Financial Decision Making Report: Analyzing SKANSKA PLC Performance

VerifiedAdded on 2022/12/09

|14

|3758

|111

Report

AI Summary

This report provides a detailed analysis of financial decision-making at SKANSKA PLC, a civil building firm. The introduction emphasizes the importance of efficient financial decision-making and its impact on organizational success. Task 1 explores the roles and duties of accounting and finance functions, including financial accounting, financial statement analysis, historical cost accounting, standard costing, and budgetary management. The report highlights the significance of these functions in planning, reporting, and managing investments and cash flow. Task 2 assesses SKANSKA PLC's performance using key financial ratios such as Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, Debtors Collection Period, and Creditors Collection Period. The analysis reveals trends in these ratios and comments on the company's financial health and efficiency. The report concludes with a summary of findings and references to support the analysis.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC............................3

TASK 2..........................................................................................................................................................7

Assessing key ratios of SKANSKA PLC evaluates organization’s performance:...................................7

Comment on performance of SKANSKA PLC, based on computed ratios:............................................8

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................12

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC............................3

TASK 2..........................................................................................................................................................7

Assessing key ratios of SKANSKA PLC evaluates organization’s performance:...................................7

Comment on performance of SKANSKA PLC, based on computed ratios:............................................8

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Decision making is one of the most important aspects of any organisation, and it is largely

dependent on management. The word "financial decision making" refers to the mechanism with

which a corporate accounting officer determines necessity resources in necessary to undertake

out additional operations and allocates funds to various activities (Abdel-Basset, Sallam and

Elhoseny, 2020). This decision-making process must be carried out efficiently, as any mistake

could result in a slew of problems in the future. The project estimate is focused on SKANSKA

plc, which was established in 1778 and is headquarters in the United Kingdom. Essentially, it is a

civil building firm that undertakes major projects. With better control of their affairs, the

organisation employs a variety of management accounting methods. The report is divided into

two sections: Task one and Task two. The first job is to gather knowledge well about accounting

& financial divisions' roles and duties. Various sorts of management accounting approaches are

discussed in the article, as well as their functions in effective organising and implementing. A

corporation's finance and business departments play a critical role in the careful handling of its

financial capital. Essentially, a corporation's success is determined by how effectively the finance

and accounting departments conduct their duties. Both divisions have distinct positions and

responsibilities. Accounting and finance divisions, on the other hand, are inextricably linked.

When it comes to gathering financial reports and filing accurate financial statements at the start

of the budget year, the finance department plays a vital role. Although the accounting department

is responsible for recording all financial statements in a structured way such that the finance

department can receive the details it requires.

TASK 1

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC.

The term management accounting (MA) refers to the process of providing financial and

non-financial information to management so that they can plan ahead. There are a number of MA

techniques that are particularly applicable to companies, including:

Financial accounting is a financial tool that is linked to the economic work shift and is

focused on forecasting projected sales and expenditures. Financial planning may be useful in

some cases, including in the SKANSKA industry, since it allows them to effectively manage

Decision making is one of the most important aspects of any organisation, and it is largely

dependent on management. The word "financial decision making" refers to the mechanism with

which a corporate accounting officer determines necessity resources in necessary to undertake

out additional operations and allocates funds to various activities (Abdel-Basset, Sallam and

Elhoseny, 2020). This decision-making process must be carried out efficiently, as any mistake

could result in a slew of problems in the future. The project estimate is focused on SKANSKA

plc, which was established in 1778 and is headquarters in the United Kingdom. Essentially, it is a

civil building firm that undertakes major projects. With better control of their affairs, the

organisation employs a variety of management accounting methods. The report is divided into

two sections: Task one and Task two. The first job is to gather knowledge well about accounting

& financial divisions' roles and duties. Various sorts of management accounting approaches are

discussed in the article, as well as their functions in effective organising and implementing. A

corporation's finance and business departments play a critical role in the careful handling of its

financial capital. Essentially, a corporation's success is determined by how effectively the finance

and accounting departments conduct their duties. Both divisions have distinct positions and

responsibilities. Accounting and finance divisions, on the other hand, are inextricably linked.

When it comes to gathering financial reports and filing accurate financial statements at the start

of the budget year, the finance department plays a vital role. Although the accounting department

is responsible for recording all financial statements in a structured way such that the finance

department can receive the details it requires.

TASK 1

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC.

The term management accounting (MA) refers to the process of providing financial and

non-financial information to management so that they can plan ahead. There are a number of MA

techniques that are particularly applicable to companies, including:

Financial accounting is a financial tool that is linked to the economic work shift and is

focused on forecasting projected sales and expenditures. Financial planning may be useful in

some cases, including in the SKANSKA industry, since it allows them to effectively manage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their resources. They would then be able to better allocate the money to the different types of

operations as a result of this (Li and Chapman, 2020).

Financial statement analysis consists of a variety of records such as a tax estimate, a

balance sheet, a cash flow statement, a ratio summary, and so on. The analysis of such business

statements in depth may be helpful in determining a company's current status. Financial

statements, much as in the selected SKANSKA business, are useful for determining their current

position. There are mentioned roles and duties of both department of accounting and finance

such as:

Historical cost accounting: According to commonly agreed accounting standards, historical

cost is a type of accounting that is used for money. The value of the assets should be measured as

per the upfront cost, although in the company SKANSKA above.

Standard costing can be identified as either a costing system for estimating the potential

costs of various activities. Normal costing is the name given to this method of cost accounting.

As in the case of the SKANSKA group, money advisors should use this costing approach to

accurately calculate potential costs of manufacturing activities so that real costs can be compared

to the forecast (Wadesango and Ncube, 2020).

Budgetary management refers to the extension of budgetary forecasting to the analysis of

an entity's financial statements. They schedule expenditures including such cash forecasts,

administrative expenditures, and so on to manage the financial performance under the

SKANSKA Company listed above.

Functions

Reporting feature: This function involves financial reporting by a firm's accounting

department in addition to supporting higher authority in decision-making decisions using

organised financial details, resulting in more efficient decisions to be made in the time allocated.

Improving financial reporting at SKANSKA PLC is critical in order to encourage healthy

decision-making by leadership for the organization's long success.

Investment position: In terms of controlling the appropriate income streams accessible

to an organisation, the financing commission's investments role is required for the effectiveness

operations as a result of this (Li and Chapman, 2020).

Financial statement analysis consists of a variety of records such as a tax estimate, a

balance sheet, a cash flow statement, a ratio summary, and so on. The analysis of such business

statements in depth may be helpful in determining a company's current status. Financial

statements, much as in the selected SKANSKA business, are useful for determining their current

position. There are mentioned roles and duties of both department of accounting and finance

such as:

Historical cost accounting: According to commonly agreed accounting standards, historical

cost is a type of accounting that is used for money. The value of the assets should be measured as

per the upfront cost, although in the company SKANSKA above.

Standard costing can be identified as either a costing system for estimating the potential

costs of various activities. Normal costing is the name given to this method of cost accounting.

As in the case of the SKANSKA group, money advisors should use this costing approach to

accurately calculate potential costs of manufacturing activities so that real costs can be compared

to the forecast (Wadesango and Ncube, 2020).

Budgetary management refers to the extension of budgetary forecasting to the analysis of

an entity's financial statements. They schedule expenditures including such cash forecasts,

administrative expenditures, and so on to manage the financial performance under the

SKANSKA Company listed above.

Functions

Reporting feature: This function involves financial reporting by a firm's accounting

department in addition to supporting higher authority in decision-making decisions using

organised financial details, resulting in more efficient decisions to be made in the time allocated.

Improving financial reporting at SKANSKA PLC is critical in order to encourage healthy

decision-making by leadership for the organization's long success.

Investment position: In terms of controlling the appropriate income streams accessible

to an organisation, the financing commission's investments role is required for the effectiveness

of expenditure initiatives. In order for a business to increase its average lifespan, profitability,

and eventually succeed, it is important to decide the most appropriate and effective investment

plan.

Working capital is an indicator of day-to-day corporate transactions that are part of ongoing

activities. To maintain a consistent performance of the economy, it is important to successfully

manage a company's capital spending. SKANSKA PLC needs to improve its financial

performance system so that it can make more integral part of the management assessments. A

further task of the finance department is to monitor funding decisions so that the company can

identify established financial resources using the most appropriate financing approach to produce

the best results for its success (Meredith, Blake and Kerr, 2020).

Roles and duties

Predictions and financial planning: One of the most important responsibilities of the

finance department is to both plan appropriate strategies and identify deficiencies or other

practises that lead to cost incompetence and diminishing margins in an enterprise. Financial

planning supports a company in a lot of areas, but it's a critical aspect that can be carefully

prepared so that cost-effective plans can be adopted and the company's profitability can be

enhanced. At SKANSKA PLC, resource allocation activities are prioritised because they are the

basis for an organization's strategic growth and advancement needs, as well as promoting good

and efficient technological practises.

Cash flow management: The finance office is responsible for effectively handling sales

and expenditures in order to improve business pivotal impact and capital growth, allowing

activities to move properly. As a result, the financial activities of SKANSKA PLC must be

conducted out in the same manner that profits and expenditures are properly mirrored (Ahmad,

Susanti and Mukhibad, 2020).

Payroll: One of the most important responsibilities of the finance department is to

adequate support strategies and identifies weaknesses and other practises that contribute to cost

inefficiency and diminishing profitability in an enterprise. Budgeting helps an enterprise in a

multitude of areas, but it's a critical aspect that can be carefully prepared in order to execute and

develop expense initiatives.

and eventually succeed, it is important to decide the most appropriate and effective investment

plan.

Working capital is an indicator of day-to-day corporate transactions that are part of ongoing

activities. To maintain a consistent performance of the economy, it is important to successfully

manage a company's capital spending. SKANSKA PLC needs to improve its financial

performance system so that it can make more integral part of the management assessments. A

further task of the finance department is to monitor funding decisions so that the company can

identify established financial resources using the most appropriate financing approach to produce

the best results for its success (Meredith, Blake and Kerr, 2020).

Roles and duties

Predictions and financial planning: One of the most important responsibilities of the

finance department is to both plan appropriate strategies and identify deficiencies or other

practises that lead to cost incompetence and diminishing margins in an enterprise. Financial

planning supports a company in a lot of areas, but it's a critical aspect that can be carefully

prepared so that cost-effective plans can be adopted and the company's profitability can be

enhanced. At SKANSKA PLC, resource allocation activities are prioritised because they are the

basis for an organization's strategic growth and advancement needs, as well as promoting good

and efficient technological practises.

Cash flow management: The finance office is responsible for effectively handling sales

and expenditures in order to improve business pivotal impact and capital growth, allowing

activities to move properly. As a result, the financial activities of SKANSKA PLC must be

conducted out in the same manner that profits and expenditures are properly mirrored (Ahmad,

Susanti and Mukhibad, 2020).

Payroll: One of the most important responsibilities of the finance department is to

adequate support strategies and identifies weaknesses and other practises that contribute to cost

inefficiency and diminishing profitability in an enterprise. Budgeting helps an enterprise in a

multitude of areas, but it's a critical aspect that can be carefully prepared in order to execute and

develop expense initiatives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Critical analysis

The above-mentioned MA techniques are critical for companies because they aid in the

correct presentation of financial as well as non information. The following is how the importance

of such approaches is defined:

Output measurement- These techniques are helpful in measuring the true outcomes of a

company's activities. It may be useful to compare actual costs with expected costs from the

above SKANSKA market, such as cost accounting technique. If the actual cost is lower, the

impact on the corporation's financial statements would be important.

Enhance market productivity- A key feature of these approaches is that they are good at

improving organisational success. That's how methodologies like financial forecasts will help

businesses perform better. These techniques are useful in SKANSKA's industry for improving

the efficiency of their various manufacturing activities (Ahmed, Noreen, Ramakrishnan and

Abdullah, 2021).

The above-mentioned advantages are universal to all, and in addition to these advantages,

these methods play a particular function, such as:

• Importance in organising MA methods are crucial for effective scheduling. It's partially

because a wide range of techniques, including such managerial accounting and distribution

benefits, are accessible. In the basis of these strategies, businesses can make reliable predictions

and accurately compile financial statements. They might use MA approaches to formulate their

financial plan, much like the SKANSKA Corporation. Abovementioned advantages are universal

to all, and in addition to these advantages, these approaches play a particular function, including

such:

• Importance in organising MA methods are crucial for effective scheduling. It's partially

because a wide range of techniques, including such managerial accounting and distribution

benefits, are accessible. In the basis of these strategies, businesses can make reliable predictions

and accurately compile financial statements. They might use MA approaches to formulate their

financial plan, much like the SKANSKA Corporation. They may also collect important expense

The above-mentioned MA techniques are critical for companies because they aid in the

correct presentation of financial as well as non information. The following is how the importance

of such approaches is defined:

Output measurement- These techniques are helpful in measuring the true outcomes of a

company's activities. It may be useful to compare actual costs with expected costs from the

above SKANSKA market, such as cost accounting technique. If the actual cost is lower, the

impact on the corporation's financial statements would be important.

Enhance market productivity- A key feature of these approaches is that they are good at

improving organisational success. That's how methodologies like financial forecasts will help

businesses perform better. These techniques are useful in SKANSKA's industry for improving

the efficiency of their various manufacturing activities (Ahmed, Noreen, Ramakrishnan and

Abdullah, 2021).

The above-mentioned advantages are universal to all, and in addition to these advantages,

these methods play a particular function, such as:

• Importance in organising MA methods are crucial for effective scheduling. It's partially

because a wide range of techniques, including such managerial accounting and distribution

benefits, are accessible. In the basis of these strategies, businesses can make reliable predictions

and accurately compile financial statements. They might use MA approaches to formulate their

financial plan, much like the SKANSKA Corporation. Abovementioned advantages are universal

to all, and in addition to these advantages, these approaches play a particular function, including

such:

• Importance in organising MA methods are crucial for effective scheduling. It's partially

because a wide range of techniques, including such managerial accounting and distribution

benefits, are accessible. In the basis of these strategies, businesses can make reliable predictions

and accurately compile financial statements. They might use MA approaches to formulate their

financial plan, much like the SKANSKA Corporation. They may also collect important expense

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and revenue data that might contribute to improved preparation for the next accounting period

(Camerer, 2020).

These are some of the potential implications of accounting management techniques in the

SKANSKA market. Such accounting techniques can play a crucial role for them in addition to its

effects on increasing their businesses.

TASK 2

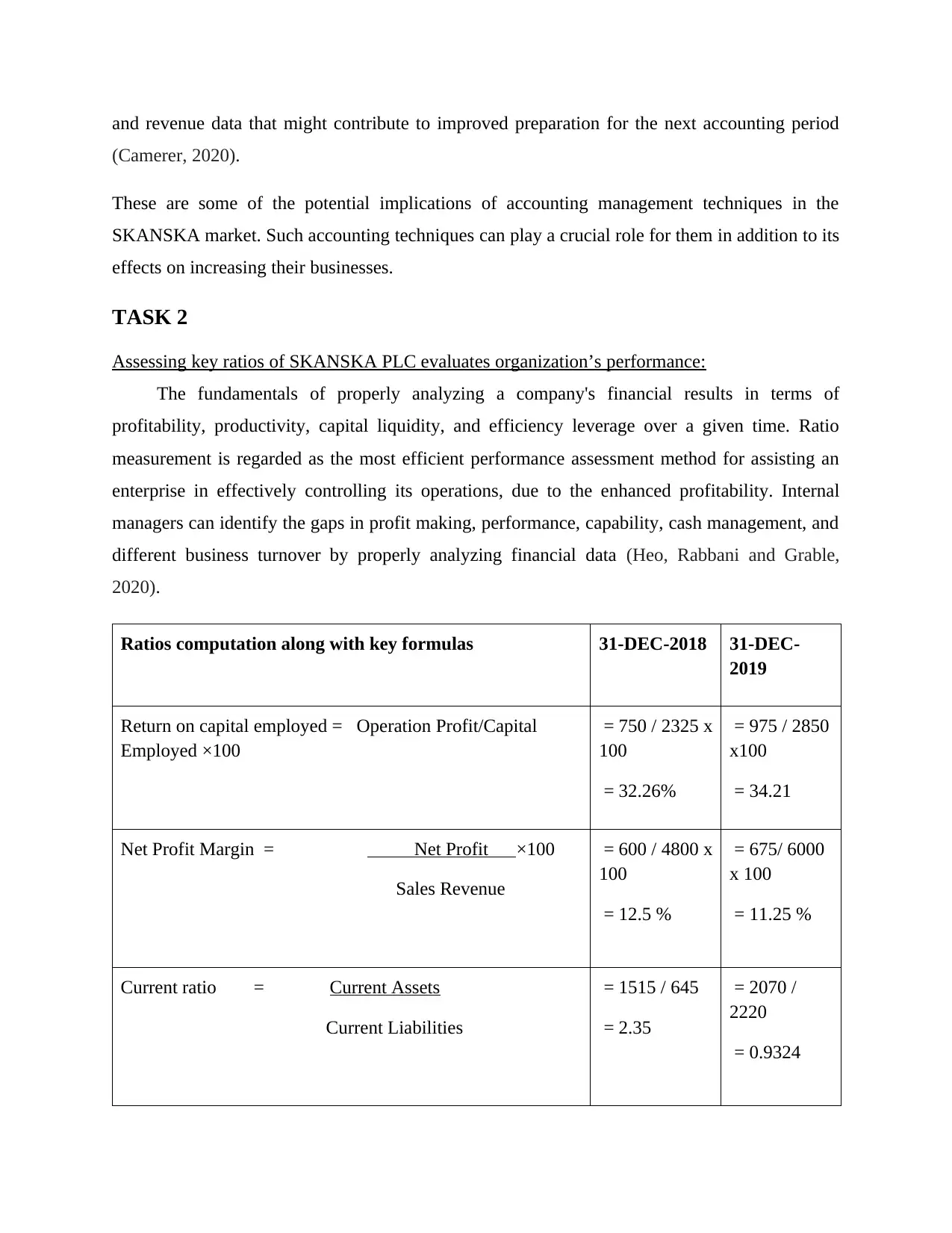

Assessing key ratios of SKANSKA PLC evaluates organization’s performance:

The fundamentals of properly analyzing a company's financial results in terms of

profitability, productivity, capital liquidity, and efficiency leverage over a given time. Ratio

measurement is regarded as the most efficient performance assessment method for assisting an

enterprise in effectively controlling its operations, due to the enhanced profitability. Internal

managers can identify the gaps in profit making, performance, capability, cash management, and

different business turnover by properly analyzing financial data (Heo, Rabbani and Grable,

2020).

Ratios computation along with key formulas 31-DEC-2018 31-DEC-

2019

Return on capital employed = Operation Profit/Capital

Employed ×100

= 750 / 2325 x

100

= 32.26%

= 975 / 2850

x100

= 34.21

Net Profit Margin = Net Profit ×100

Sales Revenue

= 600 / 4800 x

100

= 12.5 %

= 675/ 6000

x 100

= 11.25 %

Current ratio = Current Assets

Current Liabilities

= 1515 / 645

= 2.35

= 2070 /

2220

= 0.9324

(Camerer, 2020).

These are some of the potential implications of accounting management techniques in the

SKANSKA market. Such accounting techniques can play a crucial role for them in addition to its

effects on increasing their businesses.

TASK 2

Assessing key ratios of SKANSKA PLC evaluates organization’s performance:

The fundamentals of properly analyzing a company's financial results in terms of

profitability, productivity, capital liquidity, and efficiency leverage over a given time. Ratio

measurement is regarded as the most efficient performance assessment method for assisting an

enterprise in effectively controlling its operations, due to the enhanced profitability. Internal

managers can identify the gaps in profit making, performance, capability, cash management, and

different business turnover by properly analyzing financial data (Heo, Rabbani and Grable,

2020).

Ratios computation along with key formulas 31-DEC-2018 31-DEC-

2019

Return on capital employed = Operation Profit/Capital

Employed ×100

= 750 / 2325 x

100

= 32.26%

= 975 / 2850

x100

= 34.21

Net Profit Margin = Net Profit ×100

Sales Revenue

= 600 / 4800 x

100

= 12.5 %

= 675/ 6000

x 100

= 11.25 %

Current ratio = Current Assets

Current Liabilities

= 1515 / 645

= 2.35

= 2070 /

2220

= 0.9324

Debtors collection period = Trade Receivable ×365

Credit Sales

= 900 / 4800 x

365

= 68.43

= 68 Days

= 1200/

6000 x 365

= 73 days

Creditors collection period = Trade Payables ×365

Credit Purchases

= 570 / 4800 x

365

= 43.34

= 43 Days

= 2100 /

6000 x 365

= 127.75

= 128 Days

Comment on performance of SKANSKA PLC, based on computed ratios:

Return on capital employed: ROCE is a financial ratio that measures the true

performance and efficiency of a company's overall capital funds. A higher ROCE would indicate

a much more effective use of overall working investment capital; the ROCE would be higher

than the cost of capital. When this isn't the case, the company is less effective and doesn't

provide enough money for its owners. The calculation of ROCE is a useful method for

comparing earnings through companies based on the amount of capital spent. Focusing solely on

EBIT is insufficient to determine which company is profitable. Investors must examine

portfolios and calculate ROCE (Marqués, García and Sánchez, 2020). For calculating the

business's future profits due to different existing debts and expenses, most people find ROCE to

be a more reliable tool than ROE.

As previously stated, Skanska Plc's ROCE ratio was 32.26 percent in 2018 and 34.21

percent in 2019, indicating an upward trend in the ROCE. A high Roe indicates that a pound of

capital invested in the firm produces more profits. A higher percent ROCE is advantageous

because it indicates that the entity generates more revenue per pound of investment capital. A

low yield is associated with a lower ROCE percentage. A company with less resources but the

same earning as its competitors would see a higher return on the total amount of money spent. As

a result, in the case of Skanska Plc, such an improvement means that the company's ability to

generate a return on total capital invested has increased over time.

Credit Sales

= 900 / 4800 x

365

= 68.43

= 68 Days

= 1200/

6000 x 365

= 73 days

Creditors collection period = Trade Payables ×365

Credit Purchases

= 570 / 4800 x

365

= 43.34

= 43 Days

= 2100 /

6000 x 365

= 127.75

= 128 Days

Comment on performance of SKANSKA PLC, based on computed ratios:

Return on capital employed: ROCE is a financial ratio that measures the true

performance and efficiency of a company's overall capital funds. A higher ROCE would indicate

a much more effective use of overall working investment capital; the ROCE would be higher

than the cost of capital. When this isn't the case, the company is less effective and doesn't

provide enough money for its owners. The calculation of ROCE is a useful method for

comparing earnings through companies based on the amount of capital spent. Focusing solely on

EBIT is insufficient to determine which company is profitable. Investors must examine

portfolios and calculate ROCE (Marqués, García and Sánchez, 2020). For calculating the

business's future profits due to different existing debts and expenses, most people find ROCE to

be a more reliable tool than ROE.

As previously stated, Skanska Plc's ROCE ratio was 32.26 percent in 2018 and 34.21

percent in 2019, indicating an upward trend in the ROCE. A high Roe indicates that a pound of

capital invested in the firm produces more profits. A higher percent ROCE is advantageous

because it indicates that the entity generates more revenue per pound of investment capital. A

low yield is associated with a lower ROCE percentage. A company with less resources but the

same earning as its competitors would see a higher return on the total amount of money spent. As

a result, in the case of Skanska Plc, such an improvement means that the company's ability to

generate a return on total capital invested has increased over time.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net margin ratio: The net margin of a company measures how successful it is to make a

profit on a pound of sales. This is one of the most important corporate profitability. Both factors

that have an effect on an enterprise's profitability level, either under administrative management

or not, are included in net margin. The higher the figure, the more effective the business

company is at managing costs. In this regard, based on an analysis of Skanska Plc's ratios, it was

discovered that the firm's total ratio margin in 2019 was just 11, 25 percent, down from 12,5

percent in 2018, due to a slight fall in the gross NP percentage. This decrease in net profit margin

shows that Skanska Plc's real success in converting total sales into income has deteriorated over

the reported time span. The company should focus on this factor in small amounts to work

properly. The revenue value of this company should be enhanced, while the gross business

expenditure should be minimised (Zulaihati, Susanti and Widyastuti, 2020).

Current ratio: The current ratio is a big short-run financial leverage that is used to

determine a company's total leverage state when looking at the relationship between all current

assets and current liabilities. In layman's terms, it's a strategy for determining but whether or not

the company's total assets balance will cover all of its current liabilities. This ratio is used not

only to assess liquidity problems, and also to ultimately determine how working resources can be

used. Whether this ratio is greater than 2, the company's financial situation can appear to be

appealing. Customers and other affiliated companies should be assured with a current ratio that

the company will be able to compensate off brief payments or current commitments with existing

cash reserves and other financial assets. This ratio allows management to consider their future

cash flow policy in order to resolve current liquidity problems. Credit cards or talks with retailers

to delay such transactions are probable to result from discussions with the bank. As per that table

reflecting Skanska Plc's current ratios, the company's current ratios in 2018 were 2.34, which fell

to 0.9324, meaning a significant decrease in this ratio (Amoozad Mahdiraji, Hafeez and Razavi

Hajiagha, 2020).

This estimation drop in the ratio is a warning sign for Skanska Plc's financial health. This

decrease in the current ratio means that perhaps the corporation's ability to meet its short-term

payables and obligations has been severely harmed. This feature should be prioritised by the

corporation because it could have a long-term impact on Skanska's ability to compete in the

profit on a pound of sales. This is one of the most important corporate profitability. Both factors

that have an effect on an enterprise's profitability level, either under administrative management

or not, are included in net margin. The higher the figure, the more effective the business

company is at managing costs. In this regard, based on an analysis of Skanska Plc's ratios, it was

discovered that the firm's total ratio margin in 2019 was just 11, 25 percent, down from 12,5

percent in 2018, due to a slight fall in the gross NP percentage. This decrease in net profit margin

shows that Skanska Plc's real success in converting total sales into income has deteriorated over

the reported time span. The company should focus on this factor in small amounts to work

properly. The revenue value of this company should be enhanced, while the gross business

expenditure should be minimised (Zulaihati, Susanti and Widyastuti, 2020).

Current ratio: The current ratio is a big short-run financial leverage that is used to

determine a company's total leverage state when looking at the relationship between all current

assets and current liabilities. In layman's terms, it's a strategy for determining but whether or not

the company's total assets balance will cover all of its current liabilities. This ratio is used not

only to assess liquidity problems, and also to ultimately determine how working resources can be

used. Whether this ratio is greater than 2, the company's financial situation can appear to be

appealing. Customers and other affiliated companies should be assured with a current ratio that

the company will be able to compensate off brief payments or current commitments with existing

cash reserves and other financial assets. This ratio allows management to consider their future

cash flow policy in order to resolve current liquidity problems. Credit cards or talks with retailers

to delay such transactions are probable to result from discussions with the bank. As per that table

reflecting Skanska Plc's current ratios, the company's current ratios in 2018 were 2.34, which fell

to 0.9324, meaning a significant decrease in this ratio (Amoozad Mahdiraji, Hafeez and Razavi

Hajiagha, 2020).

This estimation drop in the ratio is a warning sign for Skanska Plc's financial health. This

decrease in the current ratio means that perhaps the corporation's ability to meet its short-term

payables and obligations has been severely harmed. This feature should be prioritised by the

corporation because it could have a long-term impact on Skanska's ability to compete in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

industry. Although this just shows the company's short-term liquidity situation, failure to pay

attention to such a ratio result will lead to undesirable financial conditions.

Average receivable days: Debtors-collection period refers to the average fact that it is

difficult an organisation to recover its trading credit revenue for a given time period, usually

measured in days. This proportion is measured by the company in order to manage the efficiency

and effectiveness of credit practises and collection mechanisms. Whenever the percentage is

high, it shows the firm takes longer to receive credits or trade receivables. In this case, a lower

ratio indicates that the firm's credit policy or collection mechanisms are efficient.

As seen in the table, Skanska Plc's debt recovery cycle in 2018 and 2019 was 68 days and

73 days, overall, indicating an increase in the collection period. However, this is not a positive

sign for the company, as the enterprise requires more money in 2019 than that in 2018 to retrieve

the sum of accounts receivable. It could lead to a negative capital expenditure situation in the

company. The increase in this proportion can have a significant impact on the economic object's

short-term financial condition (van Houdt, 2020).

Average payable days: This ratio simply depicts the average time it takes a corporation

to pay its exchange payables or creditors. In most cases, a corporate company does not make any

of its purchases in cash; rather, the majority of its purchases are made on credit. This percentage

specifies however many days an organization typically pays its company and investors

dependent on gross average credit transactions and trade creditors balances. A shorter term

indicates that the firm has a better liquidity status because it needs less time to pay exchange

creditors. Although a shorter average-payable time indicates that the company does not have

enough liquid reserves or capital to pay any of its brief obligations and trade creditors. As a

result, a longer total payable time indicates that the firm has to concentrate on capital

expenditures and cash flow because its short-term liquidity buffer is not as strong. According to

Skanska Plc's recorded ratios, borrowers' collection periods were 128 days and 43 days in 2019

and 2018, accordingly, reflecting an extended payout period to creditors.

This growing pattern over time indicates that the business entity's willingness to pay its

investors has diminished over time. This increase in the timeframe means that the corporation

does not have sufficient or fair funds to pay creditors in a timely manner, indicating a depleted

attention to such a ratio result will lead to undesirable financial conditions.

Average receivable days: Debtors-collection period refers to the average fact that it is

difficult an organisation to recover its trading credit revenue for a given time period, usually

measured in days. This proportion is measured by the company in order to manage the efficiency

and effectiveness of credit practises and collection mechanisms. Whenever the percentage is

high, it shows the firm takes longer to receive credits or trade receivables. In this case, a lower

ratio indicates that the firm's credit policy or collection mechanisms are efficient.

As seen in the table, Skanska Plc's debt recovery cycle in 2018 and 2019 was 68 days and

73 days, overall, indicating an increase in the collection period. However, this is not a positive

sign for the company, as the enterprise requires more money in 2019 than that in 2018 to retrieve

the sum of accounts receivable. It could lead to a negative capital expenditure situation in the

company. The increase in this proportion can have a significant impact on the economic object's

short-term financial condition (van Houdt, 2020).

Average payable days: This ratio simply depicts the average time it takes a corporation

to pay its exchange payables or creditors. In most cases, a corporate company does not make any

of its purchases in cash; rather, the majority of its purchases are made on credit. This percentage

specifies however many days an organization typically pays its company and investors

dependent on gross average credit transactions and trade creditors balances. A shorter term

indicates that the firm has a better liquidity status because it needs less time to pay exchange

creditors. Although a shorter average-payable time indicates that the company does not have

enough liquid reserves or capital to pay any of its brief obligations and trade creditors. As a

result, a longer total payable time indicates that the firm has to concentrate on capital

expenditures and cash flow because its short-term liquidity buffer is not as strong. According to

Skanska Plc's recorded ratios, borrowers' collection periods were 128 days and 43 days in 2019

and 2018, accordingly, reflecting an extended payout period to creditors.

This growing pattern over time indicates that the business entity's willingness to pay its

investors has diminished over time. This increase in the timeframe means that the corporation

does not have sufficient or fair funds to pay creditors in a timely manner, indicating a depleted

liquidity situation. In addition, in manufacturing, if a company pays its vendors late, it will hurt

the company's goodwill, that could lead to big suppliers withdrawing their help.

CONCLUSION

The aforementioned study concluded that financial decision-making inside a market or firm

setting is a critical component because it enables for the identification of the company's

performance and the organization's long-term viability. To promote more rational decision-

making, a wide range of factors and strategies are needed. In order to achieve the corporate

objectives within a set time period, executives must consider different aspects of financial

decision-making. It also entails the calculation and analysis of ratios, which helps management

to assess the company's overall success over time and make choices based on the results of

various ratios. Share holders and other primary stakeholders may use financial ratios to assess

the viability of invested capital in the form of securities or by other methods in the company.

the company's goodwill, that could lead to big suppliers withdrawing their help.

CONCLUSION

The aforementioned study concluded that financial decision-making inside a market or firm

setting is a critical component because it enables for the identification of the company's

performance and the organization's long-term viability. To promote more rational decision-

making, a wide range of factors and strategies are needed. In order to achieve the corporate

objectives within a set time period, executives must consider different aspects of financial

decision-making. It also entails the calculation and analysis of ratios, which helps management

to assess the company's overall success over time and make choices based on the results of

various ratios. Share holders and other primary stakeholders may use financial ratios to assess

the viability of invested capital in the form of securities or by other methods in the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.