Report on Financial Decision Making and Ratio Analysis for SKANSA PLC

VerifiedAdded on 2023/01/05

|12

|3719

|52

Report

AI Summary

This report provides a comprehensive financial analysis of SKANSA PLC, a UK-based construction company. It begins with an introduction to financial decision-making and its importance, highlighting the key aspects businesses must consider. Task 1 focuses on the significance of accounting and finance functions, duties, and roles within SKANSA PLC, detailing various types of accounting functions such as financial planning, managerial accounting, and financial accounting. The report emphasizes the importance of these functions in monitoring earnings, planning, allocating resources, and managing funds. Task 2 involves the calculation and analysis of financial ratios, specifically the Return on Capital Employed (ROCE), to assess the company's financial performance. The report includes the calculation of ROCE for 2018 and 2019, providing insights into how effectively SKANSA PLC utilizes its capital. The analysis helps understand the company's profitability and efficiency in managing its capital investments, concluding with an overview of the company's financial health.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:.............3

TASK 2............................................................................................................................................7

Calculation of of ratios for the company and comment on performance of company................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:.............3

TASK 2............................................................................................................................................7

Calculation of of ratios for the company and comment on performance of company................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial decision-making relates to set of activities or mechanism of assessing the positives and

negatives of decisions when it applies to the application of capital. The major aim of this study-

report is to highlight all key aspects that all enterprises need to consider in attempt to

take appropriate business financial decisions. Financial decision making provides assistance to

leverage available financial resources to accomplish the goals of the company, until a sufficient

standard of business financial performance is attained (Valaskova, Bartosova and Kubala, 2019).

This offers both a strategic as well as conceptual basis for the process of financial decision-

making. The main facets of entire financial decision-making apply to funding, investments,

dividends and managing of net-working capital. The current study is primarily based on

the SKANSA PLC, which is UK based construction corporation formed in year-1984. Study-

report cover thorough evaluation of company's financial position by using ratio analysis.

TASK 1

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:

Accounting and finance both these concepts aggregately have primary role for the company that

are used to carry out its operations in order to meet corporate objectives. The method of

recognizing, acquiring, categorising and reporting financial findings relating to a firm is regarded

to be accounting that is crucial for determining the adequate business decisions. Any firm must

evaluate the financial operations and the information which offer the relevant information as well

as to control the operations. In the case of SKANSKA PLC, both accounting as well as finance'

key functions are employed by administration to monitor their company by monitoring both sales

and expenses relevant to the company that enables to improve effectiveness (Kim, Gutter and

Spangler, 2017).

Types of accounting and finance function

Financial planning: this described as the primary function within business for the

organisation's financial scheduling and preparation as well as making budgets with help

of this. In company SKANSKA, mangers are accountable for execution of on financial

planning process by taking into consideration all accounting and financial transactions.

Managerial Accounting: This is the practice for formulating reports, managing both

accounting and finance processes and compiling business-related records. The

Financial decision-making relates to set of activities or mechanism of assessing the positives and

negatives of decisions when it applies to the application of capital. The major aim of this study-

report is to highlight all key aspects that all enterprises need to consider in attempt to

take appropriate business financial decisions. Financial decision making provides assistance to

leverage available financial resources to accomplish the goals of the company, until a sufficient

standard of business financial performance is attained (Valaskova, Bartosova and Kubala, 2019).

This offers both a strategic as well as conceptual basis for the process of financial decision-

making. The main facets of entire financial decision-making apply to funding, investments,

dividends and managing of net-working capital. The current study is primarily based on

the SKANSA PLC, which is UK based construction corporation formed in year-1984. Study-

report cover thorough evaluation of company's financial position by using ratio analysis.

TASK 1

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:

Accounting and finance both these concepts aggregately have primary role for the company that

are used to carry out its operations in order to meet corporate objectives. The method of

recognizing, acquiring, categorising and reporting financial findings relating to a firm is regarded

to be accounting that is crucial for determining the adequate business decisions. Any firm must

evaluate the financial operations and the information which offer the relevant information as well

as to control the operations. In the case of SKANSKA PLC, both accounting as well as finance'

key functions are employed by administration to monitor their company by monitoring both sales

and expenses relevant to the company that enables to improve effectiveness (Kim, Gutter and

Spangler, 2017).

Types of accounting and finance function

Financial planning: this described as the primary function within business for the

organisation's financial scheduling and preparation as well as making budgets with help

of this. In company SKANSKA, mangers are accountable for execution of on financial

planning process by taking into consideration all accounting and financial transactions.

Managerial Accounting: This is the practice for formulating reports, managing both

accounting and finance processes and compiling business-related records. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

administration of SKANSKA performs these functions to support the appropriate

business decisions by compiling financial and integral reports.

Financial accounting: It concerns the maintaining of accounting records for all

transactions, use of the double-entry accounting system and the preparation of final

statements that are sufficient for fulfilling the multiple governmental specifications for

legislative reporting, stock exchange and financial regulators. The financial accountant,

who will usually report to top management, is the individual accountable for this work in

most mid to large enterprises.

Supporting the business strategy and making financial policies: Finance manager is

accountable for making financial environment which supports financial and business

strategy. The right combination of shorter-term and longer-term finance and capital

resources ought to be made accessible to fulfil the organisation 's objective and have the

organisational agility required to take advantage of potential opportunities. All executives

have primary function to generate value, and the chief duty of finance officer is to allow

them to achieve so (Loerwald and Stemmann, 2016).

Importance of Accounting and finance functions, duties and roles:

Monitoring Earnings and Expenditure: accounting finance is key aspect in

enterprise that allow it to monitor the earnings and spending accrued or actually

incurred/earned in business. It is crucial for entity to classify the expenditures and monitor the

function. In the SKANSKA Corporation, administration employs accounting and finances

processes to monitor earnings as well as expenditures which contribute to enhance productivity

(Black, 2019).

Sound and effective business planning: finances and accounting processes are required

in the enterprise as they help to devise effective plans and tactics that will serve to improve the

functioning in competitive marketplace and to accomplish the targets. There is a significant

requirement of this in SKANSKA PLC to effectively accomplish the different administrative

tasks. In this context, administration emphasizes primarily on fund management, revenues,

business growth, the setting of targeted profitability and the determination of the stock

level which helps to gain competitive advantages.

Allocation of business resources: various activities are performed in the enterprise

thus it is necessary for managers to employ accounting and finance aspects that will enable them

business decisions by compiling financial and integral reports.

Financial accounting: It concerns the maintaining of accounting records for all

transactions, use of the double-entry accounting system and the preparation of final

statements that are sufficient for fulfilling the multiple governmental specifications for

legislative reporting, stock exchange and financial regulators. The financial accountant,

who will usually report to top management, is the individual accountable for this work in

most mid to large enterprises.

Supporting the business strategy and making financial policies: Finance manager is

accountable for making financial environment which supports financial and business

strategy. The right combination of shorter-term and longer-term finance and capital

resources ought to be made accessible to fulfil the organisation 's objective and have the

organisational agility required to take advantage of potential opportunities. All executives

have primary function to generate value, and the chief duty of finance officer is to allow

them to achieve so (Loerwald and Stemmann, 2016).

Importance of Accounting and finance functions, duties and roles:

Monitoring Earnings and Expenditure: accounting finance is key aspect in

enterprise that allow it to monitor the earnings and spending accrued or actually

incurred/earned in business. It is crucial for entity to classify the expenditures and monitor the

function. In the SKANSKA Corporation, administration employs accounting and finances

processes to monitor earnings as well as expenditures which contribute to enhance productivity

(Black, 2019).

Sound and effective business planning: finances and accounting processes are required

in the enterprise as they help to devise effective plans and tactics that will serve to improve the

functioning in competitive marketplace and to accomplish the targets. There is a significant

requirement of this in SKANSKA PLC to effectively accomplish the different administrative

tasks. In this context, administration emphasizes primarily on fund management, revenues,

business growth, the setting of targeted profitability and the determination of the stock

level which helps to gain competitive advantages.

Allocation of business resources: various activities are performed in the enterprise

thus it is necessary for managers to employ accounting and finance aspects that will enable them

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to manage business resources and allocate resources to such different activities/functions in order

to achieve the business objective. Managers of the SKANSKA PLC apply accounting and

finance data to recognize all accessible business resources and allocate them to

increase efficiency with optimal resource usages.

Action plan for Long-term objectives: the company seeks to expand and broaden its operations

to a broad level as well as to attain vision. pTo do same, manager are required to devise long-

term strategy. But long-term plan can be implemented in business by an effective action plan

which so they apply accounting and finance processes and extracted information for this. In

SKANSKA, managers use accounting and financial details to support their action plan

for achieving longer term objectives (Bouzguenda, 2018).

Managing and generating funds: to commence and continue operating an enterprise, funds are

essential thus business managers have to ascertain adequacy of funds in business as to operate

business functions effectively. Accounting and finance here in this case is vital for them as to

assess the exact requirement of funds, manage the flow of funds within business as well as

identifies the effective sources of funds. The administration of SKANSKA employs financial

and accounting processes to effective monitoring of funds, maintain adequate

liquidity position of company as well as recognise best alternative to raise funds when required

(Davis and Davis, 2019).

Revenue Management: This strategy is main initiatives initiated by finance department

for those relevant to money or cash equivalents. The sales control strategy includes amount of

liability that may be taken by the organisation at any given time frame or duration. Revenue

operations and administration are typically controlled by Assistant Finance Manager or Junior

Accountant, while Chief Financial Officer manages any element of FA. As a construction firm,

SKANSKA PLC should have adequate sales control to ensure that any construction project has

the anticipated revenue level. SKANSKA PLC would also require proper sales forecasting

methods to be reliable and less dependent on assumptions (dos Santos, Pires and Fernández,

2018).

Investment valuation method: this is technique developed by accounting and finance division,

it is a quite useful business method. Since it allows investor to determine the result

of investment, investor can recognize the appropriate choice among the options by

utilizing investment appraisal methodology. SKANSKA PLC is a well-known construction firm

to achieve the business objective. Managers of the SKANSKA PLC apply accounting and

finance data to recognize all accessible business resources and allocate them to

increase efficiency with optimal resource usages.

Action plan for Long-term objectives: the company seeks to expand and broaden its operations

to a broad level as well as to attain vision. pTo do same, manager are required to devise long-

term strategy. But long-term plan can be implemented in business by an effective action plan

which so they apply accounting and finance processes and extracted information for this. In

SKANSKA, managers use accounting and financial details to support their action plan

for achieving longer term objectives (Bouzguenda, 2018).

Managing and generating funds: to commence and continue operating an enterprise, funds are

essential thus business managers have to ascertain adequacy of funds in business as to operate

business functions effectively. Accounting and finance here in this case is vital for them as to

assess the exact requirement of funds, manage the flow of funds within business as well as

identifies the effective sources of funds. The administration of SKANSKA employs financial

and accounting processes to effective monitoring of funds, maintain adequate

liquidity position of company as well as recognise best alternative to raise funds when required

(Davis and Davis, 2019).

Revenue Management: This strategy is main initiatives initiated by finance department

for those relevant to money or cash equivalents. The sales control strategy includes amount of

liability that may be taken by the organisation at any given time frame or duration. Revenue

operations and administration are typically controlled by Assistant Finance Manager or Junior

Accountant, while Chief Financial Officer manages any element of FA. As a construction firm,

SKANSKA PLC should have adequate sales control to ensure that any construction project has

the anticipated revenue level. SKANSKA PLC would also require proper sales forecasting

methods to be reliable and less dependent on assumptions (dos Santos, Pires and Fernández,

2018).

Investment valuation method: this is technique developed by accounting and finance division,

it is a quite useful business method. Since it allows investor to determine the result

of investment, investor can recognize the appropriate choice among the options by

utilizing investment appraisal methodology. SKANSKA PLC is a well-known construction firm

which holds a broad investment account. In order to retain current investors and draw further

investors, accounting and finance division of SKANSKA must develop suitable investment

valuation strategies to draw the current investment entity along with potential investors to market

(Sapkauskiene and Orlovskij, 2017).

Establishing Accounting Policy and Procedures Manual: key duties of accounts and

finance division is the development of accounting policy that regulate all accounting

& finance transactions. Such policies will ensure that any transaction is carried out

internally externally throughout the sector. since such policies needs to be accepted by upper

executives, they are originally developed by accounting and finance division. Accounting policy

decisions are rules developed by accounting and finance division. Accounting practises are very

relevant for SKANSKA, as they can allow the company to maintain track of any sale.

Monitoring transactions is most important things to remember and handle, since losing trace of

even single transaction will disrupt the entire financial system of the company.

Budgeting: This is one of main foundations of every company. This has to be achieved

effectively, and the success of the company rests largely on how effectively budgets are being

created. Budgeting is a crucial feature of accounting and finance division since it holds a full list

of figures within the company. Finance department could review the figures and determine the

current state of the firm. Budgets allow customers to anticipate a vision of the future such that

the agency has to be productive enough to function appropriately. Budgeting is essential for all

larger or smaller companies, such that SKANSKA PLC, as a well-known large company,

requires considerably more budgeting for facing the challenges of competitiveness on market.

SKANSKA PLC. Has to determine the priorities to be set in accordance with existing market

assessments, along with status of the rival. Without adequate budgeting methods, accurate

planning is not feasible (Motylska-Kuzma, 2017).

Eradicating frauds: one of key tasks of accountants inside an company is to prevent

frauds and emphasize accountability in all transactions. It is impossible for upper management to

avoid theft on their own. Higher management is heavily reliant on accounting and finance

division for the avoidance of fraud. Since inflows and outflows are maintained by finance

department, department should be mainly accountable as greater responsibility brings significant

responsibilities. The larger the scale of the company, the greater workforce and the greater the

opportunity for bribery in the company. SKANSKA PLC is huge company, and it's much more

investors, accounting and finance division of SKANSKA must develop suitable investment

valuation strategies to draw the current investment entity along with potential investors to market

(Sapkauskiene and Orlovskij, 2017).

Establishing Accounting Policy and Procedures Manual: key duties of accounts and

finance division is the development of accounting policy that regulate all accounting

& finance transactions. Such policies will ensure that any transaction is carried out

internally externally throughout the sector. since such policies needs to be accepted by upper

executives, they are originally developed by accounting and finance division. Accounting policy

decisions are rules developed by accounting and finance division. Accounting practises are very

relevant for SKANSKA, as they can allow the company to maintain track of any sale.

Monitoring transactions is most important things to remember and handle, since losing trace of

even single transaction will disrupt the entire financial system of the company.

Budgeting: This is one of main foundations of every company. This has to be achieved

effectively, and the success of the company rests largely on how effectively budgets are being

created. Budgeting is a crucial feature of accounting and finance division since it holds a full list

of figures within the company. Finance department could review the figures and determine the

current state of the firm. Budgets allow customers to anticipate a vision of the future such that

the agency has to be productive enough to function appropriately. Budgeting is essential for all

larger or smaller companies, such that SKANSKA PLC, as a well-known large company,

requires considerably more budgeting for facing the challenges of competitiveness on market.

SKANSKA PLC. Has to determine the priorities to be set in accordance with existing market

assessments, along with status of the rival. Without adequate budgeting methods, accurate

planning is not feasible (Motylska-Kuzma, 2017).

Eradicating frauds: one of key tasks of accountants inside an company is to prevent

frauds and emphasize accountability in all transactions. It is impossible for upper management to

avoid theft on their own. Higher management is heavily reliant on accounting and finance

division for the avoidance of fraud. Since inflows and outflows are maintained by finance

department, department should be mainly accountable as greater responsibility brings significant

responsibilities. The larger the scale of the company, the greater workforce and the greater the

opportunity for bribery in the company. SKANSKA PLC is huge company, and it's much more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

difficult for a major corporation to cope with frauds. Accounting and financial divisions must

maintain a tight watch on accountability to support SKANSKA PLC eradicate fraud as a whole

(Oehler, Horn and Wedlich, 2018).

Accounting & finance division of SKANSKA PLC should consider functions and roles

described in order to remain an effective business entity. Finance Department as a whole has a

high degree of significance for strengthening of industry. That is why it has a larger duty to

coming up with right strategies and methods to ensuring that the company goal is achieved as

needed. Through the correct application of the strategies and practises proposed by accounting

and finance division, SKANSKA is more able to keep its role or raise it to whole new standard.

Accounting-and-finance practices are crucial for reviewing, maintaining and managing all

financial operations related to business as well as used to carry out all operations. In order to

establish and operate a business, it is important to have a clear comprehension of accounting and

finance aspects that take effect within business while functioning, such that they can be managed

appropriately.

The efficient accounting and finance division of SKANSKA PLC would carry lot of

advantages to the company. Department would be enabled to keep customers optimistic by

delivering the best image of financial stability. The Department would therefore be prepared to

have an acceptable compromise among risk and benefit value creation. Financially, it reflects an

acceptable balance between risk and benefit wealth creation. Financial management promotes a

structured and well-organized decision-making process for the group. SKANSKA PLC would

also have strategic edge as the group will be allowed to adapt efficiently to everything relating

to financial aspect. The total activities of department will function well, and one of crucial

aspects is flow of financing to cover the expenditures properly.

TASK 2

Calculation of of ratios for the company and comment on performance of company

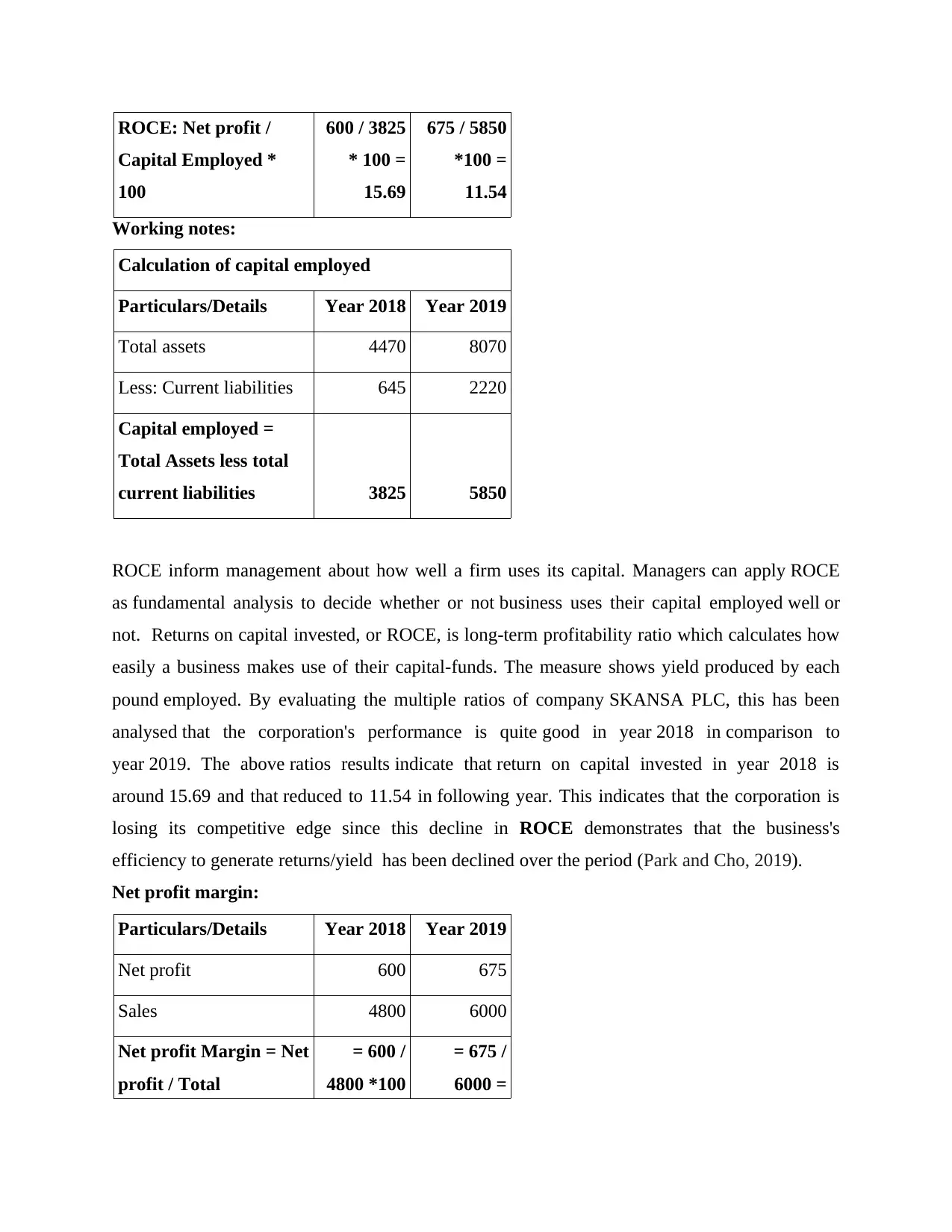

Return on capital employed:

Particulars/Details Year 2018 Year 2019

Net profits 600 675

Capital employed 3825 5850

maintain a tight watch on accountability to support SKANSKA PLC eradicate fraud as a whole

(Oehler, Horn and Wedlich, 2018).

Accounting & finance division of SKANSKA PLC should consider functions and roles

described in order to remain an effective business entity. Finance Department as a whole has a

high degree of significance for strengthening of industry. That is why it has a larger duty to

coming up with right strategies and methods to ensuring that the company goal is achieved as

needed. Through the correct application of the strategies and practises proposed by accounting

and finance division, SKANSKA is more able to keep its role or raise it to whole new standard.

Accounting-and-finance practices are crucial for reviewing, maintaining and managing all

financial operations related to business as well as used to carry out all operations. In order to

establish and operate a business, it is important to have a clear comprehension of accounting and

finance aspects that take effect within business while functioning, such that they can be managed

appropriately.

The efficient accounting and finance division of SKANSKA PLC would carry lot of

advantages to the company. Department would be enabled to keep customers optimistic by

delivering the best image of financial stability. The Department would therefore be prepared to

have an acceptable compromise among risk and benefit value creation. Financially, it reflects an

acceptable balance between risk and benefit wealth creation. Financial management promotes a

structured and well-organized decision-making process for the group. SKANSKA PLC would

also have strategic edge as the group will be allowed to adapt efficiently to everything relating

to financial aspect. The total activities of department will function well, and one of crucial

aspects is flow of financing to cover the expenditures properly.

TASK 2

Calculation of of ratios for the company and comment on performance of company

Return on capital employed:

Particulars/Details Year 2018 Year 2019

Net profits 600 675

Capital employed 3825 5850

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ROCE: Net profit /

Capital Employed *

100

600 / 3825

* 100 =

15.69

675 / 5850

*100 =

11.54

Working notes:

Calculation of capital employed

Particulars/Details Year 2018 Year 2019

Total assets 4470 8070

Less: Current liabilities 645 2220

Capital employed =

Total Assets less total

current liabilities 3825 5850

ROCE inform management about how well a firm uses its capital. Managers can apply ROCE

as fundamental analysis to decide whether or not business uses their capital employed well or

not. Returns on capital invested, or ROCE, is long-term profitability ratio which calculates how

easily a business makes use of their capital-funds. The measure shows yield produced by each

pound employed. By evaluating the multiple ratios of company SKANSA PLC, this has been

analysed that the corporation's performance is quite good in year 2018 in comparison to

year 2019. The above ratios results indicate that return on capital invested in year 2018 is

around 15.69 and that reduced to 11.54 in following year. This indicates that the corporation is

losing its competitive edge since this decline in ROCE demonstrates that the business's

efficiency to generate returns/yield has been declined over the period (Park and Cho, 2019).

Net profit margin:

Particulars/Details Year 2018 Year 2019

Net profit 600 675

Sales 4800 6000

Net profit Margin = Net

profit / Total

= 600 /

4800 *100

= 675 /

6000 =

Capital Employed *

100

600 / 3825

* 100 =

15.69

675 / 5850

*100 =

11.54

Working notes:

Calculation of capital employed

Particulars/Details Year 2018 Year 2019

Total assets 4470 8070

Less: Current liabilities 645 2220

Capital employed =

Total Assets less total

current liabilities 3825 5850

ROCE inform management about how well a firm uses its capital. Managers can apply ROCE

as fundamental analysis to decide whether or not business uses their capital employed well or

not. Returns on capital invested, or ROCE, is long-term profitability ratio which calculates how

easily a business makes use of their capital-funds. The measure shows yield produced by each

pound employed. By evaluating the multiple ratios of company SKANSA PLC, this has been

analysed that the corporation's performance is quite good in year 2018 in comparison to

year 2019. The above ratios results indicate that return on capital invested in year 2018 is

around 15.69 and that reduced to 11.54 in following year. This indicates that the corporation is

losing its competitive edge since this decline in ROCE demonstrates that the business's

efficiency to generate returns/yield has been declined over the period (Park and Cho, 2019).

Net profit margin:

Particulars/Details Year 2018 Year 2019

Net profit 600 675

Sales 4800 6000

Net profit Margin = Net

profit / Total

= 600 /

4800 *100

= 675 /

6000 =

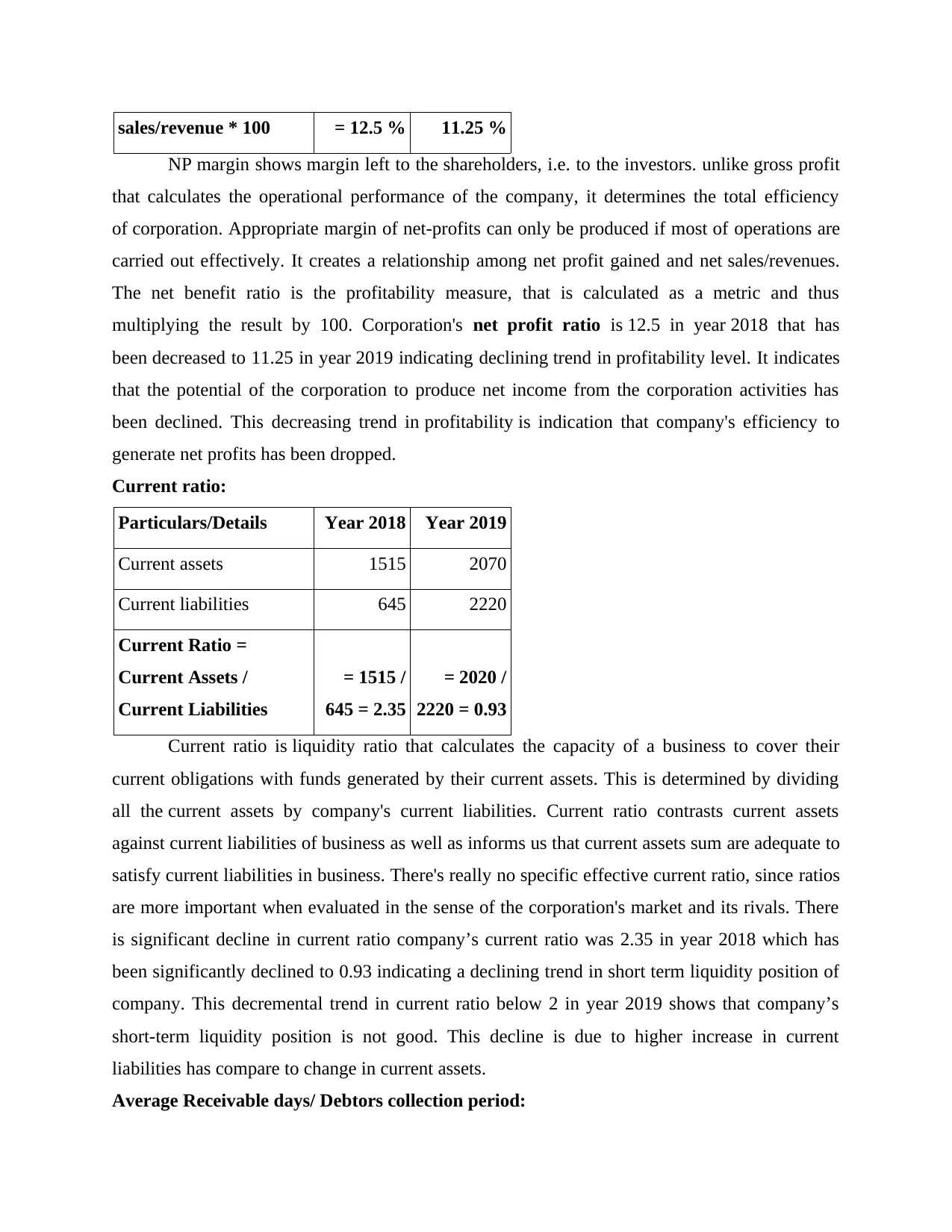

sales/revenue * 100 = 12.5 % 11.25 %

NP margin shows margin left to the shareholders, i.e. to the investors. unlike gross profit

that calculates the operational performance of the company, it determines the total efficiency

of corporation. Appropriate margin of net-profits can only be produced if most of operations are

carried out effectively. It creates a relationship among net profit gained and net sales/revenues.

The net benefit ratio is the profitability measure, that is calculated as a metric and thus

multiplying the result by 100. Corporation's net profit ratio is 12.5 in year 2018 that has

been decreased to 11.25 in year 2019 indicating declining trend in profitability level. It indicates

that the potential of the corporation to produce net income from the corporation activities has

been declined. This decreasing trend in profitability is indication that company's efficiency to

generate net profits has been dropped.

Current ratio:

Particulars/Details Year 2018 Year 2019

Current assets 1515 2070

Current liabilities 645 2220

Current Ratio =

Current Assets /

Current Liabilities

= 1515 /

645 = 2.35

= 2020 /

2220 = 0.93

Current ratio is liquidity ratio that calculates the capacity of a business to cover their

current obligations with funds generated by their current assets. This is determined by dividing

all the current assets by company's current liabilities. Current ratio contrasts current assets

against current liabilities of business as well as informs us that current assets sum are adequate to

satisfy current liabilities in business. There's really no specific effective current ratio, since ratios

are more important when evaluated in the sense of the corporation's market and its rivals. There

is significant decline in current ratio company’s current ratio was 2.35 in year 2018 which has

been significantly declined to 0.93 indicating a declining trend in short term liquidity position of

company. This decremental trend in current ratio below 2 in year 2019 shows that company’s

short-term liquidity position is not good. This decline is due to higher increase in current

liabilities has compare to change in current assets.

Average Receivable days/ Debtors collection period:

NP margin shows margin left to the shareholders, i.e. to the investors. unlike gross profit

that calculates the operational performance of the company, it determines the total efficiency

of corporation. Appropriate margin of net-profits can only be produced if most of operations are

carried out effectively. It creates a relationship among net profit gained and net sales/revenues.

The net benefit ratio is the profitability measure, that is calculated as a metric and thus

multiplying the result by 100. Corporation's net profit ratio is 12.5 in year 2018 that has

been decreased to 11.25 in year 2019 indicating declining trend in profitability level. It indicates

that the potential of the corporation to produce net income from the corporation activities has

been declined. This decreasing trend in profitability is indication that company's efficiency to

generate net profits has been dropped.

Current ratio:

Particulars/Details Year 2018 Year 2019

Current assets 1515 2070

Current liabilities 645 2220

Current Ratio =

Current Assets /

Current Liabilities

= 1515 /

645 = 2.35

= 2020 /

2220 = 0.93

Current ratio is liquidity ratio that calculates the capacity of a business to cover their

current obligations with funds generated by their current assets. This is determined by dividing

all the current assets by company's current liabilities. Current ratio contrasts current assets

against current liabilities of business as well as informs us that current assets sum are adequate to

satisfy current liabilities in business. There's really no specific effective current ratio, since ratios

are more important when evaluated in the sense of the corporation's market and its rivals. There

is significant decline in current ratio company’s current ratio was 2.35 in year 2018 which has

been significantly declined to 0.93 indicating a declining trend in short term liquidity position of

company. This decremental trend in current ratio below 2 in year 2019 shows that company’s

short-term liquidity position is not good. This decline is due to higher increase in current

liabilities has compare to change in current assets.

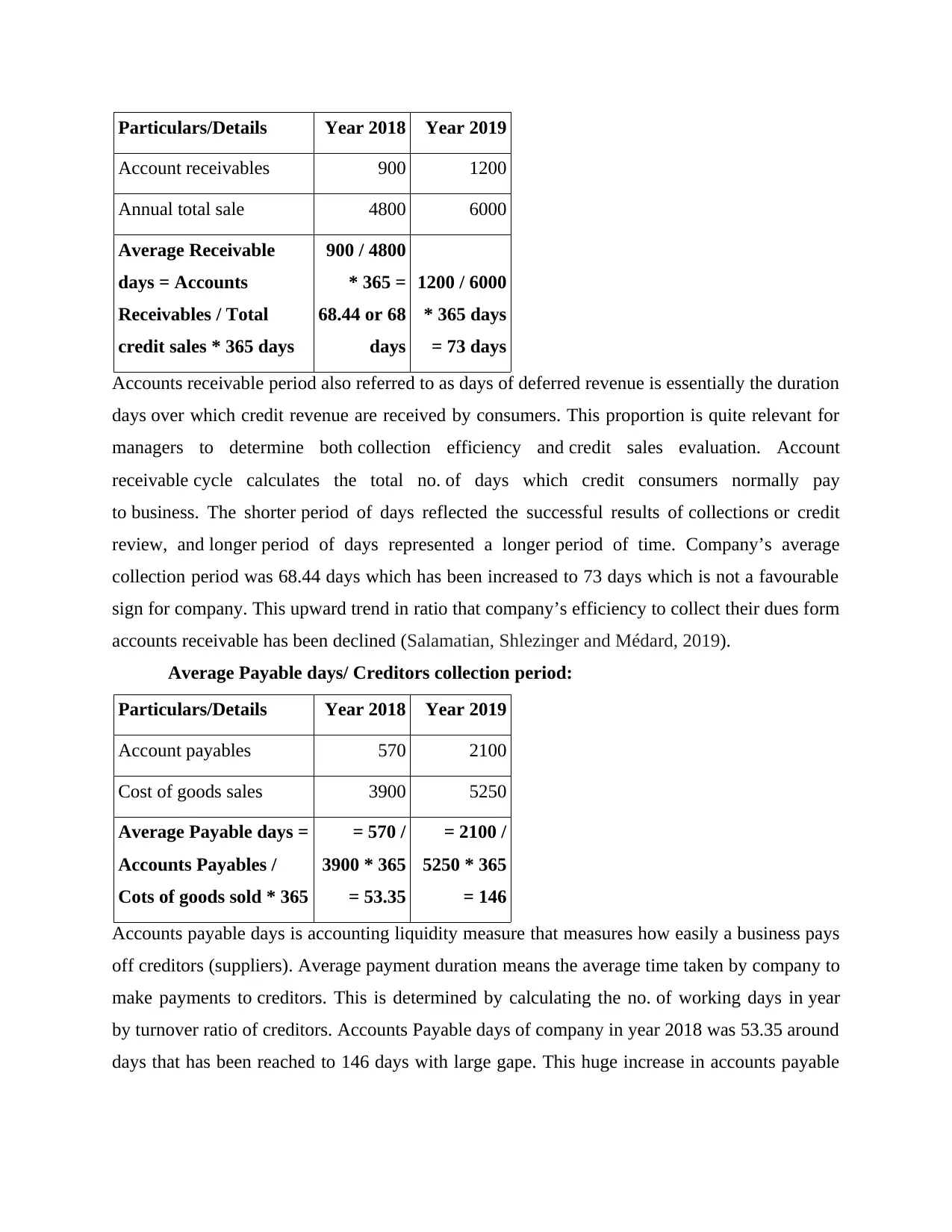

Average Receivable days/ Debtors collection period:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars/Details Year 2018 Year 2019

Account receivables 900 1200

Annual total sale 4800 6000

Average Receivable

days = Accounts

Receivables / Total

credit sales * 365 days

900 / 4800

* 365 =

68.44 or 68

days

1200 / 6000

* 365 days

= 73 days

Accounts receivable period also referred to as days of deferred revenue is essentially the duration

days over which credit revenue are received by consumers. This proportion is quite relevant for

managers to determine both collection efficiency and credit sales evaluation. Account

receivable cycle calculates the total no. of days which credit consumers normally pay

to business. The shorter period of days reflected the successful results of collections or credit

review, and longer period of days represented a longer period of time. Company’s average

collection period was 68.44 days which has been increased to 73 days which is not a favourable

sign for company. This upward trend in ratio that company’s efficiency to collect their dues form

accounts receivable has been declined (Salamatian, Shlezinger and Médard, 2019).

Average Payable days/ Creditors collection period:

Particulars/Details Year 2018 Year 2019

Account payables 570 2100

Cost of goods sales 3900 5250

Average Payable days =

Accounts Payables /

Cots of goods sold * 365

= 570 /

3900 * 365

= 53.35

= 2100 /

5250 * 365

= 146

Accounts payable days is accounting liquidity measure that measures how easily a business pays

off creditors (suppliers). Average payment duration means the average time taken by company to

make payments to creditors. This is determined by calculating the no. of working days in year

by turnover ratio of creditors. Accounts Payable days of company in year 2018 was 53.35 around

days that has been reached to 146 days with large gape. This huge increase in accounts payable

Account receivables 900 1200

Annual total sale 4800 6000

Average Receivable

days = Accounts

Receivables / Total

credit sales * 365 days

900 / 4800

* 365 =

68.44 or 68

days

1200 / 6000

* 365 days

= 73 days

Accounts receivable period also referred to as days of deferred revenue is essentially the duration

days over which credit revenue are received by consumers. This proportion is quite relevant for

managers to determine both collection efficiency and credit sales evaluation. Account

receivable cycle calculates the total no. of days which credit consumers normally pay

to business. The shorter period of days reflected the successful results of collections or credit

review, and longer period of days represented a longer period of time. Company’s average

collection period was 68.44 days which has been increased to 73 days which is not a favourable

sign for company. This upward trend in ratio that company’s efficiency to collect their dues form

accounts receivable has been declined (Salamatian, Shlezinger and Médard, 2019).

Average Payable days/ Creditors collection period:

Particulars/Details Year 2018 Year 2019

Account payables 570 2100

Cost of goods sales 3900 5250

Average Payable days =

Accounts Payables /

Cots of goods sold * 365

= 570 /

3900 * 365

= 53.35

= 2100 /

5250 * 365

= 146

Accounts payable days is accounting liquidity measure that measures how easily a business pays

off creditors (suppliers). Average payment duration means the average time taken by company to

make payments to creditors. This is determined by calculating the no. of working days in year

by turnover ratio of creditors. Accounts Payable days of company in year 2018 was 53.35 around

days that has been reached to 146 days with large gape. This huge increase in accounts payable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

days indicates that company’s shorter term liquidity position is not good as company is delaying

in payments to its suppliers.

Overall analysis of all the ratios shows that company’s performance in year 2019 has

been declined in comparison to year 2018. Company’s profitability performance has been

declined over the period as well as there is also decline in ROCE, these points out the decline in

financial performance of company.

CONCLUSION

It has been inferred from above project study that process of financial decision-making

is crucial factor that must be regarded by all companies as it promotes the effective

accomplishments of both long-term and shorter-term targets. Both accounting & finance tasks,

responsibilities and requirements are quite relevant to all enterprises, as they can lead

to successful execution of business and operating activities. When attempting to

evaluate financial state of the organisation, it is quite useful for companies to consider the

evaluation of financial ratio. The various measures that may be employed to assess the financial

condition of the firm are the ROCE, the NP margin, the current ratio, the receivable collection

period and the repayment duration.

in payments to its suppliers.

Overall analysis of all the ratios shows that company’s performance in year 2019 has

been declined in comparison to year 2018. Company’s profitability performance has been

declined over the period as well as there is also decline in ROCE, these points out the decline in

financial performance of company.

CONCLUSION

It has been inferred from above project study that process of financial decision-making

is crucial factor that must be regarded by all companies as it promotes the effective

accomplishments of both long-term and shorter-term targets. Both accounting & finance tasks,

responsibilities and requirements are quite relevant to all enterprises, as they can lead

to successful execution of business and operating activities. When attempting to

evaluate financial state of the organisation, it is quite useful for companies to consider the

evaluation of financial ratio. The various measures that may be employed to assess the financial

condition of the firm are the ROCE, the NP margin, the current ratio, the receivable collection

period and the repayment duration.

REFERENCES

Books and Journals:

Valaskova, K., Bartosova, V. and Kubala, P., 2019. Behavioural aspects of the financial

decision-making. Organizacija, 52(1), pp.22-31.

Kim, J., Gutter, M.S. and Spangler, T., 2017. Review of family financial decision making:

Suggestions for future research and implications for financial education. Journal of

Financial Counseling and Planning, 28(2), pp.253-267.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International handbook of

financial literacy (pp. 25-38). Springer, Singapore.

Rai, D. and Lin, C.W.W., 2019. The influence of implicit self-theories on consumer financial

decision making. Journal of Business Research, 95, pp.316-325.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Bouzguenda, K., 2018. Emotional intelligence and financial decision making: Are we talking

about a paradigmatic shift or a change in practices?. Research in International Business

and Finance. 44. pp.273-284.

Davis, C. E. and Davis, E., 2019. Managerial accounting. John Wiley & Sons.

dos Santos, J.P.F., Pires, A.M.M. and Fernández, P.O., 2018. The importance to financial

information in the decision-making process in company’s family structure. Contaduría

y administración, 63(2), p.12.

Sapkauskiene, A. and Orlovskij, S., 2017. The usefulness of fair value estimates for financial

decision making–a literature review. Zeszyty Teoretyczne Rachunkowości, (93 (149)),

pp.163-173.

Motylska-Kuzma, A., 2017. The financial decisions of family businesses. Journal of Family

Business Management.

Oehler, A., Horn, M. and Wedlich, F., 2018. Young adults’ subjective and objective risk attitude

in financial decision making. Review of Behavioral Finance.

Oktyawati, D. and Fajri, F. A., 2019. The influence of accounting internal control and human

resources capacity on reliability and timeliness of regional government financial

reporting (a study in Special Region of Yogyakarta Province). Jurnal Perspektif

Pembiayaan Dan Pembangunan Daerah. 6(4). pp.525-534.

Park, I. and Cho, S., 2019. The influence of number line estimation precision and numeracy on

risky financial decision making. International Journal of Psychology. 54(4). pp.530-

538.

Salamatian, S., Shlezinger, N.,and Médard, M., 2019, July. Task-based quantization for

recovering quadratic functions using principal inertia components. In 2019 IEEE

International Symposium on Information Theory (ISIT) (pp. 390-394). IEEE.

Books and Journals:

Valaskova, K., Bartosova, V. and Kubala, P., 2019. Behavioural aspects of the financial

decision-making. Organizacija, 52(1), pp.22-31.

Kim, J., Gutter, M.S. and Spangler, T., 2017. Review of family financial decision making:

Suggestions for future research and implications for financial education. Journal of

Financial Counseling and Planning, 28(2), pp.253-267.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International handbook of

financial literacy (pp. 25-38). Springer, Singapore.

Rai, D. and Lin, C.W.W., 2019. The influence of implicit self-theories on consumer financial

decision making. Journal of Business Research, 95, pp.316-325.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Bouzguenda, K., 2018. Emotional intelligence and financial decision making: Are we talking

about a paradigmatic shift or a change in practices?. Research in International Business

and Finance. 44. pp.273-284.

Davis, C. E. and Davis, E., 2019. Managerial accounting. John Wiley & Sons.

dos Santos, J.P.F., Pires, A.M.M. and Fernández, P.O., 2018. The importance to financial

information in the decision-making process in company’s family structure. Contaduría

y administración, 63(2), p.12.

Sapkauskiene, A. and Orlovskij, S., 2017. The usefulness of fair value estimates for financial

decision making–a literature review. Zeszyty Teoretyczne Rachunkowości, (93 (149)),

pp.163-173.

Motylska-Kuzma, A., 2017. The financial decisions of family businesses. Journal of Family

Business Management.

Oehler, A., Horn, M. and Wedlich, F., 2018. Young adults’ subjective and objective risk attitude

in financial decision making. Review of Behavioral Finance.

Oktyawati, D. and Fajri, F. A., 2019. The influence of accounting internal control and human

resources capacity on reliability and timeliness of regional government financial

reporting (a study in Special Region of Yogyakarta Province). Jurnal Perspektif

Pembiayaan Dan Pembangunan Daerah. 6(4). pp.525-534.

Park, I. and Cho, S., 2019. The influence of number line estimation precision and numeracy on

risky financial decision making. International Journal of Psychology. 54(4). pp.530-

538.

Salamatian, S., Shlezinger, N.,and Médard, M., 2019, July. Task-based quantization for

recovering quadratic functions using principal inertia components. In 2019 IEEE

International Symposium on Information Theory (ISIT) (pp. 390-394). IEEE.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.