Financial Decision Making Report: Analysis of SKANSKA PLC Performance

VerifiedAdded on 2022/12/16

|12

|4013

|69

Report

AI Summary

This report provides a comprehensive analysis of SKANSKA PLC's financial performance, focusing on the role of accounting and finance within the organization. The study begins with an overview of accounting and finance functions, detailing their responsibilities and positions within a business context. The main body of the report conducts a ratio analysis of SKANSKA PLC over two years, utilizing financial statement data to assess the company's performance from an investor's perspective. Key financial ratios, including Return on Capital Employed, Net Profit Margin, and Current Ratio, are calculated and evaluated. The report explores the impact of these ratios on SKANSKA PLC's financial health and operational efficiency, and discusses the implications of the findings. The analysis includes a discussion on the importance of accounting ratios in business, supporting the answer with research and references. The report also analyzes the role of management accounting techniques in planning, control, and decision-making processes within the company, and explains how these techniques can be best applied to enhance company practices. The report also touches on how management accounting techniques like financial planning, statement analysis, and budgeting, influence the financial landscape of SKANSKA PLC. The report concludes with a summary of the key findings and recommendations based on the financial data and ratio analysis.

Financial Decision Making

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This study-report is formulated for management of SKANSA Limited, taking into account

the organization 's financial data The role of accounts and finance functions within corporation

are addressed in the first section of this study. This also provides an overview of the accounting

and finance division's responsibilities and positions in the business. In second section of the

study, numerous ratios are measured for the corporation over two years utilizing information

from business's financial statements, and comments regarding the corporation's performance

from perspective of investor has been made.

2

This study-report is formulated for management of SKANSA Limited, taking into account

the organization 's financial data The role of accounts and finance functions within corporation

are addressed in the first section of this study. This also provides an overview of the accounting

and finance division's responsibilities and positions in the business. In second section of the

study, numerous ratios are measured for the corporation over two years utilizing information

from business's financial statements, and comments regarding the corporation's performance

from perspective of investor has been made.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Main Body.......................................................................................................................................4

Task 1...............................................................................................................................................4

Accounting & Finance Overview...........................................................................................4

Accounting & Finance Department........................................................................................4

Accounting Department..........................................................................................................5

Finance Department:..............................................................................................................7

Task 2...............................................................................................................................................8

Ratio analysis of SKANSKSA PLC.......................................................................................8

Performance Evaluation of SKANSKA PLC.........................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Main Body.......................................................................................................................................4

Task 1...............................................................................................................................................4

Accounting & Finance Overview...........................................................................................4

Accounting & Finance Department........................................................................................4

Accounting Department..........................................................................................................5

Finance Department:..............................................................................................................7

Task 2...............................................................................................................................................8

Ratio analysis of SKANSKSA PLC.......................................................................................8

Performance Evaluation of SKANSKA PLC.........................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Accounting and finance are considered to be key aspects of an enterprise since they depict all

financial details. It primarily consists of business's financial statements, accounting information,

including multiple performance evaluation instruments that are used to determine a corporation 's

financial status in the related sector (Black, 2019). Accounting is primarily concerned with day-

to-day financial reports as well as information management of company concern, while finance

is concerned with the usage of those data in relation to an organization's potential growth

prospects using appropriate techniques and minimizing costs. In this regard SKANSKA PLC '

performance, which is one of the pioneering construction enterprises in United Kingdom, has

been analysed. Accounts and Finance division's functions of SKANSKA PLC has been analysed

in this study, including these division's roles and responsibilities in the organization. In addition,

a ratio study will be performed in attempt to assess the corporation 's performance in terms of

potential growth.

Main Body

Task 1

Accounting & Finance Overview

Accounting implies to process of tracking and maintaining business activities in

accounting records, while finance is process of managing money that flows in as well as out of

business entity. This is regarded as an essential component of enterprise that deals with financial

matters and is accountable for a firm's long-term growth.

To function effectively, SKANSKA PLC, being construction company, needs a substantial

financial investment as well as a sufficient investor pool. As a result, this particular segment is

critical to the corporation 's ultimate growth and expansion. Whether this is day-to-day operating

or capital-based activities, it's indeed critical to handle a corporation's finances in an acceptable

way for longer term. Multiple stakeholders in a business serve an important role in financing and

accounting concerns in order for the firm to attain financial as well as non-fiscal performance

(Çera and Tuzi, 2019).

4

Accounting and finance are considered to be key aspects of an enterprise since they depict all

financial details. It primarily consists of business's financial statements, accounting information,

including multiple performance evaluation instruments that are used to determine a corporation 's

financial status in the related sector (Black, 2019). Accounting is primarily concerned with day-

to-day financial reports as well as information management of company concern, while finance

is concerned with the usage of those data in relation to an organization's potential growth

prospects using appropriate techniques and minimizing costs. In this regard SKANSKA PLC '

performance, which is one of the pioneering construction enterprises in United Kingdom, has

been analysed. Accounts and Finance division's functions of SKANSKA PLC has been analysed

in this study, including these division's roles and responsibilities in the organization. In addition,

a ratio study will be performed in attempt to assess the corporation 's performance in terms of

potential growth.

Main Body

Task 1

Accounting & Finance Overview

Accounting implies to process of tracking and maintaining business activities in

accounting records, while finance is process of managing money that flows in as well as out of

business entity. This is regarded as an essential component of enterprise that deals with financial

matters and is accountable for a firm's long-term growth.

To function effectively, SKANSKA PLC, being construction company, needs a substantial

financial investment as well as a sufficient investor pool. As a result, this particular segment is

critical to the corporation 's ultimate growth and expansion. Whether this is day-to-day operating

or capital-based activities, it's indeed critical to handle a corporation's finances in an acceptable

way for longer term. Multiple stakeholders in a business serve an important role in financing and

accounting concerns in order for the firm to attain financial as well as non-fiscal performance

(Çera and Tuzi, 2019).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting & Finance Department

Every firm's accounts and finance division is in responsibility of ensuring that everything

functions smoothly as well as ensuring effective financial management practices and monitoring

of financial affairs and taking appropriate steps to facilitate all business operations. No

organization or corporation may operate efficiently without a stable sources of funds, an

effective supply of funding, and effective accounting (Finkler, Smith and Calabrese, 2018.).

A corporation 's accounting section is in charge of the financial statement planning,

general ledger management, bill processing, customer bill processing, staffing, and other

functions. In other terms, they are in-control of the organization 's total financial management,

while a firm's finance section is in-control of gathering funding for the organization managing

funds within business, and planning for the distribution of funding on various assets.

Finances and accounting are 2 distinct fields which are often messed up.

Finance is structured process of strategically managing the allocation of an organization 's assets

Accounting involve practices of recording and recording fiscal activities. Since they also deal

with management of a corporation's money financing and accounts are often mixed together. The

enterprise or organization would not prosper at any expense without a sufficient or effective

accounting and financing division (Grohmann, 2018).

Accounting Department

It is characterized as a component of business wherein financial and monetary transactions

are reported for later use in attempt to keeping control of company's financial details in attempt

to achieve reliability and productivity within a given time frame.

Functions

Financial Accounting: This is task of accounting that focuses on analysing, reporting,

and summarizing financial statements for administrators to use in making final decisions.

Cash flows statement, ratio review as well as other finance-related reporting are examples

of different financing reports. It is critical to an organization's overall growth. Its

intention is to show an accurate and fair picture of an entity 's fiscal transactions.

Management Accounting: It involves use of financial including non-financial to assist

management in making final decisions. It is centred on informing management staff

concerning financial statements such that appropriate decisions can be taken in relation to

5

Every firm's accounts and finance division is in responsibility of ensuring that everything

functions smoothly as well as ensuring effective financial management practices and monitoring

of financial affairs and taking appropriate steps to facilitate all business operations. No

organization or corporation may operate efficiently without a stable sources of funds, an

effective supply of funding, and effective accounting (Finkler, Smith and Calabrese, 2018.).

A corporation 's accounting section is in charge of the financial statement planning,

general ledger management, bill processing, customer bill processing, staffing, and other

functions. In other terms, they are in-control of the organization 's total financial management,

while a firm's finance section is in-control of gathering funding for the organization managing

funds within business, and planning for the distribution of funding on various assets.

Finances and accounting are 2 distinct fields which are often messed up.

Finance is structured process of strategically managing the allocation of an organization 's assets

Accounting involve practices of recording and recording fiscal activities. Since they also deal

with management of a corporation's money financing and accounts are often mixed together. The

enterprise or organization would not prosper at any expense without a sufficient or effective

accounting and financing division (Grohmann, 2018).

Accounting Department

It is characterized as a component of business wherein financial and monetary transactions

are reported for later use in attempt to keeping control of company's financial details in attempt

to achieve reliability and productivity within a given time frame.

Functions

Financial Accounting: This is task of accounting that focuses on analysing, reporting,

and summarizing financial statements for administrators to use in making final decisions.

Cash flows statement, ratio review as well as other finance-related reporting are examples

of different financing reports. It is critical to an organization's overall growth. Its

intention is to show an accurate and fair picture of an entity 's fiscal transactions.

Management Accounting: It involves use of financial including non-financial to assist

management in making final decisions. It is centred on informing management staff

concerning financial statements such that appropriate decisions can be taken in relation to

5

the business 's overall performance. It aids in the management of an organization's cost

structures and profitability (Li and Chapman, 2020).

Tax function: This is one of most significant dimensions of business organization that

focuses on taxation-related factors of a company It contains both direct as well as indirect

taxation that are related to an organization's finances in any way. As a result, it is

necessary to manage taxes and adhere to various regulations. It emphasizes on improving

company leverage over their global activities.

Auditing function: It has to do with detecting and preventing fraudulent activities and

discrepancies in the corporation 's financial statements This is primarily concerned with

adhering to accounting standards in such way that mistakes and fraudulent activities can

be identified more easily. Skanska Plc has also been following auditing practices and

standards in order to aid in the detection and avoidance of mistakes, and also the

recognition of accurate and authentic financial data (Moreland, 2018).

Roles and Duties

Bookkeeping: it entails regularly capturing, reviewing, and comprehending an entity's

financial transactions. For small companies, this role is typically filled by bookkeeper,

however as the organization grows and expands, this might be covered by more expert

payables and accounts receivable associates. In this regard, Skanska corporation has

developed an integrated bookkeeping system to help maintain business records more

effectively and reliably (Mumtaz, Saeed and Ramzan, 2018).

Billings: the corporation's billings unit gathers data through the shipment and client order

units in order to produce invoices for company's customers, which is sub-division

of accounting department that Skanska corporation should emphasize accordingly.

Collection: the accounting division is in control of collecting past-due invoices payments

from customers, and it uses a variety of methods to do so. The accounting team at

the Skanska corporation is expected to handle and report receivables collections data

in acceptable manner such that business's liquid assets can be handled more effectively.

Taxes: a community of advanced-degreed accountants estimates the figure of taxable

income which the company is required to receive and makes annual income tax payments

to government based on such figure. The tax party files taxation returns in variety of

jurisdictions in additions to franchise taxation, income taxes, consumption taxes, as well

6

structures and profitability (Li and Chapman, 2020).

Tax function: This is one of most significant dimensions of business organization that

focuses on taxation-related factors of a company It contains both direct as well as indirect

taxation that are related to an organization's finances in any way. As a result, it is

necessary to manage taxes and adhere to various regulations. It emphasizes on improving

company leverage over their global activities.

Auditing function: It has to do with detecting and preventing fraudulent activities and

discrepancies in the corporation 's financial statements This is primarily concerned with

adhering to accounting standards in such way that mistakes and fraudulent activities can

be identified more easily. Skanska Plc has also been following auditing practices and

standards in order to aid in the detection and avoidance of mistakes, and also the

recognition of accurate and authentic financial data (Moreland, 2018).

Roles and Duties

Bookkeeping: it entails regularly capturing, reviewing, and comprehending an entity's

financial transactions. For small companies, this role is typically filled by bookkeeper,

however as the organization grows and expands, this might be covered by more expert

payables and accounts receivable associates. In this regard, Skanska corporation has

developed an integrated bookkeeping system to help maintain business records more

effectively and reliably (Mumtaz, Saeed and Ramzan, 2018).

Billings: the corporation's billings unit gathers data through the shipment and client order

units in order to produce invoices for company's customers, which is sub-division

of accounting department that Skanska corporation should emphasize accordingly.

Collection: the accounting division is in control of collecting past-due invoices payments

from customers, and it uses a variety of methods to do so. The accounting team at

the Skanska corporation is expected to handle and report receivables collections data

in acceptable manner such that business's liquid assets can be handled more effectively.

Taxes: a community of advanced-degreed accountants estimates the figure of taxable

income which the company is required to receive and makes annual income tax payments

to government based on such figure. The tax party files taxation returns in variety of

jurisdictions in additions to franchise taxation, income taxes, consumption taxes, as well

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as property taxes. As a result, Skanska plc must handle such a process appropriately

(Njegovanovic, 2018).

Financial statement preparation: a reporting team within department creates evolving

journal entries, publishes financial statement endnotes, and publishes financials at end of

each the reporting period to bring corporation 's formal financial statements through

compliance with the applicable accounting framework. As a result, Skanska company's

financial structure must be sufficient in order for company activities to be handled

effectively over a longer period of time.

Finance Department:

This department oversees acquisition, lending, dividend, and working capital operations, both of

these are primarily connected with the proper managing of corporation funds (Roger, Otjes and

van der Veer, 2017). The following are the financial roles that can be addressed in relation to

the SKANSKA PLC:

Functions

Investment function: It contains all applicable variables that influence an organization's

investment ability in a possible investment strategy. As a result, SKANSKA corporation's

finance team is tasked with effectively and efficiently handling all of these

considerations.

Financing function: It corresponds to the elements that need organizational attention in

attempt to organize a business corporation's finances. SKANSKA Corporation has

highlighted the related sources from which construction business could potentially obtain

sufficient means of funding in attempt to broaden its activities more quickly.

Dividend function: It is the allocation of a corporation 's earnings to a select class of

shareholders that own the most stock in the organization The finance role is associated

with effectively distributing such earnings so that productivity can be sustained. As a

result, in order to foster a safe business climate, SKANSKA Corporation must implement

appropriate policies and legislation.

Working capital function: It is defined as day-to-day expenditures that must be handled

in a practical way. In this regard, SKANSKA Corporation must assess its activities

through its finance division in attempt to encourage cost-effective strategies for routine-

based expenditure.

7

(Njegovanovic, 2018).

Financial statement preparation: a reporting team within department creates evolving

journal entries, publishes financial statement endnotes, and publishes financials at end of

each the reporting period to bring corporation 's formal financial statements through

compliance with the applicable accounting framework. As a result, Skanska company's

financial structure must be sufficient in order for company activities to be handled

effectively over a longer period of time.

Finance Department:

This department oversees acquisition, lending, dividend, and working capital operations, both of

these are primarily connected with the proper managing of corporation funds (Roger, Otjes and

van der Veer, 2017). The following are the financial roles that can be addressed in relation to

the SKANSKA PLC:

Functions

Investment function: It contains all applicable variables that influence an organization's

investment ability in a possible investment strategy. As a result, SKANSKA corporation's

finance team is tasked with effectively and efficiently handling all of these

considerations.

Financing function: It corresponds to the elements that need organizational attention in

attempt to organize a business corporation's finances. SKANSKA Corporation has

highlighted the related sources from which construction business could potentially obtain

sufficient means of funding in attempt to broaden its activities more quickly.

Dividend function: It is the allocation of a corporation 's earnings to a select class of

shareholders that own the most stock in the organization The finance role is associated

with effectively distributing such earnings so that productivity can be sustained. As a

result, in order to foster a safe business climate, SKANSKA Corporation must implement

appropriate policies and legislation.

Working capital function: It is defined as day-to-day expenditures that must be handled

in a practical way. In this regard, SKANSKA Corporation must assess its activities

through its finance division in attempt to encourage cost-effective strategies for routine-

based expenditure.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Roles and Duties

The following are most common roles of SKANSKA corporation financial department:

Budgeting and forecasting: the finance division works with executives to prepare the

corporation's budgets and forecasts, and also offer financial advice. This information can

be employed to address the cash needs of each department plan organization personnel

levels, and prepare for asset acquisitions and improvements prior they become necessary.

Management of business’s cash flow: the finance division is in charge of managing all

business cash flows in as well as out of a business, and also ensuring that sufficient

funding is enough to support the business's day-to-day requirements. This area also

includes the business's credits and cash collections procedures, which assure that

distributors and lenders are paid properly and on specific schedule and also the

organization itself (Shakeel, Shahzad and Abdullah, 2020).

Management of company’s investments: in order to evaluating and choosing new

acquisitions, the financing division is in charge of handling the corporation 's current

assets. Quite apart from business's capital assets, Skanska's finance

department/unit should be focused on current assets. Since company's working capital

should be managed effectively in attempt to maximize profits in comparison to the sum

of money spent, it has an effect on the corporation’s liquidity instead of fixed assets.

Budgeting: the corporation's finance department assists the balance of the enterprise in

developing company-wide budget, that is used to plan for future expenditures in the

upcoming year, including purchase of capital and fixed assets.

Payrolls: the accounting division collects time worked details from personnel and hires

rate data from personnel resources, calculates payroll and other reductions from staff

wages, and allocates net compensation to staff in cash terms, checks, pay vouchers, or

bank transfer.

Task 2

Ratio analysis of SKANSKSA PLC

Ratio valuation is regarded as the most critical aspect of a company's financial accounting.

It is defined as an efficient performance assessment technique that has been used in the past to

assess the success of a company over a long period of time. It requires a variety of financial as

8

The following are most common roles of SKANSKA corporation financial department:

Budgeting and forecasting: the finance division works with executives to prepare the

corporation's budgets and forecasts, and also offer financial advice. This information can

be employed to address the cash needs of each department plan organization personnel

levels, and prepare for asset acquisitions and improvements prior they become necessary.

Management of business’s cash flow: the finance division is in charge of managing all

business cash flows in as well as out of a business, and also ensuring that sufficient

funding is enough to support the business's day-to-day requirements. This area also

includes the business's credits and cash collections procedures, which assure that

distributors and lenders are paid properly and on specific schedule and also the

organization itself (Shakeel, Shahzad and Abdullah, 2020).

Management of company’s investments: in order to evaluating and choosing new

acquisitions, the financing division is in charge of handling the corporation 's current

assets. Quite apart from business's capital assets, Skanska's finance

department/unit should be focused on current assets. Since company's working capital

should be managed effectively in attempt to maximize profits in comparison to the sum

of money spent, it has an effect on the corporation’s liquidity instead of fixed assets.

Budgeting: the corporation's finance department assists the balance of the enterprise in

developing company-wide budget, that is used to plan for future expenditures in the

upcoming year, including purchase of capital and fixed assets.

Payrolls: the accounting division collects time worked details from personnel and hires

rate data from personnel resources, calculates payroll and other reductions from staff

wages, and allocates net compensation to staff in cash terms, checks, pay vouchers, or

bank transfer.

Task 2

Ratio analysis of SKANSKSA PLC

Ratio valuation is regarded as the most critical aspect of a company's financial accounting.

It is defined as an efficient performance assessment technique that has been used in the past to

assess the success of a company over a long period of time. It requires a variety of financial as

8

well as non-financial indicators that are used to determine a status of the organization in the

marketplace (Yuneline and Suryana, 2020). Different metrics were used to calculate the financial

success of SKANSKA PLC, that is one of the largest constructors in the United Kingdom, over a

given time span. The accounting calculations are measured in the following way for the specified

purpose:

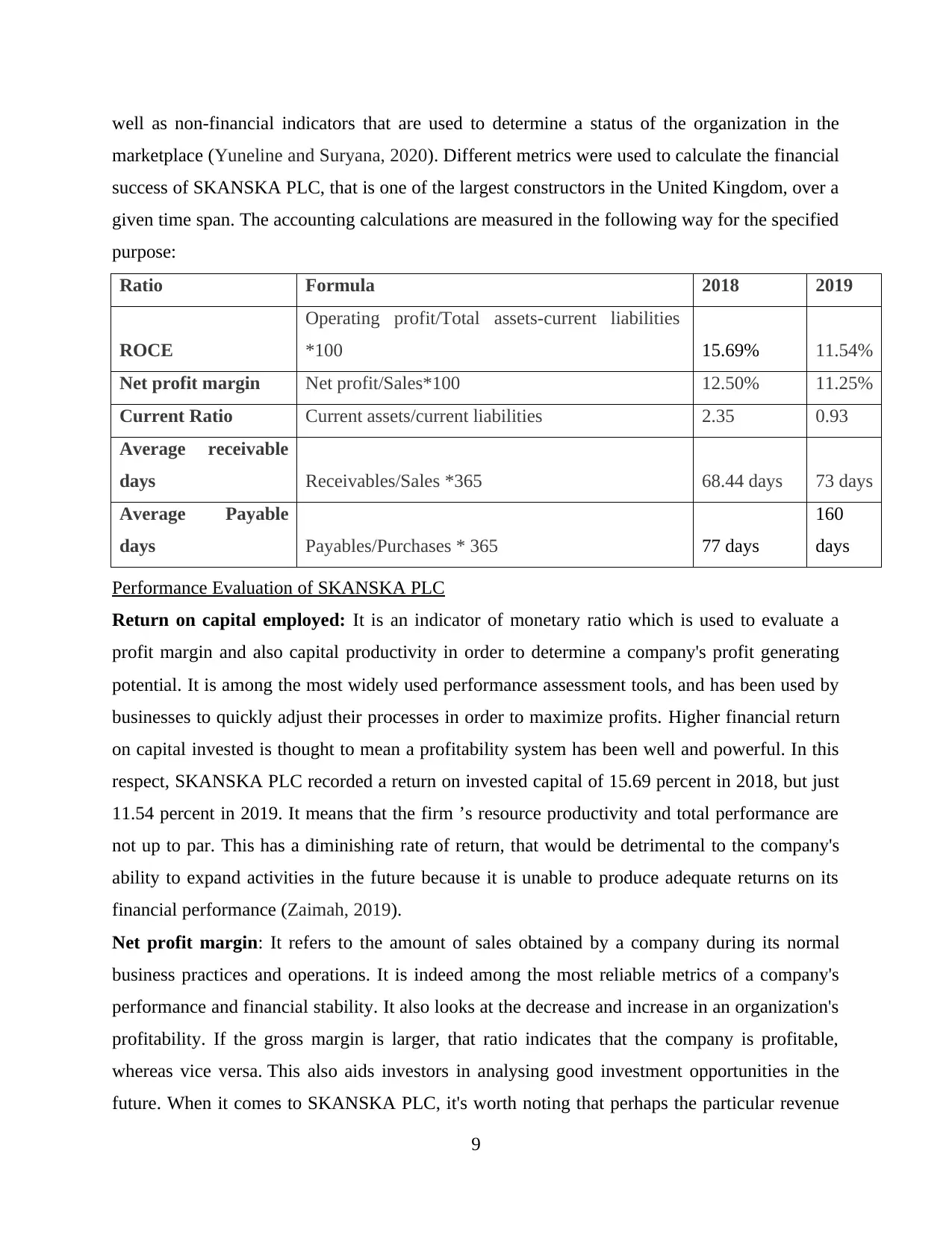

Ratio Formula 2018 2019

ROCE

Operating profit/Total assets-current liabilities

*100 15.69% 11.54%

Net profit margin Net profit/Sales*100 12.50% 11.25%

Current Ratio Current assets/current liabilities 2.35 0.93

Average receivable

days Receivables/Sales *365 68.44 days 73 days

Average Payable

days Payables/Purchases * 365 77 days

160

days

Performance Evaluation of SKANSKA PLC

Return on capital employed: It is an indicator of monetary ratio which is used to evaluate a

profit margin and also capital productivity in order to determine a company's profit generating

potential. It is among the most widely used performance assessment tools, and has been used by

businesses to quickly adjust their processes in order to maximize profits. Higher financial return

on capital invested is thought to mean a profitability system has been well and powerful. In this

respect, SKANSKA PLC recorded a return on invested capital of 15.69 percent in 2018, but just

11.54 percent in 2019. It means that the firm ’s resource productivity and total performance are

not up to par. This has a diminishing rate of return, that would be detrimental to the company's

ability to expand activities in the future because it is unable to produce adequate returns on its

financial performance (Zaimah, 2019).

Net profit margin: It refers to the amount of sales obtained by a company during its normal

business practices and operations. It is indeed among the most reliable metrics of a company's

performance and financial stability. It also looks at the decrease and increase in an organization's

profitability. If the gross margin is larger, that ratio indicates that the company is profitable,

whereas vice versa. This also aids investors in analysing good investment opportunities in the

future. When it comes to SKANSKA PLC, it's worth noting that perhaps the particular revenue

9

marketplace (Yuneline and Suryana, 2020). Different metrics were used to calculate the financial

success of SKANSKA PLC, that is one of the largest constructors in the United Kingdom, over a

given time span. The accounting calculations are measured in the following way for the specified

purpose:

Ratio Formula 2018 2019

ROCE

Operating profit/Total assets-current liabilities

*100 15.69% 11.54%

Net profit margin Net profit/Sales*100 12.50% 11.25%

Current Ratio Current assets/current liabilities 2.35 0.93

Average receivable

days Receivables/Sales *365 68.44 days 73 days

Average Payable

days Payables/Purchases * 365 77 days

160

days

Performance Evaluation of SKANSKA PLC

Return on capital employed: It is an indicator of monetary ratio which is used to evaluate a

profit margin and also capital productivity in order to determine a company's profit generating

potential. It is among the most widely used performance assessment tools, and has been used by

businesses to quickly adjust their processes in order to maximize profits. Higher financial return

on capital invested is thought to mean a profitability system has been well and powerful. In this

respect, SKANSKA PLC recorded a return on invested capital of 15.69 percent in 2018, but just

11.54 percent in 2019. It means that the firm ’s resource productivity and total performance are

not up to par. This has a diminishing rate of return, that would be detrimental to the company's

ability to expand activities in the future because it is unable to produce adequate returns on its

financial performance (Zaimah, 2019).

Net profit margin: It refers to the amount of sales obtained by a company during its normal

business practices and operations. It is indeed among the most reliable metrics of a company's

performance and financial stability. It also looks at the decrease and increase in an organization's

profitability. If the gross margin is larger, that ratio indicates that the company is profitable,

whereas vice versa. This also aids investors in analysing good investment opportunities in the

future. When it comes to SKANSKA PLC, it's worth noting that perhaps the particular revenue

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

has dropped from 2018 to 2019. In 2018, the corresponding operating margin was 12.50 percent,

while being in 2019 it was 11.25 percent. In 2018, the corresponding net profit margin was 12.50

percent, while in 2019 it was 11.25 percent. The operating margin has been declining, indicating

that the organization needs to boost its total sales generating capability over time. As a result,

proactive strategic policies must be implemented in order to meet sales targets (Park and Sela,

2018).

Current Ratio: This is the mixture of existing shareholder ’s equity that defines a firm’s short-

term liquidity status in order to effectively fund its short-term contractual obligations. If a

corporation's liquidity amount will be less than one, it is assumed that firms is unable to term

financial obligations financial commitments in a timely manner. It is among the most successful

strategies for determining an operating cash flow status such that appropriate steps can be taken

to meet the business goals. In the case of SKANSKA PLC, the current ratio throughout 2018

were 2.35, which is considered to be very good in repaying its simple obligations. In 2019, it

reported a current ratio of 0.93, which really is significantly lower than in previous years needs

more improvement in order to offset current debts. It really is important to have a sufficient

amount of cash on hand so that SKANSKA PLC can extend its activities without going into debt

but gain sufficient income over time (Camerer, 2020).

Average receivables days: It refers to the time frame where a corporation's borrower is expected

to settle their loan within a certain amount of time. It represents the creditworthiness of the

business and also the quality of the collection era. It is important to get a short receivable term in

order to handle the bank's profitability in a sustainable manner. In order for an organization to

provide successful results, it must have an appropriate account receivables time. It is important to

provide a sufficient receivables collection cycle in order for an organization to provide reliable

performance over a long period of time. When a corporation has bad loans, it means that its

financial health is inadequate, and so as a result, the organization's procedures must be improved

in order to encourage productivity. The smaller the compilation time, it is said, the best for

organization. The greater the compilation time, the worst the opportunities for organizational

advancement. In the current scenario, SKANSKA PLC has a processing time of 68.44 times in

2018 through 73 days in 2019, which would have to be improved for the business's future growth

prospects. As a result, it is necessary to change receivables allocation in order to retain the

organization's operations further (Duan, Edwards and Dwivedi, 2019).

10

while being in 2019 it was 11.25 percent. In 2018, the corresponding net profit margin was 12.50

percent, while in 2019 it was 11.25 percent. The operating margin has been declining, indicating

that the organization needs to boost its total sales generating capability over time. As a result,

proactive strategic policies must be implemented in order to meet sales targets (Park and Sela,

2018).

Current Ratio: This is the mixture of existing shareholder ’s equity that defines a firm’s short-

term liquidity status in order to effectively fund its short-term contractual obligations. If a

corporation's liquidity amount will be less than one, it is assumed that firms is unable to term

financial obligations financial commitments in a timely manner. It is among the most successful

strategies for determining an operating cash flow status such that appropriate steps can be taken

to meet the business goals. In the case of SKANSKA PLC, the current ratio throughout 2018

were 2.35, which is considered to be very good in repaying its simple obligations. In 2019, it

reported a current ratio of 0.93, which really is significantly lower than in previous years needs

more improvement in order to offset current debts. It really is important to have a sufficient

amount of cash on hand so that SKANSKA PLC can extend its activities without going into debt

but gain sufficient income over time (Camerer, 2020).

Average receivables days: It refers to the time frame where a corporation's borrower is expected

to settle their loan within a certain amount of time. It represents the creditworthiness of the

business and also the quality of the collection era. It is important to get a short receivable term in

order to handle the bank's profitability in a sustainable manner. In order for an organization to

provide successful results, it must have an appropriate account receivables time. It is important to

provide a sufficient receivables collection cycle in order for an organization to provide reliable

performance over a long period of time. When a corporation has bad loans, it means that its

financial health is inadequate, and so as a result, the organization's procedures must be improved

in order to encourage productivity. The smaller the compilation time, it is said, the best for

organization. The greater the compilation time, the worst the opportunities for organizational

advancement. In the current scenario, SKANSKA PLC has a processing time of 68.44 times in

2018 through 73 days in 2019, which would have to be improved for the business's future growth

prospects. As a result, it is necessary to change receivables allocation in order to retain the

organization's operations further (Duan, Edwards and Dwivedi, 2019).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Average payable days: That really is the timeframe at which a system is planning to reimburse

its debts to creditors within the agreed time frame. In order to provide an appropriate collection

of services for an organization even as its profitability can be sustained on a lengthy period, it

really is important to have optimal payable days. These are claimed that a prolonged payable

duration is beneficial to an operating cash flow status over a given time period, whereas a shorter

really see is detrimental. In the current scenario, SKANSKA PLC has a payable duration of 77

days in 2018 as well as 160 nights in 2019, which would be deemed to be ideal for long-term

liquidity. It really is important to provide the best payable term possible in order for the business

to run efficiently. It is important to provide the best payable word possible in order to maximize

the productivity of business processes. This is also assumed that if a corporation does not repay

its loans for an extended period of time, its market share would deteriorate, affecting the

company's long-term growth. As a result, a reasonable compensation cycle is required such that

the business can run in a more efficient manner (Lieberthal and Lampton, 2018).

CONCLUSION

In last of report, it is stated that Accounting and finance are very important for each

organization, according to the findings of this study. A new dimension called reporting and

financial services was established to handle a company's assets and expenditures in regularly to

secure that corporate activities ran smoothly. It has a significant impact on an organization's

overall growth, which would eventually benefit the organization. It performs a critical part in the

overall growth of an organization, eventually assisting in the creation of a profitable venture.

SKANSKA PLC is a leading company in the building industry, but it has been analysed in terms

of financing in this article. The importance of the financial and economics departments is also

covered in this article, as is the revenue growth review of SKANSKA PLC has to make changes

to its financial framework in order to improve its profitability in the coming years and devise an

ambitious and profitable strategy for future growth. As a result, it is advised that the corporation

take the appropriate steps. As a result, it is advised that the organization take the requisite steps

to change its existing plans and practices in order to enhance its corporate activities for the long

term.

11

its debts to creditors within the agreed time frame. In order to provide an appropriate collection

of services for an organization even as its profitability can be sustained on a lengthy period, it

really is important to have optimal payable days. These are claimed that a prolonged payable

duration is beneficial to an operating cash flow status over a given time period, whereas a shorter

really see is detrimental. In the current scenario, SKANSKA PLC has a payable duration of 77

days in 2018 as well as 160 nights in 2019, which would be deemed to be ideal for long-term

liquidity. It really is important to provide the best payable term possible in order for the business

to run efficiently. It is important to provide the best payable word possible in order to maximize

the productivity of business processes. This is also assumed that if a corporation does not repay

its loans for an extended period of time, its market share would deteriorate, affecting the

company's long-term growth. As a result, a reasonable compensation cycle is required such that

the business can run in a more efficient manner (Lieberthal and Lampton, 2018).

CONCLUSION

In last of report, it is stated that Accounting and finance are very important for each

organization, according to the findings of this study. A new dimension called reporting and

financial services was established to handle a company's assets and expenditures in regularly to

secure that corporate activities ran smoothly. It has a significant impact on an organization's

overall growth, which would eventually benefit the organization. It performs a critical part in the

overall growth of an organization, eventually assisting in the creation of a profitable venture.

SKANSKA PLC is a leading company in the building industry, but it has been analysed in terms

of financing in this article. The importance of the financial and economics departments is also

covered in this article, as is the revenue growth review of SKANSKA PLC has to make changes

to its financial framework in order to improve its profitability in the coming years and devise an

ambitious and profitable strategy for future growth. As a result, it is advised that the corporation

take the appropriate steps. As a result, it is advised that the organization take the requisite steps

to change its existing plans and practices in order to enhance its corporate activities for the long

term.

11

REFERENCES

Books and Journals

Bannier, C.E. and Schwarz, M., 2018. Gender-and education-related effects of financial literacy and

confidence on financial wealth. Journal of Economic Psychology, 67, pp.66-86.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Camerer, C., 2020. 8. Individual Decision Making. In The handbook of experimental

economics (pp. 587-704). Princeton University Press.

Çera, G. and Tuzi, B., 2019. Does gender matter in financial literacy? A case study of young

people in Tirana. Scientific papers of the University of Pardubice. Series D, Faculty of

Economics and Administration. 45/2019.

Duan, Y., Edwards, J.S. and Dwivedi, Y.K., 2019. Artificial intelligence for decision making in

the era of Big Data–evolution, challenges and research agenda. International Journal of

Information Management, 48, pp.63-71.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2018. Financial management for public, health,

and not-for-profit organizations. CQ Press.

Grohmann, A., 2018. Financial literacy and financial behavior: Evidence from the emerging

Asian middle class. Pacific-Basin Finance Journal, 48, pp.129-143.

Li, M. and Chapman, G.B., 2020. Medical decision making. The Wiley Encyclopedia of Health

Psychology, pp.347-353.

Lieberthal, K.G. and Lampton, D.M. eds., 2018. Bureaucracy, politics, and decision making in

post-Mao China (Vol. 14). University of California Press.

Moreland, K.A., 2018. Seeking financial advice and other desirable financial behaviors. Journal

of Financial Counseling and Planning, 29(2), pp.198-207.

Mumtaz, A., Saeed, T. and Ramzan, M., 2018. Factors affecting investment decision-making in

Pakistan stock exchange. International Journal of Financial Engineering, 5(04),

p.1850033.

Njegovanovic, A., 2018. Neurological aspects of finance, transmitters, emotions, mirror neuronal

activity in financial decision. Маркетинг і менеджмент інновацій, (3), pp.186-198.

Park, J.J. and Sela, A., 2018. Not my type: Why affective decision makers are reluctant to make

financial decisions. Journal of Consumer Research, 45(2), pp.298-319.

Roger, L., Otjes, S. and van der Veer, H., 2017. The financial crisis and the European

Parliament: An analysis of the Two-Pack legislation. European Union Politics, 18(4),

pp.560-580.

Shakeel, M., Shahzad, M. and Abdullah, S., 2020. Pythagorean uncertain linguistic hesitant

fuzzy weighted averaging operator and its application in financial group decision

making. Soft Computing, 24(3), pp.1585-1597.

Yuneline, M.H. and Suryana, U., 2020. Financial Literacy and its Impact on Funding Source’s

Decision-Making. International Journal of Applied Economics, Finance and

Accounting, 6(1), pp.1-10.

Zaimah, R., 2019. The probability factor influences the level of financial well-being of workers

in Malaysia. Geografia-Malaysian Journal of Society and Space, 15(3).

12

Books and Journals

Bannier, C.E. and Schwarz, M., 2018. Gender-and education-related effects of financial literacy and

confidence on financial wealth. Journal of Economic Psychology, 67, pp.66-86.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Camerer, C., 2020. 8. Individual Decision Making. In The handbook of experimental

economics (pp. 587-704). Princeton University Press.

Çera, G. and Tuzi, B., 2019. Does gender matter in financial literacy? A case study of young

people in Tirana. Scientific papers of the University of Pardubice. Series D, Faculty of

Economics and Administration. 45/2019.

Duan, Y., Edwards, J.S. and Dwivedi, Y.K., 2019. Artificial intelligence for decision making in

the era of Big Data–evolution, challenges and research agenda. International Journal of

Information Management, 48, pp.63-71.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2018. Financial management for public, health,

and not-for-profit organizations. CQ Press.

Grohmann, A., 2018. Financial literacy and financial behavior: Evidence from the emerging

Asian middle class. Pacific-Basin Finance Journal, 48, pp.129-143.

Li, M. and Chapman, G.B., 2020. Medical decision making. The Wiley Encyclopedia of Health

Psychology, pp.347-353.

Lieberthal, K.G. and Lampton, D.M. eds., 2018. Bureaucracy, politics, and decision making in

post-Mao China (Vol. 14). University of California Press.

Moreland, K.A., 2018. Seeking financial advice and other desirable financial behaviors. Journal

of Financial Counseling and Planning, 29(2), pp.198-207.

Mumtaz, A., Saeed, T. and Ramzan, M., 2018. Factors affecting investment decision-making in

Pakistan stock exchange. International Journal of Financial Engineering, 5(04),

p.1850033.

Njegovanovic, A., 2018. Neurological aspects of finance, transmitters, emotions, mirror neuronal

activity in financial decision. Маркетинг і менеджмент інновацій, (3), pp.186-198.

Park, J.J. and Sela, A., 2018. Not my type: Why affective decision makers are reluctant to make

financial decisions. Journal of Consumer Research, 45(2), pp.298-319.

Roger, L., Otjes, S. and van der Veer, H., 2017. The financial crisis and the European

Parliament: An analysis of the Two-Pack legislation. European Union Politics, 18(4),

pp.560-580.

Shakeel, M., Shahzad, M. and Abdullah, S., 2020. Pythagorean uncertain linguistic hesitant

fuzzy weighted averaging operator and its application in financial group decision

making. Soft Computing, 24(3), pp.1585-1597.

Yuneline, M.H. and Suryana, U., 2020. Financial Literacy and its Impact on Funding Source’s

Decision-Making. International Journal of Applied Economics, Finance and

Accounting, 6(1), pp.1-10.

Zaimah, R., 2019. The probability factor influences the level of financial well-being of workers

in Malaysia. Geografia-Malaysian Journal of Society and Space, 15(3).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.