Financial Feasibility Report: ALLCURE Inc - FIN20014, OUA, SP4 2018

VerifiedAdded on 2023/04/22

|20

|3721

|255

Report

AI Summary

This report provides a financial feasibility analysis for ALLCURE Inc., focusing on the production of the P-REC drug and evaluating an alternative, T-REC. The analysis utilizes NPV, IRR, and payback period calculations to determine project viability. Results indicate a positive NPV and acceptable IRR for both P-REC and T-REC. The report recommends considering qualitative factors alongside quantitative results before making a final decision. A detailed comparison of P-REC and T-REC is presented, considering different weighted average costs of capital (WACC) to provide comprehensive recommendations. Ultimately, the report advises ALLCURE Inc. on the financial implications of proceeding with either drug manufacturing project.

Report on Financial Feasibility for ALLCURE Inc.

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report presented here provides an analysis of financial feasibility for ALLCURE Inc.

ALLCURE Inc has a project under consideration. It is considering setting up a manufacturing

facility for manufacturing P-REC drug. The financial results show positive NPV of $932,255.18

and high IRR of 26.71%. Further, the payback period (3.68 years) of the project is also within

the risk appetite of the management. Thus, the project of P-REC manufacture becomes

acceptable for the company. Further, the company can also go for alternative product called T-

REC. This product also has positive outcomes in terms of NPV ($952,662.18), IRR (29.86%),

and payback period (4.06 years). However, when comparing the payback period of two products

at WACC of 24%, it is found that P-REC is better than T-REC.

2

The report presented here provides an analysis of financial feasibility for ALLCURE Inc.

ALLCURE Inc has a project under consideration. It is considering setting up a manufacturing

facility for manufacturing P-REC drug. The financial results show positive NPV of $932,255.18

and high IRR of 26.71%. Further, the payback period (3.68 years) of the project is also within

the risk appetite of the management. Thus, the project of P-REC manufacture becomes

acceptable for the company. Further, the company can also go for alternative product called T-

REC. This product also has positive outcomes in terms of NPV ($952,662.18), IRR (29.86%),

and payback period (4.06 years). However, when comparing the payback period of two products

at WACC of 24%, it is found that P-REC is better than T-REC.

2

Contents

Introduction.................................................................................................................................................4

Findings.......................................................................................................................................................4

Quantitative.............................................................................................................................................4

Qualitative...............................................................................................................................................5

Recommendations and Justifications...........................................................................................................6

Detailed Comparison of P-REC and T-REC and Further Recommendations..............................................6

Conclusion...................................................................................................................................................8

References...................................................................................................................................................9

Appendix...................................................................................................................................................10

3

Introduction.................................................................................................................................................4

Findings.......................................................................................................................................................4

Quantitative.............................................................................................................................................4

Qualitative...............................................................................................................................................5

Recommendations and Justifications...........................................................................................................6

Detailed Comparison of P-REC and T-REC and Further Recommendations..............................................6

Conclusion...................................................................................................................................................8

References...................................................................................................................................................9

Appendix...................................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Assessing the financial feasibility is essential to ensure that the project under

consideration would be profitable for the company. With this aim, the firms conduct financial

feasibility of a project which involves evaluating project’s NPV, IRR, and payback period

(Rossi, 2015). The NPV evaluation among all is considered to be the most significant and thus,

the decision to accept or reject the project revolves around the result of NPV. As a thumb rule, if

the NPV is positive, the project is considered for implementation else it is rejected and the

proposal is turned down. In the current case, ALLCURE Inc is considering implementing a

project which involves developing a drug prototype called P-REC. Further, the company also

wishes to check the financial feasibility of an alternative of the prototype called T-REC. In this

connection, this report has been prepared with a view to assess the financial feasibility of P-REC

and T-REC by applying the tools such as NPV, IRR, payback period, and cross rate analysis.

Findings

Quantitative

Quantitative analysis is conducted applying mathematical tools and techniques. The

capital budgeting tools are applied to conduct quantitative analysis which involves application of

NPV, IRR, and payback period (Vecchi and Casalini, 2018). ALLCURE Inc is considering

setting up a production line for manufacturing of P-REC drug. This project involves huge capital

investments so it becomes essential for the company to evaluate that whether the project would

provide adequate returns or not.

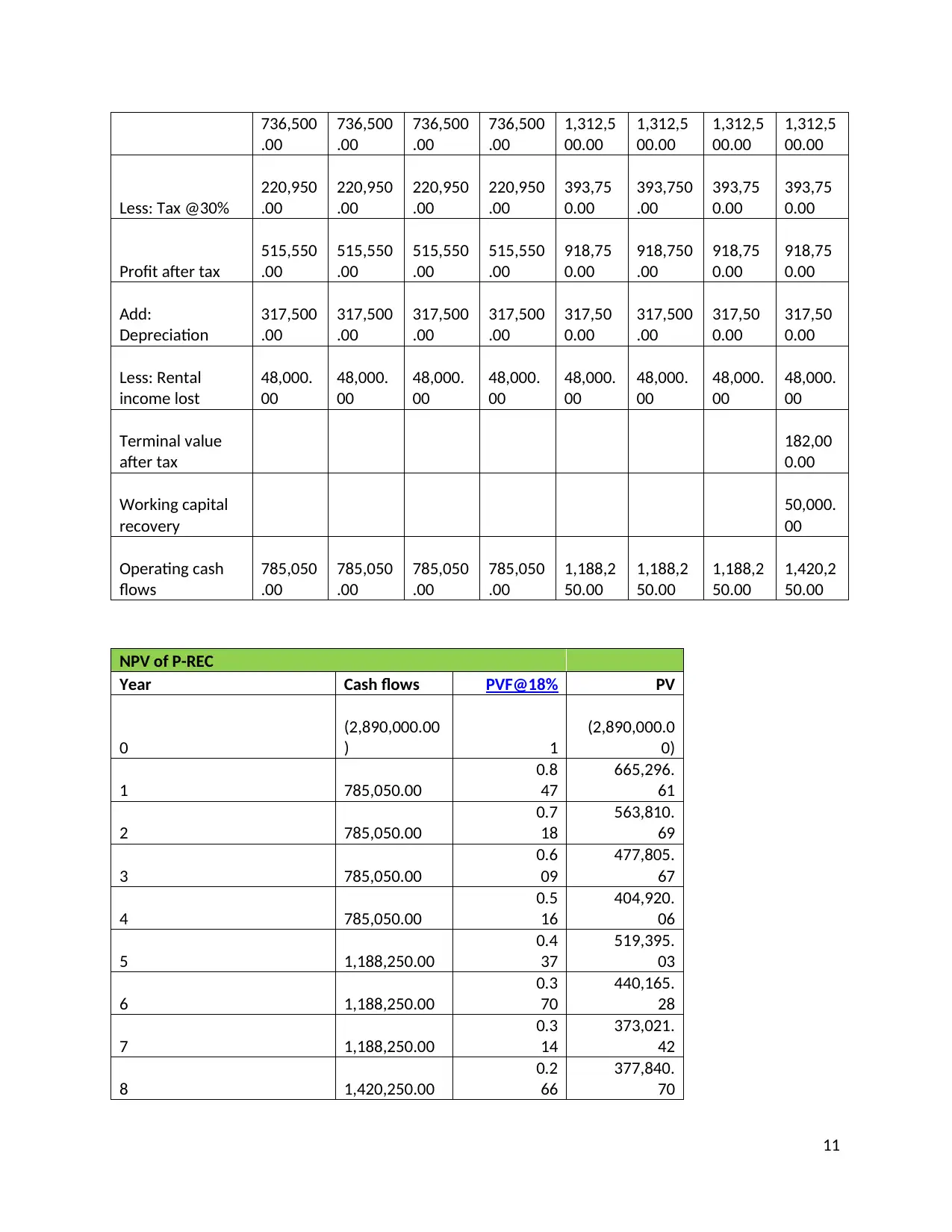

Net Present Value of the Project

The net present value is computed by deducting the present value of all future cash

inflows expected from the project over its life time from the initial investment. The present

values of the cash inflows of the project are computed by discounting the cash inflows at an

appropriate discount rate. The appropriate discount rate is taken at weighted average cost of

capital of the firm. However, the estimation of weighted average cost of capital quite tricky and

it involves consideration of several factors (Goyat and Nain, 2016).

The net present value of P-REC is worked out to be $932,255.45 which indicates that the

project is financially viable. This net present value has been worked out by deducting present

4

Assessing the financial feasibility is essential to ensure that the project under

consideration would be profitable for the company. With this aim, the firms conduct financial

feasibility of a project which involves evaluating project’s NPV, IRR, and payback period

(Rossi, 2015). The NPV evaluation among all is considered to be the most significant and thus,

the decision to accept or reject the project revolves around the result of NPV. As a thumb rule, if

the NPV is positive, the project is considered for implementation else it is rejected and the

proposal is turned down. In the current case, ALLCURE Inc is considering implementing a

project which involves developing a drug prototype called P-REC. Further, the company also

wishes to check the financial feasibility of an alternative of the prototype called T-REC. In this

connection, this report has been prepared with a view to assess the financial feasibility of P-REC

and T-REC by applying the tools such as NPV, IRR, payback period, and cross rate analysis.

Findings

Quantitative

Quantitative analysis is conducted applying mathematical tools and techniques. The

capital budgeting tools are applied to conduct quantitative analysis which involves application of

NPV, IRR, and payback period (Vecchi and Casalini, 2018). ALLCURE Inc is considering

setting up a production line for manufacturing of P-REC drug. This project involves huge capital

investments so it becomes essential for the company to evaluate that whether the project would

provide adequate returns or not.

Net Present Value of the Project

The net present value is computed by deducting the present value of all future cash

inflows expected from the project over its life time from the initial investment. The present

values of the cash inflows of the project are computed by discounting the cash inflows at an

appropriate discount rate. The appropriate discount rate is taken at weighted average cost of

capital of the firm. However, the estimation of weighted average cost of capital quite tricky and

it involves consideration of several factors (Goyat and Nain, 2016).

The net present value of P-REC is worked out to be $932,255.45 which indicates that the

project is financially viable. This net present value has been worked out by deducting present

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

value of cash inflows of 8 years from the initial investment amount. The amount of initial

investment is worked out to be $2,890,000. The amount of present value of net cash inflows over

the period of 8 years is worked out to be $8,125,200. It could be observed that the cash inflows

for the first 4 years are lesser as compared to the cash inflows of last 4 years. The company

would be operating at 100% capacity from the 5th year onward which will cause the cash inflows

to increase substantially.

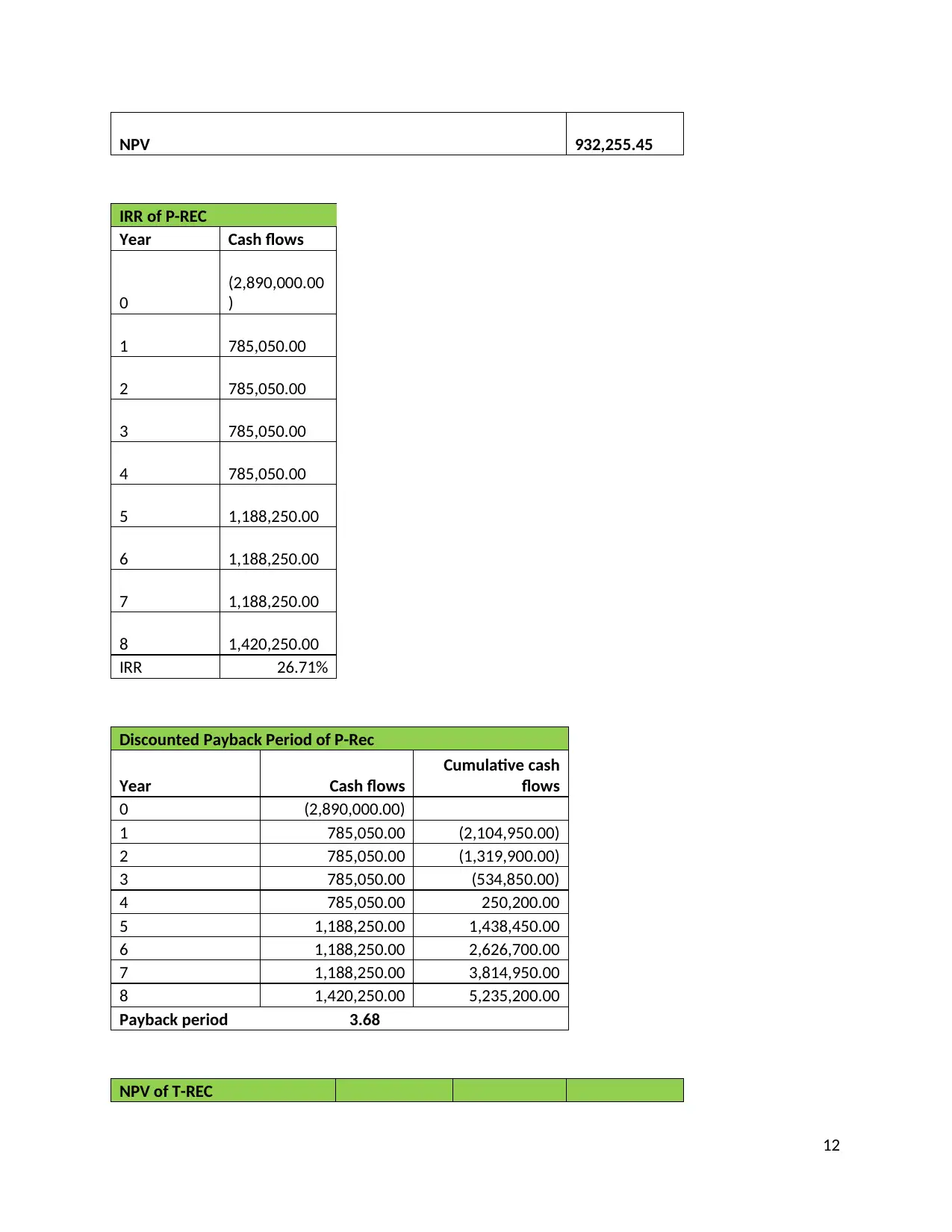

Internal Rate of Return (IRR)

Internal rate of return plays a crucial role in analyzing a project’s financial feasibility.

Internal rate of return is the cut off rate at which the project neither earns positive NPV nor

incurs loss (Kerzner and Kerzner, 2017). So, the NPV is zero at internal rate of return. This

implies that the project’s IRR should be higher than the discount rate to make it a feasible choice

for the company. In the case of P-REC, the IRR of the project has been worked out to be 26.71%

which is higher than the discount rate of 18%. This indicates that the project is financially viable.

Payback Period

Apart from the above discussed two capital budgeting tools, payback period is another

important tool. Payback period is calculated to know the time period to be taken in the recovery

of the initial investment amount. The company would accept a project with lower payback

period. In the current case, the management of ALLCURE Inc apprehends that the payback

period of the project should be 5 years or less. The payback period of P-REC is worked out to be

3.68 years which is lower than what the management apprehends. So, the project becomes

acceptable for ALLCURE Inc.

Qualitative

It could be seen the quantitative analysis discussed above shows that the project of P-

REC is financially viable. However, it is pertinent to note here that the decision to accept the

proposal and move forward with its implementation does not only depend upon the quantitative

analysis, a qualitative analysis of the project is also necessary. The qualitative analysis entails

analysis of the project’s implementation effects on operational aspects of the firm (Hartas, 2015).

In the case of ALLCURE Inc, the management should consider the effect of implementation of

P-REC project on the sale of its existing products also. It is quite possible that the sale of P-REC

5

investment is worked out to be $2,890,000. The amount of present value of net cash inflows over

the period of 8 years is worked out to be $8,125,200. It could be observed that the cash inflows

for the first 4 years are lesser as compared to the cash inflows of last 4 years. The company

would be operating at 100% capacity from the 5th year onward which will cause the cash inflows

to increase substantially.

Internal Rate of Return (IRR)

Internal rate of return plays a crucial role in analyzing a project’s financial feasibility.

Internal rate of return is the cut off rate at which the project neither earns positive NPV nor

incurs loss (Kerzner and Kerzner, 2017). So, the NPV is zero at internal rate of return. This

implies that the project’s IRR should be higher than the discount rate to make it a feasible choice

for the company. In the case of P-REC, the IRR of the project has been worked out to be 26.71%

which is higher than the discount rate of 18%. This indicates that the project is financially viable.

Payback Period

Apart from the above discussed two capital budgeting tools, payback period is another

important tool. Payback period is calculated to know the time period to be taken in the recovery

of the initial investment amount. The company would accept a project with lower payback

period. In the current case, the management of ALLCURE Inc apprehends that the payback

period of the project should be 5 years or less. The payback period of P-REC is worked out to be

3.68 years which is lower than what the management apprehends. So, the project becomes

acceptable for ALLCURE Inc.

Qualitative

It could be seen the quantitative analysis discussed above shows that the project of P-

REC is financially viable. However, it is pertinent to note here that the decision to accept the

proposal and move forward with its implementation does not only depend upon the quantitative

analysis, a qualitative analysis of the project is also necessary. The qualitative analysis entails

analysis of the project’s implementation effects on operational aspects of the firm (Hartas, 2015).

In the case of ALLCURE Inc, the management should consider the effect of implementation of

P-REC project on the sale of its existing products also. It is quite possible that the sale of P-REC

5

would affect the existing customers of the company. Further, the company should also consider

the ethical aspects also. For instance, it would be advisable for the company to consider that if

the use of P-REC would be advantageous to its customers or not. If the use of P-REC is expected

to put the health and life of its users in danger, the company should refrain from implementing

the project (Hartas, 2015).

Recommendations and Justifications

On the basis of analysis conducted above, it could be recommended that the project is

financially viable therefore the company can go ahead with its implementation. However, there

are several qualitative concerns also that the management should take into account before taking

the final decision. The project is absolutely acceptable if decision is based purely on financial

grounds.

Detailed Comparison of P-REC and T-REC and Further Recommendations

The company is considering establishing a manufacturing line for P-REC drug. The

financial evaluation of P-REC shows that the project is financial viable. However, the company

also has an alternative product of P-REC which is called T-REC. The company can manufacture

T-REC with the same production line and facilities as needed for P-REC. The results of financial

analysis of T-REC show that the NPV of T-REC is $952,662.18 which shows that this product is

also profitable. Further, the IRR of T-REC is worked out to be 29.86% and payback period is

4.06 years.

6

the ethical aspects also. For instance, it would be advisable for the company to consider that if

the use of P-REC would be advantageous to its customers or not. If the use of P-REC is expected

to put the health and life of its users in danger, the company should refrain from implementing

the project (Hartas, 2015).

Recommendations and Justifications

On the basis of analysis conducted above, it could be recommended that the project is

financially viable therefore the company can go ahead with its implementation. However, there

are several qualitative concerns also that the management should take into account before taking

the final decision. The project is absolutely acceptable if decision is based purely on financial

grounds.

Detailed Comparison of P-REC and T-REC and Further Recommendations

The company is considering establishing a manufacturing line for P-REC drug. The

financial evaluation of P-REC shows that the project is financial viable. However, the company

also has an alternative product of P-REC which is called T-REC. The company can manufacture

T-REC with the same production line and facilities as needed for P-REC. The results of financial

analysis of T-REC show that the NPV of T-REC is $952,662.18 which shows that this product is

also profitable. Further, the IRR of T-REC is worked out to be 29.86% and payback period is

4.06 years.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

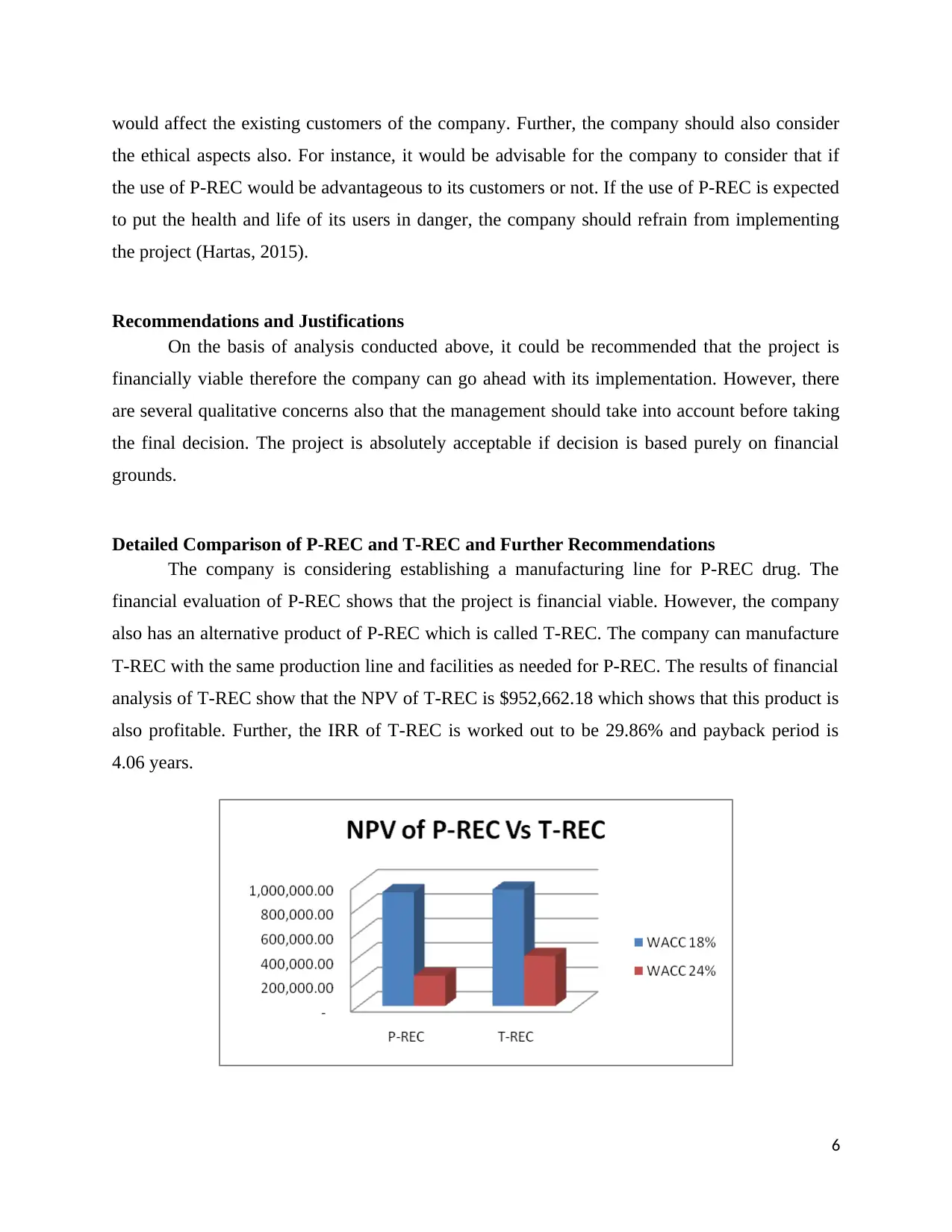

The chart above shows a comparison of NPV of P-REC and T-REC. It could be observed

that the NPV of P-REC is $932,255.45 which is lower than the NPV of T-REC of $952,662.18.

However, the difference in NPV is not significant but T-REC is more profitable than P-REC.

The NPV of T-REC is better due to its cash inflows being higher as compared to P-REC. A

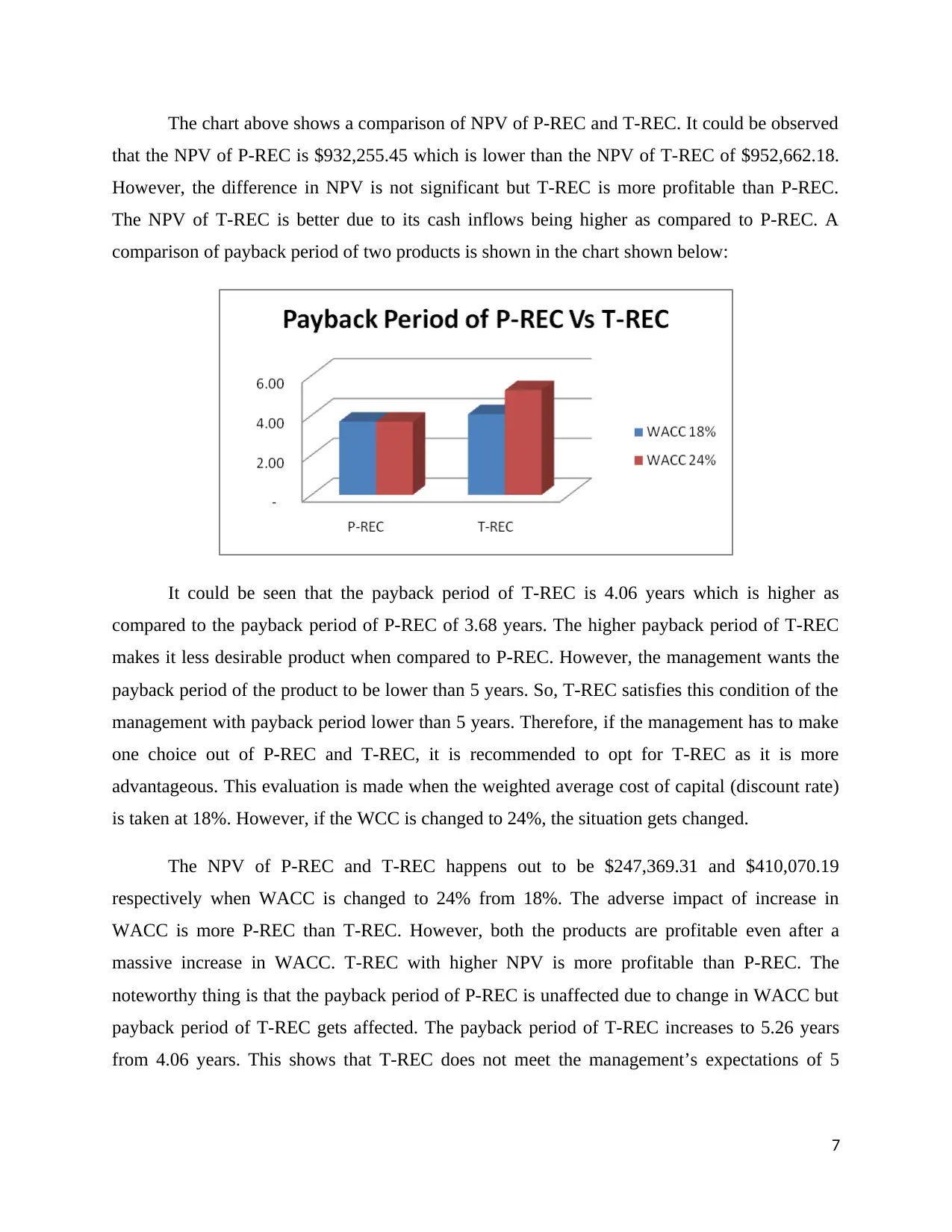

comparison of payback period of two products is shown in the chart shown below:

It could be seen that the payback period of T-REC is 4.06 years which is higher as

compared to the payback period of P-REC of 3.68 years. The higher payback period of T-REC

makes it less desirable product when compared to P-REC. However, the management wants the

payback period of the product to be lower than 5 years. So, T-REC satisfies this condition of the

management with payback period lower than 5 years. Therefore, if the management has to make

one choice out of P-REC and T-REC, it is recommended to opt for T-REC as it is more

advantageous. This evaluation is made when the weighted average cost of capital (discount rate)

is taken at 18%. However, if the WCC is changed to 24%, the situation gets changed.

The NPV of P-REC and T-REC happens out to be $247,369.31 and $410,070.19

respectively when WACC is changed to 24% from 18%. The adverse impact of increase in

WACC is more P-REC than T-REC. However, both the products are profitable even after a

massive increase in WACC. T-REC with higher NPV is more profitable than P-REC. The

noteworthy thing is that the payback period of P-REC is unaffected due to change in WACC but

payback period of T-REC gets affected. The payback period of T-REC increases to 5.26 years

from 4.06 years. This shows that T-REC does not meet the management’s expectations of 5

7

that the NPV of P-REC is $932,255.45 which is lower than the NPV of T-REC of $952,662.18.

However, the difference in NPV is not significant but T-REC is more profitable than P-REC.

The NPV of T-REC is better due to its cash inflows being higher as compared to P-REC. A

comparison of payback period of two products is shown in the chart shown below:

It could be seen that the payback period of T-REC is 4.06 years which is higher as

compared to the payback period of P-REC of 3.68 years. The higher payback period of T-REC

makes it less desirable product when compared to P-REC. However, the management wants the

payback period of the product to be lower than 5 years. So, T-REC satisfies this condition of the

management with payback period lower than 5 years. Therefore, if the management has to make

one choice out of P-REC and T-REC, it is recommended to opt for T-REC as it is more

advantageous. This evaluation is made when the weighted average cost of capital (discount rate)

is taken at 18%. However, if the WCC is changed to 24%, the situation gets changed.

The NPV of P-REC and T-REC happens out to be $247,369.31 and $410,070.19

respectively when WACC is changed to 24% from 18%. The adverse impact of increase in

WACC is more P-REC than T-REC. However, both the products are profitable even after a

massive increase in WACC. T-REC with higher NPV is more profitable than P-REC. The

noteworthy thing is that the payback period of P-REC is unaffected due to change in WACC but

payback period of T-REC gets affected. The payback period of T-REC increases to 5.26 years

from 4.06 years. This shows that T-REC does not meet the management’s expectations of 5

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

years payback period at 24% WACC. Therefore, if the WACC is 24%, it is recommended to the

management to opt for P-REC.

Conclusion

It is essential to conduct the quantitative as well as qualitative analysis of the project

before locking into a decision of investment. In this report the quantitative and qualitative

analysis has been conducted for ALLCURE Inc which is considering implementing a project for

manufacturing of drugs. The results of analysis show that P-REC product is profitable and hence

the company can go ahead with its production plan. However, there is another good option

available in the name of T-REC which is also equally good but when compared at 24% WACC;

it becomes less desirable due to higher payback period of 5.26 years.

8

management to opt for P-REC.

Conclusion

It is essential to conduct the quantitative as well as qualitative analysis of the project

before locking into a decision of investment. In this report the quantitative and qualitative

analysis has been conducted for ALLCURE Inc which is considering implementing a project for

manufacturing of drugs. The results of analysis show that P-REC product is profitable and hence

the company can go ahead with its production plan. However, there is another good option

available in the name of T-REC which is also equally good but when compared at 24% WACC;

it becomes less desirable due to higher payback period of 5.26 years.

8

References

Goyat, S. and Nain, A., 2016. Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), pp.278-280.

Hartas, D. ed., 2015. Educational research and inquiry: Qualitative and quantitative

approaches. Bloomsbury Publishing.

Kerzner, H. and Kerzner, H.R., 2017. Project management: a systems approach to planning,

scheduling, and controlling. John Wiley & Sons.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

Vecchi, V. and Casalini, F., 2018. Principles of Capital Budgeting for the Assessment of PPP

Projects. In Public-Private Partnerships in Health (pp. 65-84). Palgrave Macmillan, Cham.

9

Goyat, S. and Nain, A., 2016. Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), pp.278-280.

Hartas, D. ed., 2015. Educational research and inquiry: Qualitative and quantitative

approaches. Bloomsbury Publishing.

Kerzner, H. and Kerzner, H.R., 2017. Project management: a systems approach to planning,

scheduling, and controlling. John Wiley & Sons.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

Vecchi, V. and Casalini, F., 2018. Principles of Capital Budgeting for the Assessment of PPP

Projects. In Public-Private Partnerships in Health (pp. 65-84). Palgrave Macmillan, Cham.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

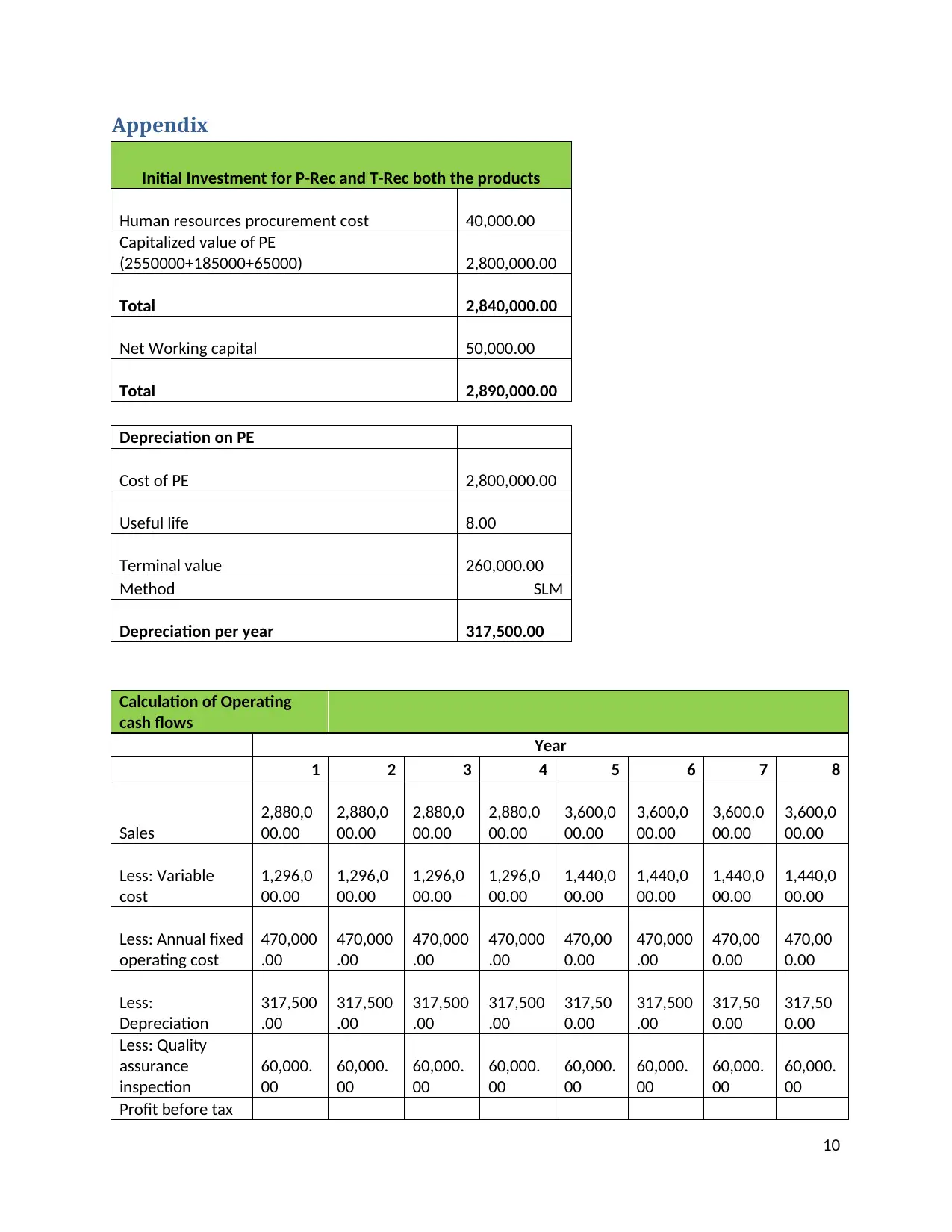

Appendix

Initial Investment for P-Rec and T-Rec both the products

Human resources procurement cost 40,000.00

Capitalized value of PE

(2550000+185000+65000) 2,800,000.00

Total 2,840,000.00

Net Working capital 50,000.00

Total 2,890,000.00

Depreciation on PE

Cost of PE 2,800,000.00

Useful life 8.00

Terminal value 260,000.00

Method SLM

Depreciation per year 317,500.00

Calculation of Operating

cash flows

Year

1 2 3 4 5 6 7 8

Sales

2,880,0

00.00

2,880,0

00.00

2,880,0

00.00

2,880,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

Less: Variable

cost

1,296,0

00.00

1,296,0

00.00

1,296,0

00.00

1,296,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

Less: Annual fixed

operating cost

470,000

.00

470,000

.00

470,000

.00

470,000

.00

470,00

0.00

470,000

.00

470,00

0.00

470,00

0.00

Less:

Depreciation

317,500

.00

317,500

.00

317,500

.00

317,500

.00

317,50

0.00

317,500

.00

317,50

0.00

317,50

0.00

Less: Quality

assurance

inspection

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

Profit before tax

10

Initial Investment for P-Rec and T-Rec both the products

Human resources procurement cost 40,000.00

Capitalized value of PE

(2550000+185000+65000) 2,800,000.00

Total 2,840,000.00

Net Working capital 50,000.00

Total 2,890,000.00

Depreciation on PE

Cost of PE 2,800,000.00

Useful life 8.00

Terminal value 260,000.00

Method SLM

Depreciation per year 317,500.00

Calculation of Operating

cash flows

Year

1 2 3 4 5 6 7 8

Sales

2,880,0

00.00

2,880,0

00.00

2,880,0

00.00

2,880,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

Less: Variable

cost

1,296,0

00.00

1,296,0

00.00

1,296,0

00.00

1,296,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

Less: Annual fixed

operating cost

470,000

.00

470,000

.00

470,000

.00

470,000

.00

470,00

0.00

470,000

.00

470,00

0.00

470,00

0.00

Less:

Depreciation

317,500

.00

317,500

.00

317,500

.00

317,500

.00

317,50

0.00

317,500

.00

317,50

0.00

317,50

0.00

Less: Quality

assurance

inspection

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

Profit before tax

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

736,500

.00

736,500

.00

736,500

.00

736,500

.00

1,312,5

00.00

1,312,5

00.00

1,312,5

00.00

1,312,5

00.00

Less: Tax @30%

220,950

.00

220,950

.00

220,950

.00

220,950

.00

393,75

0.00

393,750

.00

393,75

0.00

393,75

0.00

Profit after tax

515,550

.00

515,550

.00

515,550

.00

515,550

.00

918,75

0.00

918,750

.00

918,75

0.00

918,75

0.00

Add:

Depreciation

317,500

.00

317,500

.00

317,500

.00

317,500

.00

317,50

0.00

317,500

.00

317,50

0.00

317,50

0.00

Less: Rental

income lost

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

Terminal value

after tax

182,00

0.00

Working capital

recovery

50,000.

00

Operating cash

flows

785,050

.00

785,050

.00

785,050

.00

785,050

.00

1,188,2

50.00

1,188,2

50.00

1,188,2

50.00

1,420,2

50.00

NPV of P-REC

Year Cash flows PVF@18% PV

0

(2,890,000.00

) 1

(2,890,000.0

0)

1 785,050.00

0.8

47

665,296.

61

2 785,050.00

0.7

18

563,810.

69

3 785,050.00

0.6

09

477,805.

67

4 785,050.00

0.5

16

404,920.

06

5 1,188,250.00

0.4

37

519,395.

03

6 1,188,250.00

0.3

70

440,165.

28

7 1,188,250.00

0.3

14

373,021.

42

8 1,420,250.00

0.2

66

377,840.

70

11

.00

736,500

.00

736,500

.00

736,500

.00

1,312,5

00.00

1,312,5

00.00

1,312,5

00.00

1,312,5

00.00

Less: Tax @30%

220,950

.00

220,950

.00

220,950

.00

220,950

.00

393,75

0.00

393,750

.00

393,75

0.00

393,75

0.00

Profit after tax

515,550

.00

515,550

.00

515,550

.00

515,550

.00

918,75

0.00

918,750

.00

918,75

0.00

918,75

0.00

Add:

Depreciation

317,500

.00

317,500

.00

317,500

.00

317,500

.00

317,50

0.00

317,500

.00

317,50

0.00

317,50

0.00

Less: Rental

income lost

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

Terminal value

after tax

182,00

0.00

Working capital

recovery

50,000.

00

Operating cash

flows

785,050

.00

785,050

.00

785,050

.00

785,050

.00

1,188,2

50.00

1,188,2

50.00

1,188,2

50.00

1,420,2

50.00

NPV of P-REC

Year Cash flows PVF@18% PV

0

(2,890,000.00

) 1

(2,890,000.0

0)

1 785,050.00

0.8

47

665,296.

61

2 785,050.00

0.7

18

563,810.

69

3 785,050.00

0.6

09

477,805.

67

4 785,050.00

0.5

16

404,920.

06

5 1,188,250.00

0.4

37

519,395.

03

6 1,188,250.00

0.3

70

440,165.

28

7 1,188,250.00

0.3

14

373,021.

42

8 1,420,250.00

0.2

66

377,840.

70

11

NPV 932,255.45

IRR of P-REC

Year Cash flows

0

(2,890,000.00

)

1 785,050.00

2 785,050.00

3 785,050.00

4 785,050.00

5 1,188,250.00

6 1,188,250.00

7 1,188,250.00

8 1,420,250.00

IRR 26.71%

Discounted Payback Period of P-Rec

Year Cash flows

Cumulative cash

flows

0 (2,890,000.00)

1 785,050.00 (2,104,950.00)

2 785,050.00 (1,319,900.00)

3 785,050.00 (534,850.00)

4 785,050.00 250,200.00

5 1,188,250.00 1,438,450.00

6 1,188,250.00 2,626,700.00

7 1,188,250.00 3,814,950.00

8 1,420,250.00 5,235,200.00

Payback period 3.68

NPV of T-REC

12

IRR of P-REC

Year Cash flows

0

(2,890,000.00

)

1 785,050.00

2 785,050.00

3 785,050.00

4 785,050.00

5 1,188,250.00

6 1,188,250.00

7 1,188,250.00

8 1,420,250.00

IRR 26.71%

Discounted Payback Period of P-Rec

Year Cash flows

Cumulative cash

flows

0 (2,890,000.00)

1 785,050.00 (2,104,950.00)

2 785,050.00 (1,319,900.00)

3 785,050.00 (534,850.00)

4 785,050.00 250,200.00

5 1,188,250.00 1,438,450.00

6 1,188,250.00 2,626,700.00

7 1,188,250.00 3,814,950.00

8 1,420,250.00 5,235,200.00

Payback period 3.68

NPV of T-REC

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.