Financial Performance Analysis and Decision Making for Roast Ltd.

VerifiedAdded on 2023/01/16

|15

|4546

|57

Report

AI Summary

This report provides a comprehensive financial analysis of Roast Ltd., a UK-based coffee chain, focusing on financial decision-making. It begins with an executive summary and an overview of the coffee house industry in the UK. The main body delves into a detailed analysis of Roast Ltd.'s financial performance using profit and loss statement analysis, balance sheet analysis, and cash flow statement analysis, employing ratio analysis techniques to assess profitability, liquidity, and efficiency. The report also examines the application of investment appraisal techniques to support financial decisions, including forecasting and the identification of different sources of finance. The analysis reveals key trends in Roast Ltd.'s financial health and provides insights that could inform strategic decisions, particularly regarding potential acquisitions.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................4

MAIN BODY...................................................................................................................................4

PART 1: Review about Coffee House Industry...............................................................................4

PART 2: Analysis of business performance....................................................................................5

2.1 Profit and loss statement analysis of Roast Ltd. Through usage of ratio analysis technique

.....................................................................................................................................................5

2.2 Analysis of Balance sheet through usage of ratio analysis technique...................................7

2.3 Cash Flow Statement analysis with the help of operating cash cycle computation and

dividend policy............................................................................................................................9

PART 3: Application and determination of contribution of Investment Appraisal techniques.....12

3.1 Forecasting about management along with usage of investment appraisal-techniques......12

3.2 Identification of different sources of finance......................................................................13

REFERENCES..............................................................................................................................15

.......................................................................................................................................................15

EXECUTIVE SUMMARY.............................................................................................................4

MAIN BODY...................................................................................................................................4

PART 1: Review about Coffee House Industry...............................................................................4

PART 2: Analysis of business performance....................................................................................5

2.1 Profit and loss statement analysis of Roast Ltd. Through usage of ratio analysis technique

.....................................................................................................................................................5

2.2 Analysis of Balance sheet through usage of ratio analysis technique...................................7

2.3 Cash Flow Statement analysis with the help of operating cash cycle computation and

dividend policy............................................................................................................................9

PART 3: Application and determination of contribution of Investment Appraisal techniques.....12

3.1 Forecasting about management along with usage of investment appraisal-techniques......12

3.2 Identification of different sources of finance......................................................................13

REFERENCES..............................................................................................................................15

.......................................................................................................................................................15

EXECUTIVE SUMMARY

Financial decision is a process that contains the responsibility in respect to all the

decisions that have relation with liabilities and stakeholders equity of an organisation along with

issuance of bonds. These are of three different types and known as application, procurement and

distribution of funds. This has significant amount of contribution behind the attainment of

organisational goals. The organisation considered under this report is Roast Ltd. It is a cafe chain

that has operations in all over UK. The main aim of this report is about the analysis of the final

accounts of an organisation that assist in formulation of decisions by the management of

Starbucks.

The aspects covered in this report includes analysis of the facts about industry and

determination of business performance with the help of different type of ratios. Also, covers the

application of investment appraisal-techniques that assist in building investment related

decisions.

MAIN BODY

PART 1: Review about Coffee House Industry

It is important to analyse industry as this will help to get the information in relation to the

aspects present in market along with their impact. The contribution of this exercise is optimum in

nature regarding development of the business activities. It assist the management in formulation

of their different decisions along with strategies that enable the organisation to attain

sustainability in industry. In the current report, analysis is done in respect of Coffee House

Industry of UK. The gathered information in relation to such analysis is presented below:

This industry is large in nature and having significant contribution in the economy of UK.

The number of business organisation operates in this industry are huge in amount and

consists both registered or unregistered. Many organisations has diversified business

activities and indulge in the selling activities of cold and soft drinks too.

Ascertained from the analysis that there are many factors upon which success of this

industry depends includes social and economic condition of UK. The society and

individuals of UK are prefer to consume coffee. Also, the positive trend is visible in per

capita income. This shows the positive sign for the growth of this industry along with all

the organisations prevails in same (Current coffee house industry of United Kingdom.

Financial decision is a process that contains the responsibility in respect to all the

decisions that have relation with liabilities and stakeholders equity of an organisation along with

issuance of bonds. These are of three different types and known as application, procurement and

distribution of funds. This has significant amount of contribution behind the attainment of

organisational goals. The organisation considered under this report is Roast Ltd. It is a cafe chain

that has operations in all over UK. The main aim of this report is about the analysis of the final

accounts of an organisation that assist in formulation of decisions by the management of

Starbucks.

The aspects covered in this report includes analysis of the facts about industry and

determination of business performance with the help of different type of ratios. Also, covers the

application of investment appraisal-techniques that assist in building investment related

decisions.

MAIN BODY

PART 1: Review about Coffee House Industry

It is important to analyse industry as this will help to get the information in relation to the

aspects present in market along with their impact. The contribution of this exercise is optimum in

nature regarding development of the business activities. It assist the management in formulation

of their different decisions along with strategies that enable the organisation to attain

sustainability in industry. In the current report, analysis is done in respect of Coffee House

Industry of UK. The gathered information in relation to such analysis is presented below:

This industry is large in nature and having significant contribution in the economy of UK.

The number of business organisation operates in this industry are huge in amount and

consists both registered or unregistered. Many organisations has diversified business

activities and indulge in the selling activities of cold and soft drinks too.

Ascertained from the analysis that there are many factors upon which success of this

industry depends includes social and economic condition of UK. The society and

individuals of UK are prefer to consume coffee. Also, the positive trend is visible in per

capita income. This shows the positive sign for the growth of this industry along with all

the organisations prevails in same (Current coffee house industry of United Kingdom.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2019). The sound economy of UK, assist the organisations under this industry to focus

over expansion along with improvement in quality of their products and services that

directly contributes in the growth towards positive direction.

Increment in demand towards coffee is common in this industry. This would be the

reason that organisations offering coffee has large number of customers along with high

market share.

One of the main challenge that have been faced by Cafes Coffee Shops or business

industry is emergence of more substitute beverages which turn to decline sales and

profitability of company (Correia, Dussault and Pontes, 2015).

Variation in minimum wages also have a main effect on operations of an organization

profitability. Beverages industry mainly employ a fairly huge range of low-paid workers.

As it will help an organization in development of its growth and success.

One of the best advantage or benefit for Cafes Coffee Shops is to growth their business

operations in various nations like India, China etc. These counties have biggest

population as compare to other nation.

PART 2: Analysis of business performance

2.1 Profit and loss statement analysis of Roast Ltd. Through usage of ratio analysis technique

Profit and loss statement is one of the main document of the organisation. This contains

the information about the transactions through which an organisation passes off during the one

year of time period. Adherence of all the accounting principles and effective formulation of

profit and loss account provide the information about profit ans loss in year end. The future

contribution of this towards an management is understood from the fact that this will provides an

opportunity to formulate effective budgets that contains reliable and accurate projections

(Epstein, Buhovac and Yuthas, 2015).

In the current report, analysis of profit and loss account of Roast Ltd. Is ascertained for

the purpose of determine its condition in market. The growth of 25.32% was seen in the turnover

of this organisation in between the year of 2017 to 2018. The figure noticed in 2017 was

£2022000 and this was increased in year 2018 and grab the figure of £2534000. The growth is

also visible in the sales of this organisation in percentage of 32.23 in between 2017 to 2018. It

was increased from £1505000 to £1990000. Increasing trend is visible in operating expenses

over expansion along with improvement in quality of their products and services that

directly contributes in the growth towards positive direction.

Increment in demand towards coffee is common in this industry. This would be the

reason that organisations offering coffee has large number of customers along with high

market share.

One of the main challenge that have been faced by Cafes Coffee Shops or business

industry is emergence of more substitute beverages which turn to decline sales and

profitability of company (Correia, Dussault and Pontes, 2015).

Variation in minimum wages also have a main effect on operations of an organization

profitability. Beverages industry mainly employ a fairly huge range of low-paid workers.

As it will help an organization in development of its growth and success.

One of the best advantage or benefit for Cafes Coffee Shops is to growth their business

operations in various nations like India, China etc. These counties have biggest

population as compare to other nation.

PART 2: Analysis of business performance

2.1 Profit and loss statement analysis of Roast Ltd. Through usage of ratio analysis technique

Profit and loss statement is one of the main document of the organisation. This contains

the information about the transactions through which an organisation passes off during the one

year of time period. Adherence of all the accounting principles and effective formulation of

profit and loss account provide the information about profit ans loss in year end. The future

contribution of this towards an management is understood from the fact that this will provides an

opportunity to formulate effective budgets that contains reliable and accurate projections

(Epstein, Buhovac and Yuthas, 2015).

In the current report, analysis of profit and loss account of Roast Ltd. Is ascertained for

the purpose of determine its condition in market. The growth of 25.32% was seen in the turnover

of this organisation in between the year of 2017 to 2018. The figure noticed in 2017 was

£2022000 and this was increased in year 2018 and grab the figure of £2534000. The growth is

also visible in the sales of this organisation in percentage of 32.23 in between 2017 to 2018. It

was increased from £1505000 to £1990000. Increasing trend is visible in operating expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

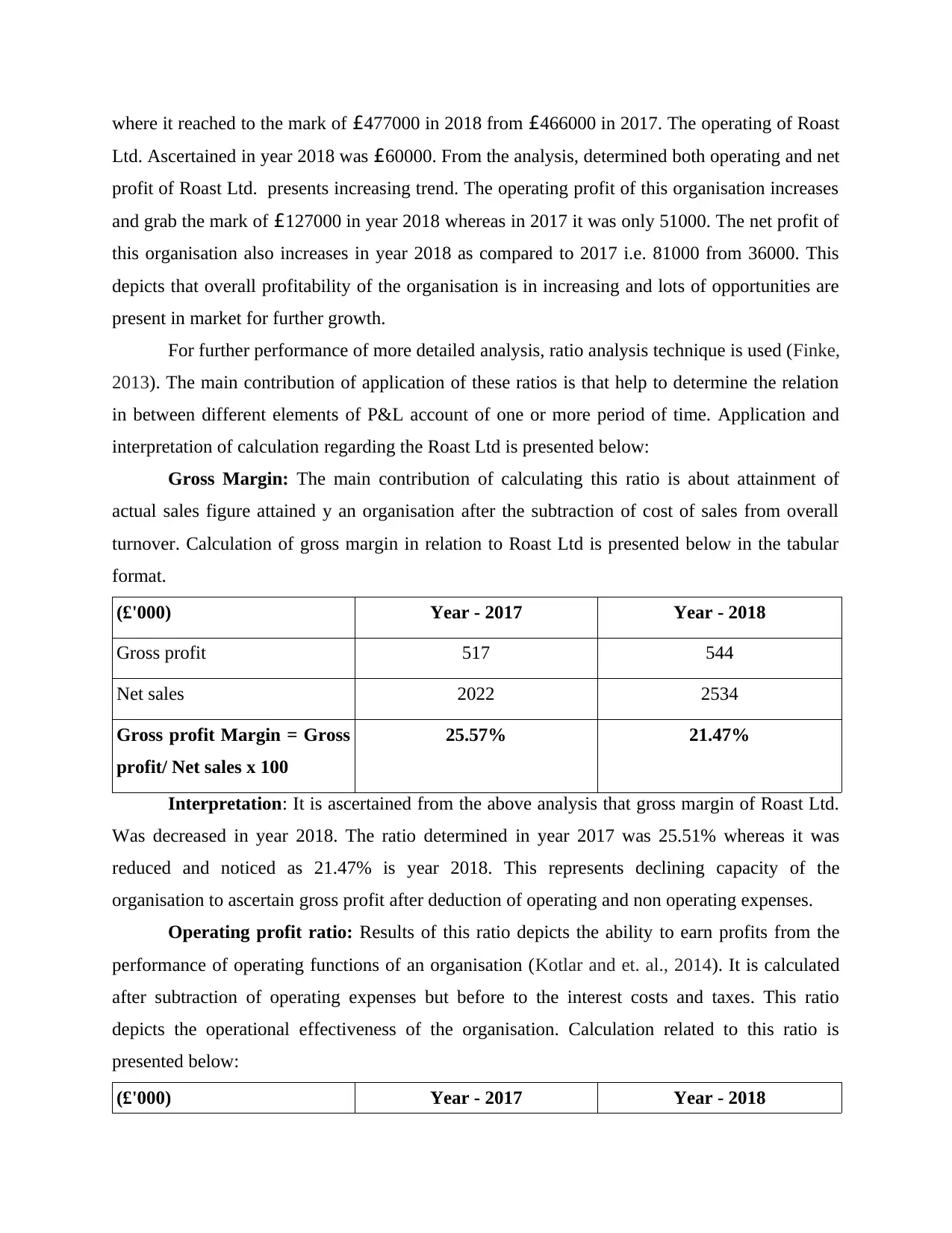

where it reached to the mark of £477000 in 2018 from £466000 in 2017. The operating of Roast

Ltd. Ascertained in year 2018 was £60000. From the analysis, determined both operating and net

profit of Roast Ltd. presents increasing trend. The operating profit of this organisation increases

and grab the mark of £127000 in year 2018 whereas in 2017 it was only 51000. The net profit of

this organisation also increases in year 2018 as compared to 2017 i.e. 81000 from 36000. This

depicts that overall profitability of the organisation is in increasing and lots of opportunities are

present in market for further growth.

For further performance of more detailed analysis, ratio analysis technique is used (Finke,

2013). The main contribution of application of these ratios is that help to determine the relation

in between different elements of P&L account of one or more period of time. Application and

interpretation of calculation regarding the Roast Ltd is presented below:

Gross Margin: The main contribution of calculating this ratio is about attainment of

actual sales figure attained y an organisation after the subtraction of cost of sales from overall

turnover. Calculation of gross margin in relation to Roast Ltd is presented below in the tabular

format.

(£'000) Year - 2017 Year - 2018

Gross profit 517 544

Net sales 2022 2534

Gross profit Margin = Gross

profit/ Net sales x 100

25.57% 21.47%

Interpretation: It is ascertained from the above analysis that gross margin of Roast Ltd.

Was decreased in year 2018. The ratio determined in year 2017 was 25.51% whereas it was

reduced and noticed as 21.47% is year 2018. This represents declining capacity of the

organisation to ascertain gross profit after deduction of operating and non operating expenses.

Operating profit ratio: Results of this ratio depicts the ability to earn profits from the

performance of operating functions of an organisation (Kotlar and et. al., 2014). It is calculated

after subtraction of operating expenses but before to the interest costs and taxes. This ratio

depicts the operational effectiveness of the organisation. Calculation related to this ratio is

presented below:

(£'000) Year - 2017 Year - 2018

Ltd. Ascertained in year 2018 was £60000. From the analysis, determined both operating and net

profit of Roast Ltd. presents increasing trend. The operating profit of this organisation increases

and grab the mark of £127000 in year 2018 whereas in 2017 it was only 51000. The net profit of

this organisation also increases in year 2018 as compared to 2017 i.e. 81000 from 36000. This

depicts that overall profitability of the organisation is in increasing and lots of opportunities are

present in market for further growth.

For further performance of more detailed analysis, ratio analysis technique is used (Finke,

2013). The main contribution of application of these ratios is that help to determine the relation

in between different elements of P&L account of one or more period of time. Application and

interpretation of calculation regarding the Roast Ltd is presented below:

Gross Margin: The main contribution of calculating this ratio is about attainment of

actual sales figure attained y an organisation after the subtraction of cost of sales from overall

turnover. Calculation of gross margin in relation to Roast Ltd is presented below in the tabular

format.

(£'000) Year - 2017 Year - 2018

Gross profit 517 544

Net sales 2022 2534

Gross profit Margin = Gross

profit/ Net sales x 100

25.57% 21.47%

Interpretation: It is ascertained from the above analysis that gross margin of Roast Ltd.

Was decreased in year 2018. The ratio determined in year 2017 was 25.51% whereas it was

reduced and noticed as 21.47% is year 2018. This represents declining capacity of the

organisation to ascertain gross profit after deduction of operating and non operating expenses.

Operating profit ratio: Results of this ratio depicts the ability to earn profits from the

performance of operating functions of an organisation (Kotlar and et. al., 2014). It is calculated

after subtraction of operating expenses but before to the interest costs and taxes. This ratio

depicts the operational effectiveness of the organisation. Calculation related to this ratio is

presented below:

(£'000) Year - 2017 Year - 2018

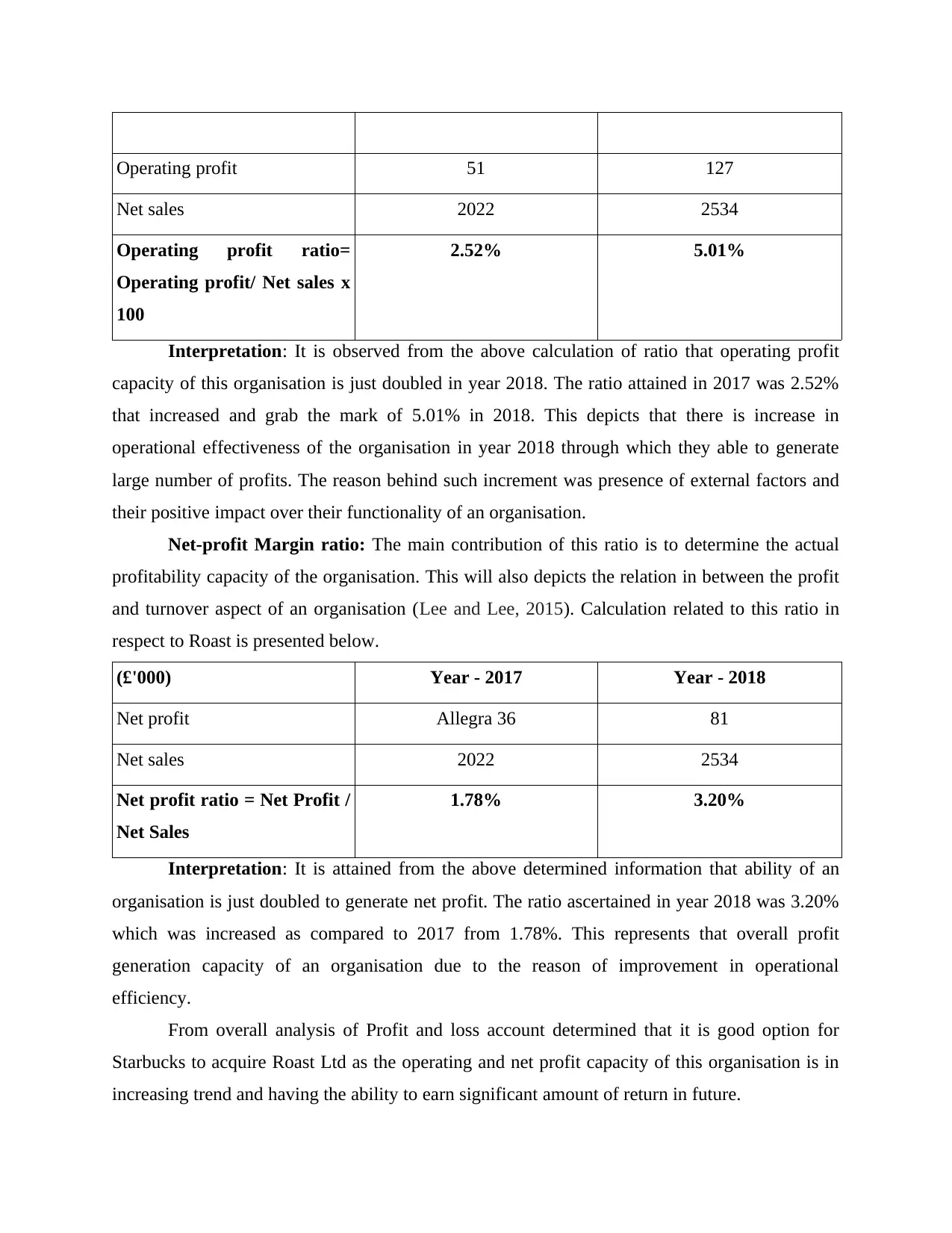

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio=

Operating profit/ Net sales x

100

2.52% 5.01%

Interpretation: It is observed from the above calculation of ratio that operating profit

capacity of this organisation is just doubled in year 2018. The ratio attained in 2017 was 2.52%

that increased and grab the mark of 5.01% in 2018. This depicts that there is increase in

operational effectiveness of the organisation in year 2018 through which they able to generate

large number of profits. The reason behind such increment was presence of external factors and

their positive impact over their functionality of an organisation.

Net-profit Margin ratio: The main contribution of this ratio is to determine the actual

profitability capacity of the organisation. This will also depicts the relation in between the profit

and turnover aspect of an organisation (Lee and Lee, 2015). Calculation related to this ratio in

respect to Roast is presented below.

(£'000) Year - 2017 Year - 2018

Net profit Allegra 36 81

Net sales 2022 2534

Net profit ratio = Net Profit /

Net Sales

1.78% 3.20%

Interpretation: It is attained from the above determined information that ability of an

organisation is just doubled to generate net profit. The ratio ascertained in year 2018 was 3.20%

which was increased as compared to 2017 from 1.78%. This represents that overall profit

generation capacity of an organisation due to the reason of improvement in operational

efficiency.

From overall analysis of Profit and loss account determined that it is good option for

Starbucks to acquire Roast Ltd as the operating and net profit capacity of this organisation is in

increasing trend and having the ability to earn significant amount of return in future.

Net sales 2022 2534

Operating profit ratio=

Operating profit/ Net sales x

100

2.52% 5.01%

Interpretation: It is observed from the above calculation of ratio that operating profit

capacity of this organisation is just doubled in year 2018. The ratio attained in 2017 was 2.52%

that increased and grab the mark of 5.01% in 2018. This depicts that there is increase in

operational effectiveness of the organisation in year 2018 through which they able to generate

large number of profits. The reason behind such increment was presence of external factors and

their positive impact over their functionality of an organisation.

Net-profit Margin ratio: The main contribution of this ratio is to determine the actual

profitability capacity of the organisation. This will also depicts the relation in between the profit

and turnover aspect of an organisation (Lee and Lee, 2015). Calculation related to this ratio in

respect to Roast is presented below.

(£'000) Year - 2017 Year - 2018

Net profit Allegra 36 81

Net sales 2022 2534

Net profit ratio = Net Profit /

Net Sales

1.78% 3.20%

Interpretation: It is attained from the above determined information that ability of an

organisation is just doubled to generate net profit. The ratio ascertained in year 2018 was 3.20%

which was increased as compared to 2017 from 1.78%. This represents that overall profit

generation capacity of an organisation due to the reason of improvement in operational

efficiency.

From overall analysis of Profit and loss account determined that it is good option for

Starbucks to acquire Roast Ltd as the operating and net profit capacity of this organisation is in

increasing trend and having the ability to earn significant amount of return in future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

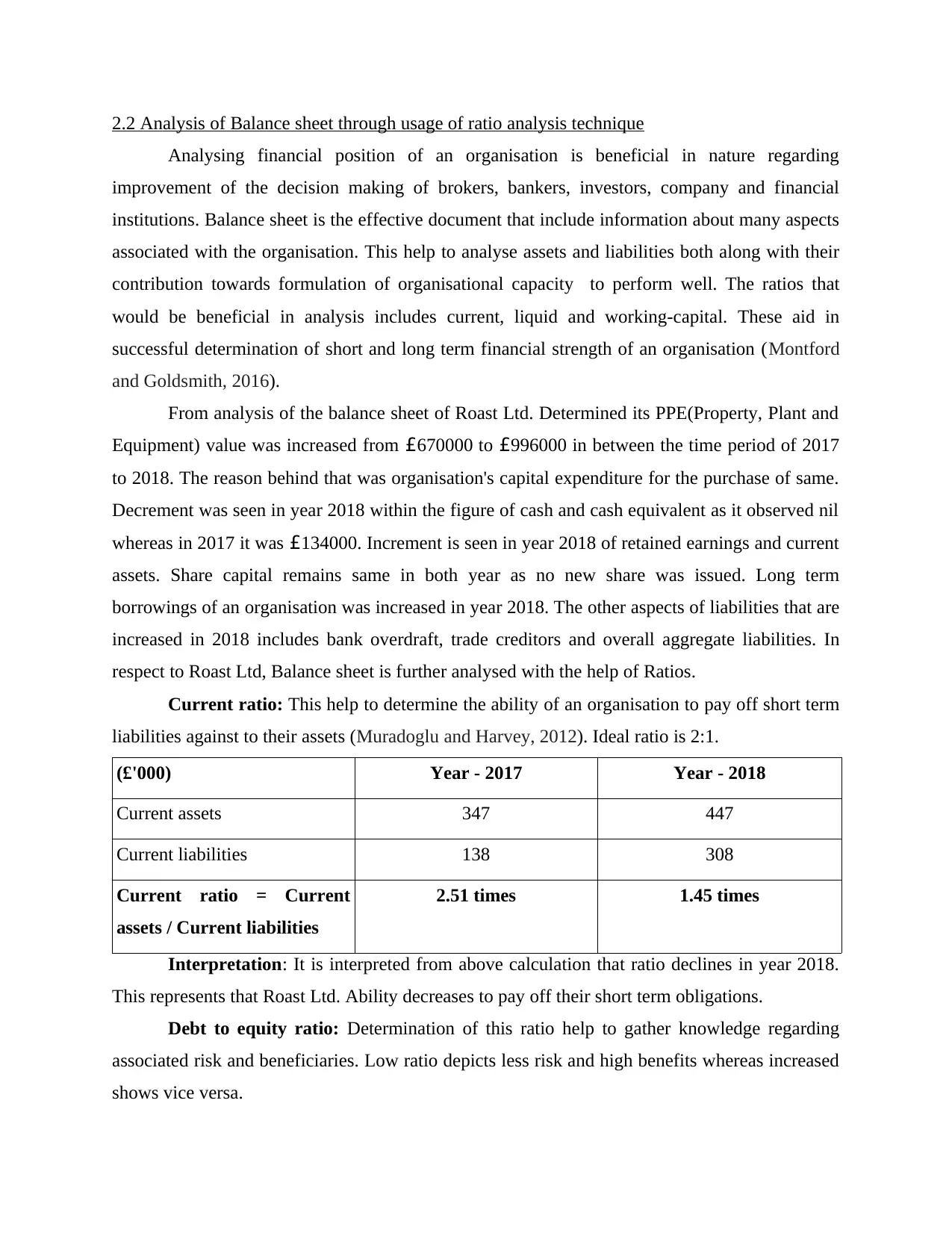

2.2 Analysis of Balance sheet through usage of ratio analysis technique

Analysing financial position of an organisation is beneficial in nature regarding

improvement of the decision making of brokers, bankers, investors, company and financial

institutions. Balance sheet is the effective document that include information about many aspects

associated with the organisation. This help to analyse assets and liabilities both along with their

contribution towards formulation of organisational capacity to perform well. The ratios that

would be beneficial in analysis includes current, liquid and working-capital. These aid in

successful determination of short and long term financial strength of an organisation (Montford

and Goldsmith, 2016).

From analysis of the balance sheet of Roast Ltd. Determined its PPE(Property, Plant and

Equipment) value was increased from £670000 to £996000 in between the time period of 2017

to 2018. The reason behind that was organisation's capital expenditure for the purchase of same.

Decrement was seen in year 2018 within the figure of cash and cash equivalent as it observed nil

whereas in 2017 it was £134000. Increment is seen in year 2018 of retained earnings and current

assets. Share capital remains same in both year as no new share was issued. Long term

borrowings of an organisation was increased in year 2018. The other aspects of liabilities that are

increased in 2018 includes bank overdraft, trade creditors and overall aggregate liabilities. In

respect to Roast Ltd, Balance sheet is further analysed with the help of Ratios.

Current ratio: This help to determine the ability of an organisation to pay off short term

liabilities against to their assets (Muradoglu and Harvey, 2012). Ideal ratio is 2:1.

(£'000) Year - 2017 Year - 2018

Current assets 347 447

Current liabilities 138 308

Current ratio = Current

assets / Current liabilities

2.51 times 1.45 times

Interpretation: It is interpreted from above calculation that ratio declines in year 2018.

This represents that Roast Ltd. Ability decreases to pay off their short term obligations.

Debt to equity ratio: Determination of this ratio help to gather knowledge regarding

associated risk and beneficiaries. Low ratio depicts less risk and high benefits whereas increased

shows vice versa.

Analysing financial position of an organisation is beneficial in nature regarding

improvement of the decision making of brokers, bankers, investors, company and financial

institutions. Balance sheet is the effective document that include information about many aspects

associated with the organisation. This help to analyse assets and liabilities both along with their

contribution towards formulation of organisational capacity to perform well. The ratios that

would be beneficial in analysis includes current, liquid and working-capital. These aid in

successful determination of short and long term financial strength of an organisation (Montford

and Goldsmith, 2016).

From analysis of the balance sheet of Roast Ltd. Determined its PPE(Property, Plant and

Equipment) value was increased from £670000 to £996000 in between the time period of 2017

to 2018. The reason behind that was organisation's capital expenditure for the purchase of same.

Decrement was seen in year 2018 within the figure of cash and cash equivalent as it observed nil

whereas in 2017 it was £134000. Increment is seen in year 2018 of retained earnings and current

assets. Share capital remains same in both year as no new share was issued. Long term

borrowings of an organisation was increased in year 2018. The other aspects of liabilities that are

increased in 2018 includes bank overdraft, trade creditors and overall aggregate liabilities. In

respect to Roast Ltd, Balance sheet is further analysed with the help of Ratios.

Current ratio: This help to determine the ability of an organisation to pay off short term

liabilities against to their assets (Muradoglu and Harvey, 2012). Ideal ratio is 2:1.

(£'000) Year - 2017 Year - 2018

Current assets 347 447

Current liabilities 138 308

Current ratio = Current

assets / Current liabilities

2.51 times 1.45 times

Interpretation: It is interpreted from above calculation that ratio declines in year 2018.

This represents that Roast Ltd. Ability decreases to pay off their short term obligations.

Debt to equity ratio: Determination of this ratio help to gather knowledge regarding

associated risk and beneficiaries. Low ratio depicts less risk and high benefits whereas increased

shows vice versa.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

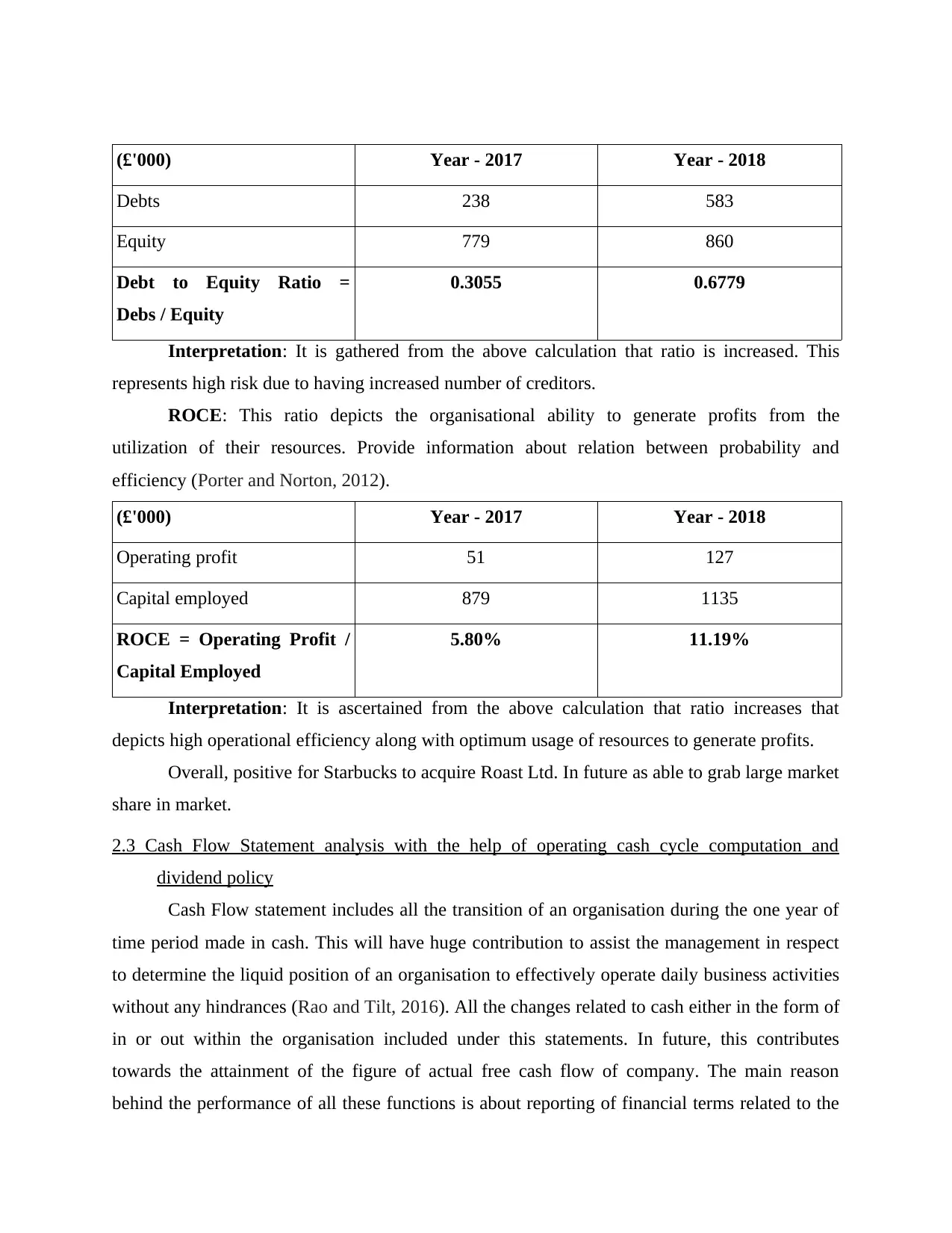

(£'000) Year - 2017 Year - 2018

Debts 238 583

Equity 779 860

Debt to Equity Ratio =

Debs / Equity

0.3055 0.6779

Interpretation: It is gathered from the above calculation that ratio is increased. This

represents high risk due to having increased number of creditors.

ROCE: This ratio depicts the organisational ability to generate profits from the

utilization of their resources. Provide information about relation between probability and

efficiency (Porter and Norton, 2012).

(£'000) Year - 2017 Year - 2018

Operating profit 51 127

Capital employed 879 1135

ROCE = Operating Profit /

Capital Employed

5.80% 11.19%

Interpretation: It is ascertained from the above calculation that ratio increases that

depicts high operational efficiency along with optimum usage of resources to generate profits.

Overall, positive for Starbucks to acquire Roast Ltd. In future as able to grab large market

share in market.

2.3 Cash Flow Statement analysis with the help of operating cash cycle computation and

dividend policy

Cash Flow statement includes all the transition of an organisation during the one year of

time period made in cash. This will have huge contribution to assist the management in respect

to determine the liquid position of an organisation to effectively operate daily business activities

without any hindrances (Rao and Tilt, 2016). All the changes related to cash either in the form of

in or out within the organisation included under this statements. In future, this contributes

towards the attainment of the figure of actual free cash flow of company. The main reason

behind the performance of all these functions is about reporting of financial terms related to the

Debts 238 583

Equity 779 860

Debt to Equity Ratio =

Debs / Equity

0.3055 0.6779

Interpretation: It is gathered from the above calculation that ratio is increased. This

represents high risk due to having increased number of creditors.

ROCE: This ratio depicts the organisational ability to generate profits from the

utilization of their resources. Provide information about relation between probability and

efficiency (Porter and Norton, 2012).

(£'000) Year - 2017 Year - 2018

Operating profit 51 127

Capital employed 879 1135

ROCE = Operating Profit /

Capital Employed

5.80% 11.19%

Interpretation: It is ascertained from the above calculation that ratio increases that

depicts high operational efficiency along with optimum usage of resources to generate profits.

Overall, positive for Starbucks to acquire Roast Ltd. In future as able to grab large market

share in market.

2.3 Cash Flow Statement analysis with the help of operating cash cycle computation and

dividend policy

Cash Flow statement includes all the transition of an organisation during the one year of

time period made in cash. This will have huge contribution to assist the management in respect

to determine the liquid position of an organisation to effectively operate daily business activities

without any hindrances (Rao and Tilt, 2016). All the changes related to cash either in the form of

in or out within the organisation included under this statements. In future, this contributes

towards the attainment of the figure of actual free cash flow of company. The main reason

behind the performance of all these functions is about reporting of financial terms related to the

organisation. The different kind of transactions that are considered under this includes proceeds

of bond, capital gain, sales of assets, key debt service, personal expenditures etc.

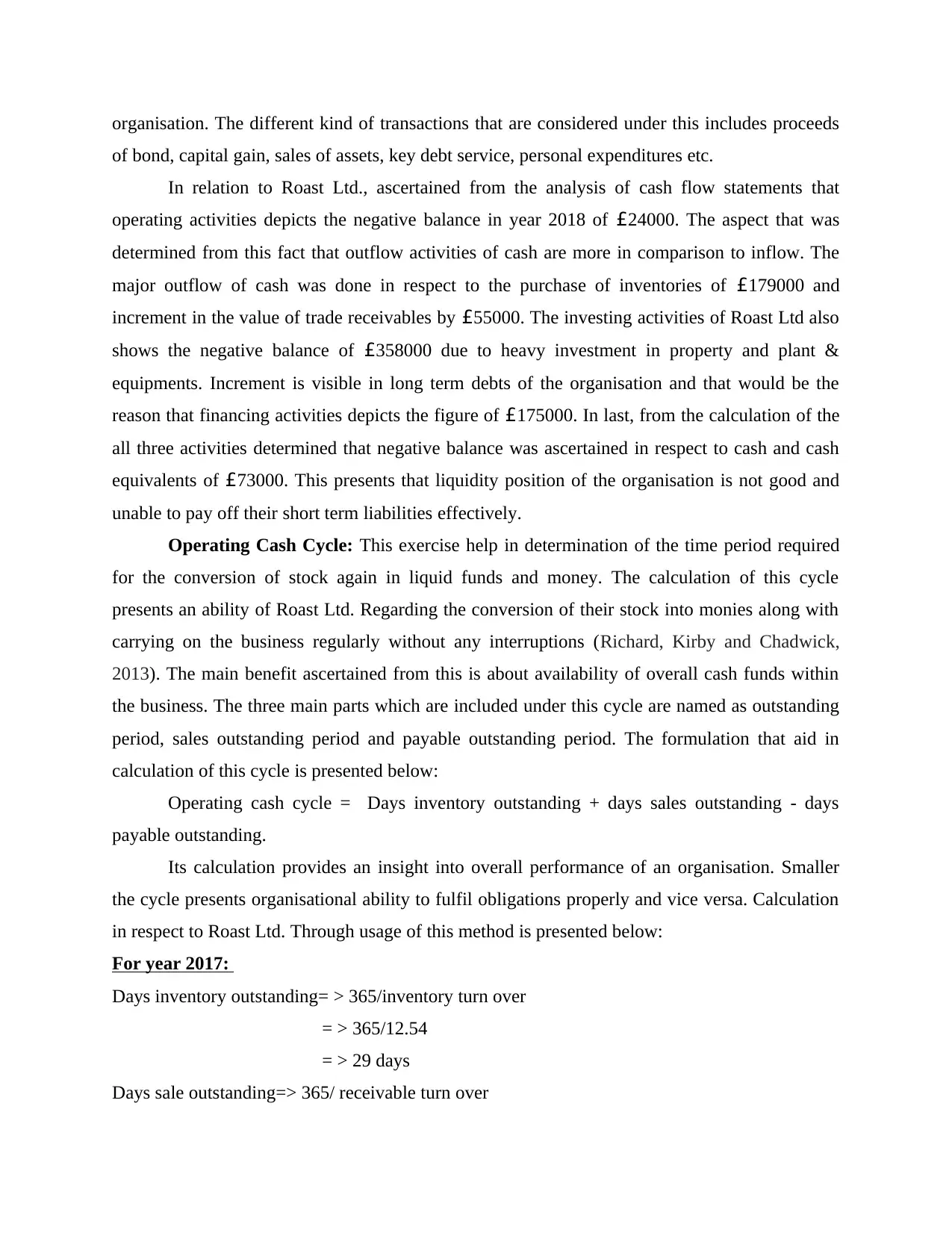

In relation to Roast Ltd., ascertained from the analysis of cash flow statements that

operating activities depicts the negative balance in year 2018 of £24000. The aspect that was

determined from this fact that outflow activities of cash are more in comparison to inflow. The

major outflow of cash was done in respect to the purchase of inventories of £179000 and

increment in the value of trade receivables by £55000. The investing activities of Roast Ltd also

shows the negative balance of £358000 due to heavy investment in property and plant &

equipments. Increment is visible in long term debts of the organisation and that would be the

reason that financing activities depicts the figure of £175000. In last, from the calculation of the

all three activities determined that negative balance was ascertained in respect to cash and cash

equivalents of £73000. This presents that liquidity position of the organisation is not good and

unable to pay off their short term liabilities effectively.

Operating Cash Cycle: This exercise help in determination of the time period required

for the conversion of stock again in liquid funds and money. The calculation of this cycle

presents an ability of Roast Ltd. Regarding the conversion of their stock into monies along with

carrying on the business regularly without any interruptions (Richard, Kirby and Chadwick,

2013). The main benefit ascertained from this is about availability of overall cash funds within

the business. The three main parts which are included under this cycle are named as outstanding

period, sales outstanding period and payable outstanding period. The formulation that aid in

calculation of this cycle is presented below:

Operating cash cycle = Days inventory outstanding + days sales outstanding - days

payable outstanding.

Its calculation provides an insight into overall performance of an organisation. Smaller

the cycle presents organisational ability to fulfil obligations properly and vice versa. Calculation

in respect to Roast Ltd. Through usage of this method is presented below:

For year 2017:

Days inventory outstanding= > 365/inventory turn over

= > 365/12.54

= > 29 days

Days sale outstanding=> 365/ receivable turn over

of bond, capital gain, sales of assets, key debt service, personal expenditures etc.

In relation to Roast Ltd., ascertained from the analysis of cash flow statements that

operating activities depicts the negative balance in year 2018 of £24000. The aspect that was

determined from this fact that outflow activities of cash are more in comparison to inflow. The

major outflow of cash was done in respect to the purchase of inventories of £179000 and

increment in the value of trade receivables by £55000. The investing activities of Roast Ltd also

shows the negative balance of £358000 due to heavy investment in property and plant &

equipments. Increment is visible in long term debts of the organisation and that would be the

reason that financing activities depicts the figure of £175000. In last, from the calculation of the

all three activities determined that negative balance was ascertained in respect to cash and cash

equivalents of £73000. This presents that liquidity position of the organisation is not good and

unable to pay off their short term liabilities effectively.

Operating Cash Cycle: This exercise help in determination of the time period required

for the conversion of stock again in liquid funds and money. The calculation of this cycle

presents an ability of Roast Ltd. Regarding the conversion of their stock into monies along with

carrying on the business regularly without any interruptions (Richard, Kirby and Chadwick,

2013). The main benefit ascertained from this is about availability of overall cash funds within

the business. The three main parts which are included under this cycle are named as outstanding

period, sales outstanding period and payable outstanding period. The formulation that aid in

calculation of this cycle is presented below:

Operating cash cycle = Days inventory outstanding + days sales outstanding - days

payable outstanding.

Its calculation provides an insight into overall performance of an organisation. Smaller

the cycle presents organisational ability to fulfil obligations properly and vice versa. Calculation

in respect to Roast Ltd. Through usage of this method is presented below:

For year 2017:

Days inventory outstanding= > 365/inventory turn over

= > 365/12.54

= > 29 days

Days sale outstanding=> 365/ receivable turn over

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= > 365/21.74

= > 17 days

Days payable outstanding=> 365/ payable turn over

= > 365/ 10.90

=> 33 days

So operating cash cycle => (29+17-33) days

=> 13 days

Working Note:

Inventory turn over= cost of sales/ average inventory

=> £1505/£120

=> 12.54

Receivable turn over => net sales/account receivable

=> £2022/£93

=> 21.74

Payable turn over => cost of sales/ account payable

= £1505/£138

= 10.90

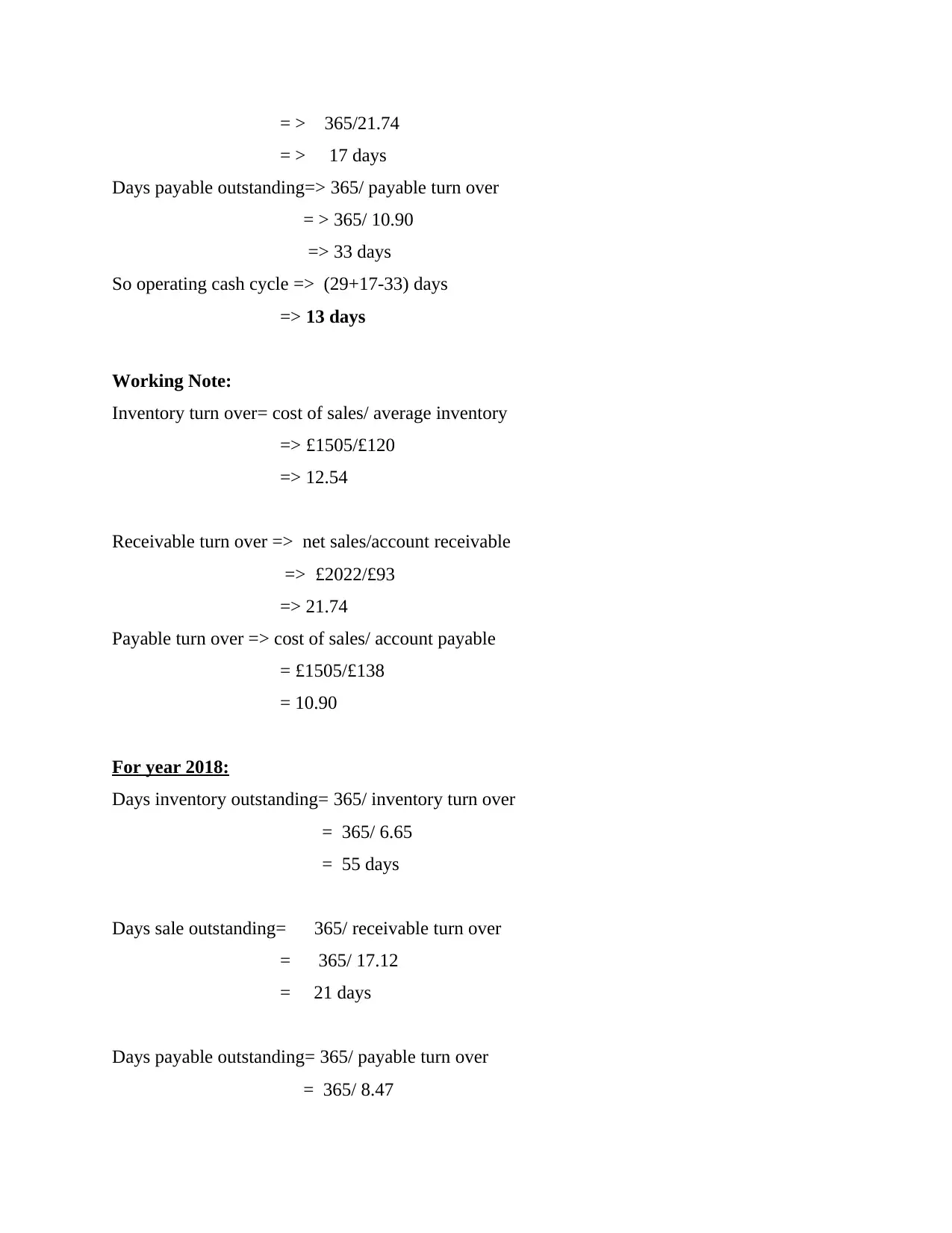

For year 2018:

Days inventory outstanding= 365/ inventory turn over

= 365/ 6.65

= 55 days

Days sale outstanding= 365/ receivable turn over

= 365/ 17.12

= 21 days

Days payable outstanding= 365/ payable turn over

= 365/ 8.47

= > 17 days

Days payable outstanding=> 365/ payable turn over

= > 365/ 10.90

=> 33 days

So operating cash cycle => (29+17-33) days

=> 13 days

Working Note:

Inventory turn over= cost of sales/ average inventory

=> £1505/£120

=> 12.54

Receivable turn over => net sales/account receivable

=> £2022/£93

=> 21.74

Payable turn over => cost of sales/ account payable

= £1505/£138

= 10.90

For year 2018:

Days inventory outstanding= 365/ inventory turn over

= 365/ 6.65

= 55 days

Days sale outstanding= 365/ receivable turn over

= 365/ 17.12

= 21 days

Days payable outstanding= 365/ payable turn over

= 365/ 8.47

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 44 days

So operating cash cycle= (55+21-44) days

= 32 days

Working Note:

Inventory turn over= Cost of sales/ average inventory

= 1990/ 299

= 6.65

Receivable turn over= Net sales/ account receivable

= 2534/148

= 17.12

Payable turn over = Cost of sales/ account payable

= 1990/235

= 8.47

Interpretation: It is determined from the above calculation that operating cash cycle of

Roast Ltd . Is 13 days. This depicts that organisation is able to convert stock into cash within 1 3

days. It is sufficient in nature but can be optimised.

Dividend Policy: This help in management of dividend-payout by an organisation to its

shareholders (Saxonberg and Sirovátka, 2014). No divided policy is adopted by Roast Ltd. As

dividend-payout is zero. In year 2018, no divided was paid by the organisation to its shareholders

PART 3: Application and determination of contribution of Investment

Appraisal techniques

3.1 Forecasting about management along with usage of investment appraisal-techniques

Monetary is a crucial factor so management of Roast limited is more focused to raise

about £ 500 million as a capital between the period of 5 years. With such huge amount of cash

flow it is easy for organisation to raise capital in proper manner. The estimate idea to collect cash

receipt is £ 60, £ 112, £ 148, £ 180 and £ 224 million. Further, this predication is wrong for the

year 2018 due to decline in the gross margin and cash flow of organisation. Therefore, with the

appropriate forecast it is easy to readjust company's current performance.

So operating cash cycle= (55+21-44) days

= 32 days

Working Note:

Inventory turn over= Cost of sales/ average inventory

= 1990/ 299

= 6.65

Receivable turn over= Net sales/ account receivable

= 2534/148

= 17.12

Payable turn over = Cost of sales/ account payable

= 1990/235

= 8.47

Interpretation: It is determined from the above calculation that operating cash cycle of

Roast Ltd . Is 13 days. This depicts that organisation is able to convert stock into cash within 1 3

days. It is sufficient in nature but can be optimised.

Dividend Policy: This help in management of dividend-payout by an organisation to its

shareholders (Saxonberg and Sirovátka, 2014). No divided policy is adopted by Roast Ltd. As

dividend-payout is zero. In year 2018, no divided was paid by the organisation to its shareholders

PART 3: Application and determination of contribution of Investment

Appraisal techniques

3.1 Forecasting about management along with usage of investment appraisal-techniques

Monetary is a crucial factor so management of Roast limited is more focused to raise

about £ 500 million as a capital between the period of 5 years. With such huge amount of cash

flow it is easy for organisation to raise capital in proper manner. The estimate idea to collect cash

receipt is £ 60, £ 112, £ 148, £ 180 and £ 224 million. Further, this predication is wrong for the

year 2018 due to decline in the gross margin and cash flow of organisation. Therefore, with the

appropriate forecast it is easy to readjust company's current performance.

Appraisal techniques are consider more useful tools which are applied by an organisation

to viability of any financial investment and decision (Starcke and Brand, 2012). There are

various techniques of investment appraisal which are determined as below:

Payback period: This introduces to the amount of time period that takes to recover the

investment cost. As stated in exhibit:3, payback period of company is 4 year. This clearly

explains that an organisation would recover its cash outflow which is £ 500 in four year. One of

the main benefit of this technique is it is a a casual and simplex approach. Main drawback of this

tool is in this time value of money is completely ignored.

Accounting rate of return: This is also known as an average rate of return which is a

financial ration and applied in capital budgeting (Epstein, Buhovac and Yuthas, 2015). As stated

in exhibit:3, average rate of investment is around 18%. It is a favourable amount and also below

the forecasted average rate-of-return e.g. 10% so investment is feasible as it is effective for an

organisation to get better return for investment. Main advantage of this technique as it clearly

explain level of profitability for any project of an organisation. Drawback of this tool is it also

ignores time value of money.

Net present value: This introduces as a differences between the present value of cash

inflow and cash outflow over a time period. According to the figures shows in exhibit:3 net

present value of company project is £ 110 million at discounting rate of 5%. It is a favourable

amount that indicate financial viability of any investment. Main advantage of this technique as it

help an organisation in measurement of profitability level. Estimation of opportunity cost is a

major drawback of Appraisal techniques.

3.2 Identification of different sources of finance

In an organisation, the aspect of finance plays a significant role as it lead them to manage

and handle its all managerial as well as operational function in a smooth manner (Kotlar and et.

al., 2014). However, in regard of Roast Ltd, it is desired to expand its market division into Italy,

for which the overall amount which company has been estimated that £400k. Hence, in order to

accomplish the business goal in an effective manner, Roast Ltd, take an initiative to approach

various kind of finance sources which are as follows with their benefits and drawbacks:

Commercial Bank

This source is regraded as one of the most familiar financial institution who deliver the

service of granting loans, accept deposit, offers basic financial products such as saving accounts,

to viability of any financial investment and decision (Starcke and Brand, 2012). There are

various techniques of investment appraisal which are determined as below:

Payback period: This introduces to the amount of time period that takes to recover the

investment cost. As stated in exhibit:3, payback period of company is 4 year. This clearly

explains that an organisation would recover its cash outflow which is £ 500 in four year. One of

the main benefit of this technique is it is a a casual and simplex approach. Main drawback of this

tool is in this time value of money is completely ignored.

Accounting rate of return: This is also known as an average rate of return which is a

financial ration and applied in capital budgeting (Epstein, Buhovac and Yuthas, 2015). As stated

in exhibit:3, average rate of investment is around 18%. It is a favourable amount and also below

the forecasted average rate-of-return e.g. 10% so investment is feasible as it is effective for an

organisation to get better return for investment. Main advantage of this technique as it clearly

explain level of profitability for any project of an organisation. Drawback of this tool is it also

ignores time value of money.

Net present value: This introduces as a differences between the present value of cash

inflow and cash outflow over a time period. According to the figures shows in exhibit:3 net

present value of company project is £ 110 million at discounting rate of 5%. It is a favourable

amount that indicate financial viability of any investment. Main advantage of this technique as it

help an organisation in measurement of profitability level. Estimation of opportunity cost is a

major drawback of Appraisal techniques.

3.2 Identification of different sources of finance

In an organisation, the aspect of finance plays a significant role as it lead them to manage

and handle its all managerial as well as operational function in a smooth manner (Kotlar and et.

al., 2014). However, in regard of Roast Ltd, it is desired to expand its market division into Italy,

for which the overall amount which company has been estimated that £400k. Hence, in order to

accomplish the business goal in an effective manner, Roast Ltd, take an initiative to approach

various kind of finance sources which are as follows with their benefits and drawbacks:

Commercial Bank

This source is regraded as one of the most familiar financial institution who deliver the

service of granting loans, accept deposit, offers basic financial products such as saving accounts,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.