University Finance: Managing Financial Resources and Decisions Report

VerifiedAdded on 2019/12/03

|31

|6508

|25

Report

AI Summary

This report comprehensively examines financial resource management and decision-making. It begins by exploring various sources of finance for enterprises, including bank loans, equity, and debentures, along with their implications and suitability for different business types. The report then delves into the importance of financial planning, types of financial information required by managers (income statements, balance sheets, and cash flow statements), and explanatory notes on financial statements. The core of the report involves an in-depth analysis of a sales budget and cash flow forecast, calculation of breakeven points under different scenarios, and the application of project evaluation techniques like payback period, ARR, NPV, and IRR. Finally, the report concludes with a discussion of financial terms, formats of financial statements for different business structures (sole trader, company, partnership, and non-profit organizations), and a detailed ratio analysis to evaluate company performance.

MANAGING FINANCIAL

RESOURCES AND DECISIONS

RESOURCES AND DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance for enterprises ........................................................................................3

1.2 Implications of source of finance .........................................................................................3

1.3 Selection of source of finance ..............................................................................................5

TASK 2............................................................................................................................................5

2.2 Importance of financial planning..........................................................................................6

2.3 Types of financial information required by the managers....................................................6

2.4 Explanatory notes on financial statements with reference to finance and cost ....................7

TASK 3............................................................................................................................................7

3.1 Analysis of sales budget and cash flow forecast...................................................................7

3.2 Calculation of breakeven point under different options........................................................9

3.3 Project evaluation techniques..............................................................................................13

TASK 4..........................................................................................................................................15

4.1 Explanation on various terms and accounts........................................................................15

4.2 Format of financial statements for different business ........................................................16

..................................................................................................................................................16

4.3 Ratio analysis......................................................................................................................29

CONCLSUION .............................................................................................................................30

REFERECNES..............................................................................................................................31

INDEX OF TABLES

Table 1: Implications of sources of finance.....................................................................................4

Table 2: Sample income statement..................................................................................................8

Table 3: Sample balance sheet.........................................................................................................8

Table 4: Break even in case of increase in sales price...................................................................11

Table 5: Break even in case of increase or decrease in fixed cost.................................................11

Table 6: Break even in case of increase or decrease in material rates...........................................12

Table 7: Break even in case of increase or decrease in labor rates................................................13

Table 8: Calculation of payback period method............................................................................14

Table 9: Calculation of ARR.........................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance for enterprises ........................................................................................3

1.2 Implications of source of finance .........................................................................................3

1.3 Selection of source of finance ..............................................................................................5

TASK 2............................................................................................................................................5

2.2 Importance of financial planning..........................................................................................6

2.3 Types of financial information required by the managers....................................................6

2.4 Explanatory notes on financial statements with reference to finance and cost ....................7

TASK 3............................................................................................................................................7

3.1 Analysis of sales budget and cash flow forecast...................................................................7

3.2 Calculation of breakeven point under different options........................................................9

3.3 Project evaluation techniques..............................................................................................13

TASK 4..........................................................................................................................................15

4.1 Explanation on various terms and accounts........................................................................15

4.2 Format of financial statements for different business ........................................................16

..................................................................................................................................................16

4.3 Ratio analysis......................................................................................................................29

CONCLSUION .............................................................................................................................30

REFERECNES..............................................................................................................................31

INDEX OF TABLES

Table 1: Implications of sources of finance.....................................................................................4

Table 2: Sample income statement..................................................................................................8

Table 3: Sample balance sheet.........................................................................................................8

Table 4: Break even in case of increase in sales price...................................................................11

Table 5: Break even in case of increase or decrease in fixed cost.................................................11

Table 6: Break even in case of increase or decrease in material rates...........................................12

Table 7: Break even in case of increase or decrease in labor rates................................................13

Table 8: Calculation of payback period method............................................................................14

Table 9: Calculation of ARR.........................................................................................................14

Table 10: Calculation of NPV........................................................................................................15

Table 11: Calculation of IRR.........................................................................................................15

Table 12: Ratio analysis.................................................................................................................31

ILLUSTRATION INDEX

Illustration 1: Sole trader income statement..................................................................................17

Illustration 2: Balance sheet of sole trader.....................................................................................18

Illustration 3: Cash flow statement of sole trader..........................................................................19

Illustration 4: Income statement of company.................................................................................22

Illustration 5: Balance sheet of company.......................................................................................23

Illustration 6: Cash flow statement of company............................................................................24

Illustration 7: Income statement of partnership.............................................................................25

Illustration 8: Balance sheet of partnership...................................................................................26

Illustration 9: Cash flow statement for partnership........................................................................27

Illustration 10: Income statement of nonprofit organizations........................................................29

Illustration 11: Balance sheet of nonprofit organizations..............................................................30

Table 11: Calculation of IRR.........................................................................................................15

Table 12: Ratio analysis.................................................................................................................31

ILLUSTRATION INDEX

Illustration 1: Sole trader income statement..................................................................................17

Illustration 2: Balance sheet of sole trader.....................................................................................18

Illustration 3: Cash flow statement of sole trader..........................................................................19

Illustration 4: Income statement of company.................................................................................22

Illustration 5: Balance sheet of company.......................................................................................23

Illustration 6: Cash flow statement of company............................................................................24

Illustration 7: Income statement of partnership.............................................................................25

Illustration 8: Balance sheet of partnership...................................................................................26

Illustration 9: Cash flow statement for partnership........................................................................27

Illustration 10: Income statement of nonprofit organizations........................................................29

Illustration 11: Balance sheet of nonprofit organizations..............................................................30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance plays a vital role in growth of an organization. Thus, it is necessary to look after

various issues related to the finance. In respect to this in report sources of finance are described

and along with this their suitability to business requirements is also defined. At the middle part

of the report, project evaluation techniques are applied and their results are interpreted in proper

manner. Along with this breaks even analysis is also done on the available options and their

interpretation is also done in proper manner. At the end of the report, ratio analysis is done and

company performance is evaluated from various points.

TASK 1

1.1 Sources of finance for enterprises

New and small in size Bank loan- Under this mode of finance loan is taken from banks at fixed or floating

interest rate. Business firms must take a loan at the fixed interest rate and must also make

sure that they are taking an amount of loan that is match to their current financial

condition. Bank overdraft- In order to finance working capital requirements firm can take use a

bank overdraft facility. In return firm will need to pay interest on same (Bougheas, Mizen

and Yalcin, 2006).

Old and large in size Equity- In this mode of finance firm will issue shares by bringing IPO of FPO. Under this

individuals and institution will give capital to the company and will get ownership on

same. At the end of the year firm pay dividend to the shareholders due to their ownership

in the company.

Debentures- It is an acknowledgment of debt taken by the company. In this mode of

finance firm receive debt from general public and in return it pay interest to the debenture

holders (Abor, 2005).

1.2 Implications of source of finance

Table 1: Implications of sources of finance

Advantages Disadvantages Legal Cost

Finance plays a vital role in growth of an organization. Thus, it is necessary to look after

various issues related to the finance. In respect to this in report sources of finance are described

and along with this their suitability to business requirements is also defined. At the middle part

of the report, project evaluation techniques are applied and their results are interpreted in proper

manner. Along with this breaks even analysis is also done on the available options and their

interpretation is also done in proper manner. At the end of the report, ratio analysis is done and

company performance is evaluated from various points.

TASK 1

1.1 Sources of finance for enterprises

New and small in size Bank loan- Under this mode of finance loan is taken from banks at fixed or floating

interest rate. Business firms must take a loan at the fixed interest rate and must also make

sure that they are taking an amount of loan that is match to their current financial

condition. Bank overdraft- In order to finance working capital requirements firm can take use a

bank overdraft facility. In return firm will need to pay interest on same (Bougheas, Mizen

and Yalcin, 2006).

Old and large in size Equity- In this mode of finance firm will issue shares by bringing IPO of FPO. Under this

individuals and institution will give capital to the company and will get ownership on

same. At the end of the year firm pay dividend to the shareholders due to their ownership

in the company.

Debentures- It is an acknowledgment of debt taken by the company. In this mode of

finance firm receive debt from general public and in return it pay interest to the debenture

holders (Abor, 2005).

1.2 Implications of source of finance

Table 1: Implications of sources of finance

Advantages Disadvantages Legal Cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

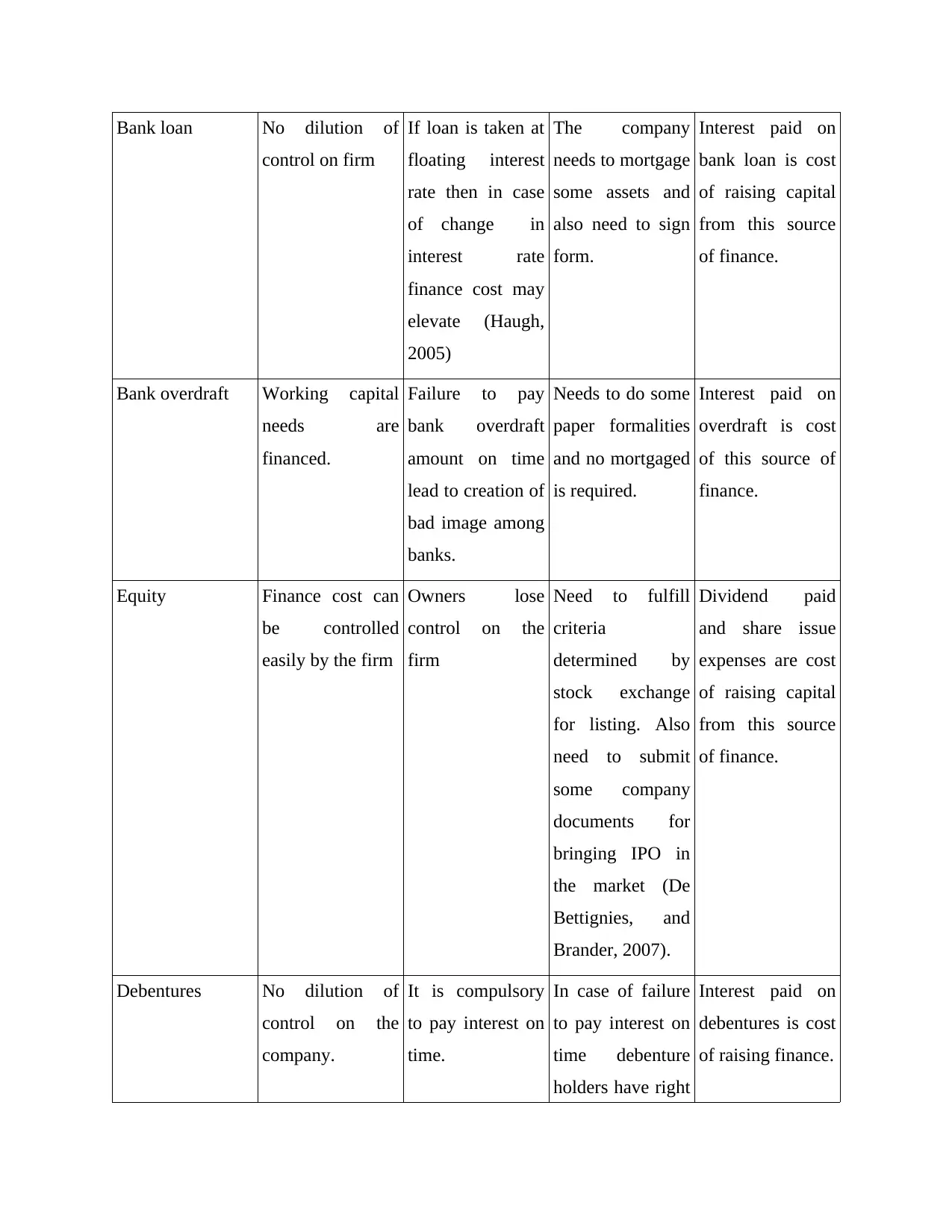

Bank loan No dilution of

control on firm

If loan is taken at

floating interest

rate then in case

of change in

interest rate

finance cost may

elevate (Haugh,

2005)

The company

needs to mortgage

some assets and

also need to sign

form.

Interest paid on

bank loan is cost

of raising capital

from this source

of finance.

Bank overdraft Working capital

needs are

financed.

Failure to pay

bank overdraft

amount on time

lead to creation of

bad image among

banks.

Needs to do some

paper formalities

and no mortgaged

is required.

Interest paid on

overdraft is cost

of this source of

finance.

Equity Finance cost can

be controlled

easily by the firm

Owners lose

control on the

firm

Need to fulfill

criteria

determined by

stock exchange

for listing. Also

need to submit

some company

documents for

bringing IPO in

the market (De

Bettignies, and

Brander, 2007).

Dividend paid

and share issue

expenses are cost

of raising capital

from this source

of finance.

Debentures No dilution of

control on the

company.

It is compulsory

to pay interest on

time.

In case of failure

to pay interest on

time debenture

holders have right

Interest paid on

debentures is cost

of raising finance.

control on firm

If loan is taken at

floating interest

rate then in case

of change in

interest rate

finance cost may

elevate (Haugh,

2005)

The company

needs to mortgage

some assets and

also need to sign

form.

Interest paid on

bank loan is cost

of raising capital

from this source

of finance.

Bank overdraft Working capital

needs are

financed.

Failure to pay

bank overdraft

amount on time

lead to creation of

bad image among

banks.

Needs to do some

paper formalities

and no mortgaged

is required.

Interest paid on

overdraft is cost

of this source of

finance.

Equity Finance cost can

be controlled

easily by the firm

Owners lose

control on the

firm

Need to fulfill

criteria

determined by

stock exchange

for listing. Also

need to submit

some company

documents for

bringing IPO in

the market (De

Bettignies, and

Brander, 2007).

Dividend paid

and share issue

expenses are cost

of raising capital

from this source

of finance.

Debentures No dilution of

control on the

company.

It is compulsory

to pay interest on

time.

In case of failure

to pay interest on

time debenture

holders have right

Interest paid on

debentures is cost

of raising finance.

to sue on the

company

1.3 Selection of source of finance

New business

In this case bank loan will be available to the new businesses because it is not in position

that it can raise capital from equity of venture capitalists. In case of bank loan debt must be taken

at fixed interest rate so that even interest rates get changed firm finance cost remains same.

Large business

In case of large sized firm equity can be used as a source of finance. Because in this

source of finance there will be no fixed finance cost (O’donnell, et.al, 2008). In other words, firm

will be in position to make adjustment in the finance cost in terms of dividend rate and non

dividend payment in specific fiscal year.

Small group of people

Small group of people can join hands to acquire a single company and they can use bank

loan to finance their requirements (Ageba and Amha, 2006). Since, they altogether are eligible to

raise capital form equity. In sane they as a unit cannot issue debentures and due to this reason

bank loan is appropriate for them.

TASK 2

2.1 Cost of different source of finance Bank loan- Interest paid on bank loan are cost of this source of finance. This cost can be

static or flexible. If loan is taken at floating interest rate then cost will be flexible. In

same way of loan taken at fixed rate then it will be said to be static in nature. It is highly

recommend to the firm that loan must be taken at fixed interest rate so that no change

takes place in finance cost of the firm (Allen, F., Qian and Qian, 2005). Bank overdraft- In this case also interest is charged by the bank for the loan taken by the

firm from them. This cost is fixed in nature. Equity- Dividend paid to the shareholders is a cost of raising capital from this source of

finance. It is not necessary to pay dividend every year. Even company earns profit it may

company

1.3 Selection of source of finance

New business

In this case bank loan will be available to the new businesses because it is not in position

that it can raise capital from equity of venture capitalists. In case of bank loan debt must be taken

at fixed interest rate so that even interest rates get changed firm finance cost remains same.

Large business

In case of large sized firm equity can be used as a source of finance. Because in this

source of finance there will be no fixed finance cost (O’donnell, et.al, 2008). In other words, firm

will be in position to make adjustment in the finance cost in terms of dividend rate and non

dividend payment in specific fiscal year.

Small group of people

Small group of people can join hands to acquire a single company and they can use bank

loan to finance their requirements (Ageba and Amha, 2006). Since, they altogether are eligible to

raise capital form equity. In sane they as a unit cannot issue debentures and due to this reason

bank loan is appropriate for them.

TASK 2

2.1 Cost of different source of finance Bank loan- Interest paid on bank loan are cost of this source of finance. This cost can be

static or flexible. If loan is taken at floating interest rate then cost will be flexible. In

same way of loan taken at fixed rate then it will be said to be static in nature. It is highly

recommend to the firm that loan must be taken at fixed interest rate so that no change

takes place in finance cost of the firm (Allen, F., Qian and Qian, 2005). Bank overdraft- In this case also interest is charged by the bank for the loan taken by the

firm from them. This cost is fixed in nature. Equity- Dividend paid to the shareholders is a cost of raising capital from this source of

finance. It is not necessary to pay dividend every year. Even company earns profit it may

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

deny from paying dividend to the shareholders. Hence, finance cost is adjustable in case

of equity.

Debentures- In case of this source of finance also interest is paid by the firm to the

debenture holders. It is fixed finance cost and cannot be altered like can be done in case

of bank loan (Abor and Biekpe, 2006). In case of downturn in economy interest payment

may create heavy burden on the firm.

2.2 Importance of financial planning

Financial planning has a great importance for the business because money is a resource

that is limited available to the firm. On other hand, firm perform lots of activities that required

finance. Hence, this makes it inevitable for the firm to make prudent use of the finance. There are

various categories of activities for which finance is required like investment and finance

activities. In these activities there are many sub activities (Corsatea, Giaccaria. and Arántegui,

2014). By preparing a finance plan firm determine from where it will arrange finance and way in

which it will use funds in all these sub activities; so that they can be performed easily without

any problem. Hence, it can be said that by making this plan funds are allocated among several

activities in legitimate manner and make best possible use of this scarce resource.

2.3 Types of financial information required by the managers

Types of financial information that are required for decision making purpose are as

follows. Income statement- In this statement all information about income and expenses is made

available. By reviewing these statement managers comes to know about expenses where

they make extravagance. Hence, it can be said that this statement helps managers in

identifying areas where they are making a mistake and needs to take immediate action to

rectify mistake (Huggins, 2008). Balance sheet- By analyzing balance sheet managers came to know about the financial

position of the company. By doing this managers also identify various areas where they

gives fabulous and poor performance. Hence, managers form a tactics to convert their

weakness in to strength. In this way, balance sheet gets improved for the next financial

year.

Cash flow statement- This statement indicate the areas from which cash inflow happen

and domains where these cash flows are incurred by the business (Hyman, 2013). Thus,

of equity.

Debentures- In case of this source of finance also interest is paid by the firm to the

debenture holders. It is fixed finance cost and cannot be altered like can be done in case

of bank loan (Abor and Biekpe, 2006). In case of downturn in economy interest payment

may create heavy burden on the firm.

2.2 Importance of financial planning

Financial planning has a great importance for the business because money is a resource

that is limited available to the firm. On other hand, firm perform lots of activities that required

finance. Hence, this makes it inevitable for the firm to make prudent use of the finance. There are

various categories of activities for which finance is required like investment and finance

activities. In these activities there are many sub activities (Corsatea, Giaccaria. and Arántegui,

2014). By preparing a finance plan firm determine from where it will arrange finance and way in

which it will use funds in all these sub activities; so that they can be performed easily without

any problem. Hence, it can be said that by making this plan funds are allocated among several

activities in legitimate manner and make best possible use of this scarce resource.

2.3 Types of financial information required by the managers

Types of financial information that are required for decision making purpose are as

follows. Income statement- In this statement all information about income and expenses is made

available. By reviewing these statement managers comes to know about expenses where

they make extravagance. Hence, it can be said that this statement helps managers in

identifying areas where they are making a mistake and needs to take immediate action to

rectify mistake (Huggins, 2008). Balance sheet- By analyzing balance sheet managers came to know about the financial

position of the company. By doing this managers also identify various areas where they

gives fabulous and poor performance. Hence, managers form a tactics to convert their

weakness in to strength. In this way, balance sheet gets improved for the next financial

year.

Cash flow statement- This statement indicate the areas from which cash inflow happen

and domains where these cash flows are incurred by the business (Hyman, 2013). Thus,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analysis of this statement helps firm in formulating its cash management strategy for the

next financial year.

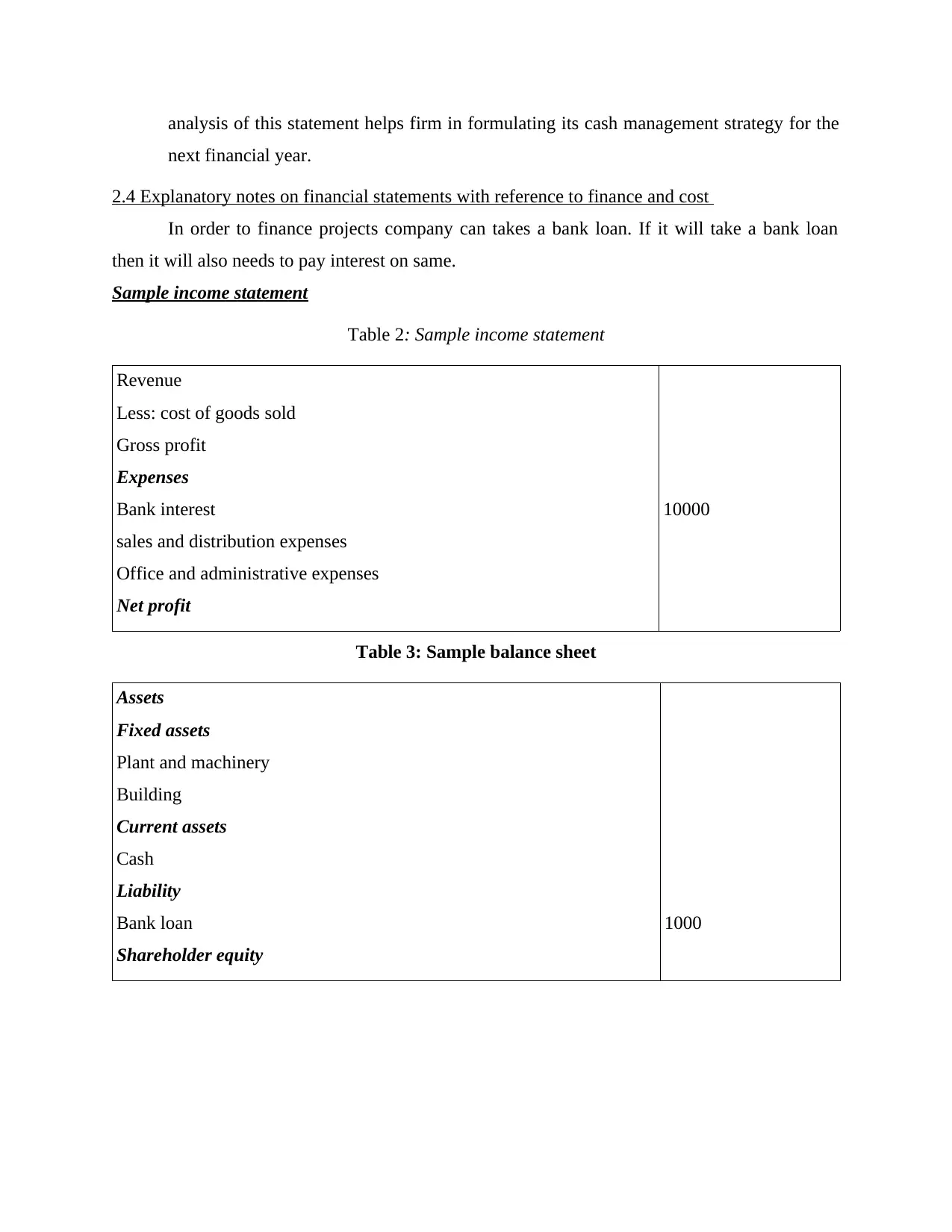

2.4 Explanatory notes on financial statements with reference to finance and cost

In order to finance projects company can takes a bank loan. If it will take a bank loan

then it will also needs to pay interest on same.

Sample income statement

Table 2: Sample income statement

Revenue

Less: cost of goods sold

Gross profit

Expenses

Bank interest

sales and distribution expenses

Office and administrative expenses

Net profit

10000

Table 3: Sample balance sheet

Assets

Fixed assets

Plant and machinery

Building

Current assets

Cash

Liability

Bank loan

Shareholder equity

1000

next financial year.

2.4 Explanatory notes on financial statements with reference to finance and cost

In order to finance projects company can takes a bank loan. If it will take a bank loan

then it will also needs to pay interest on same.

Sample income statement

Table 2: Sample income statement

Revenue

Less: cost of goods sold

Gross profit

Expenses

Bank interest

sales and distribution expenses

Office and administrative expenses

Net profit

10000

Table 3: Sample balance sheet

Assets

Fixed assets

Plant and machinery

Building

Current assets

Cash

Liability

Bank loan

Shareholder equity

1000

TASK 3

3.1 Analysis of sales budget and cash flow forecast

To

The directors of ABC manufacturing ltd

Date: 7th December 2015

Following are reasons for fluctuation recommendations for sales and cash flow forecast.

Sales budget- In case of sales budget of ABC manufacturing ltd it has been observed that sales

of the firm is increasing continuously. But it failed to beat expected level of sales that is

revealed by the budget figures. This is a big problem for an organization that it is not able to

achieve expected level of sales every month. Moreover, gap between actual and sales figures

also increase. This second big problem for ABC manufacturing ltd. The main reason behind

increase in gap is that business environment changed suddenly. Due to this reason management

is not able to make accurate anticipation of sales for upcoming month. Strong currency

exchange rate and poor economic conditions of foreign nations is big reason behind slow

growth rate of sales. In order to reduce cash deficit firm needs to abstain from making large

amount of credit sales (El-Gamal, 2006). In case of default of foreign partners burden on the

firm will increase. On other hand, firm need to make efforts to recover debt amount from

debtors. This will increase cash inflow and cash deficit will reduce to large extent. The issue is

that firm is facing problems in making accurate anticipation. In order solve this problem

managers need to analyze economic data and need to correlate demand for the specific product

with mentioned data. By doing this with movement in values of economic data company will

be able to predict likely movement in demand for their product in upcoming month.

Cash flow forecast

From data of cash flow forecast it can be seen that sales of the firm is fluctuating and

mostly is in range of 250 to 300. Sometimes it crosses these limits above or below. Fluctuation

rate is also very high. Same thing is observed in case of deficit and surplus. Lack of consistency

in sales and surplus/ deficit balance is a major problem. This happens because firm failed to

make accurate prediction. Secondly, it does not make any sort of change in its expenses. Even

sales were not in line to expectation from the month of January to June then also its expenses

remain static. Due to this no adjustment happens in cash surplus/ deficit amount and they keep

3.1 Analysis of sales budget and cash flow forecast

To

The directors of ABC manufacturing ltd

Date: 7th December 2015

Following are reasons for fluctuation recommendations for sales and cash flow forecast.

Sales budget- In case of sales budget of ABC manufacturing ltd it has been observed that sales

of the firm is increasing continuously. But it failed to beat expected level of sales that is

revealed by the budget figures. This is a big problem for an organization that it is not able to

achieve expected level of sales every month. Moreover, gap between actual and sales figures

also increase. This second big problem for ABC manufacturing ltd. The main reason behind

increase in gap is that business environment changed suddenly. Due to this reason management

is not able to make accurate anticipation of sales for upcoming month. Strong currency

exchange rate and poor economic conditions of foreign nations is big reason behind slow

growth rate of sales. In order to reduce cash deficit firm needs to abstain from making large

amount of credit sales (El-Gamal, 2006). In case of default of foreign partners burden on the

firm will increase. On other hand, firm need to make efforts to recover debt amount from

debtors. This will increase cash inflow and cash deficit will reduce to large extent. The issue is

that firm is facing problems in making accurate anticipation. In order solve this problem

managers need to analyze economic data and need to correlate demand for the specific product

with mentioned data. By doing this with movement in values of economic data company will

be able to predict likely movement in demand for their product in upcoming month.

Cash flow forecast

From data of cash flow forecast it can be seen that sales of the firm is fluctuating and

mostly is in range of 250 to 300. Sometimes it crosses these limits above or below. Fluctuation

rate is also very high. Same thing is observed in case of deficit and surplus. Lack of consistency

in sales and surplus/ deficit balance is a major problem. This happens because firm failed to

make accurate prediction. Secondly, it does not make any sort of change in its expenses. Even

sales were not in line to expectation from the month of January to June then also its expenses

remain static. Due to this no adjustment happens in cash surplus/ deficit amount and they keep

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on fluctuating sharply (Marlow, Patton, 2005). Thus, it is recommended that firm must curtail

its advertisement and other expenses. By doing this fluctuation in cash flows can be reduced to

large extent.

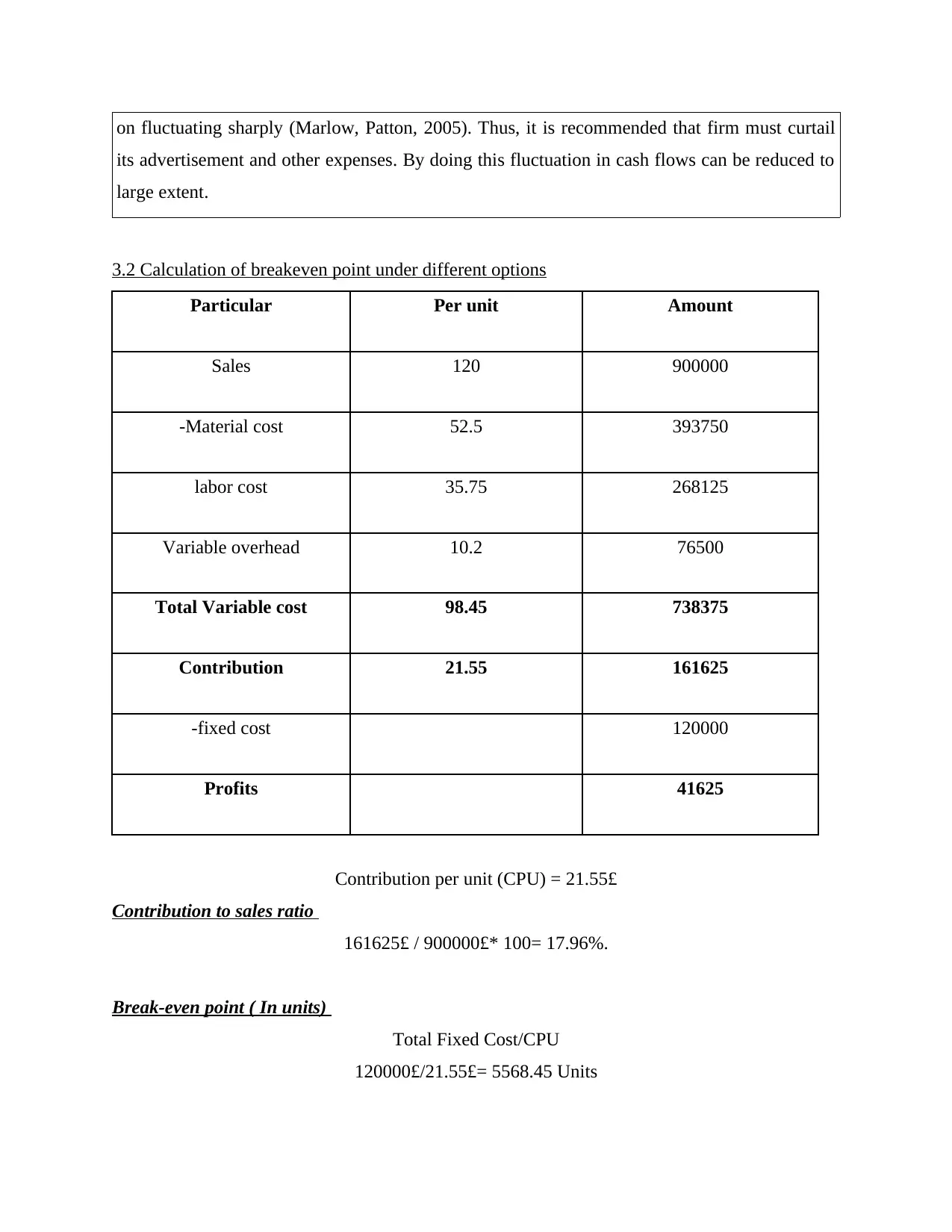

3.2 Calculation of breakeven point under different options

Particular Per unit Amount

Sales 120 900000

-Material cost 52.5 393750

labor cost 35.75 268125

Variable overhead 10.2 76500

Total Variable cost 98.45 738375

Contribution 21.55 161625

-fixed cost 120000

Profits 41625

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio

161625£ / 900000£* 100= 17.96%.

Break-even point ( In units)

Total Fixed Cost/CPU

120000£/21.55£= 5568.45 Units

its advertisement and other expenses. By doing this fluctuation in cash flows can be reduced to

large extent.

3.2 Calculation of breakeven point under different options

Particular Per unit Amount

Sales 120 900000

-Material cost 52.5 393750

labor cost 35.75 268125

Variable overhead 10.2 76500

Total Variable cost 98.45 738375

Contribution 21.55 161625

-fixed cost 120000

Profits 41625

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio

161625£ / 900000£* 100= 17.96%.

Break-even point ( In units)

Total Fixed Cost/CPU

120000£/21.55£= 5568.45 Units

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

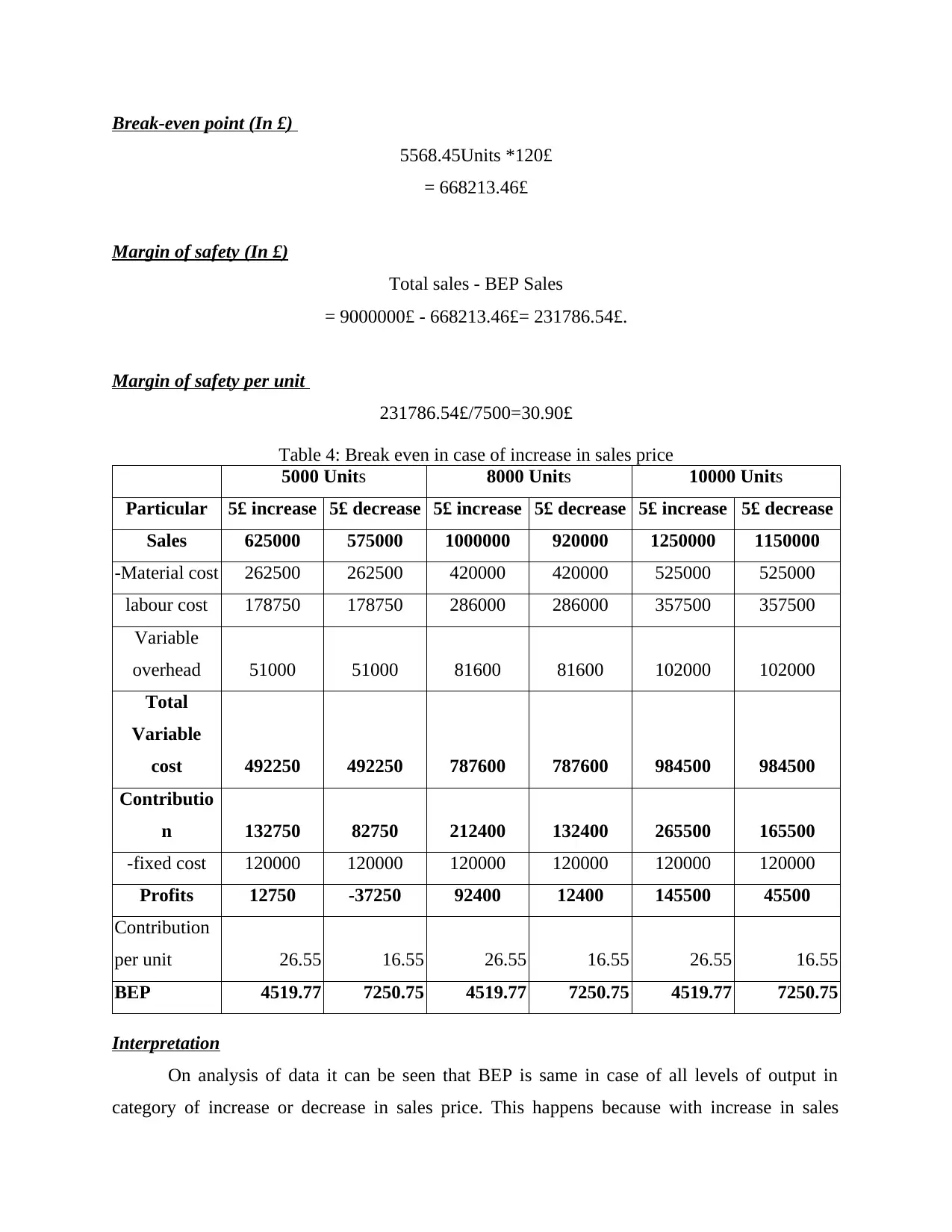

Break-even point (In £)

5568.45Units *120£

= 668213.46£

Margin of safety (In £)

Total sales - BEP Sales

= 9000000£ - 668213.46£= 231786.54£.

Margin of safety per unit

231786.54£/7500=30.90£

Table 4: Break even in case of increase in sales price

5000 Units 8000 Units 10000 Units

Particular 5£ increase 5£ decrease 5£ increase 5£ decrease 5£ increase 5£ decrease

Sales 625000 575000 1000000 920000 1250000 1150000

-Material cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

cost 492250 492250 787600 787600 984500 984500

Contributio

n 132750 82750 212400 132400 265500 165500

-fixed cost 120000 120000 120000 120000 120000 120000

Profits 12750 -37250 92400 12400 145500 45500

Contribution

per unit 26.55 16.55 26.55 16.55 26.55 16.55

BEP 4519.77 7250.75 4519.77 7250.75 4519.77 7250.75

Interpretation

On analysis of data it can be seen that BEP is same in case of all levels of output in

category of increase or decrease in sales price. This happens because with increase in sales

5568.45Units *120£

= 668213.46£

Margin of safety (In £)

Total sales - BEP Sales

= 9000000£ - 668213.46£= 231786.54£.

Margin of safety per unit

231786.54£/7500=30.90£

Table 4: Break even in case of increase in sales price

5000 Units 8000 Units 10000 Units

Particular 5£ increase 5£ decrease 5£ increase 5£ decrease 5£ increase 5£ decrease

Sales 625000 575000 1000000 920000 1250000 1150000

-Material cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

cost 492250 492250 787600 787600 984500 984500

Contributio

n 132750 82750 212400 132400 265500 165500

-fixed cost 120000 120000 120000 120000 120000 120000

Profits 12750 -37250 92400 12400 145500 45500

Contribution

per unit 26.55 16.55 26.55 16.55 26.55 16.55

BEP 4519.77 7250.75 4519.77 7250.75 4519.77 7250.75

Interpretation

On analysis of data it can be seen that BEP is same in case of all levels of output in

category of increase or decrease in sales price. This happens because with increase in sales

variable cost also increase at same rate. Due to this reason contribution per unit is same for all

level of output but very with change in sales price. It will be better to increase sales price if sales

are increase because in this case cost are recovered by selling less units.

Table 5: Break even in case of increase or decrease in fixed cost

5000 Units 8000 Units 10000 Units

Particular

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

Sales 600000 600000 960000 960000 1200000 1200000

-Material cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

cost 492250 492250 787600 787600 984500 984500

Contributio

n 107750 107750 172400 172400 215500 215500

-fixed cost 125000 115000 125000 115000 125000 115000

Profits -17250 -7250 47400 57400 90500 100500

CPU 21.55 21.55 21.55 21.55 21.55 21.55

BEP 5800.46 5336.42 5800.46 5336.42 5800.46 5336.43

Interpretation

On the table it can be seen that fixed cost is changed on every level of output. Even

though BEP is same on all level of output but very in case of increase and decrease in fixed cost.

This happens because no change is taken place in contribution in all level of output. It will be

better to reduce fixed cost because by doing this firm needs to produce fewer units to cover its

production cost.

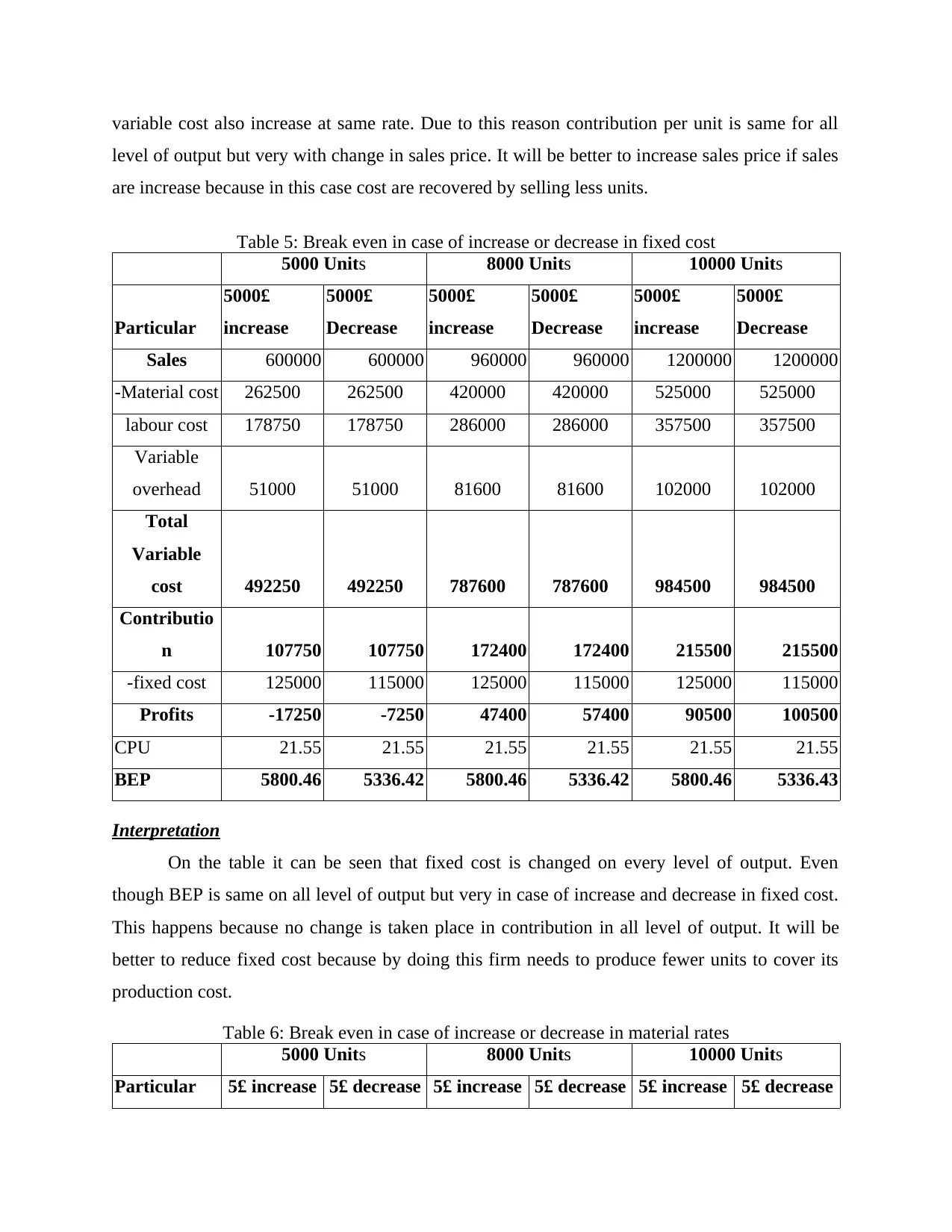

Table 6: Break even in case of increase or decrease in material rates

5000 Units 8000 Units 10000 Units

Particular 5£ increase 5£ decrease 5£ increase 5£ decrease 5£ increase 5£ decrease

level of output but very with change in sales price. It will be better to increase sales price if sales

are increase because in this case cost are recovered by selling less units.

Table 5: Break even in case of increase or decrease in fixed cost

5000 Units 8000 Units 10000 Units

Particular

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

Sales 600000 600000 960000 960000 1200000 1200000

-Material cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

cost 492250 492250 787600 787600 984500 984500

Contributio

n 107750 107750 172400 172400 215500 215500

-fixed cost 125000 115000 125000 115000 125000 115000

Profits -17250 -7250 47400 57400 90500 100500

CPU 21.55 21.55 21.55 21.55 21.55 21.55

BEP 5800.46 5336.42 5800.46 5336.42 5800.46 5336.43

Interpretation

On the table it can be seen that fixed cost is changed on every level of output. Even

though BEP is same on all level of output but very in case of increase and decrease in fixed cost.

This happens because no change is taken place in contribution in all level of output. It will be

better to reduce fixed cost because by doing this firm needs to produce fewer units to cover its

production cost.

Table 6: Break even in case of increase or decrease in material rates

5000 Units 8000 Units 10000 Units

Particular 5£ increase 5£ decrease 5£ increase 5£ decrease 5£ increase 5£ decrease

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.