Decision Support Tools: Profit Analysis and Regression

VerifiedAdded on 2019/10/31

|7

|1107

|270

Homework Assignment

AI Summary

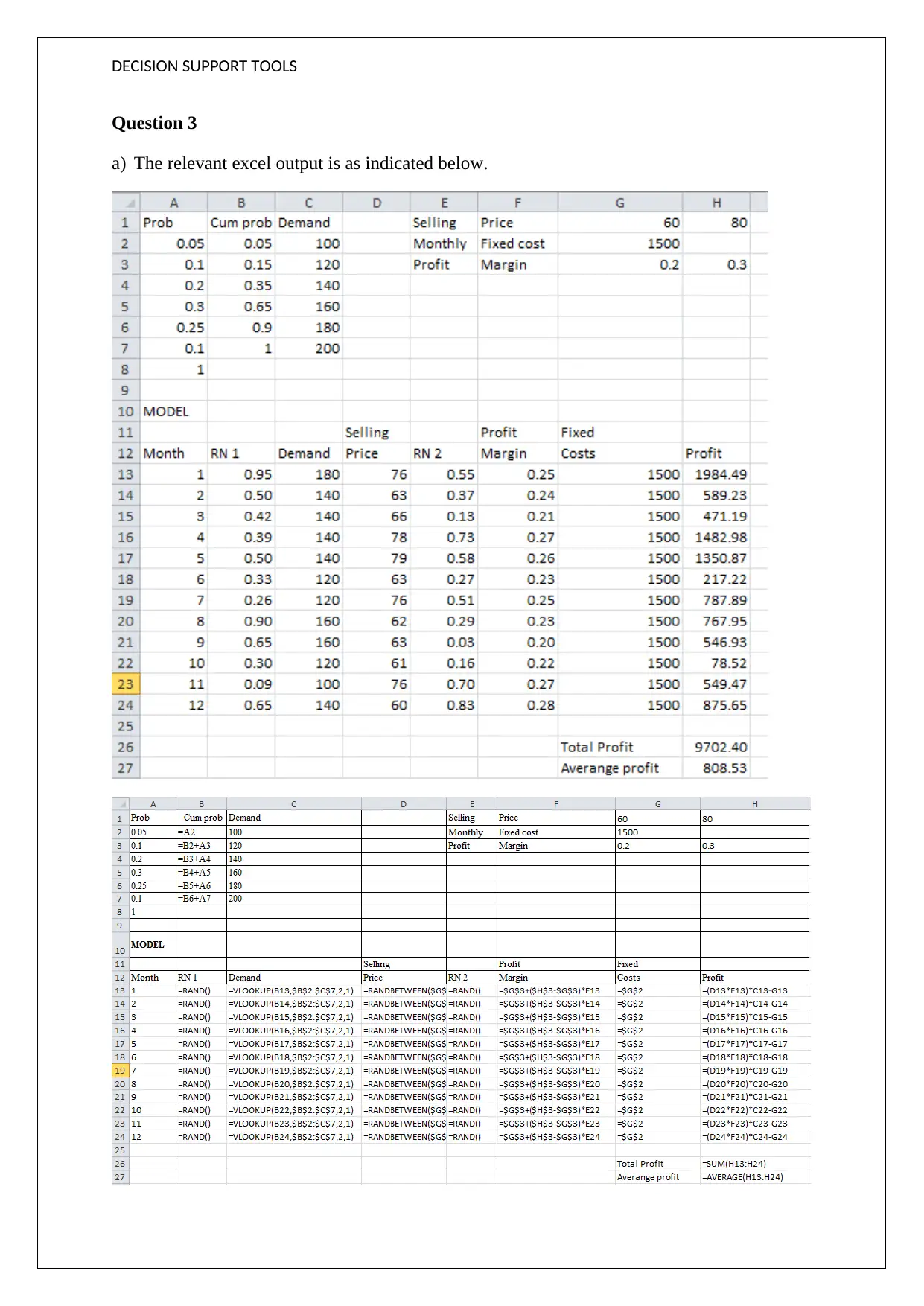

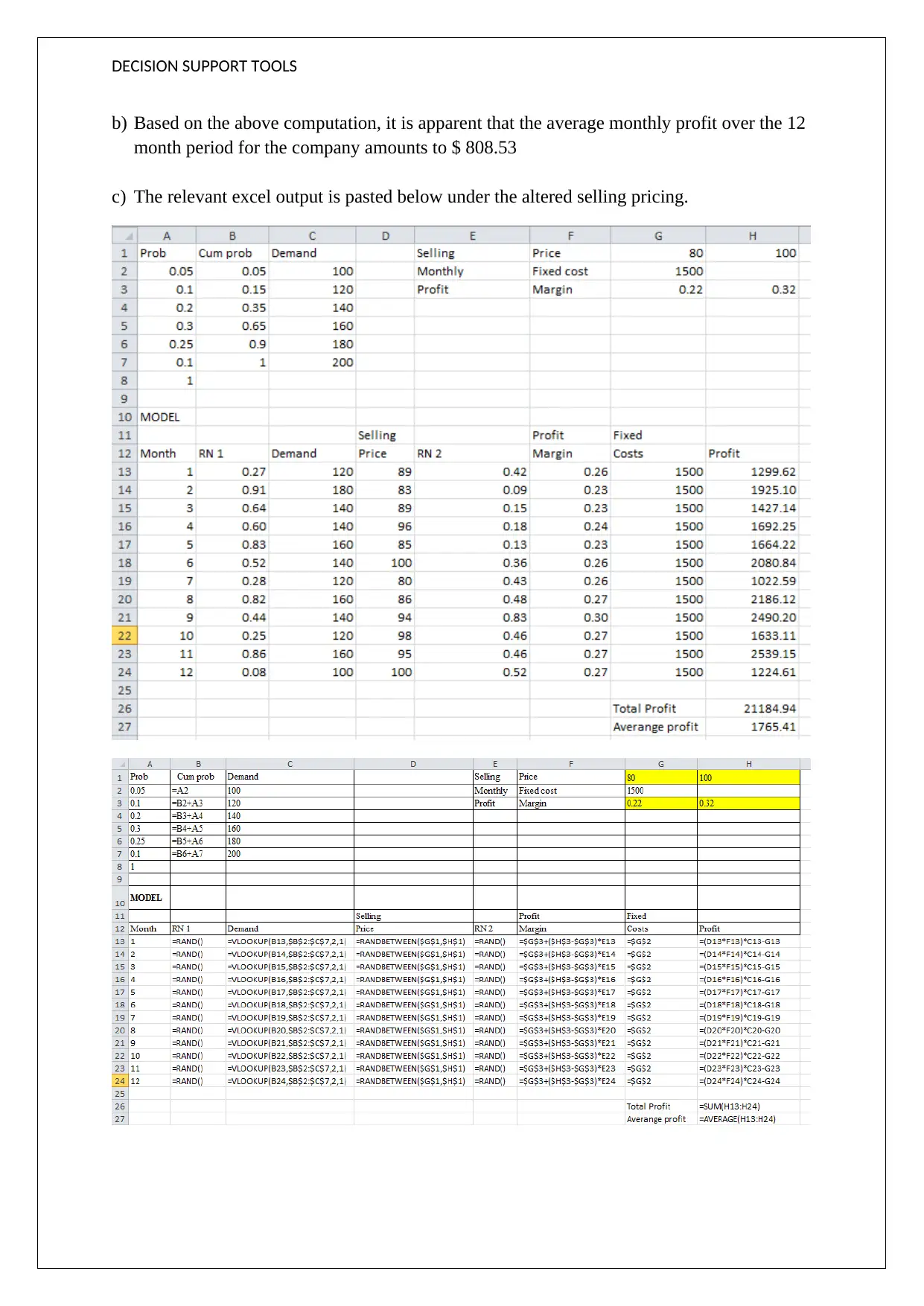

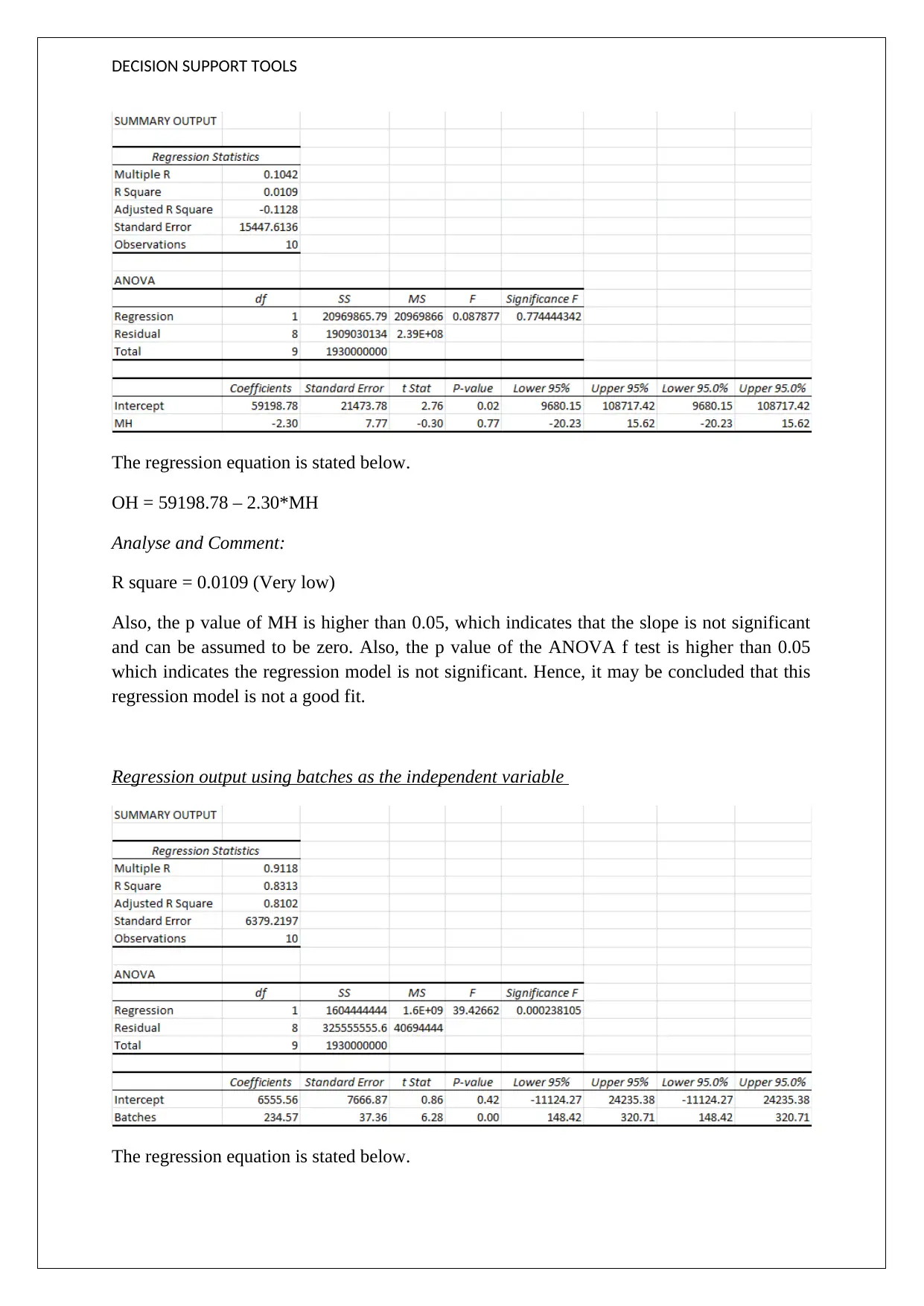

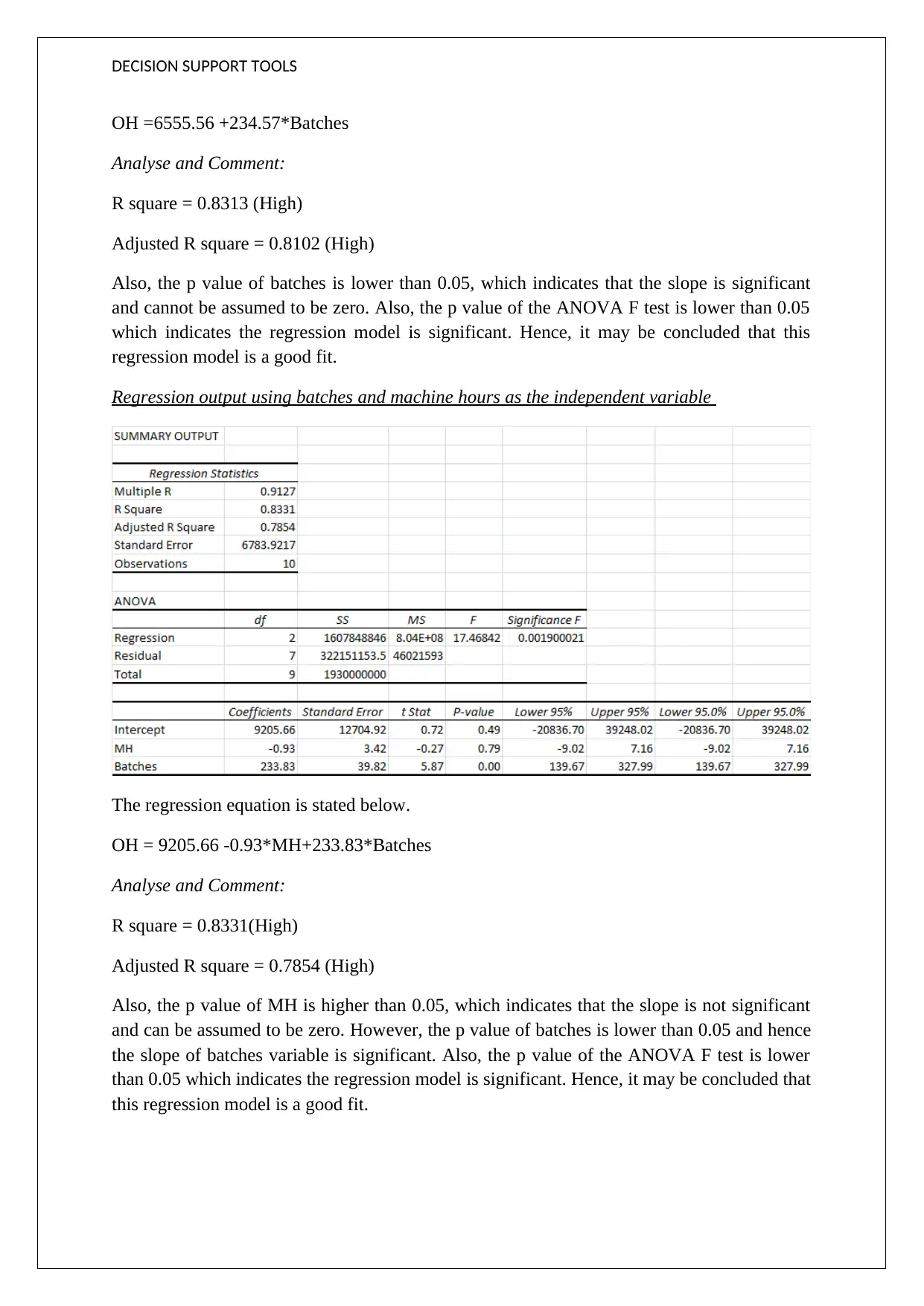

This assignment solution delves into the application of decision support tools for financial analysis. It begins with an analysis of profit changes due to price adjustments, including considerations of potential sales impacts. The solution then demonstrates the high-low method for determining regression coefficients and evaluates the effectiveness of different regression models (using machine hours and batches as independent variables) for estimating overhead costs, concluding that a regression model using batches is the best fit. Finally, the assignment addresses contribution margin analysis, break-even points, and target sales volume calculations for different products, considering both pre-tax and post-tax profit targets. The solution provides detailed calculations and explanations for each step, illustrating how financial data can be used to inform decision-making.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.