Financial Accounting for Managerial Decision Making: GSK PLC Analysis

VerifiedAdded on 2023/01/13

|9

|1836

|62

Report

AI Summary

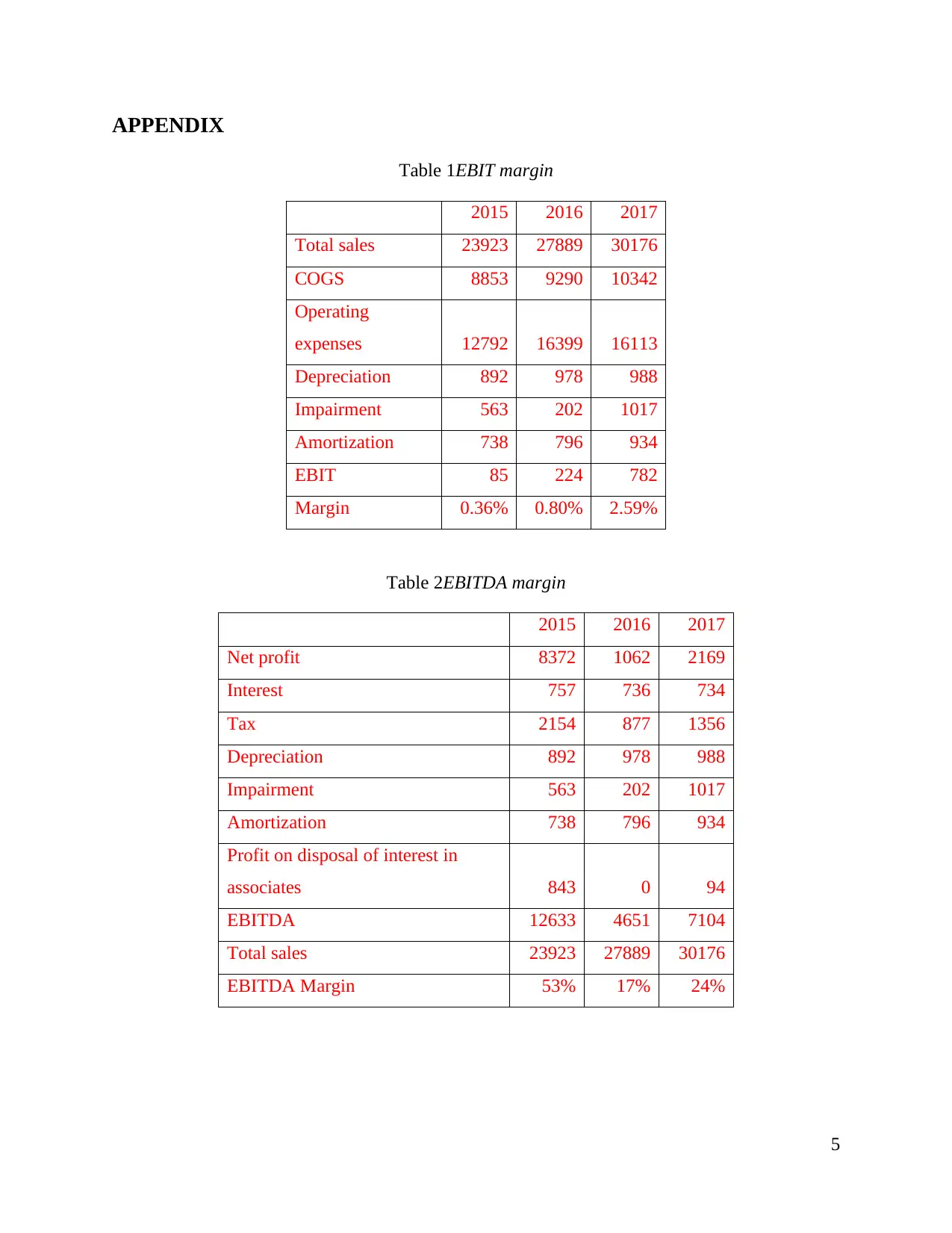

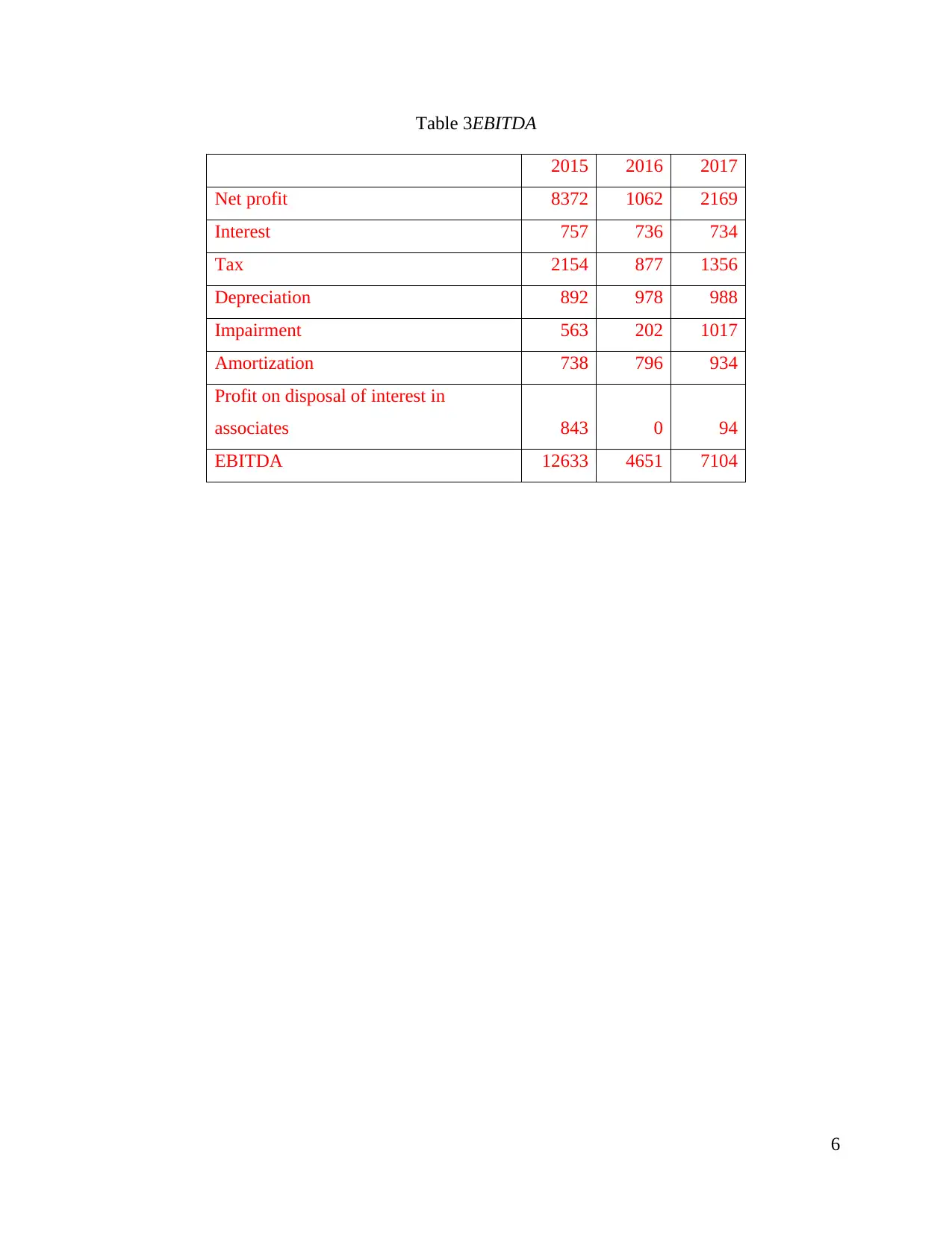

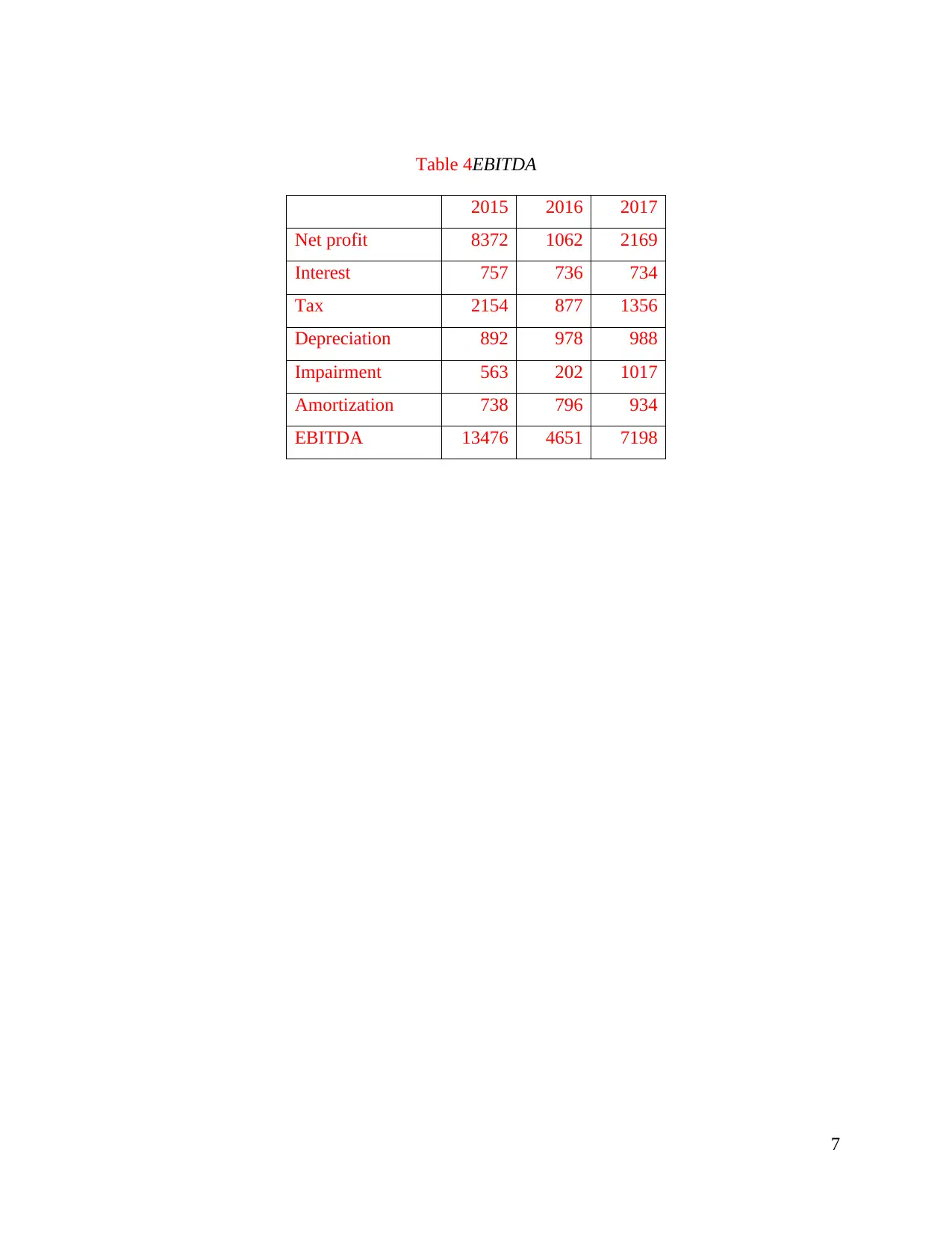

This report provides an analysis of EBIT (Earnings Before Interest and Tax) and EBITDA (Earnings Before Interest, Tax, Depreciation, and Amortization) for Glaxo Smithkline PLC (GSK PLC). The introduction highlights the importance of investment valuation and the use of EBIT and EBITDA. The report computes and interprets these ratios for GSK, discussing their significance in financial analysis. It evaluates expert statements on revenue recognition and depreciation, concluding that both EBIT and EBITDA are crucial metrics for investors, reflecting a firm's earnings and expense control. The appendix includes tables showing EBIT and EBITDA margins, and relevant financial data for 2015-2017. The report also explores the usefulness of EBITDA, emphasizing its importance in assessing a company's performance and its impact on profitability. The evaluation of statements highlights how new revenue recognition standards assist stakeholders and how accurate depreciation practices produce accurate asset valuation. The analysis concludes with a summary of the findings and their implications for investors.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.