to ensure

the assets within the company. Apart from all this it determines the assets worth

and ensure the assets availability (Brockman and et.al., 2019).

Finance function: The finance function of panini Ltd create strategy to manage

the funds of the company and check that the organization can generate funds

through many ways. It also answerable for making the issues and it is usually

based upon the financial reports of the organization. It involves some various

kinds of finance function along with its duties and responsibility of these functions

within the entity that are given below:

Investment function: The main purpose of investment function is to indicate the

comparison between the worth of interest and the firm’s investment. They usually

invest its money in those technology who are newly introduced in the market and

useful for the society as well. This type of investment accomplishing success in

future for making high profit.

Financing function: This is one of the most important function of finance in which

it assists in sustaining and utilizing of financial funds for the impressive growth

and expansion of company’s activity. It also controls the strategy of financial

resources (Chen, Zhang and Nie, 2020).

Dividend function: The dividend function is usually assists to provide the profits in

a divided form to its company shareholders. In any year if organization generate

profit then firm distribute profit to its board members and partners of the

organization then it distributes in a form of dividend to its equity and preference

shareholders of the company.

Working capital function: The function of working capital helps to recover the

company short -term expenditures which are particularly due within a year. They

use cheaper source of finance for the expansion and development of the

organization. Every firm generates high profit in the organization so, they work

very efficiently and necessary to concentrate more in their operational activities

and reduce the expenses as well.

Part B: Sources of finance

Before starting any projected task, firm required to create funds for their daily

operational activities. They necessary to complete various types of expenditures it

involves bills payable, inventory and tools. In simple words it is the process in which

company creates resources for their business tasks (Chowdhury, Rahman and

Sankaran, 2021). Company can generate financing through internal and external path:

Internal finance source: The funds which generates from within the organization.

It involves some kinds of internal techniques which are given below:

personal savings: This type of savings helps the owners of the company to invest

the money in their business it creates funds for the company through the

personal savings of the entrepreneur. It mainly performs to fulfil the basic future

requirement of the company. If company perform the task of the organization and

due to the shortage of funds they face difficulty, then company owner can use

such type of savings to execute the task in the company.

Retained earnings: If company makes profit in their firm then it uses few or

completed funds in the organization and again invest to grow its money. This

3

the proper structure of accounting, the auditor of the company required to ensure

the assets within the company. Apart from all this it determines the assets worth

and ensure the assets availability (Brockman and et.al., 2019).

Finance function: The finance function of panini Ltd create strategy to manage

the funds of the company and check that the organization can generate funds

through many ways. It also answerable for making the issues and it is usually

based upon the financial reports of the organization. It involves some various

kinds of finance function along with its duties and responsibility of these functions

within the entity that are given below:

Investment function: The main purpose of investment function is to indicate the

comparison between the worth of interest and the firm’s investment. They usually

invest its money in those technology who are newly introduced in the market and

useful for the society as well. This type of investment accomplishing success in

future for making high profit.

Financing function: This is one of the most important function of finance in which

it assists in sustaining and utilizing of financial funds for the impressive growth

and expansion of company’s activity. It also controls the strategy of financial

resources (Chen, Zhang and Nie, 2020).

Dividend function: The dividend function is usually assists to provide the profits in

a divided form to its company shareholders. In any year if organization generate

profit then firm distribute profit to its board members and partners of the

organization then it distributes in a form of dividend to its equity and preference

shareholders of the company.

Working capital function: The function of working capital helps to recover the

company short -term expenditures which are particularly due within a year. They

use cheaper source of finance for the expansion and development of the

organization. Every firm generates high profit in the organization so, they work

very efficiently and necessary to concentrate more in their operational activities

and reduce the expenses as well.

Part B: Sources of finance

Before starting any projected task, firm required to create funds for their daily

operational activities. They necessary to complete various types of expenditures it

involves bills payable, inventory and tools. In simple words it is the process in which

company creates resources for their business tasks (Chowdhury, Rahman and

Sankaran, 2021). Company can generate financing through internal and external path:

Internal finance source: The funds which generates from within the organization.

It involves some kinds of internal techniques which are given below:

personal savings: This type of savings helps the owners of the company to invest

the money in their business it creates funds for the company through the

personal savings of the entrepreneur. It mainly performs to fulfil the basic future

requirement of the company. If company perform the task of the organization and

due to the shortage of funds they face difficulty, then company owner can use

such type of savings to execute the task in the company.

Retained earnings: If company makes profit in their firm then it uses few or

completed funds in the organization and again invest to grow its money. This

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

source of finance does not involve interest charges or needed the dividend

payment. Which can make it a useful source of finance (Endrawes and et.al.,

2020).

Selling off assets: It involves selling of goods and services which are owned by

the firm. It mainly useful for the firm when it’s not highly utilize the products or it

needed to create funds speedily. Assets of the firm which can be sold like, tools,

inventories and machinery.

External finance source: It involves those funds which generate from outside the

business. There are some external techniques which are given below:

loan from commercial bank: If company wants to generate funds in their business

then they can apply for the loan in commercial bank to perform the operational

activity of the company. But the banks provide the loan against some property or

assets of the firm which are required to be considered as a same value of loan

amount. If company fail to pay its loan, then it recovers through the assets of the

firm.

Relatives and friends: It is an another source of finance which create funds in the

company through borrow money to friends and family members for the

investment reason in the organization. This borrowed money not required to be

repaid or paid with low or no charge of interest (Endrawes and et.al., 2020).

By issuing equity shares: If company wants to generate funds in the organization

then they have some source of finance to create funds in their business by

issuing equity shares in the public. If the company is reputed and earn profit in

last few years then more individual show their interest in the shares of the

company and buy the shares of the organization and it will automatically

maximise the funds of the entity and assists the organization to achieve their

targets and objectives.

TASK 2

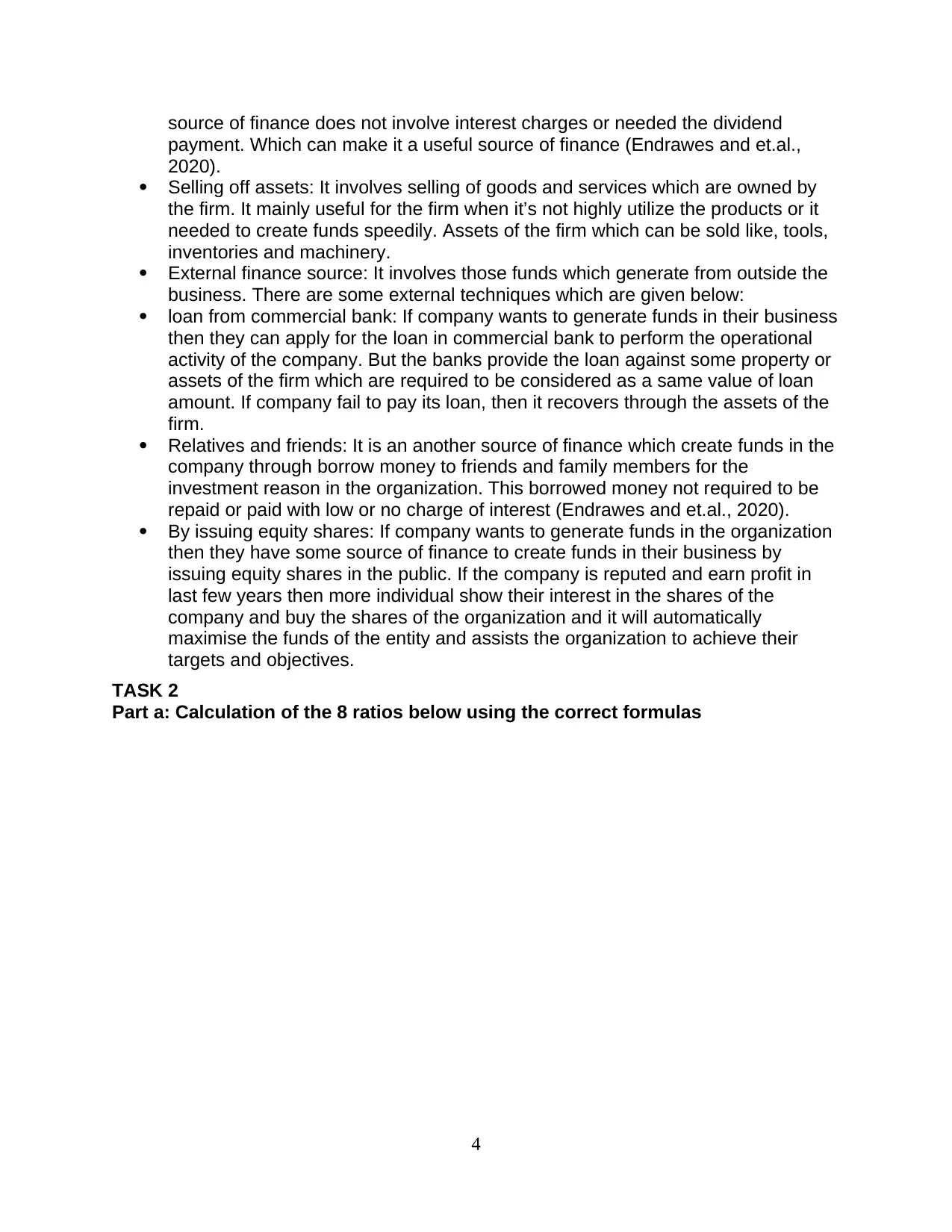

Part a: Calculation of the 8 ratios below using the correct formulas

4

payment. Which can make it a useful source of finance (Endrawes and et.al.,

2020).

Selling off assets: It involves selling of goods and services which are owned by

the firm. It mainly useful for the firm when it’s not highly utilize the products or it

needed to create funds speedily. Assets of the firm which can be sold like, tools,

inventories and machinery.

External finance source: It involves those funds which generate from outside the

business. There are some external techniques which are given below:

loan from commercial bank: If company wants to generate funds in their business

then they can apply for the loan in commercial bank to perform the operational

activity of the company. But the banks provide the loan against some property or

assets of the firm which are required to be considered as a same value of loan

amount. If company fail to pay its loan, then it recovers through the assets of the

firm.

Relatives and friends: It is an another source of finance which create funds in the

company through borrow money to friends and family members for the

investment reason in the organization. This borrowed money not required to be

repaid or paid with low or no charge of interest (Endrawes and et.al., 2020).

By issuing equity shares: If company wants to generate funds in the organization

then they have some source of finance to create funds in their business by

issuing equity shares in the public. If the company is reputed and earn profit in

last few years then more individual show their interest in the shares of the

company and buy the shares of the organization and it will automatically

maximise the funds of the entity and assists the organization to achieve their

targets and objectives.

TASK 2

Part a: Calculation of the 8 ratios below using the correct formulas

4

Part b: Individual analysis of each ratio based on the numerical results from part

a

For this part, you should provide the below points for each of the 8 above ratios. Each

ratio analysis should be presented in a single paragraph (total: 8 paragraphs)

(i) Gross profit margin

a. This is the income determined after deducting the association's labor and

sales and assembly costs of the product.

b. b. The scale tells how well the organization exhibits: The scale accounts

for the productivity of the organization, which is determined after deducting

costs incurred in functional exercises. This ratio is determined by

separating net earnings from the business' transactions.

c. C. Contrast the 2018 data with the data determined in 2019: the

5

a

For this part, you should provide the below points for each of the 8 above ratios. Each

ratio analysis should be presented in a single paragraph (total: 8 paragraphs)

(i) Gross profit margin

a. This is the income determined after deducting the association's labor and

sales and assembly costs of the product.

b. b. The scale tells how well the organization exhibits: The scale accounts

for the productivity of the organization, which is determined after deducting

costs incurred in functional exercises. This ratio is determined by

separating net earnings from the business' transactions.

c. C. Contrast the 2018 data with the data determined in 2019: the

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

interpretation of the 2019 scale adjustment is the result of the institutional

exhibition adjustment. The organization's net benefit decreased by more

than 6% in one year due to the expansion of costs due to administration,

while the proportion of transactions expanded relatively less, and the

resulting expansion of expenses.

d. d. How Proportional Value works from now on: Organizations need to cut

expenses that result in costs and organizational costs. The walkthrough

must be confirmed by the association in order to get to know the real

exhibition of the organization. Associations need to use more liquid assets

and reduce waste from time spent assembling merchandise (Endrawes

and et.al., 2020).

(ii) Operating profit margin

a. This income ratio reflects the associations brought about by the work

activities of the enterprise.

b. b. What the ratio says about the organization's presentation: This ratio

helps determine the organization's exhibition: This ratio helps to decide

based on the execution of the business and the overall progress of the

business.

c. C. Reason for the change in the proportion from 2018 to 2019: The reason

for the adjustment in 2019 is that the proficiency brought by the

organization in the work is not high, and it can continue to develop further

in 2018.

d. d. The Work Scale Approach From Now: In 2019, businesses need to

reduce the cost of work to build the benefits of the organization. It

facilitates the legitimate use of an organization's accessible resources by

saving additional costs incurred during the assembly process (Khoruzhy

and et.al., 2021).

(iii) ROCE

a. This ratio helps in deciding to purchase from the funds that the business

uses in its business mission. It helps to create the interests of the

organization and break down the areas where the interests are identified.

b. b. What is the proportion of the organization's exhibitions: As can be seen

from the above definition, the organization is reaping key benefits from its

mission and generating enough revenue to understand the productivity of

the association.

c. C. Reason for the change somewhere in the 2018 and 2019 ranges: In

this process, the time of year a business earns depends on the rate of

return on capital used. How much income is generated by the capital

employed by the business. Businesses made gains in 2018 and almost

none in 2019, reducing overall business productivity.

d. d. The way to increase the proportional value from now on: it further

6

exhibition adjustment. The organization's net benefit decreased by more

than 6% in one year due to the expansion of costs due to administration,

while the proportion of transactions expanded relatively less, and the

resulting expansion of expenses.

d. d. How Proportional Value works from now on: Organizations need to cut

expenses that result in costs and organizational costs. The walkthrough

must be confirmed by the association in order to get to know the real

exhibition of the organization. Associations need to use more liquid assets

and reduce waste from time spent assembling merchandise (Endrawes

and et.al., 2020).

(ii) Operating profit margin

a. This income ratio reflects the associations brought about by the work

activities of the enterprise.

b. b. What the ratio says about the organization's presentation: This ratio

helps determine the organization's exhibition: This ratio helps to decide

based on the execution of the business and the overall progress of the

business.

c. C. Reason for the change in the proportion from 2018 to 2019: The reason

for the adjustment in 2019 is that the proficiency brought by the

organization in the work is not high, and it can continue to develop further

in 2018.

d. d. The Work Scale Approach From Now: In 2019, businesses need to

reduce the cost of work to build the benefits of the organization. It

facilitates the legitimate use of an organization's accessible resources by

saving additional costs incurred during the assembly process (Khoruzhy

and et.al., 2021).

(iii) ROCE

a. This ratio helps in deciding to purchase from the funds that the business

uses in its business mission. It helps to create the interests of the

organization and break down the areas where the interests are identified.

b. b. What is the proportion of the organization's exhibitions: As can be seen

from the above definition, the organization is reaping key benefits from its

mission and generating enough revenue to understand the productivity of

the association.

c. C. Reason for the change somewhere in the 2018 and 2019 ranges: In

this process, the time of year a business earns depends on the rate of

return on capital used. How much income is generated by the capital

employed by the business. Businesses made gains in 2018 and almost

none in 2019, reducing overall business productivity.

d. d. The way to increase the proportional value from now on: it further

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expands the benefits and reduces the cost of doing business that helps

increase the company's productivity. This equation takes advantage of

interest and assesses prior interest.

(iv) Current ratio

a. This ratio helps determine the liquidity of the business. This proportion

mainly includes the continuing resources and current liabilities of the

enterprise and the temporary liabilities of the enterprise. This ratio reflects

the relationship between ongoing liabilities and current resources.

b. b. What the scale shows for the organization's exhibition: This scale

estimates the organization's momentary presentation, which contains

fleeting responsibilities and fleeting resources. This ratio shows the

connection between an organization's ongoing resources and current

commitments.

c. C. Reasons for the change in the proportions in 2018-2019: Explanation of

the continuous proportion adjustment, worrying that the responsibility will

expand with the expansion of continuous resources and current liabilities.

d. d. Approach to dealing with proportional value from now on: This ratio

helps the association determine the firm's tentative commitment and

current resources. These exercises also include those of the current

proportions that are required to further develop the ongoing liquidity

situation of the business (Lu and et.al., 2022).

(v) Quick ratio

a. One. This ratio helps determine the true liquidity of the business, which is

determined by deducting the organization's inventory and prepayments.

b. b. How does the ratio affect the organization's exhibitions: This ratio helps

determine the execution of the business by separating ongoing resources

and current liabilities.

c. C. Reasons for the change in the proportion of a certain place from 2018

to 2019: Due to the high organizational obligations, the purpose of

adjusting the proportion quickly.

(vi) Inventory turnover days

a. One. This ratio determines the amount of time the stock is replaced over

the entire time frame.

b. b. What does scale do to an organization's presentation: It helps

determine an organization's presentation by knowing the amount of time

an organization can turn around inventory.

c. C. Reason for the change in the proportion of a certain place from 2018 to

2019: The bylaw adjusted the proportion due to the expansion of the

agency's cost of selling goods.

d. d. How Proportional Values Work from Now: Associations may additionally

reduce typical stocks to amplify the revolution in stock turnover.

(vii) Debtor’s collection period

7

increase the company's productivity. This equation takes advantage of

interest and assesses prior interest.

(iv) Current ratio

a. This ratio helps determine the liquidity of the business. This proportion

mainly includes the continuing resources and current liabilities of the

enterprise and the temporary liabilities of the enterprise. This ratio reflects

the relationship between ongoing liabilities and current resources.

b. b. What the scale shows for the organization's exhibition: This scale

estimates the organization's momentary presentation, which contains

fleeting responsibilities and fleeting resources. This ratio shows the

connection between an organization's ongoing resources and current

commitments.

c. C. Reasons for the change in the proportions in 2018-2019: Explanation of

the continuous proportion adjustment, worrying that the responsibility will

expand with the expansion of continuous resources and current liabilities.

d. d. Approach to dealing with proportional value from now on: This ratio

helps the association determine the firm's tentative commitment and

current resources. These exercises also include those of the current

proportions that are required to further develop the ongoing liquidity

situation of the business (Lu and et.al., 2022).

(v) Quick ratio

a. One. This ratio helps determine the true liquidity of the business, which is

determined by deducting the organization's inventory and prepayments.

b. b. How does the ratio affect the organization's exhibitions: This ratio helps

determine the execution of the business by separating ongoing resources

and current liabilities.

c. C. Reasons for the change in the proportion of a certain place from 2018

to 2019: Due to the high organizational obligations, the purpose of

adjusting the proportion quickly.

(vi) Inventory turnover days

a. One. This ratio determines the amount of time the stock is replaced over

the entire time frame.

b. b. What does scale do to an organization's presentation: It helps

determine an organization's presentation by knowing the amount of time

an organization can turn around inventory.

c. C. Reason for the change in the proportion of a certain place from 2018 to

2019: The bylaw adjusted the proportion due to the expansion of the

agency's cost of selling goods.

d. d. How Proportional Values Work from Now: Associations may additionally

reduce typical stocks to amplify the revolution in stock turnover.

(vii) Debtor’s collection period

7

a. The time span to determine the time span to understand the borrower's

expected time span for the classification.

b. b. Explanation of the proportion of institutions participating in the

exhibition: The trading volume of the association has expanded, and the

number of days for institutions to collect payments has also increased.

c. C. Reasons for the change in the proportion from 2018 to 2019: With the

increase of institutional accounts receivable, institutional accounts

receivable decreased.

d. d. How the value of the ratio works from now on: The ratio changes

because the result of the adjustment expands the number of days in which

the executive is advised to recover the amount due to an increase in

borrowers.

(viii) Creditor’s collection period

a. The time span over which management decides the amount determines

the time span over which the organization makes payments to account

holders.

b. b. The ratio indicates how well the organization is exhibiting: The ratio

indicates that the organization will receive a bit longer than last year from

account holders.

c. C. Reasons for the change in the ratio from 2018 to 2019: the decrease in

foreign exchange payable and the increase in organizational transaction

costs.

d. d. How to calculate proportional value from now on: This ratio helps

determine the productivity of a job. The classification of proficiency and

low level shows the effectiveness of the business.

CONCLUSION

From the above report it can be inferred that Panini Ltd and different business

capabilities and execution have collapsed. In the long run, these capabilities contribute

to the future productivity of businesses and businesses. It also helps to suggest areas

where the government can use its resources and assets to make more purchases. A

further different ratio was determined to determine the presentation of the organization

as soon as possible rather than late, in addition to the engaging view of the business.

8

expected time span for the classification.

b. b. Explanation of the proportion of institutions participating in the

exhibition: The trading volume of the association has expanded, and the

number of days for institutions to collect payments has also increased.

c. C. Reasons for the change in the proportion from 2018 to 2019: With the

increase of institutional accounts receivable, institutional accounts

receivable decreased.

d. d. How the value of the ratio works from now on: The ratio changes

because the result of the adjustment expands the number of days in which

the executive is advised to recover the amount due to an increase in

borrowers.

(viii) Creditor’s collection period

a. The time span over which management decides the amount determines

the time span over which the organization makes payments to account

holders.

b. b. The ratio indicates how well the organization is exhibiting: The ratio

indicates that the organization will receive a bit longer than last year from

account holders.

c. C. Reasons for the change in the ratio from 2018 to 2019: the decrease in

foreign exchange payable and the increase in organizational transaction

costs.

d. d. How to calculate proportional value from now on: This ratio helps

determine the productivity of a job. The classification of proficiency and

low level shows the effectiveness of the business.

CONCLUSION

From the above report it can be inferred that Panini Ltd and different business

capabilities and execution have collapsed. In the long run, these capabilities contribute

to the future productivity of businesses and businesses. It also helps to suggest areas

where the government can use its resources and assets to make more purchases. A

further different ratio was determined to determine the presentation of the organization

as soon as possible rather than late, in addition to the engaging view of the business.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abdulkarim, M.E., Umlai, M.I. and Al-Saudi, L.F., 2020. Exploring the role of innovation

in the level of readiness to adopt IPSAS. Journal of Accounting &

Organizational Change.

Ahmed, H.O., 2019. Perception of Practitioners on Forensic Accounting as a Tool for

Fraud Detection and Prevention (Doctoral dissertation, Kwara State University

(Nigeria)).

Amaning, N and et.al., 2021. Qualitative analysis on accounting ethics education for

bachelor students. International Journal of Critical Accounting. 12(2). pp.156-

177.

Brockman, P and et.al., 2019. CEO internal experience and voluntary disclosure quality:

Evidence from management forecasts. Journal of Business Finance &

Accounting. 46(3-4). pp.420-456.

Chen, L., Zhang, X. and Nie, D., 2020. Who contributes to a firm's long-term

performance, major institutional investors or the CEO?. International Journal of

Accounting and Finance. 10(4). pp.212-232.

Chowdhury, H., Rahman, S. and Sankaran, H., 2021. Leverage deviation from the

target debt ratio and leasing. Accounting & Finance. 61(2). pp.3481-3515.

Endrawes, M and et.al., 2020. Audit committee characteristics and financial statement

comparability. Accounting & Finance. 60(3). pp.2361-2395.

Khoruzhy, L.I and et.al., 2021, December. Reporting system in the adaptive accounting

and analytical system of providing inter-organizational collaboration of AIC

organizations. In AIP Conference Proceedings (Vol. 2442, No. 1, p. 020014).

AIP Publishing LLC.

Lu, J and et.al., 2022. Financial controller turnover: An early warning sign of

deteriorating financial reporting quality. Accounting & Finance.

Obenpong Kwabi, F and et.al., 2022. Economic policy uncertainty and cost of capital:

the mediating effects of foreign equity portfolio flow. Review of Quantitative

Finance and Accounting, pp.1-25.

Storozhuk, T. and Blyshchyk, L., 2019. Interpretation of the" Financial Reporting"

Definition. Oblik i finansi. (4). pp.54-62.

Xu, C and et.al., 2021. Real earnings management in bankrupt firms. Journal of

Corporate Accounting & Finance. 32(2). pp.22-38.

Yi, Z and et.al., 2018. The impact of consumer fairness seeking on distribution channel

selection: Direct selling vs. agent selling. Production and Operations

Management. 27(6). pp.1148-1167.

9

Books and Journals

Abdulkarim, M.E., Umlai, M.I. and Al-Saudi, L.F., 2020. Exploring the role of innovation

in the level of readiness to adopt IPSAS. Journal of Accounting &

Organizational Change.

Ahmed, H.O., 2019. Perception of Practitioners on Forensic Accounting as a Tool for

Fraud Detection and Prevention (Doctoral dissertation, Kwara State University

(Nigeria)).

Amaning, N and et.al., 2021. Qualitative analysis on accounting ethics education for

bachelor students. International Journal of Critical Accounting. 12(2). pp.156-

177.

Brockman, P and et.al., 2019. CEO internal experience and voluntary disclosure quality:

Evidence from management forecasts. Journal of Business Finance &

Accounting. 46(3-4). pp.420-456.

Chen, L., Zhang, X. and Nie, D., 2020. Who contributes to a firm's long-term

performance, major institutional investors or the CEO?. International Journal of

Accounting and Finance. 10(4). pp.212-232.

Chowdhury, H., Rahman, S. and Sankaran, H., 2021. Leverage deviation from the

target debt ratio and leasing. Accounting & Finance. 61(2). pp.3481-3515.

Endrawes, M and et.al., 2020. Audit committee characteristics and financial statement

comparability. Accounting & Finance. 60(3). pp.2361-2395.

Khoruzhy, L.I and et.al., 2021, December. Reporting system in the adaptive accounting

and analytical system of providing inter-organizational collaboration of AIC

organizations. In AIP Conference Proceedings (Vol. 2442, No. 1, p. 020014).

AIP Publishing LLC.

Lu, J and et.al., 2022. Financial controller turnover: An early warning sign of

deteriorating financial reporting quality. Accounting & Finance.

Obenpong Kwabi, F and et.al., 2022. Economic policy uncertainty and cost of capital:

the mediating effects of foreign equity portfolio flow. Review of Quantitative

Finance and Accounting, pp.1-25.

Storozhuk, T. and Blyshchyk, L., 2019. Interpretation of the" Financial Reporting"

Definition. Oblik i finansi. (4). pp.54-62.

Xu, C and et.al., 2021. Real earnings management in bankrupt firms. Journal of

Corporate Accounting & Finance. 32(2). pp.22-38.

Yi, Z and et.al., 2018. The impact of consumer fairness seeking on distribution channel

selection: Direct selling vs. agent selling. Production and Operations

Management. 27(6). pp.1148-1167.

9

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.