Financial Management Report: Dividend Policy and Market Value

VerifiedAdded on 2020/06/04

|9

|2255

|28

Report

AI Summary

This report delves into the critical aspects of dividend policy and its profound influence on a company's market value. It begins by exploring the concepts of dividend irrelevance and relevancy, examining the perspectives of both investors and corporate entities. The report analyzes the Modigliani-Miller (MM) model, which posits dividend irrelevance under certain conditions, and contrasts it with Gordon's model, which emphasizes the significance of dividend policy in determining firm value. Furthermore, the report addresses the agency problem, a conflict of interest between management and shareholders, and how dividend policies can exacerbate or mitigate these issues. It explores how dividend decisions affect market capitalization and company valuation. The report also examines the impact of taxes and transaction costs on dividend decisions and their implications for shareholders' wealth and ultimately concludes with a comprehensive overview of how dividend policies are set and their impact on the market and the agency relationship.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Discussing the proposition that a company's dividend policy is irrelevant to its market value. .3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Discussing the proposition that a company's dividend policy is irrelevant to its market value. .3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Financial management is the process that investors and business units employ for

ensuring effective as well as efficient usage of funds. Attainment of high profit margin is one of

the main objectives of both investors and business organization. With the motive to fulfill the

expectation level of investor’s business unit offers return to the shareholders in the form of

dividend. In the context of business unit, executives and management team plays a vital role in

setting out dividend policy. Hence, in this, report will provide deeper insight about the aspects of

dividend relevancy and irrelevancy. Besides this, it also depicts the manner in which dividend

policy has influence on market value. It also sheds light on the extent to which dividend policies

employed by the firm create agency problem or issues.

MAIN BODY

Discussing the proposition that a company's dividend policy is irrelevant to its market value

In the recent times, matter pertaining to the influence of firm’s dividend policy on the

current share price level has gained high importance. Now, from corporate officials to investors

as well as economists everyone is concerned about the impact that dividend policies of the firm

have on market value.

Dividend irrelevancy

According to the views of Hamza and Hassan (2017, p1), dividend irrelevance theory

entails that investors are not concerned with the dividend policies employed by the firm.

Moreover, as per such theoretical framework, for fulfilling cash requirements investors can sell

out the part of their equity shares. MM model states that dividend policy is irrelevant in a perfect

world where no taxes and bankruptcy costs take place. However, on the critical note, Wanjohi

(2017, pp.183-205) stated that assumptions undertaken by MM are irrelevant pertaining to the

existence of perfect capital market with no tax implications. Further, such theory is also

criticized as it assumes that wealth of the shareholders not highly influences from dividends. The

rationale behind the same is transaction cost which in turn associated with the selling of shares or

cash inflows. On the basis of this MM theory of irrelevancy, Ali, Mohamad and Baharuddin

Financial management is the process that investors and business units employ for

ensuring effective as well as efficient usage of funds. Attainment of high profit margin is one of

the main objectives of both investors and business organization. With the motive to fulfill the

expectation level of investor’s business unit offers return to the shareholders in the form of

dividend. In the context of business unit, executives and management team plays a vital role in

setting out dividend policy. Hence, in this, report will provide deeper insight about the aspects of

dividend relevancy and irrelevancy. Besides this, it also depicts the manner in which dividend

policy has influence on market value. It also sheds light on the extent to which dividend policies

employed by the firm create agency problem or issues.

MAIN BODY

Discussing the proposition that a company's dividend policy is irrelevant to its market value

In the recent times, matter pertaining to the influence of firm’s dividend policy on the

current share price level has gained high importance. Now, from corporate officials to investors

as well as economists everyone is concerned about the impact that dividend policies of the firm

have on market value.

Dividend irrelevancy

According to the views of Hamza and Hassan (2017, p1), dividend irrelevance theory

entails that investors are not concerned with the dividend policies employed by the firm.

Moreover, as per such theoretical framework, for fulfilling cash requirements investors can sell

out the part of their equity shares. MM model states that dividend policy is irrelevant in a perfect

world where no taxes and bankruptcy costs take place. However, on the critical note, Wanjohi

(2017, pp.183-205) stated that assumptions undertaken by MM are irrelevant pertaining to the

existence of perfect capital market with no tax implications. Further, such theory is also

criticized as it assumes that wealth of the shareholders not highly influences from dividends. The

rationale behind the same is transaction cost which in turn associated with the selling of shares or

cash inflows. On the basis of this MM theory of irrelevancy, Ali, Mohamad and Baharuddin

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(2018) stated that dividend policy has no significant impact on the share prices and capital

structure of the firm. Moreover, MM theory presents that when investors get high dividend then

they are expected or encouraged to invest surplus cash flow in the stock of an organization.

Hence, in accordance with the dividend irrelevancy framework, under perfect market conditions,

investors do not care about return appreciation from dividend or stock price.

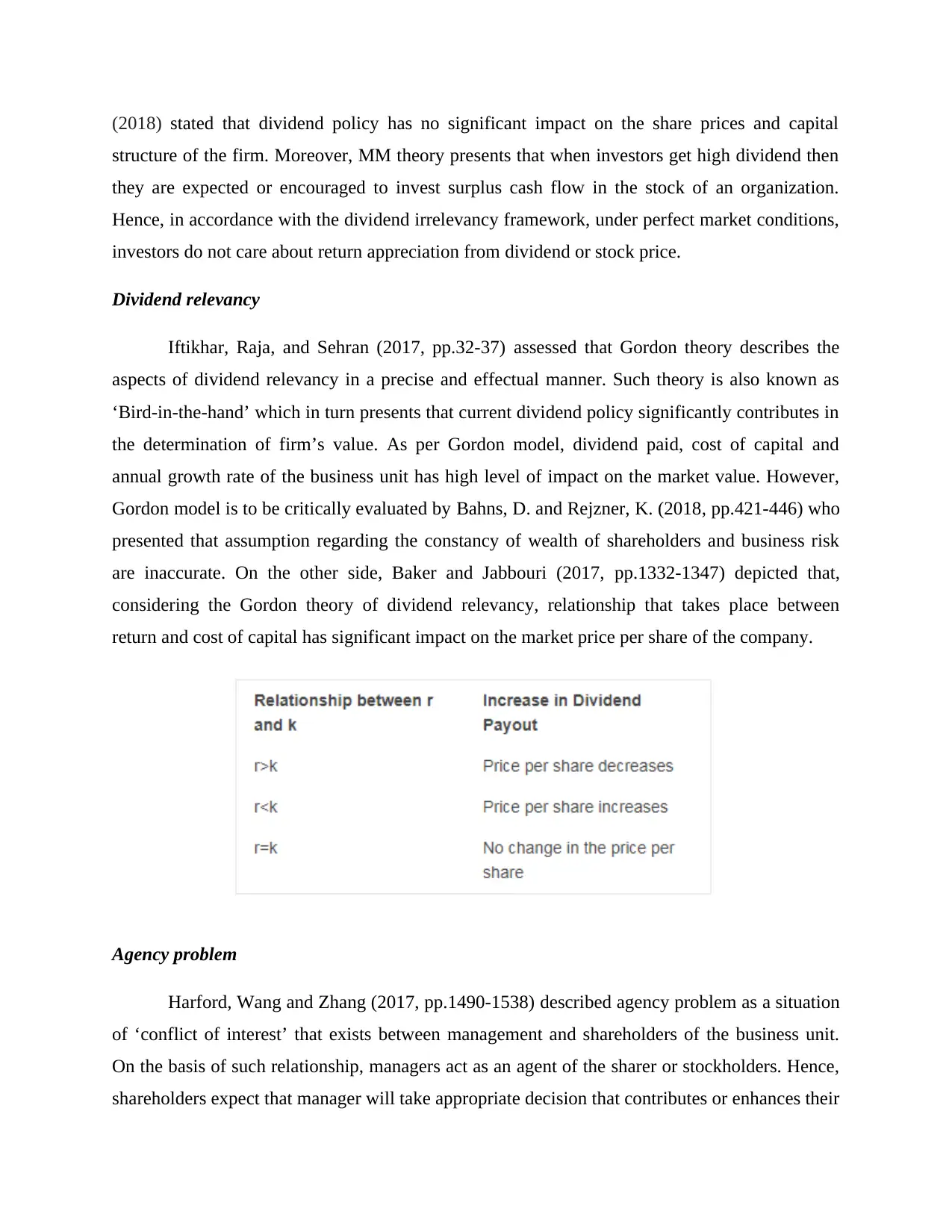

Dividend relevancy

Iftikhar, Raja, and Sehran (2017, pp.32-37) assessed that Gordon theory describes the

aspects of dividend relevancy in a precise and effectual manner. Such theory is also known as

‘Bird-in-the-hand’ which in turn presents that current dividend policy significantly contributes in

the determination of firm’s value. As per Gordon model, dividend paid, cost of capital and

annual growth rate of the business unit has high level of impact on the market value. However,

Gordon model is to be critically evaluated by Bahns, D. and Rejzner, K. (2018, pp.421-446) who

presented that assumption regarding the constancy of wealth of shareholders and business risk

are inaccurate. On the other side, Baker and Jabbouri (2017, pp.1332-1347) depicted that,

considering the Gordon theory of dividend relevancy, relationship that takes place between

return and cost of capital has significant impact on the market price per share of the company.

Agency problem

Harford, Wang and Zhang (2017, pp.1490-1538) described agency problem as a situation

of ‘conflict of interest’ that exists between management and shareholders of the business unit.

On the basis of such relationship, managers act as an agent of the sharer or stockholders. Hence,

shareholders expect that manager will take appropriate decision that contributes or enhances their

structure of the firm. Moreover, MM theory presents that when investors get high dividend then

they are expected or encouraged to invest surplus cash flow in the stock of an organization.

Hence, in accordance with the dividend irrelevancy framework, under perfect market conditions,

investors do not care about return appreciation from dividend or stock price.

Dividend relevancy

Iftikhar, Raja, and Sehran (2017, pp.32-37) assessed that Gordon theory describes the

aspects of dividend relevancy in a precise and effectual manner. Such theory is also known as

‘Bird-in-the-hand’ which in turn presents that current dividend policy significantly contributes in

the determination of firm’s value. As per Gordon model, dividend paid, cost of capital and

annual growth rate of the business unit has high level of impact on the market value. However,

Gordon model is to be critically evaluated by Bahns, D. and Rejzner, K. (2018, pp.421-446) who

presented that assumption regarding the constancy of wealth of shareholders and business risk

are inaccurate. On the other side, Baker and Jabbouri (2017, pp.1332-1347) depicted that,

considering the Gordon theory of dividend relevancy, relationship that takes place between

return and cost of capital has significant impact on the market price per share of the company.

Agency problem

Harford, Wang and Zhang (2017, pp.1490-1538) described agency problem as a situation

of ‘conflict of interest’ that exists between management and shareholders of the business unit.

On the basis of such relationship, managers act as an agent of the sharer or stockholders. Hence,

shareholders expect that manager will take appropriate decision that contributes or enhances their

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

wealth. As per the agency relationship principal (manager) performs task on the behalf of

shareholders. Bebchuk, Cohen and Hirst (2017, pp.89-102) mentioned in their study that agency

problem arises due to the incentive issue. Moreover, agents may be motivated to perform acts in

a undesirable manner or in against to the best interest of shareholder when they provided with the

incentives for acting in a certain way. Sun, et al. (2017, pp.186-199) found that agency problem

can be reduced or eliminated through altering the structure of compensation. In addition to this,

through the means of performance feedback and independent evaluation accountability of the

agents can be ensured for suitable decision making.

Company market value

Market value of the company implies for capitalization that is determined through

multiplying outstanding shares with the current price. In other words, market capitalization refers

to the value of company’s outstanding shares. Investors lay high level of emphasis on

determining the figure of market capitalization with the motive to assess the size of business

operations. Hence, value of market cap or company is highly significant which in turn helps in

attracting more investors.

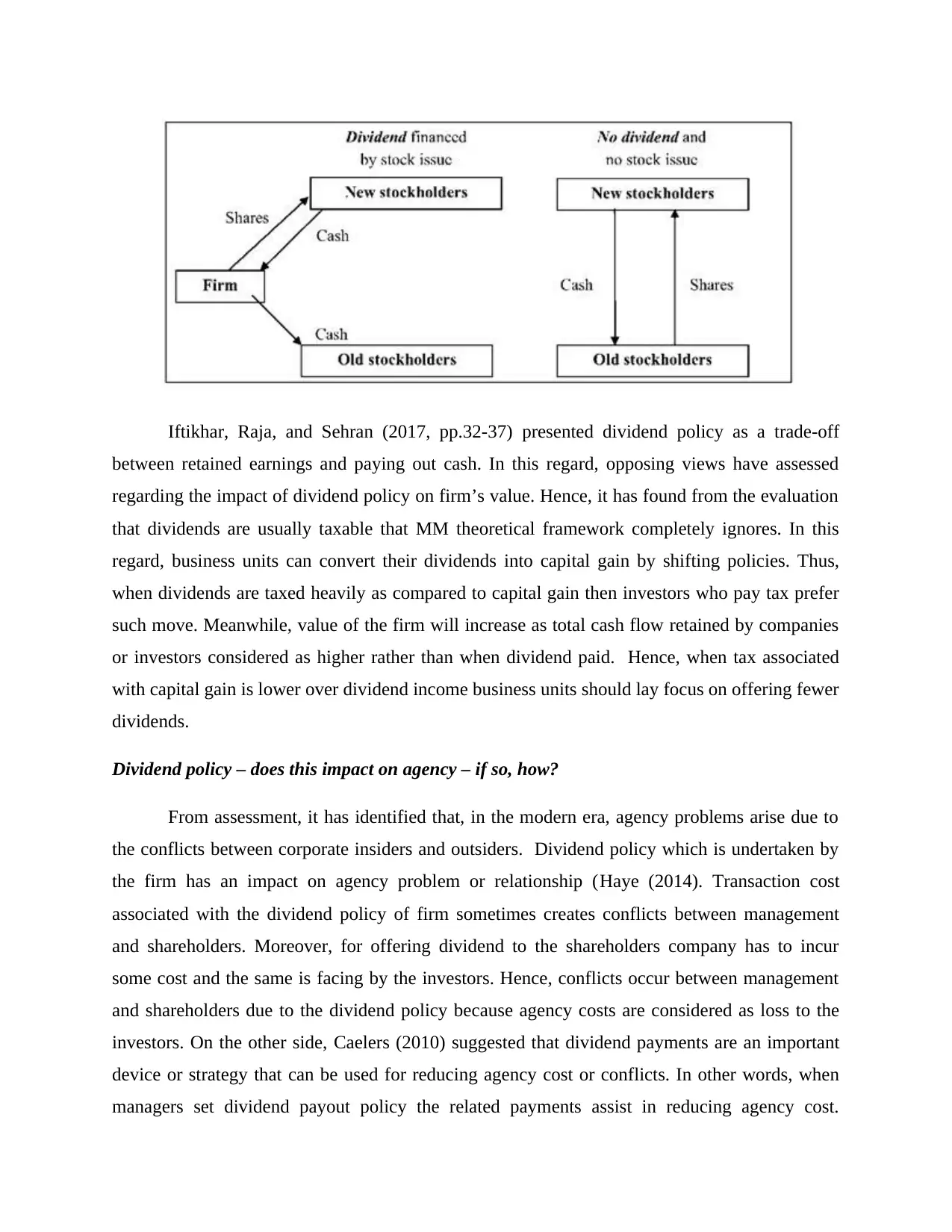

How does a dividend policy affect market value?

MM model is based on some specific assumptions such as no market imperfections, taxes

and transaction cost exists (Ani, 2018). This theoretical framework regarding dividend policy

entails that investors do not need dividend for converting their shares into cash. On the basis of

Miller and Modigliani model investors will not be ready to pay high prices for the firm having

more dividend payouts. MM model or framework states that firm has settled its investment

programme. As per MM model, any surplus from financing decision will be paid out in the form

of dividend. In the case, when firm takes decision in relation to increasing dividend without

changing the debt level then extra returns are financed through the means of equity issue. Hence,

in this, new shareholders contribute with cash in the exchange for new share issuance. Thus,

subsequently, new cash generated is paid out in the form of dividend. Referring such aspect, it

can be depicted that cash is exchanged for the payment of shares so no significant impact takes

place on the value of firm.

shareholders. Bebchuk, Cohen and Hirst (2017, pp.89-102) mentioned in their study that agency

problem arises due to the incentive issue. Moreover, agents may be motivated to perform acts in

a undesirable manner or in against to the best interest of shareholder when they provided with the

incentives for acting in a certain way. Sun, et al. (2017, pp.186-199) found that agency problem

can be reduced or eliminated through altering the structure of compensation. In addition to this,

through the means of performance feedback and independent evaluation accountability of the

agents can be ensured for suitable decision making.

Company market value

Market value of the company implies for capitalization that is determined through

multiplying outstanding shares with the current price. In other words, market capitalization refers

to the value of company’s outstanding shares. Investors lay high level of emphasis on

determining the figure of market capitalization with the motive to assess the size of business

operations. Hence, value of market cap or company is highly significant which in turn helps in

attracting more investors.

How does a dividend policy affect market value?

MM model is based on some specific assumptions such as no market imperfections, taxes

and transaction cost exists (Ani, 2018). This theoretical framework regarding dividend policy

entails that investors do not need dividend for converting their shares into cash. On the basis of

Miller and Modigliani model investors will not be ready to pay high prices for the firm having

more dividend payouts. MM model or framework states that firm has settled its investment

programme. As per MM model, any surplus from financing decision will be paid out in the form

of dividend. In the case, when firm takes decision in relation to increasing dividend without

changing the debt level then extra returns are financed through the means of equity issue. Hence,

in this, new shareholders contribute with cash in the exchange for new share issuance. Thus,

subsequently, new cash generated is paid out in the form of dividend. Referring such aspect, it

can be depicted that cash is exchanged for the payment of shares so no significant impact takes

place on the value of firm.

Iftikhar, Raja, and Sehran (2017, pp.32-37) presented dividend policy as a trade-off

between retained earnings and paying out cash. In this regard, opposing views have assessed

regarding the impact of dividend policy on firm’s value. Hence, it has found from the evaluation

that dividends are usually taxable that MM theoretical framework completely ignores. In this

regard, business units can convert their dividends into capital gain by shifting policies. Thus,

when dividends are taxed heavily as compared to capital gain then investors who pay tax prefer

such move. Meanwhile, value of the firm will increase as total cash flow retained by companies

or investors considered as higher rather than when dividend paid. Hence, when tax associated

with capital gain is lower over dividend income business units should lay focus on offering fewer

dividends.

Dividend policy – does this impact on agency – if so, how?

From assessment, it has identified that, in the modern era, agency problems arise due to

the conflicts between corporate insiders and outsiders. Dividend policy which is undertaken by

the firm has an impact on agency problem or relationship (Haye (2014). Transaction cost

associated with the dividend policy of firm sometimes creates conflicts between management

and shareholders. Moreover, for offering dividend to the shareholders company has to incur

some cost and the same is facing by the investors. Hence, conflicts occur between management

and shareholders due to the dividend policy because agency costs are considered as loss to the

investors. On the other side, Caelers (2010) suggested that dividend payments are an important

device or strategy that can be used for reducing agency cost or conflicts. In other words, when

managers set dividend payout policy the related payments assist in reducing agency cost.

between retained earnings and paying out cash. In this regard, opposing views have assessed

regarding the impact of dividend policy on firm’s value. Hence, it has found from the evaluation

that dividends are usually taxable that MM theoretical framework completely ignores. In this

regard, business units can convert their dividends into capital gain by shifting policies. Thus,

when dividends are taxed heavily as compared to capital gain then investors who pay tax prefer

such move. Meanwhile, value of the firm will increase as total cash flow retained by companies

or investors considered as higher rather than when dividend paid. Hence, when tax associated

with capital gain is lower over dividend income business units should lay focus on offering fewer

dividends.

Dividend policy – does this impact on agency – if so, how?

From assessment, it has identified that, in the modern era, agency problems arise due to

the conflicts between corporate insiders and outsiders. Dividend policy which is undertaken by

the firm has an impact on agency problem or relationship (Haye (2014). Transaction cost

associated with the dividend policy of firm sometimes creates conflicts between management

and shareholders. Moreover, for offering dividend to the shareholders company has to incur

some cost and the same is facing by the investors. Hence, conflicts occur between management

and shareholders due to the dividend policy because agency costs are considered as loss to the

investors. On the other side, Caelers (2010) suggested that dividend payments are an important

device or strategy that can be used for reducing agency cost or conflicts. In other words, when

managers set dividend payout policy the related payments assist in reducing agency cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, it has identified from the evaluation that agency approach is highly moving away from

the assumptions of MM theory or model. Firstly, firm’s investment policy cannot be separated

from its dividend policy because strategy pertaining to paying out dividends may reduce the

efficiency of marginal investment. Secondly, allocation of all the profit margins to the

shareholders cannot be taken for granted. Thus, dividend is paid on a pro-rata basis which in turn

offers benefit to the outsiders relative to retained earnings. However, Parikh (2018) presented in

their study that when dividends are paid then equity of the firm is maintained at its target level

through the issuance of additional common stock. Business units rarely sell equity shares for

offsetting dividend payment and maintaining a constant financial structure. Meanwhile, in

against to the dividend irrelevance assumption policy associated with the same influence asset

composition, capital structure, investment plans and therefore firm’s value.

CONCLUSION

By summing up this, it has been articulated that dividend policy of the firm has

significant impact on the market value of firm. It can be seen in the report that tax is one of the

main factors that have significant influence on the firm’s value. Thus, referring the trend of tax

business units should set dividend policy. Besides this, it can be inferred that the main objective

of firm behind offering dividends to the shareholders is to reduce agency cost especially the one

takes place between management and investors.

the assumptions of MM theory or model. Firstly, firm’s investment policy cannot be separated

from its dividend policy because strategy pertaining to paying out dividends may reduce the

efficiency of marginal investment. Secondly, allocation of all the profit margins to the

shareholders cannot be taken for granted. Thus, dividend is paid on a pro-rata basis which in turn

offers benefit to the outsiders relative to retained earnings. However, Parikh (2018) presented in

their study that when dividends are paid then equity of the firm is maintained at its target level

through the issuance of additional common stock. Business units rarely sell equity shares for

offsetting dividend payment and maintaining a constant financial structure. Meanwhile, in

against to the dividend irrelevance assumption policy associated with the same influence asset

composition, capital structure, investment plans and therefore firm’s value.

CONCLUSION

By summing up this, it has been articulated that dividend policy of the firm has

significant impact on the market value of firm. It can be seen in the report that tax is one of the

main factors that have significant influence on the firm’s value. Thus, referring the trend of tax

business units should set dividend policy. Besides this, it can be inferred that the main objective

of firm behind offering dividends to the shareholders is to reduce agency cost especially the one

takes place between management and investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ali, N. Y., Mohamad, Z. and Baharuddin, N. S. (2018). THE IMPACT OF OWNERSHIP

STRUCTURE ON DIVIDEND POLICY: EVIDENCE OF MALAYSIAN LISTED

FIRMS. Journal of Global Business and Social Entrepreneurship (GBSE), 4(10).

Bahns, D. and Rejzner, K. (2018). The Quantum Sine-Gordon Model in Perturbative

AQFT. Communications in Mathematical Physics, 357(1), pp.421-446.

Baker, H.K. and Jabbouri, I. (2017). How Moroccan institutional investors view dividend

policy. Managerial Finance, 43(12), pp.1332-1347.

Bebchuk, L. A., Cohen, A. and Hirst, S. (2017). The Agency Problems of Institutional

Investors. Journal of Economic Perspectives, 31(3), pp.89-102.

Hamza, S. M. and Hassan, Z. (2017). Impact of dividend policy on shareholders wealth: a

comparative study among dividend paying and non-paying technology based firm’s in

usa. International Journal of Information, Business and Management, 9(3), p.1.

Harford, J., Wang, C. and Zhang, K. (2017). Foreign cash: Taxes, internal capital markets, and

agency problems. The Review of Financial Studies, 30(5), pp.1490-1538.

Haye, E., (2014). Dividend Policy and Agency Effects: A Look at Financial Firms. International

Journal of Economics and Finance, 6(2).

Iftikhar, A. B., Raja, N.U.D.J. and Sehran, K. N. (2017). IMPACT OF DIVIDEND POLICY ON

STOCK PRICES OF FIRM. Theoretical & Applied Science, (3), pp.32-37.

Sun, J. et al. (2017). Principal–principal agency problems and stock price crash risk: Evidence

from the split‐share structure reform in China. Corporate Governance: An International

Review, 25(3), pp.186-199.

Books and Journals

Ali, N. Y., Mohamad, Z. and Baharuddin, N. S. (2018). THE IMPACT OF OWNERSHIP

STRUCTURE ON DIVIDEND POLICY: EVIDENCE OF MALAYSIAN LISTED

FIRMS. Journal of Global Business and Social Entrepreneurship (GBSE), 4(10).

Bahns, D. and Rejzner, K. (2018). The Quantum Sine-Gordon Model in Perturbative

AQFT. Communications in Mathematical Physics, 357(1), pp.421-446.

Baker, H.K. and Jabbouri, I. (2017). How Moroccan institutional investors view dividend

policy. Managerial Finance, 43(12), pp.1332-1347.

Bebchuk, L. A., Cohen, A. and Hirst, S. (2017). The Agency Problems of Institutional

Investors. Journal of Economic Perspectives, 31(3), pp.89-102.

Hamza, S. M. and Hassan, Z. (2017). Impact of dividend policy on shareholders wealth: a

comparative study among dividend paying and non-paying technology based firm’s in

usa. International Journal of Information, Business and Management, 9(3), p.1.

Harford, J., Wang, C. and Zhang, K. (2017). Foreign cash: Taxes, internal capital markets, and

agency problems. The Review of Financial Studies, 30(5), pp.1490-1538.

Haye, E., (2014). Dividend Policy and Agency Effects: A Look at Financial Firms. International

Journal of Economics and Finance, 6(2).

Iftikhar, A. B., Raja, N.U.D.J. and Sehran, K. N. (2017). IMPACT OF DIVIDEND POLICY ON

STOCK PRICES OF FIRM. Theoretical & Applied Science, (3), pp.32-37.

Sun, J. et al. (2017). Principal–principal agency problems and stock price crash risk: Evidence

from the split‐share structure reform in China. Corporate Governance: An International

Review, 25(3), pp.186-199.

Wanjohi, M. M. (2017). Effects of dividend policy on shareholders wealth: Evidence from

insurance firms in the Kenya. International Academic Journal of Economics and

Finance, 2(3), pp.183-205.

Online

Ani, G. (2018). Dividend Irrelevance Theory. Online. Available through: <

http://www.dividend.com/dividend-education/dividend-irrelevance-theory/>. [Accessed on

7th March 2018].

Caelers, L. (2010). The relation between dividend policies and agency conflicts. Online.

Available through: < http://arno.uvt.nl/show.cgi?fid=107724>. [Accessed on 7th March

2018].

Parikh, C. (2018). Dividend Policy and Agency Problems. 2018. Online. Available through: <

https://capitalideasonline.com/wordpress/dividend-policy-and-agency-problems/>. [Accessed

on 7th March 2018].

insurance firms in the Kenya. International Academic Journal of Economics and

Finance, 2(3), pp.183-205.

Online

Ani, G. (2018). Dividend Irrelevance Theory. Online. Available through: <

http://www.dividend.com/dividend-education/dividend-irrelevance-theory/>. [Accessed on

7th March 2018].

Caelers, L. (2010). The relation between dividend policies and agency conflicts. Online.

Available through: < http://arno.uvt.nl/show.cgi?fid=107724>. [Accessed on 7th March

2018].

Parikh, C. (2018). Dividend Policy and Agency Problems. 2018. Online. Available through: <

https://capitalideasonline.com/wordpress/dividend-policy-and-agency-problems/>. [Accessed

on 7th March 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.