Financial Analysis, Budgeting, and Investment Decisions

VerifiedAdded on 2020/05/04

|7

|1074

|35

Homework Assignment

AI Summary

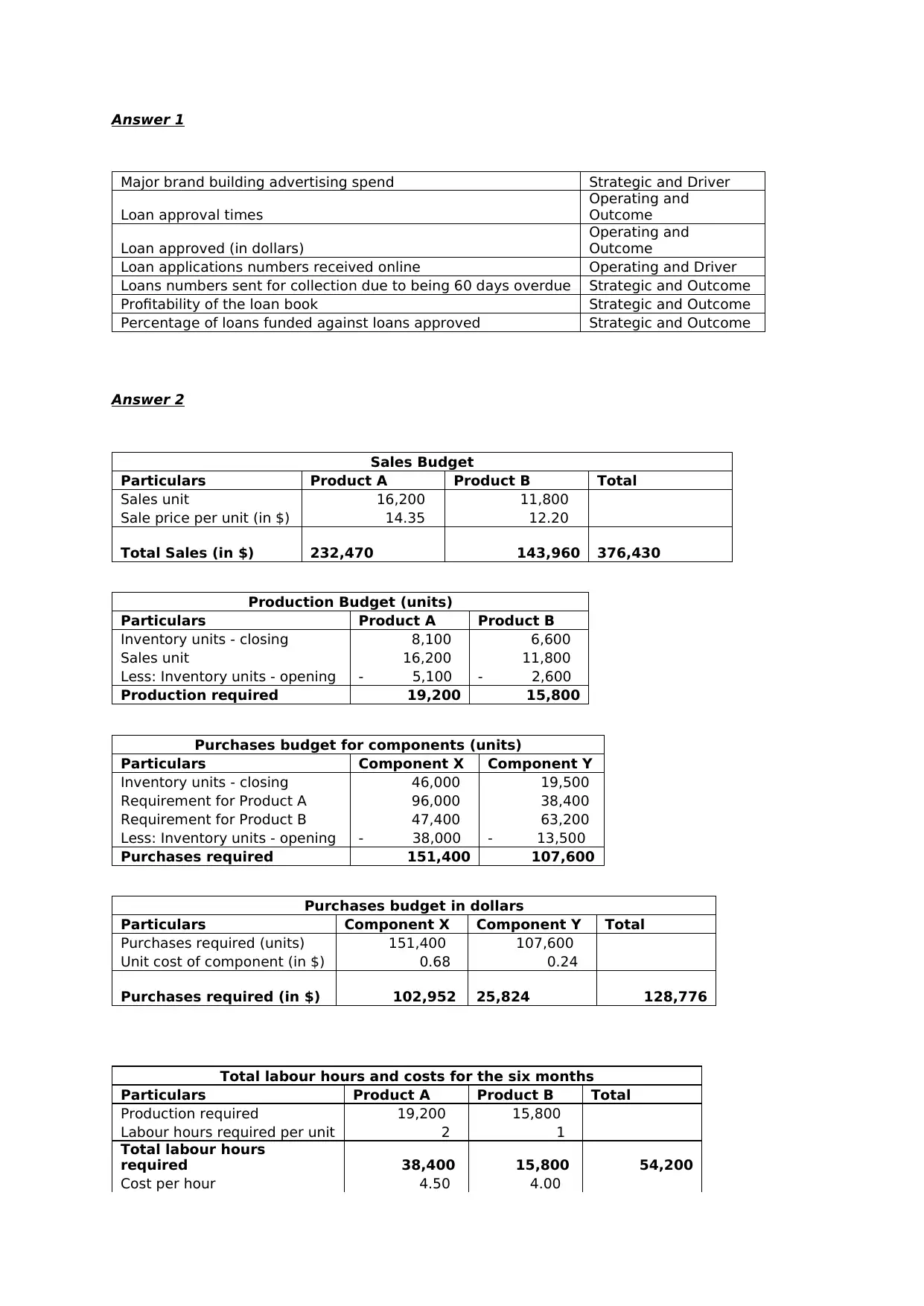

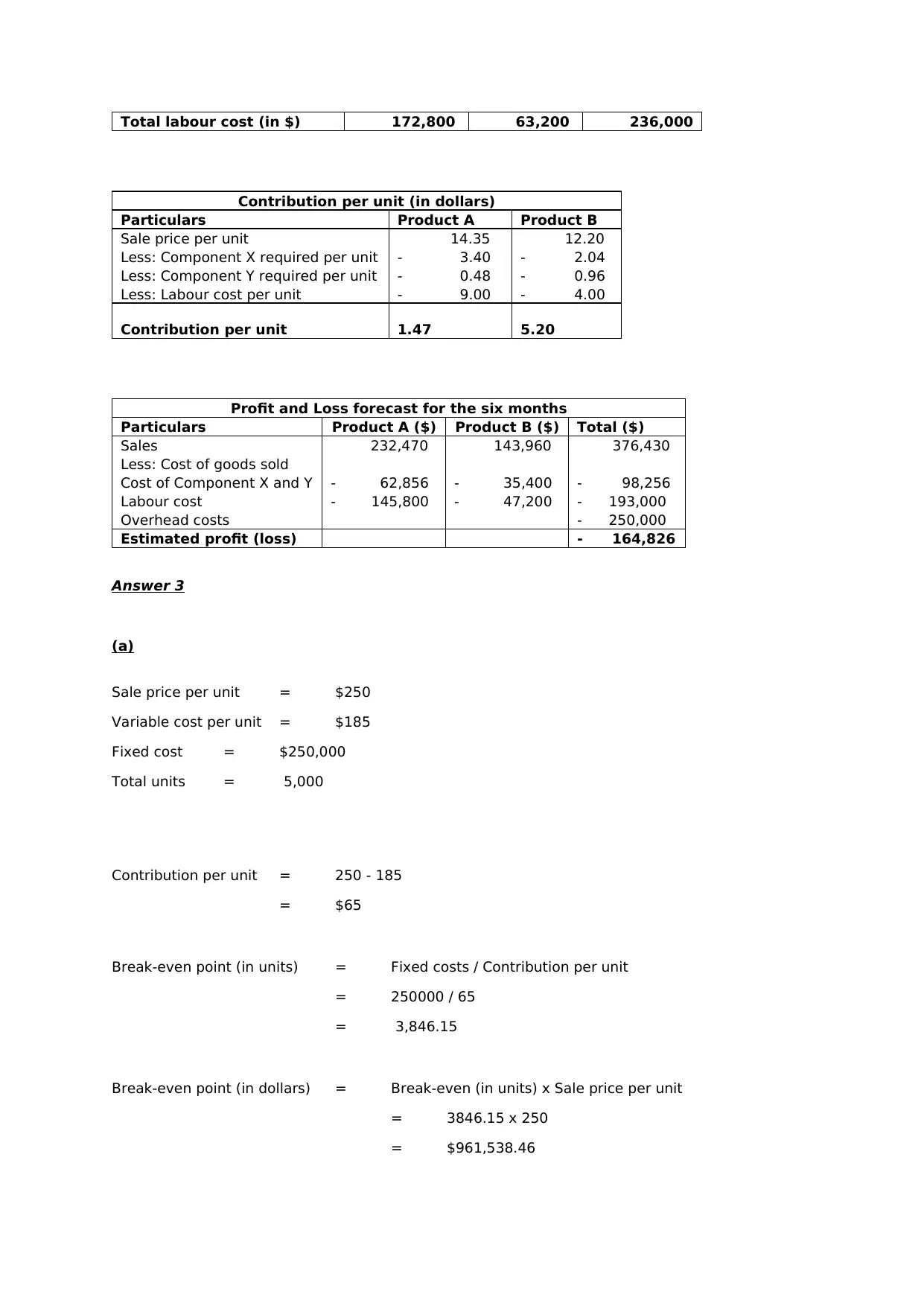

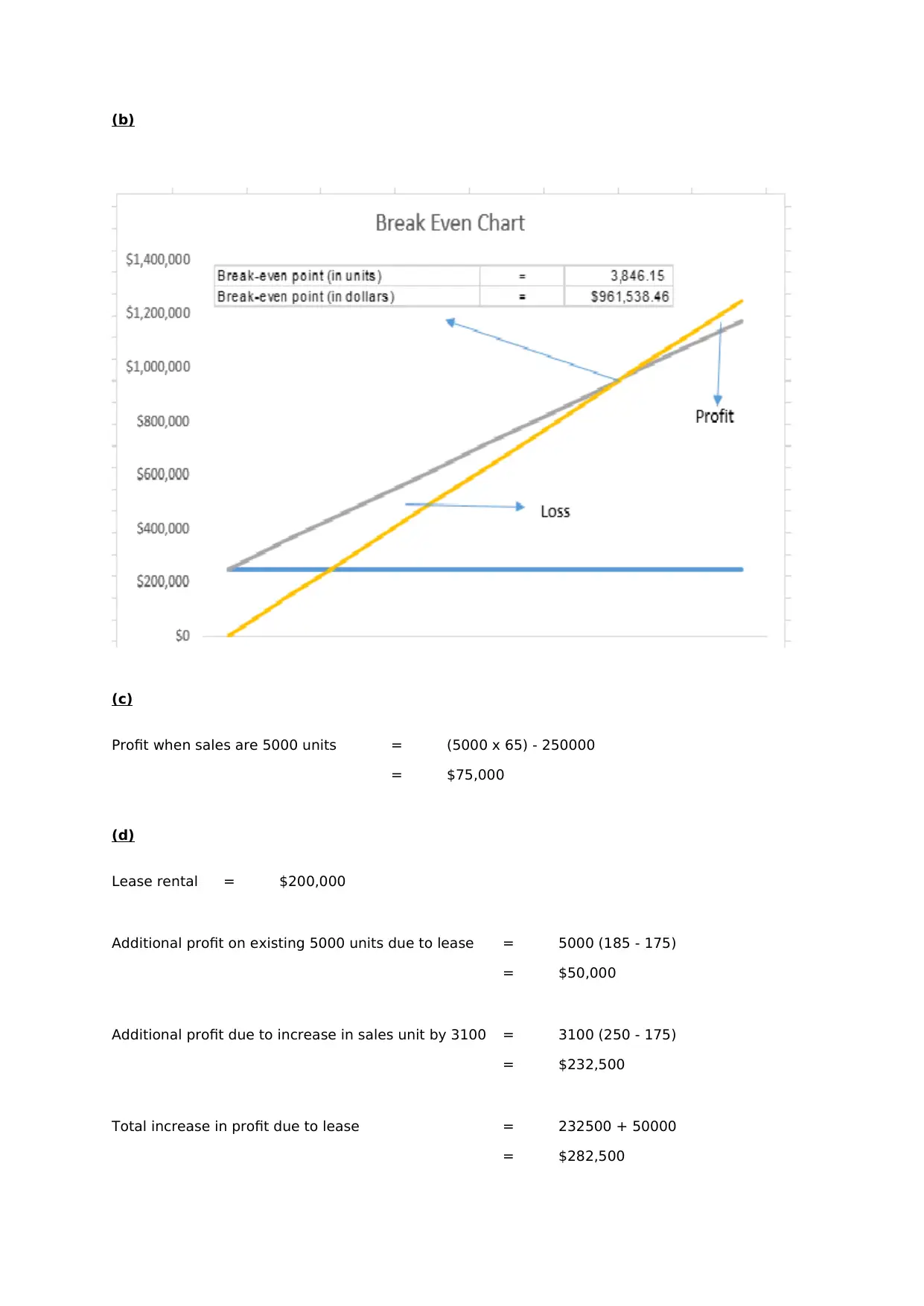

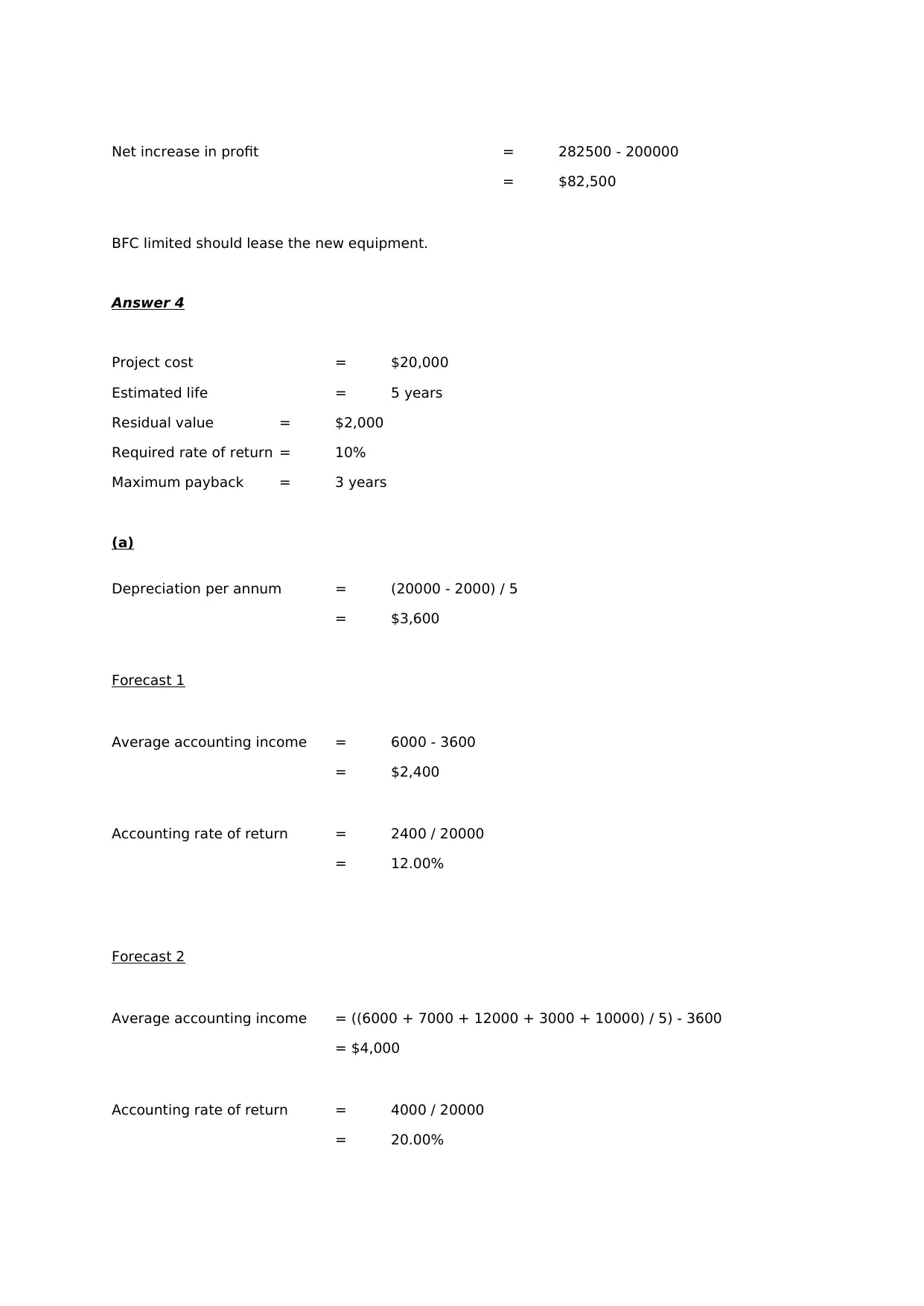

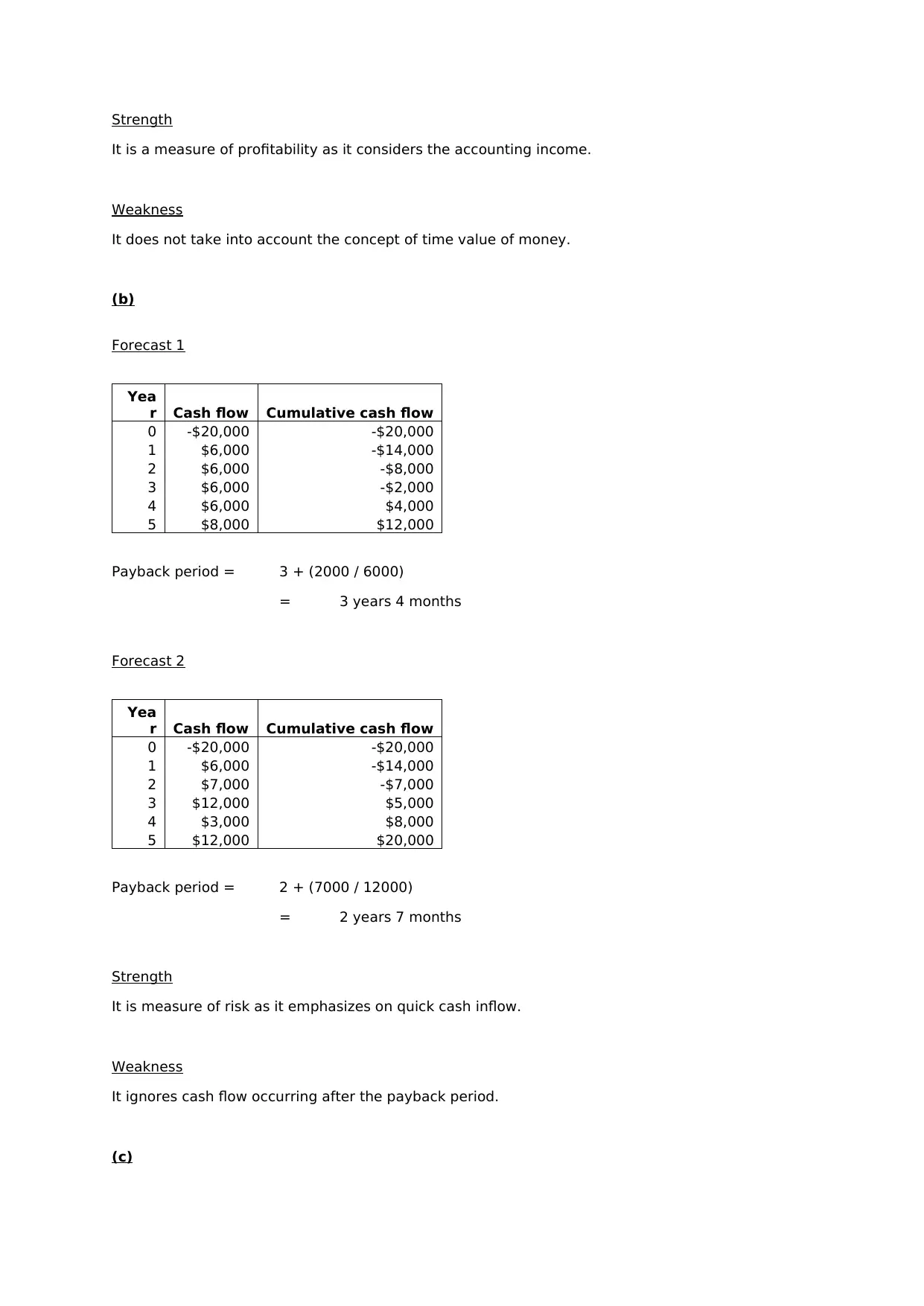

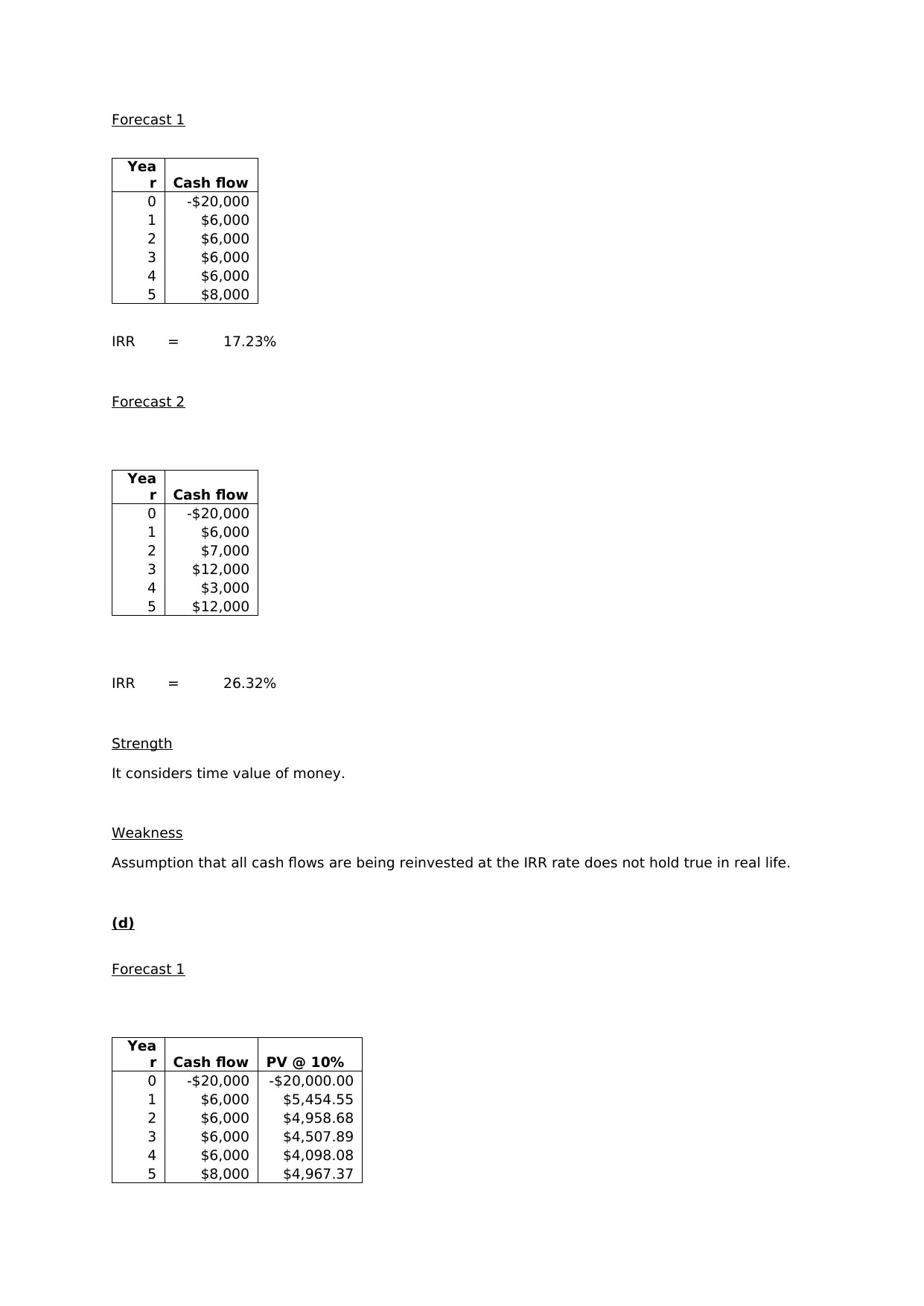

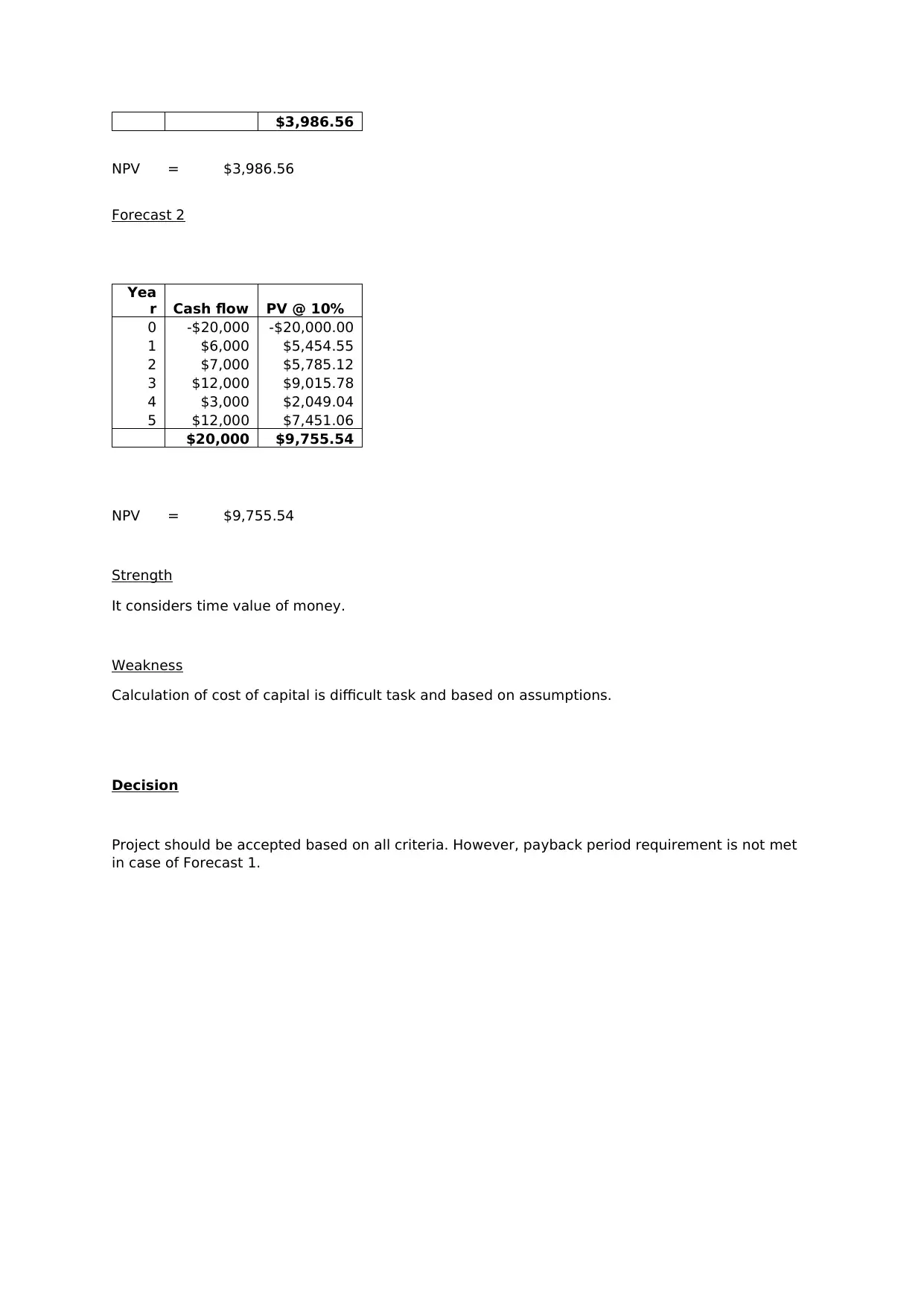

This assignment provides a comprehensive financial analysis, covering various aspects of financial planning and decision-making. It begins with an analysis of key performance indicators, including advertising spend, loan approval times, and profitability metrics. The assignment then delves into sales and production budgeting, including detailed calculations for product sales, production requirements, and component purchases. A profit and loss forecast is also included, projecting financial performance over a six-month period. Further, the assignment explores break-even analysis, determining the break-even point in units and dollars, and assessing the impact of leasing equipment on profitability. Finally, the assignment evaluates investment decisions using different appraisal techniques, such as accounting rate of return, payback period, internal rate of return, and net present value, providing a comparative analysis of the strengths and weaknesses of each method.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.