Financial Resource Management and Decisions for Radisson PLC Report

VerifiedAdded on 2020/01/21

|20

|6128

|238

Report

AI Summary

This report examines the financial resource management and strategic decisions of Radisson PLC, a medium-sized computer software manufacturing company. It explores various financing options, including issuing equity shares, loan stock, long-term bank loans, and leasing, analyzing their implications on the business. The report delves into the advantages and disadvantages of each source, considering factors like legal, financial, dilution of control, and bankruptcy implications. Furthermore, it compares debt and equity financing structures, assessing their impact on the company's capital structure. The analysis provides insights into selecting appropriate financing sources for Radisson PLC's expansion plans, considering factors like business nature and project requirements. The report also includes retained earnings and sale of assets as potential financial resources. The report discusses the management's uncertainty about capital structure and the importance of analyzing the cost of funding through debt versus equity finance.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

1

RESOURCES AND

DECISIONS

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A.............................................................................................................................................3

B.............................................................................................................................................6

TASK 2 ...........................................................................................................................................7

A.............................................................................................................................................7

B.............................................................................................................................................8

C.............................................................................................................................................9

TASK 3..........................................................................................................................................11

A...........................................................................................................................................11

B...........................................................................................................................................12

C...........................................................................................................................................14

TASK 4..........................................................................................................................................15

A...........................................................................................................................................15

B...........................................................................................................................................16

C...........................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A.............................................................................................................................................3

B.............................................................................................................................................6

TASK 2 ...........................................................................................................................................7

A.............................................................................................................................................7

B.............................................................................................................................................8

C.............................................................................................................................................9

TASK 3..........................................................................................................................................11

A...........................................................................................................................................11

B...........................................................................................................................................12

C...........................................................................................................................................14

TASK 4..........................................................................................................................................15

A...........................................................................................................................................15

B...........................................................................................................................................16

C...........................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

2

INTRODUCTION

Sourcing money should be arranged by a variety of reasons. Business organisations

requires funds to perform activities (Hayre, 2015). Traditional areas of need may be for capital

asset acquisition for entity. The development of something innovative requires some investment

for its entire process. From ideology up to its production until it came into existence, every stage

requires some investment.

Normally, such development are financed internally, where as capital for acquisition of

any asset is an external source transaction. In this era of some stiff liquidity, many organisation

have to look for short term capital in the way of overdrafts or loans in order to provide a cash

flow cushion. Interest rates can vary from organisation to organisation and also according to its

purpose. The present report is based on Radisson PLC which is a medium sized computer

software manufacturing company operating in London.

The entity have to manage about their arrangement of financial resources and their

implication on business. The entity has recently acquired a long term contract to provide bespoke

software for various companies around UK (Chandra, 2011). The operations manager believes

that there are lots of opportunities to expand their operations and to increase their market share in

industry.

TASK 1

A

Financing plays a very prominent role in working of every lucrative enterprise. The need

of capital requirement by business endeavours their funds, which generate revenues. However,

not every entity have this opportunity to have instant access to money. The abundance of funding

options makes its easier for business owners to select the various sources of financing which

helps entity to participate in business activities as per companies' needs. As Radisson PLC

acquired a long term contract for providing software assistance, for that they have to work on

their projects and requirement of funds goes high for that (Chandra, 2011). There are several

options available for funding. Some of them are discussed as follows:

Issuing equity share:

Ordinary shares are issued by the owners of the company. They are issued on a nominal

value or face value of the list price of share. The market value of listed company bears no

relationship to their nominal value, until or unless shares are issued for cash. There are several

3

Sourcing money should be arranged by a variety of reasons. Business organisations

requires funds to perform activities (Hayre, 2015). Traditional areas of need may be for capital

asset acquisition for entity. The development of something innovative requires some investment

for its entire process. From ideology up to its production until it came into existence, every stage

requires some investment.

Normally, such development are financed internally, where as capital for acquisition of

any asset is an external source transaction. In this era of some stiff liquidity, many organisation

have to look for short term capital in the way of overdrafts or loans in order to provide a cash

flow cushion. Interest rates can vary from organisation to organisation and also according to its

purpose. The present report is based on Radisson PLC which is a medium sized computer

software manufacturing company operating in London.

The entity have to manage about their arrangement of financial resources and their

implication on business. The entity has recently acquired a long term contract to provide bespoke

software for various companies around UK (Chandra, 2011). The operations manager believes

that there are lots of opportunities to expand their operations and to increase their market share in

industry.

TASK 1

A

Financing plays a very prominent role in working of every lucrative enterprise. The need

of capital requirement by business endeavours their funds, which generate revenues. However,

not every entity have this opportunity to have instant access to money. The abundance of funding

options makes its easier for business owners to select the various sources of financing which

helps entity to participate in business activities as per companies' needs. As Radisson PLC

acquired a long term contract for providing software assistance, for that they have to work on

their projects and requirement of funds goes high for that (Chandra, 2011). There are several

options available for funding. Some of them are discussed as follows:

Issuing equity share:

Ordinary shares are issued by the owners of the company. They are issued on a nominal

value or face value of the list price of share. The market value of listed company bears no

relationship to their nominal value, until or unless shares are issued for cash. There are several

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

forms of shares such as deferred ordinary shares, new issues, right issues, preference shares, etc.

by which Radisson Plc group is able to raise finance.

Loan Stock:

Another source of finance is loan stock is a long term debt capital financing technique

adopted by company on which they have to pay interest on a predetermined rate of interest to

lenders. Holders of loan stock are long termed creditors of company. Debenture is a form of loan

stock, legally defined as a written acknowledgement of debt incurred by company, normally

containing provisions about the payment of interest and eventual repayment of capital amount.

When a business expands their operational area its becomes challenging for enterprise to

adopt the most appropriate source of financing for the particular situation. While selecting the

source of finance, there are some implications of different source which business have to attain.

Each source have its own merits and demerits. Radisson PLC have to select the appropriate

source of financing with analysing its advantages and disadvantages (Voss, Sirdeshmukh, and

Voss, 2008). Depending upon the suitability for purpose, the adopted source should match the

terms of finance of projects. They are as follows:

Long term bank loans:

A debt financing obligation issued by bank or any financial institution for organisations

that hold legal claims to borrowers assets. The loan is considered the most important to all other

claim against borrowers, which in the event of bankruptcy, bank loan is the first to be repaid,

before any other interested parties receives any payment.

Implications:

Legal Implication: Subject to asset seizure in case of default.

Financial Implication: For instance, interest should be paid on monthly, quarterly, half

yearly, or annually basis by the Radisson group to the banks after taking debt from the bank.

Dilution of control implication:There is no dilution of control.

Bankruptcy Implication: Bank have the obligation to recover the loan form the asset used

to secure loan, if in future organisation become insolvent.

Equity Share:

Equity ownership is accompanied by providing voting rights and entitling the holder to a

share of company's success through dividends or capital appreciation. These denominations

provide a holder several rights and through this the shareholders become the owner of the

respective company (Remund, 2010). The characteristics like they have their term in company as

4

by which Radisson Plc group is able to raise finance.

Loan Stock:

Another source of finance is loan stock is a long term debt capital financing technique

adopted by company on which they have to pay interest on a predetermined rate of interest to

lenders. Holders of loan stock are long termed creditors of company. Debenture is a form of loan

stock, legally defined as a written acknowledgement of debt incurred by company, normally

containing provisions about the payment of interest and eventual repayment of capital amount.

When a business expands their operational area its becomes challenging for enterprise to

adopt the most appropriate source of financing for the particular situation. While selecting the

source of finance, there are some implications of different source which business have to attain.

Each source have its own merits and demerits. Radisson PLC have to select the appropriate

source of financing with analysing its advantages and disadvantages (Voss, Sirdeshmukh, and

Voss, 2008). Depending upon the suitability for purpose, the adopted source should match the

terms of finance of projects. They are as follows:

Long term bank loans:

A debt financing obligation issued by bank or any financial institution for organisations

that hold legal claims to borrowers assets. The loan is considered the most important to all other

claim against borrowers, which in the event of bankruptcy, bank loan is the first to be repaid,

before any other interested parties receives any payment.

Implications:

Legal Implication: Subject to asset seizure in case of default.

Financial Implication: For instance, interest should be paid on monthly, quarterly, half

yearly, or annually basis by the Radisson group to the banks after taking debt from the bank.

Dilution of control implication:There is no dilution of control.

Bankruptcy Implication: Bank have the obligation to recover the loan form the asset used

to secure loan, if in future organisation become insolvent.

Equity Share:

Equity ownership is accompanied by providing voting rights and entitling the holder to a

share of company's success through dividends or capital appreciation. These denominations

provide a holder several rights and through this the shareholders become the owner of the

respective company (Remund, 2010). The characteristics like they have their term in company as

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

long as it exists or until they withdraw themselves from company, have the privilege to buy

additional share directly from company, etc.

Implications:

Legal Implications: Equity holders have right to vote in board meeting and any other

proceedings related to them.

Financial Implication: As per the equity source of finance the PLC group has no

obligation to pay to equity holders, if they bear losses in any financial year.

Dilution of control implication: The equity holders have their diluted control in

proceedings of company as they are the owners of company.

Bankruptcy:They are last one to be paid from the residual asset of the company incase of

insolvency.

Leasing:

The acquisitions of assets particularly expensive capital requirements, leasing facility

allows a business to use asset over a fixed period of time, in returns of regular payment. As with

hire purchase, the business customer will normally be responsible for maintenance of the

equipment.

Implications:

Legal Implications: Legal agreement is required in case of leasing, here the PLC

company have to complete all the formalities in terms of documents which are legal.

Financial Implication: Tax charged on monthly lease rental and on residual value at the

end of lease. Entity can claim lease rental as a tax deduction.

Dilution of control implication: Control over company is not diluted but pull out of asset

in case of default that may hamper operations.

Bankruptcy: Suppliers have right to sue the party for first payment in case of bankruptcy.

Retained Earnings:

The amount of earnings retained within the business is termed as retained earnings. It has

a direct impact on the amount of dividends because this is the amount which is not distributed

among the shareholders. The amount which is not distributed is use in the PLC firm in order to

raise capital and expand the projects. This could be turns into great sources of financing for

sweet menu as they are continuously making profits over the years.

Implications:

Legal Implications: Have to be shown for tax purposes in financial statements.

5

additional share directly from company, etc.

Implications:

Legal Implications: Equity holders have right to vote in board meeting and any other

proceedings related to them.

Financial Implication: As per the equity source of finance the PLC group has no

obligation to pay to equity holders, if they bear losses in any financial year.

Dilution of control implication: The equity holders have their diluted control in

proceedings of company as they are the owners of company.

Bankruptcy:They are last one to be paid from the residual asset of the company incase of

insolvency.

Leasing:

The acquisitions of assets particularly expensive capital requirements, leasing facility

allows a business to use asset over a fixed period of time, in returns of regular payment. As with

hire purchase, the business customer will normally be responsible for maintenance of the

equipment.

Implications:

Legal Implications: Legal agreement is required in case of leasing, here the PLC

company have to complete all the formalities in terms of documents which are legal.

Financial Implication: Tax charged on monthly lease rental and on residual value at the

end of lease. Entity can claim lease rental as a tax deduction.

Dilution of control implication: Control over company is not diluted but pull out of asset

in case of default that may hamper operations.

Bankruptcy: Suppliers have right to sue the party for first payment in case of bankruptcy.

Retained Earnings:

The amount of earnings retained within the business is termed as retained earnings. It has

a direct impact on the amount of dividends because this is the amount which is not distributed

among the shareholders. The amount which is not distributed is use in the PLC firm in order to

raise capital and expand the projects. This could be turns into great sources of financing for

sweet menu as they are continuously making profits over the years.

Implications:

Legal Implications: Have to be shown for tax purposes in financial statements.

5

Financial Implication: Company have to bear lack of profitability due to its financial

implications.

Dilution of control implication: Entity may loose control over their earnings as their

Bankruptcy: The entity may face the bankruptcy as they may face negative earnings

Sale of Assets: If business entity tends to sale their any asset for obtaining some finance, this

conclude a loss in business fixed asset. Whit this the Mentioned PLC enterprise can acquire

money but may lose an asset.

Implications:

Legal Implications: Proper sale agreement need to be prepared.

Financial Implication: The sale of asset may be done on profit or on loss which

sometimes may not be suitable in context of company.

Dilution of control implication: After sale the control of asset transferred to the new

users.

Bankruptcy: Sale agreement tends to get cancelled if buyer fails to pay amount due to

bankruptcy.

B

As there several ways of raising the funds for the organisations. The source of finance

should relate with nature of business as it provides entity an appropriate opportunity of funding.

As Radisson PLC is in stage of expanding their business activities, they have several options

available to fund their financial resources for expansion plans. Large organisations are able to

use a wider variety of finance sources than are smaller ones (Meyer and et. al., 2009). Saving are

an obvious way to putting money into business but as being a large scale organisations its not

provide enough assistance for the future plans. In contrast, companies raise finance by issuing

shares. Large companies often have thousands of different shareholders. There are several

number options available for the Radisson Plc in order to raise the fund in business. From

various sources, appropriate sources for respective firm are given as below:

Equity Shares: As per the equity source the company raise fund through offering shares

in the market. These helps to the business in terms of finance to set up and expand business

activities. This is appropriate because the company is raise fund from various shareholder which

are become a part of the firm and company has to pay only dividend amount to them. There is

not any another extra costs has to pay the firm for raising fund.

6

implications.

Dilution of control implication: Entity may loose control over their earnings as their

Bankruptcy: The entity may face the bankruptcy as they may face negative earnings

Sale of Assets: If business entity tends to sale their any asset for obtaining some finance, this

conclude a loss in business fixed asset. Whit this the Mentioned PLC enterprise can acquire

money but may lose an asset.

Implications:

Legal Implications: Proper sale agreement need to be prepared.

Financial Implication: The sale of asset may be done on profit or on loss which

sometimes may not be suitable in context of company.

Dilution of control implication: After sale the control of asset transferred to the new

users.

Bankruptcy: Sale agreement tends to get cancelled if buyer fails to pay amount due to

bankruptcy.

B

As there several ways of raising the funds for the organisations. The source of finance

should relate with nature of business as it provides entity an appropriate opportunity of funding.

As Radisson PLC is in stage of expanding their business activities, they have several options

available to fund their financial resources for expansion plans. Large organisations are able to

use a wider variety of finance sources than are smaller ones (Meyer and et. al., 2009). Saving are

an obvious way to putting money into business but as being a large scale organisations its not

provide enough assistance for the future plans. In contrast, companies raise finance by issuing

shares. Large companies often have thousands of different shareholders. There are several

number options available for the Radisson Plc in order to raise the fund in business. From

various sources, appropriate sources for respective firm are given as below:

Equity Shares: As per the equity source the company raise fund through offering shares

in the market. These helps to the business in terms of finance to set up and expand business

activities. This is appropriate because the company is raise fund from various shareholder which

are become a part of the firm and company has to pay only dividend amount to them. There is

not any another extra costs has to pay the firm for raising fund.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Banks: Another specific source of finance is bank loan which helps to finance capital

projects and overdrafts helps to manage the cash flow structures. As per the source the firm have

to pay only interest rate to the bank and there is no need to pay another costs of finance. Hence,

for the Radisson Plc the bank loan and equity share are appropriate.

To earn some extra finance, a business can borrow loans from banks as well as financial

institutions. A loan helps the organisation to secure a sufficient amount of funds at a time to meet

out business activities. Repayment of loan is made with interest. The lender of money needs to

know all the business opportunities and risks involved and will therefore want to see a detailed

business plan.

These are some financial resources which helps the Radisson PLC to fund their financial

resources (Daily and et. al., 2009). Depending on their scenarios of their projects they can opt

any of the option as required for long term or may be for short term.

TASK 2

A

The management of Radisson PLC is unsure about the capital structure of company and

for funding the project they have decided to analyse the cost of funding by equity versus debt

finance structures (Malmi and Brown, 2008). The decision of financing fund by debt or by equity

have some major impacts on entity. These are discussed here under:

Debt Finance

It refers to borrow money from outside source with the promise to payback the borrowed

amount along with interest on an agreed date. Some businesses feel timid from borrowing

money, but debt financing certainly have its own advantages. It can be utilised to fund any kind

or size of business. As per the finance the Radisson Plc firm is able to raise fund from the debt or

loan. For debt finance there are bank, financial institutions etc. are available.

Some businesses feel timid from borrowing money, but debt financing certainly have its

own advantages. It can be utilised to fund any kind or size of business.

Equity Finance

In the world of small business, equity financing, means raising capital by selling shares of

a business to investors. Unlike debts, the raised capital isn't paid back in instalments along with

interest. Instead, investors put money into the Radisson group and become partial owners of that

business. They are then entitled to a share of the business's profits over time. Most investors

expect a return on their investment within three to five years

7

projects and overdrafts helps to manage the cash flow structures. As per the source the firm have

to pay only interest rate to the bank and there is no need to pay another costs of finance. Hence,

for the Radisson Plc the bank loan and equity share are appropriate.

To earn some extra finance, a business can borrow loans from banks as well as financial

institutions. A loan helps the organisation to secure a sufficient amount of funds at a time to meet

out business activities. Repayment of loan is made with interest. The lender of money needs to

know all the business opportunities and risks involved and will therefore want to see a detailed

business plan.

These are some financial resources which helps the Radisson PLC to fund their financial

resources (Daily and et. al., 2009). Depending on their scenarios of their projects they can opt

any of the option as required for long term or may be for short term.

TASK 2

A

The management of Radisson PLC is unsure about the capital structure of company and

for funding the project they have decided to analyse the cost of funding by equity versus debt

finance structures (Malmi and Brown, 2008). The decision of financing fund by debt or by equity

have some major impacts on entity. These are discussed here under:

Debt Finance

It refers to borrow money from outside source with the promise to payback the borrowed

amount along with interest on an agreed date. Some businesses feel timid from borrowing

money, but debt financing certainly have its own advantages. It can be utilised to fund any kind

or size of business. As per the finance the Radisson Plc firm is able to raise fund from the debt or

loan. For debt finance there are bank, financial institutions etc. are available.

Some businesses feel timid from borrowing money, but debt financing certainly have its

own advantages. It can be utilised to fund any kind or size of business.

Equity Finance

In the world of small business, equity financing, means raising capital by selling shares of

a business to investors. Unlike debts, the raised capital isn't paid back in instalments along with

interest. Instead, investors put money into the Radisson group and become partial owners of that

business. They are then entitled to a share of the business's profits over time. Most investors

expect a return on their investment within three to five years

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is not for everyone, but provide a alternative to debt for several business owners. In

fact, equity financing cannot be charged with the two biggest gripes business owners level

against debt financing: the constraint it places on available cash flow and the risk associated with

personally guaranteeing a loan (Malmi and Brown, 2008).

In an appropriate market it is said to be that the finance policy which is being adopted by

a company should be Debt Equity Financial Structure having a ratio in Debt and Equity is of

0.5:1 and it is considered as the best policy being opted by the company for financing its funds

and financial resources. The policy adopted by Radisson PLC should be compiler of Debt and

Equity as its helps the organisation to manages its funds and also perform in the interest of

stakeholders as well as organisation.

B

Framing the structure of financial plan is a considerable step for the entity to decide about

its future planning and to evaluate about the working of entity. The financial plan, or budget as it

is also known, helps company to manages its day to day decision making policies (Siano,

Kitchen and Giovanna Confetto, 2010). Comparing forecast numbers to actual results yields

important information about the overall financial health and efficiency of business. Even one

person company also needs a financial plan to carry out their activity. The Radisson PLC is

going to expand their business so they have to frame a proper plan relating to their needs and

requirements of funds and their utilisation. Some of them are discussed here under:

Cash Management:

Every business have a monthly or seasonal variation in texture of revenue, which depicts

the time period when entity have plenty of cash and a scenario where they have shortage. In

framing a financial plan, entity have to take these cycles into account to keep a tight rein on

expenditures during forecast low revenue periods. Poor cash management can result in negative

consequences such as not being able to make payroll. The cash cushion allows the business to

take advantage of opportunities that arise, such as the chance to purchase inventory from a

supplier at temporarily reduced prices.

Spotting Trends:

An entity have obligation of taking various decision in a course of month that it can be

difficult to analyse that which decision have what kind of effect business activities. Preparing a

financial plan, involves settings some quantifiable targets which helps to compare with the actual

8

fact, equity financing cannot be charged with the two biggest gripes business owners level

against debt financing: the constraint it places on available cash flow and the risk associated with

personally guaranteeing a loan (Malmi and Brown, 2008).

In an appropriate market it is said to be that the finance policy which is being adopted by

a company should be Debt Equity Financial Structure having a ratio in Debt and Equity is of

0.5:1 and it is considered as the best policy being opted by the company for financing its funds

and financial resources. The policy adopted by Radisson PLC should be compiler of Debt and

Equity as its helps the organisation to manages its funds and also perform in the interest of

stakeholders as well as organisation.

B

Framing the structure of financial plan is a considerable step for the entity to decide about

its future planning and to evaluate about the working of entity. The financial plan, or budget as it

is also known, helps company to manages its day to day decision making policies (Siano,

Kitchen and Giovanna Confetto, 2010). Comparing forecast numbers to actual results yields

important information about the overall financial health and efficiency of business. Even one

person company also needs a financial plan to carry out their activity. The Radisson PLC is

going to expand their business so they have to frame a proper plan relating to their needs and

requirements of funds and their utilisation. Some of them are discussed here under:

Cash Management:

Every business have a monthly or seasonal variation in texture of revenue, which depicts

the time period when entity have plenty of cash and a scenario where they have shortage. In

framing a financial plan, entity have to take these cycles into account to keep a tight rein on

expenditures during forecast low revenue periods. Poor cash management can result in negative

consequences such as not being able to make payroll. The cash cushion allows the business to

take advantage of opportunities that arise, such as the chance to purchase inventory from a

supplier at temporarily reduced prices.

Spotting Trends:

An entity have obligation of taking various decision in a course of month that it can be

difficult to analyse that which decision have what kind of effect business activities. Preparing a

financial plan, involves settings some quantifiable targets which helps to compare with the actual

8

results during a financial year (Voss, Sirdeshmukh and Voss, 2008). Trends in the sales of

individual products help the entity make decisions about how to allocate marketing dollars.

Financial planning plays an integral role in each and every organisation to run the firm

very smoothly and earn profit. Assessment of financial plan in context of various terms of the

enterprise are given as below: Identification of shortages and surpluses: Financial plan is very helpful to identify

situation of financial resources in the business. When company is going to make the

financial plan for upcoming years then it able to derive that, there is a shortage or surplus

of finance. It helps to prepare of formulate strategies which lead to increase profitability

and performance of the firm in the industry. Budgeting: The process where the firm is able to identify incomes and expenditures for

next financial years, known as a budgeting process. It is one type of financial plan where

it forecast and prepare budget, it will give informations that for next year how much

financial resources will be require. It helps to management in order to make effective

products and services and enhance performance level in the industry as well. Implications of failure finance adequately: It is very necessary for every enterprise that

it has adequate finance in order to run the business very smoothly. If finance is not

adequate in anyone functions or departments of the firm then overall production or

business process will hamper which lead to affects the firm in negative manner. With

help of financial plan the management is able to overcome or reduce this type of

obstacles and problems.

Over trading: A situation where firm is produce goods and services in more numbers

compare to availability of resources and requirements, known as an over trading. When

this type of situation occurs in the management then it can overcome by proper financial

plan. From effective budget preparation also firm can reduce over trading, because

budget gives informations related to cash inflows and outflows for upcoming year and

estimate production level as well.

C

The finance department of a company is section which generates a variety of information

for the entity and its higher authorities for making decisions required by the company. The

financial system of Radisson PLC provide some realistic objective picture of actual business

position in company (Chandra, 2011). Financial system depicts the information of past

9

individual products help the entity make decisions about how to allocate marketing dollars.

Financial planning plays an integral role in each and every organisation to run the firm

very smoothly and earn profit. Assessment of financial plan in context of various terms of the

enterprise are given as below: Identification of shortages and surpluses: Financial plan is very helpful to identify

situation of financial resources in the business. When company is going to make the

financial plan for upcoming years then it able to derive that, there is a shortage or surplus

of finance. It helps to prepare of formulate strategies which lead to increase profitability

and performance of the firm in the industry. Budgeting: The process where the firm is able to identify incomes and expenditures for

next financial years, known as a budgeting process. It is one type of financial plan where

it forecast and prepare budget, it will give informations that for next year how much

financial resources will be require. It helps to management in order to make effective

products and services and enhance performance level in the industry as well. Implications of failure finance adequately: It is very necessary for every enterprise that

it has adequate finance in order to run the business very smoothly. If finance is not

adequate in anyone functions or departments of the firm then overall production or

business process will hamper which lead to affects the firm in negative manner. With

help of financial plan the management is able to overcome or reduce this type of

obstacles and problems.

Over trading: A situation where firm is produce goods and services in more numbers

compare to availability of resources and requirements, known as an over trading. When

this type of situation occurs in the management then it can overcome by proper financial

plan. From effective budget preparation also firm can reduce over trading, because

budget gives informations related to cash inflows and outflows for upcoming year and

estimate production level as well.

C

The finance department of a company is section which generates a variety of information

for the entity and its higher authorities for making decisions required by the company. The

financial system of Radisson PLC provide some realistic objective picture of actual business

position in company (Chandra, 2011). Financial system depicts the information of past

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance of organisation. These statements can be compared with the results achieved by

similar companies or in previous periods to identify area for improvement.

Profit and Loss accounts providing details of whether the business is making efficient use of

financial resources.

Balance Sheet information providing details of a businesses assets and liabilities, as well

as the liquidity of the business.

Sales and purchases information setting out particular types of trading and accounts with

particular customers and suppliers.

Information about the purchase of assets and liabilities.

Information about the wages paid out by a business.

Information about costs (Remund, 2010).

By providing a steady and up-to-date flow of information, a business is able to make appropriate

decisions about:

How to reduce costs

How to increase sales

How to raise profitability

When to purchase new capital assets

The best sources of finance, and duration, etc.

In the present case to raise fund there is two options are selected such as bank loan and

equity shares which are impact to the financial statements of Radisson PLC group. Impact on

financial statements form both sources of finance are gives as below:

Bank Loan: When company raise finance in business through loan then in balance sheet

of PLC group liabilities will be increase and treated as a long term debt in liability side.

Apart from this in profit and loss expenses will increase and net profit will decrease due

to paying interest amount to the bank. In income statement it will be treated as an interest

amount in expense side.

Equity Shares: Another source is equity share which have cost is dividend amount. In the

income statements profit will be decrease and it will be treated as a dividend amount in

expense side. After that in balance sheet liabilities side it will be treated as a capital.

10

similar companies or in previous periods to identify area for improvement.

Profit and Loss accounts providing details of whether the business is making efficient use of

financial resources.

Balance Sheet information providing details of a businesses assets and liabilities, as well

as the liquidity of the business.

Sales and purchases information setting out particular types of trading and accounts with

particular customers and suppliers.

Information about the purchase of assets and liabilities.

Information about the wages paid out by a business.

Information about costs (Remund, 2010).

By providing a steady and up-to-date flow of information, a business is able to make appropriate

decisions about:

How to reduce costs

How to increase sales

How to raise profitability

When to purchase new capital assets

The best sources of finance, and duration, etc.

In the present case to raise fund there is two options are selected such as bank loan and

equity shares which are impact to the financial statements of Radisson PLC group. Impact on

financial statements form both sources of finance are gives as below:

Bank Loan: When company raise finance in business through loan then in balance sheet

of PLC group liabilities will be increase and treated as a long term debt in liability side.

Apart from this in profit and loss expenses will increase and net profit will decrease due

to paying interest amount to the bank. In income statement it will be treated as an interest

amount in expense side.

Equity Shares: Another source is equity share which have cost is dividend amount. In the

income statements profit will be decrease and it will be treated as a dividend amount in

expense side. After that in balance sheet liabilities side it will be treated as a capital.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hence, financial statements are affects after raising fund from different sources of

finance.

TASK 3

A

Budget is an estimation of the revenue and expenses over a specified future period and is

compiled and re-evaluated on a periodic basis. Budget takes important place in every business.

With help of budget the Radisson Plc is able to compare budgeted data with actual data. By this

the management can know that expected data are variate from actual data or not, if not then able

to take corrective actions. Budget variation is helps to derive performance of the business by

various methods. The management able to know with help of variance analysis that firm is able

to meet with budgeted sales and profit or not. Importance of budget are following below:

1. First of all, the budget necessitates the establishment of a program and regulates and

emphasizes performance within that program. Company cannot prepare a budget without

first establishing a complete program, after which changes in the program will reflect as

variances in the budget.

2. It encourages participation and promotes understanding by club officers and other club

employees such as the club manager and the professional.

3. It requires that all expenditures be specifically labelled, whereby they immediately gain

identity.

4. The budget identifies immediate needs for the coming year. Budget variances point out

areas of concern, such as too much labour being used in one area, possibly suggesting the

purchase of a new piece of maintenance equipment.

5. It provides continuity of operations, especially helpful when super intended or club

officers change.

6. It provides the superintendent with a vehicle to evaluate his maintenance program.

7. Budgets regulate inventories. It restricts the purchase and storing of unneeded supplies.

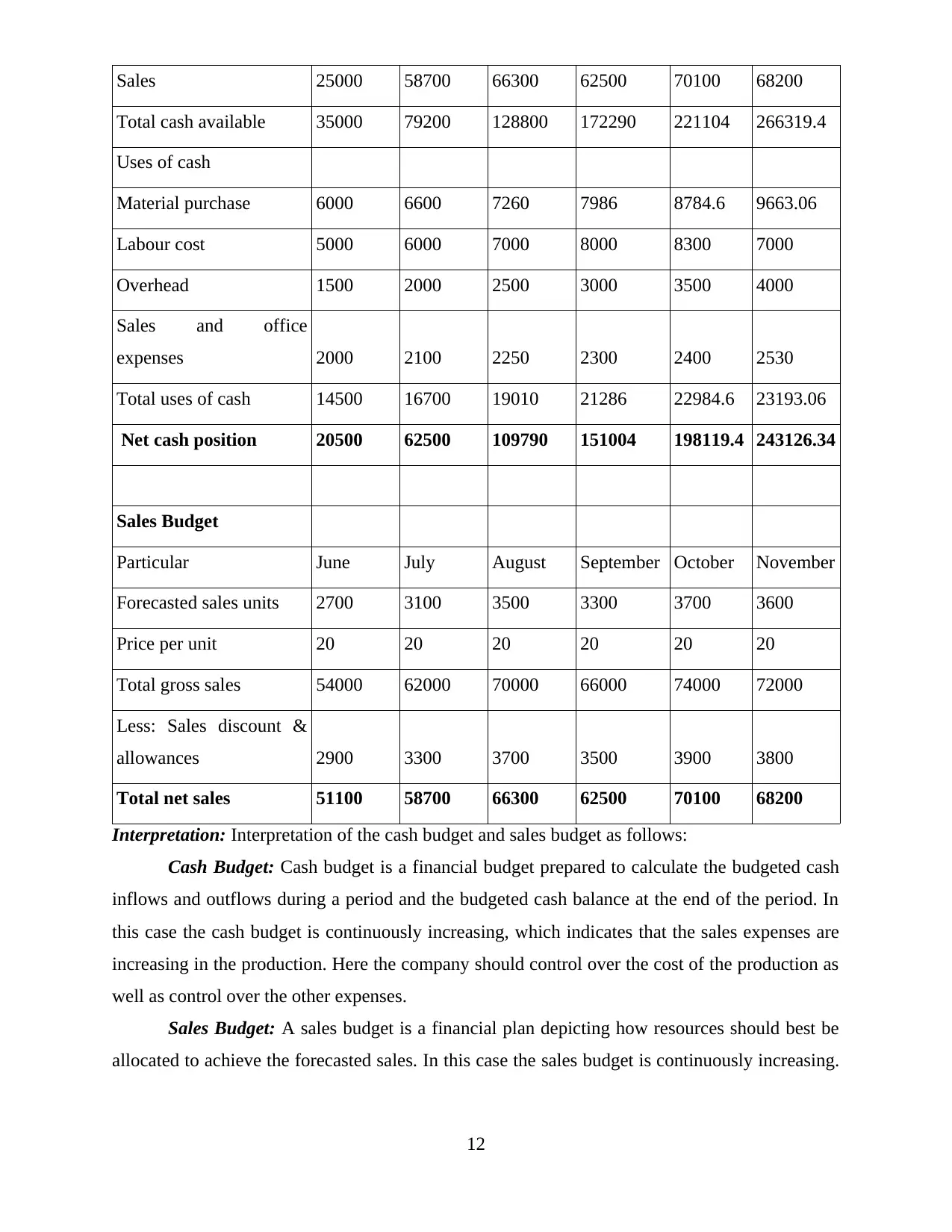

Table 1: Cash and Sales Budget

Cash Budget

Particular June July August September October November

Opening balance 10000 20500 62500 109790 151004 198119.4

11

finance.

TASK 3

A

Budget is an estimation of the revenue and expenses over a specified future period and is

compiled and re-evaluated on a periodic basis. Budget takes important place in every business.

With help of budget the Radisson Plc is able to compare budgeted data with actual data. By this

the management can know that expected data are variate from actual data or not, if not then able

to take corrective actions. Budget variation is helps to derive performance of the business by

various methods. The management able to know with help of variance analysis that firm is able

to meet with budgeted sales and profit or not. Importance of budget are following below:

1. First of all, the budget necessitates the establishment of a program and regulates and

emphasizes performance within that program. Company cannot prepare a budget without

first establishing a complete program, after which changes in the program will reflect as

variances in the budget.

2. It encourages participation and promotes understanding by club officers and other club

employees such as the club manager and the professional.

3. It requires that all expenditures be specifically labelled, whereby they immediately gain

identity.

4. The budget identifies immediate needs for the coming year. Budget variances point out

areas of concern, such as too much labour being used in one area, possibly suggesting the

purchase of a new piece of maintenance equipment.

5. It provides continuity of operations, especially helpful when super intended or club

officers change.

6. It provides the superintendent with a vehicle to evaluate his maintenance program.

7. Budgets regulate inventories. It restricts the purchase and storing of unneeded supplies.

Table 1: Cash and Sales Budget

Cash Budget

Particular June July August September October November

Opening balance 10000 20500 62500 109790 151004 198119.4

11

Sales 25000 58700 66300 62500 70100 68200

Total cash available 35000 79200 128800 172290 221104 266319.4

Uses of cash

Material purchase 6000 6600 7260 7986 8784.6 9663.06

Labour cost 5000 6000 7000 8000 8300 7000

Overhead 1500 2000 2500 3000 3500 4000

Sales and office

expenses 2000 2100 2250 2300 2400 2530

Total uses of cash 14500 16700 19010 21286 22984.6 23193.06

Net cash position 20500 62500 109790 151004 198119.4 243126.34

Sales Budget

Particular June July August September October November

Forecasted sales units 2700 3100 3500 3300 3700 3600

Price per unit 20 20 20 20 20 20

Total gross sales 54000 62000 70000 66000 74000 72000

Less: Sales discount &

allowances 2900 3300 3700 3500 3900 3800

Total net sales 51100 58700 66300 62500 70100 68200

Interpretation: Interpretation of the cash budget and sales budget as follows:

Cash Budget: Cash budget is a financial budget prepared to calculate the budgeted cash

inflows and outflows during a period and the budgeted cash balance at the end of the period. In

this case the cash budget is continuously increasing, which indicates that the sales expenses are

increasing in the production. Here the company should control over the cost of the production as

well as control over the other expenses.

Sales Budget: A sales budget is a financial plan depicting how resources should best be

allocated to achieve the forecasted sales. In this case the sales budget is continuously increasing.

12

Total cash available 35000 79200 128800 172290 221104 266319.4

Uses of cash

Material purchase 6000 6600 7260 7986 8784.6 9663.06

Labour cost 5000 6000 7000 8000 8300 7000

Overhead 1500 2000 2500 3000 3500 4000

Sales and office

expenses 2000 2100 2250 2300 2400 2530

Total uses of cash 14500 16700 19010 21286 22984.6 23193.06

Net cash position 20500 62500 109790 151004 198119.4 243126.34

Sales Budget

Particular June July August September October November

Forecasted sales units 2700 3100 3500 3300 3700 3600

Price per unit 20 20 20 20 20 20

Total gross sales 54000 62000 70000 66000 74000 72000

Less: Sales discount &

allowances 2900 3300 3700 3500 3900 3800

Total net sales 51100 58700 66300 62500 70100 68200

Interpretation: Interpretation of the cash budget and sales budget as follows:

Cash Budget: Cash budget is a financial budget prepared to calculate the budgeted cash

inflows and outflows during a period and the budgeted cash balance at the end of the period. In

this case the cash budget is continuously increasing, which indicates that the sales expenses are

increasing in the production. Here the company should control over the cost of the production as

well as control over the other expenses.

Sales Budget: A sales budget is a financial plan depicting how resources should best be

allocated to achieve the forecasted sales. In this case the sales budget is continuously increasing.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.