Accounting Treatment & Journal Entries: Financial Event Analysis

VerifiedAdded on 2023/06/05

|12

|2263

|333

Homework Assignment

AI Summary

This assignment provides solutions to various accounting scenarios involving changes in accounting estimates, prior period errors, investment valuation, fraudulent activities, share issuance, deferred tax, asset revaluation, and impairment losses, all under the framework of Australian Accounting Standards Board (AASB) guidelines. It includes detailed journal entries and calculations for scenarios like depreciation adjustments, correction of prior period errors, share application and allotment, forfeiture and reissue of shares, determination of current and deferred tax liabilities, accounting for revaluation of assets, and calculation and allocation of impairment losses. The solutions demonstrate the practical application of AASB standards such as AASB 108, AASB 110, and AASB 136, providing a comprehensive guide to handling complex financial accounting issues.

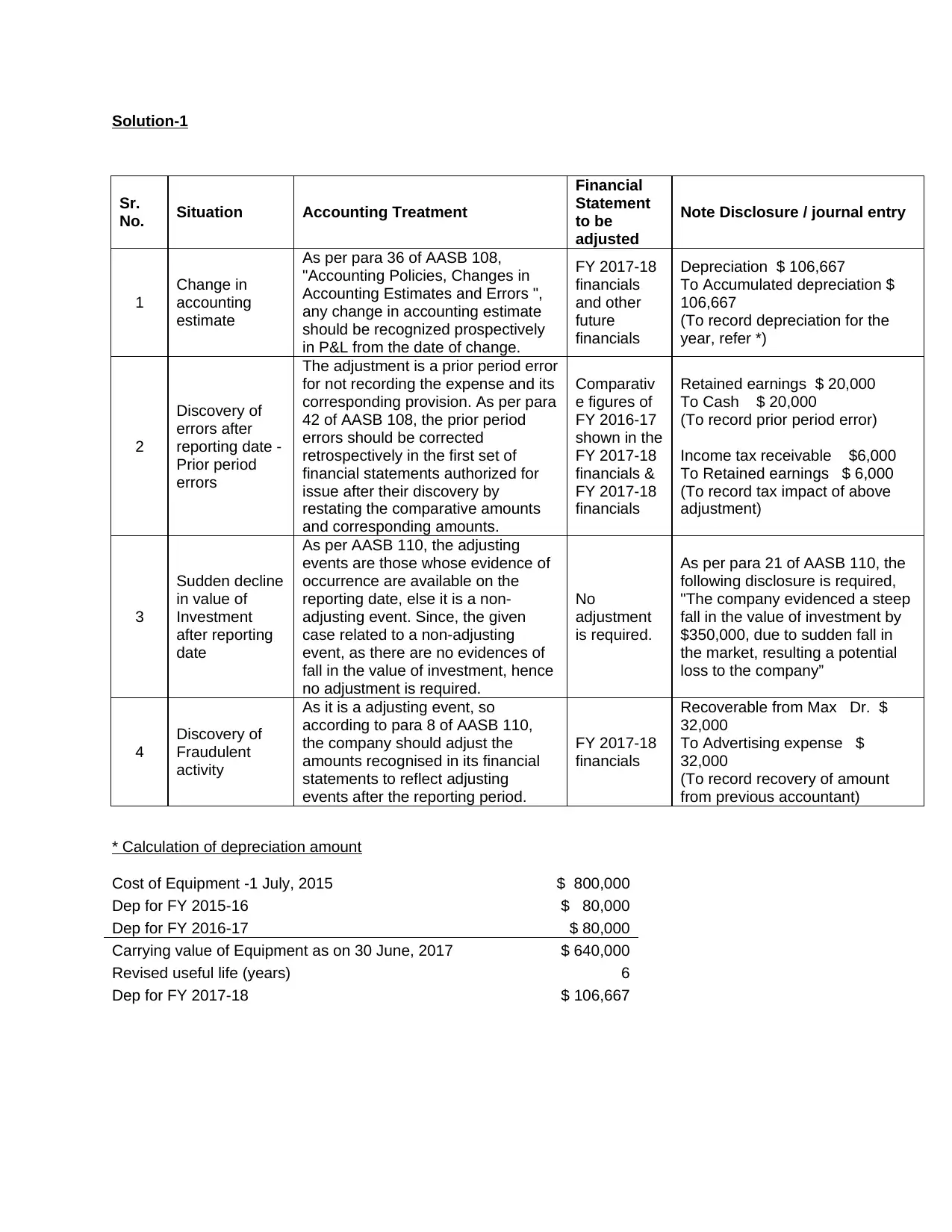

Solution-1

Sr.

No. Situation Accounting Treatment

Financial

Statement

to be

adjusted

Note Disclosure / journal entry

1

Change in

accounting

estimate

As per para 36 of AASB 108,

"Accounting Policies, Changes in

Accounting Estimates and Errors ",

any change in accounting estimate

should be recognized prospectively

in P&L from the date of change.

FY 2017-18

financials

and other

future

financials

Depreciation $ 106,667

To Accumulated depreciation $

106,667

(To record depreciation for the

year, refer *)

2

Discovery of

errors after

reporting date -

Prior period

errors

The adjustment is a prior period error

for not recording the expense and its

corresponding provision. As per para

42 of AASB 108, the prior period

errors should be corrected

retrospectively in the first set of

financial statements authorized for

issue after their discovery by

restating the comparative amounts

and corresponding amounts.

Comparativ

e figures of

FY 2016-17

shown in the

FY 2017-18

financials &

FY 2017-18

financials

Retained earnings $ 20,000

To Cash $ 20,000

(To record prior period error)

Income tax receivable $6,000

To Retained earnings $ 6,000

(To record tax impact of above

adjustment)

3

Sudden decline

in value of

Investment

after reporting

date

As per AASB 110, the adjusting

events are those whose evidence of

occurrence are available on the

reporting date, else it is a non-

adjusting event. Since, the given

case related to a non-adjusting

event, as there are no evidences of

fall in the value of investment, hence

no adjustment is required.

No

adjustment

is required.

As per para 21 of AASB 110, the

following disclosure is required,

"The company evidenced a steep

fall in the value of investment by

$350,000, due to sudden fall in

the market, resulting a potential

loss to the company”

4

Discovery of

Fraudulent

activity

As it is a adjusting event, so

according to para 8 of AASB 110,

the company should adjust the

amounts recognised in its financial

statements to reflect adjusting

events after the reporting period.

FY 2017-18

financials

Recoverable from Max Dr. $

32,000

To Advertising expense $

32,000

(To record recovery of amount

from previous accountant)

* Calculation of depreciation amount

Cost of Equipment -1 July, 2015 $ 800,000

Dep for FY 2015-16 $ 80,000

Dep for FY 2016-17 $ 80,000

Carrying value of Equipment as on 30 June, 2017 $ 640,000

Revised useful life (years) 6

Dep for FY 2017-18 $ 106,667

Sr.

No. Situation Accounting Treatment

Financial

Statement

to be

adjusted

Note Disclosure / journal entry

1

Change in

accounting

estimate

As per para 36 of AASB 108,

"Accounting Policies, Changes in

Accounting Estimates and Errors ",

any change in accounting estimate

should be recognized prospectively

in P&L from the date of change.

FY 2017-18

financials

and other

future

financials

Depreciation $ 106,667

To Accumulated depreciation $

106,667

(To record depreciation for the

year, refer *)

2

Discovery of

errors after

reporting date -

Prior period

errors

The adjustment is a prior period error

for not recording the expense and its

corresponding provision. As per para

42 of AASB 108, the prior period

errors should be corrected

retrospectively in the first set of

financial statements authorized for

issue after their discovery by

restating the comparative amounts

and corresponding amounts.

Comparativ

e figures of

FY 2016-17

shown in the

FY 2017-18

financials &

FY 2017-18

financials

Retained earnings $ 20,000

To Cash $ 20,000

(To record prior period error)

Income tax receivable $6,000

To Retained earnings $ 6,000

(To record tax impact of above

adjustment)

3

Sudden decline

in value of

Investment

after reporting

date

As per AASB 110, the adjusting

events are those whose evidence of

occurrence are available on the

reporting date, else it is a non-

adjusting event. Since, the given

case related to a non-adjusting

event, as there are no evidences of

fall in the value of investment, hence

no adjustment is required.

No

adjustment

is required.

As per para 21 of AASB 110, the

following disclosure is required,

"The company evidenced a steep

fall in the value of investment by

$350,000, due to sudden fall in

the market, resulting a potential

loss to the company”

4

Discovery of

Fraudulent

activity

As it is a adjusting event, so

according to para 8 of AASB 110,

the company should adjust the

amounts recognised in its financial

statements to reflect adjusting

events after the reporting period.

FY 2017-18

financials

Recoverable from Max Dr. $

32,000

To Advertising expense $

32,000

(To record recovery of amount

from previous accountant)

* Calculation of depreciation amount

Cost of Equipment -1 July, 2015 $ 800,000

Dep for FY 2015-16 $ 80,000

Dep for FY 2016-17 $ 80,000

Carrying value of Equipment as on 30 June, 2017 $ 640,000

Revised useful life (years) 6

Dep for FY 2017-18 $ 106,667

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

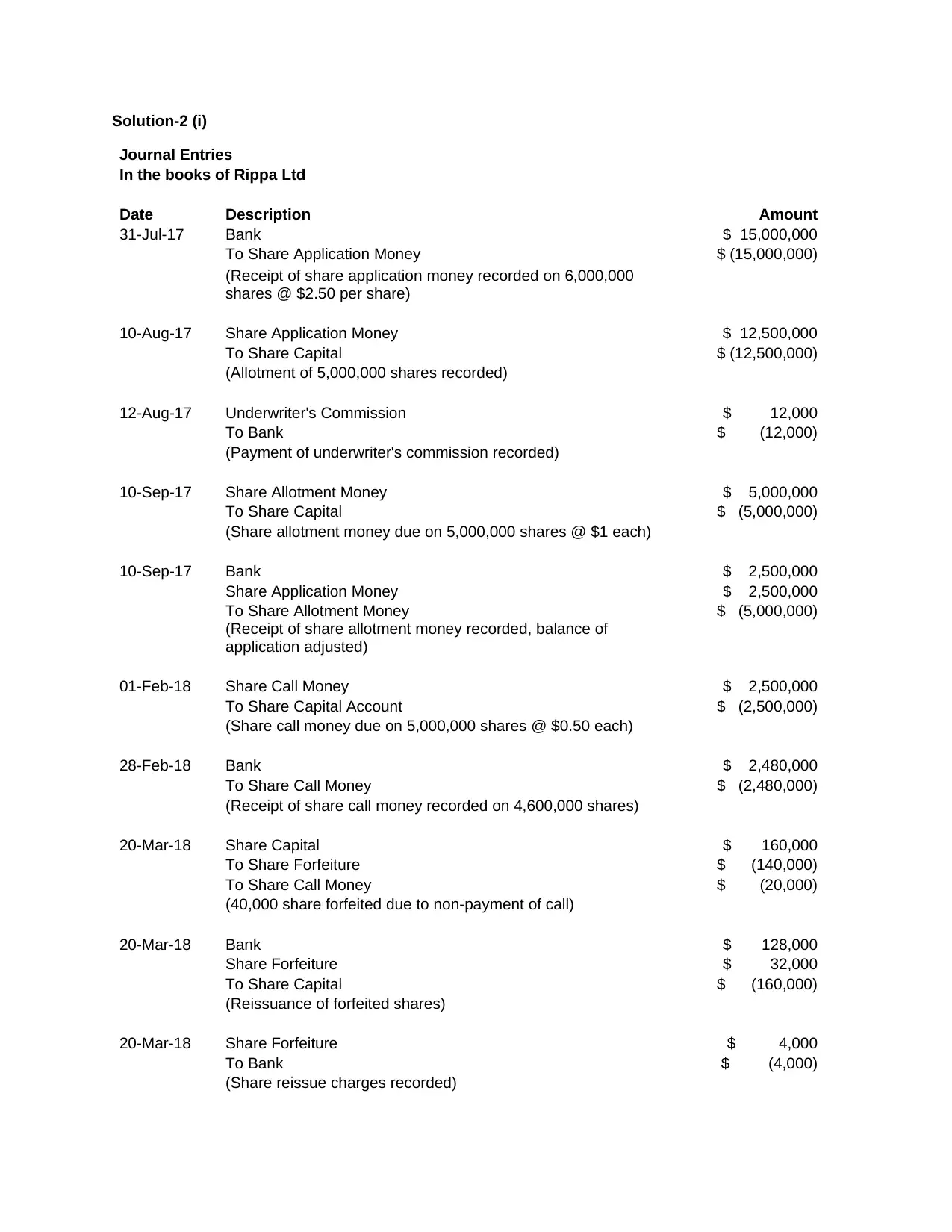

Solution-2 (i)

Journal Entries

In the books of Rippa Ltd

Date Description Amount

31-Jul-17 Bank $ 15,000,000

To Share Application Money $ (15,000,000)

(Receipt of share application money recorded on 6,000,000

shares @ $2.50 per share)

10-Aug-17 Share Application Money $ 12,500,000

To Share Capital $ (12,500,000)

(Allotment of 5,000,000 shares recorded)

12-Aug-17 Underwriter's Commission $ 12,000

To Bank $ (12,000)

(Payment of underwriter's commission recorded)

10-Sep-17 Share Allotment Money $ 5,000,000

To Share Capital $ (5,000,000)

(Share allotment money due on 5,000,000 shares @ $1 each)

10-Sep-17 Bank $ 2,500,000

Share Application Money $ 2,500,000

To Share Allotment Money $ (5,000,000)

(Receipt of share allotment money recorded, balance of

application adjusted)

01-Feb-18 Share Call Money $ 2,500,000

To Share Capital Account $ (2,500,000)

(Share call money due on 5,000,000 shares @ $0.50 each)

28-Feb-18 Bank $ 2,480,000

To Share Call Money $ (2,480,000)

(Receipt of share call money recorded on 4,600,000 shares)

20-Mar-18 Share Capital $ 160,000

To Share Forfeiture $ (140,000)

To Share Call Money $ (20,000)

(40,000 share forfeited due to non-payment of call)

20-Mar-18 Bank $ 128,000

Share Forfeiture $ 32,000

To Share Capital $ (160,000)

(Reissuance of forfeited shares)

20-Mar-18 Share Forfeiture $ 4,000

To Bank $ (4,000)

(Share reissue charges recorded)

Journal Entries

In the books of Rippa Ltd

Date Description Amount

31-Jul-17 Bank $ 15,000,000

To Share Application Money $ (15,000,000)

(Receipt of share application money recorded on 6,000,000

shares @ $2.50 per share)

10-Aug-17 Share Application Money $ 12,500,000

To Share Capital $ (12,500,000)

(Allotment of 5,000,000 shares recorded)

12-Aug-17 Underwriter's Commission $ 12,000

To Bank $ (12,000)

(Payment of underwriter's commission recorded)

10-Sep-17 Share Allotment Money $ 5,000,000

To Share Capital $ (5,000,000)

(Share allotment money due on 5,000,000 shares @ $1 each)

10-Sep-17 Bank $ 2,500,000

Share Application Money $ 2,500,000

To Share Allotment Money $ (5,000,000)

(Receipt of share allotment money recorded, balance of

application adjusted)

01-Feb-18 Share Call Money $ 2,500,000

To Share Capital Account $ (2,500,000)

(Share call money due on 5,000,000 shares @ $0.50 each)

28-Feb-18 Bank $ 2,480,000

To Share Call Money $ (2,480,000)

(Receipt of share call money recorded on 4,600,000 shares)

20-Mar-18 Share Capital $ 160,000

To Share Forfeiture $ (140,000)

To Share Call Money $ (20,000)

(40,000 share forfeited due to non-payment of call)

20-Mar-18 Bank $ 128,000

Share Forfeiture $ 32,000

To Share Capital $ (160,000)

(Reissuance of forfeited shares)

20-Mar-18 Share Forfeiture $ 4,000

To Bank $ (4,000)

(Share reissue charges recorded)

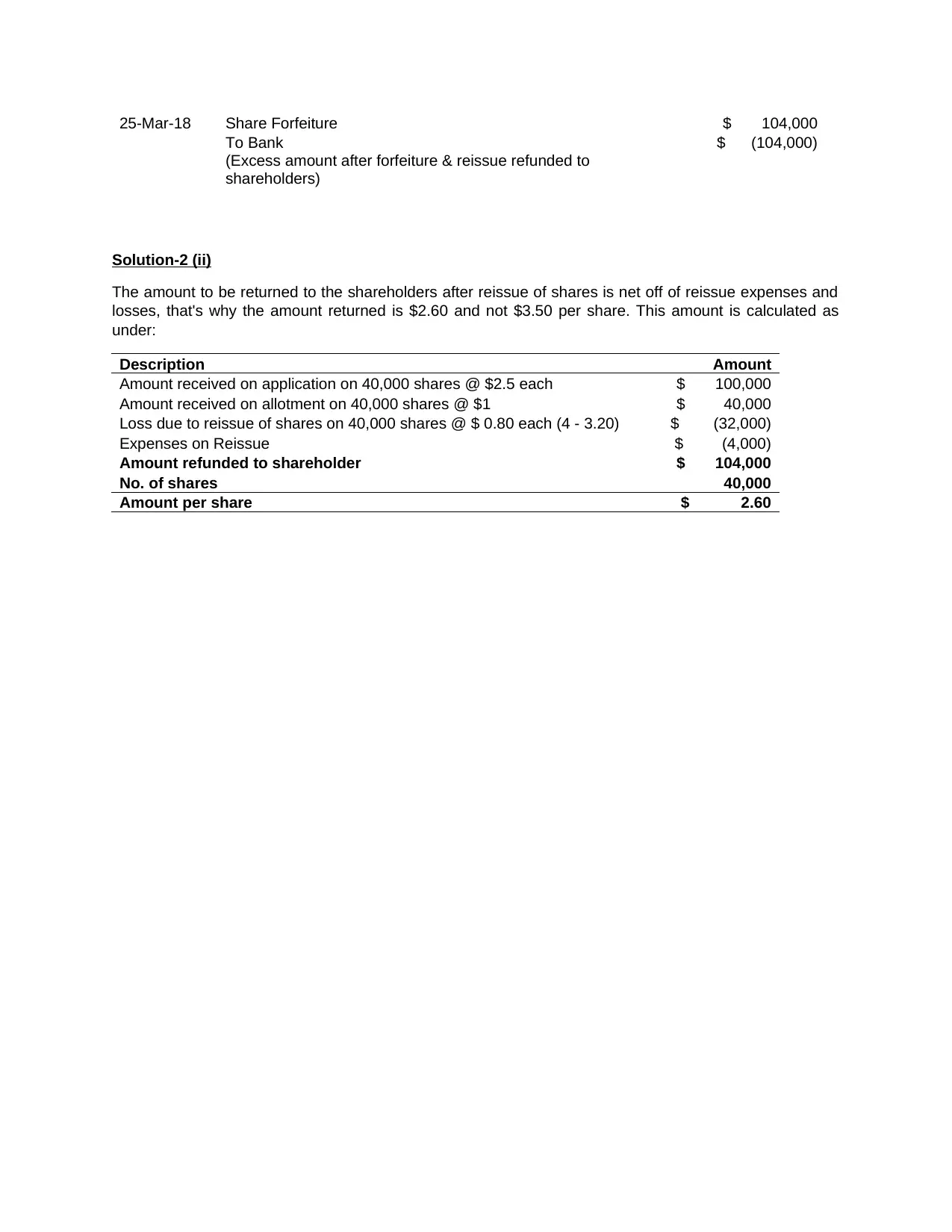

25-Mar-18 Share Forfeiture $ 104,000

To Bank $ (104,000)

(Excess amount after forfeiture & reissue refunded to

shareholders)

Solution-2 (ii)

The amount to be returned to the shareholders after reissue of shares is net off of reissue expenses and

losses, that's why the amount returned is $2.60 and not $3.50 per share. This amount is calculated as

under:

Description Amount

Amount received on application on 40,000 shares @ $2.5 each $ 100,000

Amount received on allotment on 40,000 shares @ $1 $ 40,000

Loss due to reissue of shares on 40,000 shares @ $ 0.80 each (4 - 3.20) $ (32,000)

Expenses on Reissue $ (4,000)

Amount refunded to shareholder $ 104,000

No. of shares 40,000

Amount per share $ 2.60

To Bank $ (104,000)

(Excess amount after forfeiture & reissue refunded to

shareholders)

Solution-2 (ii)

The amount to be returned to the shareholders after reissue of shares is net off of reissue expenses and

losses, that's why the amount returned is $2.60 and not $3.50 per share. This amount is calculated as

under:

Description Amount

Amount received on application on 40,000 shares @ $2.5 each $ 100,000

Amount received on allotment on 40,000 shares @ $1 $ 40,000

Loss due to reissue of shares on 40,000 shares @ $ 0.80 each (4 - 3.20) $ (32,000)

Expenses on Reissue $ (4,000)

Amount refunded to shareholder $ 104,000

No. of shares 40,000

Amount per share $ 2.60

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

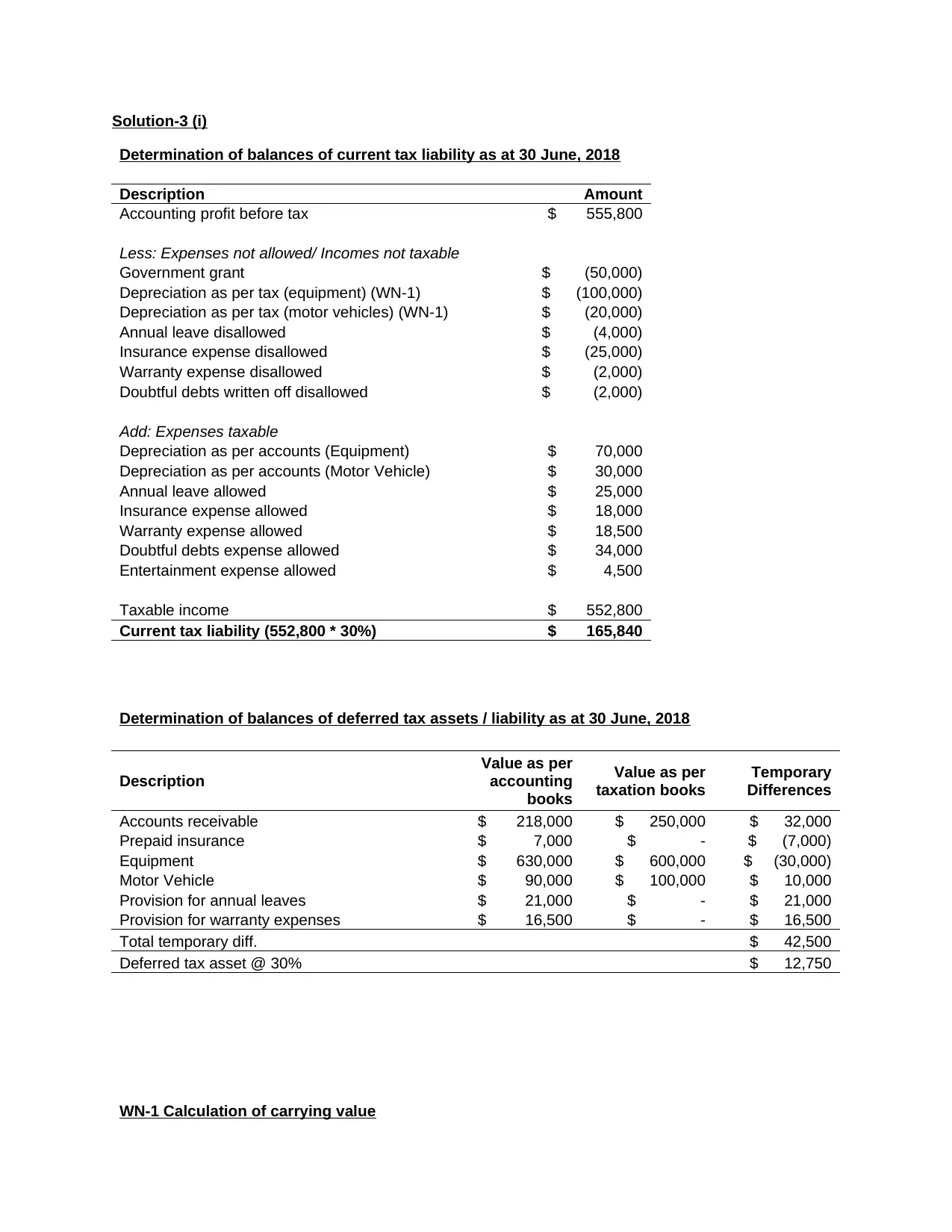

Solution-3 (i)

Determination of balances of current tax liability as at 30 June, 2018

Description Amount

Accounting profit before tax $ 555,800

Less: Expenses not allowed/ Incomes not taxable

Government grant $ (50,000)

Depreciation as per tax (equipment) (WN-1) $ (100,000)

Depreciation as per tax (motor vehicles) (WN-1) $ (20,000)

Annual leave disallowed $ (4,000)

Insurance expense disallowed $ (25,000)

Warranty expense disallowed $ (2,000)

Doubtful debts written off disallowed $ (2,000)

Add: Expenses taxable

Depreciation as per accounts (Equipment) $ 70,000

Depreciation as per accounts (Motor Vehicle) $ 30,000

Annual leave allowed $ 25,000

Insurance expense allowed $ 18,000

Warranty expense allowed $ 18,500

Doubtful debts expense allowed $ 34,000

Entertainment expense allowed $ 4,500

Taxable income $ 552,800

Current tax liability (552,800 * 30%) $ 165,840

Determination of balances of deferred tax assets / liability as at 30 June, 2018

Description

Value as per

accounting

books

Value as per

taxation books

Temporary

Differences

Accounts receivable $ 218,000 $ 250,000 $ 32,000

Prepaid insurance $ 7,000 $ - $ (7,000)

Equipment $ 630,000 $ 600,000 $ (30,000)

Motor Vehicle $ 90,000 $ 100,000 $ 10,000

Provision for annual leaves $ 21,000 $ - $ 21,000

Provision for warranty expenses $ 16,500 $ - $ 16,500

Total temporary diff. $ 42,500

Deferred tax asset @ 30% $ 12,750

WN-1 Calculation of carrying value

Determination of balances of current tax liability as at 30 June, 2018

Description Amount

Accounting profit before tax $ 555,800

Less: Expenses not allowed/ Incomes not taxable

Government grant $ (50,000)

Depreciation as per tax (equipment) (WN-1) $ (100,000)

Depreciation as per tax (motor vehicles) (WN-1) $ (20,000)

Annual leave disallowed $ (4,000)

Insurance expense disallowed $ (25,000)

Warranty expense disallowed $ (2,000)

Doubtful debts written off disallowed $ (2,000)

Add: Expenses taxable

Depreciation as per accounts (Equipment) $ 70,000

Depreciation as per accounts (Motor Vehicle) $ 30,000

Annual leave allowed $ 25,000

Insurance expense allowed $ 18,000

Warranty expense allowed $ 18,500

Doubtful debts expense allowed $ 34,000

Entertainment expense allowed $ 4,500

Taxable income $ 552,800

Current tax liability (552,800 * 30%) $ 165,840

Determination of balances of deferred tax assets / liability as at 30 June, 2018

Description

Value as per

accounting

books

Value as per

taxation books

Temporary

Differences

Accounts receivable $ 218,000 $ 250,000 $ 32,000

Prepaid insurance $ 7,000 $ - $ (7,000)

Equipment $ 630,000 $ 600,000 $ (30,000)

Motor Vehicle $ 90,000 $ 100,000 $ 10,000

Provision for annual leaves $ 21,000 $ - $ 21,000

Provision for warranty expenses $ 16,500 $ - $ 16,500

Total temporary diff. $ 42,500

Deferred tax asset @ 30% $ 12,750

WN-1 Calculation of carrying value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

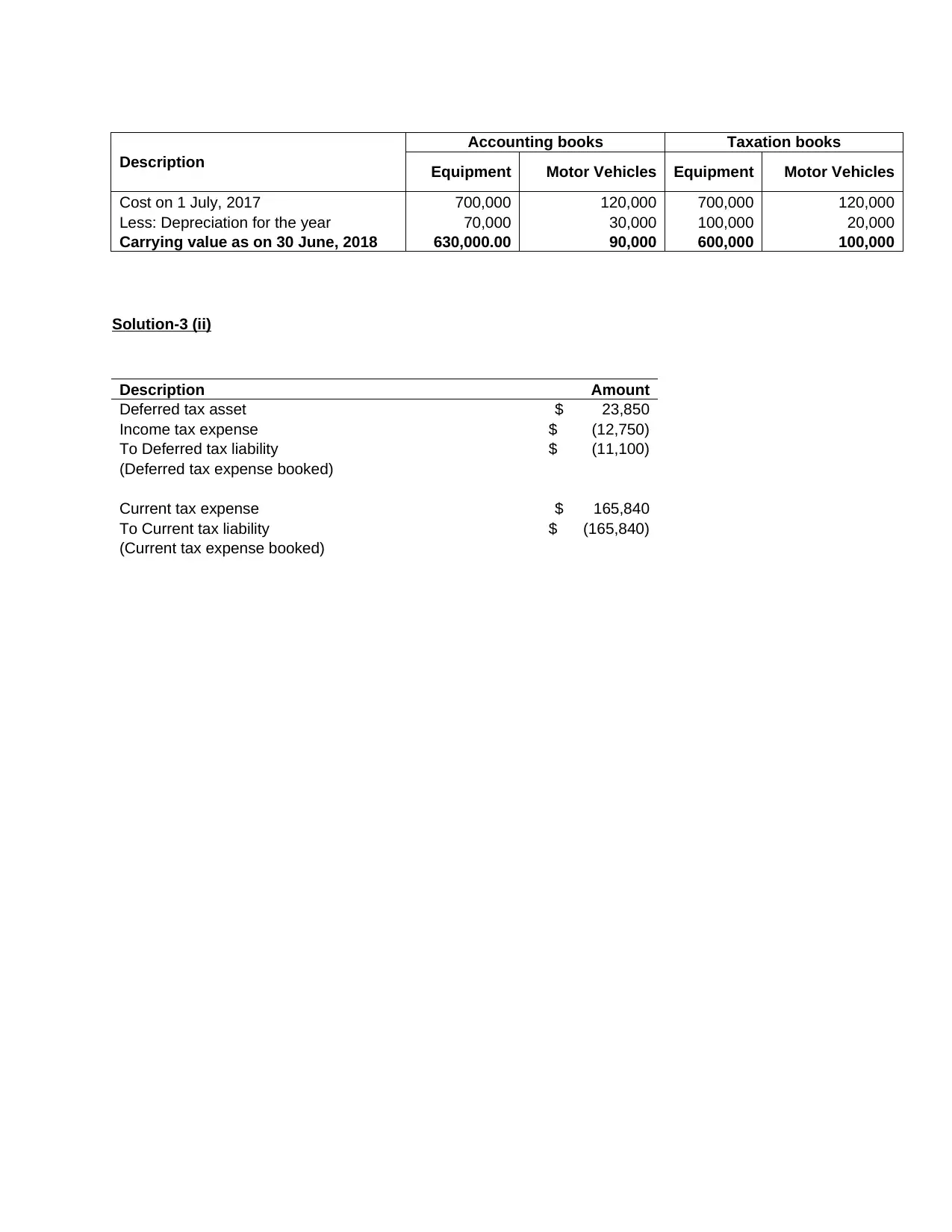

Description

Accounting books Taxation books

Equipment Motor Vehicles Equipment Motor Vehicles

Cost on 1 July, 2017 700,000 120,000 700,000 120,000

Less: Depreciation for the year 70,000 30,000 100,000 20,000

Carrying value as on 30 June, 2018 630,000.00 90,000 600,000 100,000

Solution-3 (ii)

Description Amount

Deferred tax asset $ 23,850

Income tax expense $ (12,750)

To Deferred tax liability $ (11,100)

(Deferred tax expense booked)

Current tax expense $ 165,840

To Current tax liability $ (165,840)

(Current tax expense booked)

Accounting books Taxation books

Equipment Motor Vehicles Equipment Motor Vehicles

Cost on 1 July, 2017 700,000 120,000 700,000 120,000

Less: Depreciation for the year 70,000 30,000 100,000 20,000

Carrying value as on 30 June, 2018 630,000.00 90,000 600,000 100,000

Solution-3 (ii)

Description Amount

Deferred tax asset $ 23,850

Income tax expense $ (12,750)

To Deferred tax liability $ (11,100)

(Deferred tax expense booked)

Current tax expense $ 165,840

To Current tax liability $ (165,840)

(Current tax expense booked)

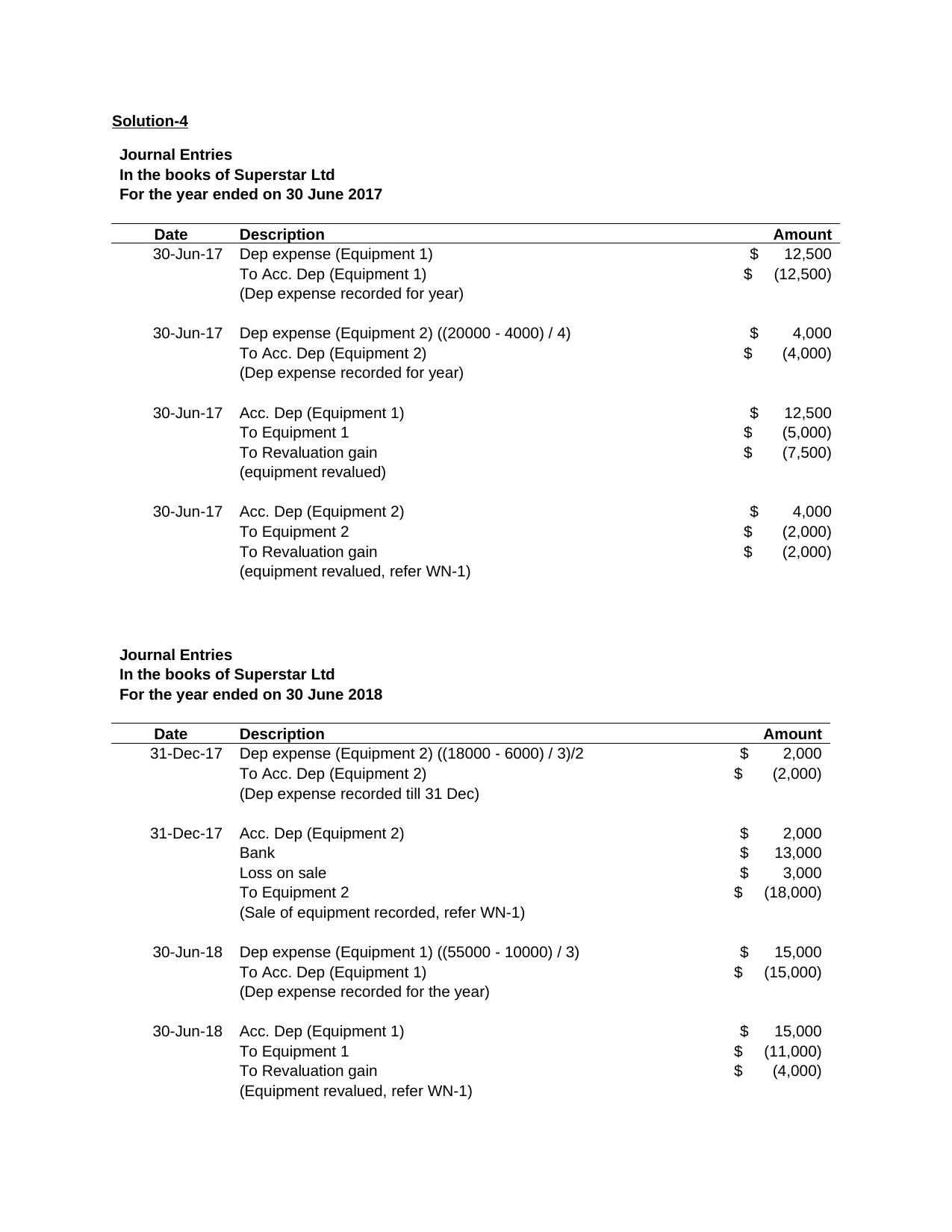

Solution-4

Journal Entries

In the books of Superstar Ltd

For the year ended on 30 June 2017

Date Description Amount

30-Jun-17 Dep expense (Equipment 1) $ 12,500

To Acc. Dep (Equipment 1) $ (12,500)

(Dep expense recorded for year)

30-Jun-17 Dep expense (Equipment 2) ((20000 - 4000) / 4) $ 4,000

To Acc. Dep (Equipment 2) $ (4,000)

(Dep expense recorded for year)

30-Jun-17 Acc. Dep (Equipment 1) $ 12,500

To Equipment 1 $ (5,000)

To Revaluation gain $ (7,500)

(equipment revalued)

30-Jun-17 Acc. Dep (Equipment 2) $ 4,000

To Equipment 2 $ (2,000)

To Revaluation gain $ (2,000)

(equipment revalued, refer WN-1)

Journal Entries

In the books of Superstar Ltd

For the year ended on 30 June 2018

Date Description Amount

31-Dec-17 Dep expense (Equipment 2) ((18000 - 6000) / 3)/2 $ 2,000

To Acc. Dep (Equipment 2) $ (2,000)

(Dep expense recorded till 31 Dec)

31-Dec-17 Acc. Dep (Equipment 2) $ 2,000

Bank $ 13,000

Loss on sale $ 3,000

To Equipment 2 $ (18,000)

(Sale of equipment recorded, refer WN-1)

30-Jun-18 Dep expense (Equipment 1) ((55000 - 10000) / 3) $ 15,000

To Acc. Dep (Equipment 1) $ (15,000)

(Dep expense recorded for the year)

30-Jun-18 Acc. Dep (Equipment 1) $ 15,000

To Equipment 1 $ (11,000)

To Revaluation gain $ (4,000)

(Equipment revalued, refer WN-1)

Journal Entries

In the books of Superstar Ltd

For the year ended on 30 June 2017

Date Description Amount

30-Jun-17 Dep expense (Equipment 1) $ 12,500

To Acc. Dep (Equipment 1) $ (12,500)

(Dep expense recorded for year)

30-Jun-17 Dep expense (Equipment 2) ((20000 - 4000) / 4) $ 4,000

To Acc. Dep (Equipment 2) $ (4,000)

(Dep expense recorded for year)

30-Jun-17 Acc. Dep (Equipment 1) $ 12,500

To Equipment 1 $ (5,000)

To Revaluation gain $ (7,500)

(equipment revalued)

30-Jun-17 Acc. Dep (Equipment 2) $ 4,000

To Equipment 2 $ (2,000)

To Revaluation gain $ (2,000)

(equipment revalued, refer WN-1)

Journal Entries

In the books of Superstar Ltd

For the year ended on 30 June 2018

Date Description Amount

31-Dec-17 Dep expense (Equipment 2) ((18000 - 6000) / 3)/2 $ 2,000

To Acc. Dep (Equipment 2) $ (2,000)

(Dep expense recorded till 31 Dec)

31-Dec-17 Acc. Dep (Equipment 2) $ 2,000

Bank $ 13,000

Loss on sale $ 3,000

To Equipment 2 $ (18,000)

(Sale of equipment recorded, refer WN-1)

30-Jun-18 Dep expense (Equipment 1) ((55000 - 10000) / 3) $ 15,000

To Acc. Dep (Equipment 1) $ (15,000)

(Dep expense recorded for the year)

30-Jun-18 Acc. Dep (Equipment 1) $ 15,000

To Equipment 1 $ (11,000)

To Revaluation gain $ (4,000)

(Equipment revalued, refer WN-1)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

WN-1- Determination of revaluation gain / loss on sale on equipment:

Equipment 1

Determination Amount

As on 30 June, 2017

Fair valued amount $ 55,000

Carrying amount as on 30 June, 2017 (60,000-12,500) $ 47,500

Revaluation gain (55,000-47,500) $ 7,500

As on 30 June, 2018

Fair valued amount $ 44,000

Carrying amount as on 30 June, 2018 (55,000-15,000) $ 40,000

Revaluation gain (44,000-40,000) $ 4,000

Equipment 2

Description Amount

As on 30 June, 2017

Fair valued amount $ 18,000

Carrying amount as on 30 June, 2017 (20,000-4,000) $ 16,000

Revaluation gain (18,000-16,000) $ 2,000

As on 30 June, 2018

Carrying amount as on 31 Dec, 2017 (18,000-2,000) $ 16,000

Proceeds from sale of equipment $ 13,000

Loss on sale of equipment $ 3,000

Equipment 1

Determination Amount

As on 30 June, 2017

Fair valued amount $ 55,000

Carrying amount as on 30 June, 2017 (60,000-12,500) $ 47,500

Revaluation gain (55,000-47,500) $ 7,500

As on 30 June, 2018

Fair valued amount $ 44,000

Carrying amount as on 30 June, 2018 (55,000-15,000) $ 40,000

Revaluation gain (44,000-40,000) $ 4,000

Equipment 2

Description Amount

As on 30 June, 2017

Fair valued amount $ 18,000

Carrying amount as on 30 June, 2017 (20,000-4,000) $ 16,000

Revaluation gain (18,000-16,000) $ 2,000

As on 30 June, 2018

Carrying amount as on 31 Dec, 2017 (18,000-2,000) $ 16,000

Proceeds from sale of equipment $ 13,000

Loss on sale of equipment $ 3,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

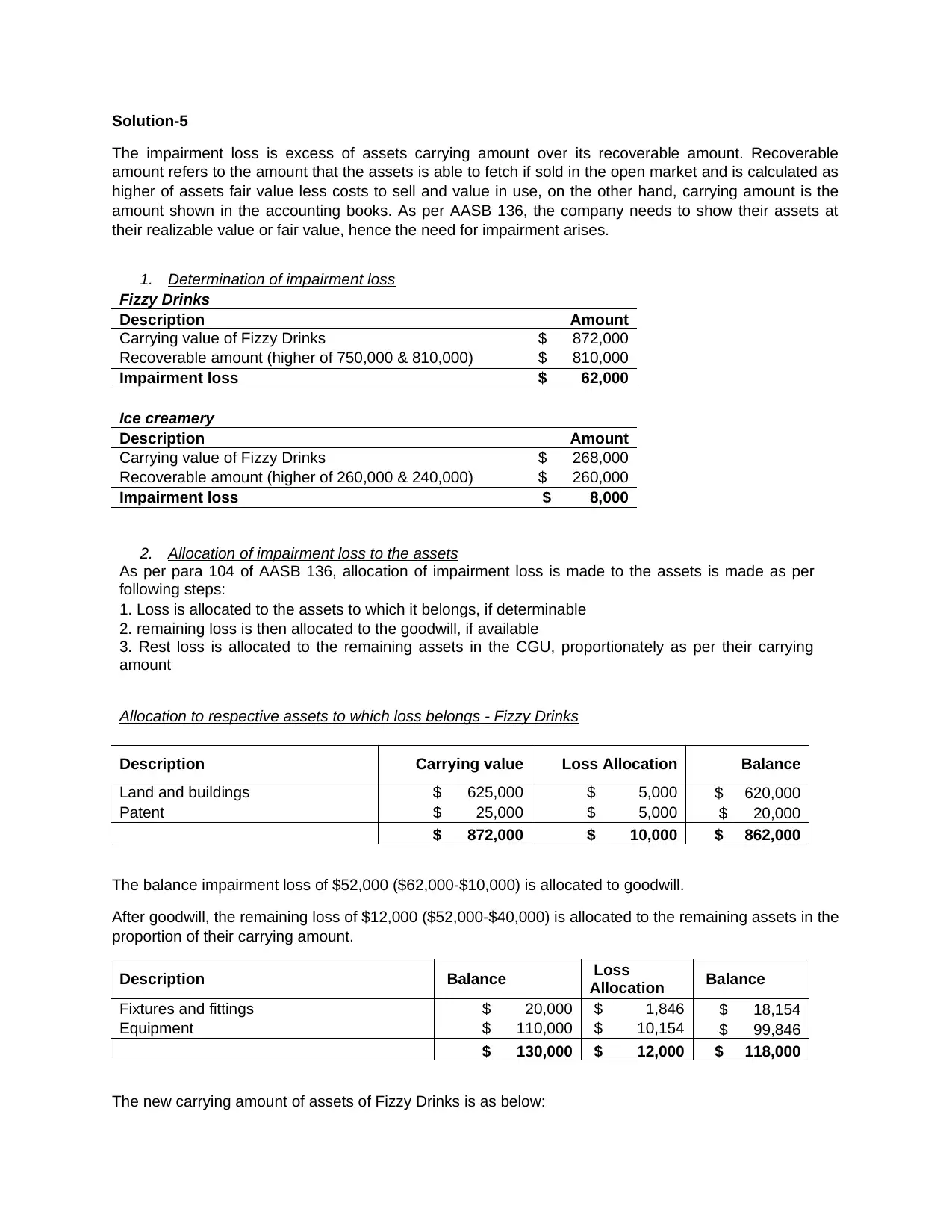

Solution-5

The impairment loss is excess of assets carrying amount over its recoverable amount. Recoverable

amount refers to the amount that the assets is able to fetch if sold in the open market and is calculated as

higher of assets fair value less costs to sell and value in use, on the other hand, carrying amount is the

amount shown in the accounting books. As per AASB 136, the company needs to show their assets at

their realizable value or fair value, hence the need for impairment arises.

1. Determination of impairment loss

Fizzy Drinks

Description Amount

Carrying value of Fizzy Drinks $ 872,000

Recoverable amount (higher of 750,000 & 810,000) $ 810,000

Impairment loss $ 62,000

Ice creamery

Description Amount

Carrying value of Fizzy Drinks $ 268,000

Recoverable amount (higher of 260,000 & 240,000) $ 260,000

Impairment loss $ 8,000

2. Allocation of impairment loss to the assets

As per para 104 of AASB 136, allocation of impairment loss is made to the assets is made as per

following steps:

1. Loss is allocated to the assets to which it belongs, if determinable

2. remaining loss is then allocated to the goodwill, if available

3. Rest loss is allocated to the remaining assets in the CGU, proportionately as per their carrying

amount

Allocation to respective assets to which loss belongs - Fizzy Drinks

Description Carrying value Loss Allocation Balance

Land and buildings $ 625,000 $ 5,000 $ 620,000

Patent $ 25,000 $ 5,000 $ 20,000

$ 872,000 $ 10,000 $ 862,000

The balance impairment loss of $52,000 ($62,000-$10,000) is allocated to goodwill.

After goodwill, the remaining loss of $12,000 ($52,000-$40,000) is allocated to the remaining assets in the

proportion of their carrying amount.

Description Balance Loss

Allocation Balance

Fixtures and fittings $ 20,000 $ 1,846 $ 18,154

Equipment $ 110,000 $ 10,154 $ 99,846

$ 130,000 $ 12,000 $ 118,000

The new carrying amount of assets of Fizzy Drinks is as below:

The impairment loss is excess of assets carrying amount over its recoverable amount. Recoverable

amount refers to the amount that the assets is able to fetch if sold in the open market and is calculated as

higher of assets fair value less costs to sell and value in use, on the other hand, carrying amount is the

amount shown in the accounting books. As per AASB 136, the company needs to show their assets at

their realizable value or fair value, hence the need for impairment arises.

1. Determination of impairment loss

Fizzy Drinks

Description Amount

Carrying value of Fizzy Drinks $ 872,000

Recoverable amount (higher of 750,000 & 810,000) $ 810,000

Impairment loss $ 62,000

Ice creamery

Description Amount

Carrying value of Fizzy Drinks $ 268,000

Recoverable amount (higher of 260,000 & 240,000) $ 260,000

Impairment loss $ 8,000

2. Allocation of impairment loss to the assets

As per para 104 of AASB 136, allocation of impairment loss is made to the assets is made as per

following steps:

1. Loss is allocated to the assets to which it belongs, if determinable

2. remaining loss is then allocated to the goodwill, if available

3. Rest loss is allocated to the remaining assets in the CGU, proportionately as per their carrying

amount

Allocation to respective assets to which loss belongs - Fizzy Drinks

Description Carrying value Loss Allocation Balance

Land and buildings $ 625,000 $ 5,000 $ 620,000

Patent $ 25,000 $ 5,000 $ 20,000

$ 872,000 $ 10,000 $ 862,000

The balance impairment loss of $52,000 ($62,000-$10,000) is allocated to goodwill.

After goodwill, the remaining loss of $12,000 ($52,000-$40,000) is allocated to the remaining assets in the

proportion of their carrying amount.

Description Balance Loss

Allocation Balance

Fixtures and fittings $ 20,000 $ 1,846 $ 18,154

Equipment $ 110,000 $ 10,154 $ 99,846

$ 130,000 $ 12,000 $ 118,000

The new carrying amount of assets of Fizzy Drinks is as below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

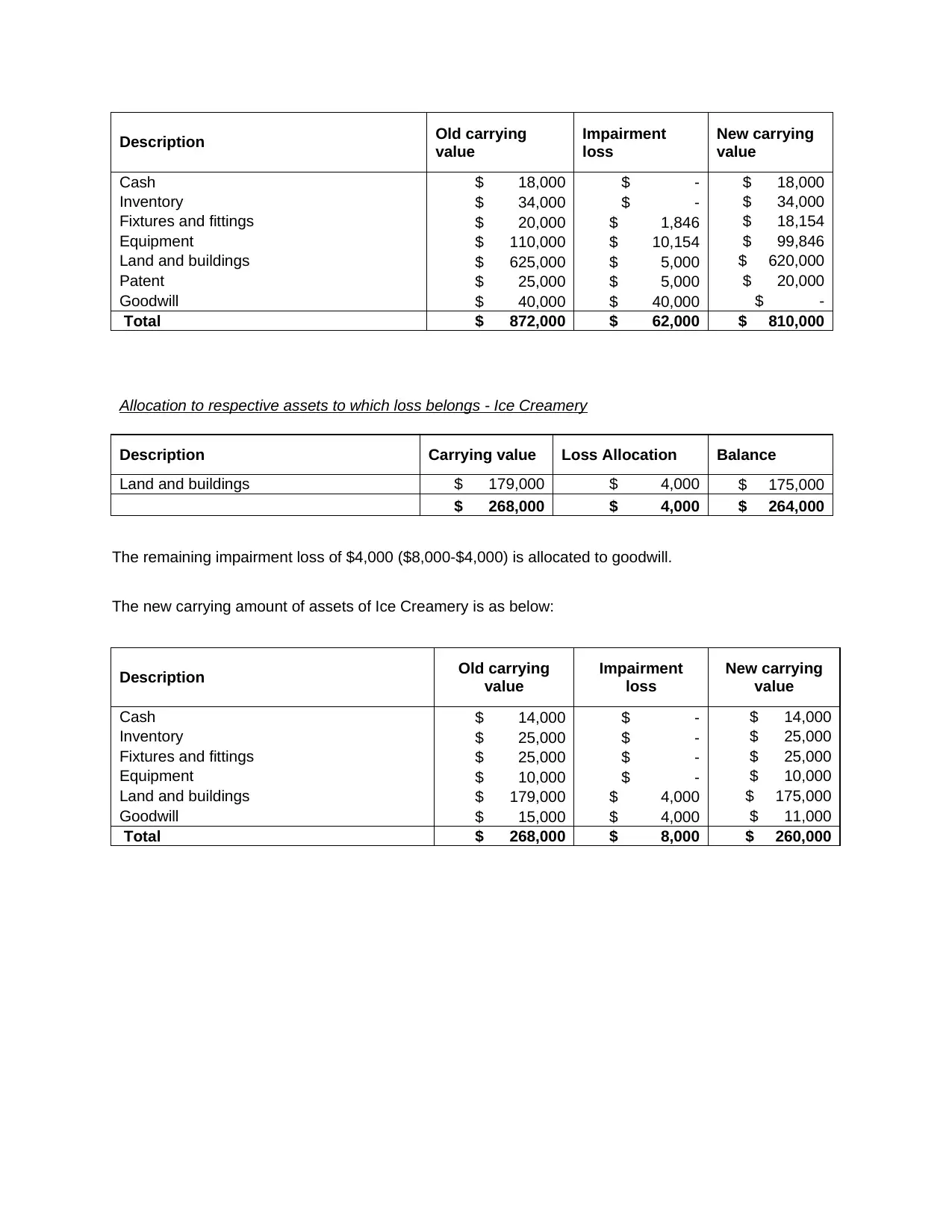

Description Old carrying

value

Impairment

loss

New carrying

value

Cash $ 18,000 $ - $ 18,000

Inventory $ 34,000 $ - $ 34,000

Fixtures and fittings $ 20,000 $ 1,846 $ 18,154

Equipment $ 110,000 $ 10,154 $ 99,846

Land and buildings $ 625,000 $ 5,000 $ 620,000

Patent $ 25,000 $ 5,000 $ 20,000

Goodwill $ 40,000 $ 40,000 $ -

Total $ 872,000 $ 62,000 $ 810,000

Allocation to respective assets to which loss belongs - Ice Creamery

Description Carrying value Loss Allocation Balance

Land and buildings $ 179,000 $ 4,000 $ 175,000

$ 268,000 $ 4,000 $ 264,000

The remaining impairment loss of $4,000 ($8,000-$4,000) is allocated to goodwill.

The new carrying amount of assets of Ice Creamery is as below:

Description Old carrying

value

Impairment

loss

New carrying

value

Cash $ 14,000 $ - $ 14,000

Inventory $ 25,000 $ - $ 25,000

Fixtures and fittings $ 25,000 $ - $ 25,000

Equipment $ 10,000 $ - $ 10,000

Land and buildings $ 179,000 $ 4,000 $ 175,000

Goodwill $ 15,000 $ 4,000 $ 11,000

Total $ 268,000 $ 8,000 $ 260,000

value

Impairment

loss

New carrying

value

Cash $ 18,000 $ - $ 18,000

Inventory $ 34,000 $ - $ 34,000

Fixtures and fittings $ 20,000 $ 1,846 $ 18,154

Equipment $ 110,000 $ 10,154 $ 99,846

Land and buildings $ 625,000 $ 5,000 $ 620,000

Patent $ 25,000 $ 5,000 $ 20,000

Goodwill $ 40,000 $ 40,000 $ -

Total $ 872,000 $ 62,000 $ 810,000

Allocation to respective assets to which loss belongs - Ice Creamery

Description Carrying value Loss Allocation Balance

Land and buildings $ 179,000 $ 4,000 $ 175,000

$ 268,000 $ 4,000 $ 264,000

The remaining impairment loss of $4,000 ($8,000-$4,000) is allocated to goodwill.

The new carrying amount of assets of Ice Creamery is as below:

Description Old carrying

value

Impairment

loss

New carrying

value

Cash $ 14,000 $ - $ 14,000

Inventory $ 25,000 $ - $ 25,000

Fixtures and fittings $ 25,000 $ - $ 25,000

Equipment $ 10,000 $ - $ 10,000

Land and buildings $ 179,000 $ 4,000 $ 175,000

Goodwill $ 15,000 $ 4,000 $ 11,000

Total $ 268,000 $ 8,000 $ 260,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

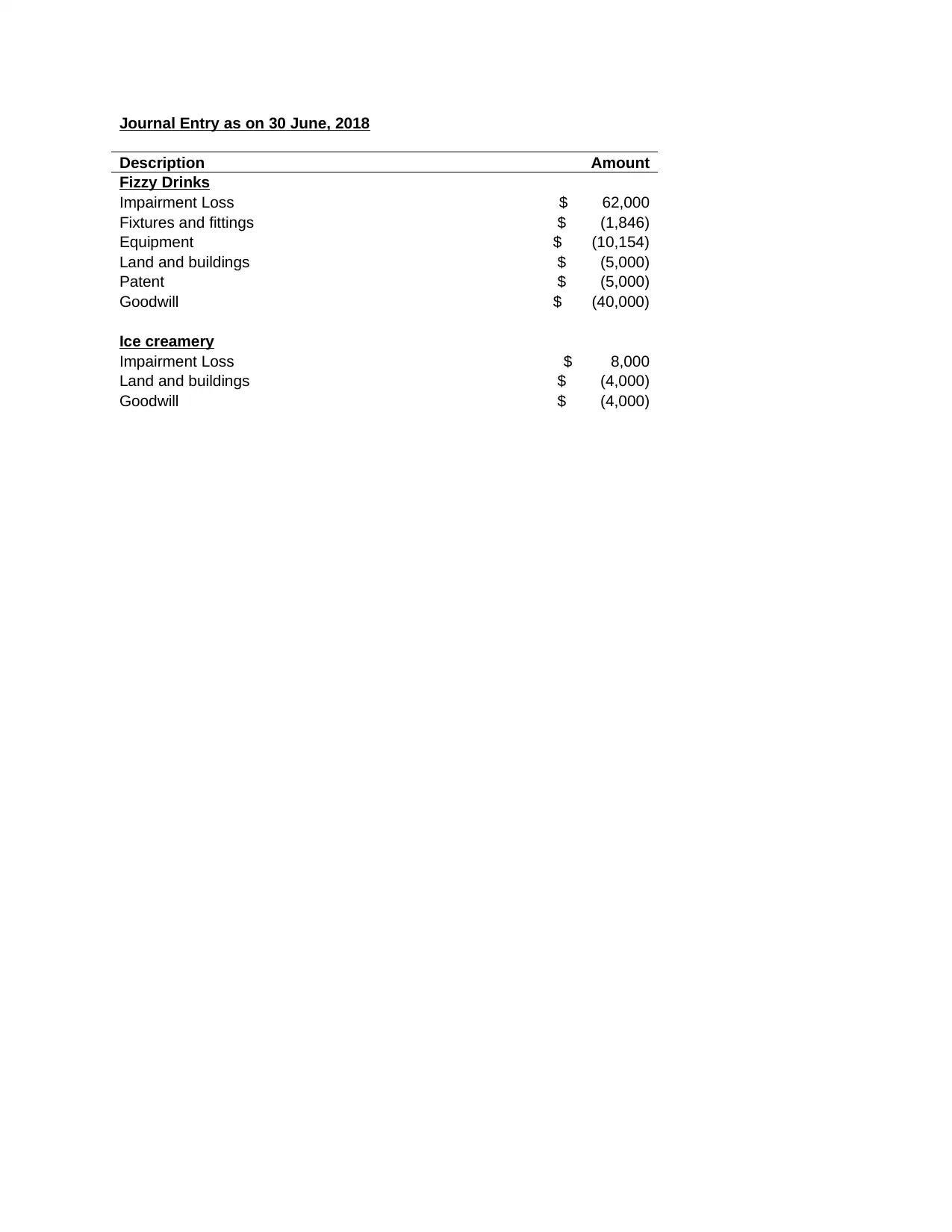

Journal Entry as on 30 June, 2018

Description Amount

Fizzy Drinks

Impairment Loss $ 62,000

Fixtures and fittings $ (1,846)

Equipment $ (10,154)

Land and buildings $ (5,000)

Patent $ (5,000)

Goodwill $ (40,000)

Ice creamery

Impairment Loss $ 8,000

Land and buildings $ (4,000)

Goodwill $ (4,000)

Description Amount

Fizzy Drinks

Impairment Loss $ 62,000

Fixtures and fittings $ (1,846)

Equipment $ (10,154)

Land and buildings $ (5,000)

Patent $ (5,000)

Goodwill $ (40,000)

Ice creamery

Impairment Loss $ 8,000

Land and buildings $ (4,000)

Goodwill $ (4,000)

References:

http://www.aasb.gov.au/admin/file/content105/c9/AASB108_07-04_COMPjan15_07-15.pdf

http://www.aasb.gov.au/admin/file/content105/c9/AASB110_08-15.pdf

https://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

http://www.aasb.gov.au/admin/file/content105/c9/AASB108_07-04_COMPjan15_07-15.pdf

http://www.aasb.gov.au/admin/file/content105/c9/AASB110_08-15.pdf

https://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.