Financial Decision Making: Accounting Functions & Ratio Analysis

VerifiedAdded on 2023/06/14

|14

|3734

|71

Report

AI Summary

This report critically evaluates the role of accounting and financial functions in financial decision-making, using Alpha Limited as a case study. It begins by defining financial decision-making and highlighting its importance in organizational finance. The report then assesses accounting functions, including tracking, recording, and reporting financial transactions, and finance functions, such as financing, investment, and dividend decisions. It uses examples from Alpha Ltd to illustrate these functions' impact on operational efficiency. The report calculates and analyzes key financial ratios for Alpha Limited for the years 2017 and 2018, including Return on Capital Employed, Net Profit Margin Ratio, Current Ratio, Average Receivable Days, and Average Payable Days. Based on these ratios, it comments on the company's performance from an investor's perspective, noting areas of concern and potential risks. The report concludes by emphasizing the inseparable and essential nature of accounting and finance activities in ensuring organizational resilience and competitive advantage.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1- ..........................................................................................................................................3

ACCOUNTING AND FINANCIAL FUNCTIONS-..................................................................3

TASK 2-...........................................................................................................................................6

(A) CALCULATION OF RATIOS- ...........................................................................................6

(B) COMMENTS ON THE PERFORMANCE OF ALPHA LIMITED- ..................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1- ..........................................................................................................................................3

ACCOUNTING AND FINANCIAL FUNCTIONS-..................................................................3

TASK 2-...........................................................................................................................................6

(A) CALCULATION OF RATIOS- ...........................................................................................6

(B) COMMENTS ON THE PERFORMANCE OF ALPHA LIMITED- ..................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial decision-making is a crucial act by the financial manager relating to the

financing-mix of an organization. It is concerned with the borrowing and allocation of funds

required for the investment decisions. A firm has to decide the method of funding by assessing

its financial situation and the characteristics of the source of finance, this set of activities are

known as financial decision-making (Chen, 2018.) In this report the role of accounting and

financial functions will be critically evaluated and will also be substantiated with relevant

examples. Then the financial rations will be calculated and analysed in reference to the asked

entity and will be critically analysed from the perspective of a potential investor. The report will

broadly discuss how the accounting and financial functions are significant in financial decision-

making and how it can drive the operational efficiency of a corporate institution.

TASK 1-

Accounting and Financial functions-

Accounting and finance functions are key parts of the management. It won't be

exaggeration citing these functions as the backbone of all activities. The Accounting functions

call attention to the process of tracking, storing, recording, analysing, summarizing and reporting

of a company's financial transactions. On the other hand financial functions stand for a part of

financial management in which deals with planning procurement, investment, credit and

collection, loans and advances, tax and insurance etc. further it can also be classified in three

main segments financing decision, investment decision and dividend decision. The success of an

organisation hugely depends on the accounting and finance practices of it. Operational efficiency

of the business is directly linked with it. The efficiency of an entity is nowadays depends on the

data availability, which is why to possessing great data base is now a necessity not a luxury for

the institutions (Sedevich-Fons, 2019.)

Role of Accounting functions — As it is defined a bunch of activities which ensures better

recording and providing data for better management and control of the business. There is a set of

activities under it. In modern business environment the data of the business plays vital role like

in planning, controlling, forecasting, decision-making etc. It is a testimony of various financial

activities of the business. It provides data of their business transactions, fund status, liquidity

Financial decision-making is a crucial act by the financial manager relating to the

financing-mix of an organization. It is concerned with the borrowing and allocation of funds

required for the investment decisions. A firm has to decide the method of funding by assessing

its financial situation and the characteristics of the source of finance, this set of activities are

known as financial decision-making (Chen, 2018.) In this report the role of accounting and

financial functions will be critically evaluated and will also be substantiated with relevant

examples. Then the financial rations will be calculated and analysed in reference to the asked

entity and will be critically analysed from the perspective of a potential investor. The report will

broadly discuss how the accounting and financial functions are significant in financial decision-

making and how it can drive the operational efficiency of a corporate institution.

TASK 1-

Accounting and Financial functions-

Accounting and finance functions are key parts of the management. It won't be

exaggeration citing these functions as the backbone of all activities. The Accounting functions

call attention to the process of tracking, storing, recording, analysing, summarizing and reporting

of a company's financial transactions. On the other hand financial functions stand for a part of

financial management in which deals with planning procurement, investment, credit and

collection, loans and advances, tax and insurance etc. further it can also be classified in three

main segments financing decision, investment decision and dividend decision. The success of an

organisation hugely depends on the accounting and finance practices of it. Operational efficiency

of the business is directly linked with it. The efficiency of an entity is nowadays depends on the

data availability, which is why to possessing great data base is now a necessity not a luxury for

the institutions (Sedevich-Fons, 2019.)

Role of Accounting functions — As it is defined a bunch of activities which ensures better

recording and providing data for better management and control of the business. There is a set of

activities under it. In modern business environment the data of the business plays vital role like

in planning, controlling, forecasting, decision-making etc. It is a testimony of various financial

activities of the business. It provides data of their business transactions, fund status, liquidity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

situation etc. The role of accounting are control of financial policy, formation of planning,

preparation of the budget, cost control, evaluation of employees' performance, prevention of

errors and frauds, exhibiting financial affairs, communicating financial information etc.

Over the years there are other branches of accounting also introduced which aims specific

purpose for instance- Management accounting aims to assist management in managerial

decision-making. In management accounting there are multiple works are performed for helping

the managers of various stages. In it generally we perform ratio analysis, cash flow statement,

fund flow statement, common size statements, comparative statements etc. For better

fortification, lots of institutions are following MIS( Management Information System). Whose

role is to draw the road map for a strong management information system so that various relevant

information can be processed further and then being reported to the managers for whom it is

relevant. Whereas cost accounting helps cost managers in controlling the cost of the products. In

cost accounting the entire aim is to aid the cost management and make them more competent

with this regard. It performs the role of helping in pricing, formulate cost efficiency policies and

complying with the legitimacy as well. The role of accounting can be perceived by the given

instance (Kozlowski, 2018).

For example- In ALPHA Ltd it is seen that the Net Profit Margin Ratio of the firm has

been declined in the year 2018, from 12.5 to 8.75%. It was due to higher cost of production. This

accounting information is generated by management accounting and will be helping management

. Taking it into focus it can be concluded that in ALPHA Ltd the operational activities are

underperforming, specifically the cost management is no efficiently working. Net credit purchase

of the company is also reported higher in the books of account but it did not hike the revenues

which is also a discussable issue. In the absence of accounting managers and other key position

holders would be helpless in decision-making.

But there is a dark side of accounting as well. It may mislead the conclusions to certain

degree. There are so many accounting standards and practices in the business fraternity. But

every and each business is a separate in nature and also faces different situations as well.

Applying same set of regimes may take down the usefulness of the accounting reports. There

may be some other qualitative elements as well which are explicitly avoided in modern

preparation of the budget, cost control, evaluation of employees' performance, prevention of

errors and frauds, exhibiting financial affairs, communicating financial information etc.

Over the years there are other branches of accounting also introduced which aims specific

purpose for instance- Management accounting aims to assist management in managerial

decision-making. In management accounting there are multiple works are performed for helping

the managers of various stages. In it generally we perform ratio analysis, cash flow statement,

fund flow statement, common size statements, comparative statements etc. For better

fortification, lots of institutions are following MIS( Management Information System). Whose

role is to draw the road map for a strong management information system so that various relevant

information can be processed further and then being reported to the managers for whom it is

relevant. Whereas cost accounting helps cost managers in controlling the cost of the products. In

cost accounting the entire aim is to aid the cost management and make them more competent

with this regard. It performs the role of helping in pricing, formulate cost efficiency policies and

complying with the legitimacy as well. The role of accounting can be perceived by the given

instance (Kozlowski, 2018).

For example- In ALPHA Ltd it is seen that the Net Profit Margin Ratio of the firm has

been declined in the year 2018, from 12.5 to 8.75%. It was due to higher cost of production. This

accounting information is generated by management accounting and will be helping management

. Taking it into focus it can be concluded that in ALPHA Ltd the operational activities are

underperforming, specifically the cost management is no efficiently working. Net credit purchase

of the company is also reported higher in the books of account but it did not hike the revenues

which is also a discussable issue. In the absence of accounting managers and other key position

holders would be helpless in decision-making.

But there is a dark side of accounting as well. It may mislead the conclusions to certain

degree. There are so many accounting standards and practices in the business fraternity. But

every and each business is a separate in nature and also faces different situations as well.

Applying same set of regimes may take down the usefulness of the accounting reports. There

may be some other qualitative elements as well which are explicitly avoided in modern

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting practices. And sometime we just consider mathematical expressions for being driven

to conclusion which is not too much reliable. For instance in this case where ALPHA Ltd is not

performing good in the year 2018 compares to 2017. It is also possible that it is a half picture.

This company is there from 1954 and serving the customers from more than 70 years. The

performance of two consecutive years is not sufficient to decide the way forward. There may be

some short term factors which had caused this jeopardy to the entity but it is possible that the

waste size of the company may help it in getting its position back. There are many more fuzzy

functions of accounting like manual mistakes, individualism, manipulation, only monetary

expressions etc. Yet it can't be eliminated due to the wide range of well-bing it brings to the

business (Doktoralina, 2018)

Role of Finance functions- Finance functions can be broadly bifurcated in three parts-

Financing, Investing, Dividend distribution. Finance is also called the blood of a business and

any mismanagement with it may outperform the entire operations. In finance functions there are

multiple tasks to be performed. Such as in financing it is decided that how to arrange funds on

right time, in required amount and from such sources which can minimize the risks and also

reduce the burden of cost of capital. Further more at one the finance is arranged then it is decided

that how and in what it should be invested so that can maximize the capacity of the fund to pop

out returns for the organisation then at last it is decided that how much share of the profit or net

revenue should be redeployed and how much should be announced as dividend. (Hassan,

2020.)So altogether it is a cluster of multiple activities whose final pursuit is to create a strong

finance environment within a business. It decides the well performance of various finance

activities and insure their better role in surging revenues for the business. The role of finance

functions can be experienced by the given instances

For example- The ALPHA Ltd. Was having debt of 7,50,000 euros in 2017 but in 2018 it

was 15,00,000 which is a failure of their finance activity. Since it is a general phenomenon that

if you are not generating enough profits then it is better to go with owner's fund where there is no

fixed rate of return has to be given. In 2017 the finance cost was just 75,000 euros but in 2018 it

was 1,50,000 euros, which significantly impacted their EBIT.

to conclusion which is not too much reliable. For instance in this case where ALPHA Ltd is not

performing good in the year 2018 compares to 2017. It is also possible that it is a half picture.

This company is there from 1954 and serving the customers from more than 70 years. The

performance of two consecutive years is not sufficient to decide the way forward. There may be

some short term factors which had caused this jeopardy to the entity but it is possible that the

waste size of the company may help it in getting its position back. There are many more fuzzy

functions of accounting like manual mistakes, individualism, manipulation, only monetary

expressions etc. Yet it can't be eliminated due to the wide range of well-bing it brings to the

business (Doktoralina, 2018)

Role of Finance functions- Finance functions can be broadly bifurcated in three parts-

Financing, Investing, Dividend distribution. Finance is also called the blood of a business and

any mismanagement with it may outperform the entire operations. In finance functions there are

multiple tasks to be performed. Such as in financing it is decided that how to arrange funds on

right time, in required amount and from such sources which can minimize the risks and also

reduce the burden of cost of capital. Further more at one the finance is arranged then it is decided

that how and in what it should be invested so that can maximize the capacity of the fund to pop

out returns for the organisation then at last it is decided that how much share of the profit or net

revenue should be redeployed and how much should be announced as dividend. (Hassan,

2020.)So altogether it is a cluster of multiple activities whose final pursuit is to create a strong

finance environment within a business. It decides the well performance of various finance

activities and insure their better role in surging revenues for the business. The role of finance

functions can be experienced by the given instances

For example- The ALPHA Ltd. Was having debt of 7,50,000 euros in 2017 but in 2018 it

was 15,00,000 which is a failure of their finance activity. Since it is a general phenomenon that

if you are not generating enough profits then it is better to go with owner's fund where there is no

fixed rate of return has to be given. In 2017 the finance cost was just 75,000 euros but in 2018 it

was 1,50,000 euros, which significantly impacted their EBIT.

In finance functions investment policy is also framed which decided the future of finance in an

organisation. In the case of ALPHA Ltd. It has no investment externally. About dividend policy

so the company has retained good reserves, it was 5,62,500 euros in 2017 and in 2018 it was

8,25,000 euros, which defines that the entity wants to utilize the revenue funds for their

expansions or for strengthening their operations. These both examples are articulating the role of

finance functions in an organisation.

Along with these pros there are a few cons as well. It is arguably said that the financial

functions introduce couple of perils as well as like- if such policies are rigid in nature then will

restrict the entity to take advantage of prevailing opportunities. Future is not certain and the core

function of planning is to plan for future which makes this task complicated and a minute

mistake may hurt the financial predictions. Generally it is seen organisations pay more attention

to fund-raising and less to fund utilization, in such cases they end up being profitless (Zhang,

Zhang and Pei, 2019.)

Despite having these lacunas of finance functions it can be concluded that both

accounting and finance activities are inseparable and essential functions of any organisation,

which make them more resilient and prolific in the competitive business environment and give

upper-hand in financial decision-making (Zhou, 2018. )

TASK 2-

(a) Calculation of ratios-

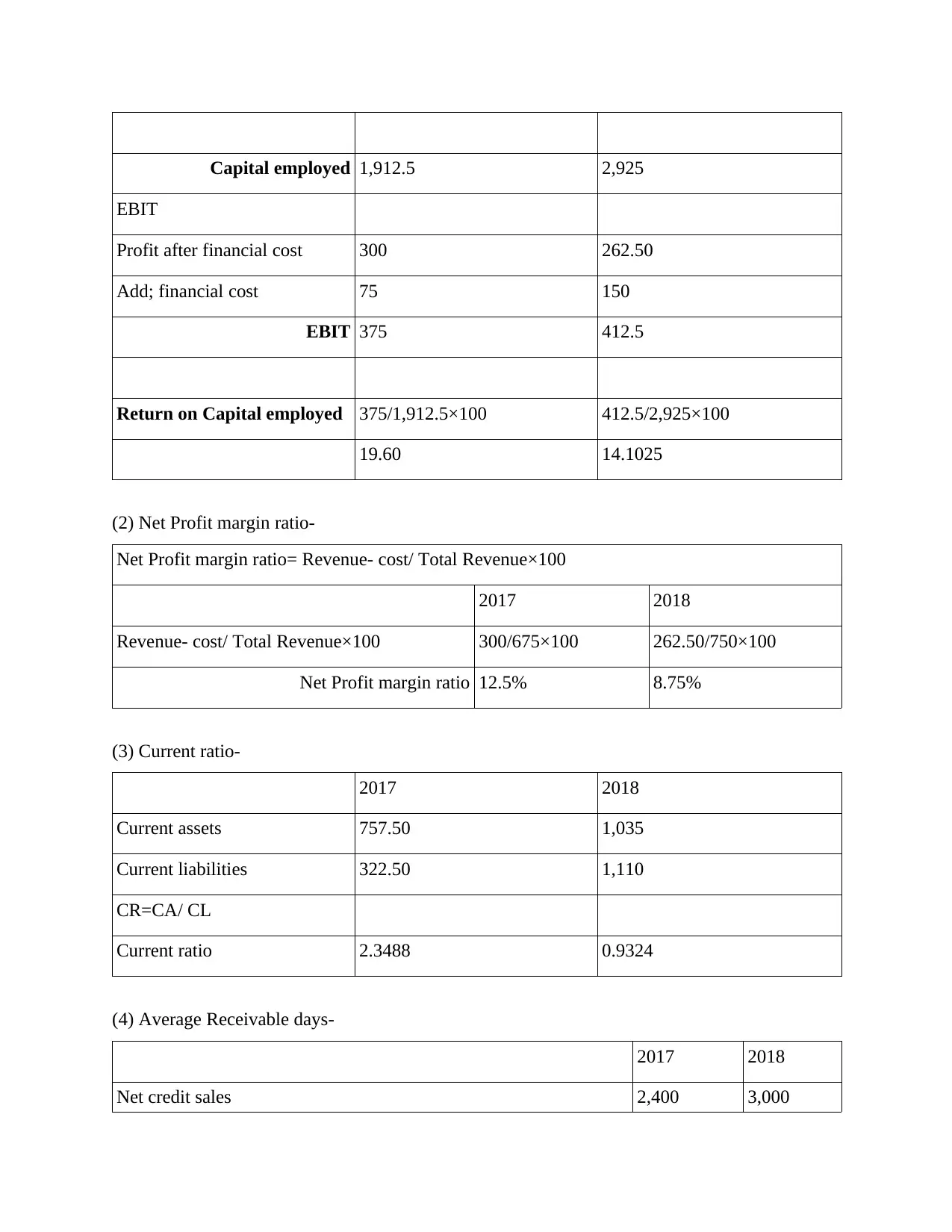

(1) Return on capital employed-

Return on capital employed= EBIT/ Capital employed

Capital employed= Total assets- Current liabilities

2017 2018

Total Assets 2,235 4,035

Current liabilities 322.50 1,110

organisation. In the case of ALPHA Ltd. It has no investment externally. About dividend policy

so the company has retained good reserves, it was 5,62,500 euros in 2017 and in 2018 it was

8,25,000 euros, which defines that the entity wants to utilize the revenue funds for their

expansions or for strengthening their operations. These both examples are articulating the role of

finance functions in an organisation.

Along with these pros there are a few cons as well. It is arguably said that the financial

functions introduce couple of perils as well as like- if such policies are rigid in nature then will

restrict the entity to take advantage of prevailing opportunities. Future is not certain and the core

function of planning is to plan for future which makes this task complicated and a minute

mistake may hurt the financial predictions. Generally it is seen organisations pay more attention

to fund-raising and less to fund utilization, in such cases they end up being profitless (Zhang,

Zhang and Pei, 2019.)

Despite having these lacunas of finance functions it can be concluded that both

accounting and finance activities are inseparable and essential functions of any organisation,

which make them more resilient and prolific in the competitive business environment and give

upper-hand in financial decision-making (Zhou, 2018. )

TASK 2-

(a) Calculation of ratios-

(1) Return on capital employed-

Return on capital employed= EBIT/ Capital employed

Capital employed= Total assets- Current liabilities

2017 2018

Total Assets 2,235 4,035

Current liabilities 322.50 1,110

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital employed 1,912.5 2,925

EBIT

Profit after financial cost 300 262.50

Add; financial cost 75 150

EBIT 375 412.5

Return on Capital employed 375/1,912.5×100 412.5/2,925×100

19.60 14.1025

(2) Net Profit margin ratio-

Net Profit margin ratio= Revenue- cost/ Total Revenue×100

2017 2018

Revenue- cost/ Total Revenue×100 300/675×100 262.50/750×100

Net Profit margin ratio 12.5% 8.75%

(3) Current ratio-

2017 2018

Current assets 757.50 1,035

Current liabilities 322.50 1,110

CR=CA/ CL

Current ratio 2.3488 0.9324

(4) Average Receivable days-

2017 2018

Net credit sales 2,400 3,000

EBIT

Profit after financial cost 300 262.50

Add; financial cost 75 150

EBIT 375 412.5

Return on Capital employed 375/1,912.5×100 412.5/2,925×100

19.60 14.1025

(2) Net Profit margin ratio-

Net Profit margin ratio= Revenue- cost/ Total Revenue×100

2017 2018

Revenue- cost/ Total Revenue×100 300/675×100 262.50/750×100

Net Profit margin ratio 12.5% 8.75%

(3) Current ratio-

2017 2018

Current assets 757.50 1,035

Current liabilities 322.50 1,110

CR=CA/ CL

Current ratio 2.3488 0.9324

(4) Average Receivable days-

2017 2018

Net credit sales 2,400 3,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Average receivables 450 600

2,400/365 3,000/365

Average collection per day 6.5753 8.2191

450/6.5753 600/8.2191

Average receivable collection period 68.43 days 73 days

(5) Average Payable days-

2017 2018

Net credit purchase 1,350 2,400

Average payable 285 1,050

1,350/365 2,400/365

Average payment per day 3.6986 6.5753

285/3.6986 1,050/6.575

Average payable days 77.05 days 159.68 days

(b) Comments on the performance of ALPHA limited-

(1) Return on capital employed- Capital employed refers to the excess of Total assets over

current liabilities, simply it defines the amount which is employed to generate revenues for the

organisation. As an investor it is prominent for it to measure the return rate on the capital

employed of an entity and prefer the firm with higher ROCE. For ALPHA Ltd it was 19.60 % in

2017 whereas in 2018 it was 14.10 %. which is indicating their poor performance in the second

year. There may be some causes like- low amount of EBIT. Earlier it was 375 and then 412.5,

which is looking absolutely higher but in relation to invested amount or capital employed it is

low. Since capital employed in 2017 was 1912.5 and in 2018 it was 2925. There may be other

reasons as well. For instance- lower sales, or high cost of production, higher prices of purchase

etc. It may lead to a few circumstances as well like- the lower rate of return on capital may

2,400/365 3,000/365

Average collection per day 6.5753 8.2191

450/6.5753 600/8.2191

Average receivable collection period 68.43 days 73 days

(5) Average Payable days-

2017 2018

Net credit purchase 1,350 2,400

Average payable 285 1,050

1,350/365 2,400/365

Average payment per day 3.6986 6.5753

285/3.6986 1,050/6.575

Average payable days 77.05 days 159.68 days

(b) Comments on the performance of ALPHA limited-

(1) Return on capital employed- Capital employed refers to the excess of Total assets over

current liabilities, simply it defines the amount which is employed to generate revenues for the

organisation. As an investor it is prominent for it to measure the return rate on the capital

employed of an entity and prefer the firm with higher ROCE. For ALPHA Ltd it was 19.60 % in

2017 whereas in 2018 it was 14.10 %. which is indicating their poor performance in the second

year. There may be some causes like- low amount of EBIT. Earlier it was 375 and then 412.5,

which is looking absolutely higher but in relation to invested amount or capital employed it is

low. Since capital employed in 2017 was 1912.5 and in 2018 it was 2925. There may be other

reasons as well. For instance- lower sales, or high cost of production, higher prices of purchase

etc. It may lead to a few circumstances as well like- the lower rate of return on capital may

bother the loan-providers, and they may go for taking their money back, which will ultimately

affect the investors. (Casielles, 2019.) So as an investor it won't be a smart decision to invest in

such entity which is constantly experiencing downfall in term of their returns on capital

employed. Since it shows that the deployed money is not returning revenues in the amount it is

expected. At the same time if this rate is lower than the average rate of the particular industry

then there is no scope of investment. It would be a risky and non-lucrative alternative for the

investor.

(2) Net profit margin ratio- It is the ratio which compares the profit of a company to the total

amount of money it brings in. Here in this case it was 12.5% in 2017 and 8.75% in 2018. which

shows that the retention rate of the total revenue is lower comparatively. Higher the rate is

considered better for the investor's point of view. In the year it is toppled and came to 8.75%

which depicts that if company generate $100 revenue in sales then it is able to keep just $8.75,

as their net profit. It is also indicating poor operational performance of the entity since it was

higher last year. There may be range of causes and effects of this case but these may be

considerable- Occurring higher cost of goods sold, generating lower revenue on sales, low

selling during the period etc. Here in this case by general observation it can be concluded that in

the year the Total revenue were less than 2018 but the cost part was also lower. In 2017 the net

revenue was 300 whereas in 2017 it was 262.50, which is lower. It is not a good symbol. In the

year 2017 the production cost was lower due to the purchase price but in the year 2018 the

purchase price is higher and it must be the biggest cause of this toppling. Here it is prominent for

an investor to analyse the causes of it. If the price is hiked due to general or unavoidable reasons

then such nuances can be avoided and if it was just poor management of the company then it

should not be ignored. And it is a negative indication for a potential investor (Hasanudin and

Awaloedin, 2020.)

(3) Current Ratio- It shows the relationship between the short term assets and liabilities of an

entity. Here in this case for ALPHA Ltd it was 2.34 in the year 2017 and in 2018 it was 0.93.

Which is not a good sign. The ideal current ratio is considered 1.5 to 3. which shows that for

paying one dollar debt the firm is having one and half dollar. In the year 2017 it is satisfactory

but in 2018 there is dubious sign for the potential investor. There may be such causes and effects

affect the investors. (Casielles, 2019.) So as an investor it won't be a smart decision to invest in

such entity which is constantly experiencing downfall in term of their returns on capital

employed. Since it shows that the deployed money is not returning revenues in the amount it is

expected. At the same time if this rate is lower than the average rate of the particular industry

then there is no scope of investment. It would be a risky and non-lucrative alternative for the

investor.

(2) Net profit margin ratio- It is the ratio which compares the profit of a company to the total

amount of money it brings in. Here in this case it was 12.5% in 2017 and 8.75% in 2018. which

shows that the retention rate of the total revenue is lower comparatively. Higher the rate is

considered better for the investor's point of view. In the year it is toppled and came to 8.75%

which depicts that if company generate $100 revenue in sales then it is able to keep just $8.75,

as their net profit. It is also indicating poor operational performance of the entity since it was

higher last year. There may be range of causes and effects of this case but these may be

considerable- Occurring higher cost of goods sold, generating lower revenue on sales, low

selling during the period etc. Here in this case by general observation it can be concluded that in

the year the Total revenue were less than 2018 but the cost part was also lower. In 2017 the net

revenue was 300 whereas in 2017 it was 262.50, which is lower. It is not a good symbol. In the

year 2017 the production cost was lower due to the purchase price but in the year 2018 the

purchase price is higher and it must be the biggest cause of this toppling. Here it is prominent for

an investor to analyse the causes of it. If the price is hiked due to general or unavoidable reasons

then such nuances can be avoided and if it was just poor management of the company then it

should not be ignored. And it is a negative indication for a potential investor (Hasanudin and

Awaloedin, 2020.)

(3) Current Ratio- It shows the relationship between the short term assets and liabilities of an

entity. Here in this case for ALPHA Ltd it was 2.34 in the year 2017 and in 2018 it was 0.93.

Which is not a good sign. The ideal current ratio is considered 1.5 to 3. which shows that for

paying one dollar debt the firm is having one and half dollar. In the year 2017 it is satisfactory

but in 2018 there is dubious sign for the potential investor. There may be such causes and effects

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of this fall- company has generated more short-term debts which are to be paid in the future,

there is surge in both current assets and liabilities in the year 2018 but inter-relatively it is lower,

which caused this unfavourable expressions. 0.93 is a horrendous figure which shows that at

present the entity is just having 0.93 dollar against the short term debt of 1 dollar. Which is a

negative sign for them. (Koksal, Sbeta and Yildiz, 2019.) It can adversely impact the operational

efficiency of the firm. It is seen on many occasions that firm with insufficient working capital

got failed in achieving their operational goals. As a potential investor it must be seen that how

the company will set off it in emergency and if it is not manageable then the investment won't be

safe.

(4) Average Receivable collection period- It refers to the length of time a business needs to

collect its accounts receivables. Companies calculate the average collection period to ensure that

they have enough cash on hand to meet their financial obligations. This period indicates the

effectiveness of a company's average receivable management practices. Lower the period is

considered good. If it is less than 30 days then it's a favourable sign. For the ALPHA Ltd it was

68.43 days in 2017 and in 2018 it was 73 days. Both are not good by it got worse in 2018 which

is a negative sign. There may be mismanagement of receivable collection policy of the entity, or

there may be poor responses from the payers. It is not a healthy practice since it will lead to poor

short term liquidity. It will not impact the current ration expressions due to the same nature of

cash and receivables for accounting point of view but for an investor it can't be avoided. They

ought to look into the issues behind it. (Siele and Tibbs, 2019. )If it is low then somehow it will

impact the capacity of the entity to pay back to their payables. For investor scrutinizing the

causes and analysing their implications is a must needed practice. Here it can be concluded that it

is a little poor but there is no such huge variability in two years.

(5) Average payable days- stands for the average time period taken by an organisation for paying

off its dues with respect to purchases of materials that are bought on the credit basis from the

suppliers of the company. Keeping it lower is considered good so that the benefit of cash

discount can be availed. For ALPHA Ltd. It was 77.05 days in 2017 but in 2018 it hiked up to

159.68 days. Which is significantly high. There may be poor payment management by the entity

and other reasons consist less availability of funds or liquidity issues etc. It is not a good

there is surge in both current assets and liabilities in the year 2018 but inter-relatively it is lower,

which caused this unfavourable expressions. 0.93 is a horrendous figure which shows that at

present the entity is just having 0.93 dollar against the short term debt of 1 dollar. Which is a

negative sign for them. (Koksal, Sbeta and Yildiz, 2019.) It can adversely impact the operational

efficiency of the firm. It is seen on many occasions that firm with insufficient working capital

got failed in achieving their operational goals. As a potential investor it must be seen that how

the company will set off it in emergency and if it is not manageable then the investment won't be

safe.

(4) Average Receivable collection period- It refers to the length of time a business needs to

collect its accounts receivables. Companies calculate the average collection period to ensure that

they have enough cash on hand to meet their financial obligations. This period indicates the

effectiveness of a company's average receivable management practices. Lower the period is

considered good. If it is less than 30 days then it's a favourable sign. For the ALPHA Ltd it was

68.43 days in 2017 and in 2018 it was 73 days. Both are not good by it got worse in 2018 which

is a negative sign. There may be mismanagement of receivable collection policy of the entity, or

there may be poor responses from the payers. It is not a healthy practice since it will lead to poor

short term liquidity. It will not impact the current ration expressions due to the same nature of

cash and receivables for accounting point of view but for an investor it can't be avoided. They

ought to look into the issues behind it. (Siele and Tibbs, 2019. )If it is low then somehow it will

impact the capacity of the entity to pay back to their payables. For investor scrutinizing the

causes and analysing their implications is a must needed practice. Here it can be concluded that it

is a little poor but there is no such huge variability in two years.

(5) Average payable days- stands for the average time period taken by an organisation for paying

off its dues with respect to purchases of materials that are bought on the credit basis from the

suppliers of the company. Keeping it lower is considered good so that the benefit of cash

discount can be availed. For ALPHA Ltd. It was 77.05 days in 2017 but in 2018 it hiked up to

159.68 days. Which is significantly high. There may be poor payment management by the entity

and other reasons consist less availability of funds or liquidity issues etc. It is not a good

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indication, which is citing that the entity is not in the position to pay back to their suppliers. It

may destroy their relationship possibly with suppliers and tarnish their image as well. For an

investor this can't be ignored. It shows poor management and operational performance which

may cause horrendous damages to the entity in the future so investing in such entity is not safe

highlighting this point.

Observing all the ratios it is being pointed out that currently the entity is underperforming in the

all segments of their business in such predicament it won't be a wise decision to invest in such

entity. At the same time their performance in second year is a severe threat for a novice investor

(Zhagyparova,)

CONCLUSION

From the analysis done in the report above it can be concluded that in the report firstly

the accounting and finance functions are elaborately discussed. The character of accounting and

finance activities were evaluated keeping the disadvantageous factors of it in mind. Further the

report also used substantive and logical examples to articulate the role in more clear and

perceivable way. Along with it the report had also calculated financial ratios for the ALPHA Ltd

and then defined the mathematical expressions from the perspective of potential investor that

how the comparative or relatives changes in the ratios for given two years may influence the

decision of investors. And what had been the possible causes and effects of these changes.

Report had concluded various aspects of financial decision-making and logically represented it

with appropriate examples and explanations.

may destroy their relationship possibly with suppliers and tarnish their image as well. For an

investor this can't be ignored. It shows poor management and operational performance which

may cause horrendous damages to the entity in the future so investing in such entity is not safe

highlighting this point.

Observing all the ratios it is being pointed out that currently the entity is underperforming in the

all segments of their business in such predicament it won't be a wise decision to invest in such

entity. At the same time their performance in second year is a severe threat for a novice investor

(Zhagyparova,)

CONCLUSION

From the analysis done in the report above it can be concluded that in the report firstly

the accounting and finance functions are elaborately discussed. The character of accounting and

finance activities were evaluated keeping the disadvantageous factors of it in mind. Further the

report also used substantive and logical examples to articulate the role in more clear and

perceivable way. Along with it the report had also calculated financial ratios for the ALPHA Ltd

and then defined the mathematical expressions from the perspective of potential investor that

how the comparative or relatives changes in the ratios for given two years may influence the

decision of investors. And what had been the possible causes and effects of these changes.

Report had concluded various aspects of financial decision-making and logically represented it

with appropriate examples and explanations.

REFERENCES

Books and Journals

Casielles, J., 2019. ROE, ROCE, Beneficio Económico y EVA (Return on Equity, Return on

Capital Employed, Economic Benefit and Economic Added Value). Available at SSRN

3394255.

Chen, T. Y., 2018. An outranking approach using a risk attitudinal assignment model involving

Pythagorean fuzzy information and its application to financial decision making. Applied

soft computing. 71. pp.460-487.

Doktoralina, 2018. Role of accounting zakat as a support function in supply chain management:

A resurrection of the Islamic economy. International Journal of Supply Chain

Management. 7(5). pp.336-342.

Hasanudin, H. and Awaloedin, D. T., 2020. Pengaruh Current Ratio, Debt To Equity Ratio Dan

Net Profit Margin Terhadap Return Saham Pada Perusahaan Jasa Sub Sektor

Telekomunikasi Yang Terdaftar Di Bei Periode 2012-2018. Jurnal Rekayasa Informasi.

9(1). pp.6-19.

Hassan, 2020. Challenges for the Islamic Finance and banking in post COVID era and the role

of Fintech. Journal of Economic Cooperation & Development. 41(3). pp.93-116.

Books and Journals

Casielles, J., 2019. ROE, ROCE, Beneficio Económico y EVA (Return on Equity, Return on

Capital Employed, Economic Benefit and Economic Added Value). Available at SSRN

3394255.

Chen, T. Y., 2018. An outranking approach using a risk attitudinal assignment model involving

Pythagorean fuzzy information and its application to financial decision making. Applied

soft computing. 71. pp.460-487.

Doktoralina, 2018. Role of accounting zakat as a support function in supply chain management:

A resurrection of the Islamic economy. International Journal of Supply Chain

Management. 7(5). pp.336-342.

Hasanudin, H. and Awaloedin, D. T., 2020. Pengaruh Current Ratio, Debt To Equity Ratio Dan

Net Profit Margin Terhadap Return Saham Pada Perusahaan Jasa Sub Sektor

Telekomunikasi Yang Terdaftar Di Bei Periode 2012-2018. Jurnal Rekayasa Informasi.

9(1). pp.6-19.

Hassan, 2020. Challenges for the Islamic Finance and banking in post COVID era and the role

of Fintech. Journal of Economic Cooperation & Development. 41(3). pp.93-116.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.