Financial Management Report: Equity Finance and Capital Budgeting

VerifiedAdded on 2021/02/19

|14

|3749

|18

Report

AI Summary

This report delves into key aspects of financial management, focusing on long-term and equity finance, and investment appraisal techniques. It begins with an introduction to financial management and its role in an organization, emphasizing fund acquisition and effective utilization for profitability. The report then analyzes a rights issue scenario, calculating the number of shares, theoretical ex-right price, and expected earnings per share under different right issue prices, and interpreting the results. It further evaluates the benefits of scrip dividends for companies and shareholders. The report also includes capital budgeting analysis, calculating payback period, accounting rate of return, net present value, and internal rate of return for a project. Finally, it critically evaluates the advantages and disadvantages of capital budgeting techniques, such as net present value and payback period, providing a comprehensive overview of financial decision-making.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction .....................................................................................................................................3

(b).................................................................................................................................................3

1) Number of shares & Theoretical ex-right price ......................................................................3

3) Expected earnings per share....................................................................................................3

4) Forms of issue for each of the right issue price ......................................................................3

(c) Critically evaluating the benefits of the scrip dividends to company and the shareholders . 5

(a) Calculation .............................................................................................................................6

(b) Evaluating the advantages and the disadvantages of the capital budgeting techniques.........9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

(b).................................................................................................................................................3

1) Number of shares & Theoretical ex-right price ......................................................................3

3) Expected earnings per share....................................................................................................3

4) Forms of issue for each of the right issue price ......................................................................3

(c) Critically evaluating the benefits of the scrip dividends to company and the shareholders . 5

(a) Calculation .............................................................................................................................6

(b) Evaluating the advantages and the disadvantages of the capital budgeting techniques.........9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Introduction

Financial management is considered as the organic function of the business organization

as it relates with obtaining the physical resources for carrying out production activities and the

other operations of the business with paying the compensation to suppliers. In other words

financial management refers to the operational activity that focuses on acquisition of the funds,

effective utilization of funds for gaining larger profitability. Financial management is been

viewed as the integral part of an entire management instead of the staff that is concerned with the

raising of the funds within the operation. The present study is based on various aspects of the

financial statements that includes long term finance and the equity finance. Furthermore, it

describes the several investment appraisal tools with its benefits and the limitations.

Question 2

(b)

1) Number of shares & Theoretical ex-right price

EX-right price refers to the market price that the stock theoretically has the new right

issue (kob and Whitby, 2017). It is used by the company in order to offer more shares to the

shareholders at the discounted price.

3) Expected earnings per share

Earning per share is been computed by dividing the profits of the company with that of

the outstanding shares (Price and Williams, 2018). The resultant outcome reflect the profitability

of an enterprise. It is common for the organization to report for the earning per share which is

been adjusted for the potential dilution of the shares and the extraordinary items.

4) Forms of issue for each of the right issue price

Right issue refers to the right that is given by the company to its existing shareholders for

raising the additional capital (Mateus, Farinha and Soares, 2017). Right issue price is the price at

which the new shares are been issued is less than the market price that is prevailing in the

market. In other words, it means that the shares are issued at discount rate.

Particulars Amount (£)

Current market value of Brand (6,00,000*1.90) 11,40,000

Financial management is considered as the organic function of the business organization

as it relates with obtaining the physical resources for carrying out production activities and the

other operations of the business with paying the compensation to suppliers. In other words

financial management refers to the operational activity that focuses on acquisition of the funds,

effective utilization of funds for gaining larger profitability. Financial management is been

viewed as the integral part of an entire management instead of the staff that is concerned with the

raising of the funds within the operation. The present study is based on various aspects of the

financial statements that includes long term finance and the equity finance. Furthermore, it

describes the several investment appraisal tools with its benefits and the limitations.

Question 2

(b)

1) Number of shares & Theoretical ex-right price

EX-right price refers to the market price that the stock theoretically has the new right

issue (kob and Whitby, 2017). It is used by the company in order to offer more shares to the

shareholders at the discounted price.

3) Expected earnings per share

Earning per share is been computed by dividing the profits of the company with that of

the outstanding shares (Price and Williams, 2018). The resultant outcome reflect the profitability

of an enterprise. It is common for the organization to report for the earning per share which is

been adjusted for the potential dilution of the shares and the extraordinary items.

4) Forms of issue for each of the right issue price

Right issue refers to the right that is given by the company to its existing shareholders for

raising the additional capital (Mateus, Farinha and Soares, 2017). Right issue price is the price at

which the new shares are been issued is less than the market price that is prevailing in the

market. In other words, it means that the shares are issued at discount rate.

Particulars Amount (£)

Current market value of Brand (6,00,000*1.90) 11,40,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Funds to be raised through right issue 1,800000

Final market value 13,20,000

Particulars Amount (£)

Earnings before rights issue (700000*0.2) 1,40,000

Earnings from new funds (1,80,000*0.2) 36000

Total earnings after rights issue 1,76,000

Particulars Right issue price at 1.80

Number of new shares (180000/1.80) 1,00,000

Total shares in issue (600000+100000) 7,00,000

Theoretical ex- rights price (1320000/700000) £1.89 per share

New EPS =100*(176000/700000) 25.14 price per share

Form of rights issue (600000/100000) 6, i.e 1 for shares 6

Particulars Right issue price at 1.60

Number of new shares (180000/1.60) 1,12,500

Total shares in issue (600000+112500) 7,12,500

Theoretical ex- rights price (1320000/712500) £1.85 per share

New EPS =100*(176000/712500) 24.7 price per share

Form of rights issue (600000/112500) 5.33, i.e 1 for shares 5.33

Final market value 13,20,000

Particulars Amount (£)

Earnings before rights issue (700000*0.2) 1,40,000

Earnings from new funds (1,80,000*0.2) 36000

Total earnings after rights issue 1,76,000

Particulars Right issue price at 1.80

Number of new shares (180000/1.80) 1,00,000

Total shares in issue (600000+100000) 7,00,000

Theoretical ex- rights price (1320000/700000) £1.89 per share

New EPS =100*(176000/700000) 25.14 price per share

Form of rights issue (600000/100000) 6, i.e 1 for shares 6

Particulars Right issue price at 1.60

Number of new shares (180000/1.60) 1,12,500

Total shares in issue (600000+112500) 7,12,500

Theoretical ex- rights price (1320000/712500) £1.85 per share

New EPS =100*(176000/712500) 24.7 price per share

Form of rights issue (600000/112500) 5.33, i.e 1 for shares 5.33

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

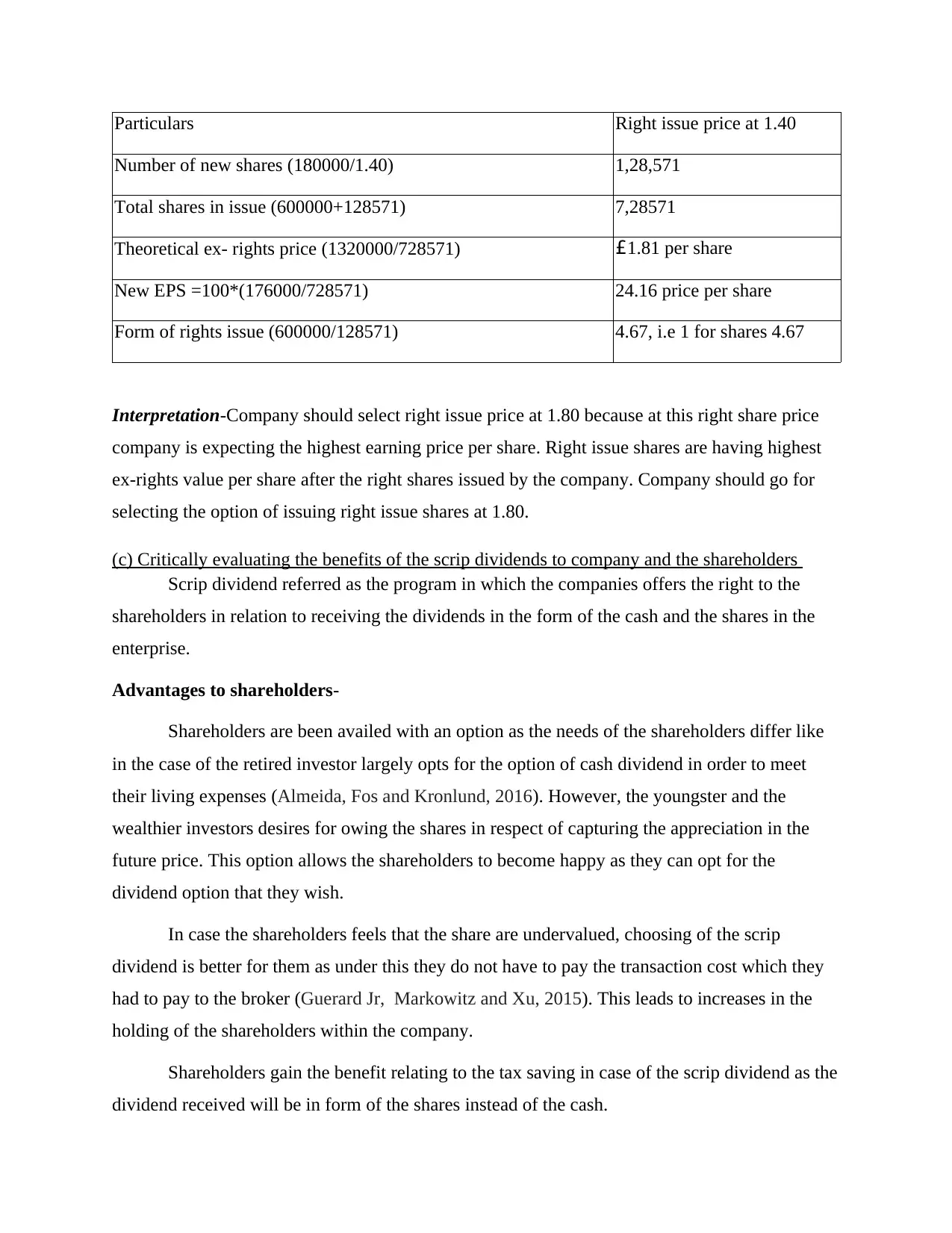

Particulars Right issue price at 1.40

Number of new shares (180000/1.40) 1,28,571

Total shares in issue (600000+128571) 7,28571

Theoretical ex- rights price (1320000/728571) £1.81 per share

New EPS =100*(176000/728571) 24.16 price per share

Form of rights issue (600000/128571) 4.67, i.e 1 for shares 4.67

Interpretation-Company should select right issue price at 1.80 because at this right share price

company is expecting the highest earning price per share. Right issue shares are having highest

ex-rights value per share after the right shares issued by the company. Company should go for

selecting the option of issuing right issue shares at 1.80.

(c) Critically evaluating the benefits of the scrip dividends to company and the shareholders

Scrip dividend referred as the program in which the companies offers the right to the

shareholders in relation to receiving the dividends in the form of the cash and the shares in the

enterprise.

Advantages to shareholders-

Shareholders are been availed with an option as the needs of the shareholders differ like

in the case of the retired investor largely opts for the option of cash dividend in order to meet

their living expenses (Almeida, Fos and Kronlund, 2016). However, the youngster and the

wealthier investors desires for owing the shares in respect of capturing the appreciation in the

future price. This option allows the shareholders to become happy as they can opt for the

dividend option that they wish.

In case the shareholders feels that the share are undervalued, choosing of the scrip

dividend is better for them as under this they do not have to pay the transaction cost which they

had to pay to the broker (Guerard Jr, Markowitz and Xu, 2015). This leads to increases in the

holding of the shareholders within the company.

Shareholders gain the benefit relating to the tax saving in case of the scrip dividend as the

dividend received will be in form of the shares instead of the cash.

Number of new shares (180000/1.40) 1,28,571

Total shares in issue (600000+128571) 7,28571

Theoretical ex- rights price (1320000/728571) £1.81 per share

New EPS =100*(176000/728571) 24.16 price per share

Form of rights issue (600000/128571) 4.67, i.e 1 for shares 4.67

Interpretation-Company should select right issue price at 1.80 because at this right share price

company is expecting the highest earning price per share. Right issue shares are having highest

ex-rights value per share after the right shares issued by the company. Company should go for

selecting the option of issuing right issue shares at 1.80.

(c) Critically evaluating the benefits of the scrip dividends to company and the shareholders

Scrip dividend referred as the program in which the companies offers the right to the

shareholders in relation to receiving the dividends in the form of the cash and the shares in the

enterprise.

Advantages to shareholders-

Shareholders are been availed with an option as the needs of the shareholders differ like

in the case of the retired investor largely opts for the option of cash dividend in order to meet

their living expenses (Almeida, Fos and Kronlund, 2016). However, the youngster and the

wealthier investors desires for owing the shares in respect of capturing the appreciation in the

future price. This option allows the shareholders to become happy as they can opt for the

dividend option that they wish.

In case the shareholders feels that the share are undervalued, choosing of the scrip

dividend is better for them as under this they do not have to pay the transaction cost which they

had to pay to the broker (Guerard Jr, Markowitz and Xu, 2015). This leads to increases in the

holding of the shareholders within the company.

Shareholders gain the benefit relating to the tax saving in case of the scrip dividend as the

dividend received will be in form of the shares instead of the cash.

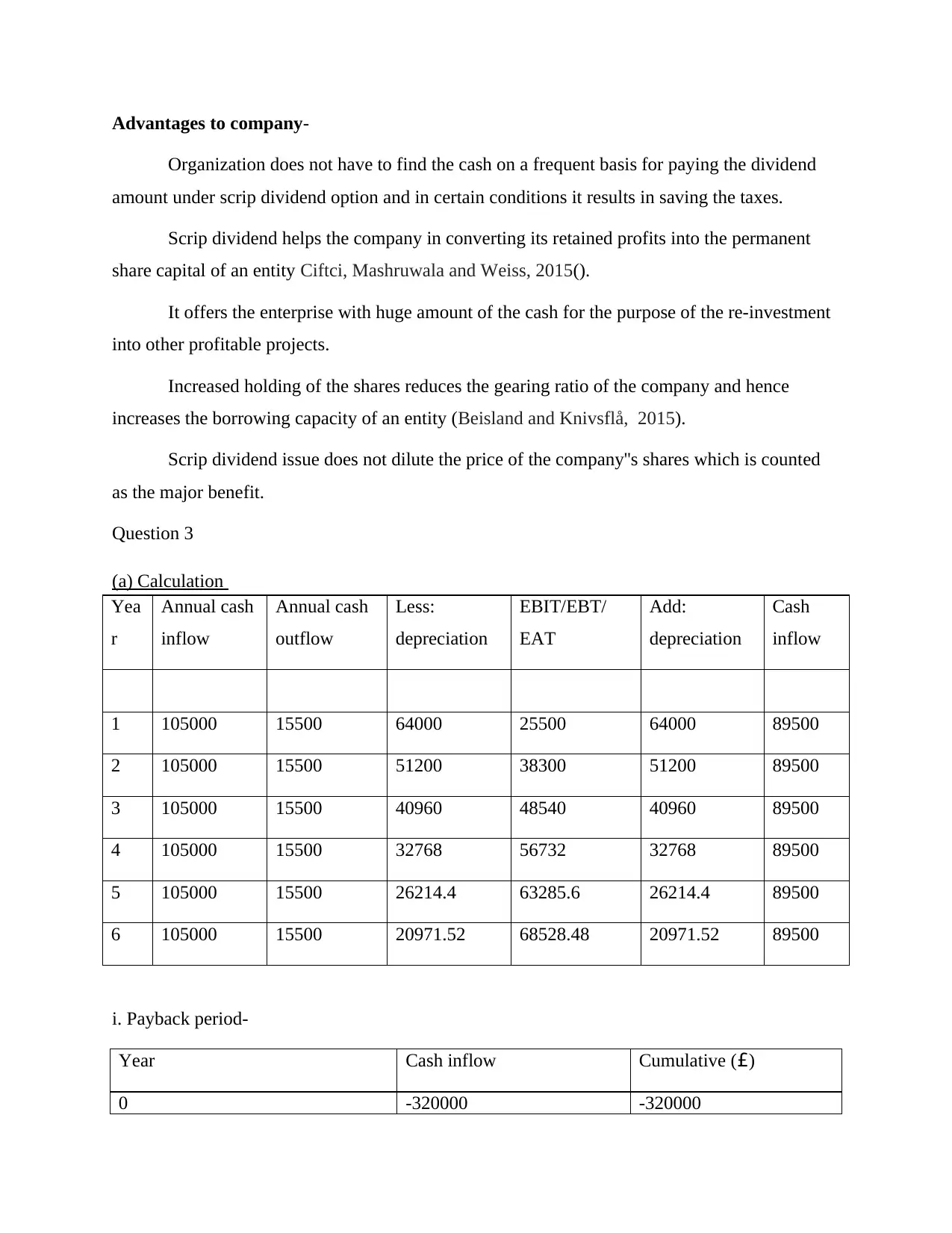

Advantages to company-

Organization does not have to find the cash on a frequent basis for paying the dividend

amount under scrip dividend option and in certain conditions it results in saving the taxes.

Scrip dividend helps the company in converting its retained profits into the permanent

share capital of an entity Ciftci, Mashruwala and Weiss, 2015().

It offers the enterprise with huge amount of the cash for the purpose of the re-investment

into other profitable projects.

Increased holding of the shares reduces the gearing ratio of the company and hence

increases the borrowing capacity of an entity (Beisland and Knivsflå, 2015).

Scrip dividend issue does not dilute the price of the company''s shares which is counted

as the major benefit.

Question 3

(a) Calculation

Yea

r

Annual cash

inflow

Annual cash

outflow

Less:

depreciation

EBIT/EBT/

EAT

Add:

depreciation

Cash

inflow

1 105000 15500 64000 25500 64000 89500

2 105000 15500 51200 38300 51200 89500

3 105000 15500 40960 48540 40960 89500

4 105000 15500 32768 56732 32768 89500

5 105000 15500 26214.4 63285.6 26214.4 89500

6 105000 15500 20971.52 68528.48 20971.52 89500

i. Payback period-

Year Cash inflow Cumulative (£)

0 -320000 -320000

Organization does not have to find the cash on a frequent basis for paying the dividend

amount under scrip dividend option and in certain conditions it results in saving the taxes.

Scrip dividend helps the company in converting its retained profits into the permanent

share capital of an entity Ciftci, Mashruwala and Weiss, 2015().

It offers the enterprise with huge amount of the cash for the purpose of the re-investment

into other profitable projects.

Increased holding of the shares reduces the gearing ratio of the company and hence

increases the borrowing capacity of an entity (Beisland and Knivsflå, 2015).

Scrip dividend issue does not dilute the price of the company''s shares which is counted

as the major benefit.

Question 3

(a) Calculation

Yea

r

Annual cash

inflow

Annual cash

outflow

Less:

depreciation

EBIT/EBT/

EAT

Add:

depreciation

Cash

inflow

1 105000 15500 64000 25500 64000 89500

2 105000 15500 51200 38300 51200 89500

3 105000 15500 40960 48540 40960 89500

4 105000 15500 32768 56732 32768 89500

5 105000 15500 26214.4 63285.6 26214.4 89500

6 105000 15500 20971.52 68528.48 20971.52 89500

i. Payback period-

Year Cash inflow Cumulative (£)

0 -320000 -320000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

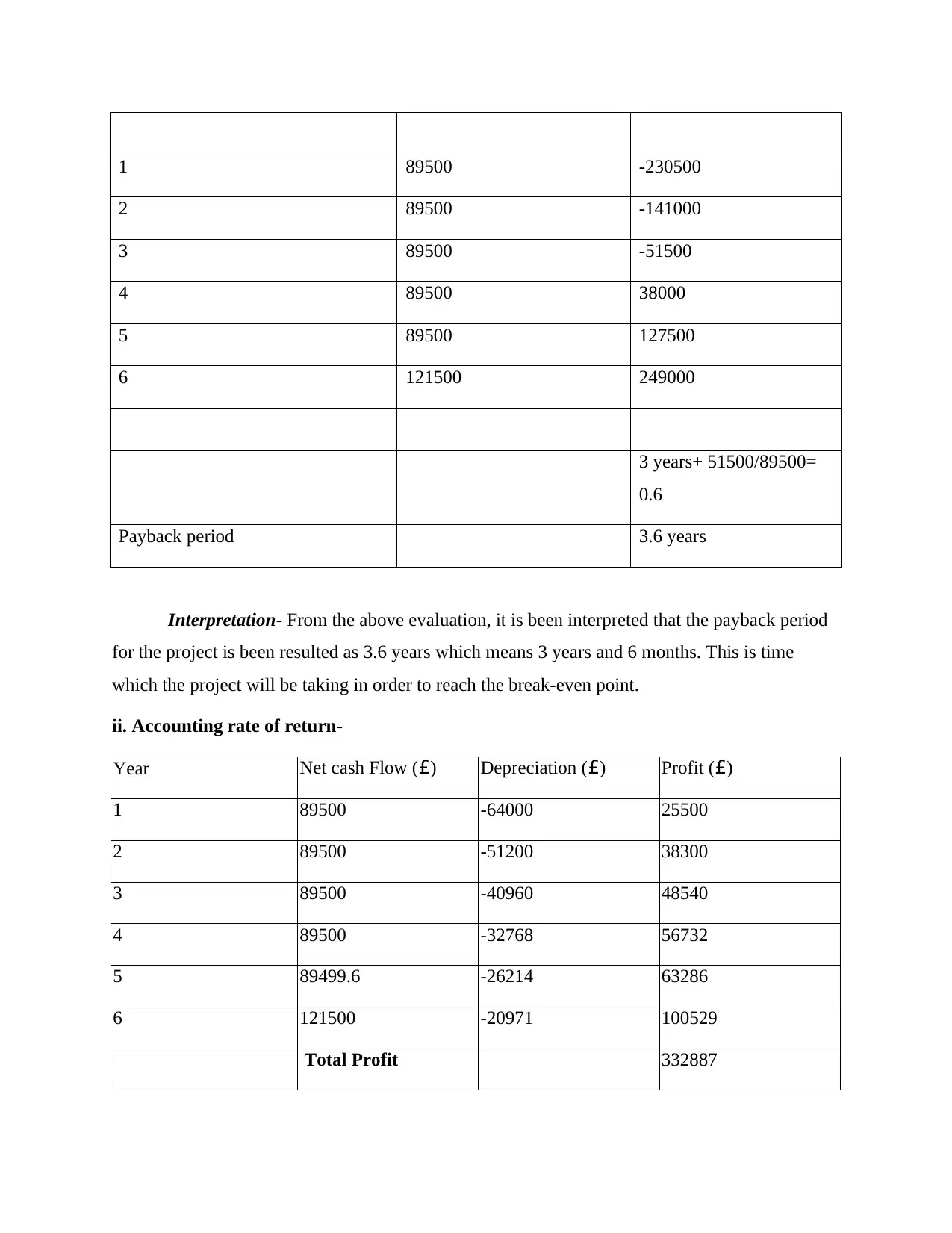

1 89500 -230500

2 89500 -141000

3 89500 -51500

4 89500 38000

5 89500 127500

6 121500 249000

3 years+ 51500/89500=

0.6

Payback period 3.6 years

Interpretation- From the above evaluation, it is been interpreted that the payback period

for the project is been resulted as 3.6 years which means 3 years and 6 months. This is time

which the project will be taking in order to reach the break-even point.

ii. Accounting rate of return-

Year Net cash Flow (£) Depreciation (£) Profit (£)

1 89500 -64000 25500

2 89500 -51200 38300

3 89500 -40960 48540

4 89500 -32768 56732

5 89499.6 -26214 63286

6 121500 -20971 100529

Total Profit 332887

2 89500 -141000

3 89500 -51500

4 89500 38000

5 89500 127500

6 121500 249000

3 years+ 51500/89500=

0.6

Payback period 3.6 years

Interpretation- From the above evaluation, it is been interpreted that the payback period

for the project is been resulted as 3.6 years which means 3 years and 6 months. This is time

which the project will be taking in order to reach the break-even point.

ii. Accounting rate of return-

Year Net cash Flow (£) Depreciation (£) Profit (£)

1 89500 -64000 25500

2 89500 -51200 38300

3 89500 -40960 48540

4 89500 -32768 56732

5 89499.6 -26214 63286

6 121500 -20971 100529

Total Profit 332887

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Useful Life 6 years

Average Profit £55,481.17

Accounting rate of return= Average Profit/ Initial Investment *100

ARR = £ 55481/£ 320000*100 =17.33 %

Interpretation- From the above analysis, it been viewed that the percentage return from

the investment made by the company in the project equated to 29.64%. This clearly states that

the project is facilitating the greater returns against the cost incurred in the investment.

iii. Net present value-

Year Cash

inflow

PV factor @

12%

Amount

((£)

1 89500 0.893 79910.71

2 89500 0.797 71348.85

3 89500 0.712 63704.33

4 89500 0.636 56878.86

5 89500 0.567 50784.7

6 121500 0.507 61600.5

Sum of discounted cash

flows

384248

Less: initial investment 320000

Net Present Value 64248

Average Profit £55,481.17

Accounting rate of return= Average Profit/ Initial Investment *100

ARR = £ 55481/£ 320000*100 =17.33 %

Interpretation- From the above analysis, it been viewed that the percentage return from

the investment made by the company in the project equated to 29.64%. This clearly states that

the project is facilitating the greater returns against the cost incurred in the investment.

iii. Net present value-

Year Cash

inflow

PV factor @

12%

Amount

((£)

1 89500 0.893 79910.71

2 89500 0.797 71348.85

3 89500 0.712 63704.33

4 89500 0.636 56878.86

5 89500 0.567 50784.7

6 121500 0.507 61600.5

Sum of discounted cash

flows

384248

Less: initial investment 320000

Net Present Value 64248

Interpretation- From the above analysis it is been observed that the net present value

resulted as 64248 which is a positive value. This means that the project is highly profitable and is

the best opportunity for the organization in which the investment could provide higher returns.

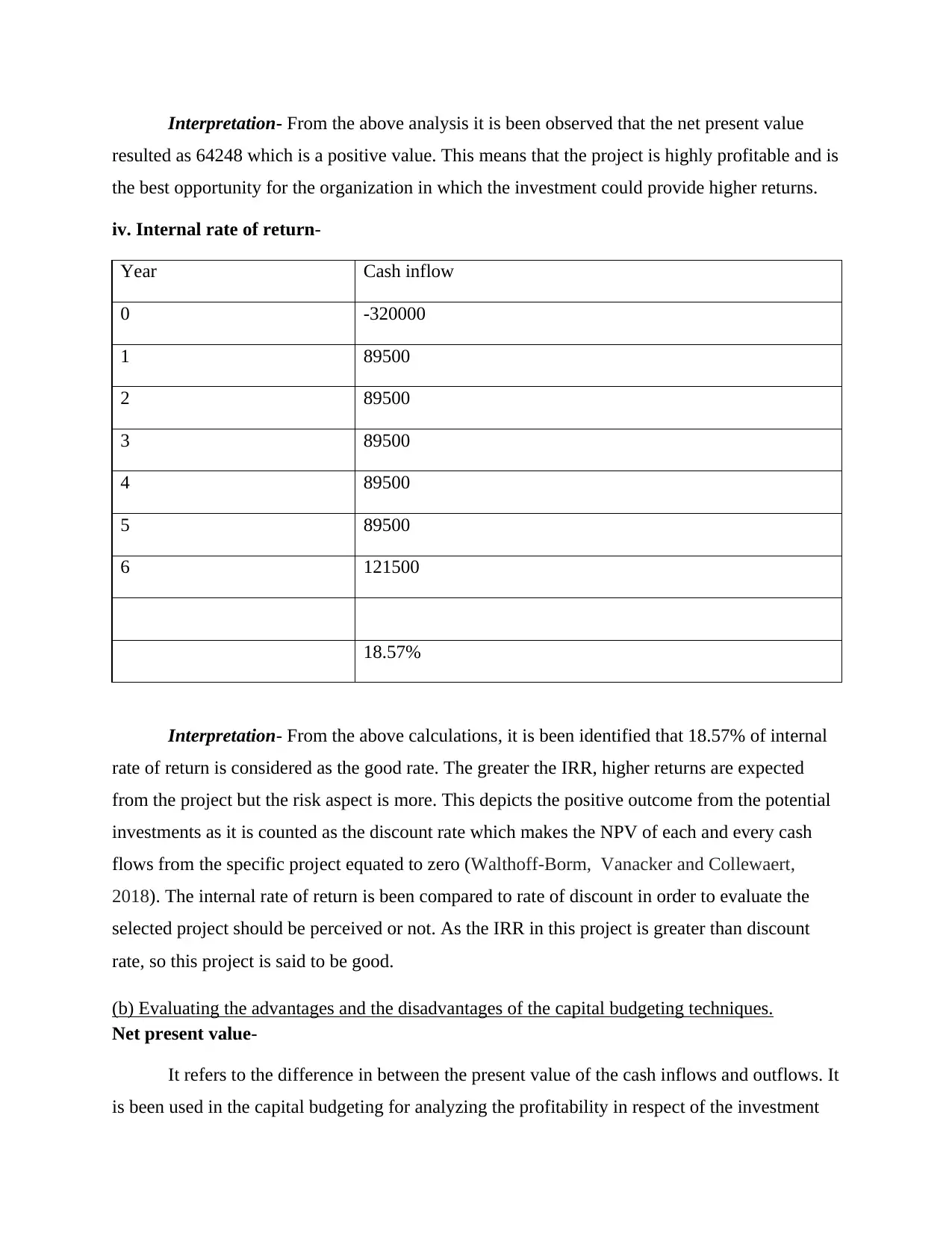

iv. Internal rate of return-

Year Cash inflow

0 -320000

1 89500

2 89500

3 89500

4 89500

5 89500

6 121500

18.57%

Interpretation- From the above calculations, it is been identified that 18.57% of internal

rate of return is considered as the good rate. The greater the IRR, higher returns are expected

from the project but the risk aspect is more. This depicts the positive outcome from the potential

investments as it is counted as the discount rate which makes the NPV of each and every cash

flows from the specific project equated to zero (Walthoff‐Borm, Vanacker and Collewaert,

2018). The internal rate of return is been compared to rate of discount in order to evaluate the

selected project should be perceived or not. As the IRR in this project is greater than discount

rate, so this project is said to be good.

(b) Evaluating the advantages and the disadvantages of the capital budgeting techniques.

Net present value-

It refers to the difference in between the present value of the cash inflows and outflows. It

is been used in the capital budgeting for analyzing the profitability in respect of the investment

resulted as 64248 which is a positive value. This means that the project is highly profitable and is

the best opportunity for the organization in which the investment could provide higher returns.

iv. Internal rate of return-

Year Cash inflow

0 -320000

1 89500

2 89500

3 89500

4 89500

5 89500

6 121500

18.57%

Interpretation- From the above calculations, it is been identified that 18.57% of internal

rate of return is considered as the good rate. The greater the IRR, higher returns are expected

from the project but the risk aspect is more. This depicts the positive outcome from the potential

investments as it is counted as the discount rate which makes the NPV of each and every cash

flows from the specific project equated to zero (Walthoff‐Borm, Vanacker and Collewaert,

2018). The internal rate of return is been compared to rate of discount in order to evaluate the

selected project should be perceived or not. As the IRR in this project is greater than discount

rate, so this project is said to be good.

(b) Evaluating the advantages and the disadvantages of the capital budgeting techniques.

Net present value-

It refers to the difference in between the present value of the cash inflows and outflows. It

is been used in the capital budgeting for analyzing the profitability in respect of the investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

project (Alkaraan, 2017). Positive net present value describes that the project is profitable and

the negative net present value associated with the investment results in unprofitable outcomes.

NPV is computed by subtracting the cash outflows from the cash inflows.

Benefits-Net present value provides more importance to time value of the money factor.

At the time of making the calculation under NPV, both the cash flow values are considered that

is before and after over the time period of project. Under this technique, High priority is been

given to the profitability and the risk of the proposal. It helps in enhancing the value of the firm

in the overall market as it indicates the profitability that will be generated from the project in

which the company has made investments.

Limitations-Net present value is a difficult and time consuming method because it

requires assessment of all the cash inflows and outflows of the project. It does not facilitate

accurate results if the investment amount of the mutually exclusive proposal is not been equal.

While assessing the net present value for the project, it creates difficulty in calculating the

discount rate appropriately. At the time when the project is of an unequal life, net present value

does not provide the correct decision making.

Payback period-

It means the length of the time that is required for recovering the cost of the investment. It is

stated as the time taken by the investment for reaching to the break-even point. The desirability

of the particular investment is been directly relates to the payback period. The lesser the time of

the payback reflects that the investment made is more attractive (Mahmoud and Neale, 2016).

The concept of payback is been generally used within the financial and the capital budgeting. It

is also used for determining cost savings from the technology that is energy efficient.

Benefits- This method is easy to use and simple to understand as it needs few inputs for

the calculation in comparison to the other investment appraisal technique. It helps the managers

in making quicker decisions as they could be able to calculate the payback period quickly. The

information facilitated by the payback period is crucial in comparison to other investment

appraisal methods as it focuses on ascertaining lower risk in the project. It provides the

the negative net present value associated with the investment results in unprofitable outcomes.

NPV is computed by subtracting the cash outflows from the cash inflows.

Benefits-Net present value provides more importance to time value of the money factor.

At the time of making the calculation under NPV, both the cash flow values are considered that

is before and after over the time period of project. Under this technique, High priority is been

given to the profitability and the risk of the proposal. It helps in enhancing the value of the firm

in the overall market as it indicates the profitability that will be generated from the project in

which the company has made investments.

Limitations-Net present value is a difficult and time consuming method because it

requires assessment of all the cash inflows and outflows of the project. It does not facilitate

accurate results if the investment amount of the mutually exclusive proposal is not been equal.

While assessing the net present value for the project, it creates difficulty in calculating the

discount rate appropriately. At the time when the project is of an unequal life, net present value

does not provide the correct decision making.

Payback period-

It means the length of the time that is required for recovering the cost of the investment. It is

stated as the time taken by the investment for reaching to the break-even point. The desirability

of the particular investment is been directly relates to the payback period. The lesser the time of

the payback reflects that the investment made is more attractive (Mahmoud and Neale, 2016).

The concept of payback is been generally used within the financial and the capital budgeting. It

is also used for determining cost savings from the technology that is energy efficient.

Benefits- This method is easy to use and simple to understand as it needs few inputs for

the calculation in comparison to the other investment appraisal technique. It helps the managers

in making quicker decisions as they could be able to calculate the payback period quickly. The

information facilitated by the payback period is crucial in comparison to other investment

appraisal methods as it focuses on ascertaining lower risk in the project. It provides the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

preference to the liquidity and helps the company in recovering the cost for the purpose of

making the investment in the other growing projects. It is the most useful method in the

consequences of the uncertainty or the technological changes. This factor of the uncertainty

creates difficulty in projecting future cash flows on an annual basis. Thus, the projects that

results in shorter payback period enables in reducing possibility of the loss because of the

obsolescence.

Limitations- Payback period ignores time value of money which is been considered as

the most important concept for the business. It considers the cash flow till the recovery of the

initial investment and fails to consider cash flow in the subsequent years. It ignores the analysis

of the profitability as shorter payback does not depict that the project will generate profits

(Sangster, 1993). This results the project to unviable condition after the ending of the payback

period.

This approach is not considered as realistic in the normal course of the business as the capital

investments are not counted as the one-time investment. Instead, it needs further investment as

well in the coming years. The projects also has the irregular inflow of the cash.

Accounting rate of return-

It refers to the percentage return rate that is expected to receive on an investment or the

asset in comparison with the cost of initial investment. Accounting rate of return divides the

average revenue from the asset by enterprise initial investments in order to derive the ratio or the

return that is expected over life of the asset (Ashford, Dyson and Hodges, 1988). It does not

consider time value of the money which is an integral part for maintaining the business.

Benefits- Accounting rate of return is based on the accounting information and thus it

does need any other special reports for determining the rate of return. It is easiest to compute and

very simple in understanding. It considers total profits and the savings for the overall economic

life of project. This technique is based on the accounting profit and hence helps in measuring

profitability from the investment. It provides for the comparison of the project relating to new

product with tat of the project of reduced cost and also the other competitive nature projects.

Accounting rate of return is the budgeting method that helps in satisfying the owners interest as

making the investment in the other growing projects. It is the most useful method in the

consequences of the uncertainty or the technological changes. This factor of the uncertainty

creates difficulty in projecting future cash flows on an annual basis. Thus, the projects that

results in shorter payback period enables in reducing possibility of the loss because of the

obsolescence.

Limitations- Payback period ignores time value of money which is been considered as

the most important concept for the business. It considers the cash flow till the recovery of the

initial investment and fails to consider cash flow in the subsequent years. It ignores the analysis

of the profitability as shorter payback does not depict that the project will generate profits

(Sangster, 1993). This results the project to unviable condition after the ending of the payback

period.

This approach is not considered as realistic in the normal course of the business as the capital

investments are not counted as the one-time investment. Instead, it needs further investment as

well in the coming years. The projects also has the irregular inflow of the cash.

Accounting rate of return-

It refers to the percentage return rate that is expected to receive on an investment or the

asset in comparison with the cost of initial investment. Accounting rate of return divides the

average revenue from the asset by enterprise initial investments in order to derive the ratio or the

return that is expected over life of the asset (Ashford, Dyson and Hodges, 1988). It does not

consider time value of the money which is an integral part for maintaining the business.

Benefits- Accounting rate of return is based on the accounting information and thus it

does need any other special reports for determining the rate of return. It is easiest to compute and

very simple in understanding. It considers total profits and the savings for the overall economic

life of project. This technique is based on the accounting profit and hence helps in measuring

profitability from the investment. It provides for the comparison of the project relating to new

product with tat of the project of reduced cost and also the other competitive nature projects.

Accounting rate of return is the budgeting method that helps in satisfying the owners interest as

they show keen interest in the investment return. It is considered as the most useful method for

measuring the present performance of an enterprise.

Limitations- It ignores time value of money concept which is essential for knowing the

accurate estimations in the future. It also ignores the cash flow generated from the investment.

Accounting rate of return method do not consider the terminal value of project. This investment

appraisal method do not consider external factors which act as the major factors that affects the

profitability of project. In the projects where the investment is to be made in parts, in such cases

this method is not suitable to apply. It does not take into account the time period of various

investments. This leads to same amount of the average and the initial investment.

Internal rate of return-

It is the metric that is used in the capital budgeting for estimating profitability of the

potential investments. It is rate of discount which makes net present value for all the cash flows

from the specific project that equates to zero (Ballantine and Stray, 1998). For assessing the

future growth and the expansion, internal rate of return is been computed.

Benefits- The foremost and the important benefit of this technique is that it considers the

tie value of the money at the time evaluating the project. It is very easy to interpret this method

after the calculation of the IRR. If the cost of capital is less than the IRR, then the project will be

accepted. This method of investment appraisal helps in evaluating the correct profit as it covers

the overall economic life of the proposal. Under this method there is not any requirement for

calculating the cost of the capital and the cut-off rate. It provides much importance towards

fulfilling the wealth maximization objective.

Limitations- Economies of the scale is the major component for every business which is

been ignored by this method. The assumption regarding the reinvestment rate is impractical as

this method assumes the positive value of the future cash flows for the remaining time period. It

indulges the finance manager for compulsorily investing into the other dependent and the

contingent projects. It includes tedious calculations. This method provides more importance to

the profitability and not considers the re coupling of the capital expenditure. Sometimes, the

measuring the present performance of an enterprise.

Limitations- It ignores time value of money concept which is essential for knowing the

accurate estimations in the future. It also ignores the cash flow generated from the investment.

Accounting rate of return method do not consider the terminal value of project. This investment

appraisal method do not consider external factors which act as the major factors that affects the

profitability of project. In the projects where the investment is to be made in parts, in such cases

this method is not suitable to apply. It does not take into account the time period of various

investments. This leads to same amount of the average and the initial investment.

Internal rate of return-

It is the metric that is used in the capital budgeting for estimating profitability of the

potential investments. It is rate of discount which makes net present value for all the cash flows

from the specific project that equates to zero (Ballantine and Stray, 1998). For assessing the

future growth and the expansion, internal rate of return is been computed.

Benefits- The foremost and the important benefit of this technique is that it considers the

tie value of the money at the time evaluating the project. It is very easy to interpret this method

after the calculation of the IRR. If the cost of capital is less than the IRR, then the project will be

accepted. This method of investment appraisal helps in evaluating the correct profit as it covers

the overall economic life of the proposal. Under this method there is not any requirement for

calculating the cost of the capital and the cut-off rate. It provides much importance towards

fulfilling the wealth maximization objective.

Limitations- Economies of the scale is the major component for every business which is

been ignored by this method. The assumption regarding the reinvestment rate is impractical as

this method assumes the positive value of the future cash flows for the remaining time period. It

indulges the finance manager for compulsorily investing into the other dependent and the

contingent projects. It includes tedious calculations. This method provides more importance to

the profitability and not considers the re coupling of the capital expenditure. Sometimes, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.