Equity and Liability Analysis: Woolsworth and Wesfarmers Comparison

VerifiedAdded on 2022/10/18

|17

|3088

|15

Report

AI Summary

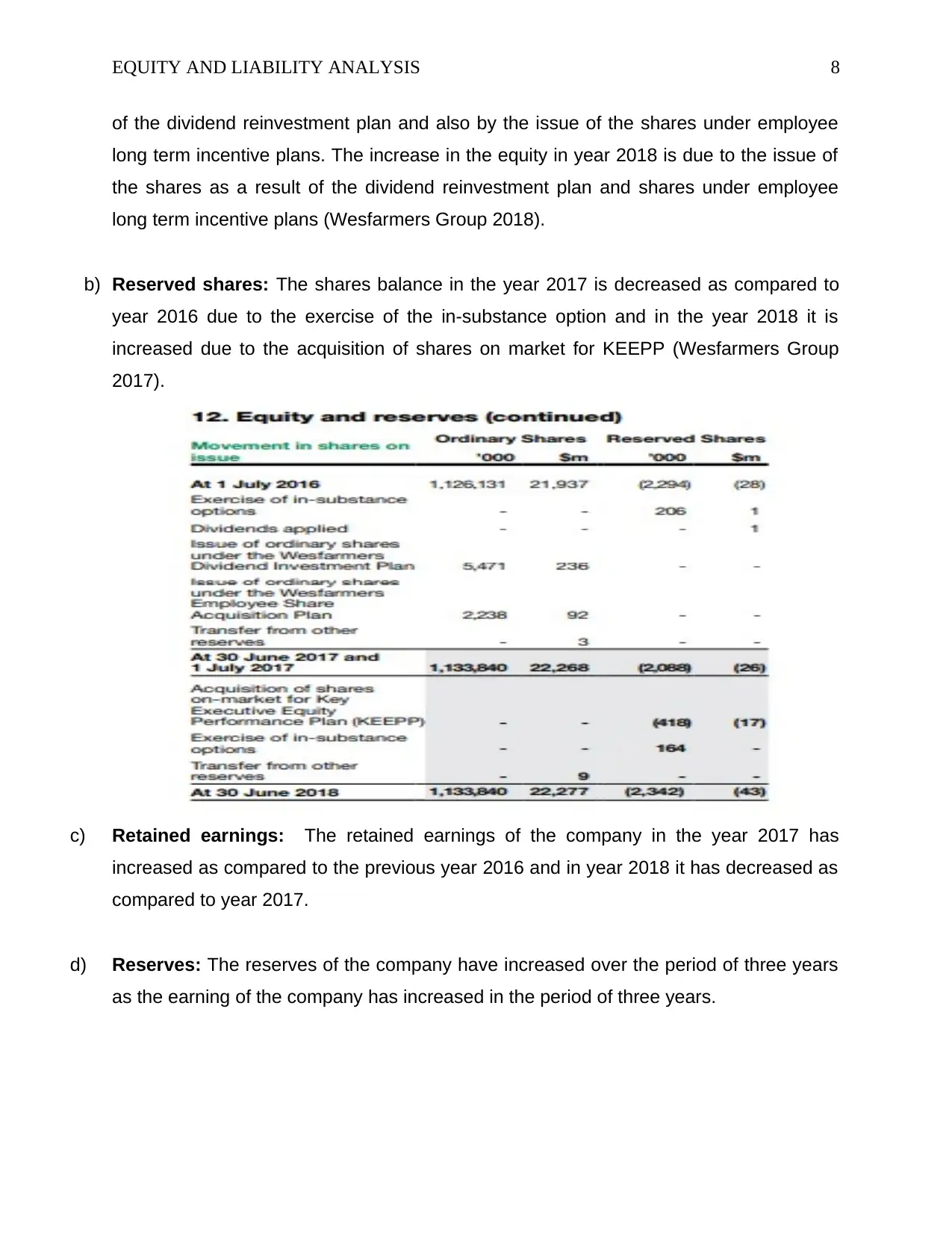

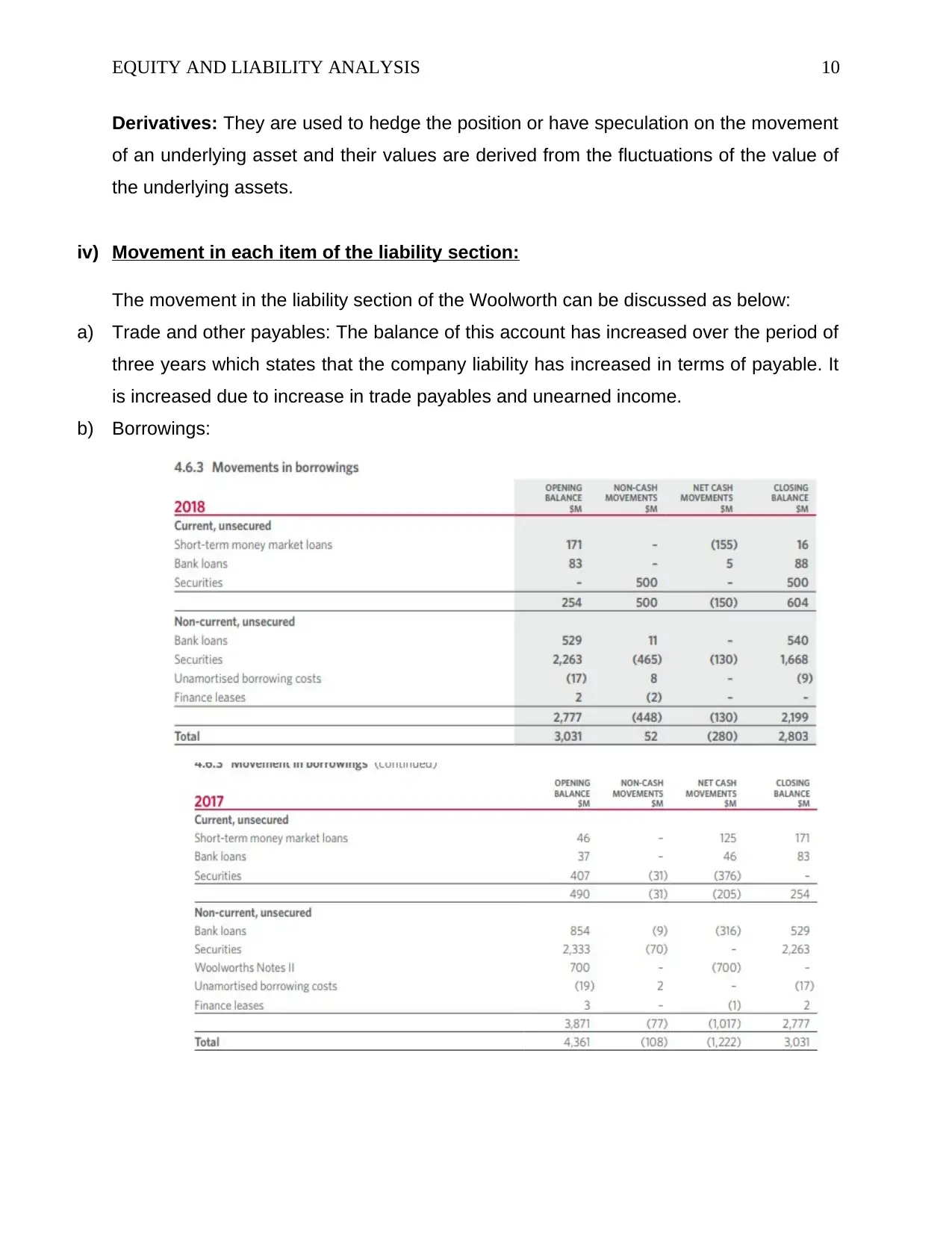

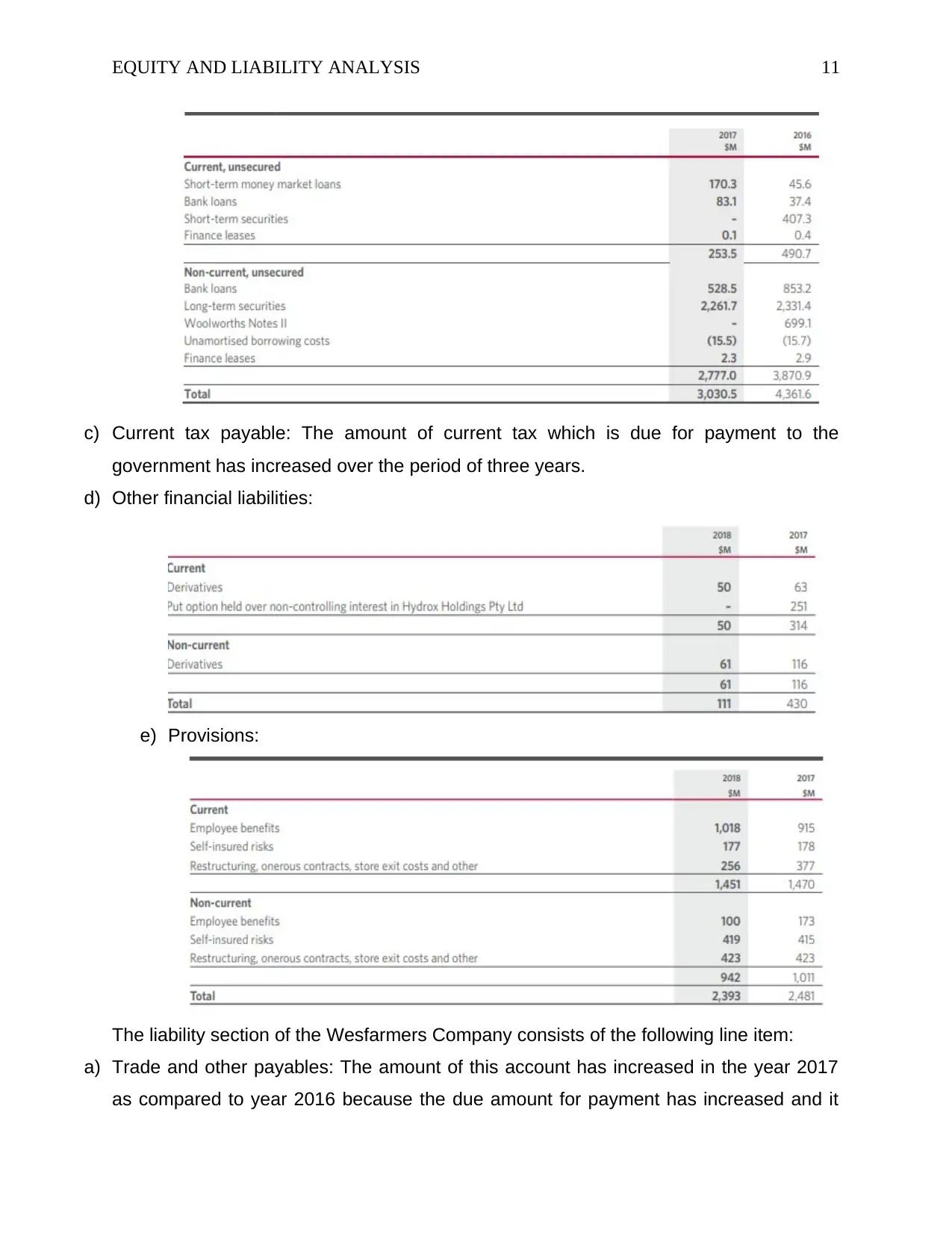

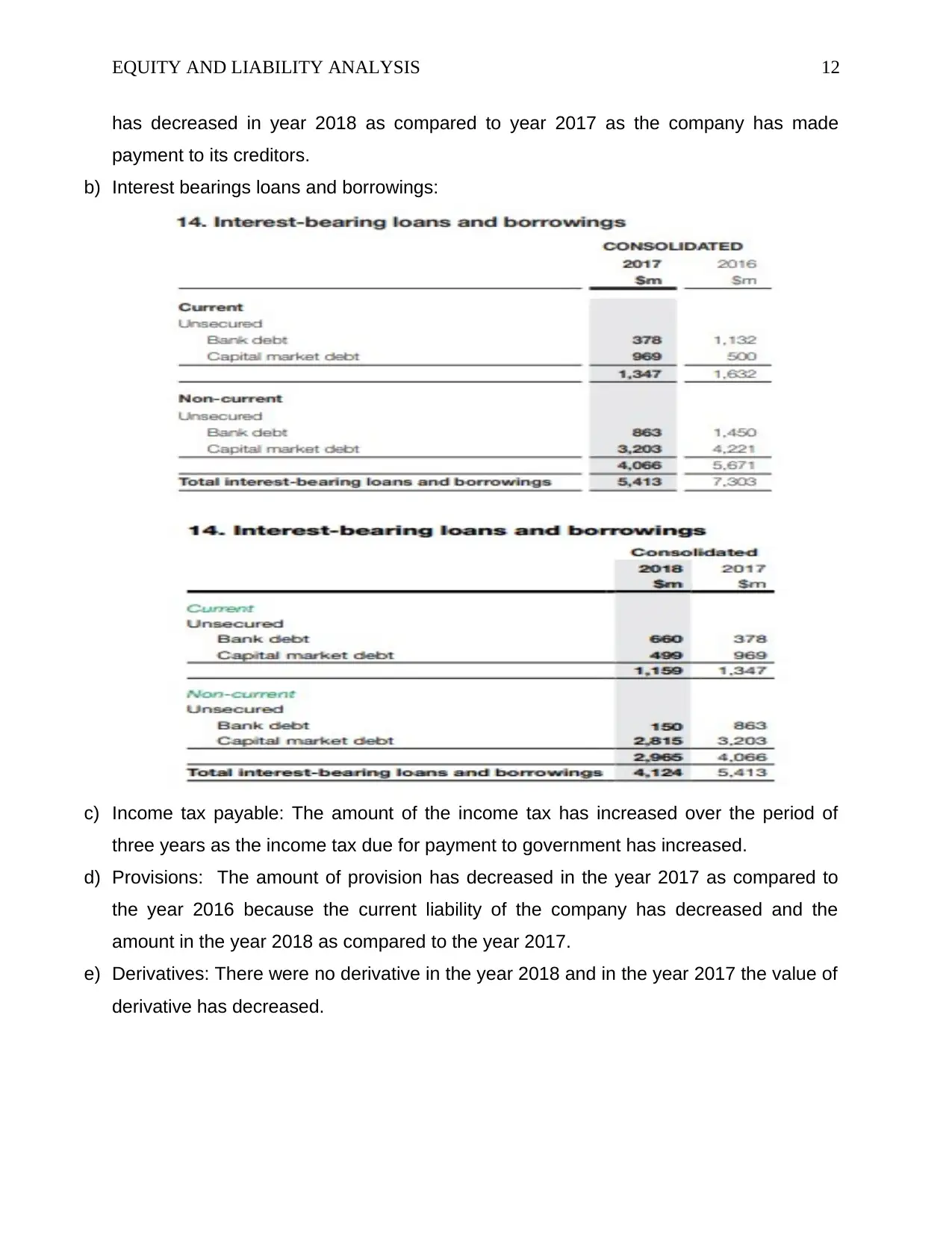

This report undertakes a comprehensive financial statement analysis, focusing on the equity and liability sections of Woolworths Group and Wesfarmers Group. It begins with an introduction to both companies, outlining their core businesses and market positions. The report then delves into the analysis of the owners' equity sections, detailing components such as contributed equity, reserves, and retained earnings for both companies. It examines the movements in each equity item over a three-year period, highlighting factors contributing to changes in share capital, reserves, and retained earnings. The liability section is then analyzed, covering items such as trade payables, borrowings, and provisions. The report discusses the movement in each liability item and concludes with a comparison of the advantages and disadvantages of different funding sources for each company. The report also includes an analysis of the three types of entities and concludes with the references used.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.