Comprehensive Report on Derivatives: Types, Applications, and Impact

VerifiedAdded on 2023/04/17

|31

|5207

|301

Report

AI Summary

This report provides a comprehensive analysis of financial derivatives, focusing on four primary types: futures, forwards, options, and swaps. It elucidates how these derivatives function, their applications in risk management and hedging, and their implications for financial systems. The report includes numerical examples to illustrate how each derivative works, along with discussions on their respective merits and demerits. It highlights the roles of hedgers and speculators in the derivatives market and emphasizes the importance of derivatives in price discovery and transaction efficiency. The analysis covers the use of futures contracts for securing future prices, forward contracts for managing foreign exchange risk, options contracts for leveraging asset values, and swap contracts for hedging against price fluctuations. Ultimately, the report underscores the significant impact of derivatives on financial systems through risk management, price discovery, and efficiency of transactions.

Running Head: DERIVATIVE 1

Derivative and Its Four Types

Student’s Name

Institutional Affiliation

Derivative and Its Four Types

Student’s Name

Institutional Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Derivative and Its Four Types 2

Abstract

Derivative performance depends on the performance of the underlying asset. Alternatively, there

are four primary types of derivatives; options, swaps, forwards, and futures. Futures contract

provide a definite value certainty on both investors, which minimizes the risks connected with

the volatility price. In spite of this fact, speculators do not prioritize on owning the underlying

product. Instead, they enter the market to make a profit from the falling and rising in prices. The

contract limits the risk exposure, which an investor trades with. Contrary, the forward contracts

are agreements to sell or buy a property at a fixed date and value. Thus, financial institutions

need to adopt approaches that minimize the risks, and reduces the impacts of severe market

movements; the management is possible through hedging. Conversely, option contracts are

derivative of financial securities, which depend on the value of the asset, which allow the

investor to put the odds in their favor. Therefore, the options contract permits a firm the rights,

but not the obligation to sell or buy an underlying asset at a stipulated price before or on a

specific date. Moreover, a swap contract is an agreement between various parties that specifies

the swap terms that may include the legs underlying value, times, and payment frequency.

Hence, the majority of people enter swaps either to hedge against others positions or to predict

the future price of the underlying currency of a free leg. Consequently, Derivatives act as

financial agreements whose returns are connected to the underlying asset performance such as

commodities, bonds, and bonds. Derivatives have a significant impact on the financial systems

through risk management, price discovery, and efficiency of transactions

Abstract

Derivative performance depends on the performance of the underlying asset. Alternatively, there

are four primary types of derivatives; options, swaps, forwards, and futures. Futures contract

provide a definite value certainty on both investors, which minimizes the risks connected with

the volatility price. In spite of this fact, speculators do not prioritize on owning the underlying

product. Instead, they enter the market to make a profit from the falling and rising in prices. The

contract limits the risk exposure, which an investor trades with. Contrary, the forward contracts

are agreements to sell or buy a property at a fixed date and value. Thus, financial institutions

need to adopt approaches that minimize the risks, and reduces the impacts of severe market

movements; the management is possible through hedging. Conversely, option contracts are

derivative of financial securities, which depend on the value of the asset, which allow the

investor to put the odds in their favor. Therefore, the options contract permits a firm the rights,

but not the obligation to sell or buy an underlying asset at a stipulated price before or on a

specific date. Moreover, a swap contract is an agreement between various parties that specifies

the swap terms that may include the legs underlying value, times, and payment frequency.

Hence, the majority of people enter swaps either to hedge against others positions or to predict

the future price of the underlying currency of a free leg. Consequently, Derivatives act as

financial agreements whose returns are connected to the underlying asset performance such as

commodities, bonds, and bonds. Derivatives have a significant impact on the financial systems

through risk management, price discovery, and efficiency of transactions

Derivative and Its Four Types 3

Table of Contents

Introduction…………………………………………………………………5

Financial Firms Utilize Certain Types of Derivatives………………………5

Futures Contracts……………………………………………………………5-7

Forward Contracts………………………………………………………….7-11

Options Contracts………………………………………………………….11-14

Swap Contracts…………………………………………………………….14-15

Numerical Examples on How Each Derivative Works…………………….15

Futures Contracts…………………………………………………………..15-19

Forward Contracts…………………………………………………………19-20

Options Contracts………………………………………………………….20-21

Swap Contracts…………………………………………………………….22-23

Merits and Demerits……………………………………………………….23

Futures Contracts………………………………………………………….23

Forward Contracts…………………………………………………………23

Options Contracts………………………………………………………….23-24

Swap Contracts…………………………………………………………….24

Implications of Derivatives………………………………………………..24-26

Table of Contents

Introduction…………………………………………………………………5

Financial Firms Utilize Certain Types of Derivatives………………………5

Futures Contracts……………………………………………………………5-7

Forward Contracts………………………………………………………….7-11

Options Contracts………………………………………………………….11-14

Swap Contracts…………………………………………………………….14-15

Numerical Examples on How Each Derivative Works…………………….15

Futures Contracts…………………………………………………………..15-19

Forward Contracts…………………………………………………………19-20

Options Contracts………………………………………………………….20-21

Swap Contracts…………………………………………………………….22-23

Merits and Demerits……………………………………………………….23

Futures Contracts………………………………………………………….23

Forward Contracts…………………………………………………………23

Options Contracts………………………………………………………….23-24

Swap Contracts…………………………………………………………….24

Implications of Derivatives………………………………………………..24-26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Derivative and Its Four Types 4

Conclusion………………………………………………………………26-27

References………………………………………………………………28-31

Conclusion………………………………………………………………26-27

References………………………………………………………………28-31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Derivative and Its Four Types 5

Derivative and Its Four Types

The derivative is an agreement between two parties that derives its value from an

underlying asset. Thus, it is a financial instrument for managing associated risks. Alternatively,

there are four common types of derivatives; options, swaps, forwards, and futures. Moreover, the

underlying corpus created can comprise of one financial security or a combination of several

financial securities. Hence, the underlying asset value is bound to shift as the assets keep

changing continuously. Generally, the underlying asset form depending on the currency, bonds,

stocks, interest, and commodities rates. Therefore, derivative performance depends on the

performance of the underlying asset. Hence, the asset trades in the market where the purchaser

and the seller mutually decide its value, then the seller gives the underlying to the purchaser and

is paid in return. Importantly, cash or spot value is the underlying price if bought immediately.

Analysis

Financial Firms Utilize Certain Types of Derivatives

Most of the retail banking attract deposits and loans. Thus, the difference between

interest rates on loans and deposits creates a profit. As such, the banks play various roles in the

derivatives market. Therefore, banks act as intermediaries in the OTC “over the counter” market,

matching purchaser and sellers, and earning commission fees (Future, n.d). Contrary, financial

institutions participate directly in the derivatives market as purchasers and sellers; they are

derivatives end users.

Futures Contracts

Derivative and Its Four Types

The derivative is an agreement between two parties that derives its value from an

underlying asset. Thus, it is a financial instrument for managing associated risks. Alternatively,

there are four common types of derivatives; options, swaps, forwards, and futures. Moreover, the

underlying corpus created can comprise of one financial security or a combination of several

financial securities. Hence, the underlying asset value is bound to shift as the assets keep

changing continuously. Generally, the underlying asset form depending on the currency, bonds,

stocks, interest, and commodities rates. Therefore, derivative performance depends on the

performance of the underlying asset. Hence, the asset trades in the market where the purchaser

and the seller mutually decide its value, then the seller gives the underlying to the purchaser and

is paid in return. Importantly, cash or spot value is the underlying price if bought immediately.

Analysis

Financial Firms Utilize Certain Types of Derivatives

Most of the retail banking attract deposits and loans. Thus, the difference between

interest rates on loans and deposits creates a profit. As such, the banks play various roles in the

derivatives market. Therefore, banks act as intermediaries in the OTC “over the counter” market,

matching purchaser and sellers, and earning commission fees (Future, n.d). Contrary, financial

institutions participate directly in the derivatives market as purchasers and sellers; they are

derivatives end users.

Futures Contracts

Derivative and Its Four Types 6

Manufactures, importers, and farmers can be termed as hedgers. As such, the hedger sells

or buys in the futures market in securing the commodity’s future price intended to be sold later in

a cash market. Hence, it would assist protect against value risks, and considered an insurance

policy of sorts. Importantly, if someone spends a long time in a futures contract, then the

individual should secure the possible low price. Furthermore, if MNCs short-selling contracts,

then the firms want a high value as possible. Unfortunately, futures contract provide a definite

value certainty on both parties, which minimizes the risks connected with the volatility price.

Using futures contract, hedging can be utilized to lock in an acceptable value margin between

raw material cost, and the retail cost of the final commodity sold.

For instance, when one considers a corn futures contract that represents 5,000 bushels of

corn. This means the corn is trading at five dollars per bushel; the contract price is 25,000

dollars. As such, futures contracts standardize on the particular quality, and amount of the

underlying product (Investopedia, 2018). Therefore, the futures value moves about the spot value

for the product based on the demand and supply.

Market participants may not aim to reduce risks, but instead, benefit from the risky nature

of the future market. These are termed as speculators, which intend to participants intend to

profit from the value changes that hedgers cover themselves against (Investopedia, 2018).

Importantly, while hedgers prioritize on minimizing their risks on their investments, speculators

want to maximize their risk. Thus, maximizing potential profits (Investopedia, n.d). Hence,

speculators do not prioritize on owning the underlying product; rather, they enter the market to

make a profit from the falling and rising in prices.

Manufactures, importers, and farmers can be termed as hedgers. As such, the hedger sells

or buys in the futures market in securing the commodity’s future price intended to be sold later in

a cash market. Hence, it would assist protect against value risks, and considered an insurance

policy of sorts. Importantly, if someone spends a long time in a futures contract, then the

individual should secure the possible low price. Furthermore, if MNCs short-selling contracts,

then the firms want a high value as possible. Unfortunately, futures contract provide a definite

value certainty on both parties, which minimizes the risks connected with the volatility price.

Using futures contract, hedging can be utilized to lock in an acceptable value margin between

raw material cost, and the retail cost of the final commodity sold.

For instance, when one considers a corn futures contract that represents 5,000 bushels of

corn. This means the corn is trading at five dollars per bushel; the contract price is 25,000

dollars. As such, futures contracts standardize on the particular quality, and amount of the

underlying product (Investopedia, 2018). Therefore, the futures value moves about the spot value

for the product based on the demand and supply.

Market participants may not aim to reduce risks, but instead, benefit from the risky nature

of the future market. These are termed as speculators, which intend to participants intend to

profit from the value changes that hedgers cover themselves against (Investopedia, 2018).

Importantly, while hedgers prioritize on minimizing their risks on their investments, speculators

want to maximize their risk. Thus, maximizing potential profits (Investopedia, n.d). Hence,

speculators do not prioritize on owning the underlying product; rather, they enter the market to

make a profit from the falling and rising in prices.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Derivative and Its Four Types 7

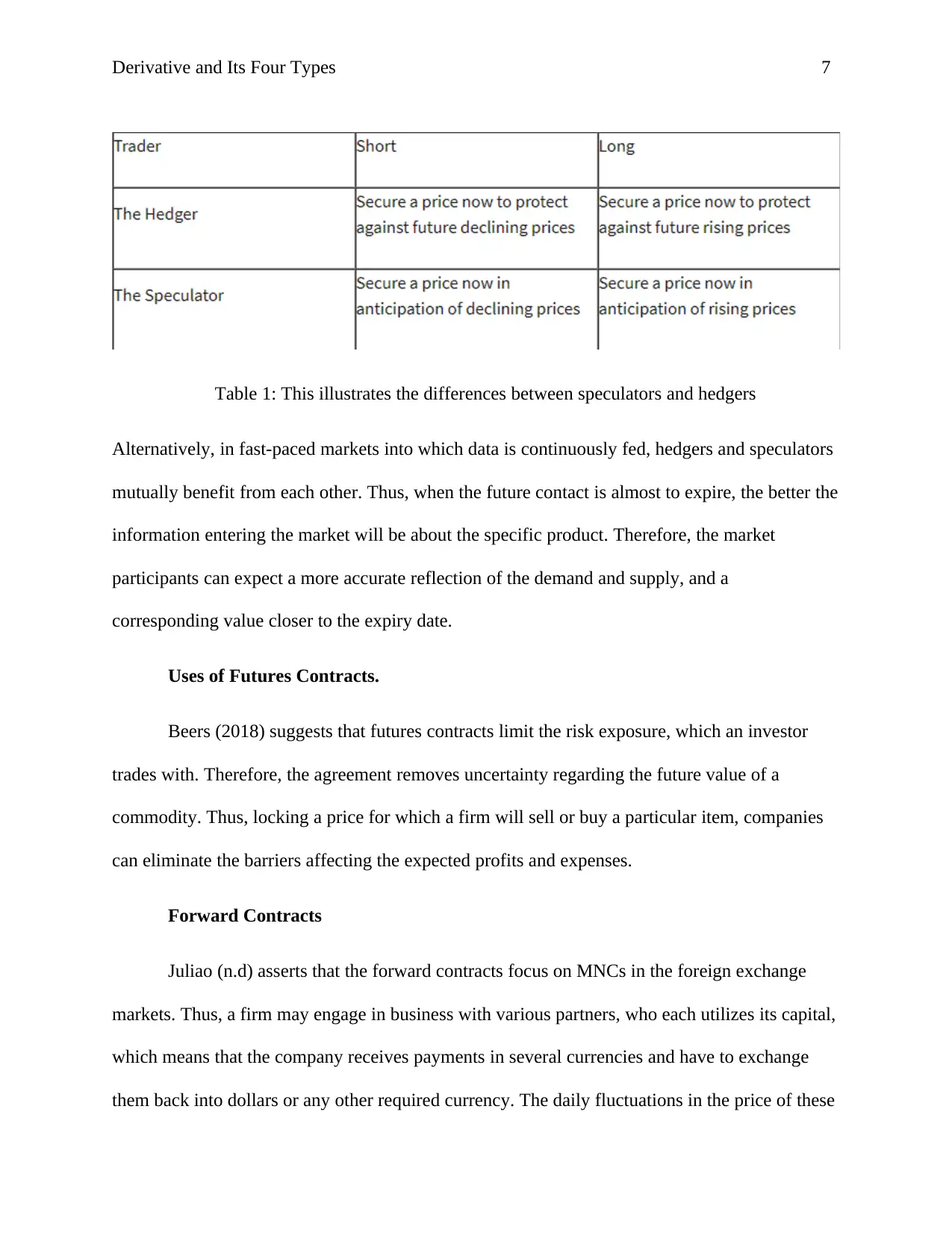

Table 1: This illustrates the differences between speculators and hedgers

Alternatively, in fast-paced markets into which data is continuously fed, hedgers and speculators

mutually benefit from each other. Thus, when the future contact is almost to expire, the better the

information entering the market will be about the specific product. Therefore, the market

participants can expect a more accurate reflection of the demand and supply, and a

corresponding value closer to the expiry date.

Uses of Futures Contracts.

Beers (2018) suggests that futures contracts limit the risk exposure, which an investor

trades with. Therefore, the agreement removes uncertainty regarding the future value of a

commodity. Thus, locking a price for which a firm will sell or buy a particular item, companies

can eliminate the barriers affecting the expected profits and expenses.

Forward Contracts

Juliao (n.d) asserts that the forward contracts focus on MNCs in the foreign exchange

markets. Thus, a firm may engage in business with various partners, who each utilizes its capital,

which means that the company receives payments in several currencies and have to exchange

them back into dollars or any other required currency. The daily fluctuations in the price of these

Table 1: This illustrates the differences between speculators and hedgers

Alternatively, in fast-paced markets into which data is continuously fed, hedgers and speculators

mutually benefit from each other. Thus, when the future contact is almost to expire, the better the

information entering the market will be about the specific product. Therefore, the market

participants can expect a more accurate reflection of the demand and supply, and a

corresponding value closer to the expiry date.

Uses of Futures Contracts.

Beers (2018) suggests that futures contracts limit the risk exposure, which an investor

trades with. Therefore, the agreement removes uncertainty regarding the future value of a

commodity. Thus, locking a price for which a firm will sell or buy a particular item, companies

can eliminate the barriers affecting the expected profits and expenses.

Forward Contracts

Juliao (n.d) asserts that the forward contracts focus on MNCs in the foreign exchange

markets. Thus, a firm may engage in business with various partners, who each utilizes its capital,

which means that the company receives payments in several currencies and have to exchange

them back into dollars or any other required currency. The daily fluctuations in the price of these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Derivative and Its Four Types 8

currencies influence the firm’s revenues and costs. Therefore, the company is at risk of losing

funds because of the severe fluctuations. It is essential that MNCs plan their profits and expenses

depending on the market exchange. Conversely, the foreign exchange market comprises of

multiple worldwide transactions utilized by investors for buying foreign currency to selling

domestic currency. Thus, each currency contains its absolute price compared to another, which

determines the exchange rate.

The primary risk of the market is the progressive fluctuations of the exchange rates,

which can bring higher profits or cause severe losses. Importantly, a financial firm needs to

adopt approaches that minimize the risks, and reduces the impacts of severe market movements;

the management is possible through hedging. It may involve using various financial instruments

that increase the protection of investors against fluctuations in the exchange rate of currency

(Juliao, n.d).

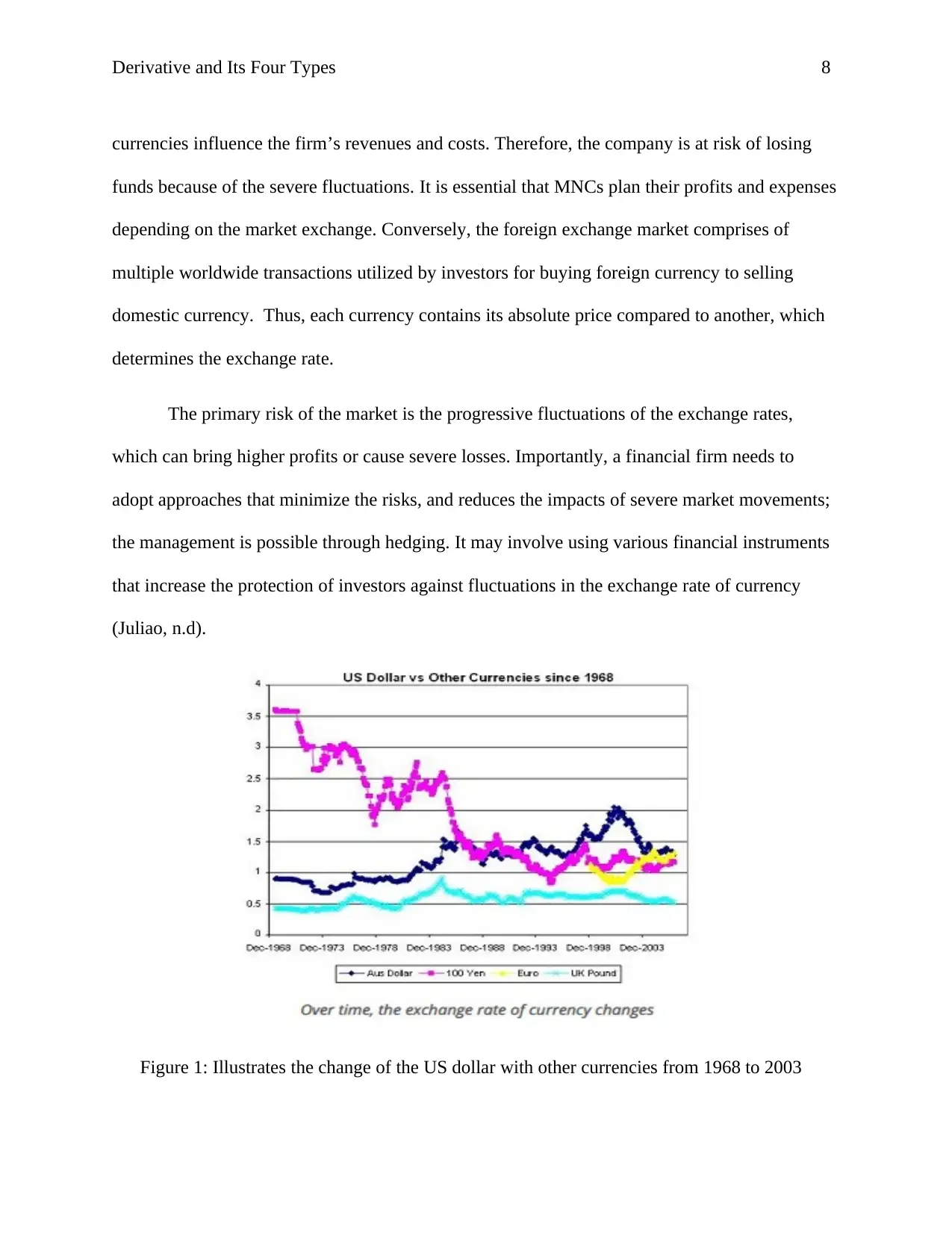

Figure 1: Illustrates the change of the US dollar with other currencies from 1968 to 2003

currencies influence the firm’s revenues and costs. Therefore, the company is at risk of losing

funds because of the severe fluctuations. It is essential that MNCs plan their profits and expenses

depending on the market exchange. Conversely, the foreign exchange market comprises of

multiple worldwide transactions utilized by investors for buying foreign currency to selling

domestic currency. Thus, each currency contains its absolute price compared to another, which

determines the exchange rate.

The primary risk of the market is the progressive fluctuations of the exchange rates,

which can bring higher profits or cause severe losses. Importantly, a financial firm needs to

adopt approaches that minimize the risks, and reduces the impacts of severe market movements;

the management is possible through hedging. It may involve using various financial instruments

that increase the protection of investors against fluctuations in the exchange rate of currency

(Juliao, n.d).

Figure 1: Illustrates the change of the US dollar with other currencies from 1968 to 2003

Derivative and Its Four Types 9

Therefore, the forward contracts are agreements to sell or buy a property at a fixed date and

value. Thus, the financial firm can receive capital during a particular time in the contract. As

such, the parties involved are usually enterprises with international banks and operations.

For instance, an American financial firm may need to know the domestic currency, and

how much the company may receive for future transactions in a foreign currency. Hence, the

firm may need to sign a forward contract with a local bank for any payments in Japanese

currency, yen, which the institution will receive in five months. Therefore, the company may

agree on an exchange rate of 116 per dollar, such that if the exchange rate goes up to 125 or

down to 105, the firm will receive the same amount of U.S dollars at 116 yen per dollar.

Importantly, forward contracts enable MNCs to know the precise exchange rate will receive in a

future date; hence, the firm does not need to make predictions.

The currency forwards occasionally follow a simple approach to determine the price or

exchange rate. It may consist of the interest rate and current rate differentials, such that if one

currency A unit plus interest from country A will equal the current value in currency B plus

interest from the same state. For example, for a two-year forward contract, one euro equals 1.15

dollars, and that the annual European interest rate is at one percent and in the U.S, it is 1.5

percent.

Therefore, one euro is equal to 1.557 U.S dollars, which means this will be the exchange rate for

the forward contract.

Therefore, the forward contracts are agreements to sell or buy a property at a fixed date and

value. Thus, the financial firm can receive capital during a particular time in the contract. As

such, the parties involved are usually enterprises with international banks and operations.

For instance, an American financial firm may need to know the domestic currency, and

how much the company may receive for future transactions in a foreign currency. Hence, the

firm may need to sign a forward contract with a local bank for any payments in Japanese

currency, yen, which the institution will receive in five months. Therefore, the company may

agree on an exchange rate of 116 per dollar, such that if the exchange rate goes up to 125 or

down to 105, the firm will receive the same amount of U.S dollars at 116 yen per dollar.

Importantly, forward contracts enable MNCs to know the precise exchange rate will receive in a

future date; hence, the firm does not need to make predictions.

The currency forwards occasionally follow a simple approach to determine the price or

exchange rate. It may consist of the interest rate and current rate differentials, such that if one

currency A unit plus interest from country A will equal the current value in currency B plus

interest from the same state. For example, for a two-year forward contract, one euro equals 1.15

dollars, and that the annual European interest rate is at one percent and in the U.S, it is 1.5

percent.

Therefore, one euro is equal to 1.557 U.S dollars, which means this will be the exchange rate for

the forward contract.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Derivative and Its Four Types 10

Forward contract participants consist of speculators and hedgers. Consequently, hedgers

do not demand a profit; instead it seeks to stabilize the revenues of their business operations.

Thus, their losses and gains are commonly offset to some percent depending on the

corresponding gain or loss in the market for the underlying property. In contrast, speculators are

occasionally not interested in taking possession of underlying properties (InvestingAnswers,

n.d). Therefore, forward contracts attract more hedgers than speculators.

Uses of Forward Contracts.

Utilizing Forward Contracts for a Rolling Hedge

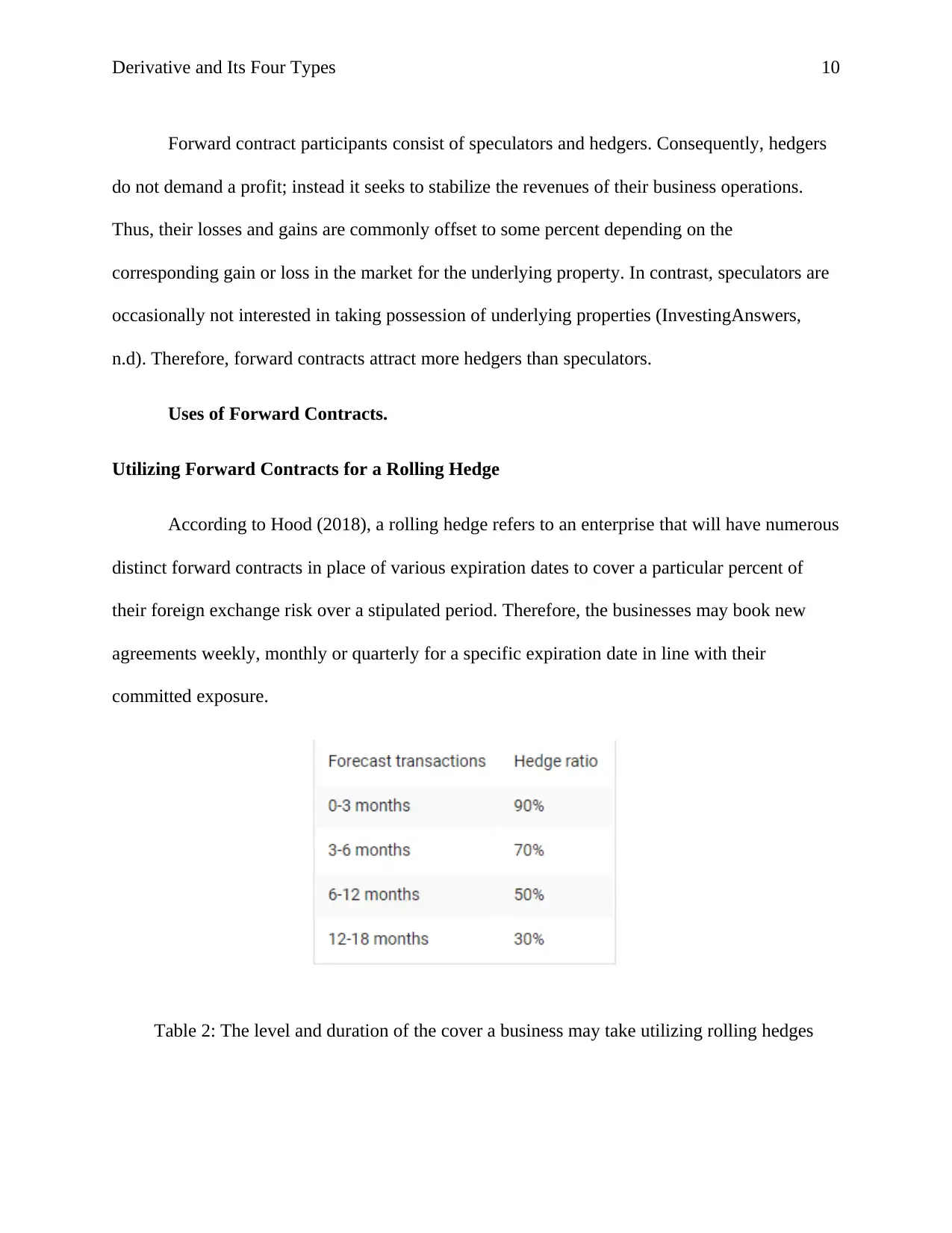

According to Hood (2018), a rolling hedge refers to an enterprise that will have numerous

distinct forward contracts in place of various expiration dates to cover a particular percent of

their foreign exchange risk over a stipulated period. Therefore, the businesses may book new

agreements weekly, monthly or quarterly for a specific expiration date in line with their

committed exposure.

Table 2: The level and duration of the cover a business may take utilizing rolling hedges

Forward contract participants consist of speculators and hedgers. Consequently, hedgers

do not demand a profit; instead it seeks to stabilize the revenues of their business operations.

Thus, their losses and gains are commonly offset to some percent depending on the

corresponding gain or loss in the market for the underlying property. In contrast, speculators are

occasionally not interested in taking possession of underlying properties (InvestingAnswers,

n.d). Therefore, forward contracts attract more hedgers than speculators.

Uses of Forward Contracts.

Utilizing Forward Contracts for a Rolling Hedge

According to Hood (2018), a rolling hedge refers to an enterprise that will have numerous

distinct forward contracts in place of various expiration dates to cover a particular percent of

their foreign exchange risk over a stipulated period. Therefore, the businesses may book new

agreements weekly, monthly or quarterly for a specific expiration date in line with their

committed exposure.

Table 2: The level and duration of the cover a business may take utilizing rolling hedges

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Derivative and Its Four Types 11

Importantly, the technique ensures that the financial institution is continuously assessing and

evaluating the currency market movements. Moreover, it reduces the time-to-time value

deviation-the shorter the time between booking hedges, the less volatile the currency value will

be from one hedge to another.

Utilizing Forward Contracts with Market Orders

Most of the MNCs commonly use rates that are budgeted for setting pricing, formulating,

and monitoring their hedging approach. Nonetheless, achieving these estimated rates is

sometimes reliant on the execution time of the forward contract. Therefore, market volatility

influences the time and date enterprise books a forward contract, which creates a massive

difference in the exchange rate resulting from market fluctuations of standard currency (Hood,

2018).

Options Contracts.

Options contract involve risks and are not appropriate for everyone. Thus, the options

trading is speculative and carry a substantial risk of loss (Downey, 2019). Therefore, option

contracts are derivative of financial securities; the value depends on the amount of the asset. This

means that the option contract allows the investor to put the odds in their favor. These types of

options consist of trade and exchange through a clearinghouse. Importantly, the options contract

permits a firm the rights, but not the obligation to sell or buy an underlying asset at a stipulated

price before or on a specific date. Nevertheless, the call option provides the holder the rights to

buy stock, while a put option grants the holder the right to sell shares.

Puts and Calls Options.

Importantly, the technique ensures that the financial institution is continuously assessing and

evaluating the currency market movements. Moreover, it reduces the time-to-time value

deviation-the shorter the time between booking hedges, the less volatile the currency value will

be from one hedge to another.

Utilizing Forward Contracts with Market Orders

Most of the MNCs commonly use rates that are budgeted for setting pricing, formulating,

and monitoring their hedging approach. Nonetheless, achieving these estimated rates is

sometimes reliant on the execution time of the forward contract. Therefore, market volatility

influences the time and date enterprise books a forward contract, which creates a massive

difference in the exchange rate resulting from market fluctuations of standard currency (Hood,

2018).

Options Contracts.

Options contract involve risks and are not appropriate for everyone. Thus, the options

trading is speculative and carry a substantial risk of loss (Downey, 2019). Therefore, option

contracts are derivative of financial securities; the value depends on the amount of the asset. This

means that the option contract allows the investor to put the odds in their favor. These types of

options consist of trade and exchange through a clearinghouse. Importantly, the options contract

permits a firm the rights, but not the obligation to sell or buy an underlying asset at a stipulated

price before or on a specific date. Nevertheless, the call option provides the holder the rights to

buy stock, while a put option grants the holder the right to sell shares.

Puts and Calls Options.

Derivative and Its Four Types 12

The call option acts as a down payment for a future purpose. For instance, a potential

property owner may spot the asset and want to purchase the house in the future, but will only

want to exercise the right once specific establishments around the area are built. Contrary, the

put option acts as an insurance policy. For example, if someone owns a home, then he or she is

likely familiar with the purchasing insurance of the property owner. Thus, an asset owner may

buy the property owner’s policy to cover their home from potential damages. Therefore, the

policy contains a face price, and provides the insurance holder cover in the event the home gets

damaged.

Over-the-Counter Options Differ from Regular Stock Options.

Kennon (2019) assert that over-the-counter options are private party contracts written to

the specifications of each side of the deal. Thus, they do not have any disclosure requirements,

and the firm is limited only in imagination as to what the option terms are. Therefore, the over-

the-counter options appeal is that the firm can transact in private and negotiation terms.

The Counterparty Risk in Over-the-Counter Options

The over-the-counter options lack the protection of an exchange. As such, the MNCs can

conclusively rely on the counterparty promise to live up to their bargaining deal. Therefore, the

options are particularly dangerous when utilized to hedge a firm’s exposure to specific risky

security or property. This is known as a basis risk because the hedges fall apart leaving the

company exposed. Alternatively, when an investment bank partnered with other MNCs to many

OTC options, then it would have entered a “black hole of the bankruptcy court.|”; this is termed

as a “daisy-chain” risk (Kennon, 2019). Therefore, it only takes a couple of over-the-counter

derivative transactions before it becomes impossible to evaluate the total exposure a financial

The call option acts as a down payment for a future purpose. For instance, a potential

property owner may spot the asset and want to purchase the house in the future, but will only

want to exercise the right once specific establishments around the area are built. Contrary, the

put option acts as an insurance policy. For example, if someone owns a home, then he or she is

likely familiar with the purchasing insurance of the property owner. Thus, an asset owner may

buy the property owner’s policy to cover their home from potential damages. Therefore, the

policy contains a face price, and provides the insurance holder cover in the event the home gets

damaged.

Over-the-Counter Options Differ from Regular Stock Options.

Kennon (2019) assert that over-the-counter options are private party contracts written to

the specifications of each side of the deal. Thus, they do not have any disclosure requirements,

and the firm is limited only in imagination as to what the option terms are. Therefore, the over-

the-counter options appeal is that the firm can transact in private and negotiation terms.

The Counterparty Risk in Over-the-Counter Options

The over-the-counter options lack the protection of an exchange. As such, the MNCs can

conclusively rely on the counterparty promise to live up to their bargaining deal. Therefore, the

options are particularly dangerous when utilized to hedge a firm’s exposure to specific risky

security or property. This is known as a basis risk because the hedges fall apart leaving the

company exposed. Alternatively, when an investment bank partnered with other MNCs to many

OTC options, then it would have entered a “black hole of the bankruptcy court.|”; this is termed

as a “daisy-chain” risk (Kennon, 2019). Therefore, it only takes a couple of over-the-counter

derivative transactions before it becomes impossible to evaluate the total exposure a financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.