Financial Analysis and Management Enterprise Report - Analysis

VerifiedAdded on 2021/02/19

|22

|5808

|21

Report

AI Summary

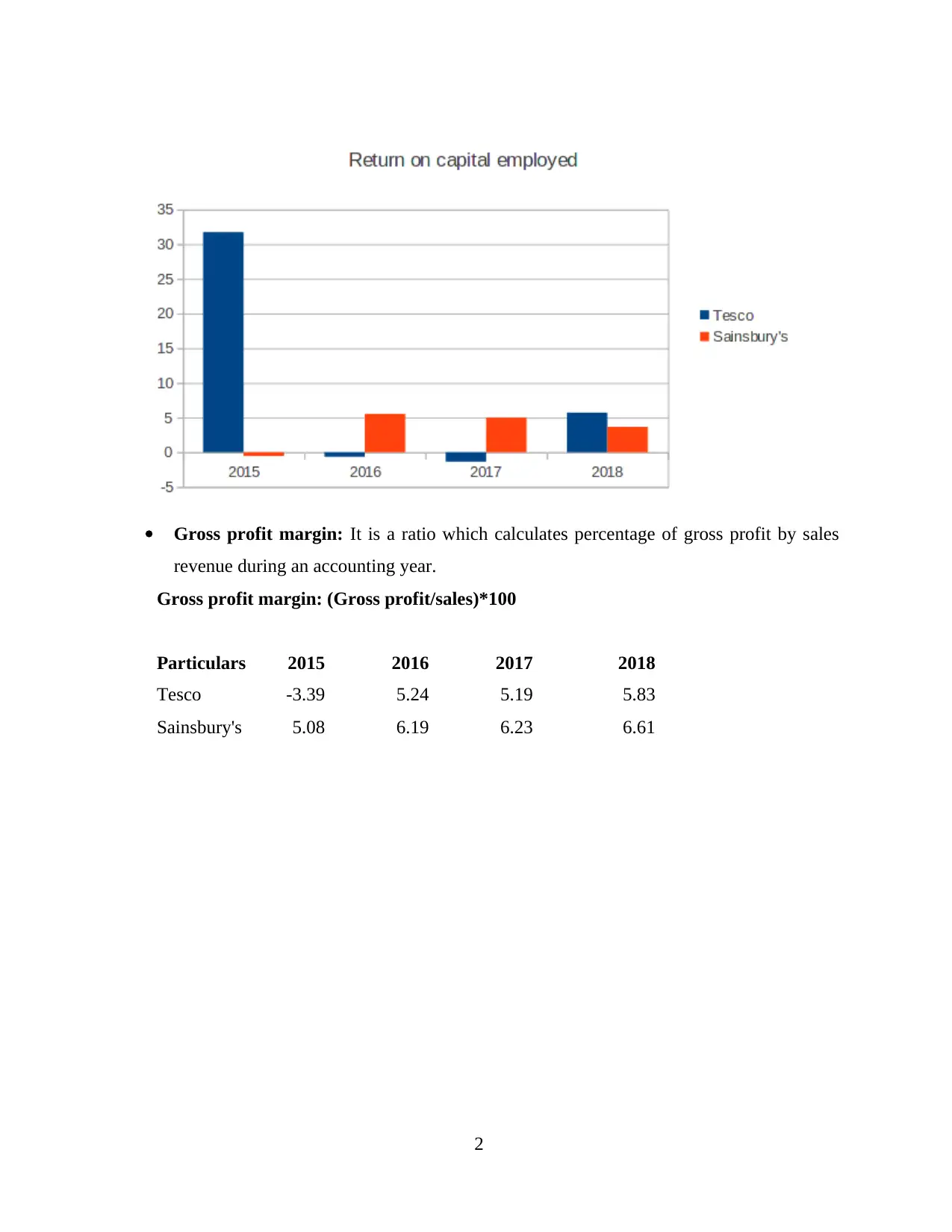

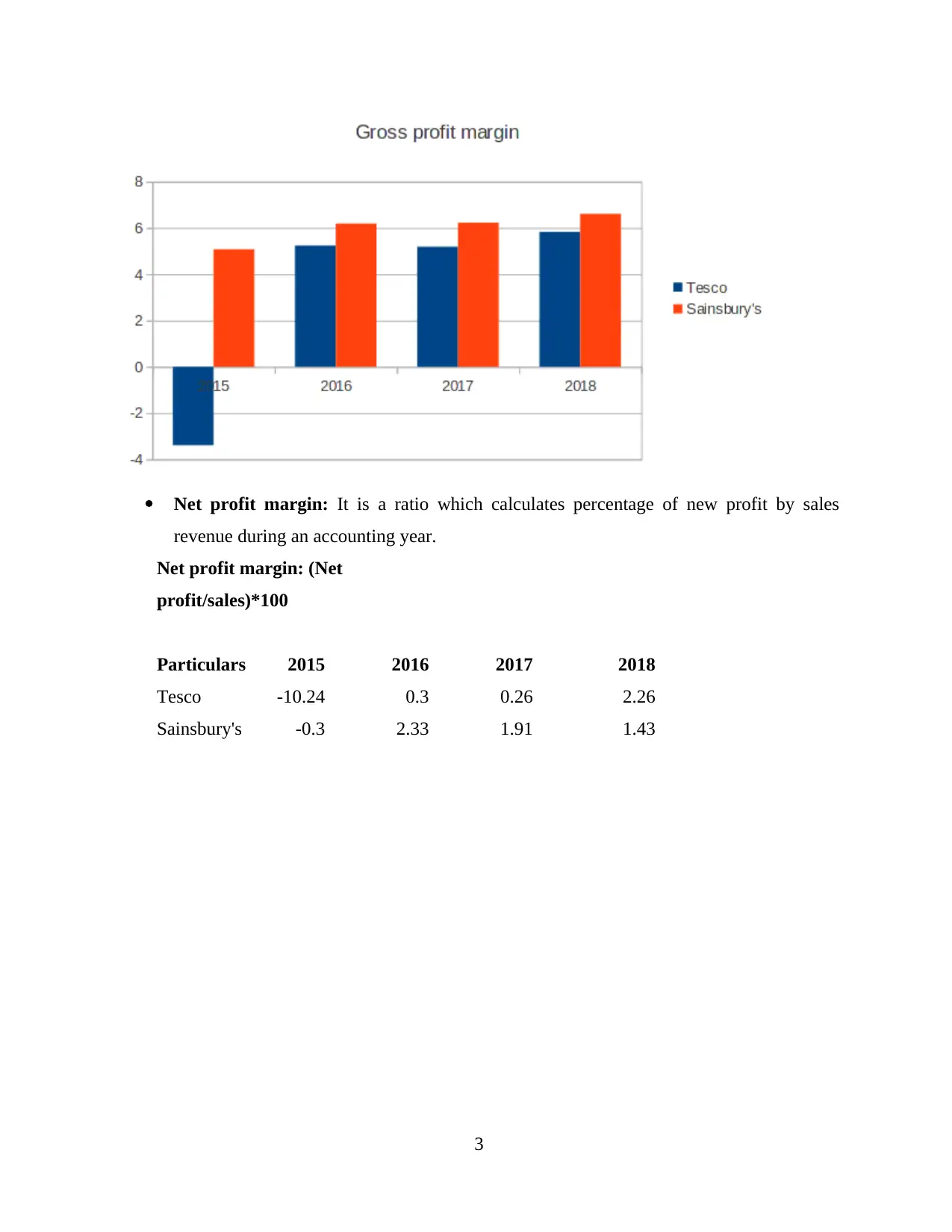

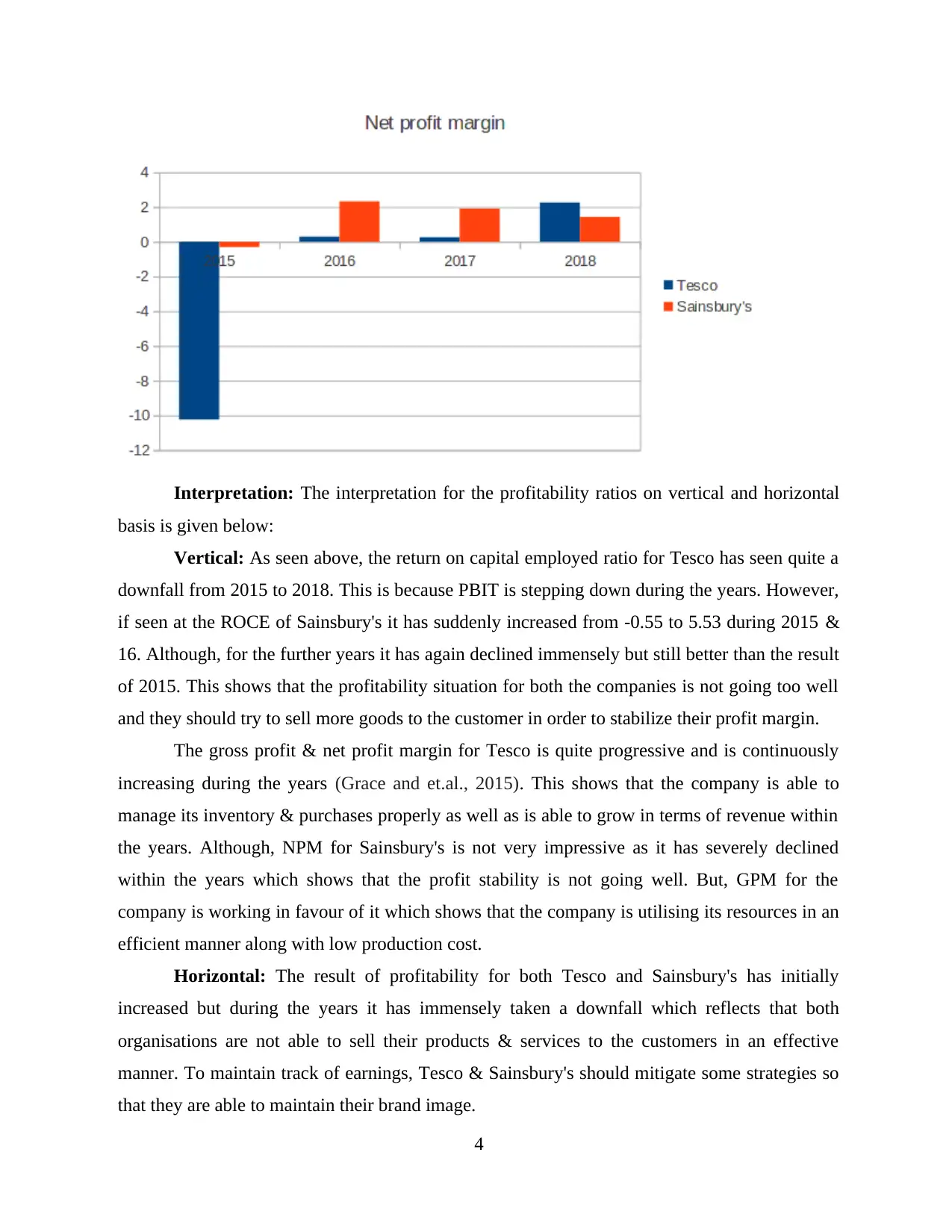

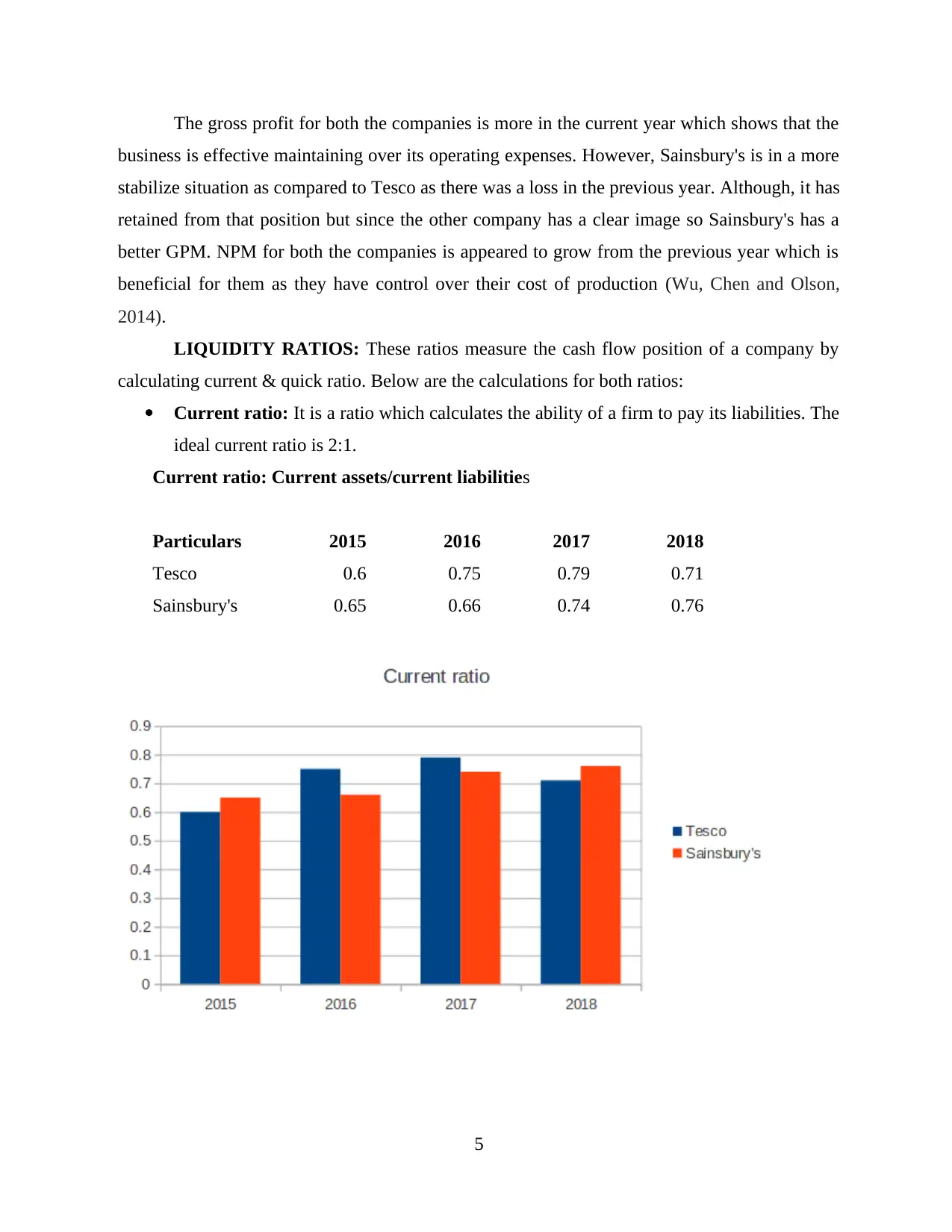

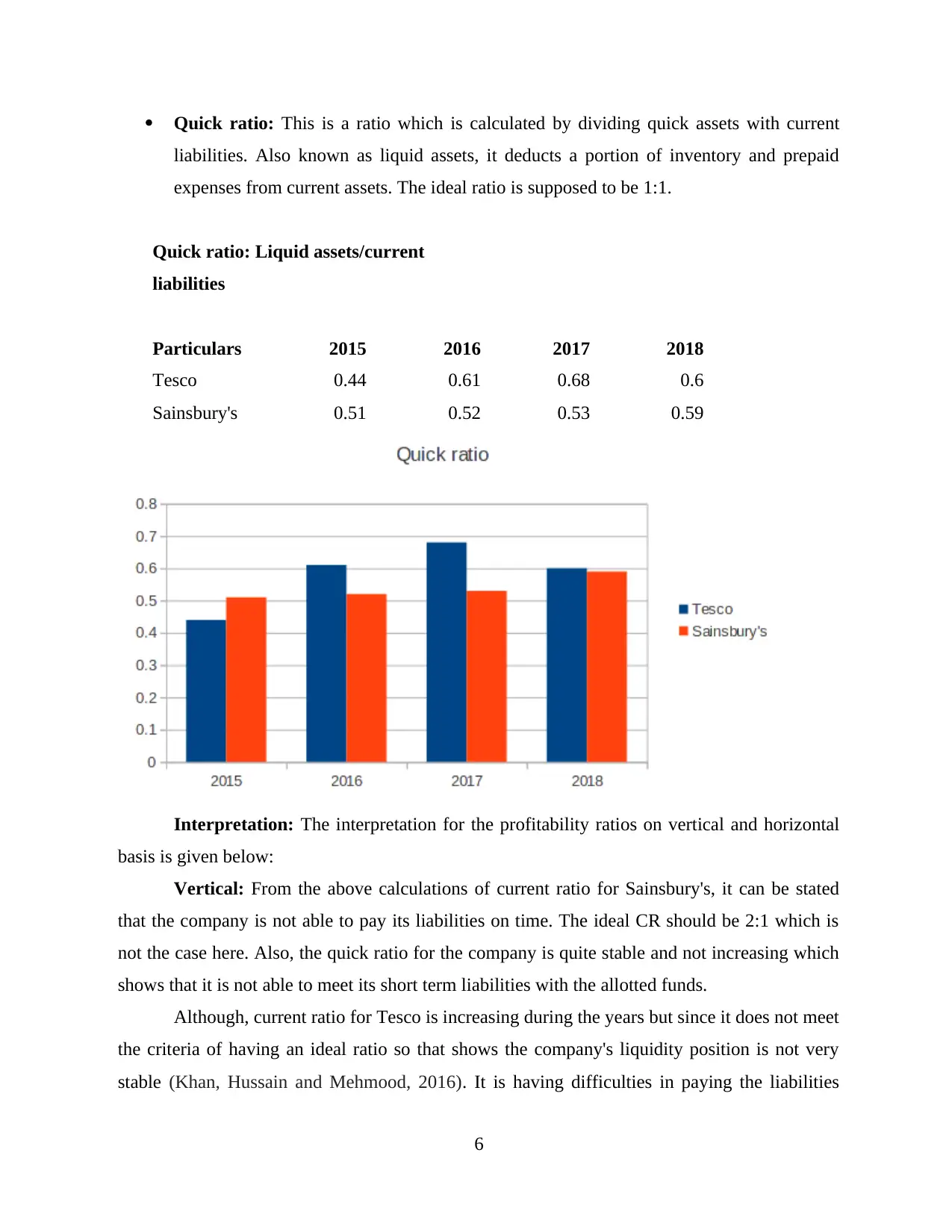

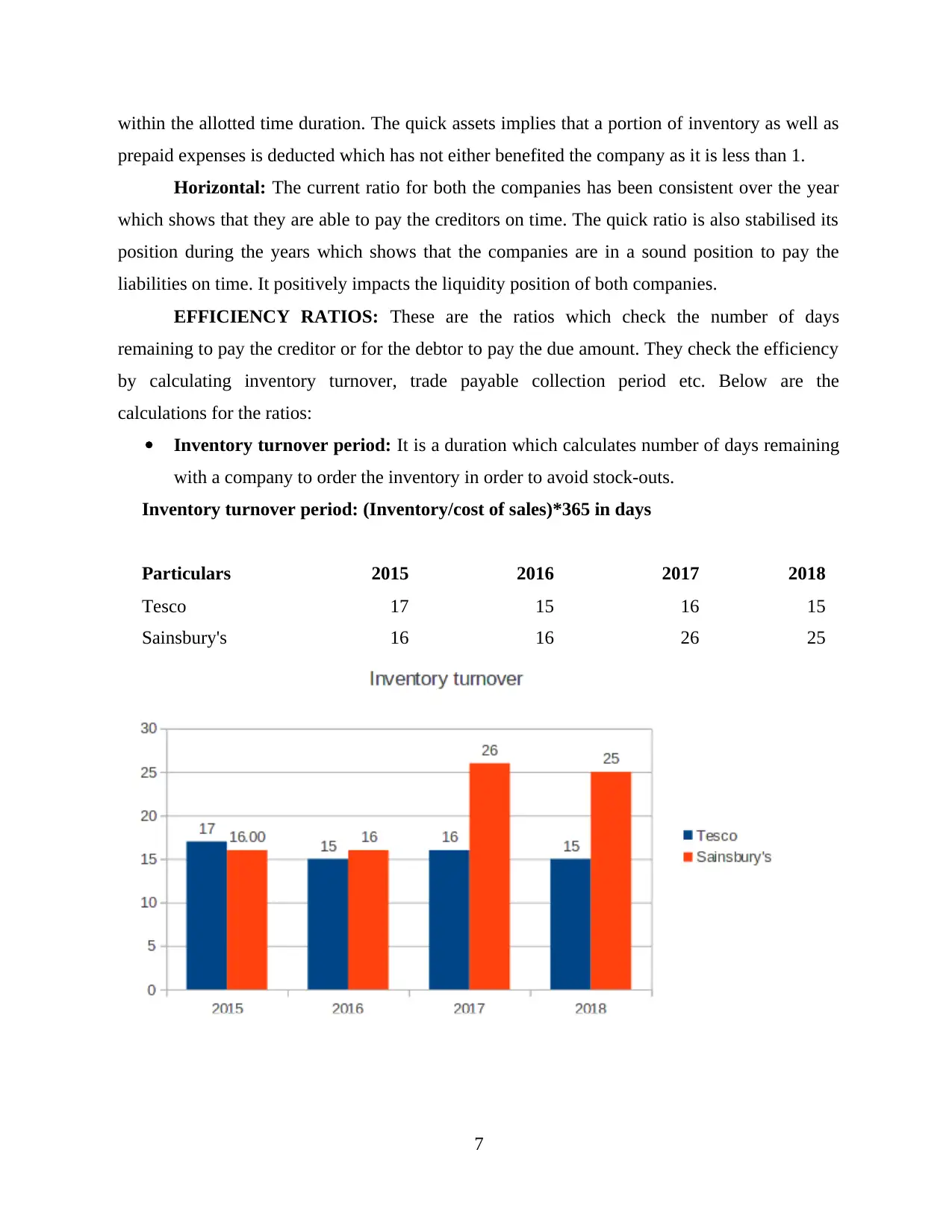

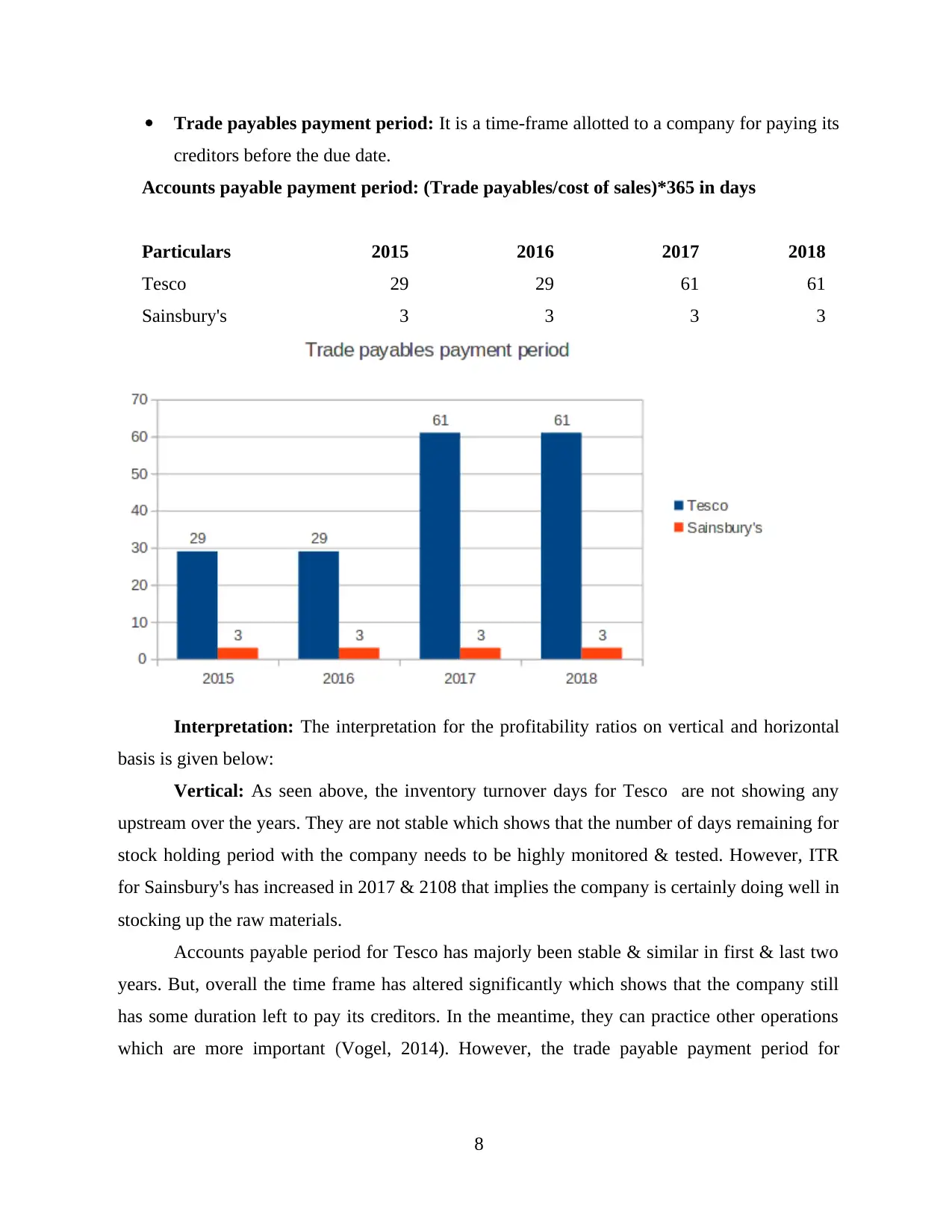

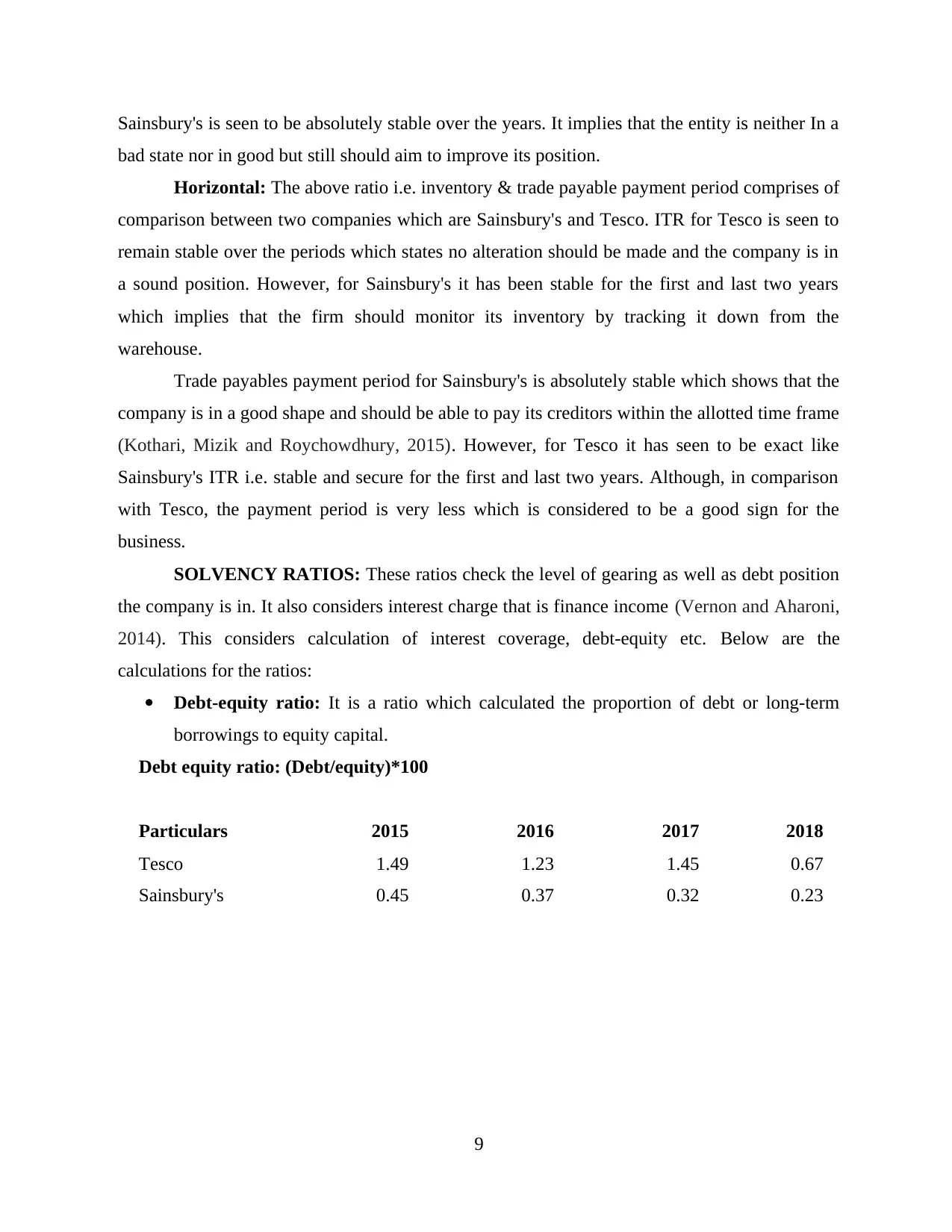

This report presents a financial analysis and management enterprise report, focusing on the comparison of two companies, Tesco and Sainsbury's, through the use of ratio analysis and working capital analysis. The report delves into profitability ratios (ROCE, GPM, NPM), liquidity ratios (current and quick ratios), efficiency ratios (inventory turnover and trade payables payment period), and solvency ratios (debt-equity and interest coverage ratios) to evaluate their financial performance over several years. The analysis includes a vertical and horizontal interpretation of the financial statements, highlighting key trends and providing insights into the companies' financial health. Additionally, the report includes a critical analysis of the cash flow statement, examining the inflows and outflows of cash related to operating, investing, and financing activities. The analysis aims to provide a comprehensive understanding of the companies' financial positions, strengths, and weaknesses, offering valuable information for stakeholders and decision-makers.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.