Financial Decisions Making Report: Analysis of Panini Ltd (BM 414)

VerifiedAdded on 2023/06/10

|15

|3887

|466

Report

AI Summary

This report analyzes the financial decisions of Panini Ltd, a medium-sized manufacturing company. It begins by discussing the roles of the accounting and finance departments, outlining their functions such as financial and management accounting, tax, auditing, investment, financing, dividend, and working capital management. The report then explores various sources of finance, including retained earnings, debt capital, and equity capital. The second part of the report involves calculating and analyzing financial ratios, particularly the gross profit margin, comparing the results over two years to assess profitability and efficiency. The analysis includes potential reasons for changes in financial performance and offers recommendations for improvement, concluding with an overall assessment of Panini Ltd's financial health and investment potential. This report serves as a comprehensive financial analysis, providing valuable insights into the company's performance and financial strategies.

BM 414 Financial Decisions

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Part a: Accounting and Finance departments..............................................................................3

Part b: Sources of Finance...........................................................................................................6

TASK 2............................................................................................................................................8

Part a: Calculation of the ratios...................................................................................................8

Part b: Analysis of Ratios Calculated........................................................................................10

Recommendations......................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Part a: Accounting and Finance departments..............................................................................3

Part b: Sources of Finance...........................................................................................................6

TASK 2............................................................................................................................................8

Part a: Calculation of the ratios...................................................................................................8

Part b: Analysis of Ratios Calculated........................................................................................10

Recommendations......................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION

Financial decisions are an essential part of every business. There are varied decisions that

together are terms are the financial decisions. The financial decisions are the concern area of the

finance department of an organization. Panini Ltd is a medium sized manufacturing company

that manufactures the breads and supplies it to the supermarkets of the region. In this report the

concept of financial and accounting department will be discussed along with the variety of

functions that are performed by these two departments. The report will highlight the sources of

finance for the company. Further in the task two of the report ratios will be calculated and

commented upon. The report will recommend the potential investors of Panini Ltd regarding

their investment decision in the company.

MAIN BODY

TASK 1

Part a: Accounting and Finance departments

1. Accounting department: In an organization accounting department is a division of

business overhead set. There are varied responsibilities over the accounting department in

an organization. The department is responsible for making the payments of the invoices,

preparation of financial statements, payment of compensation to the employees for their

services (Fogarty, 2021). Further cost accounting, timely payments to the materials and

other services providers and related activities are the concern areas of the accounting

department working within a company.

a) Financial accounting function → The accounting department of an organization performs

varies types of functions. The foremost function of the accounting department is the

financial accounting function. Financial accounting means identifying the financial

transactions from all the business transactions, recording the identified financial

transactions, summarizing them in specific formats for the further preparation of the

financial statements (Anggriani, Noviantoro and Efryanty, 2020). The prepared financial

statements are of great use for the various individuals or bodies that have any kind of

stake in the company. The analysis of the information provided by the accounting

department of the company is important for the potential investors to decide whether to

make their investment decision in the company or not.

Financial decisions are an essential part of every business. There are varied decisions that

together are terms are the financial decisions. The financial decisions are the concern area of the

finance department of an organization. Panini Ltd is a medium sized manufacturing company

that manufactures the breads and supplies it to the supermarkets of the region. In this report the

concept of financial and accounting department will be discussed along with the variety of

functions that are performed by these two departments. The report will highlight the sources of

finance for the company. Further in the task two of the report ratios will be calculated and

commented upon. The report will recommend the potential investors of Panini Ltd regarding

their investment decision in the company.

MAIN BODY

TASK 1

Part a: Accounting and Finance departments

1. Accounting department: In an organization accounting department is a division of

business overhead set. There are varied responsibilities over the accounting department in

an organization. The department is responsible for making the payments of the invoices,

preparation of financial statements, payment of compensation to the employees for their

services (Fogarty, 2021). Further cost accounting, timely payments to the materials and

other services providers and related activities are the concern areas of the accounting

department working within a company.

a) Financial accounting function → The accounting department of an organization performs

varies types of functions. The foremost function of the accounting department is the

financial accounting function. Financial accounting means identifying the financial

transactions from all the business transactions, recording the identified financial

transactions, summarizing them in specific formats for the further preparation of the

financial statements (Anggriani, Noviantoro and Efryanty, 2020). The prepared financial

statements are of great use for the various individuals or bodies that have any kind of

stake in the company. The analysis of the information provided by the accounting

department of the company is important for the potential investors to decide whether to

make their investment decision in the company or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Management accounting function → The next function of the accounting department in

every organization is management accounting. Management accounting function is

dedicated function performed by the accounting department specially for the management

of the organization. The managers in a company as a part of their roles and duties

towards the organization performs a variety of functions. The function of the top

managerial authorities of every organization is basically to make important decisions.

There are various decisions taken by the managers in an organization. These functions are

on both financial and non-financial aspects of the company. Decisions whether financial

or non-financial are taken to maximize the shareholders’ wealth. The decisions taken by

the managers of the company actually benefits the company because of the management

accounting function of the accounting department of the company. Through management

accounting function the accounting department of the company represent actual position

of the company in front of the management. Based on which the management of the

company is able to take effective decisions. The accuracy in the management accounting

function forms the basis for the decisions of the mangers to be fruitful for the business

entity.

c) Tax function → The third function of the accounting department in an organization is

namely as tax function. In large organizations there exists separate department for the

performance of all the activities related to taxations. Both the dedicated taxation

department or the accounting department under its tax function performs same functions.

Tax is accounted by the accounting department of the company. Tax impacts the

organization’s planning of cash and preparation of budgets. There should be availability

of funds in the organization for the payment of tax liabilities to the tax authorities that the

right time (Tashnazarova, 2021). Tax transactions constructs both tax liabilities and tax

assets. Tax liabilities is the sum that has to be paid by company while tax assets are the

amount that the company will receive. Recording and accounting of tax transactions is

done by the accounting department.

d) Auditing function → The auditing function of the company’s accounting department is

concerned with the assurance of accuracy in the accounting of the company. The

financial accounting is verified through the auditing function of the accounting

department. The accounting department of the organization under its auditing function is

every organization is management accounting. Management accounting function is

dedicated function performed by the accounting department specially for the management

of the organization. The managers in a company as a part of their roles and duties

towards the organization performs a variety of functions. The function of the top

managerial authorities of every organization is basically to make important decisions.

There are various decisions taken by the managers in an organization. These functions are

on both financial and non-financial aspects of the company. Decisions whether financial

or non-financial are taken to maximize the shareholders’ wealth. The decisions taken by

the managers of the company actually benefits the company because of the management

accounting function of the accounting department of the company. Through management

accounting function the accounting department of the company represent actual position

of the company in front of the management. Based on which the management of the

company is able to take effective decisions. The accuracy in the management accounting

function forms the basis for the decisions of the mangers to be fruitful for the business

entity.

c) Tax function → The third function of the accounting department in an organization is

namely as tax function. In large organizations there exists separate department for the

performance of all the activities related to taxations. Both the dedicated taxation

department or the accounting department under its tax function performs same functions.

Tax is accounted by the accounting department of the company. Tax impacts the

organization’s planning of cash and preparation of budgets. There should be availability

of funds in the organization for the payment of tax liabilities to the tax authorities that the

right time (Tashnazarova, 2021). Tax transactions constructs both tax liabilities and tax

assets. Tax liabilities is the sum that has to be paid by company while tax assets are the

amount that the company will receive. Recording and accounting of tax transactions is

done by the accounting department.

d) Auditing function → The auditing function of the company’s accounting department is

concerned with the assurance of accuracy in the accounting of the company. The

financial accounting is verified through the auditing function of the accounting

department. The accounting department of the organization under its auditing function is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

concerned with the evaluation of the processes in the business operations, proper

managing of the risks associated with the business entity, activities for controlling the

functions of the company and effective governance of the company.

2. Finance department: The finance department is one of the most important section of the

business organization. The department is responsible for the effective obtaining of funds

for the optimum undertaking of the most profitable investment alternative that is being

undertaken by the company as per the decision made by the department by proper

evaluation of the opportunities available with the company (Balakrishnan, Prakash and

Ramesh, 2020). The department is responsible for the maintenance of the optimum

working capital.

a) Investment Function → The finance department of the company is responsible for the

selection of the investment alternative for the company under its investment function.

The company in order to assure its competitive edge in the market, keeps on analysing

the opportunities that exists in its external environment. To capture the opportunities

there are various investment alternatives for every opportunity (Fachrozie and Syarvina,

2022). The finance department of the company analyses every alternative project for each

of the opportunity on the basis of the initial investment required, the time investment will

take for the repayment of the initial invested amount, the existing value of the money that

will generate in the future. The function of the finance department is to perform this

detailed evaluation and propose the most optimum alternate to the management.

b) Financing Function → In order to accept the investment option nominated, the company

requires to make the initial investment amount arranged within it. This function is taken

care by the finance department of the company. There are various options by which the

company can raise the required amount for the acceptance of the investment. The finance

department with the financing function evaluates each and every source to raise the

funds. Every fund raising alternative have its own costs attached along with risk factor.

The associated cost to the alternate source of finance can be implicit or explicit. Both are

considered while selection of the optimum alternative. The function of the finance

department is to bring the surety that the funds available with the organization are

sufficient for both the working capital requirements and long term requirements.

managing of the risks associated with the business entity, activities for controlling the

functions of the company and effective governance of the company.

2. Finance department: The finance department is one of the most important section of the

business organization. The department is responsible for the effective obtaining of funds

for the optimum undertaking of the most profitable investment alternative that is being

undertaken by the company as per the decision made by the department by proper

evaluation of the opportunities available with the company (Balakrishnan, Prakash and

Ramesh, 2020). The department is responsible for the maintenance of the optimum

working capital.

a) Investment Function → The finance department of the company is responsible for the

selection of the investment alternative for the company under its investment function.

The company in order to assure its competitive edge in the market, keeps on analysing

the opportunities that exists in its external environment. To capture the opportunities

there are various investment alternatives for every opportunity (Fachrozie and Syarvina,

2022). The finance department of the company analyses every alternative project for each

of the opportunity on the basis of the initial investment required, the time investment will

take for the repayment of the initial invested amount, the existing value of the money that

will generate in the future. The function of the finance department is to perform this

detailed evaluation and propose the most optimum alternate to the management.

b) Financing Function → In order to accept the investment option nominated, the company

requires to make the initial investment amount arranged within it. This function is taken

care by the finance department of the company. There are various options by which the

company can raise the required amount for the acceptance of the investment. The finance

department with the financing function evaluates each and every source to raise the

funds. Every fund raising alternative have its own costs attached along with risk factor.

The associated cost to the alternate source of finance can be implicit or explicit. Both are

considered while selection of the optimum alternative. The function of the finance

department is to bring the surety that the funds available with the organization are

sufficient for both the working capital requirements and long term requirements.

c) Dividend Function → The profits earned by the company are distributed among the

shareholders both first preference shareholders then the equity shareholders after the

preference shareholders after the payments have been made to the debenture holders and

the tax authorities. There exist two options with the company one is to distribute the

dividend and the second option is not to distribute the dividend. The dividend function of

the finance department is concerned with the making of such decision under its dividend

function (Kaverzina and Cherutova, 2019). The dividend is distributed when the expected

amount to be generated from the retaining of the earnings is lower than the actual market

return. The finance department decides to keep the earnings within the company in the

form of retained earnings and not distribute it to the shareholders when the company

expects to earn more by reinvesting the earnings.

d) Working capital function → The working capital is basically the short term capital

available within the company using which it pays for its short term obligations and also

make essential payments for the daily business operations. There are number of factors

that affects the decision of the finance department regarding the optimum amount that

will be sufficient for the company for its swiftness in the functioning.

Part b: Sources of Finance

1. Retained Earnings: The first source of finance that is most easily available with the

company for meeting its fund requirements is namely retained earnings (Gupta and

Singh, 2018). The retained earnings are basically the portion of profits that the company

keeps with itself instead of distributing it among the shareholders, for further

reinvestment purposes. There are certain advantages that this type of source of finance

has for the company. The stock value of the company increases with the high amount of

retained earnings as balance sheet of such business becomes lucrative for the investors

inviting further investment. This amount can be used effectively for the purpose of

growing the business.

2. Debt Capital: The next source to raise finance required for the fulfilment of expansion

purpose of the company is Debt capital. Debt issue form of raising capital is a long term

source of finance. The individuals or institutes purchasing the debentures are known as

debenture holders. They receive interest periodically against the amount invested by

them. By raising funds through this source of finance help businesses of arrange funds

shareholders both first preference shareholders then the equity shareholders after the

preference shareholders after the payments have been made to the debenture holders and

the tax authorities. There exist two options with the company one is to distribute the

dividend and the second option is not to distribute the dividend. The dividend function of

the finance department is concerned with the making of such decision under its dividend

function (Kaverzina and Cherutova, 2019). The dividend is distributed when the expected

amount to be generated from the retaining of the earnings is lower than the actual market

return. The finance department decides to keep the earnings within the company in the

form of retained earnings and not distribute it to the shareholders when the company

expects to earn more by reinvesting the earnings.

d) Working capital function → The working capital is basically the short term capital

available within the company using which it pays for its short term obligations and also

make essential payments for the daily business operations. There are number of factors

that affects the decision of the finance department regarding the optimum amount that

will be sufficient for the company for its swiftness in the functioning.

Part b: Sources of Finance

1. Retained Earnings: The first source of finance that is most easily available with the

company for meeting its fund requirements is namely retained earnings (Gupta and

Singh, 2018). The retained earnings are basically the portion of profits that the company

keeps with itself instead of distributing it among the shareholders, for further

reinvestment purposes. There are certain advantages that this type of source of finance

has for the company. The stock value of the company increases with the high amount of

retained earnings as balance sheet of such business becomes lucrative for the investors

inviting further investment. This amount can be used effectively for the purpose of

growing the business.

2. Debt Capital: The next source to raise finance required for the fulfilment of expansion

purpose of the company is Debt capital. Debt issue form of raising capital is a long term

source of finance. The individuals or institutes purchasing the debentures are known as

debenture holders. They receive interest periodically against the amount invested by

them. By raising funds through this source of finance help businesses of arrange funds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that are required along with maintaining its control over the activities. There is no

dilution of ownership of the existing owners (Advantages vs. Disadvantages of Debt

Financing, 2022). It gives tax advantage to the company as the interest payments are tax

deductible.

3. Equity Capital: The firm in order to gather funds for its expansion purpose can issue

equity shares in the market (Klimczak, 2020). The money received by issue of equity

shares is called equity capital. The company choosing the alternate of equity capital for

its finance requirement sells the part of its ownership to the public in exchange of money.

dilution of ownership of the existing owners (Advantages vs. Disadvantages of Debt

Financing, 2022). It gives tax advantage to the company as the interest payments are tax

deductible.

3. Equity Capital: The firm in order to gather funds for its expansion purpose can issue

equity shares in the market (Klimczak, 2020). The money received by issue of equity

shares is called equity capital. The company choosing the alternate of equity capital for

its finance requirement sells the part of its ownership to the public in exchange of money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Part a: Calculation of the ratios

Part a: Calculation of the ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part b: Analysis of Ratios Calculated

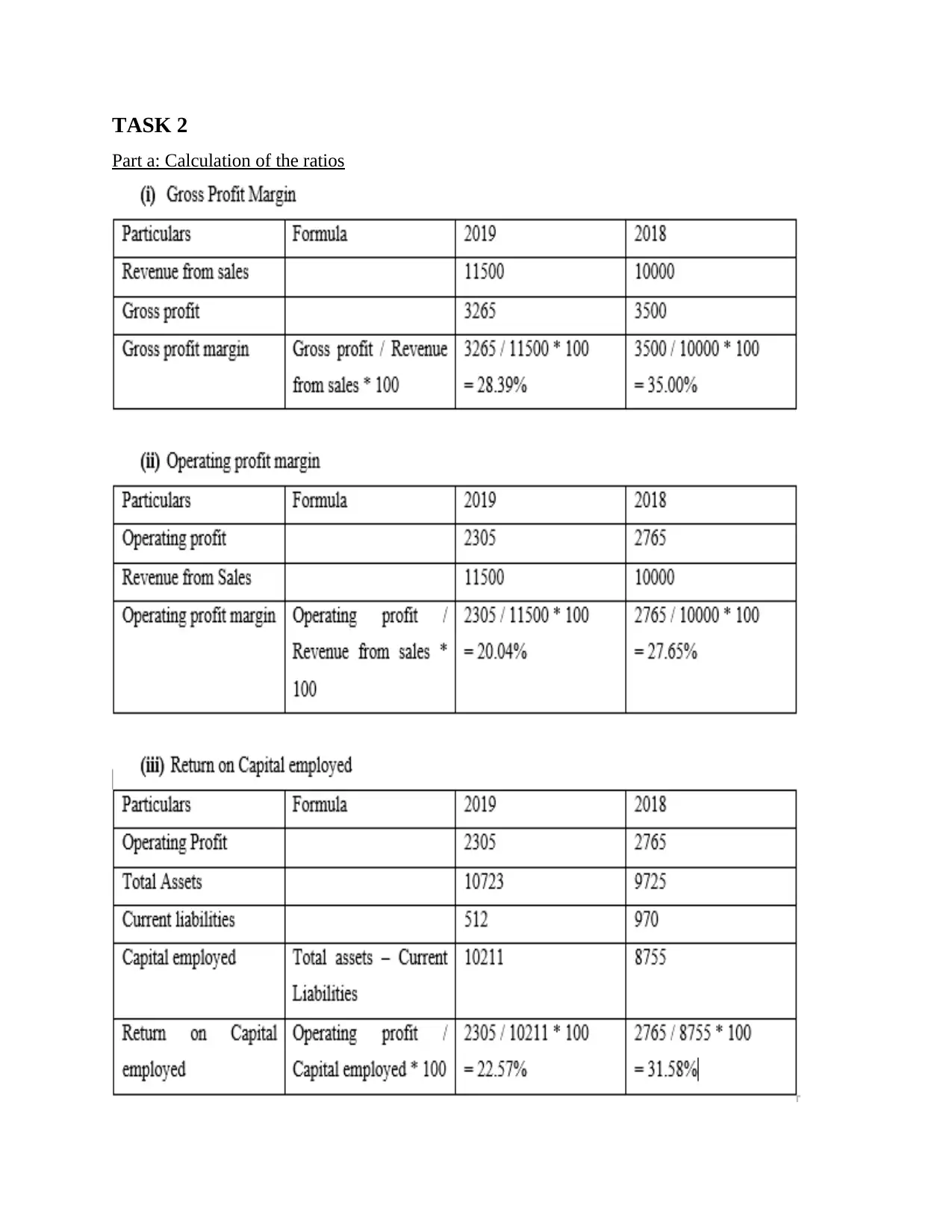

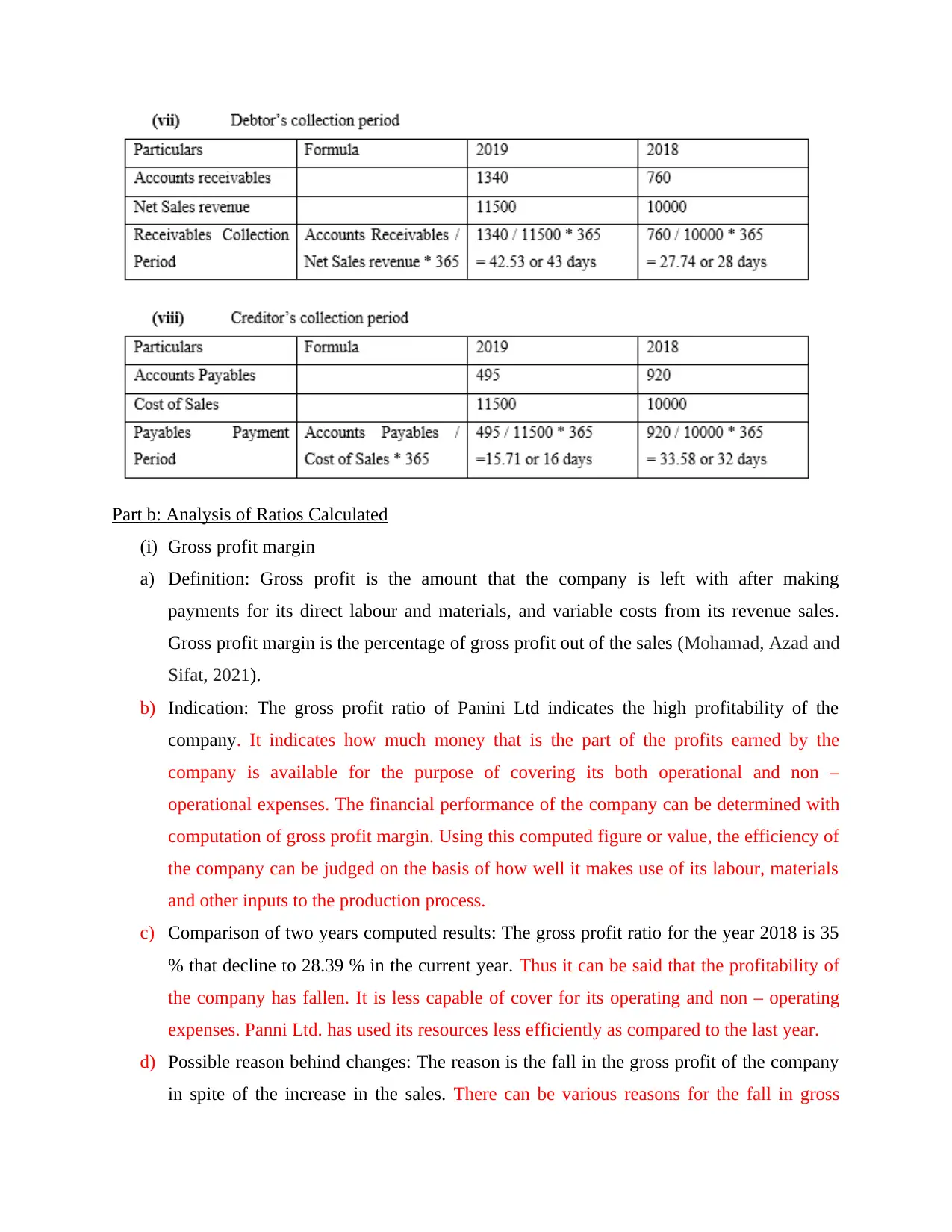

(i) Gross profit margin

a) Definition: Gross profit is the amount that the company is left with after making

payments for its direct labour and materials, and variable costs from its revenue sales.

Gross profit margin is the percentage of gross profit out of the sales (Mohamad, Azad and

Sifat, 2021).

b) Indication: The gross profit ratio of Panini Ltd indicates the high profitability of the

company. It indicates how much money that is the part of the profits earned by the

company is available for the purpose of covering its both operational and non –

operational expenses. The financial performance of the company can be determined with

computation of gross profit margin. Using this computed figure or value, the efficiency of

the company can be judged on the basis of how well it makes use of its labour, materials

and other inputs to the production process.

c) Comparison of two years computed results: The gross profit ratio for the year 2018 is 35

% that decline to 28.39 % in the current year. Thus it can be said that the profitability of

the company has fallen. It is less capable of cover for its operating and non – operating

expenses. Panni Ltd. has used its resources less efficiently as compared to the last year.

d) Possible reason behind changes: The reason is the fall in the gross profit of the company

in spite of the increase in the sales. There can be various reasons for the fall in gross

(i) Gross profit margin

a) Definition: Gross profit is the amount that the company is left with after making

payments for its direct labour and materials, and variable costs from its revenue sales.

Gross profit margin is the percentage of gross profit out of the sales (Mohamad, Azad and

Sifat, 2021).

b) Indication: The gross profit ratio of Panini Ltd indicates the high profitability of the

company. It indicates how much money that is the part of the profits earned by the

company is available for the purpose of covering its both operational and non –

operational expenses. The financial performance of the company can be determined with

computation of gross profit margin. Using this computed figure or value, the efficiency of

the company can be judged on the basis of how well it makes use of its labour, materials

and other inputs to the production process.

c) Comparison of two years computed results: The gross profit ratio for the year 2018 is 35

% that decline to 28.39 % in the current year. Thus it can be said that the profitability of

the company has fallen. It is less capable of cover for its operating and non – operating

expenses. Panni Ltd. has used its resources less efficiently as compared to the last year.

d) Possible reason behind changes: The reason is the fall in the gross profit of the company

in spite of the increase in the sales. There can be various reasons for the fall in gross

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profits indicating that company is less efficient in making effective utilisation of its

assets. Also it is not managing the costs effectively, this can be in the increasing level of

costs.

e) Improvement suggestions: For improving the situation Panini Ltd. have to control its

expenses. There are various ways by which expenses can be reduced. Optimising the

efficiency of the workforce, evaluation of the production process are some suggestions.

By evaluating its production process the company can know the areas that are wasteful or

not up to the mark as per the effective process steps.

(ii) Operating profit margin

a) Definition: Operating profit is the deduction of operating expenses from the operating

income (Al-Kassar and et.al., 2019). Operating profit margin is the percentage of

operating profit out of the revenue sales.

b) Indication: The operation profit margin of a company shows the amount of profit the

company generates after the payment for the operating costs. Operating profits earned by

the company are used in determine the potentiality of the firm in making profits exclusive

of the total of inessential factors.

c) Comparison of two years computed results: The operating profit margin of the Panini ltd

reduced by 7.61 % in the current year in comparison to the previous year. The

comparison says that the potentiality of company to earn profits reduced in the current

year.

d) Possible reason behind changes: The reason behind the figure of low operating profit

margin in the current year as compared with the previous year increase in the sales

revenue amount and decrease in the operating profit value. There is an increase in the

operating expenses of the firm by 23% in current year from the past year.

e) Improvement suggestions: For improving the operating profit ratio Panini Ltd must focus

on its operating costs. The operating costs of the company are very high. Company can

increase its operating profit by controlling its administrative expenses, selling and

distribution expenses. The channels that the company uses for selling its products can be

revised for identifying the areas where the costs can be saved.

(iii) Return on capital employed

assets. Also it is not managing the costs effectively, this can be in the increasing level of

costs.

e) Improvement suggestions: For improving the situation Panini Ltd. have to control its

expenses. There are various ways by which expenses can be reduced. Optimising the

efficiency of the workforce, evaluation of the production process are some suggestions.

By evaluating its production process the company can know the areas that are wasteful or

not up to the mark as per the effective process steps.

(ii) Operating profit margin

a) Definition: Operating profit is the deduction of operating expenses from the operating

income (Al-Kassar and et.al., 2019). Operating profit margin is the percentage of

operating profit out of the revenue sales.

b) Indication: The operation profit margin of a company shows the amount of profit the

company generates after the payment for the operating costs. Operating profits earned by

the company are used in determine the potentiality of the firm in making profits exclusive

of the total of inessential factors.

c) Comparison of two years computed results: The operating profit margin of the Panini ltd

reduced by 7.61 % in the current year in comparison to the previous year. The

comparison says that the potentiality of company to earn profits reduced in the current

year.

d) Possible reason behind changes: The reason behind the figure of low operating profit

margin in the current year as compared with the previous year increase in the sales

revenue amount and decrease in the operating profit value. There is an increase in the

operating expenses of the firm by 23% in current year from the past year.

e) Improvement suggestions: For improving the operating profit ratio Panini Ltd must focus

on its operating costs. The operating costs of the company are very high. Company can

increase its operating profit by controlling its administrative expenses, selling and

distribution expenses. The channels that the company uses for selling its products can be

revised for identifying the areas where the costs can be saved.

(iii) Return on capital employed

a) Definition: The return that the company is able to generate from the amount it has

invested (Wadhwa, 2019).

b) Indication: It indicates the efficiency of the company to generate profits out of the

amount it has invested in its assets less short term obligations. It is necessary from the

perspective of the parties who invest their valuable resources in the business. In business

money is invested by the shareholders or different institutions like banks, etc. it is way by

which businesses can justify the trust shown by such individual in their investment.

c) Comparison of two years computed results: The return on capital employed by the Panini

Ltd reduced in the year 2019 in comparison to the year 2018.

d) Possible reason behind changes: The reason behind the declining change is that the

despite of the increase in the capital employed the operating profit of the company is low

this year.

e) Improvement suggestions: The assets of the company should be utilized optimally for

improving its return on capital employed.

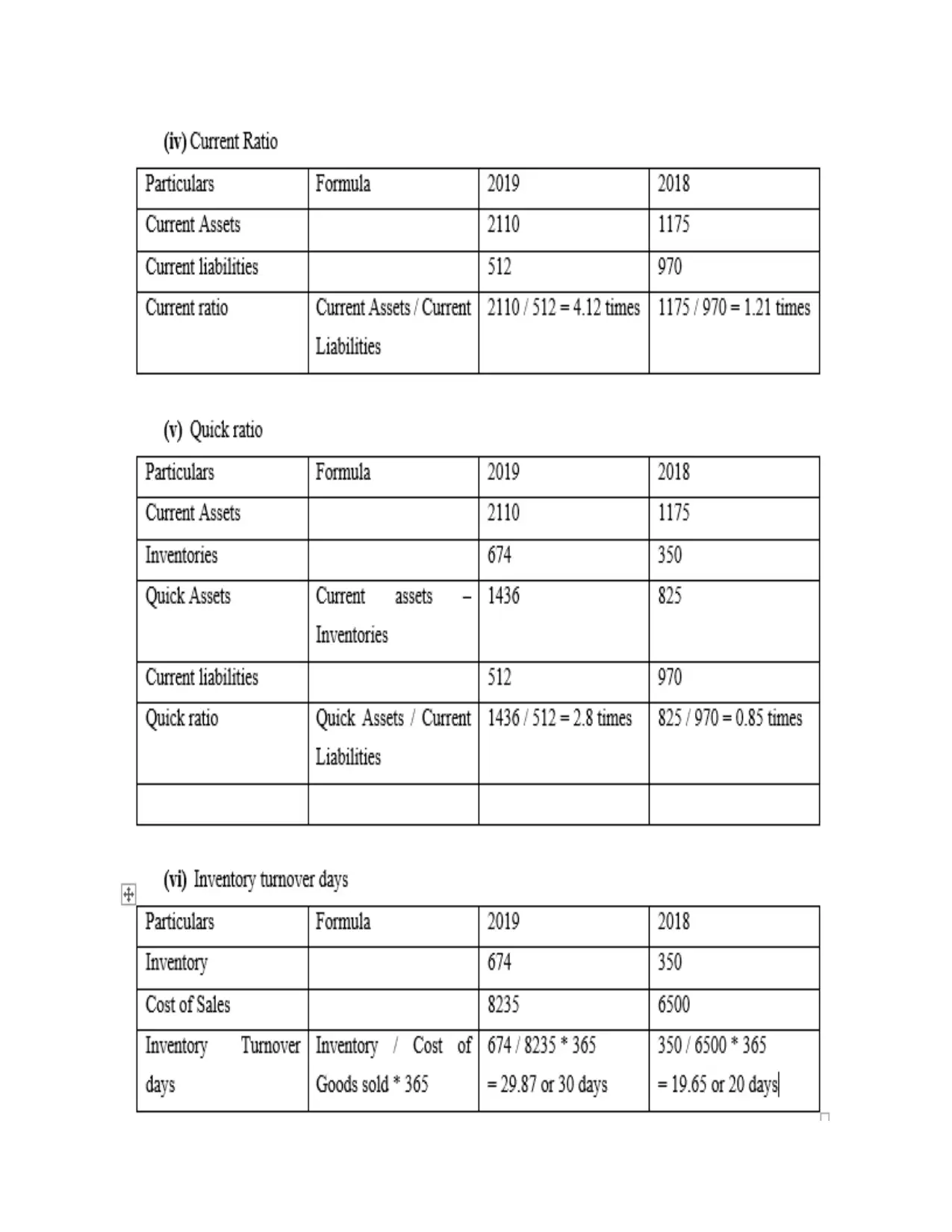

(iv)Current Ratio

a) Definition: Current ratio is ratio of the company’s current assets and its current

liabilities.

b) Indication: It indicates the capability of the firm to pay for its short term obligations.

c) Comparison of two years computed results: The current ratio of the firm increased in

comparison to the previous year.

d) Possible reason behind changes: The reason is that the current assets of the company

nearly doubled in the current year. And the current liabilities are nearly halved in the

current year.

e) Improvement suggestions: Increasing the sales volume and scale of production using

materials being supplied on credit will improve the current ratio of the company.

(v) Quick Ratio

a) Definition: A type of liquidity ratio. Quick assets divided by the current liabilities.

b) Indication: The capability of the firm to pay for its obligations using cash reserves.

c) Comparison of two years computed results: Ratio increased in comparison to the previous

year.

invested (Wadhwa, 2019).

b) Indication: It indicates the efficiency of the company to generate profits out of the

amount it has invested in its assets less short term obligations. It is necessary from the

perspective of the parties who invest their valuable resources in the business. In business

money is invested by the shareholders or different institutions like banks, etc. it is way by

which businesses can justify the trust shown by such individual in their investment.

c) Comparison of two years computed results: The return on capital employed by the Panini

Ltd reduced in the year 2019 in comparison to the year 2018.

d) Possible reason behind changes: The reason behind the declining change is that the

despite of the increase in the capital employed the operating profit of the company is low

this year.

e) Improvement suggestions: The assets of the company should be utilized optimally for

improving its return on capital employed.

(iv)Current Ratio

a) Definition: Current ratio is ratio of the company’s current assets and its current

liabilities.

b) Indication: It indicates the capability of the firm to pay for its short term obligations.

c) Comparison of two years computed results: The current ratio of the firm increased in

comparison to the previous year.

d) Possible reason behind changes: The reason is that the current assets of the company

nearly doubled in the current year. And the current liabilities are nearly halved in the

current year.

e) Improvement suggestions: Increasing the sales volume and scale of production using

materials being supplied on credit will improve the current ratio of the company.

(v) Quick Ratio

a) Definition: A type of liquidity ratio. Quick assets divided by the current liabilities.

b) Indication: The capability of the firm to pay for its obligations using cash reserves.

c) Comparison of two years computed results: Ratio increased in comparison to the previous

year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.