In-depth Financial Decision Making and Analysis of Roast Ltd

VerifiedAdded on 2023/01/12

|16

|4498

|73

Report

AI Summary

This report provides a financial decision-making analysis for Roast Ltd, a company supplying coffee to Starbucks. It begins with an industry review of the UK coffee house sector, highlighting its growth and key players. The report then delves into Roast Ltd's business performance, analyzing the statement of profit and loss, statement of financial position, and cash flow statement. Key financial ratios such as gross profit ratio, operating profit ratio, net income ratio, debt equity ratio, current ratio, and quick ratio are calculated and interpreted. The analysis reveals insights into the company's profitability, liquidity, and efficiency. Furthermore, the report examines investment appraisal methods and potential sources of finance for Roast Ltd. The operating cash cycle is calculated to assess the time required to convert raw materials into cash. The report concludes with an overall assessment of Roast Ltd's financial health and recommendations for improvement.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: Industry Review...............................................................................................................1

Top line review of current UK coffee house industry.................................................................1

PART 2: Business Performance Analysis.......................................................................................1

2.1 Statement of profit and loss...................................................................................................1

2.2 Statement of financial position..............................................................................................3

2.3 Cash Flow Statement.............................................................................................................5

Part 3: Sources of Finance and Investment Appraisal.....................................................................8

3.1 Investment appraisal..............................................................................................................8

3.2 Sources of Finance...............................................................................................................10

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: Industry Review...............................................................................................................1

Top line review of current UK coffee house industry.................................................................1

PART 2: Business Performance Analysis.......................................................................................1

2.1 Statement of profit and loss...................................................................................................1

2.2 Statement of financial position..............................................................................................3

2.3 Cash Flow Statement.............................................................................................................5

Part 3: Sources of Finance and Investment Appraisal.....................................................................8

3.1 Investment appraisal..............................................................................................................8

3.2 Sources of Finance...............................................................................................................10

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY

The concept of this paper details the financial decision-making process for the project.

The first such segment of the topic report examines various forms of financial reports, depending

on the finance firm's performance. In comparison to both the expense estimate, the second

portion of the relevant article includes various forms of methods involving accounting profit

cost, net present value, and payback date. The main discussion may be introduced to Starbucks

collective where they purchase from the limited company Roasted. Since the majority of their

statements have seen positive effects which states the good image of company.

PART 1: Industry Review

Top line review of current UK coffee house industry

It has already been established at current time that coffee sector in the UK is growing year to

year. The main explanation for market development is that consumers are growing increasingly

attached to beverages and snacks. UK's coffee shop sector is wide enough yet to add to the

growth of the country benefit of the entire. The following criteria should be listed in order to

evaluate the market analysis of it:

As per study, the coffee industry's gross GDP output for 2017 contributed to about 3.7

billion pounds (Current coffee house industry of United Kingdom, 2019).

This has been projected that the sector's sales would grow by 4.8 per cent over the

coming years and that the overall volume will be about 6.6 billion pounds.

The big resource opens to companies working in this field is to promote these coffee or

other drinks that are better tailored to fitness-friendly persons because they neglect milk

coffee.

There are many companies working in this sector. These would be Roast Ltd, Coffee

Republic. Starbucks, Costa Coffee, 2U Cafe, Muffin Split, Ritazza Caffee, Puccino's,

Nero Caffe etc.

PART 2: Business Performance Analysis

2.1 Statement of profit and loss

For the benefit of both reporting in the context primary, secondary, operational and non-

operating costs along with revenue, both corporate companies produce a report on an annual

1

The concept of this paper details the financial decision-making process for the project.

The first such segment of the topic report examines various forms of financial reports, depending

on the finance firm's performance. In comparison to both the expense estimate, the second

portion of the relevant article includes various forms of methods involving accounting profit

cost, net present value, and payback date. The main discussion may be introduced to Starbucks

collective where they purchase from the limited company Roasted. Since the majority of their

statements have seen positive effects which states the good image of company.

PART 1: Industry Review

Top line review of current UK coffee house industry

It has already been established at current time that coffee sector in the UK is growing year to

year. The main explanation for market development is that consumers are growing increasingly

attached to beverages and snacks. UK's coffee shop sector is wide enough yet to add to the

growth of the country benefit of the entire. The following criteria should be listed in order to

evaluate the market analysis of it:

As per study, the coffee industry's gross GDP output for 2017 contributed to about 3.7

billion pounds (Current coffee house industry of United Kingdom, 2019).

This has been projected that the sector's sales would grow by 4.8 per cent over the

coming years and that the overall volume will be about 6.6 billion pounds.

The big resource opens to companies working in this field is to promote these coffee or

other drinks that are better tailored to fitness-friendly persons because they neglect milk

coffee.

There are many companies working in this sector. These would be Roast Ltd, Coffee

Republic. Starbucks, Costa Coffee, 2U Cafe, Muffin Split, Ritazza Caffee, Puccino's,

Nero Caffe etc.

PART 2: Business Performance Analysis

2.1 Statement of profit and loss

For the benefit of both reporting in the context primary, secondary, operational and non-

operating costs along with revenue, both corporate companies produce a report on an annual

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

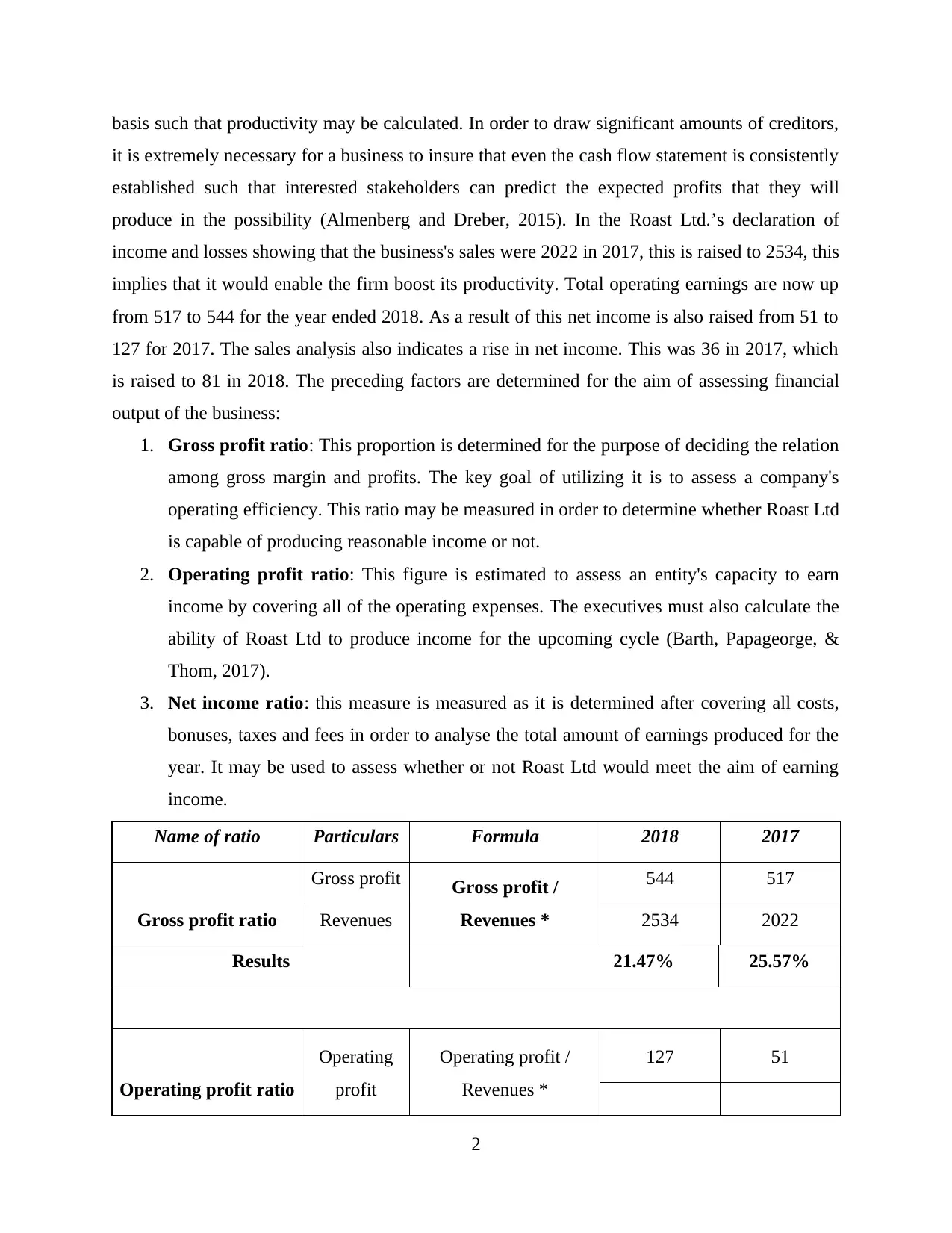

basis such that productivity may be calculated. In order to draw significant amounts of creditors,

it is extremely necessary for a business to insure that even the cash flow statement is consistently

established such that interested stakeholders can predict the expected profits that they will

produce in the possibility (Almenberg and Dreber, 2015). In the Roast Ltd.’s declaration of

income and losses showing that the business's sales were 2022 in 2017, this is raised to 2534, this

implies that it would enable the firm boost its productivity. Total operating earnings are now up

from 517 to 544 for the year ended 2018. As a result of this net income is also raised from 51 to

127 for 2017. The sales analysis also indicates a rise in net income. This was 36 in 2017, which

is raised to 81 in 2018. The preceding factors are determined for the aim of assessing financial

output of the business:

1. Gross profit ratio: This proportion is determined for the purpose of deciding the relation

among gross margin and profits. The key goal of utilizing it is to assess a company's

operating efficiency. This ratio may be measured in order to determine whether Roast Ltd

is capable of producing reasonable income or not.

2. Operating profit ratio: This figure is estimated to assess an entity's capacity to earn

income by covering all of the operating expenses. The executives must also calculate the

ability of Roast Ltd to produce income for the upcoming cycle (Barth, Papageorge, &

Thom, 2017).

3. Net income ratio: this measure is measured as it is determined after covering all costs,

bonuses, taxes and fees in order to analyse the total amount of earnings produced for the

year. It may be used to assess whether or not Roast Ltd would meet the aim of earning

income.

Name of ratio Particulars Formula 2018 2017

Gross profit ratio

Gross profit Gross profit /

Revenues *

544 517

Revenues 2534 2022

Results 21.47% 25.57%

Operating profit ratio

Operating

profit

Operating profit /

Revenues *

127 51

2

it is extremely necessary for a business to insure that even the cash flow statement is consistently

established such that interested stakeholders can predict the expected profits that they will

produce in the possibility (Almenberg and Dreber, 2015). In the Roast Ltd.’s declaration of

income and losses showing that the business's sales were 2022 in 2017, this is raised to 2534, this

implies that it would enable the firm boost its productivity. Total operating earnings are now up

from 517 to 544 for the year ended 2018. As a result of this net income is also raised from 51 to

127 for 2017. The sales analysis also indicates a rise in net income. This was 36 in 2017, which

is raised to 81 in 2018. The preceding factors are determined for the aim of assessing financial

output of the business:

1. Gross profit ratio: This proportion is determined for the purpose of deciding the relation

among gross margin and profits. The key goal of utilizing it is to assess a company's

operating efficiency. This ratio may be measured in order to determine whether Roast Ltd

is capable of producing reasonable income or not.

2. Operating profit ratio: This figure is estimated to assess an entity's capacity to earn

income by covering all of the operating expenses. The executives must also calculate the

ability of Roast Ltd to produce income for the upcoming cycle (Barth, Papageorge, &

Thom, 2017).

3. Net income ratio: this measure is measured as it is determined after covering all costs,

bonuses, taxes and fees in order to analyse the total amount of earnings produced for the

year. It may be used to assess whether or not Roast Ltd would meet the aim of earning

income.

Name of ratio Particulars Formula 2018 2017

Gross profit ratio

Gross profit Gross profit /

Revenues *

544 517

Revenues 2534 2022

Results 21.47% 25.57%

Operating profit ratio

Operating

profit

Operating profit /

Revenues *

127 51

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

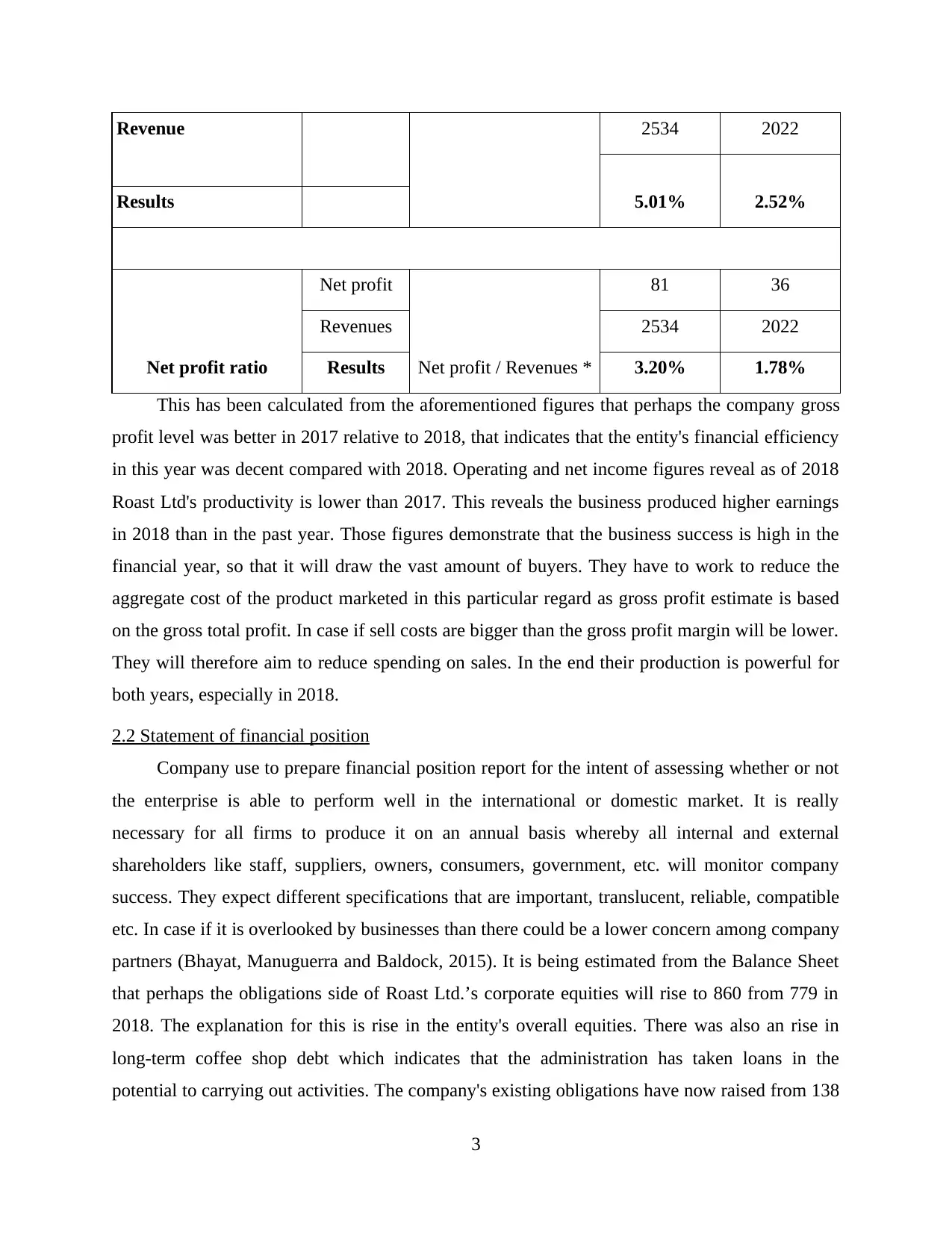

2534 2022Revenue

5.01% 2.52%Results

Net profit ratio

Net profit

Net profit / Revenues *

81 36

Revenues 2534 2022

Results 3.20% 1.78%

This has been calculated from the aforementioned figures that perhaps the company gross

profit level was better in 2017 relative to 2018, that indicates that the entity's financial efficiency

in this year was decent compared with 2018. Operating and net income figures reveal as of 2018

Roast Ltd's productivity is lower than 2017. This reveals the business produced higher earnings

in 2018 than in the past year. Those figures demonstrate that the business success is high in the

financial year, so that it will draw the vast amount of buyers. They have to work to reduce the

aggregate cost of the product marketed in this particular regard as gross profit estimate is based

on the gross total profit. In case if sell costs are bigger than the gross profit margin will be lower.

They will therefore aim to reduce spending on sales. In the end their production is powerful for

both years, especially in 2018.

2.2 Statement of financial position

Company use to prepare financial position report for the intent of assessing whether or not

the enterprise is able to perform well in the international or domestic market. It is really

necessary for all firms to produce it on an annual basis whereby all internal and external

shareholders like staff, suppliers, owners, consumers, government, etc. will monitor company

success. They expect different specifications that are important, translucent, reliable, compatible

etc. In case if it is overlooked by businesses than there could be a lower concern among company

partners (Bhayat, Manuguerra and Baldock, 2015). It is being estimated from the Balance Sheet

that perhaps the obligations side of Roast Ltd.’s corporate equities will rise to 860 from 779 in

2018. The explanation for this is rise in the entity's overall equities. There was also an rise in

long-term coffee shop debt which indicates that the administration has taken loans in the

potential to carrying out activities. The company's existing obligations have now raised from 138

3

5.01% 2.52%Results

Net profit ratio

Net profit

Net profit / Revenues *

81 36

Revenues 2534 2022

Results 3.20% 1.78%

This has been calculated from the aforementioned figures that perhaps the company gross

profit level was better in 2017 relative to 2018, that indicates that the entity's financial efficiency

in this year was decent compared with 2018. Operating and net income figures reveal as of 2018

Roast Ltd's productivity is lower than 2017. This reveals the business produced higher earnings

in 2018 than in the past year. Those figures demonstrate that the business success is high in the

financial year, so that it will draw the vast amount of buyers. They have to work to reduce the

aggregate cost of the product marketed in this particular regard as gross profit estimate is based

on the gross total profit. In case if sell costs are bigger than the gross profit margin will be lower.

They will therefore aim to reduce spending on sales. In the end their production is powerful for

both years, especially in 2018.

2.2 Statement of financial position

Company use to prepare financial position report for the intent of assessing whether or not

the enterprise is able to perform well in the international or domestic market. It is really

necessary for all firms to produce it on an annual basis whereby all internal and external

shareholders like staff, suppliers, owners, consumers, government, etc. will monitor company

success. They expect different specifications that are important, translucent, reliable, compatible

etc. In case if it is overlooked by businesses than there could be a lower concern among company

partners (Bhayat, Manuguerra and Baldock, 2015). It is being estimated from the Balance Sheet

that perhaps the obligations side of Roast Ltd.’s corporate equities will rise to 860 from 779 in

2018. The explanation for this is rise in the entity's overall equities. There was also an rise in

long-term coffee shop debt which indicates that the administration has taken loans in the

potential to carrying out activities. The company's existing obligations have now raised from 138

3

to 308. The reasons of this spike are bank overdraft and disposed payable exchange. The

inventory dimension indicates rising non-current investments, which implies the organization has

acquired additional properties, plants and facilities to better carry out operating operations.

Owing to an improvement in accounts receivable and stock levels, net assets are still growing in

the present year. In Roast Ltd.’s sense it is often measured for the intent of results measurement

corresponding ratios. All of them are defined as follows:

1. Debt equity ratio: This is among the main ratios used to calculate financial power. It

is important to utilize external obligations rather than internal assets for both

companies in order to boost the potential to produce better returns. This formula

should be determined in order to assess the very same capacity of Roast Ltd

(Chambers, Echenique and Saito, 2016).

2. Current ratio: This is a form of equity ratio that is determined to assess whether or

not an enterprise should be able to cover any of the short-term obligations with

existing assets throughout the year. This will be used to assess Roast Ltd liquidity

amount.

3. Quick ratio: In such a measure, existing core resources are taken for estimation

purposes in order to identify the capacity to satisfy short-term commitments with the

aid of capital and cash equivalents. This ratio will be determined in order to examine

whether Roast Ltd is capable to cover the liabilities from instant cash.

Calculation for important ratios is discussed underneath:

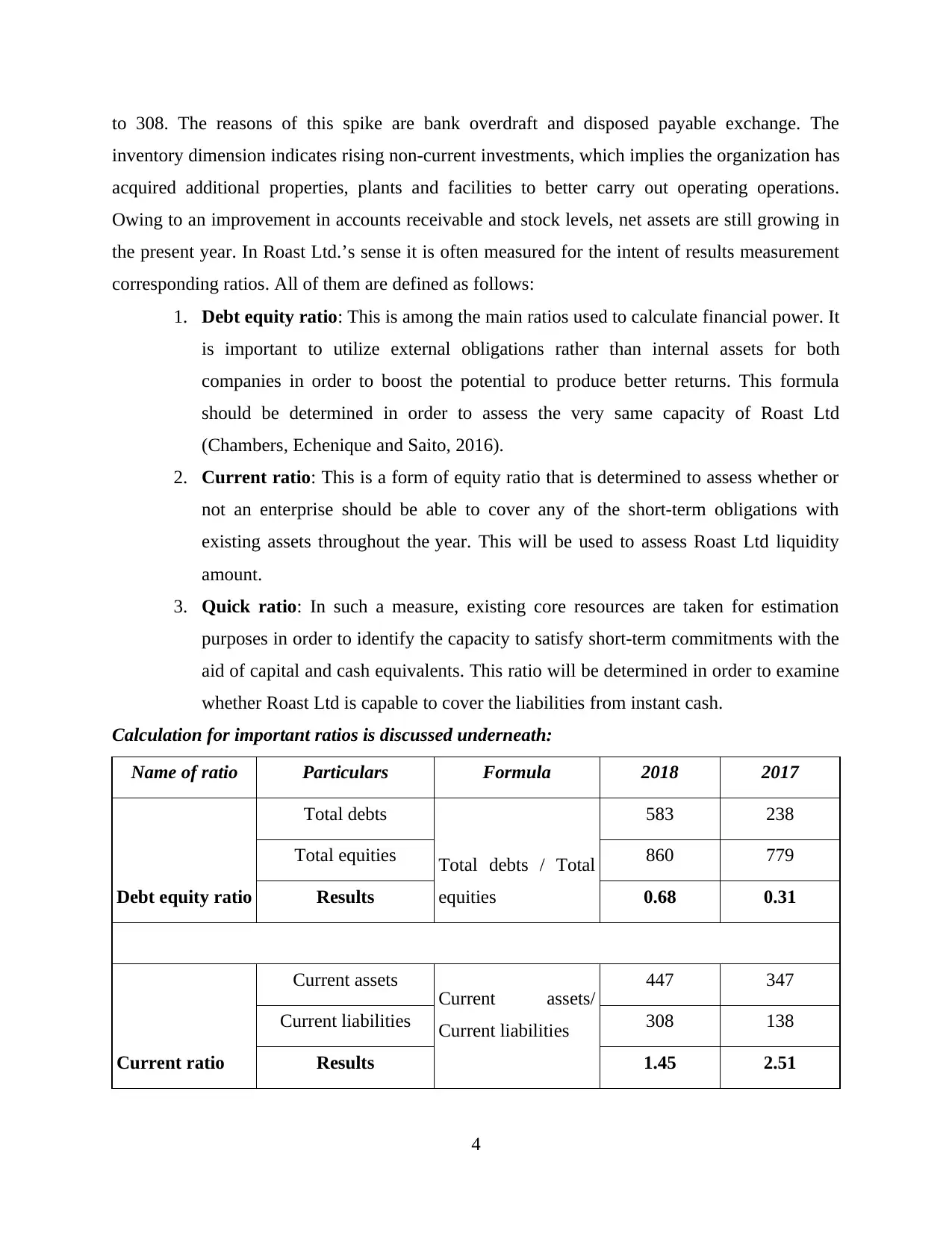

Name of ratio Particulars Formula 2018 2017

Debt equity ratio

Total debts

Total debts / Total

equities

583 238

Total equities 860 779

Results 0.68 0.31

Current ratio

Current assets Current assets/

Current liabilities

447 347

Current liabilities 308 138

Results 1.45 2.51

4

inventory dimension indicates rising non-current investments, which implies the organization has

acquired additional properties, plants and facilities to better carry out operating operations.

Owing to an improvement in accounts receivable and stock levels, net assets are still growing in

the present year. In Roast Ltd.’s sense it is often measured for the intent of results measurement

corresponding ratios. All of them are defined as follows:

1. Debt equity ratio: This is among the main ratios used to calculate financial power. It

is important to utilize external obligations rather than internal assets for both

companies in order to boost the potential to produce better returns. This formula

should be determined in order to assess the very same capacity of Roast Ltd

(Chambers, Echenique and Saito, 2016).

2. Current ratio: This is a form of equity ratio that is determined to assess whether or

not an enterprise should be able to cover any of the short-term obligations with

existing assets throughout the year. This will be used to assess Roast Ltd liquidity

amount.

3. Quick ratio: In such a measure, existing core resources are taken for estimation

purposes in order to identify the capacity to satisfy short-term commitments with the

aid of capital and cash equivalents. This ratio will be determined in order to examine

whether Roast Ltd is capable to cover the liabilities from instant cash.

Calculation for important ratios is discussed underneath:

Name of ratio Particulars Formula 2018 2017

Debt equity ratio

Total debts

Total debts / Total

equities

583 238

Total equities 860 779

Results 0.68 0.31

Current ratio

Current assets Current assets/

Current liabilities

447 347

Current liabilities 308 138

Results 1.45 2.51

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

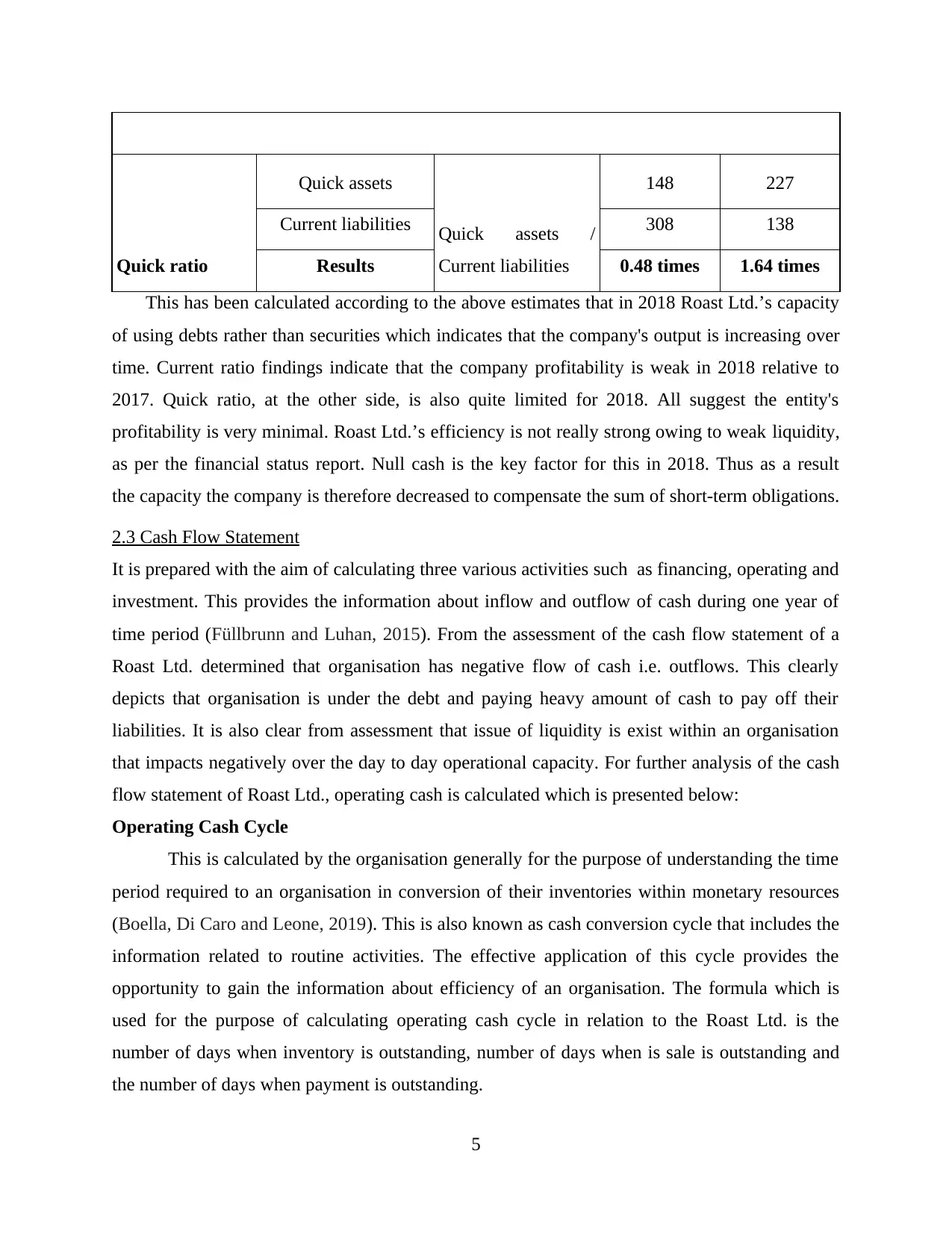

Quick ratio

Quick assets

Quick assets /

Current liabilities

148 227

Current liabilities 308 138

Results 0.48 times 1.64 times

This has been calculated according to the above estimates that in 2018 Roast Ltd.’s capacity

of using debts rather than securities which indicates that the company's output is increasing over

time. Current ratio findings indicate that the company profitability is weak in 2018 relative to

2017. Quick ratio, at the other side, is also quite limited for 2018. All suggest the entity's

profitability is very minimal. Roast Ltd.’s efficiency is not really strong owing to weak liquidity,

as per the financial status report. Null cash is the key factor for this in 2018. Thus as a result

the capacity the company is therefore decreased to compensate the sum of short-term obligations.

2.3 Cash Flow Statement

It is prepared with the aim of calculating three various activities such as financing, operating and

investment. This provides the information about inflow and outflow of cash during one year of

time period (Füllbrunn and Luhan, 2015). From the assessment of the cash flow statement of a

Roast Ltd. determined that organisation has negative flow of cash i.e. outflows. This clearly

depicts that organisation is under the debt and paying heavy amount of cash to pay off their

liabilities. It is also clear from assessment that issue of liquidity is exist within an organisation

that impacts negatively over the day to day operational capacity. For further analysis of the cash

flow statement of Roast Ltd., operating cash is calculated which is presented below:

Operating Cash Cycle

This is calculated by the organisation generally for the purpose of understanding the time

period required to an organisation in conversion of their inventories within monetary resources

(Boella, Di Caro and Leone, 2019). This is also known as cash conversion cycle that includes the

information related to routine activities. The effective application of this cycle provides the

opportunity to gain the information about efficiency of an organisation. The formula which is

used for the purpose of calculating operating cash cycle in relation to the Roast Ltd. is the

number of days when inventory is outstanding, number of days when is sale is outstanding and

the number of days when payment is outstanding.

5

Quick assets

Quick assets /

Current liabilities

148 227

Current liabilities 308 138

Results 0.48 times 1.64 times

This has been calculated according to the above estimates that in 2018 Roast Ltd.’s capacity

of using debts rather than securities which indicates that the company's output is increasing over

time. Current ratio findings indicate that the company profitability is weak in 2018 relative to

2017. Quick ratio, at the other side, is also quite limited for 2018. All suggest the entity's

profitability is very minimal. Roast Ltd.’s efficiency is not really strong owing to weak liquidity,

as per the financial status report. Null cash is the key factor for this in 2018. Thus as a result

the capacity the company is therefore decreased to compensate the sum of short-term obligations.

2.3 Cash Flow Statement

It is prepared with the aim of calculating three various activities such as financing, operating and

investment. This provides the information about inflow and outflow of cash during one year of

time period (Füllbrunn and Luhan, 2015). From the assessment of the cash flow statement of a

Roast Ltd. determined that organisation has negative flow of cash i.e. outflows. This clearly

depicts that organisation is under the debt and paying heavy amount of cash to pay off their

liabilities. It is also clear from assessment that issue of liquidity is exist within an organisation

that impacts negatively over the day to day operational capacity. For further analysis of the cash

flow statement of Roast Ltd., operating cash is calculated which is presented below:

Operating Cash Cycle

This is calculated by the organisation generally for the purpose of understanding the time

period required to an organisation in conversion of their inventories within monetary resources

(Boella, Di Caro and Leone, 2019). This is also known as cash conversion cycle that includes the

information related to routine activities. The effective application of this cycle provides the

opportunity to gain the information about efficiency of an organisation. The formula which is

used for the purpose of calculating operating cash cycle in relation to the Roast Ltd. is the

number of days when inventory is outstanding, number of days when is sale is outstanding and

the number of days when payment is outstanding.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

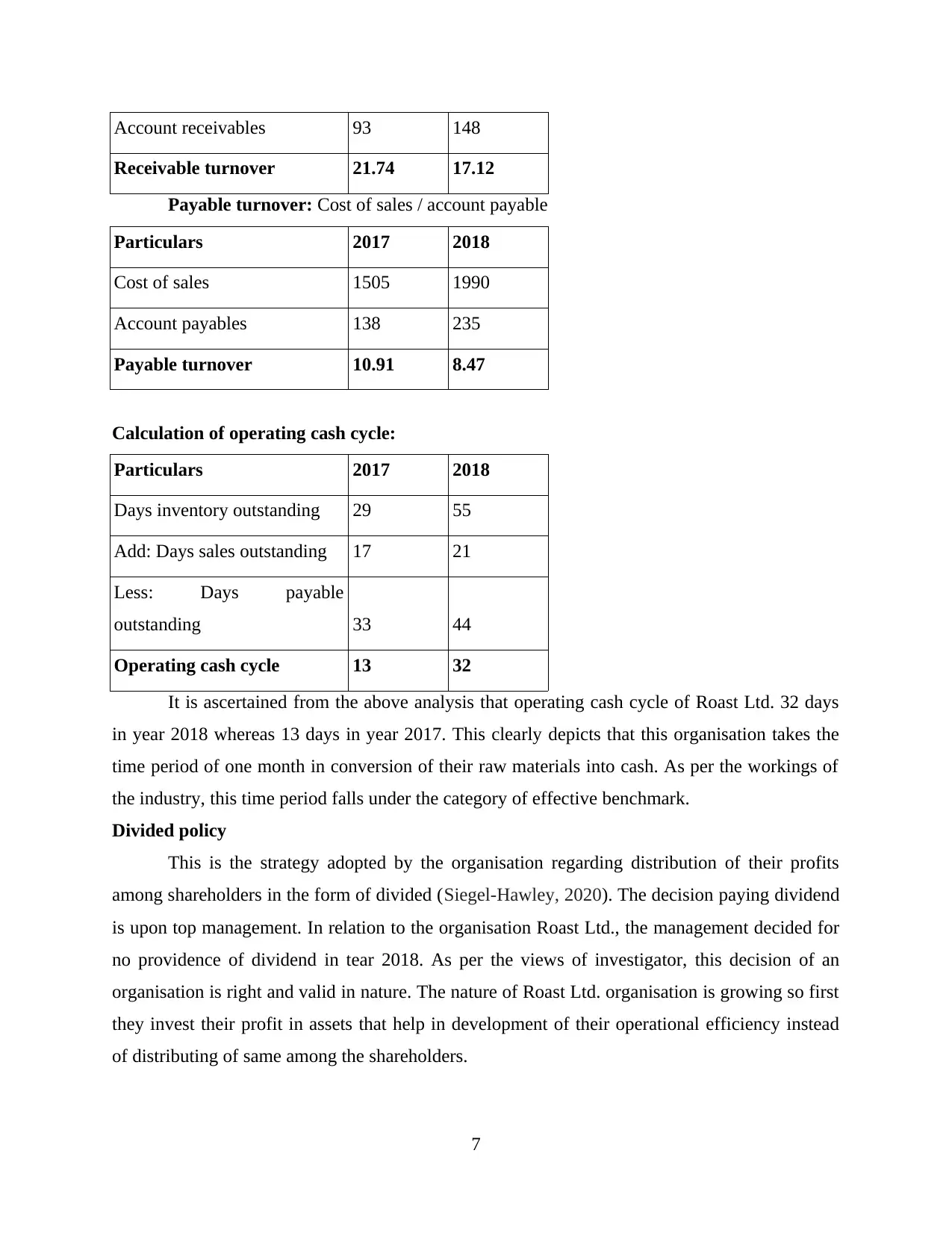

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Formula 365 / inventory turnover

Days inventory outstanding 29.11 54.80

Total days in year 365 365

Receivable turnover 21.74 17.12

Formula 365 / receivable turnover

Days sale outstanding 16.79 21.32

Total days in year 365 365

Payable turnover 10.91 8.47

Formula 365 / payable turnover

Days payable outstanding 33.46 43.09

Formula

Days inventory outstanding + days sales

outstanding - days payable outstanding

Result 13 32

Working notes:

Inventory turnover: Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

6

Total days in year 365 365

Inventory turnover 12.54 6.66

Formula 365 / inventory turnover

Days inventory outstanding 29.11 54.80

Total days in year 365 365

Receivable turnover 21.74 17.12

Formula 365 / receivable turnover

Days sale outstanding 16.79 21.32

Total days in year 365 365

Payable turnover 10.91 8.47

Formula 365 / payable turnover

Days payable outstanding 33.46 43.09

Formula

Days inventory outstanding + days sales

outstanding - days payable outstanding

Result 13 32

Working notes:

Inventory turnover: Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

6

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

It is ascertained from the above analysis that operating cash cycle of Roast Ltd. 32 days

in year 2018 whereas 13 days in year 2017. This clearly depicts that this organisation takes the

time period of one month in conversion of their raw materials into cash. As per the workings of

the industry, this time period falls under the category of effective benchmark.

Divided policy

This is the strategy adopted by the organisation regarding distribution of their profits

among shareholders in the form of divided (Siegel-Hawley, 2020). The decision paying dividend

is upon top management. In relation to the organisation Roast Ltd., the management decided for

no providence of dividend in tear 2018. As per the views of investigator, this decision of an

organisation is right and valid in nature. The nature of Roast Ltd. organisation is growing so first

they invest their profit in assets that help in development of their operational efficiency instead

of distributing of same among the shareholders.

7

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

It is ascertained from the above analysis that operating cash cycle of Roast Ltd. 32 days

in year 2018 whereas 13 days in year 2017. This clearly depicts that this organisation takes the

time period of one month in conversion of their raw materials into cash. As per the workings of

the industry, this time period falls under the category of effective benchmark.

Divided policy

This is the strategy adopted by the organisation regarding distribution of their profits

among shareholders in the form of divided (Siegel-Hawley, 2020). The decision paying dividend

is upon top management. In relation to the organisation Roast Ltd., the management decided for

no providence of dividend in tear 2018. As per the views of investigator, this decision of an

organisation is right and valid in nature. The nature of Roast Ltd. organisation is growing so first

they invest their profit in assets that help in development of their operational efficiency instead

of distributing of same among the shareholders.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the assessment of the cash flow statement, balance sheet and income statement of

an organisation, it is cleared that company is small in nature that has restricted value of profits

and revenue. While, talking about the growth and development of an organisation then the

growth rate is high that build this organisation as viable for acquirement by Starbucks

(Taghizadeh-Yazdi, Farrokhi and Mohammadi-Balani, 2020).

Part 3: Sources of Finance and Investment Appraisal

3.1 Investment appraisal

Management Forecasting

Roast Ltd. is a growing organisation. The nature of this organisation is ambitious who is

planning to develop their business in Romania through launching of their new coffee shop. The

decision of starting this organisation is taken by management in starting of the year 2017. The

management of an organisation also has forecast that they will going to earn the revenue of 300

million pounds in 2017 that will simultaneously increase up to the limit of 560 million pounds in

2018. The management also forecast the earning power for the years 2019, 2020, 2021 as 740

million pounds, 900 million pounds and 1120 million pounds. It is also assumed that the

organisation Roast Ltd. will attract high variable cost against to the business operations and able

to secure the viable amount of contribution or cash flows. The amount of cash which will be

forecasted for the following years is £60 million in 2017, £112 million in 2018, £148 million in

2019, £180 million in 2020 and £224 million in 2021 (Alves and et al., 2019).

It is clear from the above analysis that the organisation is going to earn high amount of

revenue and profits in coming 5 years of time period. The organisation does have any

contingencies plan. This will result in future as financial issue but does not impacts the viability

of project.

Investment appraisal techniques

Payback period

This is the time when the sum of the profits from your net income is necessary to purchase the

resources. A basic approach is to assess the threat related to the proposed enterprise. A

speculation with a shorter recompense period is seen as preferable, as the financial expert's

inherent expense is under threat for shorter timeframes. The estimate used to set the repayment

8

an organisation, it is cleared that company is small in nature that has restricted value of profits

and revenue. While, talking about the growth and development of an organisation then the

growth rate is high that build this organisation as viable for acquirement by Starbucks

(Taghizadeh-Yazdi, Farrokhi and Mohammadi-Balani, 2020).

Part 3: Sources of Finance and Investment Appraisal

3.1 Investment appraisal

Management Forecasting

Roast Ltd. is a growing organisation. The nature of this organisation is ambitious who is

planning to develop their business in Romania through launching of their new coffee shop. The

decision of starting this organisation is taken by management in starting of the year 2017. The

management of an organisation also has forecast that they will going to earn the revenue of 300

million pounds in 2017 that will simultaneously increase up to the limit of 560 million pounds in

2018. The management also forecast the earning power for the years 2019, 2020, 2021 as 740

million pounds, 900 million pounds and 1120 million pounds. It is also assumed that the

organisation Roast Ltd. will attract high variable cost against to the business operations and able

to secure the viable amount of contribution or cash flows. The amount of cash which will be

forecasted for the following years is £60 million in 2017, £112 million in 2018, £148 million in

2019, £180 million in 2020 and £224 million in 2021 (Alves and et al., 2019).

It is clear from the above analysis that the organisation is going to earn high amount of

revenue and profits in coming 5 years of time period. The organisation does have any

contingencies plan. This will result in future as financial issue but does not impacts the viability

of project.

Investment appraisal techniques

Payback period

This is the time when the sum of the profits from your net income is necessary to purchase the

resources. A basic approach is to assess the threat related to the proposed enterprise. A

speculation with a shorter recompense period is seen as preferable, as the financial expert's

inherent expense is under threat for shorter timeframes. The estimate used to set the repayment

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deadline is known as the repositioning strategy. The repayment deadline is communicated in

parts of years and years. The equation for the reprint strategy is overseen: Divide the cost of

money (which is assumed to be completely at the beginning of the task) by measuring the net

money flow produced by the enterprise each year (which is assumed to be consistently equal is)

(Kareva and Memedi, 2019).

This is considered as the time period that an organisation takes in ascertainment of the amount of

initial investment. This will help the management to know about the time of months and years

that they going to take for evading their all amount of initial investment. The payback period of

Roast Ltd. is ascertained as 4 years. This clearly depicts that the organisation takes the time

period of 4 years in the recovery of the initial investment of 500 million pounds (Del Baldo,

Arcari and Ruisi, 2019).

There are many different benefits and limitations are attached with using of this method

of investment appraisal. The benefit associated is that this is simple to use and easy to

understand. It means not required to have professional trained staff in calculation of payback

period. This provides the quick solution. The drawbacks attached with this includes ignorance of

time value money and unequal coverage of cash flows. This limits the analysis through

ignorance of the profitability margin and return on investment.

Accounting rate of return

ARR, additionally termed as a straight or normal speed of return, is a speculative equation that is

used to determine annual income or to benefit an enterprise. Thus, it figures out how much cash

or return you will have as a financial expert on your venture.

It is important for an organisation to attain high percentage for their project. This is so

because it enables high level of profitability. In relation to the Roast Ltd. The ARR is 18%.

The benefit associated with this ARR technique is help in comparison of two projects.

The rates associated with it is easy to calculate that provides accurate view of profit. The

limitation attached with the application of this method is about non consideration of time factor

that impacts the fast decision making ability.

NPV

9

parts of years and years. The equation for the reprint strategy is overseen: Divide the cost of

money (which is assumed to be completely at the beginning of the task) by measuring the net

money flow produced by the enterprise each year (which is assumed to be consistently equal is)

(Kareva and Memedi, 2019).

This is considered as the time period that an organisation takes in ascertainment of the amount of

initial investment. This will help the management to know about the time of months and years

that they going to take for evading their all amount of initial investment. The payback period of

Roast Ltd. is ascertained as 4 years. This clearly depicts that the organisation takes the time

period of 4 years in the recovery of the initial investment of 500 million pounds (Del Baldo,

Arcari and Ruisi, 2019).

There are many different benefits and limitations are attached with using of this method

of investment appraisal. The benefit associated is that this is simple to use and easy to

understand. It means not required to have professional trained staff in calculation of payback

period. This provides the quick solution. The drawbacks attached with this includes ignorance of

time value money and unequal coverage of cash flows. This limits the analysis through

ignorance of the profitability margin and return on investment.

Accounting rate of return

ARR, additionally termed as a straight or normal speed of return, is a speculative equation that is

used to determine annual income or to benefit an enterprise. Thus, it figures out how much cash

or return you will have as a financial expert on your venture.

It is important for an organisation to attain high percentage for their project. This is so

because it enables high level of profitability. In relation to the Roast Ltd. The ARR is 18%.

The benefit associated with this ARR technique is help in comparison of two projects.

The rates associated with it is easy to calculate that provides accurate view of profit. The

limitation attached with the application of this method is about non consideration of time factor

that impacts the fast decision making ability.

NPV

9

Net present value (NPV) is an estimate of future income (positive and negative) over the entire

existence of a speculation limited to the present. The NPV exam is a type of implicit assessment

and is widely used in funds and represents an estimate of a business, speculative security, capital

work, new discoveries, cost reduction programs, and anything that involves income.

This is also applied to the series of cash flows in relation to the different period of time. In

the current case of Roast Ltd., ascertained that organisation will have NPV of 110 million

Pounds. The aspects which ae used in the computation of this value include years, discounted

factors, cash flows and present values.

The benefit of this technique is consideration of all available years’ cash flow along with risk

factors. This is also known as the good measure of profitability. The limitations associated with

its use include estimation of opportunity cost not the investment value cost. This makes the

difficult to ascertain the exact amount of earnings and returns. This method also ignores sunk

cost and optimistic values that provide unfair position of investments (Berretta, 2019).

From the all above discussion, it is clear that investment by Roast Ltd. in opening of new

stores at Romania is viable in nature. This will help to improve their cash position and

profitability.

3.2 Sources of Finance

Sources of financing are as wide as they are long; however, they mainly fall into two

classifications: Internal and external sources of money. Internal sources of fund are reserves that

originate from inside the association. There are some examples of internal funding such as cash

from sales, sale of surplus assets as well as profits company hold back to finance development

and expansion. External source of finance are reserves raised from an outside source. Bank

overdrafts, trade credit, share issues etc. All these are considering internal and external sourcing

of finance that will be beneficial for an organisation in development of its business growth and

success in marketplace easily. Along with this, there are some useful sources of funding for

Roast Ltd, which will be explained as below with their advantages and disadvantages. These are

described as below:

Bank loan: This is an effective source of finance that helps business by providing loan to the

organisation in an agreed repayment schedule. In addition, bank loan is generally preferable

option for an organisation to raise accurate amount of capital. The main reason behind adopting

bank loan as a source of finance is that it allows Roast Ltd to do refund after some time period on

10

existence of a speculation limited to the present. The NPV exam is a type of implicit assessment

and is widely used in funds and represents an estimate of a business, speculative security, capital

work, new discoveries, cost reduction programs, and anything that involves income.

This is also applied to the series of cash flows in relation to the different period of time. In

the current case of Roast Ltd., ascertained that organisation will have NPV of 110 million

Pounds. The aspects which ae used in the computation of this value include years, discounted

factors, cash flows and present values.

The benefit of this technique is consideration of all available years’ cash flow along with risk

factors. This is also known as the good measure of profitability. The limitations associated with

its use include estimation of opportunity cost not the investment value cost. This makes the

difficult to ascertain the exact amount of earnings and returns. This method also ignores sunk

cost and optimistic values that provide unfair position of investments (Berretta, 2019).

From the all above discussion, it is clear that investment by Roast Ltd. in opening of new

stores at Romania is viable in nature. This will help to improve their cash position and

profitability.

3.2 Sources of Finance

Sources of financing are as wide as they are long; however, they mainly fall into two

classifications: Internal and external sources of money. Internal sources of fund are reserves that

originate from inside the association. There are some examples of internal funding such as cash

from sales, sale of surplus assets as well as profits company hold back to finance development

and expansion. External source of finance are reserves raised from an outside source. Bank

overdrafts, trade credit, share issues etc. All these are considering internal and external sourcing

of finance that will be beneficial for an organisation in development of its business growth and

success in marketplace easily. Along with this, there are some useful sources of funding for

Roast Ltd, which will be explained as below with their advantages and disadvantages. These are

described as below:

Bank loan: This is an effective source of finance that helps business by providing loan to the

organisation in an agreed repayment schedule. In addition, bank loan is generally preferable

option for an organisation to raise accurate amount of capital. The main reason behind adopting

bank loan as a source of finance is that it allows Roast Ltd to do refund after some time period on

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.