Financial Decision Making Report: Analysis of Tesco's Performance

VerifiedAdded on 2023/01/12

|12

|3773

|31

Report

AI Summary

This report undertakes a comprehensive analysis of Tesco's financial performance, evaluating the role of accounting and finance within the organization and its impact on decision-making. The report begins by critically assessing the functions of accounting and finance, highlighting their significance in budgeting, capital budgeting, financial statement preparation, tax management, cost control, cash flow management, and inventory management. The analysis extends to an examination of the negative aspects of accounting and finance, such as time consumption and the need for skilled employees. The core of the report involves calculating and interpreting key financial ratios, including Return on Capital Employed (ROCE), Net Profit Margin, and Current Ratio. These ratios are calculated using Tesco's financial data from 2018 and 2019, followed by a detailed commentary on the company's performance from an investor's perspective. The report also provides insights into Tesco's financial strengths and weaknesses, and the factors affecting its financial position, such as market conditions and economic policies.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Critically evaluating the role of accounting and finance.............................................................1

TASK 2............................................................................................................................................3

Calculating the five ratios and commenting on the performance of Tesco.................................3

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Critically evaluating the role of accounting and finance.............................................................1

TASK 2............................................................................................................................................3

Calculating the five ratios and commenting on the performance of Tesco.................................3

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial decision making is a procedure of analysing the financial performance of an

organisation by evaluating its financial information so that reliable decisions can be taken. This

process is related with financial analysis and performance evaluation of an organisation

(Agarwal and Mazumder, 2013). The main aim of this report is to build an understanding about

the financial aspects of an organisation which can help an investor to invest in a company. For

this purpose, a large scale retail organisation is selected which is Tesco. This is one of the best

supermarket retail organisations in United Kingdom established in the year 1919 and has

headquarters in Welwyn Garden City, England.

In this report, the functions of finance and accounting are analysed along with their critical

evaluation in order to explore their role in Tesco. In second task of this report, annual report of

Tesco is considered and then five different ratios are calculated. After the calculation, all these

ratios are used to provide a commentary on the financial performance of selected company from

the perspective of an investor.

TASK 1

Critically evaluating the role of accounting and finance

The term “finance” refers to the concept of analysing every financial transaction which is

conducted and processes by an organisation. Finance is a wider concept which includes

accounting. “Accounting” is a procedure of recording and analysing the transactions which an

organisation conducts in an accounting year.

The concepts of finance and accounting play various roles in an organisation. In context of

the selected organisation that is Tesco, role of these concepts are analysed below:

Budget & Budgetary Control: Budgetary control refers to the process of determination of

actual performance as compared to the standard or the budgeted performance. Budgetary control

is one of the key roles of accounting and finance function (Du and Zhou, 2012). It helps the

organisation to determine whether the business operations are directed towards the achievement

of organisational goals or targets. For example, in context of Tesco Ltd., accounting and finance

department has the responsibility to prepare budgets related to various departments and measure

the actual performance with the budgeted performance.

1

Financial decision making is a procedure of analysing the financial performance of an

organisation by evaluating its financial information so that reliable decisions can be taken. This

process is related with financial analysis and performance evaluation of an organisation

(Agarwal and Mazumder, 2013). The main aim of this report is to build an understanding about

the financial aspects of an organisation which can help an investor to invest in a company. For

this purpose, a large scale retail organisation is selected which is Tesco. This is one of the best

supermarket retail organisations in United Kingdom established in the year 1919 and has

headquarters in Welwyn Garden City, England.

In this report, the functions of finance and accounting are analysed along with their critical

evaluation in order to explore their role in Tesco. In second task of this report, annual report of

Tesco is considered and then five different ratios are calculated. After the calculation, all these

ratios are used to provide a commentary on the financial performance of selected company from

the perspective of an investor.

TASK 1

Critically evaluating the role of accounting and finance

The term “finance” refers to the concept of analysing every financial transaction which is

conducted and processes by an organisation. Finance is a wider concept which includes

accounting. “Accounting” is a procedure of recording and analysing the transactions which an

organisation conducts in an accounting year.

The concepts of finance and accounting play various roles in an organisation. In context of

the selected organisation that is Tesco, role of these concepts are analysed below:

Budget & Budgetary Control: Budgetary control refers to the process of determination of

actual performance as compared to the standard or the budgeted performance. Budgetary control

is one of the key roles of accounting and finance function (Du and Zhou, 2012). It helps the

organisation to determine whether the business operations are directed towards the achievement

of organisational goals or targets. For example, in context of Tesco Ltd., accounting and finance

department has the responsibility to prepare budgets related to various departments and measure

the actual performance with the budgeted performance.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital budgeting and investment appraisal: Ascertaining the profitability of any

investment opportunity and helping the management to choose the best alternative for capital

investment is another important role of finance department. It is the duty of finance managers of

the company to make sure that the funds of the organisation are being used optimally and all the

investments are made only after a thorough risk analysis.

Preparation of financial statements: One of the most important functions of accounting

and finance department is preparation of financial statements which helps the management to

determine the financial position of the company and examine any shortcomings in the financial

results obtained during any period. Preparation of financial statements helps in using various

tools such as ratio analysis which provide a better picture of the organisational performance. In

Tesco Ltd, various financial statements are analysed to understand the current financial position

of the company and the debt structure as well.

Handling tax issues- Accounting and finance department plays a crucial role in meeting

the tax requirements of the company. Evasion of tax is illegal and any fault in adhering to the tax

rules of the government can result into a huge amount of penalties charged to the organisation by

the tax department. Thus, it is very essential for the finance and accounting department to make

sure that all the tax rules are duly complied with.

Cost control- It is the duty of the finance and accounting managers of any organisation to

make policies and strategies which help in reduction of costs related to production, inventory

management, supply chains, distribution process etcetera (Koropp and et.al., 2014). Finance

department actively engages itself in classification of costs according to the return obtained by

incurring that cost or expenditure. It helps the business to achieve optimum utilisation of

resources. Any expenditure which is not fruitful and doesn’t yield any result for the organisation

is classified as waste expenditure by the finance department to help reducing costs and increasing

profit margin.

Managing cash flow- Working capital is very important for any business organisation to

ensure smooth functioning of its day to day business activities. Accounting and finance

departments make sure that there is enough cash flow within the organisation to meet the

working capital requirements and payment of any current liabilities. It helps the organisation to

execute the activities related to production and manufacturing of goods and services without any

hindrance (Kramer and Weber, 2012). The finance manager of Tesco ltd. makes sure that enough

2

investment opportunity and helping the management to choose the best alternative for capital

investment is another important role of finance department. It is the duty of finance managers of

the company to make sure that the funds of the organisation are being used optimally and all the

investments are made only after a thorough risk analysis.

Preparation of financial statements: One of the most important functions of accounting

and finance department is preparation of financial statements which helps the management to

determine the financial position of the company and examine any shortcomings in the financial

results obtained during any period. Preparation of financial statements helps in using various

tools such as ratio analysis which provide a better picture of the organisational performance. In

Tesco Ltd, various financial statements are analysed to understand the current financial position

of the company and the debt structure as well.

Handling tax issues- Accounting and finance department plays a crucial role in meeting

the tax requirements of the company. Evasion of tax is illegal and any fault in adhering to the tax

rules of the government can result into a huge amount of penalties charged to the organisation by

the tax department. Thus, it is very essential for the finance and accounting department to make

sure that all the tax rules are duly complied with.

Cost control- It is the duty of the finance and accounting managers of any organisation to

make policies and strategies which help in reduction of costs related to production, inventory

management, supply chains, distribution process etcetera (Koropp and et.al., 2014). Finance

department actively engages itself in classification of costs according to the return obtained by

incurring that cost or expenditure. It helps the business to achieve optimum utilisation of

resources. Any expenditure which is not fruitful and doesn’t yield any result for the organisation

is classified as waste expenditure by the finance department to help reducing costs and increasing

profit margin.

Managing cash flow- Working capital is very important for any business organisation to

ensure smooth functioning of its day to day business activities. Accounting and finance

departments make sure that there is enough cash flow within the organisation to meet the

working capital requirements and payment of any current liabilities. It helps the organisation to

execute the activities related to production and manufacturing of goods and services without any

hindrance (Kramer and Weber, 2012). The finance manager of Tesco ltd. makes sure that enough

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

working capital flows in the organisation for procurement of materials and meeting fixed

expenses of the company.

Inventory management – the concepts of accounting and finance helps in keeping a record

of inventory using methods such as FIFO or LIFO. In context of Tesco, this company is a retail

organisation which procures goods from suppliers and then retails them to end consumers. In this

process, it is important for this organisation to effective manage their inventory so that the threat

of theft and damage can be eliminated.

Effective decision making – The concepts of finance and accounting helps in the procedure

of developing financial statements and then analyse them using the methods such as ratio

analysis. By these methods, all stakeholders of Tesco can effective decide about the operations

and functions of the company.

Apart from the all positive roles of accounting and finance, there are few negative roles of

these concepts as well analysed below:

Time consuming – The process of accounting is a complex procedure which involves

various steps such as identifying of transactions, vouching, recording, analysing and exploring.

In order to complete all these steps, ample time is required. Tesco is a large scale organisation

which has huge number of transactions every day and in order to record them all, ample time is

acquired.

Highly skilled employees required – Another negative role which the concepts of

accounting and finance play is that the procedure of accounting requires highly skilled

employees. In order to develop an organisation’s finance statements which are appropriate

aligned with all the financial standards is a complex task which requires skills. Tesco is a large

company which can afford the wages of skilled employees but such employees are difficult to be

found.

From all the points above, it can be said that the concepts of finance and accounting plays an

important role in an organisation. It has been also analysed that along with various positive roles,

there are few negative roles as well which are played by these concepts.

TASK 2

Calculating the five ratios and commenting on the performance of Tesco

RETURN ON CAPITAL EMPLOYED

3

expenses of the company.

Inventory management – the concepts of accounting and finance helps in keeping a record

of inventory using methods such as FIFO or LIFO. In context of Tesco, this company is a retail

organisation which procures goods from suppliers and then retails them to end consumers. In this

process, it is important for this organisation to effective manage their inventory so that the threat

of theft and damage can be eliminated.

Effective decision making – The concepts of finance and accounting helps in the procedure

of developing financial statements and then analyse them using the methods such as ratio

analysis. By these methods, all stakeholders of Tesco can effective decide about the operations

and functions of the company.

Apart from the all positive roles of accounting and finance, there are few negative roles of

these concepts as well analysed below:

Time consuming – The process of accounting is a complex procedure which involves

various steps such as identifying of transactions, vouching, recording, analysing and exploring.

In order to complete all these steps, ample time is required. Tesco is a large scale organisation

which has huge number of transactions every day and in order to record them all, ample time is

acquired.

Highly skilled employees required – Another negative role which the concepts of

accounting and finance play is that the procedure of accounting requires highly skilled

employees. In order to develop an organisation’s finance statements which are appropriate

aligned with all the financial standards is a complex task which requires skills. Tesco is a large

company which can afford the wages of skilled employees but such employees are difficult to be

found.

From all the points above, it can be said that the concepts of finance and accounting plays an

important role in an organisation. It has been also analysed that along with various positive roles,

there are few negative roles as well which are played by these concepts.

TASK 2

Calculating the five ratios and commenting on the performance of Tesco

RETURN ON CAPITAL EMPLOYED

3

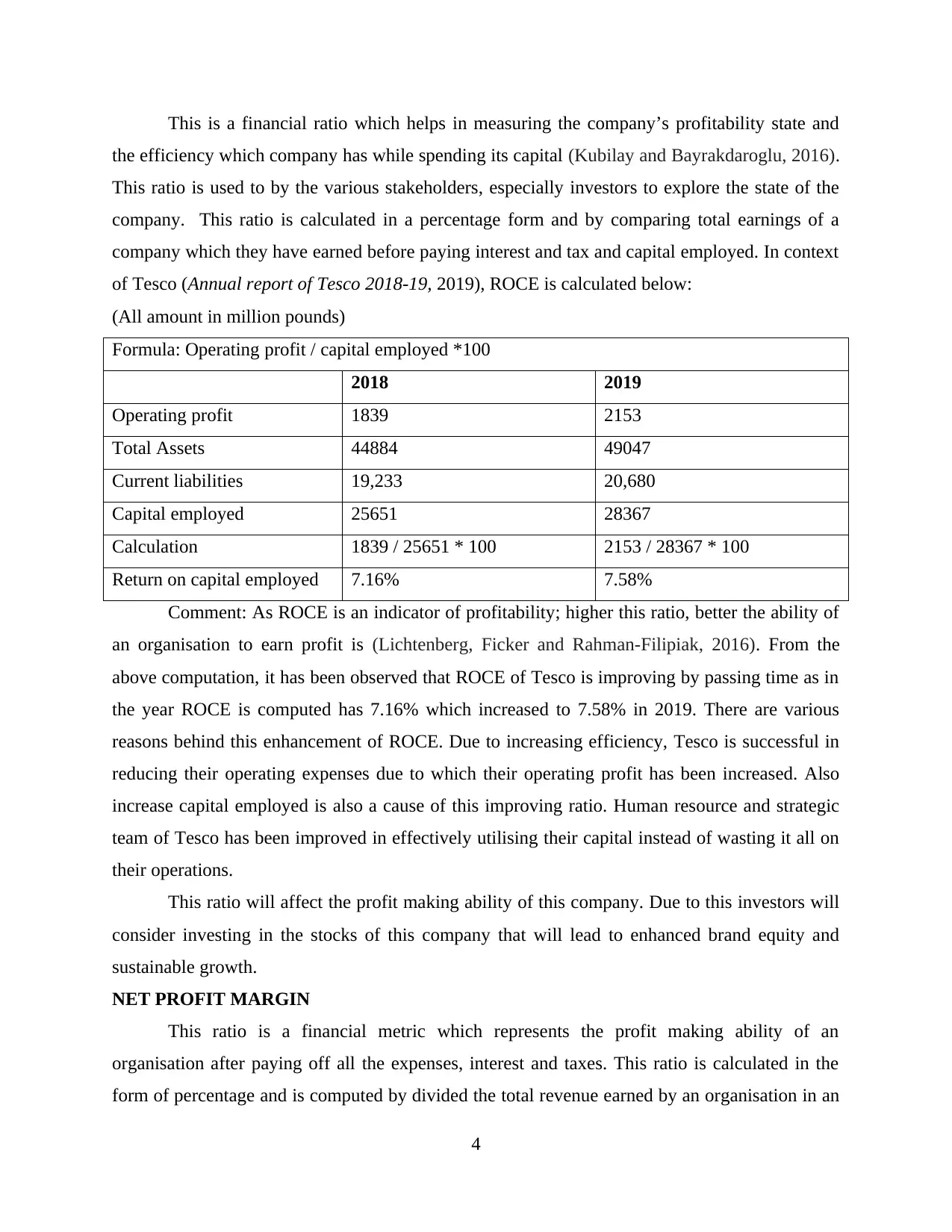

This is a financial ratio which helps in measuring the company’s profitability state and

the efficiency which company has while spending its capital (Kubilay and Bayrakdaroglu, 2016).

This ratio is used to by the various stakeholders, especially investors to explore the state of the

company. This ratio is calculated in a percentage form and by comparing total earnings of a

company which they have earned before paying interest and tax and capital employed. In context

of Tesco (Annual report of Tesco 2018-19, 2019), ROCE is calculated below:

(All amount in million pounds)

Formula: Operating profit / capital employed *100

2018 2019

Operating profit 1839 2153

Total Assets 44884 49047

Current liabilities 19,233 20,680

Capital employed 25651 28367

Calculation 1839 / 25651 * 100 2153 / 28367 * 100

Return on capital employed 7.16% 7.58%

Comment: As ROCE is an indicator of profitability; higher this ratio, better the ability of

an organisation to earn profit is (Lichtenberg, Ficker and Rahman-Filipiak, 2016). From the

above computation, it has been observed that ROCE of Tesco is improving by passing time as in

the year ROCE is computed has 7.16% which increased to 7.58% in 2019. There are various

reasons behind this enhancement of ROCE. Due to increasing efficiency, Tesco is successful in

reducing their operating expenses due to which their operating profit has been increased. Also

increase capital employed is also a cause of this improving ratio. Human resource and strategic

team of Tesco has been improved in effectively utilising their capital instead of wasting it all on

their operations.

This ratio will affect the profit making ability of this company. Due to this investors will

consider investing in the stocks of this company that will lead to enhanced brand equity and

sustainable growth.

NET PROFIT MARGIN

This ratio is a financial metric which represents the profit making ability of an

organisation after paying off all the expenses, interest and taxes. This ratio is calculated in the

form of percentage and is computed by divided the total revenue earned by an organisation in an

4

the efficiency which company has while spending its capital (Kubilay and Bayrakdaroglu, 2016).

This ratio is used to by the various stakeholders, especially investors to explore the state of the

company. This ratio is calculated in a percentage form and by comparing total earnings of a

company which they have earned before paying interest and tax and capital employed. In context

of Tesco (Annual report of Tesco 2018-19, 2019), ROCE is calculated below:

(All amount in million pounds)

Formula: Operating profit / capital employed *100

2018 2019

Operating profit 1839 2153

Total Assets 44884 49047

Current liabilities 19,233 20,680

Capital employed 25651 28367

Calculation 1839 / 25651 * 100 2153 / 28367 * 100

Return on capital employed 7.16% 7.58%

Comment: As ROCE is an indicator of profitability; higher this ratio, better the ability of

an organisation to earn profit is (Lichtenberg, Ficker and Rahman-Filipiak, 2016). From the

above computation, it has been observed that ROCE of Tesco is improving by passing time as in

the year ROCE is computed has 7.16% which increased to 7.58% in 2019. There are various

reasons behind this enhancement of ROCE. Due to increasing efficiency, Tesco is successful in

reducing their operating expenses due to which their operating profit has been increased. Also

increase capital employed is also a cause of this improving ratio. Human resource and strategic

team of Tesco has been improved in effectively utilising their capital instead of wasting it all on

their operations.

This ratio will affect the profit making ability of this company. Due to this investors will

consider investing in the stocks of this company that will lead to enhanced brand equity and

sustainable growth.

NET PROFIT MARGIN

This ratio is a financial metric which represents the profit making ability of an

organisation after paying off all the expenses, interest and taxes. This ratio is calculated in the

form of percentage and is computed by divided the total revenue earned by an organisation in an

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

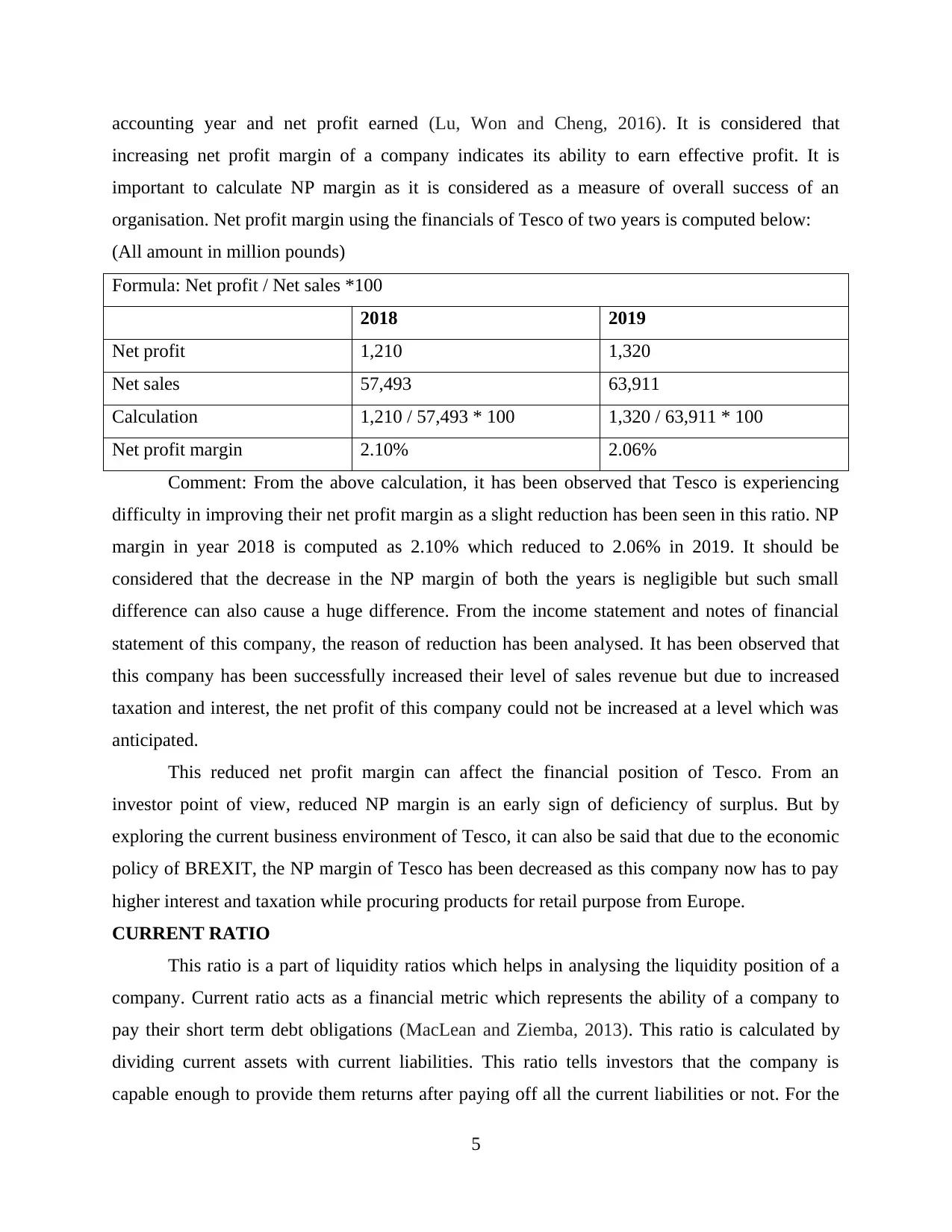

accounting year and net profit earned (Lu, Won and Cheng, 2016). It is considered that

increasing net profit margin of a company indicates its ability to earn effective profit. It is

important to calculate NP margin as it is considered as a measure of overall success of an

organisation. Net profit margin using the financials of Tesco of two years is computed below:

(All amount in million pounds)

Formula: Net profit / Net sales *100

2018 2019

Net profit 1,210 1,320

Net sales 57,493 63,911

Calculation 1,210 / 57,493 * 100 1,320 / 63,911 * 100

Net profit margin 2.10% 2.06%

Comment: From the above calculation, it has been observed that Tesco is experiencing

difficulty in improving their net profit margin as a slight reduction has been seen in this ratio. NP

margin in year 2018 is computed as 2.10% which reduced to 2.06% in 2019. It should be

considered that the decrease in the NP margin of both the years is negligible but such small

difference can also cause a huge difference. From the income statement and notes of financial

statement of this company, the reason of reduction has been analysed. It has been observed that

this company has been successfully increased their level of sales revenue but due to increased

taxation and interest, the net profit of this company could not be increased at a level which was

anticipated.

This reduced net profit margin can affect the financial position of Tesco. From an

investor point of view, reduced NP margin is an early sign of deficiency of surplus. But by

exploring the current business environment of Tesco, it can also be said that due to the economic

policy of BREXIT, the NP margin of Tesco has been decreased as this company now has to pay

higher interest and taxation while procuring products for retail purpose from Europe.

CURRENT RATIO

This ratio is a part of liquidity ratios which helps in analysing the liquidity position of a

company. Current ratio acts as a financial metric which represents the ability of a company to

pay their short term debt obligations (MacLean and Ziemba, 2013). This ratio is calculated by

dividing current assets with current liabilities. This ratio tells investors that the company is

capable enough to provide them returns after paying off all the current liabilities or not. For the

5

increasing net profit margin of a company indicates its ability to earn effective profit. It is

important to calculate NP margin as it is considered as a measure of overall success of an

organisation. Net profit margin using the financials of Tesco of two years is computed below:

(All amount in million pounds)

Formula: Net profit / Net sales *100

2018 2019

Net profit 1,210 1,320

Net sales 57,493 63,911

Calculation 1,210 / 57,493 * 100 1,320 / 63,911 * 100

Net profit margin 2.10% 2.06%

Comment: From the above calculation, it has been observed that Tesco is experiencing

difficulty in improving their net profit margin as a slight reduction has been seen in this ratio. NP

margin in year 2018 is computed as 2.10% which reduced to 2.06% in 2019. It should be

considered that the decrease in the NP margin of both the years is negligible but such small

difference can also cause a huge difference. From the income statement and notes of financial

statement of this company, the reason of reduction has been analysed. It has been observed that

this company has been successfully increased their level of sales revenue but due to increased

taxation and interest, the net profit of this company could not be increased at a level which was

anticipated.

This reduced net profit margin can affect the financial position of Tesco. From an

investor point of view, reduced NP margin is an early sign of deficiency of surplus. But by

exploring the current business environment of Tesco, it can also be said that due to the economic

policy of BREXIT, the NP margin of Tesco has been decreased as this company now has to pay

higher interest and taxation while procuring products for retail purpose from Europe.

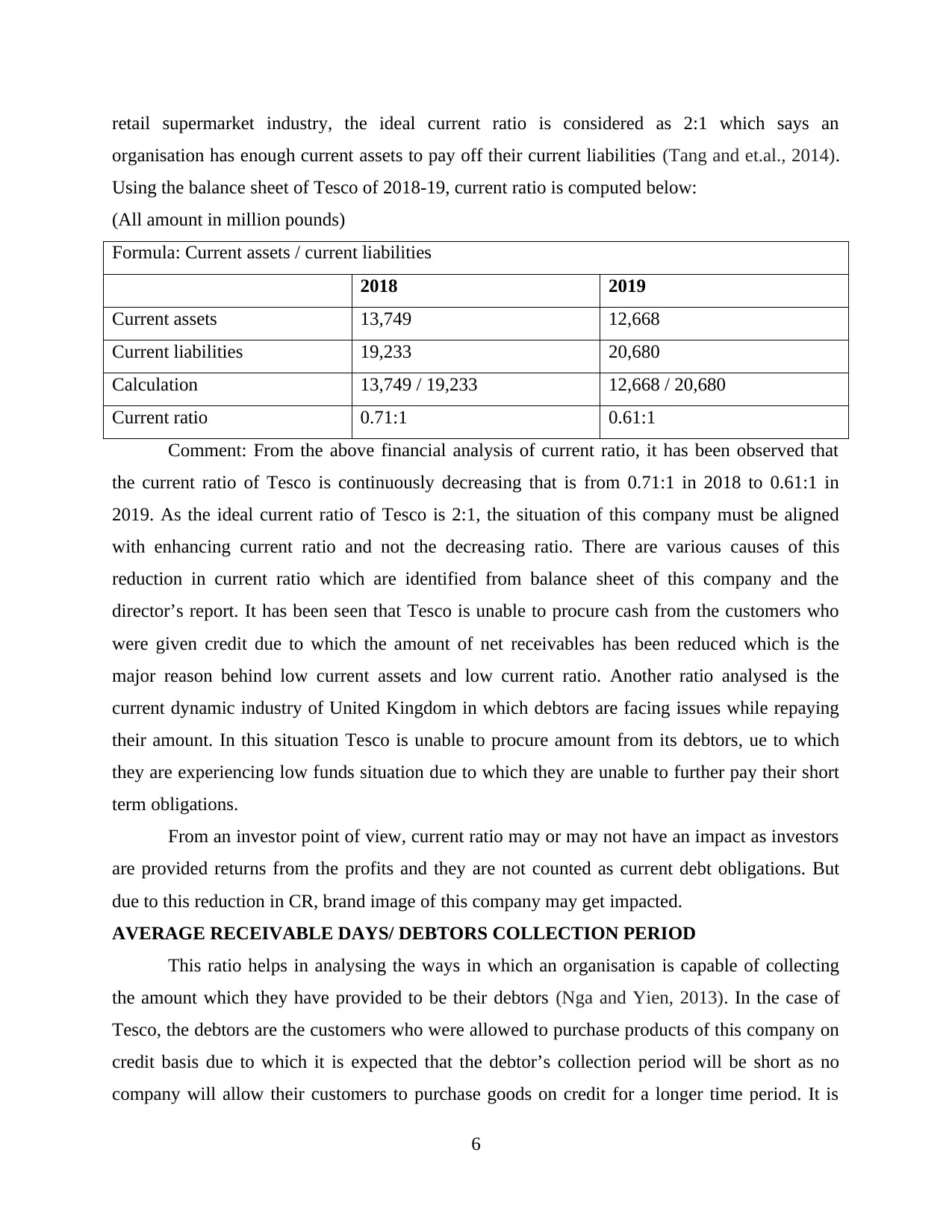

CURRENT RATIO

This ratio is a part of liquidity ratios which helps in analysing the liquidity position of a

company. Current ratio acts as a financial metric which represents the ability of a company to

pay their short term debt obligations (MacLean and Ziemba, 2013). This ratio is calculated by

dividing current assets with current liabilities. This ratio tells investors that the company is

capable enough to provide them returns after paying off all the current liabilities or not. For the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

retail supermarket industry, the ideal current ratio is considered as 2:1 which says an

organisation has enough current assets to pay off their current liabilities (Tang and et.al., 2014).

Using the balance sheet of Tesco of 2018-19, current ratio is computed below:

(All amount in million pounds)

Formula: Current assets / current liabilities

2018 2019

Current assets 13,749 12,668

Current liabilities 19,233 20,680

Calculation 13,749 / 19,233 12,668 / 20,680

Current ratio 0.71:1 0.61:1

Comment: From the above financial analysis of current ratio, it has been observed that

the current ratio of Tesco is continuously decreasing that is from 0.71:1 in 2018 to 0.61:1 in

2019. As the ideal current ratio of Tesco is 2:1, the situation of this company must be aligned

with enhancing current ratio and not the decreasing ratio. There are various causes of this

reduction in current ratio which are identified from balance sheet of this company and the

director’s report. It has been seen that Tesco is unable to procure cash from the customers who

were given credit due to which the amount of net receivables has been reduced which is the

major reason behind low current assets and low current ratio. Another ratio analysed is the

current dynamic industry of United Kingdom in which debtors are facing issues while repaying

their amount. In this situation Tesco is unable to procure amount from its debtors, ue to which

they are experiencing low funds situation due to which they are unable to further pay their short

term obligations.

From an investor point of view, current ratio may or may not have an impact as investors

are provided returns from the profits and they are not counted as current debt obligations. But

due to this reduction in CR, brand image of this company may get impacted.

AVERAGE RECEIVABLE DAYS/ DEBTORS COLLECTION PERIOD

This ratio helps in analysing the ways in which an organisation is capable of collecting

the amount which they have provided to be their debtors (Nga and Yien, 2013). In the case of

Tesco, the debtors are the customers who were allowed to purchase products of this company on

credit basis due to which it is expected that the debtor’s collection period will be short as no

company will allow their customers to purchase goods on credit for a longer time period. It is

6

organisation has enough current assets to pay off their current liabilities (Tang and et.al., 2014).

Using the balance sheet of Tesco of 2018-19, current ratio is computed below:

(All amount in million pounds)

Formula: Current assets / current liabilities

2018 2019

Current assets 13,749 12,668

Current liabilities 19,233 20,680

Calculation 13,749 / 19,233 12,668 / 20,680

Current ratio 0.71:1 0.61:1

Comment: From the above financial analysis of current ratio, it has been observed that

the current ratio of Tesco is continuously decreasing that is from 0.71:1 in 2018 to 0.61:1 in

2019. As the ideal current ratio of Tesco is 2:1, the situation of this company must be aligned

with enhancing current ratio and not the decreasing ratio. There are various causes of this

reduction in current ratio which are identified from balance sheet of this company and the

director’s report. It has been seen that Tesco is unable to procure cash from the customers who

were given credit due to which the amount of net receivables has been reduced which is the

major reason behind low current assets and low current ratio. Another ratio analysed is the

current dynamic industry of United Kingdom in which debtors are facing issues while repaying

their amount. In this situation Tesco is unable to procure amount from its debtors, ue to which

they are experiencing low funds situation due to which they are unable to further pay their short

term obligations.

From an investor point of view, current ratio may or may not have an impact as investors

are provided returns from the profits and they are not counted as current debt obligations. But

due to this reduction in CR, brand image of this company may get impacted.

AVERAGE RECEIVABLE DAYS/ DEBTORS COLLECTION PERIOD

This ratio helps in analysing the ways in which an organisation is capable of collecting

the amount which they have provided to be their debtors (Nga and Yien, 2013). In the case of

Tesco, the debtors are the customers who were allowed to purchase products of this company on

credit basis due to which it is expected that the debtor’s collection period will be short as no

company will allow their customers to purchase goods on credit for a longer time period. It is

6

considered then less this ratio is, effective company’s position in market is. Using the sales

revenue procured from income statement and trade debtors procured from balance sheet, this

ratio is calculated below:

(All amount in million pounds)

Formula: trade debtors / revenue * 365

2018 2019

Trade debtors 1,504 1,640

Revenue 57,493 63,911

Calculation 1,504 / 57,493 * 365 1,640 / 63,911 * 365

Debtors collection period 9.54 days 9.36 days

Comment: From the above financial analysis of this ratio, it has been analysed that

financial performance of Tesco is improving. The debtor’s collection period which is computed

above represents that in year 2018, Tesco was able to procure their amount from their debtors in

9.54 days which reduced in 2019 as 9.36 days. As a day cannot be divided in decimals but it this

exact calculation presents that the ability of collecting the amount is improving. There are

various causes of this improvements; one of the major cause is change in the policies of Tesco

which state that as the revenue of this company is improving, the policies must be reviewed

again.

This improved ratio will have the impact on its brand image and equity by which

investors will be satisfied to invest in this company. From the perspective of an investor,

investors will think that Tesco is capable of procuring their debt amount effectively which means

they can provide returns on time.

AVERAGE PAYABLE DAYS/ CREDITORS COLLECTION PERIOD

This ratio represents the time period in which Tesco is able to pay off their creditors. In

the context of Tesco, the creditors are the suppliers from which goods are procured by Tesco for

smooth functioning (Patel and et.al., 2012). According to the Tesco policies analysed from their

annual report, Tesco pay off their suppliers when most of their goods are sold due to which the

creditor’s collection period is greater than debtor’s collection period. Using the trade payables

from balance sheet and cost of sales from income statement, this ratio is calculated below:

(All amount in million pounds)

Formula: trade payables / cost of sales * 365

7

revenue procured from income statement and trade debtors procured from balance sheet, this

ratio is calculated below:

(All amount in million pounds)

Formula: trade debtors / revenue * 365

2018 2019

Trade debtors 1,504 1,640

Revenue 57,493 63,911

Calculation 1,504 / 57,493 * 365 1,640 / 63,911 * 365

Debtors collection period 9.54 days 9.36 days

Comment: From the above financial analysis of this ratio, it has been analysed that

financial performance of Tesco is improving. The debtor’s collection period which is computed

above represents that in year 2018, Tesco was able to procure their amount from their debtors in

9.54 days which reduced in 2019 as 9.36 days. As a day cannot be divided in decimals but it this

exact calculation presents that the ability of collecting the amount is improving. There are

various causes of this improvements; one of the major cause is change in the policies of Tesco

which state that as the revenue of this company is improving, the policies must be reviewed

again.

This improved ratio will have the impact on its brand image and equity by which

investors will be satisfied to invest in this company. From the perspective of an investor,

investors will think that Tesco is capable of procuring their debt amount effectively which means

they can provide returns on time.

AVERAGE PAYABLE DAYS/ CREDITORS COLLECTION PERIOD

This ratio represents the time period in which Tesco is able to pay off their creditors. In

the context of Tesco, the creditors are the suppliers from which goods are procured by Tesco for

smooth functioning (Patel and et.al., 2012). According to the Tesco policies analysed from their

annual report, Tesco pay off their suppliers when most of their goods are sold due to which the

creditor’s collection period is greater than debtor’s collection period. Using the trade payables

from balance sheet and cost of sales from income statement, this ratio is calculated below:

(All amount in million pounds)

Formula: trade payables / cost of sales * 365

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 2019

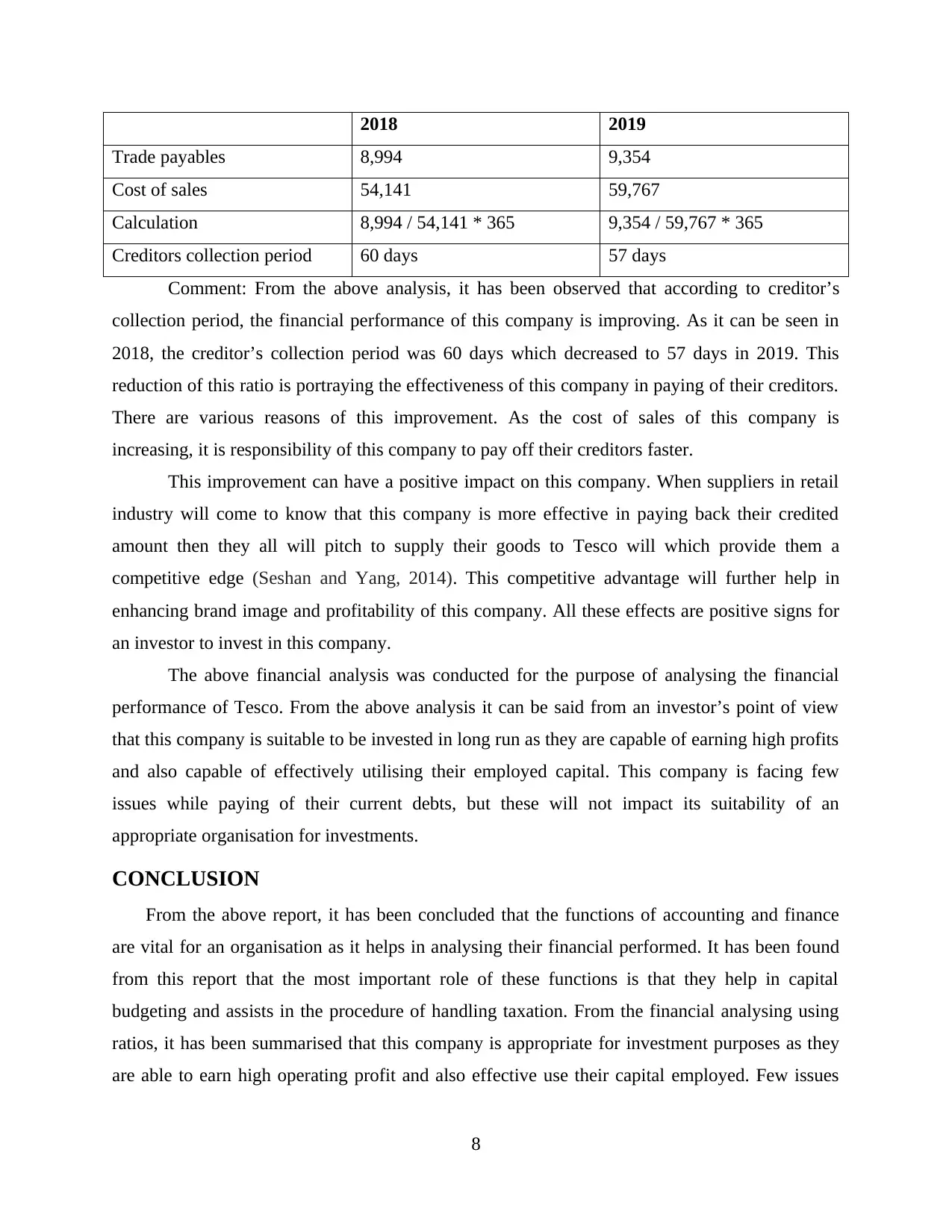

Trade payables 8,994 9,354

Cost of sales 54,141 59,767

Calculation 8,994 / 54,141 * 365 9,354 / 59,767 * 365

Creditors collection period 60 days 57 days

Comment: From the above analysis, it has been observed that according to creditor’s

collection period, the financial performance of this company is improving. As it can be seen in

2018, the creditor’s collection period was 60 days which decreased to 57 days in 2019. This

reduction of this ratio is portraying the effectiveness of this company in paying of their creditors.

There are various reasons of this improvement. As the cost of sales of this company is

increasing, it is responsibility of this company to pay off their creditors faster.

This improvement can have a positive impact on this company. When suppliers in retail

industry will come to know that this company is more effective in paying back their credited

amount then they all will pitch to supply their goods to Tesco will which provide them a

competitive edge (Seshan and Yang, 2014). This competitive advantage will further help in

enhancing brand image and profitability of this company. All these effects are positive signs for

an investor to invest in this company.

The above financial analysis was conducted for the purpose of analysing the financial

performance of Tesco. From the above analysis it can be said from an investor’s point of view

that this company is suitable to be invested in long run as they are capable of earning high profits

and also capable of effectively utilising their employed capital. This company is facing few

issues while paying of their current debts, but these will not impact its suitability of an

appropriate organisation for investments.

CONCLUSION

From the above report, it has been concluded that the functions of accounting and finance

are vital for an organisation as it helps in analysing their financial performed. It has been found

from this report that the most important role of these functions is that they help in capital

budgeting and assists in the procedure of handling taxation. From the financial analysing using

ratios, it has been summarised that this company is appropriate for investment purposes as they

are able to earn high operating profit and also effective use their capital employed. Few issues

8

Trade payables 8,994 9,354

Cost of sales 54,141 59,767

Calculation 8,994 / 54,141 * 365 9,354 / 59,767 * 365

Creditors collection period 60 days 57 days

Comment: From the above analysis, it has been observed that according to creditor’s

collection period, the financial performance of this company is improving. As it can be seen in

2018, the creditor’s collection period was 60 days which decreased to 57 days in 2019. This

reduction of this ratio is portraying the effectiveness of this company in paying of their creditors.

There are various reasons of this improvement. As the cost of sales of this company is

increasing, it is responsibility of this company to pay off their creditors faster.

This improvement can have a positive impact on this company. When suppliers in retail

industry will come to know that this company is more effective in paying back their credited

amount then they all will pitch to supply their goods to Tesco will which provide them a

competitive edge (Seshan and Yang, 2014). This competitive advantage will further help in

enhancing brand image and profitability of this company. All these effects are positive signs for

an investor to invest in this company.

The above financial analysis was conducted for the purpose of analysing the financial

performance of Tesco. From the above analysis it can be said from an investor’s point of view

that this company is suitable to be invested in long run as they are capable of earning high profits

and also capable of effectively utilising their employed capital. This company is facing few

issues while paying of their current debts, but these will not impact its suitability of an

appropriate organisation for investments.

CONCLUSION

From the above report, it has been concluded that the functions of accounting and finance

are vital for an organisation as it helps in analysing their financial performed. It has been found

from this report that the most important role of these functions is that they help in capital

budgeting and assists in the procedure of handling taxation. From the financial analysing using

ratios, it has been summarised that this company is appropriate for investment purposes as they

are able to earn high operating profit and also effective use their capital employed. Few issues

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

gained from this analysis are the difficulties which this company face due to current business

environment of United Kingdom.

9

environment of United Kingdom.

9

REFERENCES

Books and Journals

Agarwal, S. and Mazumder, B., 2013. Cognitive abilities and household financial decision

making. American Economic Journal: Applied Economics. 5(1). pp.193-207.

Du, J. and Zhou, L., 2012. Improving financial data quality using ontologies. Decision Support

Systems. 54(1). pp.76-86.

Koropp, C. and et.al., 2014. Financial decision making in family firms: An adaptation of the

theory of planned behavior. Family Business Review. 27(4). pp.307-327.

Kramer, L.A. and Weber, J.M., 2012. This is your portfolio on winter: seasonal affective

disorder and risk aversion in financial decision making. Social Psychological and

Personality Science. 3(2). pp.193-199.

Kubilay, B. and Bayrakdaroglu, A., 2016. An empirical research on investor biases in financial

decision-making, financial risk tolerance and financial personality. International Journal

of Financial Research. 7(2). pp.171-182.

Lichtenberg, P.A., Ficker, L.J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of elder

abuse & neglect. 28(1). pp.14-33.

Lu, Q., Won, J. and Cheng, J.C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management. 34(1). pp.3-21.

MacLean, L.C. and Ziemba, W.T., 2013. Handbook of the fundamentals of financial decision

making (Vol. 4). World Scientific.

Nga, J.K. and Yien, L.K., 2013. The influence of personality trait and demographics on financial

decision making among Generation Y. Young Consumers.

Patel, S.R. and et.al., 2012. Single-neuron responses in the human nucleus accumbens during a

financial decision-making task. Journal of Neuroscience. 32(21). pp.7311-7315.

Seshan, G. and Yang, D., 2014. Motivating migrants: A field experiment on financial decision-

making in transnational households. Journal of Development Economics. 108. pp.119-

127.

Tang, F. and et.al., 2014. The effects of visualization and interactivity on calibration in financial

decision-making. Behavioral Research in Accounting. 26(1). pp.25-58.

Online

Annual report of Tesco 2018-19. 2019. [Online]. Available through:

<https://www.tescoplc.com/media/476422/tesco_ara2019_full_report_web.pdf>

10

Books and Journals

Agarwal, S. and Mazumder, B., 2013. Cognitive abilities and household financial decision

making. American Economic Journal: Applied Economics. 5(1). pp.193-207.

Du, J. and Zhou, L., 2012. Improving financial data quality using ontologies. Decision Support

Systems. 54(1). pp.76-86.

Koropp, C. and et.al., 2014. Financial decision making in family firms: An adaptation of the

theory of planned behavior. Family Business Review. 27(4). pp.307-327.

Kramer, L.A. and Weber, J.M., 2012. This is your portfolio on winter: seasonal affective

disorder and risk aversion in financial decision making. Social Psychological and

Personality Science. 3(2). pp.193-199.

Kubilay, B. and Bayrakdaroglu, A., 2016. An empirical research on investor biases in financial

decision-making, financial risk tolerance and financial personality. International Journal

of Financial Research. 7(2). pp.171-182.

Lichtenberg, P.A., Ficker, L.J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of elder

abuse & neglect. 28(1). pp.14-33.

Lu, Q., Won, J. and Cheng, J.C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management. 34(1). pp.3-21.

MacLean, L.C. and Ziemba, W.T., 2013. Handbook of the fundamentals of financial decision

making (Vol. 4). World Scientific.

Nga, J.K. and Yien, L.K., 2013. The influence of personality trait and demographics on financial

decision making among Generation Y. Young Consumers.

Patel, S.R. and et.al., 2012. Single-neuron responses in the human nucleus accumbens during a

financial decision-making task. Journal of Neuroscience. 32(21). pp.7311-7315.

Seshan, G. and Yang, D., 2014. Motivating migrants: A field experiment on financial decision-

making in transnational households. Journal of Development Economics. 108. pp.119-

127.

Tang, F. and et.al., 2014. The effects of visualization and interactivity on calibration in financial

decision-making. Behavioral Research in Accounting. 26(1). pp.25-58.

Online

Annual report of Tesco 2018-19. 2019. [Online]. Available through:

<https://www.tescoplc.com/media/476422/tesco_ara2019_full_report_web.pdf>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.