Financial Derivatives Trading: Options, Futures, and Swaps Report

VerifiedAdded on 2021/01/02

|10

|2689

|291

Report

AI Summary

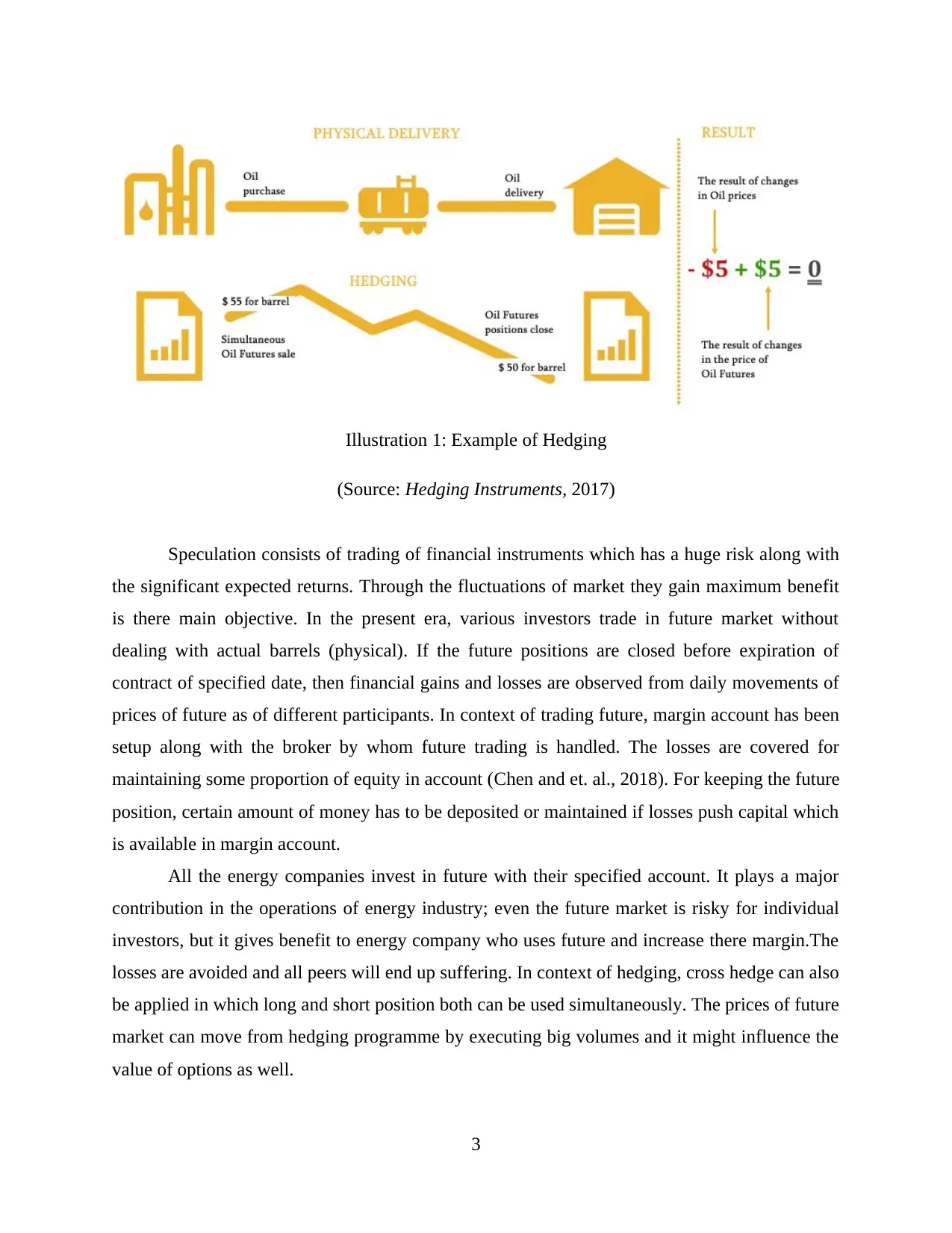

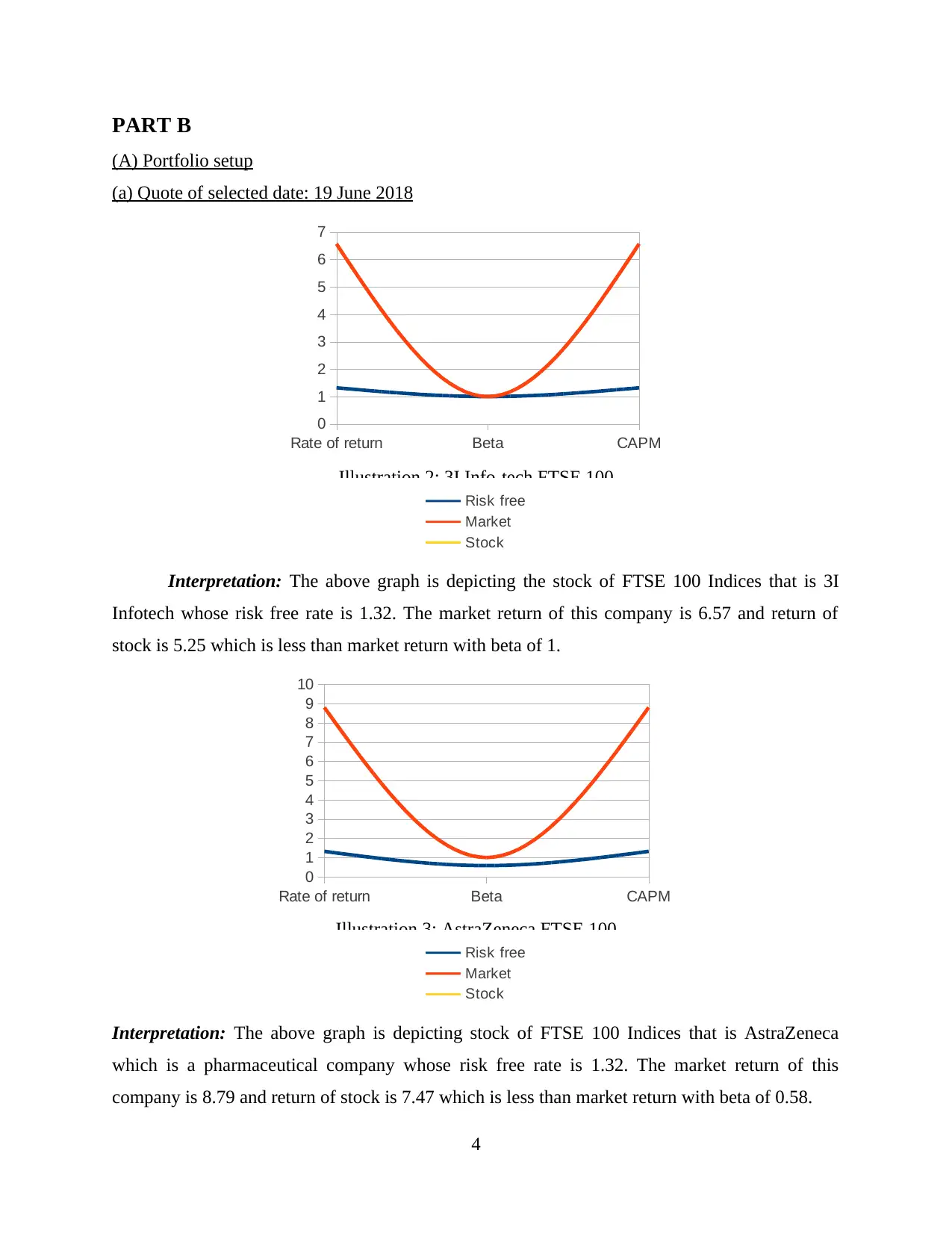

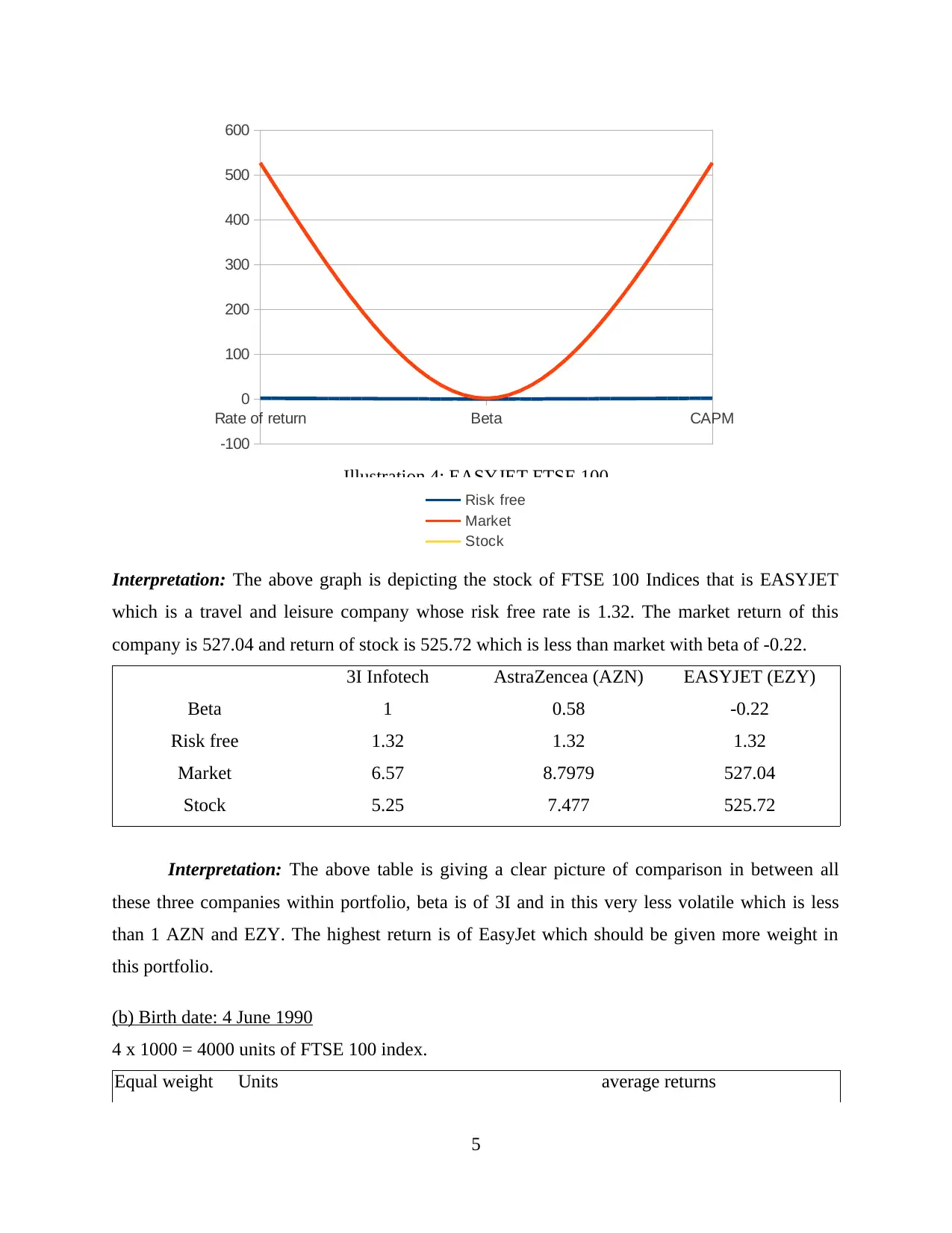

This report delves into the realm of financial derivatives, focusing on options, futures, and swaps. It begins with an introduction to the importance of futures markets in the modern economy, particularly in the context of crude oil. The report then explores the use of crude oil futures for managing risk through hedging and speculation, referencing an article on oil market trends. Part A elaborates on the origins and functions of futures markets, emphasizing their role in stabilizing income for producers and providing opportunities for speculators. It details the mechanics of crude oil futures, including the role of benchmarks like WTI and Brent crude, and how producers and consumers use these contracts to manage price risk. The report explains hedging strategies, including short and long hedges, and how they are employed to mitigate price fluctuations. Speculation in the futures market is also discussed, highlighting the role of margin accounts and the impact of future trading on energy companies. Part B presents a portfolio setup for FTSE 100 indices, analyzing the performance of 3I Infotech, AstraZeneca, and EASYJET. It includes a comparison of these companies based on beta, risk-free rates, market returns, and stock returns, providing a basis for portfolio allocation. The report also examines the risks faced by fund managers, such as interest rate risk, currency exchange rate risk, market risk, inflationary risk, and credit risk. It details the use of futures contracts for hedging these risks through long and short hedging strategies, and it concludes with hedging recommendations based on future price possibilities.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.