Financial Management Analysis: Decisions, Objectives, and Statements

VerifiedAdded on 2022/10/19

|14

|4849

|28

Report

AI Summary

This report offers a comprehensive overview of financial management, encompassing its core definitions and objectives. It details the three primary financial decisions: investment, financing, and dividend decisions, explaining their significance and impact on a company's performance. The report also explores the agency problem, outlining potential conflicts of interest and strategies to mitigate them, such as monitoring, incentives, and part ownership. Furthermore, it examines the key financial statements – the balance sheet, income statement, cash flow statement, and statement of owner's equity – and their roles in assessing a company's financial health. The report emphasizes both profit maximization and wealth maximization as critical objectives of financial management, alongside other objectives such as proper mobilization and utilization of finance, increasing efficiency, and maintaining proper cash flow. The content is designed to provide students with a solid understanding of financial management principles and practices.

Financial Management

Definitions of financial management

• According to J. F. Bradley, “Financial management is the area of business management

devoted to the judicious use of capital & careful selection of sources of capital in order to

enable a spending unit to move in the direction of reaching its goals.”

• Financial Management means planning, organizing, directing and controlling the financial

activities such as procurement and utilization of funds of the enterprise. It means applying

general management principles to financial resources of the enterprise.

• “Financial management is the operational activity of a business that is responsible for

obtaining and effectively utilizing the funds necessary for efficient operation.”

• Financial management is managing financial assets ethically, in accordance with government

regulations to achieve the organization's goals.

Functions/Decisions of Finance (Previous question)

The functions of finance involve three major decisions a company must make-

the investment decision, the financing decision, and the dividend/share repurchase decision.

1. Investment Decisions:

An investment is an asset or item acquired with the goal of generating income or

appreciation. Appreciation refers to an increase in the value of an asset over time.

Managers need to decide on the amount of investment available out of the existing finance,

on a long-term and short-term basis.

They are of two types:

I. Long-term investment decisions or Capital Budgeting mean committing funds for a

long period of time like fixed assets. These decisions are irreversible and usually include

the ones pertaining to investing in a building and/or land, acquiring new

plants/machinery or replacing the old ones, etc. These decisions determine the financial

pursuits and performance of a business.

II. Short-term investment decisions or Working Capital Management means committing

funds for a short period of time like current assets. These involve decisions pertaining to

the investment of funds in the inventory, cash, bank deposits, and other short-term

investments. They directly affect the liquidity and performance of the business.

2. Financing Decisions:

Finance is the process of raising funds or capital for any kind of expenditure.

Managers also make decisions pertaining to raising finance from long-term sources and

short-term sources.

Definitions of financial management

• According to J. F. Bradley, “Financial management is the area of business management

devoted to the judicious use of capital & careful selection of sources of capital in order to

enable a spending unit to move in the direction of reaching its goals.”

• Financial Management means planning, organizing, directing and controlling the financial

activities such as procurement and utilization of funds of the enterprise. It means applying

general management principles to financial resources of the enterprise.

• “Financial management is the operational activity of a business that is responsible for

obtaining and effectively utilizing the funds necessary for efficient operation.”

• Financial management is managing financial assets ethically, in accordance with government

regulations to achieve the organization's goals.

Functions/Decisions of Finance (Previous question)

The functions of finance involve three major decisions a company must make-

the investment decision, the financing decision, and the dividend/share repurchase decision.

1. Investment Decisions:

An investment is an asset or item acquired with the goal of generating income or

appreciation. Appreciation refers to an increase in the value of an asset over time.

Managers need to decide on the amount of investment available out of the existing finance,

on a long-term and short-term basis.

They are of two types:

I. Long-term investment decisions or Capital Budgeting mean committing funds for a

long period of time like fixed assets. These decisions are irreversible and usually include

the ones pertaining to investing in a building and/or land, acquiring new

plants/machinery or replacing the old ones, etc. These decisions determine the financial

pursuits and performance of a business.

II. Short-term investment decisions or Working Capital Management means committing

funds for a short period of time like current assets. These involve decisions pertaining to

the investment of funds in the inventory, cash, bank deposits, and other short-term

investments. They directly affect the liquidity and performance of the business.

2. Financing Decisions:

Finance is the process of raising funds or capital for any kind of expenditure.

Managers also make decisions pertaining to raising finance from long-term sources and

short-term sources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

They are of two types:

I. Financial Planning decisions which relate to estimating the sources and application of

funds.

• It means pre-estimating financial needs of an organization to ensure the availability

of adequate finance.

• The primary objective of financial planning is to plan and ensure that the funds are

available as and when required.

II. Capital Structure decisions which involve identifying sources of funds. They also involve

decisions with respect to choosing external sources like issuing shares, bonds, borrowing

from banks or internal sources like retained earnings for raising funds.

3. Dividend Decisions:

A dividend is the distribution of a company's earnings to its shareholders and is determined

by the company's board of directors. Dividends are often distributed quarterly and may be

paid out as cash or in the form of reinvestment in additional stock.

Dividend Decisions involve decisions related to the portion of profits that will be distributed

as dividend.

Two alternatives are available in dealing with the profits of a firm:

(i) they can be distributed to the shareholders in the form of dividends or

(ii) they can be retained in the business itself as retained earnings.

Shareholders always demand a higher dividend, while the management would want to retain profits

for business needs. Hence, this is a complex managerial decision.

Objective of Financial Management (Previous question)

Financial management is concerned with procurement and use of funds. Its main aim is to use

business funds in such a way that the firm’s value / earnings are maximized. Financial

management provides a frame work for selecting a proper course of action and deciding a viable

commercial strategy. The main objective of a business is to maximize the owner’s economic

welfare. This objective can be achieved by;

• Profit Maximization.

• Wealth Maximization.

1. Profit maximization: This is the main objective of financial management. The finance

manager strives to achieve optimal profit in the short term and long-term course of business.

The finance manager shall try to achieve as high as profits. The company makes a decent profit

in the long run if the finance manager makes the proper decisions using the various methods

and tools available

2. Wealth maximization: It means shareholders’ value maximization. Wealth maximization

means earning maximum wealth for shareholders. So, the finance manager tries to give

maximum dividends to shareholders. The dividend declaration and payout policy are decided

I. Financial Planning decisions which relate to estimating the sources and application of

funds.

• It means pre-estimating financial needs of an organization to ensure the availability

of adequate finance.

• The primary objective of financial planning is to plan and ensure that the funds are

available as and when required.

II. Capital Structure decisions which involve identifying sources of funds. They also involve

decisions with respect to choosing external sources like issuing shares, bonds, borrowing

from banks or internal sources like retained earnings for raising funds.

3. Dividend Decisions:

A dividend is the distribution of a company's earnings to its shareholders and is determined

by the company's board of directors. Dividends are often distributed quarterly and may be

paid out as cash or in the form of reinvestment in additional stock.

Dividend Decisions involve decisions related to the portion of profits that will be distributed

as dividend.

Two alternatives are available in dealing with the profits of a firm:

(i) they can be distributed to the shareholders in the form of dividends or

(ii) they can be retained in the business itself as retained earnings.

Shareholders always demand a higher dividend, while the management would want to retain profits

for business needs. Hence, this is a complex managerial decision.

Objective of Financial Management (Previous question)

Financial management is concerned with procurement and use of funds. Its main aim is to use

business funds in such a way that the firm’s value / earnings are maximized. Financial

management provides a frame work for selecting a proper course of action and deciding a viable

commercial strategy. The main objective of a business is to maximize the owner’s economic

welfare. This objective can be achieved by;

• Profit Maximization.

• Wealth Maximization.

1. Profit maximization: This is the main objective of financial management. The finance

manager strives to achieve optimal profit in the short term and long-term course of business.

The finance manager shall try to achieve as high as profits. The company makes a decent profit

in the long run if the finance manager makes the proper decisions using the various methods

and tools available

2. Wealth maximization: It means shareholders’ value maximization. Wealth maximization

means earning maximum wealth for shareholders. So, the finance manager tries to give

maximum dividends to shareholders. The dividend declaration and payout policy are decided

by financial management. Dividend decisions include a proper dividend policy regarding the

distribution or retaining of company profits. This is related to the performance of the company.

Better the performance, the higher is the market value of shares. In nutshell, the finance

manager tries to maximize shareholders’ value. It has some advantages such

• A firm that maximizes its profits also ensures its long-term survival.

• Wealth maximization is better for society.

• A profitable business can attract investors, which leads to a positive environment for

everyone.

• Wealth maximization considers the time value of money.

Other Objectives:

1. Proper mobilization: Mobilization of finance is an important objective of financial

management. It means utilizing effectively the sources of finance. The finance manager can

manage various sources of funds such as shares, and debentures, after estimating the financial

requirements, the finance manager must decide about the sources of finance.

2. Increase efficiency: Financial management tries to increase the efficiency of all sections of

the company. Proper distribution of finance to all departments increases the efficiency of the

entire company.

3. Proper estimation of total financial requirements: This means that the finance manager

would be able to estimate the financial requirements of the company. He should be able to

compute how much financing is required to start and run the business/ He shall estimate the

fixed and working capital requirements of the company. If not, there will be a shortage or

surplus of finance. The finance manager shall use various factors like the technology used by

the company, the number of employees used, the scale of operations, and legal requirements.

4. Proper utilization of finance: The finance manager must make optimum utilization of

finance. This can be done by using various financial tools such as managing receivables,

effective payment policy in hand, and better inventory management.

5. Maintaining proper cash flow: The financial manager shall ensure that there is a regular

supply of liquidity in the company monitoring closely all the cash inflows and outflows

reducing the instances of underflow and overflow of cash. The finance manager is entrusted

with the responsibility to maintain an optimum level of liquidity. Healthy cash flow improves

the chances of survival and success of the company.

6. Survival of company: The company must survive in this competitive business world. Hence,

the finance manager shall take all the decisions intuitively. The big decisions shall be taken

with proper due diligence and consultancy with consultants.

7. Creating reserves: The higher the reserves, the better it will be for the company to overcome

uncertainty. The company shall have an optimal dividend payout policy that will help itself to

create reserves over the year. It must also keep the profits as reserves. The reserves can be

used for the expansion of the company and for overcoming uncertainty. It can also be used to

face contingencies in the future.

distribution or retaining of company profits. This is related to the performance of the company.

Better the performance, the higher is the market value of shares. In nutshell, the finance

manager tries to maximize shareholders’ value. It has some advantages such

• A firm that maximizes its profits also ensures its long-term survival.

• Wealth maximization is better for society.

• A profitable business can attract investors, which leads to a positive environment for

everyone.

• Wealth maximization considers the time value of money.

Other Objectives:

1. Proper mobilization: Mobilization of finance is an important objective of financial

management. It means utilizing effectively the sources of finance. The finance manager can

manage various sources of funds such as shares, and debentures, after estimating the financial

requirements, the finance manager must decide about the sources of finance.

2. Increase efficiency: Financial management tries to increase the efficiency of all sections of

the company. Proper distribution of finance to all departments increases the efficiency of the

entire company.

3. Proper estimation of total financial requirements: This means that the finance manager

would be able to estimate the financial requirements of the company. He should be able to

compute how much financing is required to start and run the business/ He shall estimate the

fixed and working capital requirements of the company. If not, there will be a shortage or

surplus of finance. The finance manager shall use various factors like the technology used by

the company, the number of employees used, the scale of operations, and legal requirements.

4. Proper utilization of finance: The finance manager must make optimum utilization of

finance. This can be done by using various financial tools such as managing receivables,

effective payment policy in hand, and better inventory management.

5. Maintaining proper cash flow: The financial manager shall ensure that there is a regular

supply of liquidity in the company monitoring closely all the cash inflows and outflows

reducing the instances of underflow and overflow of cash. The finance manager is entrusted

with the responsibility to maintain an optimum level of liquidity. Healthy cash flow improves

the chances of survival and success of the company.

6. Survival of company: The company must survive in this competitive business world. Hence,

the finance manager shall take all the decisions intuitively. The big decisions shall be taken

with proper due diligence and consultancy with consultants.

7. Creating reserves: The higher the reserves, the better it will be for the company to overcome

uncertainty. The company shall have an optimal dividend payout policy that will help itself to

create reserves over the year. It must also keep the profits as reserves. The reserves can be

used for the expansion of the company and for overcoming uncertainty. It can also be used to

face contingencies in the future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8. Reduce the cost of capital: This includes risk evaluation, measuring the cost of capital, and

estimating the benefits of a particular project. Managers are responsible for deciding how

available funds should be invested in fixed or current assets to get the best available returns.

9. Prepare capital structure: This means bringing a proper balance between the different

sources of capital. This balance is necessary for liquidity, economy, flexibility, and stability.

Agency problem

Agency problem is the likelihood that managers may place personal goals ahead of corporate

goals. The agency problem arises in business when one party, known as the agent, faces the

expectation of acting in the best interest of another party, known as the principal. Conflicts of

interest can arise if the agent personally gains by not acting in the principal’s best interest.

Agency costs are costs borne by shareholders to prevent/ minimize agency problems as to

contribute to maximize owners’ wealth.

Resolving the Agency Problem

There are different ways in which principal-agent problem can be overcome, which include

monitoring, flexible working hours, incentives, division of labor and delegation of authority, part

ownership, long term contract, facilitation and support, which are discuss below:

1. Monitoring: Shareholders must establish a way of monitoring the performance of their

managers. They might make use of the services of experts to examine carefully the

operations of their managers by employing sovereign consultant to look into the managerial

activities and also satisfactory models might then be implemented.

2. Flexible Working Hours: Working hours issue might be a reason of dissatisfaction

between agents and principals, especially between workers and managers. Presently

lifestyle has greatly changed; so, people expect more indulgence (time for family,

holidays). If workers are not flexible in their working hours, they might lose their

concentration to work. Workers might not focus on the owner’s benefit, as they are not

happy with the working contacts.

3. Incentives: Shareholders can institute the use of incentives so that the managers will

behave in ways that are consistent with the shareholders’ interests such as incentives pay

which is a good way of solving the principal-agent problem affecting firms. This motivates

the workers to strive for profitability and managers are given incentives to motivate them

so also do the workers need to be given incentives too.

4. Division of Labor and Delegation of Authority: More managers should be employed to

supervise workers. So that individual workers will have manager to report too, which will

give each manager to be able to supervise their workers thoroughly. Workers (agents) are

rational utility maximizes and these utilities depend as they do more work for a given

weekly wage. There is situation which workers tend to reduce their work if they are not

closely monitored by their managers (principals).

estimating the benefits of a particular project. Managers are responsible for deciding how

available funds should be invested in fixed or current assets to get the best available returns.

9. Prepare capital structure: This means bringing a proper balance between the different

sources of capital. This balance is necessary for liquidity, economy, flexibility, and stability.

Agency problem

Agency problem is the likelihood that managers may place personal goals ahead of corporate

goals. The agency problem arises in business when one party, known as the agent, faces the

expectation of acting in the best interest of another party, known as the principal. Conflicts of

interest can arise if the agent personally gains by not acting in the principal’s best interest.

Agency costs are costs borne by shareholders to prevent/ minimize agency problems as to

contribute to maximize owners’ wealth.

Resolving the Agency Problem

There are different ways in which principal-agent problem can be overcome, which include

monitoring, flexible working hours, incentives, division of labor and delegation of authority, part

ownership, long term contract, facilitation and support, which are discuss below:

1. Monitoring: Shareholders must establish a way of monitoring the performance of their

managers. They might make use of the services of experts to examine carefully the

operations of their managers by employing sovereign consultant to look into the managerial

activities and also satisfactory models might then be implemented.

2. Flexible Working Hours: Working hours issue might be a reason of dissatisfaction

between agents and principals, especially between workers and managers. Presently

lifestyle has greatly changed; so, people expect more indulgence (time for family,

holidays). If workers are not flexible in their working hours, they might lose their

concentration to work. Workers might not focus on the owner’s benefit, as they are not

happy with the working contacts.

3. Incentives: Shareholders can institute the use of incentives so that the managers will

behave in ways that are consistent with the shareholders’ interests such as incentives pay

which is a good way of solving the principal-agent problem affecting firms. This motivates

the workers to strive for profitability and managers are given incentives to motivate them

so also do the workers need to be given incentives too.

4. Division of Labor and Delegation of Authority: More managers should be employed to

supervise workers. So that individual workers will have manager to report too, which will

give each manager to be able to supervise their workers thoroughly. Workers (agents) are

rational utility maximizes and these utilities depend as they do more work for a given

weekly wage. There is situation which workers tend to reduce their work if they are not

closely monitored by their managers (principals).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Part Ownership: If workers are given sense of ownership like, opportunity to participate

in decision making and having their own shares in the firm, this will make them to see

themselves as owners but not workers, by conveying to a worker part ownership of a

business, the owners can encourage a performance that would increase a company’s profits.

Part ownership is a good method of solving the principal-agent problem between owners

and managers and managers and workers.

6. Long Term Contract: This is another way to overcome principle agent problem, the

owners of a business can attach the success of the business to the long term wealth of its

managers. For instant, managers which are offered a long term contract with a company,

doing this will encourage the manager to develop strategies that will make him / her to

achieve profit maximization in the long run.

7. Facilitation and Support: In this situation management can give support to help

employees to deal with their fear and anxiety during transition periods. The managers can

give departmental reward on behalf of the shareholder to workers which perform well in

particular department, such reward can be inform of monetary, promotion, and this will

create competition for other worker in the department and other departments. And

shareholders can reward managers also by giving encouraging words.

Financial statements

Financial statements are written reports created by a company’s management to summarize the

business’s financial condition over a certain period (quarter, six-monthly, or yearly).

The financial statement has 4 parts

1. Balance Sheet

2. Income Statement

3. Cash Flow Statement

4. Statement of Owner’s Equity

1. Balance Sheet

The balance sheet is a financial statement that provides a snapshot of the assets, liabilities,

and shareholder’s equity.

A = L + OE

2. Income Statement

is the next financial statement everyone should look at. It looks quite different from the

balance sheet. In the income statement, it’s about the revenue and the expenses. It helps in

finding out the net profit and net loss.

3. Cash Flow Statement

The Cash Flow Statement is the third most important statement every investor should look

at. There are three separate statements of a cash flow statement. These statements are cash

flow from the operating activities, cash flow from investing activities, and cash flow from

finance activities.

in decision making and having their own shares in the firm, this will make them to see

themselves as owners but not workers, by conveying to a worker part ownership of a

business, the owners can encourage a performance that would increase a company’s profits.

Part ownership is a good method of solving the principal-agent problem between owners

and managers and managers and workers.

6. Long Term Contract: This is another way to overcome principle agent problem, the

owners of a business can attach the success of the business to the long term wealth of its

managers. For instant, managers which are offered a long term contract with a company,

doing this will encourage the manager to develop strategies that will make him / her to

achieve profit maximization in the long run.

7. Facilitation and Support: In this situation management can give support to help

employees to deal with their fear and anxiety during transition periods. The managers can

give departmental reward on behalf of the shareholder to workers which perform well in

particular department, such reward can be inform of monetary, promotion, and this will

create competition for other worker in the department and other departments. And

shareholders can reward managers also by giving encouraging words.

Financial statements

Financial statements are written reports created by a company’s management to summarize the

business’s financial condition over a certain period (quarter, six-monthly, or yearly).

The financial statement has 4 parts

1. Balance Sheet

2. Income Statement

3. Cash Flow Statement

4. Statement of Owner’s Equity

1. Balance Sheet

The balance sheet is a financial statement that provides a snapshot of the assets, liabilities,

and shareholder’s equity.

A = L + OE

2. Income Statement

is the next financial statement everyone should look at. It looks quite different from the

balance sheet. In the income statement, it’s about the revenue and the expenses. It helps in

finding out the net profit and net loss.

3. Cash Flow Statement

The Cash Flow Statement is the third most important statement every investor should look

at. There are three separate statements of a cash flow statement. These statements are cash

flow from the operating activities, cash flow from investing activities, and cash flow from

finance activities.

4. Owner’s Equity

Owner’s Equity is a financial statement that summarizes changes in the shareholder’s

equity in a given period.

Importance of financial statements (Previous question)

• Financial statements provide a snapshot of a corporation's financial health, giving insight

into its performance, operations, and cash flow.

• Financial statements are essential since they provide information about a company's

revenue, expenses, profitability, and debt.

• Financial ratio analysis involves the evaluation of line items in financial statements to

compare the results to previous periods and competitors.

• Liquidity and solvency ratios provide information about a company's ability to repay its

debts and obligations.

• Valuation ratios help determine a fair value or price target for a company's shares.

Capital Structure

Capital structure (Previous question)

Capital structure is the particular combination of debt and equity used by a company to finance

its overall operations and growth.

Capital structure = Debt/ Equity

Equity capital arises from ownership shares in a company and claims to its future cash flows and

profits. Debt comes in the form of bond issues or loans, while equity may come in the form of

common stock, preferred stock, or retained earnings. Short-term debt is also considered to be part

of the capital structure.

Debt is one of the two main ways a company can raise money in the capital markets. Companies

benefit from debt because of its tax advantages; interest payments made as a result of borrowing

funds may be tax-deductible. Debt also allows a company or business to retain ownership, unlike

equity. Additionally, in times of low-interest rates, debt is abundant and easy to access.

Equity allows outside investors to take partial ownership of the company. Equity is more

expensive than debt, especially when interest rates are low. However, unlike debt, equity does

not need to be paid back. This is a benefit to the company in the case of declining earnings. On

the other hand, equity represents a claim by the owner on the future earnings of the company.

Leverage is the use of debt (borrowed capital) in order to undertake an investment or project.

The result is to multiply the potential returns from a project. At the same time, leverage will also

multiply the potential downside risk in case the investment does not pan out. When one refers to

Owner’s Equity is a financial statement that summarizes changes in the shareholder’s

equity in a given period.

Importance of financial statements (Previous question)

• Financial statements provide a snapshot of a corporation's financial health, giving insight

into its performance, operations, and cash flow.

• Financial statements are essential since they provide information about a company's

revenue, expenses, profitability, and debt.

• Financial ratio analysis involves the evaluation of line items in financial statements to

compare the results to previous periods and competitors.

• Liquidity and solvency ratios provide information about a company's ability to repay its

debts and obligations.

• Valuation ratios help determine a fair value or price target for a company's shares.

Capital Structure

Capital structure (Previous question)

Capital structure is the particular combination of debt and equity used by a company to finance

its overall operations and growth.

Capital structure = Debt/ Equity

Equity capital arises from ownership shares in a company and claims to its future cash flows and

profits. Debt comes in the form of bond issues or loans, while equity may come in the form of

common stock, preferred stock, or retained earnings. Short-term debt is also considered to be part

of the capital structure.

Debt is one of the two main ways a company can raise money in the capital markets. Companies

benefit from debt because of its tax advantages; interest payments made as a result of borrowing

funds may be tax-deductible. Debt also allows a company or business to retain ownership, unlike

equity. Additionally, in times of low-interest rates, debt is abundant and easy to access.

Equity allows outside investors to take partial ownership of the company. Equity is more

expensive than debt, especially when interest rates are low. However, unlike debt, equity does

not need to be paid back. This is a benefit to the company in the case of declining earnings. On

the other hand, equity represents a claim by the owner on the future earnings of the company.

Leverage is the use of debt (borrowed capital) in order to undertake an investment or project.

The result is to multiply the potential returns from a project. At the same time, leverage will also

multiply the potential downside risk in case the investment does not pan out. When one refers to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a company, property, or investment as "highly leveraged," it means that item has more debt than

equity.

How can Financial Leverage affect the Value? (Previous question)

One thing is sure that wherever and whatever way one sources the finance from, it cannot change

the operating income levels. Financial leverage can, at the max, have an impact on the net income

or the EPS (Earning per Share) the reason we are discussing later. Changing the financing mix

means changing the level of debts, and this change in levels of debt can impact the interest payable

by that firm. The decrease in interest would increase the net income and thereby the EPS, and it

is a general belief that the increase in EPS leads to a rise in the firm’s value.

Apparently, under this view, financial leverage is a helpful tool to increase value, but, at the same

time, nothing comes without a cost. Financial leverage increases the risk of bankruptcy. It is

because the higher the level of debt, the higher would be the fixed obligation to honor the interest

payments to the debt’s providers.

Discussion of financial leverage has an obvious objective of finding an optimum capital structure

leading to maximization of the firm’s value. If the cost of capital is high.

Example:

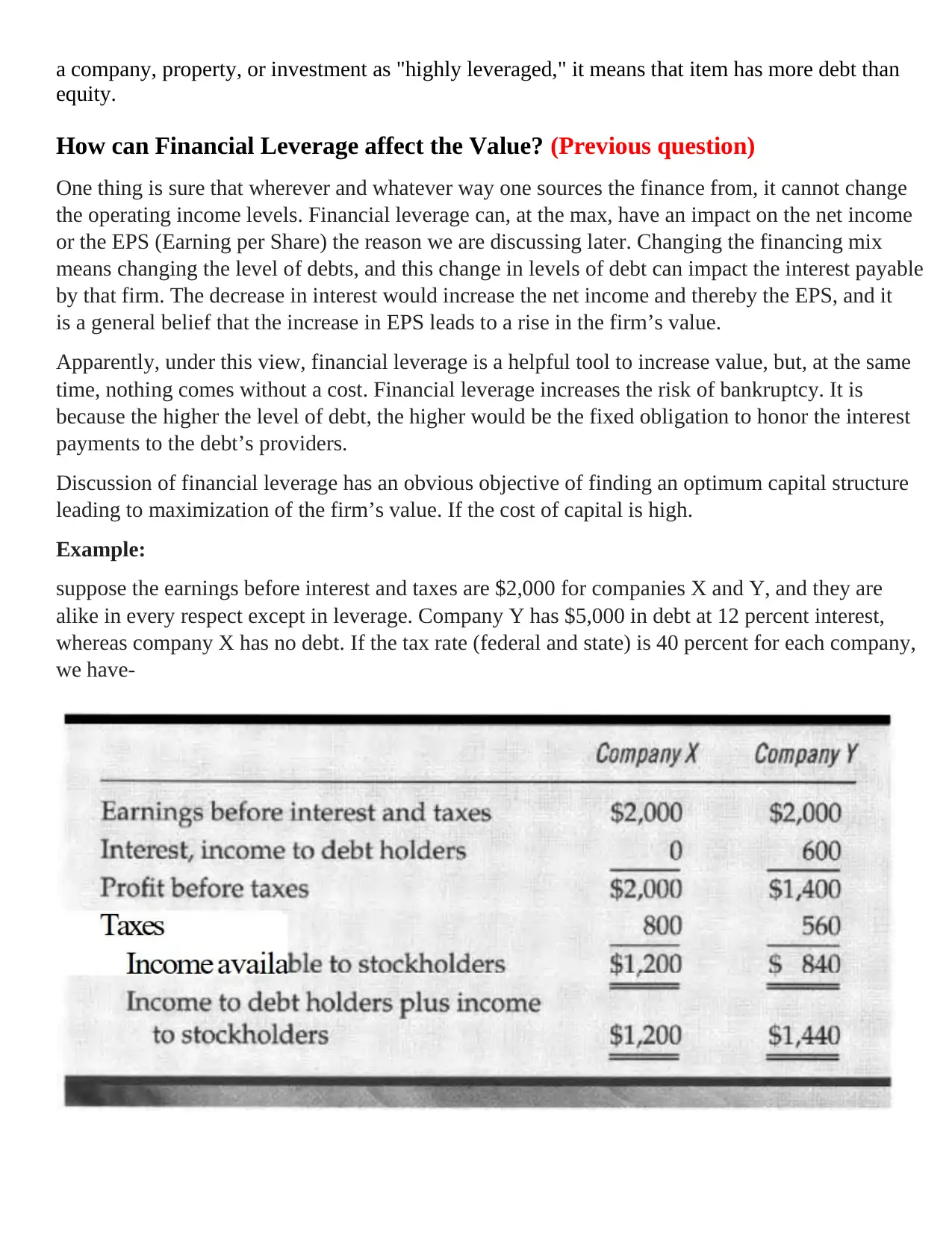

suppose the earnings before interest and taxes are $2,000 for companies X and Y, and they are

alike in every respect except in leverage. Company Y has $5,000 in debt at 12 percent interest,

whereas company X has no debt. If the tax rate (federal and state) is 40 percent for each company,

we have-

equity.

How can Financial Leverage affect the Value? (Previous question)

One thing is sure that wherever and whatever way one sources the finance from, it cannot change

the operating income levels. Financial leverage can, at the max, have an impact on the net income

or the EPS (Earning per Share) the reason we are discussing later. Changing the financing mix

means changing the level of debts, and this change in levels of debt can impact the interest payable

by that firm. The decrease in interest would increase the net income and thereby the EPS, and it

is a general belief that the increase in EPS leads to a rise in the firm’s value.

Apparently, under this view, financial leverage is a helpful tool to increase value, but, at the same

time, nothing comes without a cost. Financial leverage increases the risk of bankruptcy. It is

because the higher the level of debt, the higher would be the fixed obligation to honor the interest

payments to the debt’s providers.

Discussion of financial leverage has an obvious objective of finding an optimum capital structure

leading to maximization of the firm’s value. If the cost of capital is high.

Example:

suppose the earnings before interest and taxes are $2,000 for companies X and Y, and they are

alike in every respect except in leverage. Company Y has $5,000 in debt at 12 percent interest,

whereas company X has no debt. If the tax rate (federal and state) is 40 percent for each company,

we have-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Approaches of Capital Structure

The approaches of capital structures discuss the effect of capital structures on the value of the

firms. All the approaches in the following section discuss whether the capital structure makes

any impact on the firm’s value or not.

1. Net Income Approach

Durand suggested this approach, and he favored the financial leverage decision. According

to him, a change in financial leverage would lead to a change in the cost of capital. In short,

if the ratio of debt in the capital structure increases, the weighted average cost of capital

decreases, and hence the value of the firm increases.

2. Net Operating Income Approach

Durand also provides this approach. It is the opposite of the Net Income Approach if there

are no taxes. This approach says that the weighted average cost of capital remains constant.

It believes in the fact that the market analyses a firm as a whole and discounts at a particular

rate that has no relation to the debt-equity ratio. If tax information is given, it recommends

that WACC reduces with an increase in debt financing, and the firm’s value will start

increasing.

3. Traditional Approach

This approach does not define hard and fast facts, and it says that the cost of capital is a

function of the capital structure. The unique thing about this approach is that it believes in

an optimal capital structure. Optimal capital structure implies that the cost of capital is

minimum at a particular ratio of debt and equity, and the firm’s value is maximum.

4. Modigliani and Miller Approach (MM Approach)

It is a capital structure theory named after Franco Modigliani and Merton Miller. MM

theory proposed two propositions.

Proposition I: It says that the capital structure is irrelevant to the value of a firm. The value

of two identical firms would remain the same, and value would not affect the choice of

finance adopted to finance the assets. The value of a firm is dependent on the expected

future earnings. It is when there are no taxes.

Proposition II: It says that the financial leverage boosts the value of a firm and reduces

WACC. It is when tax information is available.

The approaches of capital structures discuss the effect of capital structures on the value of the

firms. All the approaches in the following section discuss whether the capital structure makes

any impact on the firm’s value or not.

1. Net Income Approach

Durand suggested this approach, and he favored the financial leverage decision. According

to him, a change in financial leverage would lead to a change in the cost of capital. In short,

if the ratio of debt in the capital structure increases, the weighted average cost of capital

decreases, and hence the value of the firm increases.

2. Net Operating Income Approach

Durand also provides this approach. It is the opposite of the Net Income Approach if there

are no taxes. This approach says that the weighted average cost of capital remains constant.

It believes in the fact that the market analyses a firm as a whole and discounts at a particular

rate that has no relation to the debt-equity ratio. If tax information is given, it recommends

that WACC reduces with an increase in debt financing, and the firm’s value will start

increasing.

3. Traditional Approach

This approach does not define hard and fast facts, and it says that the cost of capital is a

function of the capital structure. The unique thing about this approach is that it believes in

an optimal capital structure. Optimal capital structure implies that the cost of capital is

minimum at a particular ratio of debt and equity, and the firm’s value is maximum.

4. Modigliani and Miller Approach (MM Approach)

It is a capital structure theory named after Franco Modigliani and Merton Miller. MM

theory proposed two propositions.

Proposition I: It says that the capital structure is irrelevant to the value of a firm. The value

of two identical firms would remain the same, and value would not affect the choice of

finance adopted to finance the assets. The value of a firm is dependent on the expected

future earnings. It is when there are no taxes.

Proposition II: It says that the financial leverage boosts the value of a firm and reduces

WACC. It is when tax information is available.

Factors affecting Decisions on Capital Structure (Previous Question)

1. Cost of Equity Capital

When the company decides to have more equity, it should keep in mind the cost of equity

capital. There’s a common erroneous conclusion that equity is free of any cost. But that’s not

true. Let’s not forget about dividends. If the owner is able to get, say, 40% of net income as

dividends, the cost of equity can easily exceed the cost of borrowed capital. Business

development is relied only on reinvesting profits into capital.

2. Cost of Debt

Of course, debt is not free either. Interest and fees paid to lenders form the cost of capital. The

less the cost, the more debt can be used. One advantage of debt is that interest paid is

deductible to calculate income tax. Therefore, the more debt is used, the less is the company’s

effective tax rate.

3. Floatation Costs

Issuing equity capital also isn’t possible without incurring additional floatation costs. These

costs include various fees related to underwriting, brokerage, and receiving regulatory

approval. Generally, the costs of issuing equity capital are more than that of issuing debt.

4. Financial Flexibility

All goes well for the companies when the consumers receive their products well. Problems

come during a downturn. Even during the slowdown, the firm needs to run and thus, needs

capital. But it becomes very difficult for a company to raise capital in bad times. Therefore,

irrespective of the booming business and economy, the business should always discount for

the bad times and do not stretch its capabilities too far.

5. Change in Control

When equity is received not from existing shareholders (owners), problems of change in

control can arise. Issuing new shares to the open market (i.e., in IPOs or FPOs) introduces new

shareholders who can have a significantly different understanding of how the company should

be run. And, if they have a large stake in the company, corporate conflicts can emerge. If the

current owners want to have ultimate control over operations and lack additional funds, issuing

equity to new shareholders can be inappropriate. Hence, debt is more suitable for financing in

such cases.

6. Regulatory Frameworks

Various regulatory frameworks often prescribe what proportion of equity a company should

have in its capital structure. For example, banks are heavily regulated by central banks.

1. Cost of Equity Capital

When the company decides to have more equity, it should keep in mind the cost of equity

capital. There’s a common erroneous conclusion that equity is free of any cost. But that’s not

true. Let’s not forget about dividends. If the owner is able to get, say, 40% of net income as

dividends, the cost of equity can easily exceed the cost of borrowed capital. Business

development is relied only on reinvesting profits into capital.

2. Cost of Debt

Of course, debt is not free either. Interest and fees paid to lenders form the cost of capital. The

less the cost, the more debt can be used. One advantage of debt is that interest paid is

deductible to calculate income tax. Therefore, the more debt is used, the less is the company’s

effective tax rate.

3. Floatation Costs

Issuing equity capital also isn’t possible without incurring additional floatation costs. These

costs include various fees related to underwriting, brokerage, and receiving regulatory

approval. Generally, the costs of issuing equity capital are more than that of issuing debt.

4. Financial Flexibility

All goes well for the companies when the consumers receive their products well. Problems

come during a downturn. Even during the slowdown, the firm needs to run and thus, needs

capital. But it becomes very difficult for a company to raise capital in bad times. Therefore,

irrespective of the booming business and economy, the business should always discount for

the bad times and do not stretch its capabilities too far.

5. Change in Control

When equity is received not from existing shareholders (owners), problems of change in

control can arise. Issuing new shares to the open market (i.e., in IPOs or FPOs) introduces new

shareholders who can have a significantly different understanding of how the company should

be run. And, if they have a large stake in the company, corporate conflicts can emerge. If the

current owners want to have ultimate control over operations and lack additional funds, issuing

equity to new shareholders can be inappropriate. Hence, debt is more suitable for financing in

such cases.

6. Regulatory Frameworks

Various regulatory frameworks often prescribe what proportion of equity a company should

have in its capital structure. For example, banks are heavily regulated by central banks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7. Nature of Business and Risk

There is a risk in every business. However, risk differs from company to company, industry

to industry, nature of product or service provided, etc. For instance, a company in the business

of utilities will have fewer seasonal fluctuations than a company in the fashion industry.

Therefore, a fashion retail company will usually focus more on the optimal debt ratio than a

utility company. A lower debt asset ratio would make investors feel better about the

company’s ability to meet responsibilities even in adverse situations.

8. Operating Cash Flow

Capital structure, to some extent, is also impacted by the fixed cost. If a company uses a very

high proportion of fixed cost in the total cost, it can amplify the variability in future earnings.

If the operating leverage is high, there are more chances of a business failure, and the company

could even go to the extent of bankruptcy.

Previous years questions

1. Why should financial managers choose the capital structure that maximizes the

value of the firm?

Answer:

The main object of any organization is wealth maximization and as a financial manager to

achieve the objective and to maximize shareholder wealth maximizing firms value is

important. Maximizing firm value also will maximize shareholder wealth and achieve the

organizational goal. Changes in capital structure benefit the stockholders if and only if the

value of the firm increases. And when firms value increases because of capital structure

change it reduces the cost of capital with low WACC. And when the cost of capital is low

it increases EPS and increases market demand of the share that ultimately results in

maximizations of share value and wealth maximization. we can say that managers should

choose the capital structure that they believe will have the highest firm value because this

capital structure will be most beneficial to the firm's stockholders and company goal. We

can put the effect in the following algorithm

• Increase in firms’ value results in

• Decrease in WACC results in

• Increase in EPS results in

• Increase in market demand results in

• Increase in share value

There is a risk in every business. However, risk differs from company to company, industry

to industry, nature of product or service provided, etc. For instance, a company in the business

of utilities will have fewer seasonal fluctuations than a company in the fashion industry.

Therefore, a fashion retail company will usually focus more on the optimal debt ratio than a

utility company. A lower debt asset ratio would make investors feel better about the

company’s ability to meet responsibilities even in adverse situations.

8. Operating Cash Flow

Capital structure, to some extent, is also impacted by the fixed cost. If a company uses a very

high proportion of fixed cost in the total cost, it can amplify the variability in future earnings.

If the operating leverage is high, there are more chances of a business failure, and the company

could even go to the extent of bankruptcy.

Previous years questions

1. Why should financial managers choose the capital structure that maximizes the

value of the firm?

Answer:

The main object of any organization is wealth maximization and as a financial manager to

achieve the objective and to maximize shareholder wealth maximizing firms value is

important. Maximizing firm value also will maximize shareholder wealth and achieve the

organizational goal. Changes in capital structure benefit the stockholders if and only if the

value of the firm increases. And when firms value increases because of capital structure

change it reduces the cost of capital with low WACC. And when the cost of capital is low

it increases EPS and increases market demand of the share that ultimately results in

maximizations of share value and wealth maximization. we can say that managers should

choose the capital structure that they believe will have the highest firm value because this

capital structure will be most beneficial to the firm's stockholders and company goal. We

can put the effect in the following algorithm

• Increase in firms’ value results in

• Decrease in WACC results in

• Increase in EPS results in

• Increase in market demand results in

• Increase in share value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Time interest earned ratio

Answer:

The times interest earned (TIE) ratio is a measure of a company's ability to meet its debt

obligations based on its current income. The formula for a company's TIE number is

earnings before (EBITDA) divided by the total interest payable on bonds and other debt.

The result is a number that shows how many times a company could cover its interest

charges with its pretax earnings.

3. Common size income statement

Answer:

A common-size income statement is an income statement in which each line item of a

traditional income statement is expressed as a percentage of total sales or revenue.

Common-size income statements provide a tool for analyzing a company’s historical

performance over multiple periods (quarters or years).

4. The interest tax shield

Answer:

The term “interest tax shield” refers to the reduced income taxes brought about by

deductions to taxable income from a company’s interest expense. For instance, there are

cases where mortgages may have an interest tax shield for buyers since the mortgage

interest is deductible against income such as mortgages may have an interest tax shield for

buyers since the mortgage interest is deductible against income. One of the main objectives

of companies is to reduce their tax liability as much as possible. Interest tax shields

encourage firms to finance projects with debt since the dividends paid to equity investors

are not deductible.

5. If the companies had objective of maximizing shareholders wealth, would people

overall tend to be better or worse?

Answer:

If all companies were to focus on maximizing shareholders' wealth, then society would be

better off. Most companies tend to focus on maximizing profits, which is a short-term goal.

When management is focused on profit maximization and cost minimization, it tends to

avoid projects that are not profitable and might avoid social responsibility. However, to

attain long-term sustainability, a company must forego short-term profits and engage in

corporate governance. Therefore, pursuing long-term shareholder wealth maximization

would benefit the company, the shareholders, and society at large. Besides wealth

maximization has some advantages over profit maximization these are as follows

Answer:

The times interest earned (TIE) ratio is a measure of a company's ability to meet its debt

obligations based on its current income. The formula for a company's TIE number is

earnings before (EBITDA) divided by the total interest payable on bonds and other debt.

The result is a number that shows how many times a company could cover its interest

charges with its pretax earnings.

3. Common size income statement

Answer:

A common-size income statement is an income statement in which each line item of a

traditional income statement is expressed as a percentage of total sales or revenue.

Common-size income statements provide a tool for analyzing a company’s historical

performance over multiple periods (quarters or years).

4. The interest tax shield

Answer:

The term “interest tax shield” refers to the reduced income taxes brought about by

deductions to taxable income from a company’s interest expense. For instance, there are

cases where mortgages may have an interest tax shield for buyers since the mortgage

interest is deductible against income such as mortgages may have an interest tax shield for

buyers since the mortgage interest is deductible against income. One of the main objectives

of companies is to reduce their tax liability as much as possible. Interest tax shields

encourage firms to finance projects with debt since the dividends paid to equity investors

are not deductible.

5. If the companies had objective of maximizing shareholders wealth, would people

overall tend to be better or worse?

Answer:

If all companies were to focus on maximizing shareholders' wealth, then society would be

better off. Most companies tend to focus on maximizing profits, which is a short-term goal.

When management is focused on profit maximization and cost minimization, it tends to

avoid projects that are not profitable and might avoid social responsibility. However, to

attain long-term sustainability, a company must forego short-term profits and engage in

corporate governance. Therefore, pursuing long-term shareholder wealth maximization

would benefit the company, the shareholders, and society at large. Besides wealth

maximization has some advantages over profit maximization these are as follows

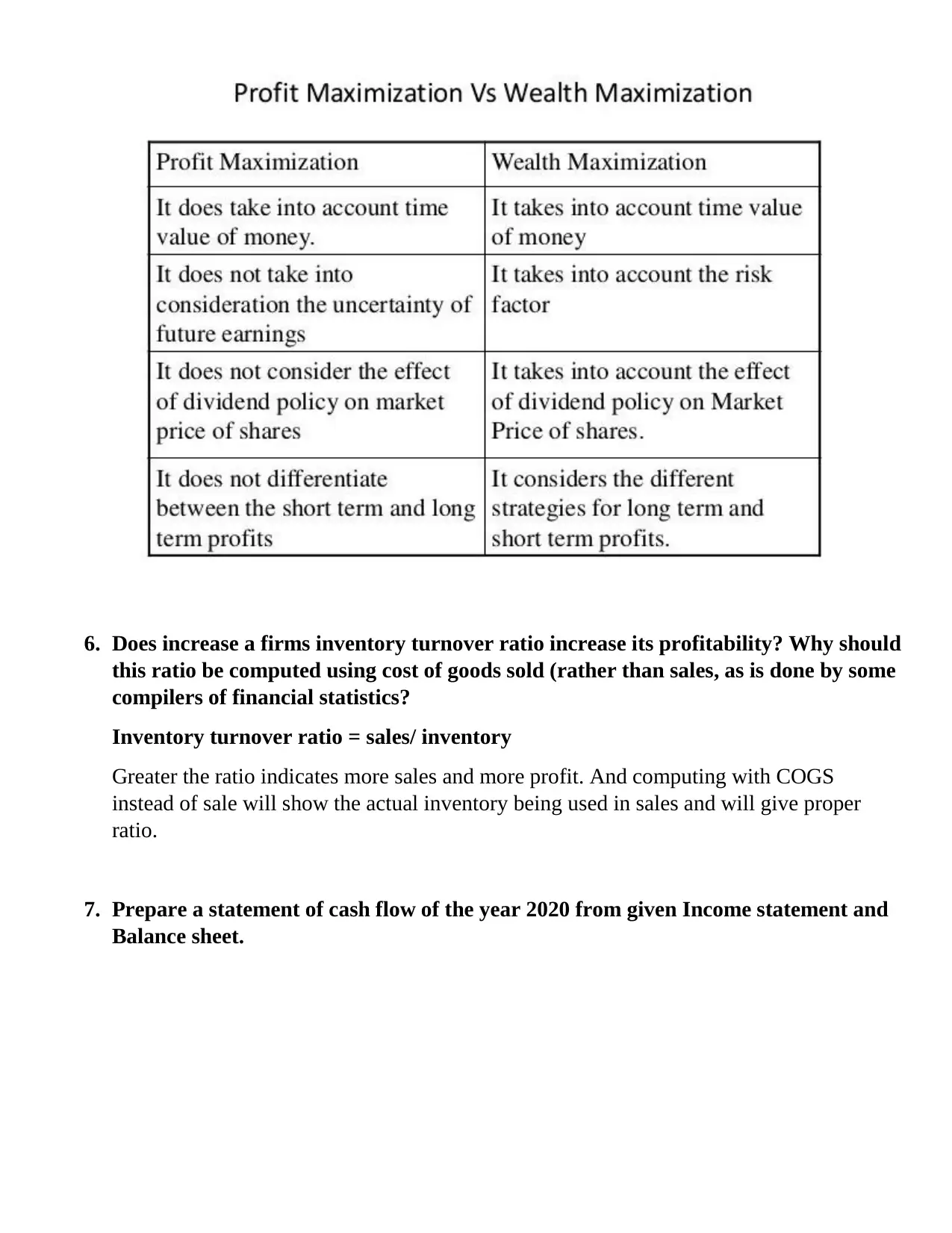

6. Does increase a firms inventory turnover ratio increase its profitability? Why should

this ratio be computed using cost of goods sold (rather than sales, as is done by some

compilers of financial statistics?

Inventory turnover ratio = sales/ inventory

Greater the ratio indicates more sales and more profit. And computing with COGS

instead of sale will show the actual inventory being used in sales and will give proper

ratio.

7. Prepare a statement of cash flow of the year 2020 from given Income statement and

Balance sheet.

this ratio be computed using cost of goods sold (rather than sales, as is done by some

compilers of financial statistics?

Inventory turnover ratio = sales/ inventory

Greater the ratio indicates more sales and more profit. And computing with COGS

instead of sale will show the actual inventory being used in sales and will give proper

ratio.

7. Prepare a statement of cash flow of the year 2020 from given Income statement and

Balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.