Managing Financial Resources and Decisions: Finance Report

VerifiedAdded on 2020/02/17

|17

|4875

|30

Report

AI Summary

This report comprehensively examines financial resource management and decision-making processes. It begins by identifying and evaluating various sources of finance available to both unincorporated and incorporated businesses, including internal and external options, and then assesses their implications. The report analyzes the costs associated with different financing methods, such as interest, dividends, and tax, and explores the importance of financial planning, including budgeting and the implications of inadequate financing, using Clariton Antiques Ltd. as a case study. Furthermore, it evaluates the information required for making financing decisions by venture capitalists, partners, and finance brokers. The report also delves into cash budgeting, its use in pricing decisions, and the application of investment appraisal techniques. Finally, it analyzes and compares financial statements using accounting ratios to assess a company's performance, providing a holistic overview of financial management practices and their impact on business operations and strategic decisions.

MANAGING FINANCIAL RESOURCES AND DECISIONS

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction......................................................................................................................................3

Task 1: LO1 (1.1, 1.2 and 1.3).........................................................................................................3

Task 2: LO2 (2.1, 2.2, 2.3 and 2.4)..................................................................................................5

Task 3: LO3 (3.1, 3.2 and 3.3).........................................................................................................9

Task 4: LO4 (4.1, 4.2 and 4.3).......................................................................................................14

Conclusion.....................................................................................................................................17

Reference list.................................................................................................................................18

2

Introduction......................................................................................................................................3

Task 1: LO1 (1.1, 1.2 and 1.3).........................................................................................................3

Task 2: LO2 (2.1, 2.2, 2.3 and 2.4)..................................................................................................5

Task 3: LO3 (3.1, 3.2 and 3.3).........................................................................................................9

Task 4: LO4 (4.1, 4.2 and 4.3).......................................................................................................14

Conclusion.....................................................................................................................................17

Reference list.................................................................................................................................18

2

Introduction

Managing financial resources is completely different from managing physical resources.

Financial resources are those resources that can be measured or valued in monetary terms or

having monetary denominations. Financial resources give rise in both gains and losses depending

upon the management techniques. The main aim of the study is to evaluate the techniques of

managing the financial resources and decision-making by properly analyzing the given tasks

with respect to the financial resources (Greene et al. 2015). It has been decided to explore the

concept of sources of finance available to the business and how the business can avail or utilize

in accordance with their need. It has also been decided to understand the financials decision

made by the business entity and investors by using the financial information related to the

business available to them. Moreover, the study focuses on the analysis of cash budget and its

use in the pricing decision. The use of investment appraisal technique is also applied to

understand the viability of the project undertaken by the company. Finally, the financial

statement of the company is analyzed and compared with the previous year’s performance by

using appropriate accounting ratios.

Task 1: LO1 (1.1, 1.2 and 1.3)

Task 1.1

Identifying the sources of finance available to both unincorporated and incorporated

business

Sources of finance refer to the availability of the sources from where any business entity,

irrespective of their size and nature can raise funds for the different business purposes. Sources

of finance are available to both unincorporated business as well as incorporated business

Sources of finance available to unincorporated business

The unincorporated business includes family trust, partnership and sole proprietorship because

they do not posses any separate legal entity from its owner. The sources of finance available to

this kind of business include personal savings, small business loan and small business line of

credit for partnership business (Corsatea et al. 2014). Sources of finance like angel investors,

private investors, business grants and bank loans are available to sole proprietorship.

Sources of finance available to incorporated business

3

Managing financial resources is completely different from managing physical resources.

Financial resources are those resources that can be measured or valued in monetary terms or

having monetary denominations. Financial resources give rise in both gains and losses depending

upon the management techniques. The main aim of the study is to evaluate the techniques of

managing the financial resources and decision-making by properly analyzing the given tasks

with respect to the financial resources (Greene et al. 2015). It has been decided to explore the

concept of sources of finance available to the business and how the business can avail or utilize

in accordance with their need. It has also been decided to understand the financials decision

made by the business entity and investors by using the financial information related to the

business available to them. Moreover, the study focuses on the analysis of cash budget and its

use in the pricing decision. The use of investment appraisal technique is also applied to

understand the viability of the project undertaken by the company. Finally, the financial

statement of the company is analyzed and compared with the previous year’s performance by

using appropriate accounting ratios.

Task 1: LO1 (1.1, 1.2 and 1.3)

Task 1.1

Identifying the sources of finance available to both unincorporated and incorporated

business

Sources of finance refer to the availability of the sources from where any business entity,

irrespective of their size and nature can raise funds for the different business purposes. Sources

of finance are available to both unincorporated business as well as incorporated business

Sources of finance available to unincorporated business

The unincorporated business includes family trust, partnership and sole proprietorship because

they do not posses any separate legal entity from its owner. The sources of finance available to

this kind of business include personal savings, small business loan and small business line of

credit for partnership business (Corsatea et al. 2014). Sources of finance like angel investors,

private investors, business grants and bank loans are available to sole proprietorship.

Sources of finance available to incorporated business

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incorporated business include any kind of corporate body or company whether may be private

limited or public limited. They possess the separate legal entity from their owner. The sources of

finance available to this kind of business include both internal and external sources. Stock and

other assets held for sale, retained profit, working capital, bank borrowings, equity funding and

bonds or securities are some of the sources of finance available to the incorporated public

companies. However, incorporated private companies can raise funds from the similar sources

but not from shares or securities, because only listed public companies are entitled to raise funds

from shares publicly (Lee et al. 2015). In addition, raising funds from the subsidiary companies

or taking the loan from subsidiaries are considered as the internal source of finance and both

public and private companies have right to raise funds from this source if the company has any

subsidiary. Apart from this, both the companies can borrow money from other companies other

than subsidiaries, which will be called as the external source of finance.

Task 1.2

Evaluating the internal and external sources of finance and their sources of finance

A business need both short term finance and long-term finance to cover their daily expenses and

to grow or expand the business respectively. Short-term finance provides the business with

working capital and long-term sources of equity funding. Assessment of implication for using

internal and external sources of finance varies from companies to companies based on their need.

Evaluating the internal source of finance and its implications

The internal source of finance can be utilized in different ways and for different purposes by the

business entity. Personal savings can be used according to the wish of the owner of the business.

Especially small business utilizes the personal savings more. Retained profit can be utilized for

obtaining or purchasing or repairing machinery, It system and vehicles. A business entity can

also utilize this source of finance for marketing and advertising purpose (Fraser et al. 2015).

Working capital can be utilized to meet daily expenses like rent, salaries, stationery, bills and

other invoice payments because working capital provides short-term money to the business.

Funds raised from selling the assets can be utilized to develop or grow new areas of business like

the purchase of property can be made by selling old property.

Evaluating the external source of finance and its implications

An external source of finance can be utilized in different ways and for different purposes by the

business entity. Shares are issued to raise funds from the public by the limited companies in

4

limited or public limited. They possess the separate legal entity from their owner. The sources of

finance available to this kind of business include both internal and external sources. Stock and

other assets held for sale, retained profit, working capital, bank borrowings, equity funding and

bonds or securities are some of the sources of finance available to the incorporated public

companies. However, incorporated private companies can raise funds from the similar sources

but not from shares or securities, because only listed public companies are entitled to raise funds

from shares publicly (Lee et al. 2015). In addition, raising funds from the subsidiary companies

or taking the loan from subsidiaries are considered as the internal source of finance and both

public and private companies have right to raise funds from this source if the company has any

subsidiary. Apart from this, both the companies can borrow money from other companies other

than subsidiaries, which will be called as the external source of finance.

Task 1.2

Evaluating the internal and external sources of finance and their sources of finance

A business need both short term finance and long-term finance to cover their daily expenses and

to grow or expand the business respectively. Short-term finance provides the business with

working capital and long-term sources of equity funding. Assessment of implication for using

internal and external sources of finance varies from companies to companies based on their need.

Evaluating the internal source of finance and its implications

The internal source of finance can be utilized in different ways and for different purposes by the

business entity. Personal savings can be used according to the wish of the owner of the business.

Especially small business utilizes the personal savings more. Retained profit can be utilized for

obtaining or purchasing or repairing machinery, It system and vehicles. A business entity can

also utilize this source of finance for marketing and advertising purpose (Fraser et al. 2015).

Working capital can be utilized to meet daily expenses like rent, salaries, stationery, bills and

other invoice payments because working capital provides short-term money to the business.

Funds raised from selling the assets can be utilized to develop or grow new areas of business like

the purchase of property can be made by selling old property.

Evaluating the external source of finance and its implications

An external source of finance can be utilized in different ways and for different purposes by the

business entity. Shares are issued to raise funds from the public by the limited companies in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exchange for a return on their investment. It helps the business to create opportunities for the

investment in the market. Loans can be used by the business for its expansion or future

development or complete the projects or repay the old loan. Business grants can be used launch a

new business in the competitive area and these grants can be available from councils or different

government bodies (Fraser et al. 2015). A company can even raise funds from debentures, but it

becomes risky for the business because they are to be paid first at the time of liquidation and the

payment of interest to them is mandatory irrespective of the profit or loss earned by the business.

Task 1.3

Evaluating the most appropriate sources of finance for Clariton Antiques Ltd

From the case problem it is found that Clariton Antiques Ltd started as partnership business and

and after a long time, it incorporated as the public limited company. The company already has

two branches in London and wants to build new branch in Birmingham. In order to open a new

branch in Birmingham, the company requires £ 0.5 million. It is found that the company already

has two loans at present and intends to raise more funds from loan. However, the company is

deciding to raise £ 0.5 million from public in terms of share. Raising money from the public in

terms of shares requires utmost care, like the cost to the company, the risk to the company, return

on investment and future viability. If the whole amount is raised as preference share, the cost to

the company will be moderate and the risk will be moderate. If the company fails in the new

business, the company will not need to pay the dividend. In case if the whole money would be

raised from debentures or loan, the risk to the company will be very high, but the cost to the

company will be very low. It is seen that Clariton already has two pending loans and need some

more loans. Thus, it 80% of £ 0.5 million can be raised from public shares and rest can be raised

from debentures. In this way, company will not face many risks and will get cost benefit.

Task 2: LO2 (2.1, 2.2, 2.3 and 2.4)

Task 2.1

Evaluating the costs of the sources of finance with reference to interest, dividends and tax

Evaluating cost of finance with reference to dividends

If the company receives funds from equity shares, the cost to company will be high and risk will

be very low, but there will be full dilution. However, payment of dividend is not compulsory,

even though the company earns profit (Baker et al. 2016). If the company receives funds from

5

investment in the market. Loans can be used by the business for its expansion or future

development or complete the projects or repay the old loan. Business grants can be used launch a

new business in the competitive area and these grants can be available from councils or different

government bodies (Fraser et al. 2015). A company can even raise funds from debentures, but it

becomes risky for the business because they are to be paid first at the time of liquidation and the

payment of interest to them is mandatory irrespective of the profit or loss earned by the business.

Task 1.3

Evaluating the most appropriate sources of finance for Clariton Antiques Ltd

From the case problem it is found that Clariton Antiques Ltd started as partnership business and

and after a long time, it incorporated as the public limited company. The company already has

two branches in London and wants to build new branch in Birmingham. In order to open a new

branch in Birmingham, the company requires £ 0.5 million. It is found that the company already

has two loans at present and intends to raise more funds from loan. However, the company is

deciding to raise £ 0.5 million from public in terms of share. Raising money from the public in

terms of shares requires utmost care, like the cost to the company, the risk to the company, return

on investment and future viability. If the whole amount is raised as preference share, the cost to

the company will be moderate and the risk will be moderate. If the company fails in the new

business, the company will not need to pay the dividend. In case if the whole money would be

raised from debentures or loan, the risk to the company will be very high, but the cost to the

company will be very low. It is seen that Clariton already has two pending loans and need some

more loans. Thus, it 80% of £ 0.5 million can be raised from public shares and rest can be raised

from debentures. In this way, company will not face many risks and will get cost benefit.

Task 2: LO2 (2.1, 2.2, 2.3 and 2.4)

Task 2.1

Evaluating the costs of the sources of finance with reference to interest, dividends and tax

Evaluating cost of finance with reference to dividends

If the company receives funds from equity shares, the cost to company will be high and risk will

be very low, but there will be full dilution. However, payment of dividend is not compulsory,

even though the company earns profit (Baker et al. 2016). If the company receives funds from

5

preference shareholders, the company the cost to company will be moderate and risk will be

moderate as well, but dilution will only rise if the company fails to pay dividend. However,

payment of dividend only becomes compulsory if the company earns profit. In case of Clariton

Antique Ltd., have decided to expand their business by raising funds of £ 0.5 million for 20%

stake from finance limited (a venture capital organization).

Funds received from finance limited = £ 500,000 (Assumed that finance limited is a shareholder)

Stake = 20%

Cost to company = £ 500,000 * 20%

= £ 100,000 (dividend)

Corporate dividend tax (7.5%) = £ 100,000 * 7.5%

= £ 7,500

Therefore, total cost to company with respect to dividend is £ 7,500

Evaluating cost of finance with reference to interest

If the company receives funds from a bank or other financial institution or debentures, the cost to

the company will be very low, but the risk will be very high, because the payment of interest is

always compulsory, whether or not the company is earning profit or loss. Moreover, during the

dissolution of the company, they will be paid first; due to this, the business enjoys low cost to the

company. It is found that Clarioton had an agreement with finance limited that finance broker

will charge 1% as a service or brokerage fee for obtaining a bank loan on the amount secured.

The term of the loan is 10 years and the annual payable interest rate is 2%.

Loan amount = £ 500,000

APR = 2%

Brokerage fee = 1%

Cost to company for 1 year = £ 500,000 * (2% +1%)

= £ 15,000

Therefore, total cost to company with respect to the interest is £ 15,000

Evaluating cost of finance with reference to tax

A public company needs to pay tax after the compulsory payment of finance cost (interest and

dividend) to get net profit. However, the corporate dividend tax is deducted from the taxable

amount, because the company pays it during the time of payment of dividend

Task 2.2

6

moderate as well, but dilution will only rise if the company fails to pay dividend. However,

payment of dividend only becomes compulsory if the company earns profit. In case of Clariton

Antique Ltd., have decided to expand their business by raising funds of £ 0.5 million for 20%

stake from finance limited (a venture capital organization).

Funds received from finance limited = £ 500,000 (Assumed that finance limited is a shareholder)

Stake = 20%

Cost to company = £ 500,000 * 20%

= £ 100,000 (dividend)

Corporate dividend tax (7.5%) = £ 100,000 * 7.5%

= £ 7,500

Therefore, total cost to company with respect to dividend is £ 7,500

Evaluating cost of finance with reference to interest

If the company receives funds from a bank or other financial institution or debentures, the cost to

the company will be very low, but the risk will be very high, because the payment of interest is

always compulsory, whether or not the company is earning profit or loss. Moreover, during the

dissolution of the company, they will be paid first; due to this, the business enjoys low cost to the

company. It is found that Clarioton had an agreement with finance limited that finance broker

will charge 1% as a service or brokerage fee for obtaining a bank loan on the amount secured.

The term of the loan is 10 years and the annual payable interest rate is 2%.

Loan amount = £ 500,000

APR = 2%

Brokerage fee = 1%

Cost to company for 1 year = £ 500,000 * (2% +1%)

= £ 15,000

Therefore, total cost to company with respect to the interest is £ 15,000

Evaluating cost of finance with reference to tax

A public company needs to pay tax after the compulsory payment of finance cost (interest and

dividend) to get net profit. However, the corporate dividend tax is deducted from the taxable

amount, because the company pays it during the time of payment of dividend

Task 2.2

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Understanding the importance of financial planning, with reference to overtrading,

budgeting and implication of failure to finance adequately for Clariton Antiques Ltd

Importance of financial planning, with reference to budgeting

Budgeting will help Clariton to make optimum utilization of its business resources. Cash budget

or revenue budget will provide the company with an idea of specific time taken by the debtors to

pay back the money and it will also help the company to make prediction of the revenue. Thus,

financial planning based on eth budgeting is very important (Baker et al. 2016).

Importance of financial planning, with reference to overtrading

Overtrading simply refers to the engagement of the company in more than one business.

Overtrading helps the company in many best ways. For instance, a company has incurred heavy

losses in one business, but it incurred heavy gain in another business, therefore, this business will

help the company to set off the loss of other business. If Clariton is engaged in overtrading, it

will help in making the financial decision regarding the procurement of funds.

Importance of financial planning, with reference to implication of failure to finance

adequately

Implication of failure to finance adequately simply states the situation of the business, where the

business is not making optimum use of its available resources. If the company is found in this

kind of situation, it needs to implement internal control properly, also prepare budgets. Thus,

Clariton must take care of the finance.

Task 2.3

Evaluating the information required for making financing decision by venture capitalist,

the partners and the finance brokers

The partners

Since Clariton is a limited company and not a partnership firm, therefore the partners are not

involved in such business.

Venture capitalist (We Finance Limited)

Since venture capitalist (We Finance Limited) is a financial institution, provide loans to the

companies, it will require the information related to the amount of loan taken by the company

throughout its business life. In addition, the Venture capitalist will acquire the information

regarding the financial performance and financial position of the company, because it will help

7

budgeting and implication of failure to finance adequately for Clariton Antiques Ltd

Importance of financial planning, with reference to budgeting

Budgeting will help Clariton to make optimum utilization of its business resources. Cash budget

or revenue budget will provide the company with an idea of specific time taken by the debtors to

pay back the money and it will also help the company to make prediction of the revenue. Thus,

financial planning based on eth budgeting is very important (Baker et al. 2016).

Importance of financial planning, with reference to overtrading

Overtrading simply refers to the engagement of the company in more than one business.

Overtrading helps the company in many best ways. For instance, a company has incurred heavy

losses in one business, but it incurred heavy gain in another business, therefore, this business will

help the company to set off the loss of other business. If Clariton is engaged in overtrading, it

will help in making the financial decision regarding the procurement of funds.

Importance of financial planning, with reference to implication of failure to finance

adequately

Implication of failure to finance adequately simply states the situation of the business, where the

business is not making optimum use of its available resources. If the company is found in this

kind of situation, it needs to implement internal control properly, also prepare budgets. Thus,

Clariton must take care of the finance.

Task 2.3

Evaluating the information required for making financing decision by venture capitalist,

the partners and the finance brokers

The partners

Since Clariton is a limited company and not a partnership firm, therefore the partners are not

involved in such business.

Venture capitalist (We Finance Limited)

Since venture capitalist (We Finance Limited) is a financial institution, provide loans to the

companies, it will require the information related to the amount of loan taken by the company

throughout its business life. In addition, the Venture capitalist will acquire the information

regarding the financial performance and financial position of the company, because it will help

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company to know whether the company is capable of paying its short term and long-term

debt.

Finance broker

The finance broker will require the financial information related to the amount of loan taken by

the company throughout its business life. In addition, finance broker will also require knowing if

the company raising most of the funds from equity shares of preference shares. Since finance

broker always involved in providing financial service for a certain amount of service charge, the

finance broker will then require these information for making financing decision.

Task 2.4

Understanding the impact on the financial statements if Clariton decides to go with either

finance broker or venture capitalist

Identifying the impact on the financial statements if Clariton decides to go with venture

capitalist

If Clariton chooses to go with Venture capitalist (We Finance Limited), the financial statements

of the company will undergo a moderate change. The loan taken by the company will be shown

as the non-current liability of the company if taken for more than a year and the amount of

interest will be shown in the profit and loss account as expenses. In addition, the loan amount

will be shown as the cash inflow in the financing activity of the cash flow statement. However,

during the time of calculating net profit, the interest amount on loan should be deducted before

the deduction of tax.

Identifying the impact on the financial statements if Clariton decides to go with finance

broker

If Clariton chooses to go with finance broker, the financial statements of the company will

undergo a moderate change. The brokerage charge or service fee of the finance broker related to

the service provided by him is to be recorded. If the finance broker provides the service related to

the securities of shares or stock, the brokerage charge should be shown as the compulsory

expense in the profit and loss account. In addition, if the finance broker provides the service

related to the approval of loan or credit, the service charge should be shown as the nominal

expense in the profit and loss account.

8

debt.

Finance broker

The finance broker will require the financial information related to the amount of loan taken by

the company throughout its business life. In addition, finance broker will also require knowing if

the company raising most of the funds from equity shares of preference shares. Since finance

broker always involved in providing financial service for a certain amount of service charge, the

finance broker will then require these information for making financing decision.

Task 2.4

Understanding the impact on the financial statements if Clariton decides to go with either

finance broker or venture capitalist

Identifying the impact on the financial statements if Clariton decides to go with venture

capitalist

If Clariton chooses to go with Venture capitalist (We Finance Limited), the financial statements

of the company will undergo a moderate change. The loan taken by the company will be shown

as the non-current liability of the company if taken for more than a year and the amount of

interest will be shown in the profit and loss account as expenses. In addition, the loan amount

will be shown as the cash inflow in the financing activity of the cash flow statement. However,

during the time of calculating net profit, the interest amount on loan should be deducted before

the deduction of tax.

Identifying the impact on the financial statements if Clariton decides to go with finance

broker

If Clariton chooses to go with finance broker, the financial statements of the company will

undergo a moderate change. The brokerage charge or service fee of the finance broker related to

the service provided by him is to be recorded. If the finance broker provides the service related to

the securities of shares or stock, the brokerage charge should be shown as the compulsory

expense in the profit and loss account. In addition, if the finance broker provides the service

related to the approval of loan or credit, the service charge should be shown as the nominal

expense in the profit and loss account.

8

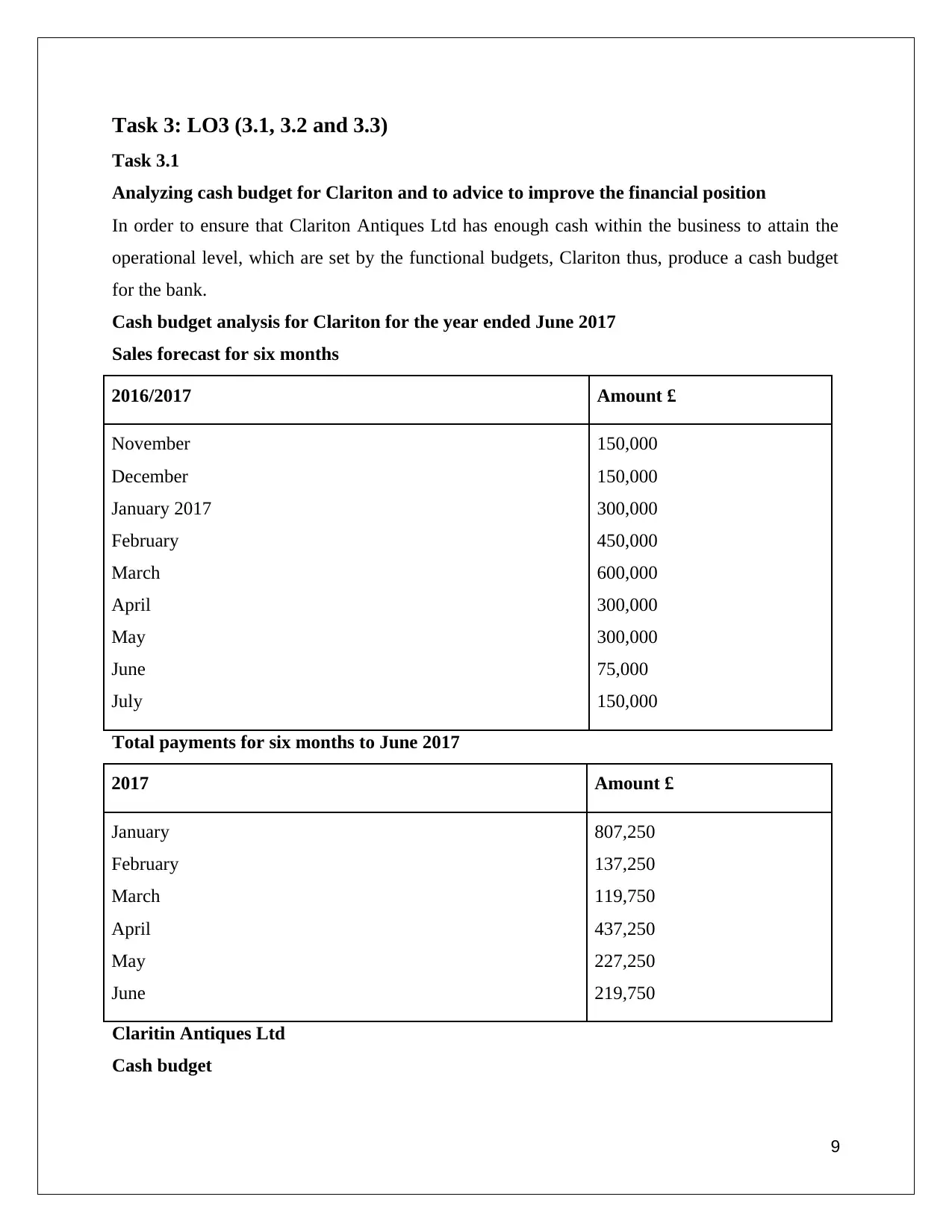

Task 3: LO3 (3.1, 3.2 and 3.3)

Task 3.1

Analyzing cash budget for Clariton and to advice to improve the financial position

In order to ensure that Clariton Antiques Ltd has enough cash within the business to attain the

operational level, which are set by the functional budgets, Clariton thus, produce a cash budget

for the bank.

Cash budget analysis for Clariton for the year ended June 2017

Sales forecast for six months

Amount £2016/2017

150,000

150,000

300,000

450,000

600,000

300,000

300,000

75,000

150,000

November

December

January 2017

February

March

April

May

June

July

Total payments for six months to June 2017

Amount £2017

807,250

137,250

119,750

437,250

227,250

219,750

January

February

March

April

May

June

Claritin Antiques Ltd

Cash budget

9

Task 3.1

Analyzing cash budget for Clariton and to advice to improve the financial position

In order to ensure that Clariton Antiques Ltd has enough cash within the business to attain the

operational level, which are set by the functional budgets, Clariton thus, produce a cash budget

for the bank.

Cash budget analysis for Clariton for the year ended June 2017

Sales forecast for six months

Amount £2016/2017

150,000

150,000

300,000

450,000

600,000

300,000

300,000

75,000

150,000

November

December

January 2017

February

March

April

May

June

July

Total payments for six months to June 2017

Amount £2017

807,250

137,250

119,750

437,250

227,250

219,750

January

February

March

April

May

June

Claritin Antiques Ltd

Cash budget

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

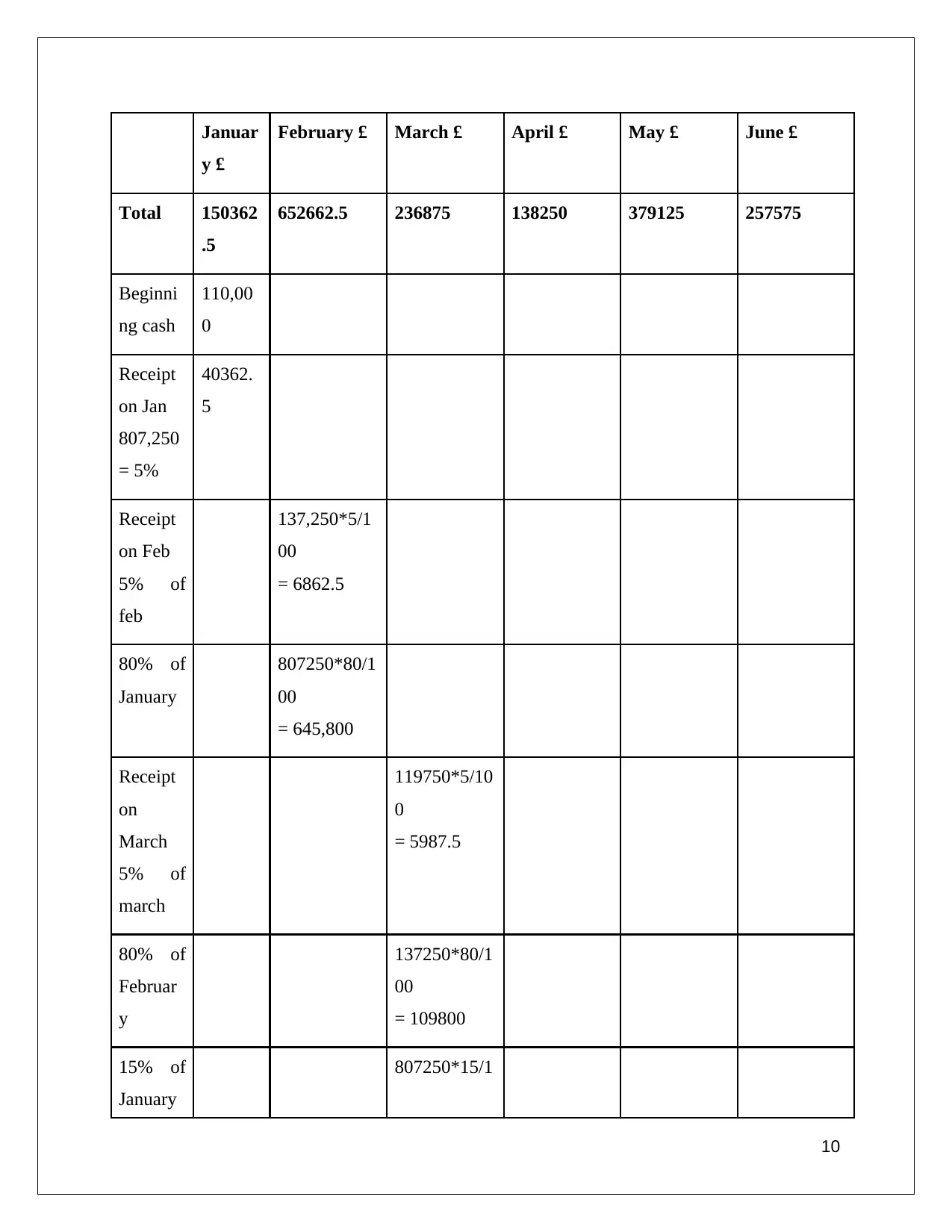

Januar

y £

February £ March £ April £ May £ June £

Total 150362

.5

652662.5 236875 138250 379125 257575

Beginni

ng cash

110,00

0

Receipt

on Jan

807,250

= 5%

40362.

5

Receipt

on Feb

5% of

feb

137,250*5/1

00

= 6862.5

80% of

January

807250*80/1

00

= 645,800

Receipt

on

March

5% of

march

119750*5/10

0

= 5987.5

80% of

Februar

y

137250*80/1

00

= 109800

15% of

January

807250*15/1

10

y £

February £ March £ April £ May £ June £

Total 150362

.5

652662.5 236875 138250 379125 257575

Beginni

ng cash

110,00

0

Receipt

on Jan

807,250

= 5%

40362.

5

Receipt

on Feb

5% of

feb

137,250*5/1

00

= 6862.5

80% of

January

807250*80/1

00

= 645,800

Receipt

on

March

5% of

march

119750*5/10

0

= 5987.5

80% of

Februar

y

137250*80/1

00

= 109800

15% of

January

807250*15/1

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

00

=121087.5

Receipt

on April

5% of

April

437250*5/10

0

= 21862.5

80% of

march

119750*80/1

00

=95800

15% of

Februar

y

137250*15/1

00

= 20587.5

Receipt

on May

5% of

may

227250*5/10

0

=11362.5

80% of

April

437250*80/1

00

= 349800

15% of

March

119750*15/1

00

=17962.5

Receipt

on June

5% of

June

219750*5/10

0

= 10987.5

11

=121087.5

Receipt

on April

5% of

April

437250*5/10

0

= 21862.5

80% of

march

119750*80/1

00

=95800

15% of

Februar

y

137250*15/1

00

= 20587.5

Receipt

on May

5% of

may

227250*5/10

0

=11362.5

80% of

April

437250*80/1

00

= 349800

15% of

March

119750*15/1

00

=17962.5

Receipt

on June

5% of

June

219750*5/10

0

= 10987.5

11

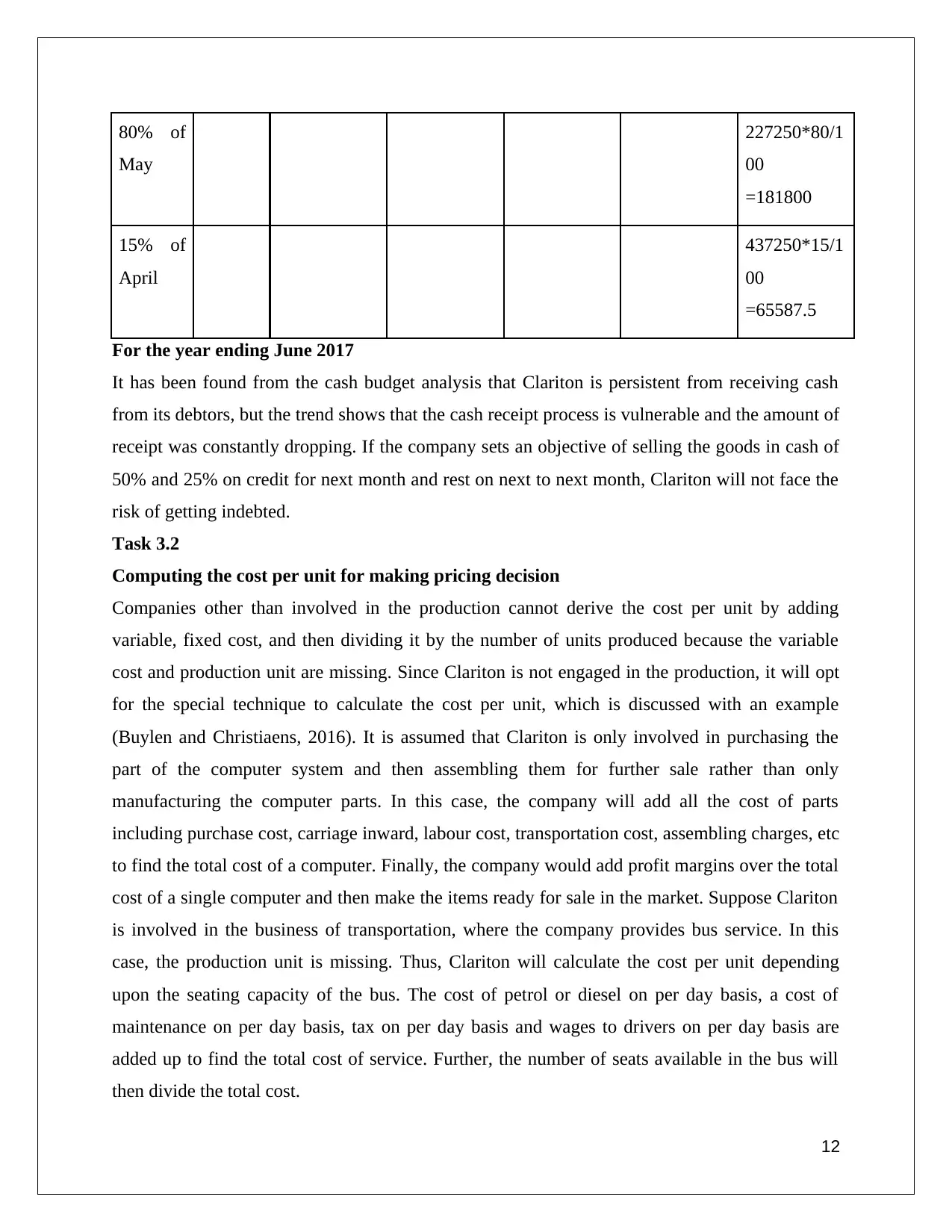

80% of

May

227250*80/1

00

=181800

15% of

April

437250*15/1

00

=65587.5

For the year ending June 2017

It has been found from the cash budget analysis that Clariton is persistent from receiving cash

from its debtors, but the trend shows that the cash receipt process is vulnerable and the amount of

receipt was constantly dropping. If the company sets an objective of selling the goods in cash of

50% and 25% on credit for next month and rest on next to next month, Clariton will not face the

risk of getting indebted.

Task 3.2

Computing the cost per unit for making pricing decision

Companies other than involved in the production cannot derive the cost per unit by adding

variable, fixed cost, and then dividing it by the number of units produced because the variable

cost and production unit are missing. Since Clariton is not engaged in the production, it will opt

for the special technique to calculate the cost per unit, which is discussed with an example

(Buylen and Christiaens, 2016). It is assumed that Clariton is only involved in purchasing the

part of the computer system and then assembling them for further sale rather than only

manufacturing the computer parts. In this case, the company will add all the cost of parts

including purchase cost, carriage inward, labour cost, transportation cost, assembling charges, etc

to find the total cost of a computer. Finally, the company would add profit margins over the total

cost of a single computer and then make the items ready for sale in the market. Suppose Clariton

is involved in the business of transportation, where the company provides bus service. In this

case, the production unit is missing. Thus, Clariton will calculate the cost per unit depending

upon the seating capacity of the bus. The cost of petrol or diesel on per day basis, a cost of

maintenance on per day basis, tax on per day basis and wages to drivers on per day basis are

added up to find the total cost of service. Further, the number of seats available in the bus will

then divide the total cost.

12

May

227250*80/1

00

=181800

15% of

April

437250*15/1

00

=65587.5

For the year ending June 2017

It has been found from the cash budget analysis that Clariton is persistent from receiving cash

from its debtors, but the trend shows that the cash receipt process is vulnerable and the amount of

receipt was constantly dropping. If the company sets an objective of selling the goods in cash of

50% and 25% on credit for next month and rest on next to next month, Clariton will not face the

risk of getting indebted.

Task 3.2

Computing the cost per unit for making pricing decision

Companies other than involved in the production cannot derive the cost per unit by adding

variable, fixed cost, and then dividing it by the number of units produced because the variable

cost and production unit are missing. Since Clariton is not engaged in the production, it will opt

for the special technique to calculate the cost per unit, which is discussed with an example

(Buylen and Christiaens, 2016). It is assumed that Clariton is only involved in purchasing the

part of the computer system and then assembling them for further sale rather than only

manufacturing the computer parts. In this case, the company will add all the cost of parts

including purchase cost, carriage inward, labour cost, transportation cost, assembling charges, etc

to find the total cost of a computer. Finally, the company would add profit margins over the total

cost of a single computer and then make the items ready for sale in the market. Suppose Clariton

is involved in the business of transportation, where the company provides bus service. In this

case, the production unit is missing. Thus, Clariton will calculate the cost per unit depending

upon the seating capacity of the bus. The cost of petrol or diesel on per day basis, a cost of

maintenance on per day basis, tax on per day basis and wages to drivers on per day basis are

added up to find the total cost of service. Further, the number of seats available in the bus will

then divide the total cost.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.