Coursework: FELM4026 Financial and Economic Literacy for Managers

VerifiedAdded on 2023/06/14

|22

|4317

|110

Report

AI Summary

This report provides an analysis of financial and economic literacy for managers, focusing on the UK economy. It examines the growth strategy of Iceland, a UK supermarket chain, highlighting product differentiation, innovation, advertising, convenience, and value. The report also delves into the determinants of housing demand and supply in the UK, discussing the impact of interest rates, mortgage availability, economic growth, and the role of the Bank of England's monetary policy. Furthermore, it assesses key macroeconomic indicators such as Gross Domestic Product (GDP), inflation, and unemployment in the UK, providing insights into the country's economic performance over recent years. The report concludes with answers to specific financial and economic questions, offering a comprehensive overview of the subject matter.

Running Head: FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Financial and Economic Literacy for Managers

Name of the Student

Name of the University

Author note

Financial and Economic Literacy for Managers

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Table of Contents

Answer 1....................................................................................................................................2

Introduction............................................................................................................................2

Iceland; supermarket chain....................................................................................................2

Growth strategy of Iceland.....................................................................................................2

Conclusion..............................................................................................................................5

Answer 2....................................................................................................................................5

Introduction............................................................................................................................5

Determinants of housing demand...........................................................................................5

Determinants of housing supply.............................................................................................6

Monetary policy of Bank of England.....................................................................................7

Conclusion..............................................................................................................................7

Answer 3....................................................................................................................................8

Introduction............................................................................................................................8

Gross Domestic Product.........................................................................................................8

Inflation................................................................................................................................10

Unemployment.....................................................................................................................11

Conclusion............................................................................................................................11

Answer 4..................................................................................................................................11

Answer 5:.................................................................................................................................13

Answer A:............................................................................................................................13

Answer B:.............................................................................................................................15

Answer C:.............................................................................................................................16

References................................................................................................................................17

Table of Contents

Answer 1....................................................................................................................................2

Introduction............................................................................................................................2

Iceland; supermarket chain....................................................................................................2

Growth strategy of Iceland.....................................................................................................2

Conclusion..............................................................................................................................5

Answer 2....................................................................................................................................5

Introduction............................................................................................................................5

Determinants of housing demand...........................................................................................5

Determinants of housing supply.............................................................................................6

Monetary policy of Bank of England.....................................................................................7

Conclusion..............................................................................................................................7

Answer 3....................................................................................................................................8

Introduction............................................................................................................................8

Gross Domestic Product.........................................................................................................8

Inflation................................................................................................................................10

Unemployment.....................................................................................................................11

Conclusion............................................................................................................................11

Answer 4..................................................................................................................................11

Answer 5:.................................................................................................................................13

Answer A:............................................................................................................................13

Answer B:.............................................................................................................................15

Answer C:.............................................................................................................................16

References................................................................................................................................17

2FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Answer 1

Introduction

In the UK economy, along with big enterprises small and medium sized enterprise

hold an important position. These sectors have significant contribution in enhancing

economic growth and provide several Job opportunities. The small and medium sized

business are motivated to invest in innovation to match the level of competition

(smallbusiness.co.uk 2018). Iceland, operating in UK’s supermarket chain though has a

comparatively small share in value chain but has interesting strategies to maintain its unique

place in the supermarket chain. The report analyzes the growth strategy of one of the UK’s

grocery retailer, Iceland.

Iceland; supermarket chain

The Iceland Food Ltd, known by the name Iceland operates in supermarket chain in

UK. The company puts emphasis on selling of frozen food, prepared vegetable and meal.

Apart from this, the company also engages in selling grocery items like meat, dairy and dry

goods. In the supermarket chain of UK, Iceland captures a market share of 2.2%

(iceland.co.uk 2018).

Growth strategy of Iceland

The grocery supermarket in UK has characteristics similar to that of an oligopoly

market. Oligopoly is a market that has few large market players capturing a major share in

the market The four major players in UK supermarkets are Tesco, Morrison, Sainsbury and

Asda (Sparks 2016).

Answer 1

Introduction

In the UK economy, along with big enterprises small and medium sized enterprise

hold an important position. These sectors have significant contribution in enhancing

economic growth and provide several Job opportunities. The small and medium sized

business are motivated to invest in innovation to match the level of competition

(smallbusiness.co.uk 2018). Iceland, operating in UK’s supermarket chain though has a

comparatively small share in value chain but has interesting strategies to maintain its unique

place in the supermarket chain. The report analyzes the growth strategy of one of the UK’s

grocery retailer, Iceland.

Iceland; supermarket chain

The Iceland Food Ltd, known by the name Iceland operates in supermarket chain in

UK. The company puts emphasis on selling of frozen food, prepared vegetable and meal.

Apart from this, the company also engages in selling grocery items like meat, dairy and dry

goods. In the supermarket chain of UK, Iceland captures a market share of 2.2%

(iceland.co.uk 2018).

Growth strategy of Iceland

The grocery supermarket in UK has characteristics similar to that of an oligopoly

market. Oligopoly is a market that has few large market players capturing a major share in

the market The four major players in UK supermarkets are Tesco, Morrison, Sainsbury and

Asda (Sparks 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

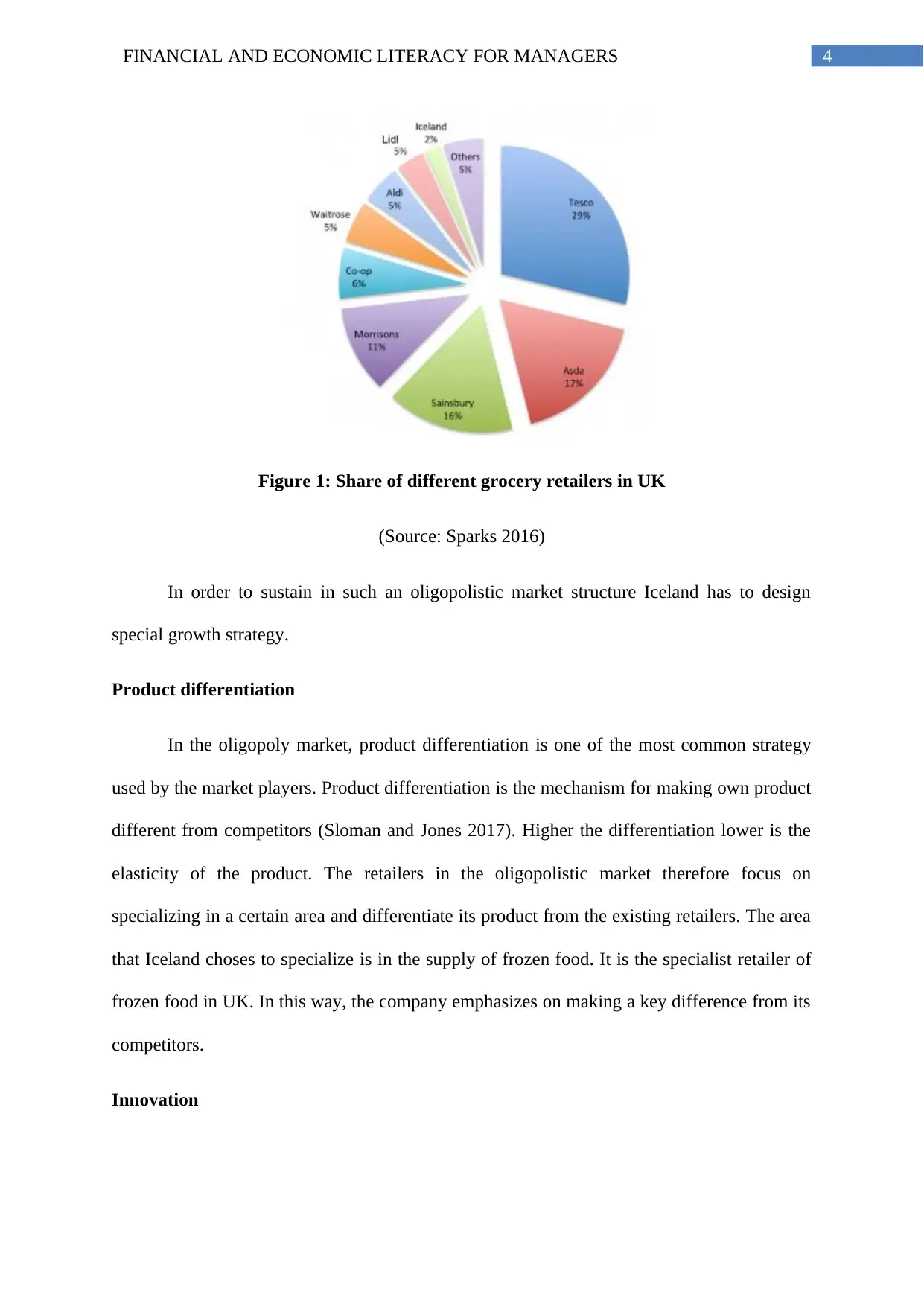

Figure 1: Share of different grocery retailers in UK

(Source: Sparks 2016)

In order to sustain in such an oligopolistic market structure Iceland has to design

special growth strategy.

Product differentiation

In the oligopoly market, product differentiation is one of the most common strategy

used by the market players. Product differentiation is the mechanism for making own product

different from competitors (Sloman and Jones 2017). Higher the differentiation lower is the

elasticity of the product. The retailers in the oligopolistic market therefore focus on

specializing in a certain area and differentiate its product from the existing retailers. The area

that Iceland choses to specialize is in the supply of frozen food. It is the specialist retailer of

frozen food in UK. In this way, the company emphasizes on making a key difference from its

competitors.

Innovation

Figure 1: Share of different grocery retailers in UK

(Source: Sparks 2016)

In order to sustain in such an oligopolistic market structure Iceland has to design

special growth strategy.

Product differentiation

In the oligopoly market, product differentiation is one of the most common strategy

used by the market players. Product differentiation is the mechanism for making own product

different from competitors (Sloman and Jones 2017). Higher the differentiation lower is the

elasticity of the product. The retailers in the oligopolistic market therefore focus on

specializing in a certain area and differentiate its product from the existing retailers. The area

that Iceland choses to specialize is in the supply of frozen food. It is the specialist retailer of

frozen food in UK. In this way, the company emphasizes on making a key difference from its

competitors.

Innovation

5FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

In order to differentiate product, company needs to invest in innovation. Innovation

helps to improve existing product by adding new features to the product. For several years.

Iceland has remained a leading brand in frozen food through extensive investment in

innovation. The company invests in innovation in new product line to satisfy its customers.

Advertising

Advertising is one of important marketing strategy in the oligopoly market. The

customers come to know about new product, specific feature of the product, price offers and

other attractive features of the product. When more and more people have information about

the competitors’ product, the market concentration reduces (Smit and Trigeorgis 2015). In

order to promote it product, Iceland designs marketing campaign. The marketing campaign

known as Power of Frozen to uplift shoppers’ view about frozen food. Overtime the company

has changed its advertising pattern to attract attention of more and more customers. From

initial store based campaign, the company gradually shifts to advertise in TV and in other

social media.

Convenience

Iceland provides a convenient means of shopping to its customers. The frozen food

offered in the stores is easy to cook and involve minimal waste. Customers can easily shop

from the local stores of Iceland whenever needed. The retailers also provide home delivery

service for purchasing above an amount of £20 (iceland.co.uk 2018). Customers can shop

online as per their convenience.

Value

The brand price of Iceland is benchmarked to ensure that it can offer same quality

product at a lower price or offer a combination of a better quality and a relatively low price.

In order to differentiate product, company needs to invest in innovation. Innovation

helps to improve existing product by adding new features to the product. For several years.

Iceland has remained a leading brand in frozen food through extensive investment in

innovation. The company invests in innovation in new product line to satisfy its customers.

Advertising

Advertising is one of important marketing strategy in the oligopoly market. The

customers come to know about new product, specific feature of the product, price offers and

other attractive features of the product. When more and more people have information about

the competitors’ product, the market concentration reduces (Smit and Trigeorgis 2015). In

order to promote it product, Iceland designs marketing campaign. The marketing campaign

known as Power of Frozen to uplift shoppers’ view about frozen food. Overtime the company

has changed its advertising pattern to attract attention of more and more customers. From

initial store based campaign, the company gradually shifts to advertise in TV and in other

social media.

Convenience

Iceland provides a convenient means of shopping to its customers. The frozen food

offered in the stores is easy to cook and involve minimal waste. Customers can easily shop

from the local stores of Iceland whenever needed. The retailers also provide home delivery

service for purchasing above an amount of £20 (iceland.co.uk 2018). Customers can shop

online as per their convenience.

Value

The brand price of Iceland is benchmarked to ensure that it can offer same quality

product at a lower price or offer a combination of a better quality and a relatively low price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Conclusion

Iceland is one of the leading frozen food seller of the UK grocery supermarket. The

company though has a comparatively small share in value chain but has interesting strategies

to maintain its unique place in the supermarket chain. Product differentiation, innovation,

convenience, advertising and value are the focus areas of the concerned company.

Answer 2

Introduction

Real estate market is an integral part of any economy. Price in the housing market is

determined from the interplay of demand and supply side factors. Since 1990s, the UK

housing market has undergone drastic changes (Wilcox and Perry 2014). A major change is

observed in the ownership status of houses, which gradually shifted towards public

ownership through because of intervention of Bank of England and local authorities. The

report briefly discusses demand and supply side factors in UK housing market and the

associated monetary policy of Bank of England.

Determinants of housing demand

Interest rate

One primary determinant of housing demand is the rate of interest for mortgage

repayment. Lower interest rate encourages people to take loan because of a lower cost of

interest. Conversely, during tight monetary policy people have a lower demand for loan. This

intron determines affordability of housing. In 1992, the prevailing interest rate in UK was as

high as 15% (Campbell and Roskelley 2018). In response to high interest rate, the housing

demand declined significantly. However, BOE took a policy of monetary easing during 1990s

and 2000s. This encouraged people to buy more houses.

Conclusion

Iceland is one of the leading frozen food seller of the UK grocery supermarket. The

company though has a comparatively small share in value chain but has interesting strategies

to maintain its unique place in the supermarket chain. Product differentiation, innovation,

convenience, advertising and value are the focus areas of the concerned company.

Answer 2

Introduction

Real estate market is an integral part of any economy. Price in the housing market is

determined from the interplay of demand and supply side factors. Since 1990s, the UK

housing market has undergone drastic changes (Wilcox and Perry 2014). A major change is

observed in the ownership status of houses, which gradually shifted towards public

ownership through because of intervention of Bank of England and local authorities. The

report briefly discusses demand and supply side factors in UK housing market and the

associated monetary policy of Bank of England.

Determinants of housing demand

Interest rate

One primary determinant of housing demand is the rate of interest for mortgage

repayment. Lower interest rate encourages people to take loan because of a lower cost of

interest. Conversely, during tight monetary policy people have a lower demand for loan. This

intron determines affordability of housing. In 1992, the prevailing interest rate in UK was as

high as 15% (Campbell and Roskelley 2018). In response to high interest rate, the housing

demand declined significantly. However, BOE took a policy of monetary easing during 1990s

and 2000s. This encouraged people to buy more houses.

8FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Availability of mortgage

Associated with interest rate, another determinant of housing demand is the

availability of mortgages that is bank’s willingness to lend deposits as mortgage. When bank

offers mortgages with multiple of bigger income then this increases effective demand of

housing. The availability of mortgage varies with interbank strength of the financial sector

(Oliner 2016). During global financial crisis, the economy has experienced a sharp increase

in cost of lending which lead to a decrease in available funds for lending mortgages. This

interrupted housing demand.

Economic growth

In times of economic expansion, people experience a rise in their real income. This

increases housing affordability and hence, housing demand.

Renting cost

If renting cost rises continuously then people have a higher tendency to buy own

house. The mortgage payment might seem cheaper than the renting cost. In housing market of

UK, renting cost if comparatively higher encouraging people to buy new house and thus

boosting demand for housing (Campbell and Roskelley 2018).

Population

The strength of population helps to determine housing demand. Along with

population, the size of household is also important in determining housing demand.

Determinants of housing supply

The effective supply of housing depend on construction of new houses in the

economy. In UK, the number of new house construction varied in different years. During

Availability of mortgage

Associated with interest rate, another determinant of housing demand is the

availability of mortgages that is bank’s willingness to lend deposits as mortgage. When bank

offers mortgages with multiple of bigger income then this increases effective demand of

housing. The availability of mortgage varies with interbank strength of the financial sector

(Oliner 2016). During global financial crisis, the economy has experienced a sharp increase

in cost of lending which lead to a decrease in available funds for lending mortgages. This

interrupted housing demand.

Economic growth

In times of economic expansion, people experience a rise in their real income. This

increases housing affordability and hence, housing demand.

Renting cost

If renting cost rises continuously then people have a higher tendency to buy own

house. The mortgage payment might seem cheaper than the renting cost. In housing market of

UK, renting cost if comparatively higher encouraging people to buy new house and thus

boosting demand for housing (Campbell and Roskelley 2018).

Population

The strength of population helps to determine housing demand. Along with

population, the size of household is also important in determining housing demand.

Determinants of housing supply

The effective supply of housing depend on construction of new houses in the

economy. In UK, the number of new house construction varied in different years. During

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

1960s, the housing market had more than 400,000 new houses per year. This number has

declined to 150,000 in the late 1990s and 2000s (Wilcox and Perry 2014).

One factor contributing to a decline in construction of new houses is restriction placed

on housing planning in land identified as green-belt land. Builders are interested in

constructing new houses only when it seems profitable to them (Oliner 2016). During boom

in housing market, supply of new house increases while in phase of declining housing price,

housing supply declines.

Monetary policy of Bank of England

Bank of England uses monetary policy tools to stabilize housing market and tries to

prevent any crash to occur in the housing market. The BOE regulates banks and interest rate

to control mortgage loan in the property market. In the last few years, the housing price in

UK has risen sharply in response to a higher demand. To restrict housing demand BOE has

imposed a cap on the borrowing. The objective of this cap is to control flow of credit once

housing price rises above expectation (McCrone and Stephens 2017). Banks in UK suffer

severe loss when borrowers are unable to repay loans once the value of the house fell below

the repayment amount. To prevent this, BOE lends money depending on the proportion of

borrowed money to the value of houses. Restriction has also been placed in relation to

income.

Conclusion

The major factors determining housing demand in UK include interest rate,

availability of mortgage, Cost of renting, population, economic growth and income. On the

supply side, the main determining factors are construction of new houses, profitability and

restriction on housing planning. The Bank of England has imposed restriction on borrowing

to control housing demand and housing price.

1960s, the housing market had more than 400,000 new houses per year. This number has

declined to 150,000 in the late 1990s and 2000s (Wilcox and Perry 2014).

One factor contributing to a decline in construction of new houses is restriction placed

on housing planning in land identified as green-belt land. Builders are interested in

constructing new houses only when it seems profitable to them (Oliner 2016). During boom

in housing market, supply of new house increases while in phase of declining housing price,

housing supply declines.

Monetary policy of Bank of England

Bank of England uses monetary policy tools to stabilize housing market and tries to

prevent any crash to occur in the housing market. The BOE regulates banks and interest rate

to control mortgage loan in the property market. In the last few years, the housing price in

UK has risen sharply in response to a higher demand. To restrict housing demand BOE has

imposed a cap on the borrowing. The objective of this cap is to control flow of credit once

housing price rises above expectation (McCrone and Stephens 2017). Banks in UK suffer

severe loss when borrowers are unable to repay loans once the value of the house fell below

the repayment amount. To prevent this, BOE lends money depending on the proportion of

borrowed money to the value of houses. Restriction has also been placed in relation to

income.

Conclusion

The major factors determining housing demand in UK include interest rate,

availability of mortgage, Cost of renting, population, economic growth and income. On the

supply side, the main determining factors are construction of new houses, profitability and

restriction on housing planning. The Bank of England has imposed restriction on borrowing

to control housing demand and housing price.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

11FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Answer 3

Introduction

The key macroeconomic indicators of an economy are Gross Domestic product and

associated growth rate, inflation rate, unemployment rate, interest rate and such others. All

these together determine macroeconomic state of a nation. The report focuses on performance

of key macroeconomic indicators of United Kingdom for the past few years.

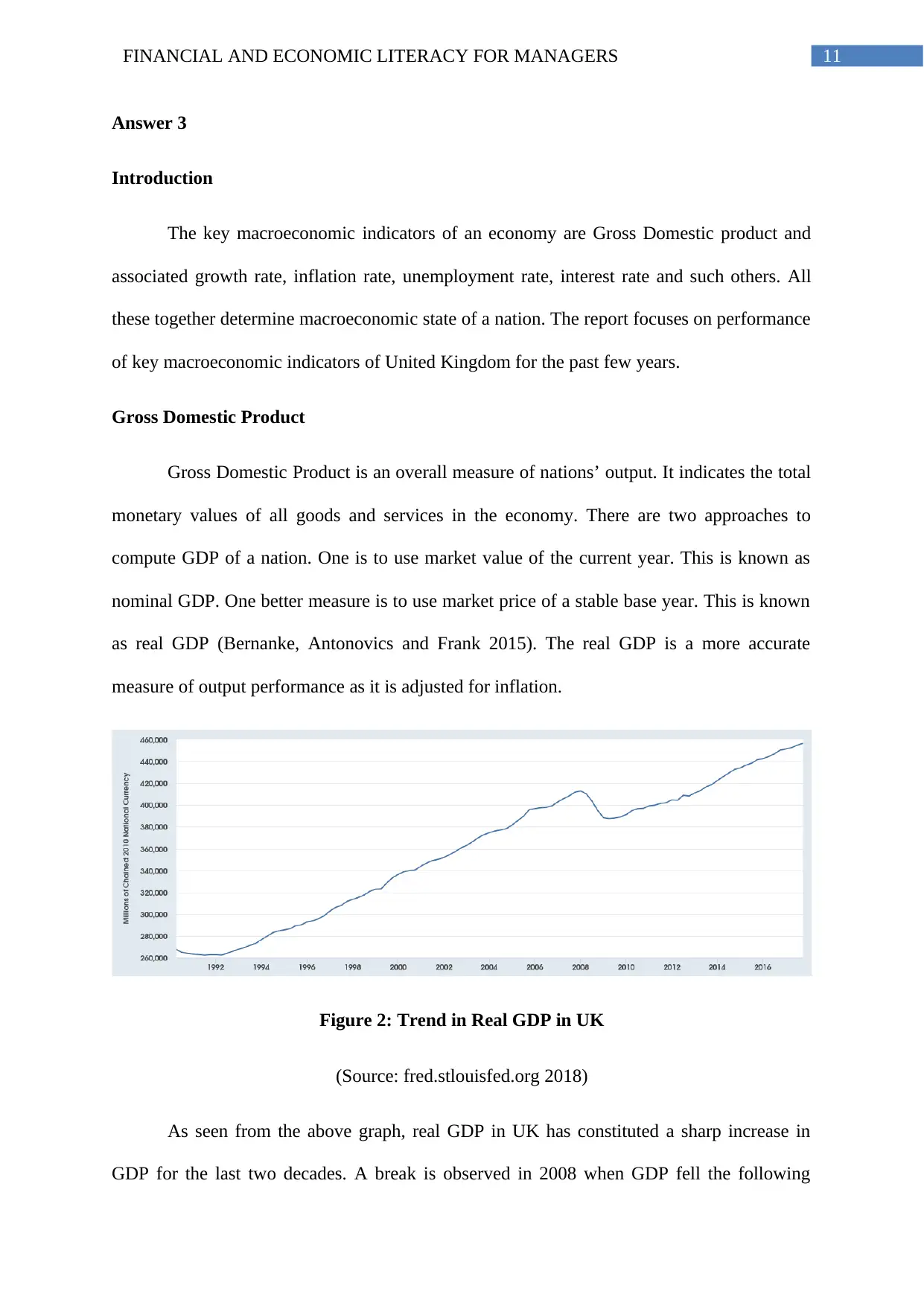

Gross Domestic Product

Gross Domestic Product is an overall measure of nations’ output. It indicates the total

monetary values of all goods and services in the economy. There are two approaches to

compute GDP of a nation. One is to use market value of the current year. This is known as

nominal GDP. One better measure is to use market price of a stable base year. This is known

as real GDP (Bernanke, Antonovics and Frank 2015). The real GDP is a more accurate

measure of output performance as it is adjusted for inflation.

Figure 2: Trend in Real GDP in UK

(Source: fred.stlouisfed.org 2018)

As seen from the above graph, real GDP in UK has constituted a sharp increase in

GDP for the last two decades. A break is observed in 2008 when GDP fell the following

Answer 3

Introduction

The key macroeconomic indicators of an economy are Gross Domestic product and

associated growth rate, inflation rate, unemployment rate, interest rate and such others. All

these together determine macroeconomic state of a nation. The report focuses on performance

of key macroeconomic indicators of United Kingdom for the past few years.

Gross Domestic Product

Gross Domestic Product is an overall measure of nations’ output. It indicates the total

monetary values of all goods and services in the economy. There are two approaches to

compute GDP of a nation. One is to use market value of the current year. This is known as

nominal GDP. One better measure is to use market price of a stable base year. This is known

as real GDP (Bernanke, Antonovics and Frank 2015). The real GDP is a more accurate

measure of output performance as it is adjusted for inflation.

Figure 2: Trend in Real GDP in UK

(Source: fred.stlouisfed.org 2018)

As seen from the above graph, real GDP in UK has constituted a sharp increase in

GDP for the last two decades. A break is observed in 2008 when GDP fell the following

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.