Analysis of Corporate Governance and Financial Issues at Carillion Plc

VerifiedAdded on 2023/01/07

|12

|3947

|1

Report

AI Summary

This report provides a comprehensive analysis of the corporate governance practices of Carillion Plc, focusing on the company's adherence to the UK corporate governance code. It delves into the specific financial governance aspects, including the roles of the board of directors, shareholders, and auditors in ensuring financial accountability. The report discusses key financial tools and ratios, such as gearing ratio, remuneration, and profit after tax, and examines the company's compliance with regulations like acting within power, common law principles, and listing rules. Furthermore, the report highlights financial governance issues, such as remuneration of board of directors, and executive pay, and the impact of these issues on the company's financial performance. The report concludes with an overview of the importance of corporate governance in maintaining financial stability and ethical business practices, making it a valuable resource for students studying finance and corporate governance. The report also touches upon the role of company's audit and its importance. The report also discusses the remuneration of the board of directors and executive pay.

Corporate Governance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................3

MAIN BODY........................................................................................................................................3

Company’s duty to comply with UK corporate governance..............................................................3

Financial governance issues...............................................................................................................7

CONCLUSION.....................................................................................................................................9

REFERENCES....................................................................................................................................11

INTRODUCTION

Corporate governance is defined as the collection of mechanism, processes and

relationship by which corporations with other stakeholders involved in the business can be

INTRODUCTION.................................................................................................................................3

MAIN BODY........................................................................................................................................3

Company’s duty to comply with UK corporate governance..............................................................3

Financial governance issues...............................................................................................................7

CONCLUSION.....................................................................................................................................9

REFERENCES....................................................................................................................................11

INTRODUCTION

Corporate governance is defined as the collection of mechanism, processes and

relationship by which corporations with other stakeholders involved in the business can be

controlled and operated. This report is based on the case study of Carillion Plc Company in

respect to its corporate governance aspects. The organisation was established in the year

1999. Tarmac group is the predecessor of the company. Headquarter of the company is

established in United Kingdom. Company is engaged in conducting operations in

construction civil engineering and facilities management functions. Henceforth, report will

emphasis on the company’s duty to comply with the corporate governance code based on the

United Kingdom. In this report code related to the financial governance applicable on

company will be specifically discuss. Different financial tools and ratios like gearing ratio,

remuneration, and profit after tax and gearing ratio will be discussed in this report. Different

aspects related to the corporate governance and financial governance of company will be

discussed in this project.

MAIN BODY

Company’s duty to comply with UK corporate governance

Corporate governance is the system that controls the company’s functions. Boards of

director in every company are solely responsible for implementing corporate governance

codes over the organisation. Shareholders also play a crucial role in the corporate governance

in order to appoint directors of company and also the auditors for controlling the financial

authenticity of the company and also in respect to satisfy themselves that the corporate

governance structure has been in the right place in the organization structure of company

(Dzomira, 2017). The code and conducts of corporate governance ensure that it is the

responsibility of the board of directors of company to setting up strategic aim of the

company, provide leadership to company, supervising the entire business activity and to

report the shareholders of company about the company’s financial position time to time. In

Carillion Plc Company shareholders of company are very much active ad aware in respect to

the professional code and conducts of the corporate governance. It becomes essential that

shareholders of company must be aware in respect to the corporate governance code and

conducts than only they can ensure the proper control over the company’s operations

otherwise management and leadership of company may influence the knowledge of the

shareholders in respect to the business operations of company.

respect to its corporate governance aspects. The organisation was established in the year

1999. Tarmac group is the predecessor of the company. Headquarter of the company is

established in United Kingdom. Company is engaged in conducting operations in

construction civil engineering and facilities management functions. Henceforth, report will

emphasis on the company’s duty to comply with the corporate governance code based on the

United Kingdom. In this report code related to the financial governance applicable on

company will be specifically discuss. Different financial tools and ratios like gearing ratio,

remuneration, and profit after tax and gearing ratio will be discussed in this report. Different

aspects related to the corporate governance and financial governance of company will be

discussed in this project.

MAIN BODY

Company’s duty to comply with UK corporate governance

Corporate governance is the system that controls the company’s functions. Boards of

director in every company are solely responsible for implementing corporate governance

codes over the organisation. Shareholders also play a crucial role in the corporate governance

in order to appoint directors of company and also the auditors for controlling the financial

authenticity of the company and also in respect to satisfy themselves that the corporate

governance structure has been in the right place in the organization structure of company

(Dzomira, 2017). The code and conducts of corporate governance ensure that it is the

responsibility of the board of directors of company to setting up strategic aim of the

company, provide leadership to company, supervising the entire business activity and to

report the shareholders of company about the company’s financial position time to time. In

Carillion Plc Company shareholders of company are very much active ad aware in respect to

the professional code and conducts of the corporate governance. It becomes essential that

shareholders of company must be aware in respect to the corporate governance code and

conducts than only they can ensure the proper control over the company’s operations

otherwise management and leadership of company may influence the knowledge of the

shareholders in respect to the business operations of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In context to the financial governance different codes are applicable over the

organisation as a part of corporate governance practices. Following are the codes that will be

applicable over the Carillion Plc Company in respect to the financial governance.

Act within power

Section 171 has allowed acting within the power as a par of the corporate governance

practice. This section provides powers to the management and directors to implement all such

practices related to company’s operations to achieve the growth and success for the

company’s business (Christensen and Hearson, 2019). This code also specify that each

director and leaders and employee must be work within the power he is associated with as a

part of the designated position role in Carillion Plc Company so that proper hierarchy of

company can be maintained. The organisation has overlapped this section many times when it

goes into liquidation and in many other cases.

Common law

Corporate governance also implements common law over the organisation. This

involve to exercise skill and care, act in the best interest of company, act within the power in

company, not to fetter direction, not to make secret profits and other related implications as a

part of the corporate governance function in company. All common laws allow company to

work in the best of the capacity to achieve the higher level of financial stability and

profitability against the operations company undertakes (Paech, 2017). Not to make secret

profit is the major implications associated with the common that associated with the financial

governance in the company. This code involves that all directors and the individuals involved

in formation of company must not make any secret profits in against to the services they are

granting to company. It is illegal to make any kind of secret profit against the services deliver

to the company in any professional capacity at the organisation. Many professionals like

chartered accountant, legal advisors, company secretary and other associated designated

officers in Carillion Plc Company serves professional services in company. It is illegal that

they make any kind of secret profits against the services they deliver to the organisation.

Company has may times been involved in practices like showing fake profits to take extra

advantages. These all actions of company is unfavourable as per the companies act.

The listing rule

organisation as a part of corporate governance practices. Following are the codes that will be

applicable over the Carillion Plc Company in respect to the financial governance.

Act within power

Section 171 has allowed acting within the power as a par of the corporate governance

practice. This section provides powers to the management and directors to implement all such

practices related to company’s operations to achieve the growth and success for the

company’s business (Christensen and Hearson, 2019). This code also specify that each

director and leaders and employee must be work within the power he is associated with as a

part of the designated position role in Carillion Plc Company so that proper hierarchy of

company can be maintained. The organisation has overlapped this section many times when it

goes into liquidation and in many other cases.

Common law

Corporate governance also implements common law over the organisation. This

involve to exercise skill and care, act in the best interest of company, act within the power in

company, not to fetter direction, not to make secret profits and other related implications as a

part of the corporate governance function in company. All common laws allow company to

work in the best of the capacity to achieve the higher level of financial stability and

profitability against the operations company undertakes (Paech, 2017). Not to make secret

profit is the major implications associated with the common that associated with the financial

governance in the company. This code involves that all directors and the individuals involved

in formation of company must not make any secret profits in against to the services they are

granting to company. It is illegal to make any kind of secret profit against the services deliver

to the company in any professional capacity at the organisation. Many professionals like

chartered accountant, legal advisors, company secretary and other associated designated

officers in Carillion Plc Company serves professional services in company. It is illegal that

they make any kind of secret profits against the services they deliver to the organisation.

Company has may times been involved in practices like showing fake profits to take extra

advantages. These all actions of company is unfavourable as per the companies act.

The listing rule

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial governance code also opposes the listing rule over the company. This code

involve that the securities of the Carillion Plc Company must be listed or the securities of

company must be listed in the United Kingdom Listing Authority’s (UKLA) in order to raise

funds for different business operations. This code of financial governance conveys all the

rules associated with the securities to be listed in the UKLA (Shi, Connelly and Hoskisson,

2017). Company needed funds to channelize various functions in company. Only once the

securities of company are listed than only company can issue shares and securities in the

crowd funding to generate funds for its financial needs. Financial governance involve

mandatory requirement of company to list its securities in order to raise funds for its financial

needs and requirements of company. Other rules like The Prospectus Rules and The

Disclosure Guidelines Rule must also be fulfilled by the company along with the general rule

of listing security at the UKLA.

Company’s audit

As per the financial governance it is compulsory that Carillion Plc Company must

conduct the audit every year. It is mandatory that company must give the authority of audit of

company to any external firm. Financial governance allows the tenure of 10 years to any

external authority to audit the financial statements and books of accounts of company. FTSE

350 Company must mandatorily put its accounts on audit over the external authorised

authority for audit of the books of accounts. It is the further responsibility of the audit

committee to give report to the shareholders of Carillion Plc Company about the financial

position of company also in respect to the fair state of affairs of company. This is also the

responsibility of the board of directors of Carillion Plc Company that books and accounts

taken as a whole for audit are fair, complete, understandable and provide the fair information

in respect to company’s financial position in a given financial year (Zachariadis, Hileman and

Scott, 2019). It is involve in the financial governance that audit is the proof that all

accounting standard and principles have been fairly followed in exactly the way they are

while completing the financial statements and books of accounts of company. Positive audit

report is the proof that all principles of accounting have been followed in such a way that

company could cope up with all principles of accounts. Profitability shown in the books of

accounts is also exact and company did not breach any trust of shareholders in form of illegal

or fake transactions included in the books of accounts of company.

Remunerations

involve that the securities of the Carillion Plc Company must be listed or the securities of

company must be listed in the United Kingdom Listing Authority’s (UKLA) in order to raise

funds for different business operations. This code of financial governance conveys all the

rules associated with the securities to be listed in the UKLA (Shi, Connelly and Hoskisson,

2017). Company needed funds to channelize various functions in company. Only once the

securities of company are listed than only company can issue shares and securities in the

crowd funding to generate funds for its financial needs. Financial governance involve

mandatory requirement of company to list its securities in order to raise funds for its financial

needs and requirements of company. Other rules like The Prospectus Rules and The

Disclosure Guidelines Rule must also be fulfilled by the company along with the general rule

of listing security at the UKLA.

Company’s audit

As per the financial governance it is compulsory that Carillion Plc Company must

conduct the audit every year. It is mandatory that company must give the authority of audit of

company to any external firm. Financial governance allows the tenure of 10 years to any

external authority to audit the financial statements and books of accounts of company. FTSE

350 Company must mandatorily put its accounts on audit over the external authorised

authority for audit of the books of accounts. It is the further responsibility of the audit

committee to give report to the shareholders of Carillion Plc Company about the financial

position of company also in respect to the fair state of affairs of company. This is also the

responsibility of the board of directors of Carillion Plc Company that books and accounts

taken as a whole for audit are fair, complete, understandable and provide the fair information

in respect to company’s financial position in a given financial year (Zachariadis, Hileman and

Scott, 2019). It is involve in the financial governance that audit is the proof that all

accounting standard and principles have been fairly followed in exactly the way they are

while completing the financial statements and books of accounts of company. Positive audit

report is the proof that all principles of accounting have been followed in such a way that

company could cope up with all principles of accounts. Profitability shown in the books of

accounts is also exact and company did not breach any trust of shareholders in form of illegal

or fake transactions included in the books of accounts of company.

Remunerations

The financial governance involve in the corporate governance also focuses over the

remunerations to board of directors of company. All members of the board of directors of the

Carillion Plc Company must get the proper remunerations in against to the services they

allocate to the company. As per the code of financial governance remunerations given to the

each board of director must be calculated as per the guidelines given by the corporate

governance. The code also specify that in case of non executive directors performance related

elements must not include while calculating the remunerations for such directors against the

services they have granted to the organisation (Omri, 2020). Remunerations of director of

company is calculated on the basis of the profitability of the Carillion Plc Company each

year. Percentage of the profitability of distributed in between all directors of company.

Performance of directors also includes in order calculating the potential remunerations

granted to each director of company. The financial governance also project that remuneration

report must be issued by company along with the financial reports of company that clearly

point out how much remuneration each directors is getting against the services at the

Carillion Plc Company. It is also clearly mentioned in the code that remuneration report must

also be available over the company’s website for the next 10 years so that any time

shareholders of company can visit the amount of remunerations shareholders of company

getting every year. To pay extra remunerations many times company’s profit has been

touched in wrong manner by showing vogue profits in books of accounts of company. These

practices are against the code of conducts.

Executive pay

In order to set reform against the executive pat financial governance has also included

the executive pay as a code. This involve that companies must report the pay ratio of

company’s CEO in the section executive pay. This is an important amendment that involve

that the pay CEO is receiving against the services allotted to the Carillion Plc Company must

get the proper payment and also the pay CEO of Carillion Plc Company is receiving must be

quoted n the name of executive pay (Danoshana and Ravivathani, 2019). This must be

revealed the clear detail about the payment CEO of company is getting. Shareholder of

company must be aware in respect to the executive pay associated with the CEO of company.

This is an important financial aspect of company. This allows the shareholders associated

with the company to analyse the financial position of company in respect to the payment

CEO is getting against the services. As the CEO of company carry a huge influence over the

business operations of company. It is proposed that a public register must be maintained in

remunerations to board of directors of company. All members of the board of directors of the

Carillion Plc Company must get the proper remunerations in against to the services they

allocate to the company. As per the code of financial governance remunerations given to the

each board of director must be calculated as per the guidelines given by the corporate

governance. The code also specify that in case of non executive directors performance related

elements must not include while calculating the remunerations for such directors against the

services they have granted to the organisation (Omri, 2020). Remunerations of director of

company is calculated on the basis of the profitability of the Carillion Plc Company each

year. Percentage of the profitability of distributed in between all directors of company.

Performance of directors also includes in order calculating the potential remunerations

granted to each director of company. The financial governance also project that remuneration

report must be issued by company along with the financial reports of company that clearly

point out how much remuneration each directors is getting against the services at the

Carillion Plc Company. It is also clearly mentioned in the code that remuneration report must

also be available over the company’s website for the next 10 years so that any time

shareholders of company can visit the amount of remunerations shareholders of company

getting every year. To pay extra remunerations many times company’s profit has been

touched in wrong manner by showing vogue profits in books of accounts of company. These

practices are against the code of conducts.

Executive pay

In order to set reform against the executive pat financial governance has also included

the executive pay as a code. This involve that companies must report the pay ratio of

company’s CEO in the section executive pay. This is an important amendment that involve

that the pay CEO is receiving against the services allotted to the Carillion Plc Company must

get the proper payment and also the pay CEO of Carillion Plc Company is receiving must be

quoted n the name of executive pay (Danoshana and Ravivathani, 2019). This must be

revealed the clear detail about the payment CEO of company is getting. Shareholder of

company must be aware in respect to the executive pay associated with the CEO of company.

This is an important financial aspect of company. This allows the shareholders associated

with the company to analyse the financial position of company in respect to the payment

CEO is getting against the services. As the CEO of company carry a huge influence over the

business operations of company. It is proposed that a public register must be maintained in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

listed company encountering shareholder opposition to pay award of 20 percent or more in

against the services allotted to company (Duque-Grisales and Aguilera-Caracuel, 2019).

All the above points project about the crucial financial governance points in respect to

the Carillion Plc Company. All these codes play a crucial role in order to maintain the proper

financial governance in the organisation.

Financial governance issues

A) Remuneration of Board of Directors

Remuneration of Board of directors is an important part in the business as they are the

key leaders that drive the business towards success. There is a principal agent relationship

between the shareholders and managers of the company. Managers of the company have the

duty of promoting business towards growth and success for which they are paid adequate

remuneration. The remuneration paid to the managers and key personnel should be enough

and reasonable for encouraging them to perform better and better and also for retaining them

in the company. But the remuneration of managers should not be in conflicts with the benefits

of the company. Managers should not work for their individual benefits sacrificing the

growth and success of the business.

The annual report of the company shows that the remuneration of the CEO is rising

with the profitability of the company. Directors must earn on their strengths to grow the

company and increase the profitability and not only over the profits of company.

The managerial remuneration paid by the company over the years is rising with the

increase in profitability of the business. Profitability of the company shows fluctuating trend

in the business which shows that the business is growing at constant rate. It sees ups and

downs in the business every year (Aguilera, Judge and Terjesen, 2018). Managers of the

company are putting significant efforts for the growth of business.

It could be evaluated from the financial reports of the business that the remuneration

to the managers is paid on the basis of profits. It complies with the requirement of large and

small size companies. The remuneration earned by the managers is adequately reflected in the

financial statements of the company. The remuneration policy of the company is approved by

the shareholders in general meeting and is implemented effectively from end of the meeting.

It could be evaluated that the years in which company growth is not seen or the

profitability goes below the previous year’s remuneration remain unchanged for that year. All

the remuneration and earnings of the managers are properly audited by the recognised

against the services allotted to company (Duque-Grisales and Aguilera-Caracuel, 2019).

All the above points project about the crucial financial governance points in respect to

the Carillion Plc Company. All these codes play a crucial role in order to maintain the proper

financial governance in the organisation.

Financial governance issues

A) Remuneration of Board of Directors

Remuneration of Board of directors is an important part in the business as they are the

key leaders that drive the business towards success. There is a principal agent relationship

between the shareholders and managers of the company. Managers of the company have the

duty of promoting business towards growth and success for which they are paid adequate

remuneration. The remuneration paid to the managers and key personnel should be enough

and reasonable for encouraging them to perform better and better and also for retaining them

in the company. But the remuneration of managers should not be in conflicts with the benefits

of the company. Managers should not work for their individual benefits sacrificing the

growth and success of the business.

The annual report of the company shows that the remuneration of the CEO is rising

with the profitability of the company. Directors must earn on their strengths to grow the

company and increase the profitability and not only over the profits of company.

The managerial remuneration paid by the company over the years is rising with the

increase in profitability of the business. Profitability of the company shows fluctuating trend

in the business which shows that the business is growing at constant rate. It sees ups and

downs in the business every year (Aguilera, Judge and Terjesen, 2018). Managers of the

company are putting significant efforts for the growth of business.

It could be evaluated from the financial reports of the business that the remuneration

to the managers is paid on the basis of profits. It complies with the requirement of large and

small size companies. The remuneration earned by the managers is adequately reflected in the

financial statements of the company. The remuneration policy of the company is approved by

the shareholders in general meeting and is implemented effectively from end of the meeting.

It could be evaluated that the years in which company growth is not seen or the

profitability goes below the previous year’s remuneration remain unchanged for that year. All

the remuneration and earnings of the managers are properly audited by the recognised

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting and auditing firms and assuring that all the remuneration to the directors and

managers are paid in accordance with requirements of regulations.

Remuneration policies of the company are also approved by the shareholders and are

in compliance with corporate governance requirements. The performance of the company is

adequate and has maintained adequate profitability ratios with the expansion and growth of

the business.

B) Gearing Ratio

The Gearing ratio refers to the capital structure of the company. it is the proportion of

debt against equity capital of company. It could be referred that company having debt capital

have higher financial risks that makes company unattractive and investors do not invest in

such companies even if they have high profits. Gearing ratio is an important ratio which

could be used for the financial leverage of the company. Management strive for having

capital structure for their firm so that their cost of capital is least. Though equity capital is the

most preferred source of capital but the cost of equity is also high and cost of debt is lower as

compared with equity. Company avails tax benefits which reduces the cost further but have

significant financial implications in business.

The gearing ratio of the company had remained between the range of 3 to 4 which

shows that the debt in the company is not increasing every year. It is making due repayments

of the principal and capitals every year that has enabled the company to manage the capital

structure. This had also kept the financial risk under control. Significant rise was in the year

2016 that increased the financial leverage to 6.32 which was highest in the period of 5 years.

The standard for good governance states that the governance is dependent over the

motive of the company which is to make profits or to increase the wealth of shareholders. In

the present it is analysed that focus of the company is towards wealth maximisation of the

shareholders as it is maintain effective control over maintain the capital structure.

It raised several questions about the sustainability of the company as increase in debt

causes financial risks. If company is increasing debts and the profits are not growing with the

same scale the company will move towards losses (Yermack, 2017). The business will be

turned out to be loss making if the financial leverage is increasing continuously.

Funds are raised if the company is not able to meet the funds requirement from the

cash flows generated. The liquidity position of company may be very weak which is, cause of

concern for the investors is. The credibility of the business is required to be ensured in such

cases as per the code of corporate governance. The credibility of the company will affect will

managers are paid in accordance with requirements of regulations.

Remuneration policies of the company are also approved by the shareholders and are

in compliance with corporate governance requirements. The performance of the company is

adequate and has maintained adequate profitability ratios with the expansion and growth of

the business.

B) Gearing Ratio

The Gearing ratio refers to the capital structure of the company. it is the proportion of

debt against equity capital of company. It could be referred that company having debt capital

have higher financial risks that makes company unattractive and investors do not invest in

such companies even if they have high profits. Gearing ratio is an important ratio which

could be used for the financial leverage of the company. Management strive for having

capital structure for their firm so that their cost of capital is least. Though equity capital is the

most preferred source of capital but the cost of equity is also high and cost of debt is lower as

compared with equity. Company avails tax benefits which reduces the cost further but have

significant financial implications in business.

The gearing ratio of the company had remained between the range of 3 to 4 which

shows that the debt in the company is not increasing every year. It is making due repayments

of the principal and capitals every year that has enabled the company to manage the capital

structure. This had also kept the financial risk under control. Significant rise was in the year

2016 that increased the financial leverage to 6.32 which was highest in the period of 5 years.

The standard for good governance states that the governance is dependent over the

motive of the company which is to make profits or to increase the wealth of shareholders. In

the present it is analysed that focus of the company is towards wealth maximisation of the

shareholders as it is maintain effective control over maintain the capital structure.

It raised several questions about the sustainability of the company as increase in debt

causes financial risks. If company is increasing debts and the profits are not growing with the

same scale the company will move towards losses (Yermack, 2017). The business will be

turned out to be loss making if the financial leverage is increasing continuously.

Funds are raised if the company is not able to meet the funds requirement from the

cash flows generated. The liquidity position of company may be very weak which is, cause of

concern for the investors is. The credibility of the business is required to be ensured in such

cases as per the code of corporate governance. The credibility of the company will affect will

affect all the stakeholders and therefore it is essential that the financial position and all the

material facts and events are disclosed by company in its financial statement.

Corporate governance protects the investors and the debt holders of the company by

requiring the company to disclose its actual performance and position every year without

misleading statements.

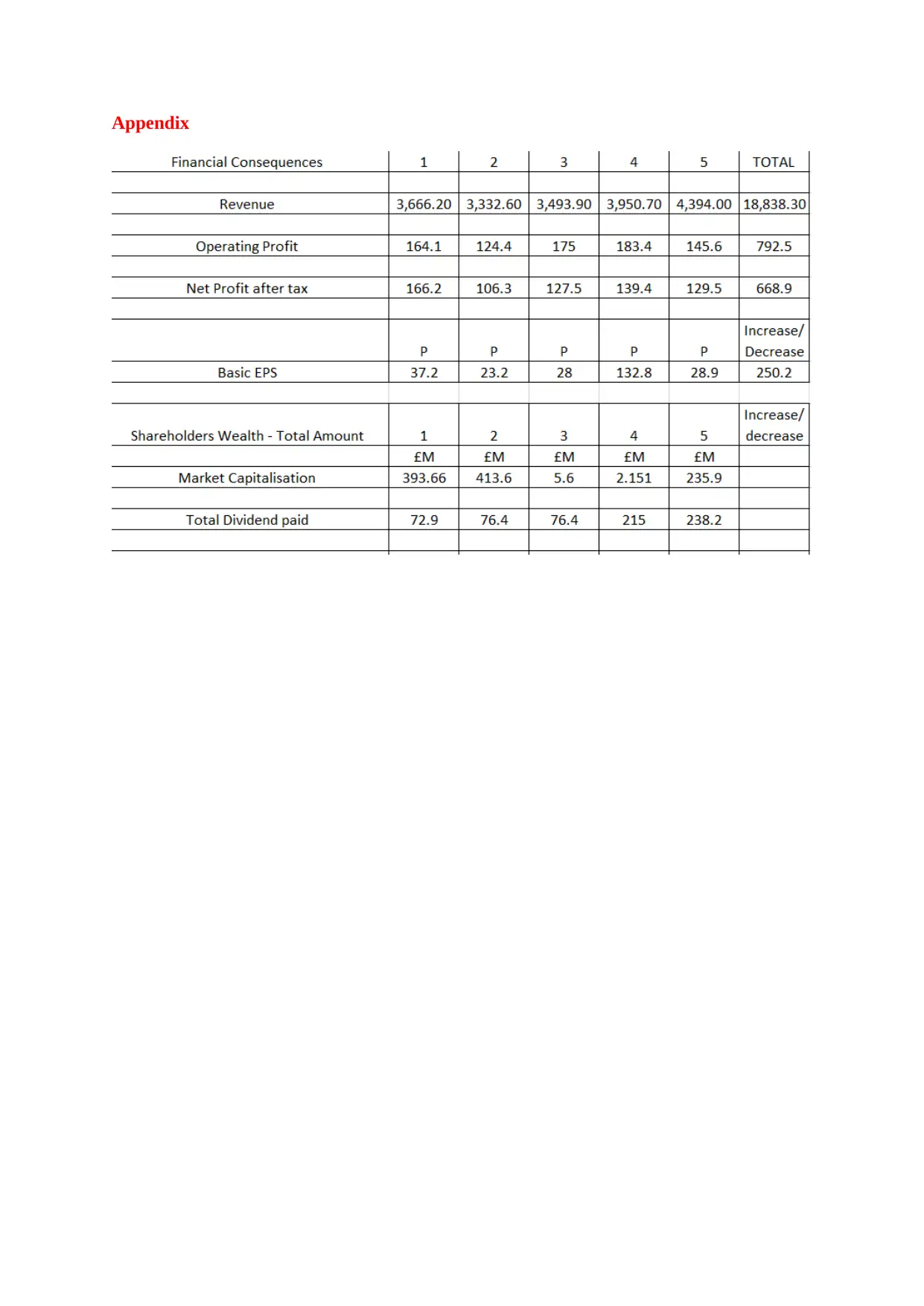

Profit after tax

Profit after tax is the net income of the company. This is the income that company has

actually generated out of the revenue. Taxation liability of company gets deducted from the

profit before tax to calculate the profit after tax. Previous few years of the Carillion Plc

Company have been productive as company could generate consistent effective returns as per

the profit after tax figures of company. The latest financial statement of company represent

that company has generated the 166.2 million pound profits after tax that is calculated from

the total revenue of company in that year is 3666.2 million pound which was further deducted

from the expenses of total was 3500 million pound which is more than the 106.3 million

pound of the year before profit after tax that is also calculated by deducting the expenses

from total revenue worth 332.6 million pound and the total expanses was 3226.3 million

pound (Kaiser and Kirton, 2019). The profit after tax of other year was 127.5 that is

calculated by reducing the total expenses of 3366.4 from the total revenue of the year was

3493.9 million pound. The usual trend of the company’s income has gone to increasing order

except the last financial year in which company has generated the decreasing trend in net

income of company. Financial governance of company have projected the exact financial

position of company which clearly shown that the company has generated the effective

revenues out of the business operations. Financial governance drives company towards

projecting the true face of company in respect to the financial position of company. The

financial position is exact and calculated as per all cods given in financial governance tool

applicable over Carillion Plc Company.

Dividend payout ratio

Dividend payout ratio project the total dividend paid to shareholders of company out

of the net income of company. This is the comparison between the dividends paid by the

company as compare to the net income earned by the company in a given financial year. The

dividend payout ratio of company has been consistently at the rate of .44 in previous few

years that is calculated by comparing net profit which is 166.2 million pound and total

material facts and events are disclosed by company in its financial statement.

Corporate governance protects the investors and the debt holders of the company by

requiring the company to disclose its actual performance and position every year without

misleading statements.

Profit after tax

Profit after tax is the net income of the company. This is the income that company has

actually generated out of the revenue. Taxation liability of company gets deducted from the

profit before tax to calculate the profit after tax. Previous few years of the Carillion Plc

Company have been productive as company could generate consistent effective returns as per

the profit after tax figures of company. The latest financial statement of company represent

that company has generated the 166.2 million pound profits after tax that is calculated from

the total revenue of company in that year is 3666.2 million pound which was further deducted

from the expenses of total was 3500 million pound which is more than the 106.3 million

pound of the year before profit after tax that is also calculated by deducting the expenses

from total revenue worth 332.6 million pound and the total expanses was 3226.3 million

pound (Kaiser and Kirton, 2019). The profit after tax of other year was 127.5 that is

calculated by reducing the total expenses of 3366.4 from the total revenue of the year was

3493.9 million pound. The usual trend of the company’s income has gone to increasing order

except the last financial year in which company has generated the decreasing trend in net

income of company. Financial governance of company have projected the exact financial

position of company which clearly shown that the company has generated the effective

revenues out of the business operations. Financial governance drives company towards

projecting the true face of company in respect to the financial position of company. The

financial position is exact and calculated as per all cods given in financial governance tool

applicable over Carillion Plc Company.

Dividend payout ratio

Dividend payout ratio project the total dividend paid to shareholders of company out

of the net income of company. This is the comparison between the dividends paid by the

company as compare to the net income earned by the company in a given financial year. The

dividend payout ratio of company has been consistently at the rate of .44 in previous few

years that is calculated by comparing net profit which is 166.2 million pound and total

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

dividend paid was 72.9 million pound. Dividend payout ratio of other year was like .72 that is

calculated from net profit 106.3 and dividend paid 76.4 million pound (Bayar, Huseynov and

Sardarli, 2018). The other year dividend payout was .6 that was calculated by comparing net

profit of 127.5 million pound with dividend of 76.4 million pound. This rate also satisfies all

the stakeholders and shareholders associated with the internal affairs of company.

Shareholders of company clearly analyse about the dividend payout ratio of company while

analysing about the financial stability of company in a given financial year. Dividend is the

return of the people invested in the affairs of company so that funding requirements of the

company can be cope up with in order to conduct business transactions.

CONCLUSION

This report has analysed about the financial governance applicable over the company.

Corporate governance codes talks about all the ethical and financial requirements board of

director of company must comply with in order to conduct the business operations. Financial

governance more like a part of the corporate governance. This involves different financial

aspects like projecting the true position of company in all its books of accounts. Company

must not mislead its shareholders by projecting the wrong financial position of company from

income statement of company. Financial governance also drive company towards paying the

specific percentage of remunerations to company’s directors in against to the services the

director of company deliver to the organisation. This also involves that mandatory audit of

company’s affairs each financial year. It is important that company must audit its books of

accounts every year from the external sources. The maximum tenure of the audit from same

firm would be maximum to 10 years. Different aspects like remuneration paid to director of

company, gearing ratio, profit after tax and dividend payout ratio are a part of the financial

governance involve in corporate governance codes.

calculated from net profit 106.3 and dividend paid 76.4 million pound (Bayar, Huseynov and

Sardarli, 2018). The other year dividend payout was .6 that was calculated by comparing net

profit of 127.5 million pound with dividend of 76.4 million pound. This rate also satisfies all

the stakeholders and shareholders associated with the internal affairs of company.

Shareholders of company clearly analyse about the dividend payout ratio of company while

analysing about the financial stability of company in a given financial year. Dividend is the

return of the people invested in the affairs of company so that funding requirements of the

company can be cope up with in order to conduct business transactions.

CONCLUSION

This report has analysed about the financial governance applicable over the company.

Corporate governance codes talks about all the ethical and financial requirements board of

director of company must comply with in order to conduct the business operations. Financial

governance more like a part of the corporate governance. This involves different financial

aspects like projecting the true position of company in all its books of accounts. Company

must not mislead its shareholders by projecting the wrong financial position of company from

income statement of company. Financial governance also drive company towards paying the

specific percentage of remunerations to company’s directors in against to the services the

director of company deliver to the organisation. This also involves that mandatory audit of

company’s affairs each financial year. It is important that company must audit its books of

accounts every year from the external sources. The maximum tenure of the audit from same

firm would be maximum to 10 years. Different aspects like remuneration paid to director of

company, gearing ratio, profit after tax and dividend payout ratio are a part of the financial

governance involve in corporate governance codes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Aguilera, R.V., Judge, W.Q. and Terjesen, S.A., 2018. Corporate governance

deviance. Academy of Management Review. 43(1). pp.87-109.

Bayar, O., Huseynov, F. and Sardarli, S., 2018. Corporate governance, Tax avoidance, and

financial constraints. Financial Management. 47(3). pp.651-677.

Christensen, R. C. and Hearson, M., 2019. The new politics of global tax governance: taking

stock a decade after the financial crisis. Review of International Political

Economy. 26(5). pp.1068-1088.

Danoshana, S. and Ravivathani, T., 2019. The impact of the corporate governance on firm

performance: A study on financial institutions in Sri Lanka. SAARJ Journal on

Banking & Insurance Research. 8(1). pp.62-67.

Duque-Grisales, E. and Aguilera-Caracuel, J., 2019. Environmental, social and governance

(ESG) scores and financial performance of multilatinas: Moderating effects of

geographic international diversification and financial slack. Journal of Business Ethics,

pp.1-20.

Dzomira, S., 2017. FINANCIAL ACCOUNTABILITY & GOVERNANCE IN AN

EMERGING COUNTRY. Corporate Ownership & Control, p.204.

Kaiser, K. and Kirton, J. J., 2019. Shaping a new international financial system: Challenges

of governance in a globalizing world. Routledge.

Omri, A., 2020. Formal versus informal entrepreneurship in emerging economies: The roles

of governance and the financial sector. Journal of Business Research. 108. pp.277-290.

Paech, P., 2017. The governance of blockchain financial networks. The Modern Law

Review. 80(6). pp.1073-1110.

Shi, W., Connelly, B. L. and Hoskisson, R. E., 2017. External corporate governance and

financial fraud: Cognitive evaluation theory insights on agency theory

prescriptions. Strategic Management Journal. 38(6). pp.1268-1286.

Yermack, D., 2017. Corporate governance and blockchains. Review of Finance. 21(1). pp.7-

31.

Zachariadis, M., Hileman, G. and Scott, S. V., 2019. Governance and control in distributed

ledgers: Understanding the challenges facing blockchain technology in financial

services. Information and Organization. 29(2). pp.105-117.

Books and Journals

Aguilera, R.V., Judge, W.Q. and Terjesen, S.A., 2018. Corporate governance

deviance. Academy of Management Review. 43(1). pp.87-109.

Bayar, O., Huseynov, F. and Sardarli, S., 2018. Corporate governance, Tax avoidance, and

financial constraints. Financial Management. 47(3). pp.651-677.

Christensen, R. C. and Hearson, M., 2019. The new politics of global tax governance: taking

stock a decade after the financial crisis. Review of International Political

Economy. 26(5). pp.1068-1088.

Danoshana, S. and Ravivathani, T., 2019. The impact of the corporate governance on firm

performance: A study on financial institutions in Sri Lanka. SAARJ Journal on

Banking & Insurance Research. 8(1). pp.62-67.

Duque-Grisales, E. and Aguilera-Caracuel, J., 2019. Environmental, social and governance

(ESG) scores and financial performance of multilatinas: Moderating effects of

geographic international diversification and financial slack. Journal of Business Ethics,

pp.1-20.

Dzomira, S., 2017. FINANCIAL ACCOUNTABILITY & GOVERNANCE IN AN

EMERGING COUNTRY. Corporate Ownership & Control, p.204.

Kaiser, K. and Kirton, J. J., 2019. Shaping a new international financial system: Challenges

of governance in a globalizing world. Routledge.

Omri, A., 2020. Formal versus informal entrepreneurship in emerging economies: The roles

of governance and the financial sector. Journal of Business Research. 108. pp.277-290.

Paech, P., 2017. The governance of blockchain financial networks. The Modern Law

Review. 80(6). pp.1073-1110.

Shi, W., Connelly, B. L. and Hoskisson, R. E., 2017. External corporate governance and

financial fraud: Cognitive evaluation theory insights on agency theory

prescriptions. Strategic Management Journal. 38(6). pp.1268-1286.

Yermack, D., 2017. Corporate governance and blockchains. Review of Finance. 21(1). pp.7-

31.

Zachariadis, M., Hileman, G. and Scott, S. V., 2019. Governance and control in distributed

ledgers: Understanding the challenges facing blockchain technology in financial

services. Information and Organization. 29(2). pp.105-117.

Appendix

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.