Financial Risk Management Report: Economic Impact and Strategies

VerifiedAdded on 2020/06/05

|12

|2656

|51

Report

AI Summary

This report on financial risk management begins with an executive summary highlighting the importance of a competent framework to mitigate undesirable events. It analyzes international and domestic economic conditions, focusing on the impact of the 2008 subprime crisis and its effects on various global economies, including Australia. The report examines the QTC yield curve and forecasts, proposing portfolio transactions such as commercial paper, interest rate swaps, and currency swaps to hedge against risks. It details the execution of portfolio transactions, forecasts of foreign exchange movements, and commodity price predictions, concluding with a discussion of the impact on portfolio composition and asset classes. The report uses data and analysis to support its recommendations and includes references and an appendix with relevant financial data.

FINANCIAL RISK MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Financial risk management is highly associated with the formulation of competent

framework that helps in reducing the level of undesirable events. It can be summarized from the

report that fall in exports and less cost control finally results in curtailment in workforce which

led to decline in demand in nation and elevation in unemployment rate in the countries. Pressure

is observed in the economy of major giants in terms of growth rate. As per latest data, economy

of varied nations contract as their PMI and IIP values are below 50. It can be revealed from the

report that , fixed rate swap will be used so that when interest rate increase benefit of spread

between cash rate and fixed rate of swap can be obtained. Besides this, it can be inferred that

currency swap will be used to hedge position against currency risk. Under this transaction will be

done in the currency swap.

Financial risk management is highly associated with the formulation of competent

framework that helps in reducing the level of undesirable events. It can be summarized from the

report that fall in exports and less cost control finally results in curtailment in workforce which

led to decline in demand in nation and elevation in unemployment rate in the countries. Pressure

is observed in the economy of major giants in terms of growth rate. As per latest data, economy

of varied nations contract as their PMI and IIP values are below 50. It can be revealed from the

report that , fixed rate swap will be used so that when interest rate increase benefit of spread

between cash rate and fixed rate of swap can be obtained. Besides this, it can be inferred that

currency swap will be used to hedge position against currency risk. Under this transaction will be

done in the currency swap.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

International economic condition................................................................................................3

Domestic economic condition.....................................................................................................3

QTC yield curve and forecast and desired positioning of portfolio............................................4

Execution of portfolio transactions..............................................................................................4

Forecast of foreign exchange movement.....................................................................................5

Forecast of commodity price.......................................................................................................5

Proposed portfolio transaction.........................................................................................................5

Strategy........................................................................................................................................5

Quarter 2 deal..................................................................................................................................6

Exposure after confirmed deals.......................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................3

International economic condition................................................................................................3

Domestic economic condition.....................................................................................................3

QTC yield curve and forecast and desired positioning of portfolio............................................4

Execution of portfolio transactions..............................................................................................4

Forecast of foreign exchange movement.....................................................................................5

Forecast of commodity price.......................................................................................................5

Proposed portfolio transaction.........................................................................................................5

Strategy........................................................................................................................................5

Quarter 2 deal..................................................................................................................................6

Exposure after confirmed deals.......................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX....................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial risk assessment is the process which is highly concerned with the identification

of uncertainties associated with the securities. In this, report will provide deeper insight about the

level of GDP during recessionary period and its impact on foreign exchange market.

International economic condition

Subprime crisis originated in the USA in the FY 2008 drastically affect global economy.

USA is the one of the major economy in the world and major importer as well as exporter of

commodity in the market. Giant banks like Layman brothers declared themselves defaulter

which directly affects large and other size corporates in the nation (Santibañez-Aguilar and et.al.,

2016). This news trigger turmoil in the USA economy and due to globalization impact of poor

economic condition of USA is observed on major global economies like UK, Germany, China,

Japan and Russia etc. Consistent erosion of profitability of the firms observed in America and

European continent, due to consistent decline demand from USA. Fall in exports and less cost

control finally results in curtailment in workforce which led to decline in demand in nation and

elevation in unemployment rate in the countries. Pressure is observed in the economy of major

giants in terms of growth rate. As per latest data, economy of varied nations contract as their

PMI and IIP values are below 50 (Liu and et.al., 2017). GDP in these nations declined sharply

and bail out packages and quantitative easing programs are launched to support economy and

people from preventing it from falling in recession. All economic indicators are signaling that

major world economies are struggling to maintain their growth rate in current economic

environment and situation is gradually going out of hands.

Domestic economic condition

GDP decline from 5% to 1.5% from 2008 to 2009 on YOY basis. This is directly

reflecting that economy of Australia is contracting. Within a year growth rate of economy shrink

by huge percentage. Decline in growth rate from 5% to 1.5% reflects that recession have heavy

impact on major industries of Australia. Sharp reduction is observed in growth rate of finance,

business consulting, mining energy and healthcare industry. Impact of this scenario is observed

on unemployment rate where percentage increased from 4% to 5.7%. It can be said that

condition of Australia is critical.

Financial risk assessment is the process which is highly concerned with the identification

of uncertainties associated with the securities. In this, report will provide deeper insight about the

level of GDP during recessionary period and its impact on foreign exchange market.

International economic condition

Subprime crisis originated in the USA in the FY 2008 drastically affect global economy.

USA is the one of the major economy in the world and major importer as well as exporter of

commodity in the market. Giant banks like Layman brothers declared themselves defaulter

which directly affects large and other size corporates in the nation (Santibañez-Aguilar and et.al.,

2016). This news trigger turmoil in the USA economy and due to globalization impact of poor

economic condition of USA is observed on major global economies like UK, Germany, China,

Japan and Russia etc. Consistent erosion of profitability of the firms observed in America and

European continent, due to consistent decline demand from USA. Fall in exports and less cost

control finally results in curtailment in workforce which led to decline in demand in nation and

elevation in unemployment rate in the countries. Pressure is observed in the economy of major

giants in terms of growth rate. As per latest data, economy of varied nations contract as their

PMI and IIP values are below 50 (Liu and et.al., 2017). GDP in these nations declined sharply

and bail out packages and quantitative easing programs are launched to support economy and

people from preventing it from falling in recession. All economic indicators are signaling that

major world economies are struggling to maintain their growth rate in current economic

environment and situation is gradually going out of hands.

Domestic economic condition

GDP decline from 5% to 1.5% from 2008 to 2009 on YOY basis. This is directly

reflecting that economy of Australia is contracting. Within a year growth rate of economy shrink

by huge percentage. Decline in growth rate from 5% to 1.5% reflects that recession have heavy

impact on major industries of Australia. Sharp reduction is observed in growth rate of finance,

business consulting, mining energy and healthcare industry. Impact of this scenario is observed

on unemployment rate where percentage increased from 4% to 5.7%. It can be said that

condition of Australia is critical.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QTC yield curve and forecast and desired positioning of portfolio

Short term: Australia cash rate in 2008 was 7% which reduced to 3.25% in the February

month of 2009. Decline was observed in the interest rate in order to enhance production

and unemployment in the nation. Reduction in interest rates will directly reduce same on

bonds and this will lead to decline in bond value.

Middle curve: Such curve is highly based on the growth level of GDP which in turn

helps investors in assessing the level of return. Moreover, future growth of GDP can

easily be assessed through the means of past indicators. From assessment, it has been

identified that during the quarter of June yield curve is falling down due to having high

mortgage interest rate and less customer spending (Hibbard and et.al., 2016). During such

period, due to the falling in the approval regarding building economy has reached to the

lower level. Further, in 2009, consumer spending level also decreased which in turn

places direct impact on the demand for loans. In the 1st quarter, overall cost of funds

increased to the significant level due to the issuance of 3 to 5 years maturity bonds.

Long end curve: From assessment, it has been identified that long term yield curve is

highly influenced from inflation. By considering such aspect, it can be stated that due to

having slow economic growth rise in inflation level was not expected. Further, by

keeping in mind the condition of 2009 it can be presented that in the 1st quarter of 2009

long term yield increased as compared to last 3 quarters.

Execution of portfolio transactions

Yield curve: From evaluation, it has been assessed that cash rate will be inclined by

RBAS in the upcoming quarters. This in turn pulls long term yield in the upcoming

quarter to a great extent.

Middle curve: Graphical presentation of 2009 clearly shows that decline in export level,

rise in unemployment level etc. are the main causes due to which GDP in the 3rd quarter

decreased. Besides this, it has been found that yield of bonds with 3 to 5 years maturity

will decline in the upcoming time period (Karakaya and Karakaya, 2017).

Long end curve: Outcome of investigation presents that long end curve and inflation is

highly correlated. On the basis of such aspect, if inflation will increase then yield also

inclines in similar direction.

Short term: Australia cash rate in 2008 was 7% which reduced to 3.25% in the February

month of 2009. Decline was observed in the interest rate in order to enhance production

and unemployment in the nation. Reduction in interest rates will directly reduce same on

bonds and this will lead to decline in bond value.

Middle curve: Such curve is highly based on the growth level of GDP which in turn

helps investors in assessing the level of return. Moreover, future growth of GDP can

easily be assessed through the means of past indicators. From assessment, it has been

identified that during the quarter of June yield curve is falling down due to having high

mortgage interest rate and less customer spending (Hibbard and et.al., 2016). During such

period, due to the falling in the approval regarding building economy has reached to the

lower level. Further, in 2009, consumer spending level also decreased which in turn

places direct impact on the demand for loans. In the 1st quarter, overall cost of funds

increased to the significant level due to the issuance of 3 to 5 years maturity bonds.

Long end curve: From assessment, it has been identified that long term yield curve is

highly influenced from inflation. By considering such aspect, it can be stated that due to

having slow economic growth rise in inflation level was not expected. Further, by

keeping in mind the condition of 2009 it can be presented that in the 1st quarter of 2009

long term yield increased as compared to last 3 quarters.

Execution of portfolio transactions

Yield curve: From evaluation, it has been assessed that cash rate will be inclined by

RBAS in the upcoming quarters. This in turn pulls long term yield in the upcoming

quarter to a great extent.

Middle curve: Graphical presentation of 2009 clearly shows that decline in export level,

rise in unemployment level etc. are the main causes due to which GDP in the 3rd quarter

decreased. Besides this, it has been found that yield of bonds with 3 to 5 years maturity

will decline in the upcoming time period (Karakaya and Karakaya, 2017).

Long end curve: Outcome of investigation presents that long end curve and inflation is

highly correlated. On the basis of such aspect, if inflation will increase then yield also

inclines in similar direction.

Forecast of foreign exchange movement

By doing investigation, it has been identified that during the period of 2008 Australian

dollar has performed in an effectual way as compared to US $. From the last 3 quarters, trend of

market is highly volatile which in turn places direct impact on the price level of securities.

Further, it has been assessed that economic condition either good or worst has direct impact on

the value of AUD $. The main examples of foreign exchange movement is that value of AUD $

has fallen down in against to Euro due to the decreasing rate of GDP (Chu and et.al., 2017). This

aspect clearly shows that GDP level has greater influence of the movement of foreign exchange.

Thus, it is suggested to the investors to lay emphasis on hedging aspect. Hence, by making

purchase of foreign currencies in the exchange of Australian dollar investors can reduce the risk

level significantly.

Forecast of commodity price

Below mentioned graphical presentation clearly shows that due to having lower demand

from Asian countries price of copper fallen down from US $ 2500/ton during the quarter of June

to September. Moreover, if the level of production decreases due to slow economic growth then

it has direct impact on the price of copper. Besides this, in the upcoming time period price of

copper will decline. The rationale behind this, US and other developed countries are making their

best efforts in relation to improving the level of GDP. Thus, it is recommended to the investors

to make focus on hedging aspect of copper after the quarter of December.

Proposed portfolio transaction

Strategy 3month commercial paper: Commercial paper are sold in the market to the institutional

investors. Annual inflation rate increased from 2% to 5% in the years 2009 (Australia

inflation rate, 2017). Cash rate is increased to control inflation and it is expected that in

the upcoming time period situation become worse (Li, H and et.al., 2015). Hence, with

increase in inflation it is expected that cash rate will enhanced. Ultimately, yield on bonds

will increased. Thus, short term bond which is commercial paper is issued at 3% interest

rate.

By doing investigation, it has been identified that during the period of 2008 Australian

dollar has performed in an effectual way as compared to US $. From the last 3 quarters, trend of

market is highly volatile which in turn places direct impact on the price level of securities.

Further, it has been assessed that economic condition either good or worst has direct impact on

the value of AUD $. The main examples of foreign exchange movement is that value of AUD $

has fallen down in against to Euro due to the decreasing rate of GDP (Chu and et.al., 2017). This

aspect clearly shows that GDP level has greater influence of the movement of foreign exchange.

Thus, it is suggested to the investors to lay emphasis on hedging aspect. Hence, by making

purchase of foreign currencies in the exchange of Australian dollar investors can reduce the risk

level significantly.

Forecast of commodity price

Below mentioned graphical presentation clearly shows that due to having lower demand

from Asian countries price of copper fallen down from US $ 2500/ton during the quarter of June

to September. Moreover, if the level of production decreases due to slow economic growth then

it has direct impact on the price of copper. Besides this, in the upcoming time period price of

copper will decline. The rationale behind this, US and other developed countries are making their

best efforts in relation to improving the level of GDP. Thus, it is recommended to the investors

to make focus on hedging aspect of copper after the quarter of December.

Proposed portfolio transaction

Strategy 3month commercial paper: Commercial paper are sold in the market to the institutional

investors. Annual inflation rate increased from 2% to 5% in the years 2009 (Australia

inflation rate, 2017). Cash rate is increased to control inflation and it is expected that in

the upcoming time period situation become worse (Li, H and et.al., 2015). Hence, with

increase in inflation it is expected that cash rate will enhanced. Ultimately, yield on bonds

will increased. Thus, short term bond which is commercial paper is issued at 3% interest

rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interest rate swap: Interest rate swap will be used to hedge against interest rate. In the

upcoming time period interest rate will increase and due to this reason there is less

uncertainty. Hence, fixed rate swap will be used so that when interest rate increase

benefit of spread between cash rate and fixed rate of swap can be obtained. Cross currency swap: Currency swap will be used to hedge position against currency

risk. Under this transaction will be done in the currency swap. By doing so against

currency fluctuation will be handled in respect to portfolio.

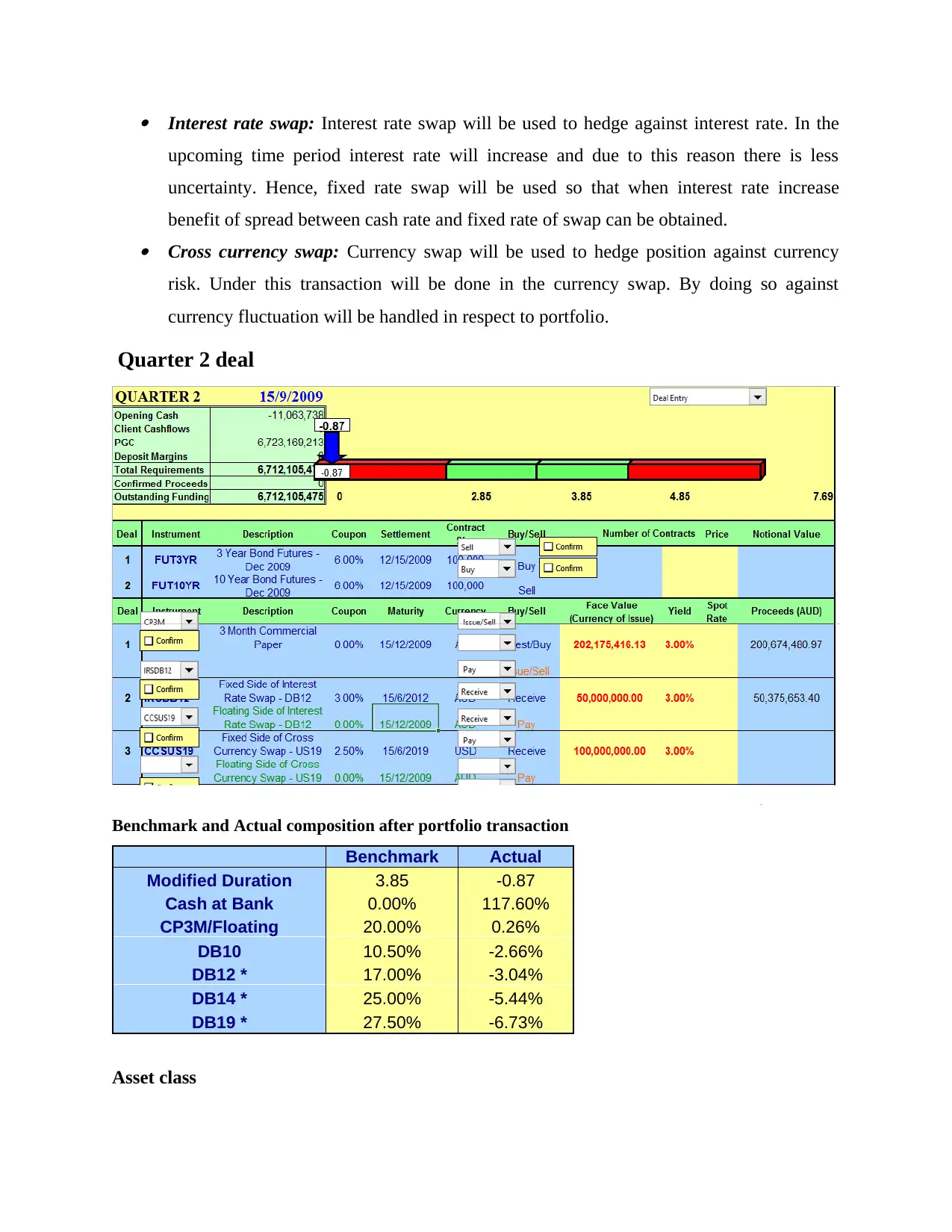

Quarter 2 deal

Benchmark and Actual composition after portfolio transaction

Benchmark Actual

Modified Duration 3.85 -0.87

Cash at Bank 0.00% 117.60%

CP3M/Floating 20.00% 0.26%

DB10 10.50% -2.66%

DB12 * 17.00% -3.04%

DB14 * 25.00% -5.44%

DB19 * 27.50% -6.73%

Asset class

upcoming time period interest rate will increase and due to this reason there is less

uncertainty. Hence, fixed rate swap will be used so that when interest rate increase

benefit of spread between cash rate and fixed rate of swap can be obtained. Cross currency swap: Currency swap will be used to hedge position against currency

risk. Under this transaction will be done in the currency swap. By doing so against

currency fluctuation will be handled in respect to portfolio.

Quarter 2 deal

Benchmark and Actual composition after portfolio transaction

Benchmark Actual

Modified Duration 3.85 -0.87

Cash at Bank 0.00% 117.60%

CP3M/Floating 20.00% 0.26%

DB10 10.50% -2.66%

DB12 * 17.00% -3.04%

DB14 * 25.00% -5.44%

DB19 * 27.50% -6.73%

Asset class

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Facility Class Proportion

Bills 0.00%

Domestic Bonds -14.01%

Eurobonds -3.58%

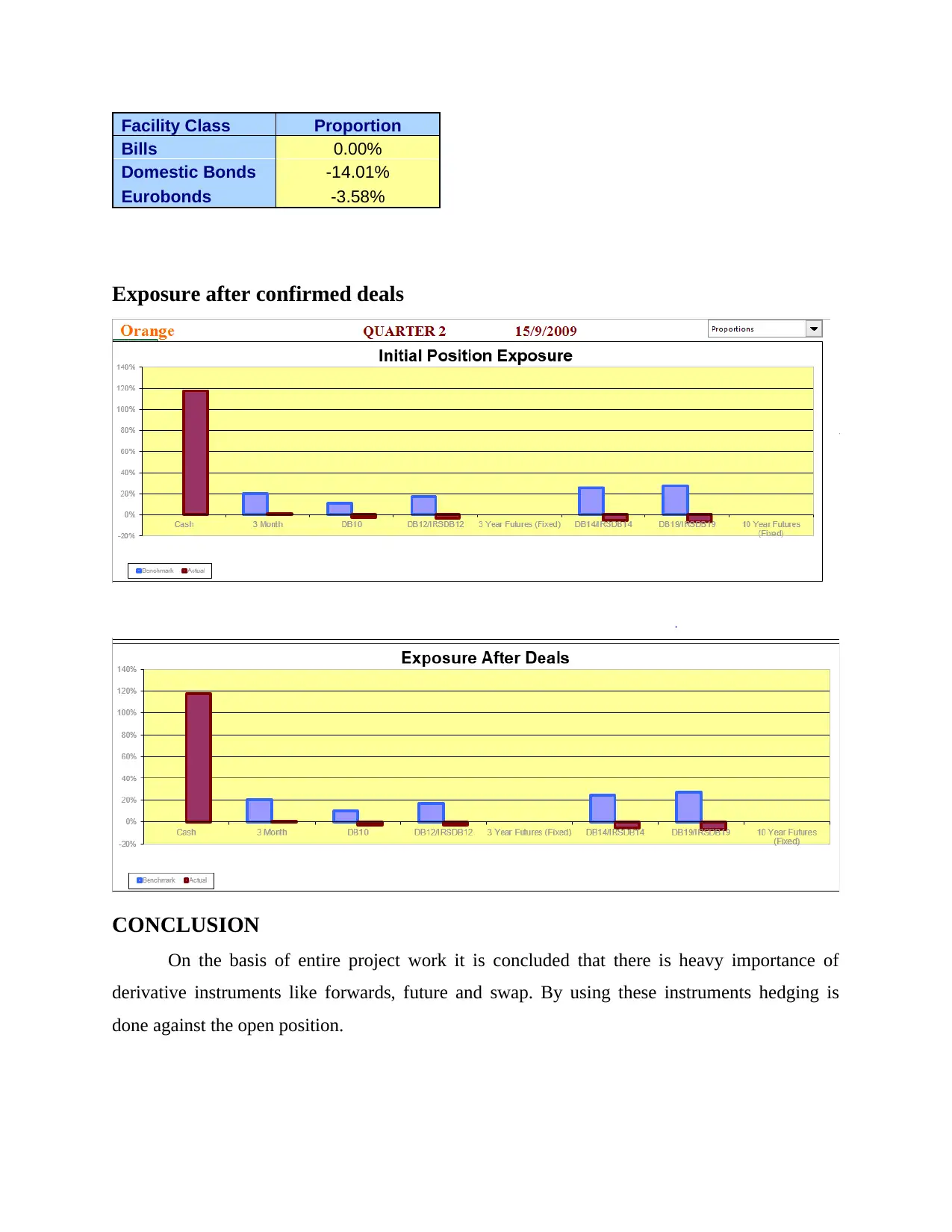

Exposure after confirmed deals

CONCLUSION

On the basis of entire project work it is concluded that there is heavy importance of

derivative instruments like forwards, future and swap. By using these instruments hedging is

done against the open position.

Bills 0.00%

Domestic Bonds -14.01%

Eurobonds -3.58%

Exposure after confirmed deals

CONCLUSION

On the basis of entire project work it is concluded that there is heavy importance of

derivative instruments like forwards, future and swap. By using these instruments hedging is

done against the open position.

REFERENCES

Books and journals

Santibañez-Aguilar, J. E. and et.al., 2016. Financial risk assessment and optimal planning of

biofuels supply chains under uncertainty. BioEnergy Research. 9(4). pp.1053-1069.

Liu, J. and et.al., 2017. Improving risk assessment in financial feasibility of international

engineering projects: A risk driver perspective. International Journal of Project

Management. 35(2). pp.204-211.

Hibbard, J. H. and et.al., 2016. Adding a measure of patient self-management capability to risk

assessment can improve prediction of high costs. Health Affairs. 35(3). pp.489-494.

Karakaya, E. and Karakaya, G., 2017. Developing a Risk Management Framework and Risk

Assessment for Non-profit Organizations: A Case Study. In Risk Management, Strategic

Thinking and Leadership in the Financial Services Industry (pp. 297-308). Springer

International Publishing.

Chu, P. L. and et.al., 2017. Financial analysis and risk assessment of hydroprocessed renewable

jet fuel production from camelina, carinata and used cooking oil. Applied Energy, 198,

pp.401-409.

Li, H. T. and et.al., 2015. A Construction and Empirical Test for Financial Risk

Assessment. International Journal of Economics and Finance. 7(8). p.68.

Online

Australia inflation rate, 2017. [Online]. Available through :<

https://tradingeconomics.com/australia/inflation-cpi>. [Accessed on 8th June 2017].

Books and journals

Santibañez-Aguilar, J. E. and et.al., 2016. Financial risk assessment and optimal planning of

biofuels supply chains under uncertainty. BioEnergy Research. 9(4). pp.1053-1069.

Liu, J. and et.al., 2017. Improving risk assessment in financial feasibility of international

engineering projects: A risk driver perspective. International Journal of Project

Management. 35(2). pp.204-211.

Hibbard, J. H. and et.al., 2016. Adding a measure of patient self-management capability to risk

assessment can improve prediction of high costs. Health Affairs. 35(3). pp.489-494.

Karakaya, E. and Karakaya, G., 2017. Developing a Risk Management Framework and Risk

Assessment for Non-profit Organizations: A Case Study. In Risk Management, Strategic

Thinking and Leadership in the Financial Services Industry (pp. 297-308). Springer

International Publishing.

Chu, P. L. and et.al., 2017. Financial analysis and risk assessment of hydroprocessed renewable

jet fuel production from camelina, carinata and used cooking oil. Applied Energy, 198,

pp.401-409.

Li, H. T. and et.al., 2015. A Construction and Empirical Test for Financial Risk

Assessment. International Journal of Economics and Finance. 7(8). p.68.

Online

Australia inflation rate, 2017. [Online]. Available through :<

https://tradingeconomics.com/australia/inflation-cpi>. [Accessed on 8th June 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

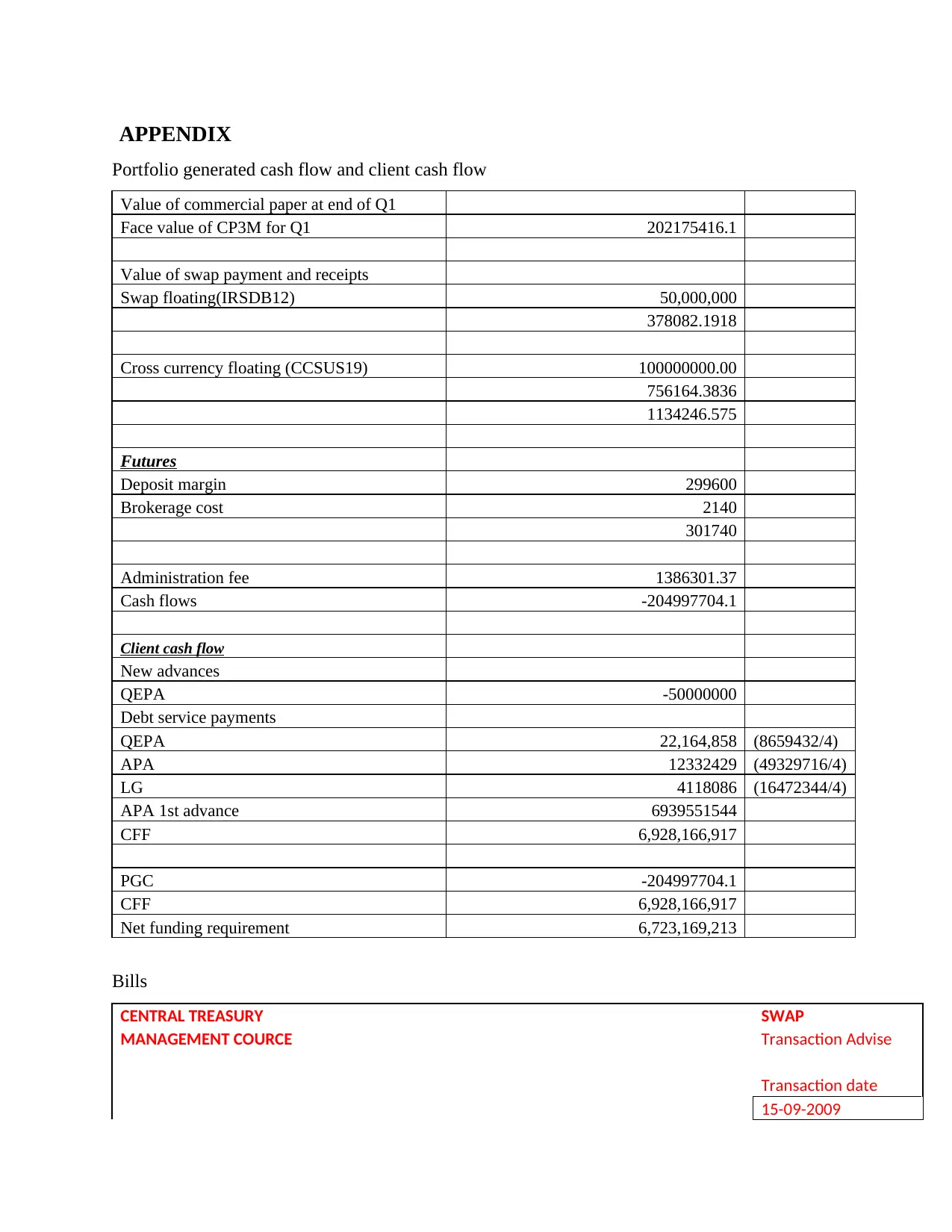

APPENDIX

Portfolio generated cash flow and client cash flow

Value of commercial paper at end of Q1

Face value of CP3M for Q1 202175416.1

Value of swap payment and receipts

Swap floating(IRSDB12) 50,000,000

378082.1918

Cross currency floating (CCSUS19) 100000000.00

756164.3836

1134246.575

Futures

Deposit margin 299600

Brokerage cost 2140

301740

Administration fee 1386301.37

Cash flows -204997704.1

Client cash flow

New advances

QEPA -50000000

Debt service payments

QEPA 22,164,858 (8659432/4)

APA 12332429 (49329716/4)

LG 4118086 (16472344/4)

APA 1st advance 6939551544

CFF 6,928,166,917

PGC -204997704.1

CFF 6,928,166,917

Net funding requirement 6,723,169,213

Bills

CENTRAL TREASURY SWAP

MANAGEMENT COURCE Transaction Advise

Transaction date

15-09-2009

Portfolio generated cash flow and client cash flow

Value of commercial paper at end of Q1

Face value of CP3M for Q1 202175416.1

Value of swap payment and receipts

Swap floating(IRSDB12) 50,000,000

378082.1918

Cross currency floating (CCSUS19) 100000000.00

756164.3836

1134246.575

Futures

Deposit margin 299600

Brokerage cost 2140

301740

Administration fee 1386301.37

Cash flows -204997704.1

Client cash flow

New advances

QEPA -50000000

Debt service payments

QEPA 22,164,858 (8659432/4)

APA 12332429 (49329716/4)

LG 4118086 (16472344/4)

APA 1st advance 6939551544

CFF 6,928,166,917

PGC -204997704.1

CFF 6,928,166,917

Net funding requirement 6,723,169,213

Bills

CENTRAL TREASURY SWAP

MANAGEMENT COURCE Transaction Advise

Transaction date

15-09-2009

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

dd/mm/yy

Security code Fixed Floating

IRSDB12 Yes Pay/Receive 202175416

IRSDB14 Currency AUD

IRSDB19 Face value 50,000,000

CCSUS12 Coupon 3%

CCSUS19 Yield% 3.25%

CCSEUR14 Spot rate 202175416

AUD

proceeds 200674480

Office use only

Deal no Checked

Swap no Entered Signature __________________

Errors

CENTRAL TREASURY SWAP

MANAGEMENT

COURCE Transaction Advise

Transaction date

15-09-2009

dd/mm/yy

Security code Fixed Floating

IRSDB12 Pay/Receive 1,000,000,00

IRSDB14 Currency AUD

IRSDB19 Face value 1,000,000,000

CCSUS12 Coupon 3%

CCSUS19

Ye

s Yield% 3.00%

CCSEUR14 Spot rate 1,000,000,00

AUD

proceeds 200674480

Office use only

Deal no

Checke

d

Swap no Entered Signature

_________________

_

Errors

Security code Fixed Floating

IRSDB12 Yes Pay/Receive 202175416

IRSDB14 Currency AUD

IRSDB19 Face value 50,000,000

CCSUS12 Coupon 3%

CCSUS19 Yield% 3.25%

CCSEUR14 Spot rate 202175416

AUD

proceeds 200674480

Office use only

Deal no Checked

Swap no Entered Signature __________________

Errors

CENTRAL TREASURY SWAP

MANAGEMENT

COURCE Transaction Advise

Transaction date

15-09-2009

dd/mm/yy

Security code Fixed Floating

IRSDB12 Pay/Receive 1,000,000,00

IRSDB14 Currency AUD

IRSDB19 Face value 1,000,000,000

CCSUS12 Coupon 3%

CCSUS19

Ye

s Yield% 3.00%

CCSEUR14 Spot rate 1,000,000,00

AUD

proceeds 200674480

Office use only

Deal no

Checke

d

Swap no Entered Signature

_________________

_

Errors

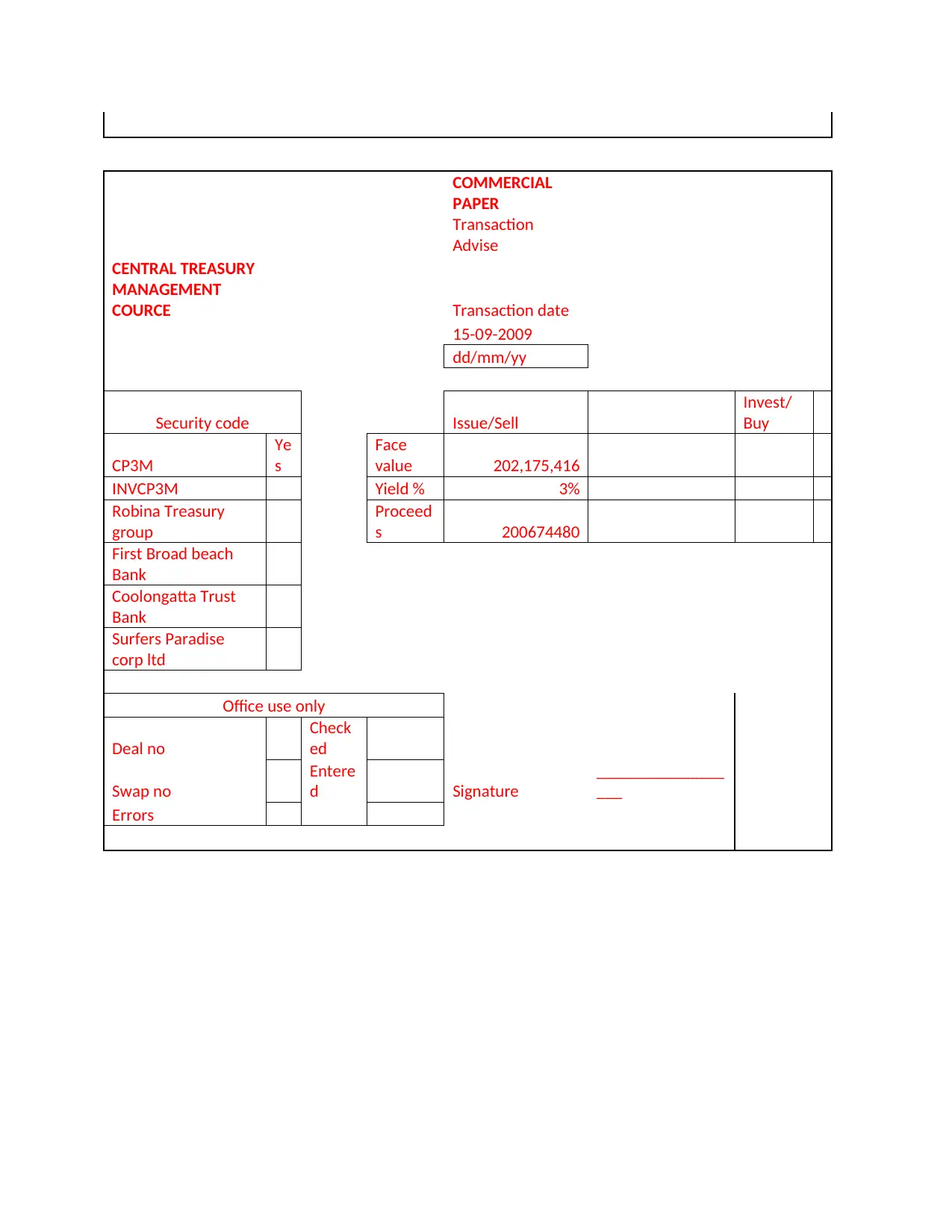

COMMERCIAL

PAPER

Transaction

Advise

CENTRAL TREASURY

MANAGEMENT

COURCE Transaction date

15-09-2009

dd/mm/yy

Security code Issue/Sell

Invest/

Buy

CP3M

Ye

s

Face

value 202,175,416

INVCP3M Yield % 3%

Robina Treasury

group

Proceed

s 200674480

First Broad beach

Bank

Coolongatta Trust

Bank

Surfers Paradise

corp ltd

Office use only

Deal no

Check

ed

Swap no

Entere

d Signature

_______________

___

Errors

PAPER

Transaction

Advise

CENTRAL TREASURY

MANAGEMENT

COURCE Transaction date

15-09-2009

dd/mm/yy

Security code Issue/Sell

Invest/

Buy

CP3M

Ye

s

Face

value 202,175,416

INVCP3M Yield % 3%

Robina Treasury

group

Proceed

s 200674480

First Broad beach

Bank

Coolongatta Trust

Bank

Surfers Paradise

corp ltd

Office use only

Deal no

Check

ed

Swap no

Entere

d Signature

_______________

___

Errors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.